Life Science Tools Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

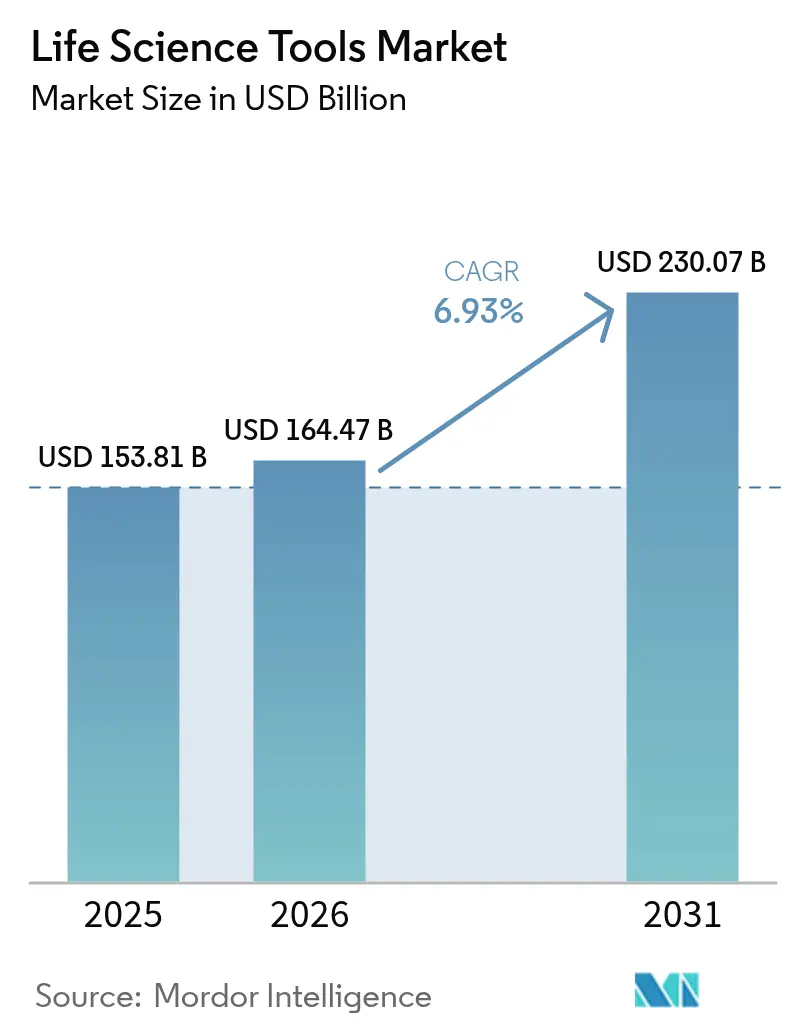

| Market Size (2026) | USD 164.47 Billion |

| Market Size (2031) | USD 230.07 Billion |

| Growth Rate (2026 - 2031) | 6.93% CAGR |

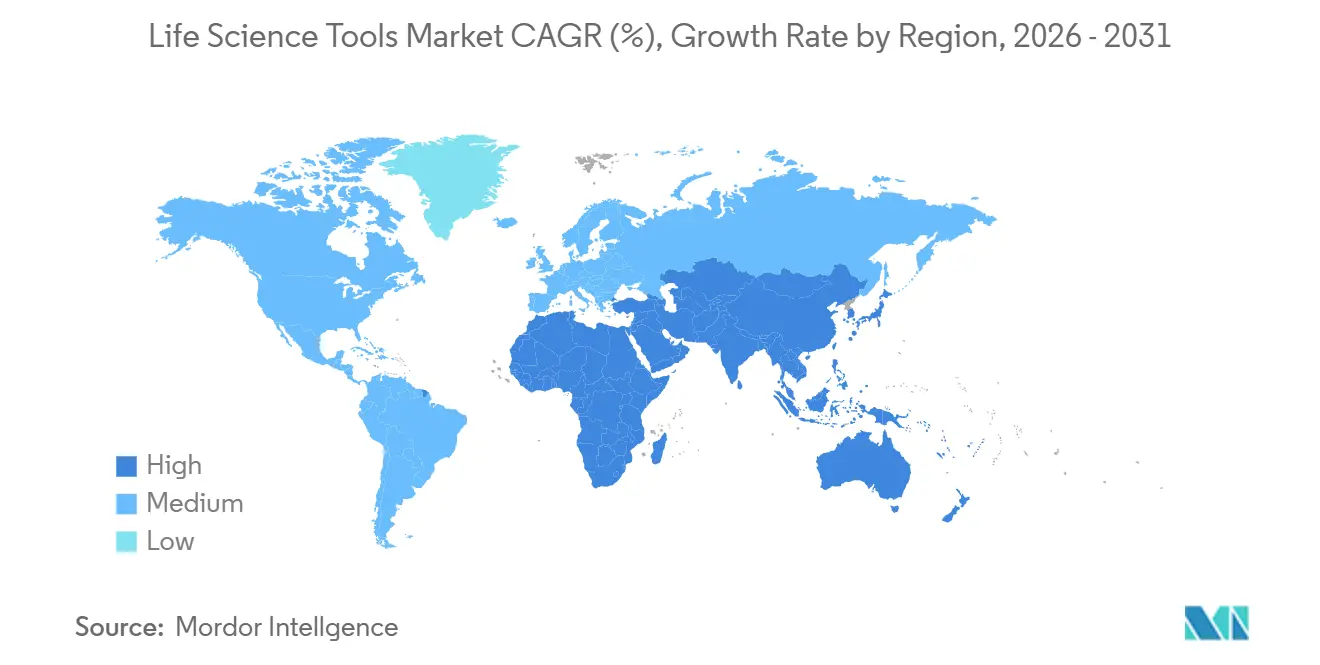

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Life Science Tools Market Analysis by Mordor Intelligence

The Life Science Tools Market size is expected to grow from USD 153.81 billion in 2025 to USD 164.47 billion in 2026 and is forecast to reach USD 230.07 billion by 2031 at 6.93% CAGR over 2026-2031.

Government grants, regulatory tailwinds for lab-developed tests, and multi-omics adoption are steering capital toward automation, sequencing, and high-resolution analytical platforms. Services are expanding faster than instruments as laboratories pivot to outsourced, pay-per-use models that lower upfront costs and accelerate compliance-driven validation cycles. Falling per-genome prices have widened clinical access to next-generation sequencing, while sustained NIH and Horizon Europe budgets continue to underwrite large-scale equipment refreshes. Meanwhile, geopolitical export controls are prompting dual-sourcing strategies that favor vendors with regional manufacturing footprints.

Rising public-sector outlays, such as the United States Congress’ proposed USD 88 billion biotechnology package for 2025, coupled with stricter FDA oversight of lab-developed tests (LDTs), are reshaping compliance needs and driving fresh demand for validated instruments. Competitive momentum remains strong; established suppliers deploy mergers, acquisitions, and portfolio extensions to defend share and open new channels, yet lingering supply-chain fragilities and shortages of trained bioinformaticians temper the near-term outlook.

Key Report Takeaways

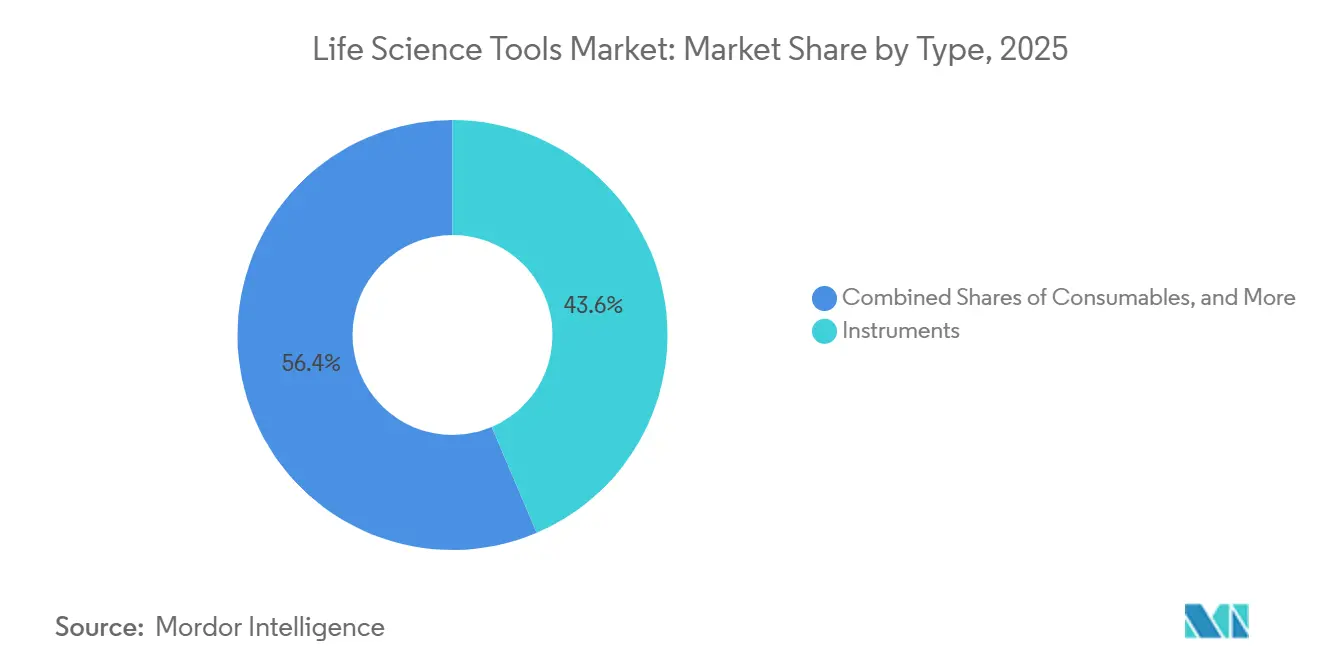

- By type, services recorded the fastest expansion at an 11.35% CAGR, while instruments retained 43.60% of the life science tools market share in 2025.

- By technology, next-generation sequencing expanded at a 16.9% CAGR; PCR & qPCR led with a 22.65% share of the life science tools market in 2025.

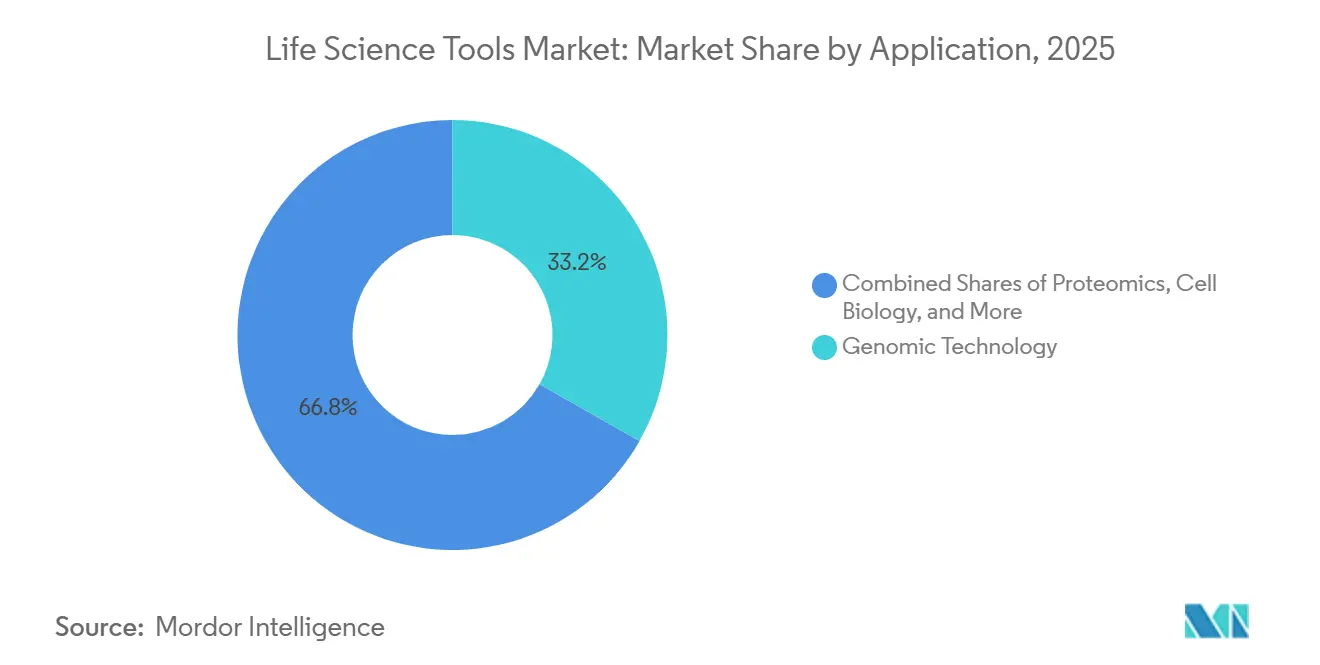

- By application, proteomics technology advanced at a 13.1% CAGR, whereas genomic technology accounted for 33.20% of the life science tools market in 2025.

- By end-user, diagnostic laboratories grew the fastest, with a 11.85% CAGR; research laboratories held 58.10% of the life science tools market share in 2025.

- Geographically, Asia-Pacific posted the highest regional CAGR of 10.95%, while North America remained the most significant regional contributor with a 40.10% share.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Life Science Tools Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in demand for biopharmaceuticals & growing research funding | +1.80% | Global; strongest in North America & Europe | Medium term (2-4 years) |

| Rising incidence of infectious diseases & genetic disorders | +1.50% | Global; higher impact in APAC & Africa | Short term (≤2 years) |

| Increasing adoption of NGS & single-cell analysis platforms | +1.20% | North America & Europe core; expanding to APAC | Medium term (2-4 years) |

| Expansion of CRISPR-based core-facility workflows | +0.90% | North America & Europe; emerging in APAC | Long term (≥4 years) |

| AI-driven high-throughput automation for multi-omics prep | +0.80% | Global; led by North America | Medium term (2-4 years) |

| Emergence of decentralized bioprocess labs in LMICs | +0.60% | APAC, MEA, Latin America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rise in Demand for Biopharmaceuticals & Growing Research Funding

Escalating focus on large-molecule therapeutics pushes laboratories to secure advanced mass spectrometers for protein characterization and high-parameter flow cytometers for cell therapy research. The United States ARPA-H's USD 2.5 billion budget, earmarked for breakthrough health platforms, underscores the government's commitment to cutting-edge instrumentation.[1]ARPA-H, “Fiscal Year 2025 Budget Overview,” arpa-h.gov European venture funding also rose, fueling orders for contract research organizations that now handle specialized analytics that were once kept in-house. Together, these forces accelerate capital buys and recurring consumables spend, reinforcing the life science tools market growth outlook. FDA approvals of 55 novel therapeutics in 2024, 43% of which were biologics, elevated demand for upstream analytics, including high-resolution mass spectrometry and automated cell-line screening.[2]U.S. Food & Drug Administration, “Novel Drug Approvals 2024,” fda.gov Horizon Europe earmarked USD 10.3 billion for health research over 2024-2025, with 28% directed toward infectious-disease and personalized-oncology projects that procure sequencers and imaging systems.[3]European Commission, “Horizon Europe Health 2024-25,” ec.europa.eu

Rising Incidence of Infectious Diseases and Genetic Disorders

WHO surveillance flagged heightened monkeypox and avian influenza activity in 2024, compelling public health labs to expand PCR testing capacity and stock multiplex NGS panels.[4]World Health Organization, “Disease Outbreak News—Monkeypox and H5N1 Updates,” who.int In parallel, nationwide rare-disease screening in the United Kingdom expanded access to genomic testing by 25%, boosting demand for automated sample-preparation systems. The dual burden of infectious threats and hereditary conditions underscores the need for scalable, rapid-turnaround platforms, advancing the life science tools market across clinical and research environments alike. WHO confirmed 6.2 million mpox cases in 2024-2025, a 34.0% jump that spurred orders for rapid PCR diagnostics and viral genomics surveillance systems. Newborn-screening panels expanded to an average of 62 genetic conditions in 2025, up from 54 two years earlier, and increased tandem mass spectrometry utilization in metabolic panels. India allocated USD 144 million for district-level molecular diagnostic hubs, planning 1,200 real-time PCR systems and 180 benchtop sequencers by 2027. PerkinElmer’s NeoBase 2 kit, launched in 2024, reduced sample-to-result time by 22%, enabling higher newborn screening throughput.

Increasing Adoption of NGS and Single-Cell Analysis Platforms

With NovaSeq X and similar systems pushing whole-genome costs below USD 200, institutions can now pursue population-scale projects without compromising budgets. Single-cell innovations from 10x Genomics propelled instrument placements 40% higher in 2024, expanding applications in oncology and immunology. These shifts prompt facilities to reconfigure workflows around high-throughput, data-intensive approaches, spurring purchases of automated library builders and high-performance computing clusters. The United States National Cancer Institute earmarked USD 1.2 billion for single-cell atlases through 2026, which is translating into bundled cell-sorting and library-preparation purchases.

Expansion of CRISPR-Based Core-Facility Workflows

Universities and research institutes have institutionalized CRISPR services, running hundreds of edits monthly with robotic liquid handlers and GMP-grade bioreactors.[5]Broad Institute, “CRISPR Screening Core Facility Services,” broadinstitute.org Standardized protocols shorten project turnaround and escalate consumable pull-through, while therapeutic CRISPR pushes demand for purification columns and advanced analytics in regulated environments, bolstering long-term equipment sales. IDT’s Alt-R CRISPR-Cas12a Ultra, launched in March 2025, delivered 3x the editing efficiency in primary T cells, expanding cell-therapy workflows. Core facilities now bundle CRISPR kits with automated liquid handlers, trimming hands-on time by 60% and boosting reproducibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced instruments | -0.40% | Global; smallest institutions hardest hit | Short term (≤2 years) |

| Stringent regulatory requirements for LDTs | -0.30% | North America & Europe; spreading worldwide | Medium term (2-4 years) |

| Shortage of skilled bioinformaticians | -0.20% | Global; most acute in APAC & emerging regions | Medium term (2-4 years) |

| Reagent supply-chain risks from export controls | -0.15% | Global; impact highest where China is primary supplier | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Instruments

Flagship mass spectrometry platforms surpass USD 1 million, placing acquisition out of reach for smaller laboratories. Academic budgets struggle to reconcile instrument upgrades with staffing needs, leading many to rely on fee-for-service core facilities. Such budget pressures slow adoption and dilute the near-term trajectory of life science tools market expansion. Thermo Fisher’s reagent-rental model allows zero upfront cost but still leaves smaller labs vulnerable to per-sample fees.

Stringent Regulatory Requirements for Lab-Developed Tests

The FDA’s 2024 LDT rule mandates extensive validation and documentation, lengthening assay launch timelines and increasing compliance expenses. Smaller diagnostic labs often retreat from innovative offerings or partner with larger networks, curbing immediate instrument purchases and dampening growth. FDA’s April 2024 rule requires high-risk LDTs to undergo pre-market review by 2027, adding document-control and validation costs. Europe’s IVDR requires a notified-body review that can cost up to EUR 150,000 per assay and take two years, pushing smaller labs to outsource. The compliance burden is concentrating testing volume at reference labs with the capacity to amortize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Accelerate Outsourcing Trends

Services rose fastest, with an 11.35% CAGR, as drug developers externalized analytics to control fixed costs and tap specialized expertise. Contract research organizations, now equipped with premium genomics and proteomics platforms, offer turnkey workflows that once demanded heavy in-house investment. Pharmaceutical clients value rapid capacity scaling and global site reach, propelling recurring fee income and enlarging the life science tools market.

Instruments maintained the largest share of the life science tools market at 43.60% in 2025. Capital expenditure patterns remained resilient among top-tier pharma firms and research universities, while consumables supplied roughly 60% of recurring revenue for leading vendors. Hybrid models that lease hardware bundled with services are taking hold, converting lump-sum equipment purchases into predictable operating expenses and deepening customer lock-in.

By Technology: NGS Surges While PCR Anchors Routine Workflows

Next-Generation Sequencing led technology expansion at a 16.9% CAGR. Clinical labs increasingly replace single-gene PCR assays with multi-gene NGS panels that consolidate testing and identify actionable variants. Population-scale genomics programmes from the United States to Singapore intensify instrument refresh cycles and spur upgrades to computational infrastructure, sustaining the life science tools market.

PCR & qPCR, despite ceding growth momentum, still accounted for 22.65% of the life science tools market in 2025. Its entrenched role in rapid pathogen detection and gene-expression analysis maintains a steady flow of consumables. Complementary technologies such as flow cytometry, mass spectrometry, and advanced separation systems broaden user options, ensuring diversified revenue pillars for suppliers.

By Application: Proteomics Gains Momentum

Proteomics posted the strongest 13.1% CAGR as drug discovery pivots toward functional protein readouts. Modern mass spectrometers, paired with refined sample-prep chemistries, now quantify thousands of proteins per run, fueling biomarker hunts and target-validation studies. The life science tools market benefits from elevated reagent usage and demand for high-resolution instruments optimized for intact protein and peptide analysis.

Genomic Technology accounted for 33.20% of the life science tools market in 2025. Clinical sequencing for rare diseases, oncology, and pharmacogenomics remains a consistent revenue generator. Cell biology solutions, including high-content imaging and stem-cell culture systems, complement genomic and proteomic insights, encouraging labs to build multi-omics suites that consolidate workflows and extend spending.

By End User: Diagnostic Labs Drive Clinical Adoption

Diagnostic laboratories expanded at a 11.85% CAGR as precision-medicine protocols entered routine practice. Laboratories upgraded their clinical-grade NGS rigs and installed AI-assisted interpretation software, shortening report turnaround time. Reimbursement frameworks covering genomic and proteomic tests accelerate instrument payback, energizing the life science tools market in healthcare settings.

Research laboratories accounted for 58.10% in 2025, underpinned by sustained public-sector grants and pharmaceutical R&D outlays. Core-facility consortia allow smaller departments to access premium equipment, spreading utilization and amortizing cost across investigators. Industry-academia partnerships funnel additional capital into shared instrumentation, anchoring long-term demand.

Geography Analysis

North America accounted for 40.10% of the life science tools market in 2025, buoyed by National Institutes of Health funding and a cluster of global tool makers headquartered in the United States. Robust venture capital flows into Boston and San Francisco biotech corridors reinforce equipment refresh cycles, though ageing campus infrastructure and intensifying grant competition may nudge growth toward mid-single digits.

Asia-Pacific, advancing at a 10.95% CAGR, is the fastest-growing region. China directed more than USD 15 billion to biotech programmes in 2024, while India’s USD 2.4 billion infusion supported distributed vaccine and biologics sites. South Korea and Singapore continue building world-class sequencing and cell-therapy hubs. These initiatives anchor long-run investments in high-capacity NGS, mass spectrometry, and automated bioprocessing, adding heft to the global life science tools market.

Europe posts stable, mid-single-digit gains amid macroeconomic uncertainties and rising energy costs, which weighed on new capital projects. Post-Brexit, the United Kingdom sought U.S. partnerships to maintain research momentum, while France and Switzerland remained strongholds for biologics analytics. Emerging centers in Poland and the Czech Republic adopted modular lab formats, providing fresh demand for compact instruments and entry-level consumables.

Regulatory Landscape

In the United States, oversight of laboratory-developed tests (LDTs) is tightening under the US Food and Drug Administration (FDA). This shift moves LDTs toward standard medical device requirements and increases the validation and documentation burden on diagnostic laboratories running PCR and NGS-based assays. Separately, the FDA signaled continued modernization of evidence generation in April 2026, initiating proof-of-concept real-time clinical trials and issuing a Request for Information for a broader pilot. That direction reinforces demand for compliant data workflows and instrument-software traceability.

In Europe, the European Medicines Agency (EMA) variations framework guideline updates became applicable from January 15, 2026, affecting lifecycle changes to regulated products and the supporting analytical packages used in development and manufacturing. In China, the National Medical Products Administration (NMPA) issued a revised Good Manufacturing Practice for Medical Devices in late 2025, with an effective date of November 1, 2026. The guidance emphasizes lifecycle risk management and supply chain accountability, and the agency also issued a 2026 medical device standards revision plan that can raise local type-testing and documentation requirements for instrument vendors and suppliers.

Competitive Landscape

Vendor concentration is moderate. Thermo Fisher Scientific, Danaher Corporation, and Agilent Technologies collectively hold sizable yet not dominant revenue positions, leveraging scale to invest in R&D and global distribution. Thermo Fisher’s USD 4.1 billion purchase of Solventum’s purification and filtration business in February 2025 broadened its bioprocessing suite and augmented cross-selling potential. Danaher folded Genedata’s bioinformatics stack into its portfolio in 2024, signalling a shift toward integrated hardware-software propositions.

Challengers such as Oxford Nanopore Technologies and Pacific Biosciences pursue differentiated sequencing chemistries that attract niche oncology and infectious-disease applications. AI-centric start-ups target data-analysis gaps by partnering with hardware vendors, aiming to bundle interpretation engines with instruments. Suppliers eye whitespace in decentralized manufacturing, field-deployable diagnostics, and full-workflow automation, areas where incumbents have limited penetration.

Strategic plays span technology licensing, region-specific manufacturing, and co-development alliances with pharma. For instance, Thermo Fisher partnered with the National Cancer Institute on the myeloMATCH trial, embedding its sequencing tools into a high-profile precision oncology study. Waters, Bruker, and BD launched application-specific columns, imaging profilers, and automated prep stations, respectively, sharpening competitive differentiation while expanding addressable spend.

Life Science Tools Industry Leaders

Illumina, Inc

Thermo Fisher Scientific Inc.

F. Hoffmann-La Roche Ltd.

Qiagen N.V.

Agilent Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven validation and higher documentation requirements are pushing laboratories and suppliers toward integrated workflows that connect instruments, reagents, software, and analytics. This creates room for turnkey, audited solutions across clinical genomics, molecular diagnostics, and biologics development. In parallel, Thermo Fisher Scientifics January 2026 collaboration with NVIDIA to integrate AI into scientific instrumentation and laboratory software points to sustained vendor investment in lab performance, automation, and data-handling capabilities that reduce manual bottlenecks in multi-omics workflows.

Multi-omics portfolio buildout and manufacturing capacity aligned to high-throughput testing are shaping near-term opportunity areas across sequencing, proteomics, and sample prep. Illuminas completion of its SomaLogic acquisition in January 2026 expands aptamer-based proteomics access within a major sequencing ecosystem, supporting broader multi-omics packages for research and translational users. On the supply side, Integrated DNA Technologies (IDT) completed an April 2026 expansion of its Coralville, Iowa manufacturing footprint that increased oligonucleotide synthesis capacity threefold. The added capacity supports NGS-based oncology and MRD workflows and improves fulfillment resilience for high-volume assay development and routine testing.

Recent Industry Developments

- May 2026: Roche entered into a definitive merger agreement to acquire PathAI for USD 750 million upfront plus up to USD 300 million in milestones. The deal expands Roches AI-driven digital pathology capabilities and strengthens its position in software-enabled diagnostics workflows that drive demand for imaging, staining, and associated lab informatics tools.

- April 2026: Thermo Fisher Scientific launched the Gibco CHOvantage GS Cell Line Development Kit, positioning it as an integrated platform to accelerate biologics development. The royalty-free, clinical-stage licensing model lowers barriers for biologics developers and supports pull-through for upstream cell line development reagents, analytics, and automation.

- January 2026: Illumina completed the acquisition of SomaLogic for USD 350 million in cash plus performance-based milestones and royalties. Integrating SomaLogics affinity proteomics technology extends Illuminas multi-omics offering and reinforces demand for end-to-end workflows spanning sample prep, measurement platforms, and downstream analysis.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the life science tools market covers instruments, consumables, reagents, and related services used in biotech, genetics, molecular biology, and cell biology workflows across research and diagnostic settings.

The scope excludes routine hospital supplies and general lab furniture, along with medical devices that are not used for life science testing or analysis.

Segmentation Overview

- By Type

- Instruments

- Consumables

- Services

- By Technology

- PCR & qPCR

- Sanger Sequencing

- Next-Generation Sequencing (NGS)

- Spatial-Omics & Single-Cell Platforms

- Separation Technologies

- Flow Cytometry

- Mass Spectrometry

- Nucleic-Acid Microarray

- Automation & Robotics Platforms

- Other Technologies

- By Application

- Genomic Technology

- Proteomic Technology

- Cell Biology Technology

- Drug Discovery & Development

- Clinical Diagnostics

- Other Applications

- By End-User

- Research Laboratories

- Diagnostic Laboratories

- Biopharmaceutical Companies

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by setting the market boundary and selecting demand indicators that can be tracked year after year. We use public sources such as the National Institutes of Health (NIH) budget and funding tables, US FDA databases for test authorizations and related updates, OECD health and R&D statistics, and World Bank macro indicators to anchor research intensity and lab activity.

To make the model workable, we also review company annual reports, investor decks, and earnings call transcripts to understand product mix and pricing commentary. Where available, trade flows are checked using customs and import-export statistics, and innovation direction is cross-checked using patent databases. The sources listed are illustrative, and we also use other public documents and databases to collect data, verify it, and clarify open questions.

Primary Interviews and Surveys

Primary work is used to pressure-test what we see in public data, and then to close gaps around average selling prices, replacement timing, and how services revenue behaves. We speak with stakeholders across instrument suppliers, reagent and consumables providers, distributors, labs, and procurement and operations teams. Inputs are balanced across major regions so country-level bias stays limited.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 16% | APAC: 44% |

| Mid tier: 45% | Functional/Unit leaders: 35% | EMEA: 35% |

| Smaller Players: 17% | Managers: 49% | Americas: 21% |

Market-Sizing & Forecasting

The size is first constructed using a top-down approach, where the spend pool is rebuilt from lab activity signals and workflow adoption across genomics, proteomics, and cell analysis. Inputs that shape the model include research funding direction, installed base growth for key instrument classes, consumables pull-through per instrument, service attachment rates, and technology mix shifts like PCR versus sequencing versus mass spectrometry.

After the total is formed, it is checked using selective bottom-up approximations such as sampled average selling price times unit volumes for major tool types, along with distributor and channel checks to avoid double counting. Where volume data is incomplete for niche tools, gaps are handled through penetration assumptions that are validated in interviews and then adjusted based on observable lab expansion and procurement cycles.

Forecasts are built using scenario analysis, since budgets, instrument replacement cycles, and pricing can move differently across regions and end users. Assumptions on pricing progression and mix are kept explicit so the forward view can be repeated and updated without needing hard-to-access datasets.

Data Validation & Update Cycle

The model is reviewed through several checks so one noisy indicator does not drive the final number. We compare outputs against independent signals such as funding trends, major instrument shipment commentary in filings, and consumables growth patterns, then investigate outliers until the underlying driver is clear.

Before sign-off, the estimates go through a multi-step internal review where assumptions are challenged and recalculated if needed. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major currency moves, large lab spending shifts, or step changes in adoption. Right before delivery, we run a fresh pass on key variables so clients receive the latest updated view.

Mordor Intelligence's Life Science Tools Market Size Measured Against Other Published Estimates

Published values for this market often do not line up because the scope boundary and the way pricing is handled can change the total quickly. Even when the same tool families are mentioned, differences in whether services are counted, how reagents are bundled, and which year currency is normalized to can move the number by billions.

A recurring gap comes from refresh cadence and currency timing, since fast-changing exchange rates and annual price resets affect reported US dollar values. Some estimates also apply a single price curve across instruments and consumables, even though consumables pull-through and discounting usually behave differently by workflow and buyer type. For that reason, the market size in Mordor Intelligence is kept tied to updated ASP logic and repeated validation checks against funding and procurement signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 153.81 B (2025) | |

| Trade Journal A | USD 176.93 B (2024) | Uses a different base year and a broader tool definition in the write-up, and the press-style estimate provides limited visibility on how services and consumables pricing were normalized. |

| Industry Bulletin B | USD 175.96 B (2025) | Runs on a longer-horizon growth frame with higher assumed price and adoption momentum, and the scope appears to combine adjacent workflow categories without clearly separating service revenue behavior. |

The spread is mainly explained by what gets bundled into the tool stack, how prices are stepped forward, and when the USD conversion is applied. When the scope boundary is kept consistent, and the pricing and mix assumptions are refreshed and checked against real-world lab activity, the resulting number is easier to trace and repeat in future updates.

Key Questions Answered in the Report

How big is the life science tools market in 2026?

The life science tools market stands at USD 164.47 billion in 2026 and is forecast to reach USD 230.07 billion by 2031 at a 6.93% CAGR.

Which segment shows the fastest growth?

Next-Generation Sequencing technology posts the top growth rate at 16.9% CAGR through 2031, driven by cost reductions and expanded clinical use.

Which region leads future expansion?

Asia-Pacific records the highest regional CAGR at 10.95%, supported by sizable public-sector biotechnology investments and manufacturing build-outs.

Why are services becoming so important?

Pharmaceutical and biotech companies outsource analytics to control fixed costs and access specialised expertise, pushing the Services segment to an 11.35% CAGR.

What regulatory changes affect market growth?

The FDA’s 2024 final rule on Lab-Developed Tests increases validation and documentation requirements, adding complexity and cost for clinical laboratories.

Page last updated on: