Bioprocess Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.91 Billion |

| Market Size (2031) | USD 13.13 Billion |

| Growth Rate (2026 - 2031) | 17.32% CAGR |

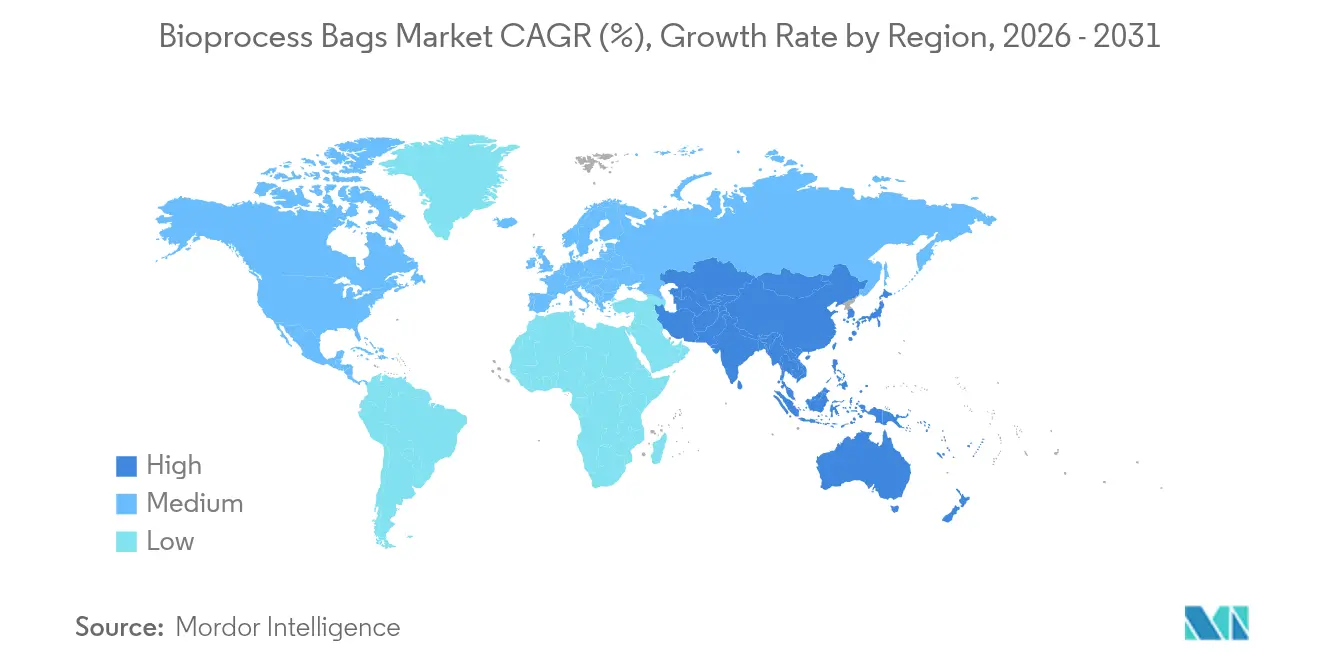

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

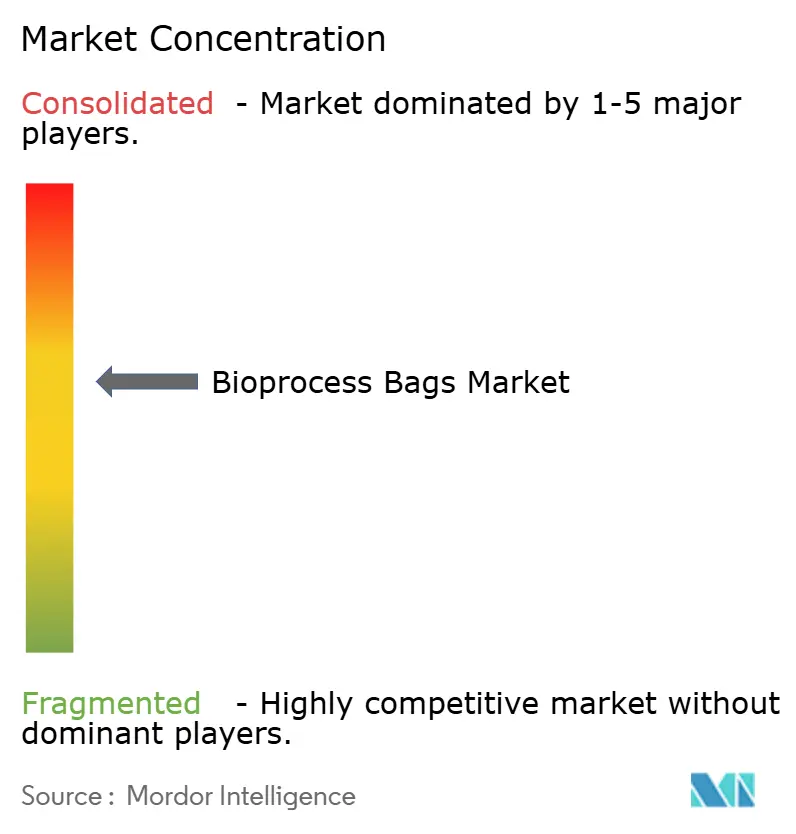

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioprocess Bags Market Analysis by Mordor Intelligence

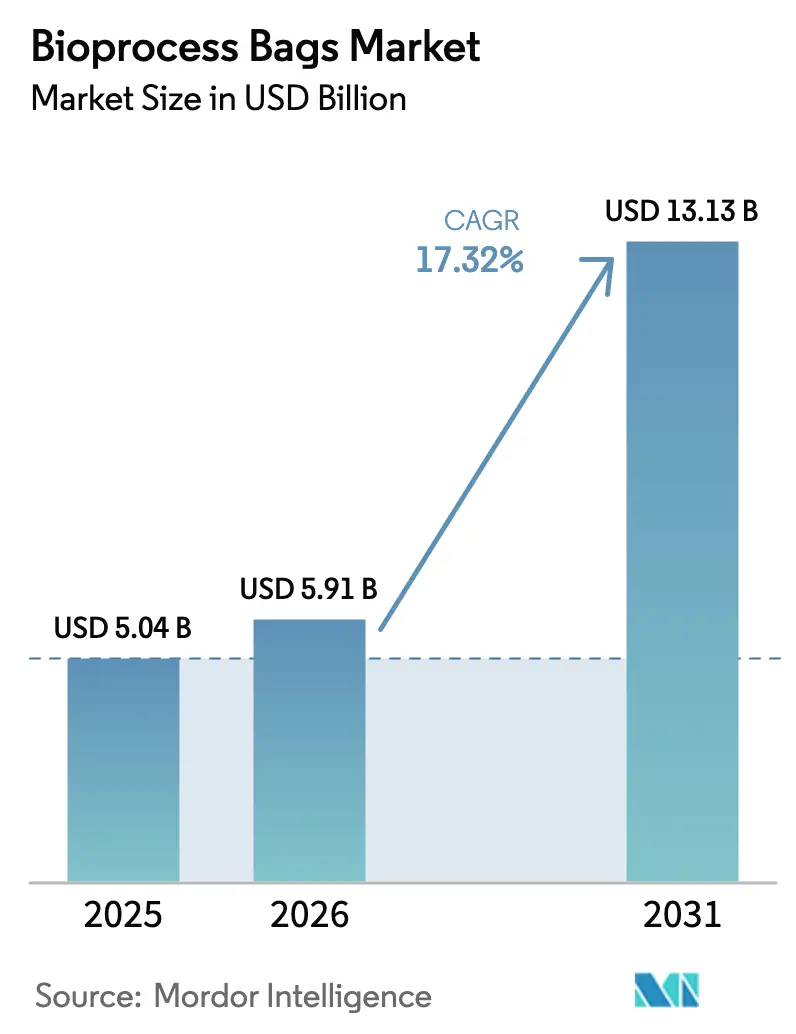

The bioprocess bags market size is expected to grow from USD 5.04 billion in 2025 to USD 5.91 billion in 2026 and is forecast to reach USD 13.13 billion by 2031 at 17.32% CAGR over 2026-2031. This powerful growth trajectory reflects how single-use technologies are replacing fixed stainless-steel systems, a change reinforced by global regulatory convergence and urgent flexibility demands from cell and gene therapy producers. Progress on environmental, social, and governance targets is aligning with operational efficiency programs as manufacturers try to lower water and energy consumption while sustaining sterile operations, further accelerating adoption of advanced polymer bags. Supply-chain localization prompted by the United States Biosecure Act has led to fresh capital spending that favors domestic bag manufacturing capacity. Meanwhile, technology partnerships, particularly around cryogenic and freeze-thaw formats, are reshaping specification standards and opening avenues for specialized suppliers able to validate closed, ultra-low-temperature workflows.

Key Report Takeaways

- By product type, single-use 3D bags led with 45.08% revenue share in 2025, while cryogenic and freeze-thaw formats are projected to post a 20.63% CAGR to 2031.

- By volume capacity, 20–200 L bags held 36.12% of the bioprocess bags market share in 2025, whereas >1,000 L systems are anticipated to scale at 19.21% CAGR through 2031.

- By material, polyethylene grades accounted for 71.05% share in 2025; fluoropolymer and other high-barrier films are forecast to grow at 18.36% CAGR.

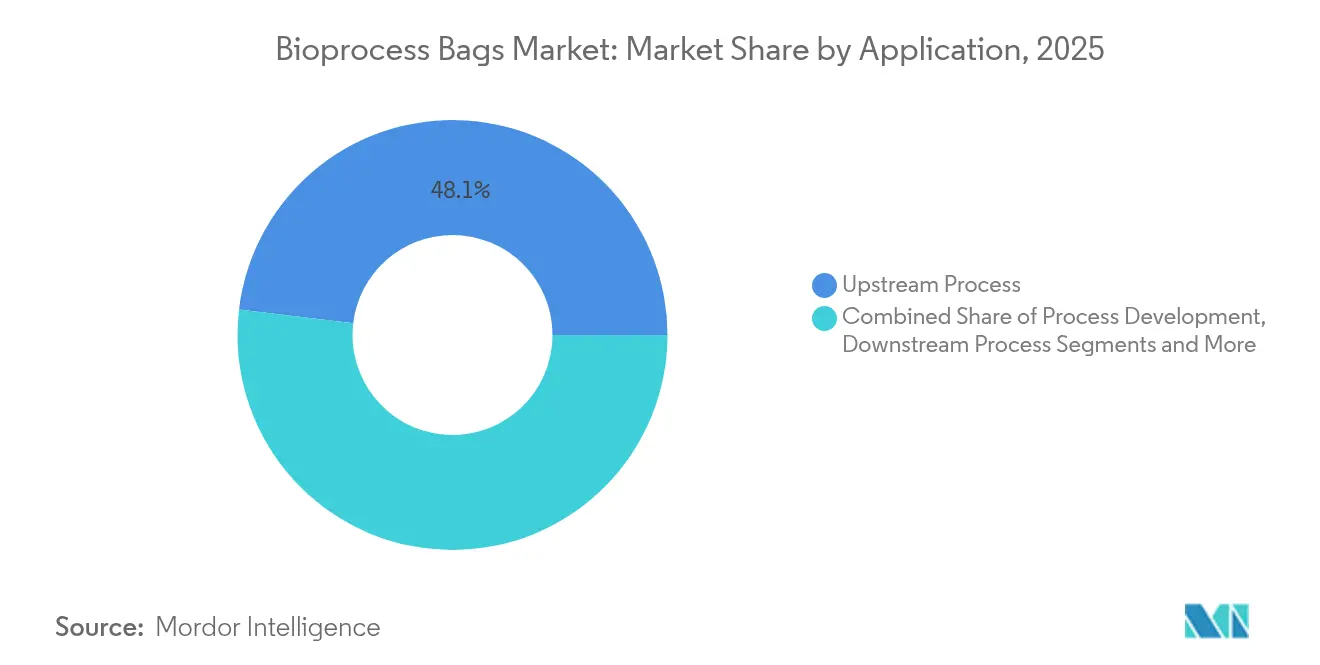

- By application, upstream processing captured 48.11% share in 2025, while downstream operations are poised for a 18.62% CAGR to 2031.

- By end user, biopharma companies controlled 55.74% share in 2025; CMOs/CDMOs represent the fastest-growing customer block at 18.24% CAGR.

- By geography, North America retained leadership with 40.88% share in 2025, while Asia-Pacific is projected to advance at 18.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bioprocess Bags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand For Biologic & Personalized Therapeutics | +4.2% | Global, with concentration in North America & EU | Long term (≥ 4 years) |

| Cost & Time Savings From Single-Use Workflows | +3.8% | Global, particularly APAC emerging markets | Medium term (2-4 years) |

| Rapid Capacity Expansion By CMOs/CDMOs | +3.1% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Closed-System Cryo- & Freeze-Thaw Bags For Cell & Gene Therapy | +2.9% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| ESG-Driven Reduction Of Water & Energy Footprint | +2.1% | EU leadership, global adoption | Long term (≥ 4 years) |

| Modular "Factory-In-A-Box" Facilities In Emerging Markets | +1.4% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Biologic & Personalized Therapeutics

Uptake of antibody-drug conjugates and autologous cell therapies pushed the FDA to clear 17 new biologic entities by mid-2024, amplifying pressure on flexible single-use infrastructure. Personalized regimens mean smaller batch sizes and greater changeover frequency, conditions under which the bioprocess bags market excels because disposables eliminate cross-contamination risk. Requirements for closed, traceable container-closure systems in the latest EMA ATMP guideline formalize single-use bags as a regulatory expectation for gene and cell therapy production[1]European Medicines Agency, “Regulatory News & Updates,” ispe.org. As demand widens geographically, every new therapeutic modality multiplies the volume and design variants needed, deepening addressable sales for suppliers positioned with modular portfolios. Collectively, these biologic pipelines anchor long-range visibility for the bioprocess bags market.

Cost & Time Savings From Single-Use Workflows

Changeover intervals have fallen from weeks to roughly 48 hours following adoption of single-use bioreactors, drastically boosting facility utilization. Eliminating cleaning validation steps cuts both direct labor hours and the documentation burden, advantages that gain prominence in multiproduct environments where regulatory audits scrutinize cross-contact risk. Capital-light distributed sites, sometimes described as factory-in-a-box modules, become feasible because single-use bags arrive gamma-irradiated and ready for immediate use, shrinking upfront spend and qualification time. Pharmaceutical producers also report faster technology transfer between continents because processes are effectively “packaged” within the bag system itself. Those cumulative savings translate into a structural incentive that sustains double-digit expansion for the bioprocess bags market.

Rapid Capacity Expansion By CMOs/CDMOs

Lonza, Samsung Biologics, Fujifilm Diosynth, and WuXi Biologics collectively control large blocks of outsourced biologic volume, and each favors standardized disposable hardware to smooth client onboarding. Planned investments, such as Samsung Biologics’ USD 1.46 billion program for 784,000 L of single-use capacity by 2025, reinforce Asia-Pacific as an anchor for future bag demand. Cost savings from consolidated procurement let CDMOs secure volume-based discounts that further steer projects toward bag formats. As global sponsors diversify supply chains to hedge geopolitical risk, they favor partners already validated on common single-use platforms, strengthening network effects inside the bioprocess bags market. These dynamics point to sustained double-digit order growth from the services segment through 2030.

Closed-System Cryo & Freeze-Thaw Bags for Cell & Gene Therapy

Cryogenic bags meeting −196 °C performance thresholds are displacing rigid vials because they handle larger volumes without breaching sterility during filling or thawing[2]Sartorius, “Bottles vs Freezing Bags: Regulatory & Quality Comparison,” sartorius.com. Fluoropolymer liners and high-barrier multilayers restrict oxygen and moisture ingress, preserving cell viability over long storage cycles. Closed tubing assemblies facilitate sterile welding and sampling, critical for advanced therapy batches that can exceed USD 1 million in value per patient. Regulatory bodies require exhaustive extractable profiling for these formats, raising entry barriers but granting compliant vendors premium pricing power. Worldwide clinical trial momentum therefore channels incremental revenue into the bioprocess bags market at a sector-leading CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost at large-scale volumes | −2.8% | Emerging markets, global | Short term (≤ 2 years) |

| Extractables/leachables in downstream steps | −1.9% | North America, Europe | Medium term (2-4 years) |

| Escalating plastic-waste rules | −1.2% | Europe leading, global spread | Long term (≥ 4 years) |

| Petrochemical polymer feedstock volatility | −0.8% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Total Cost at Large-Scale Volumes

Economic inflection appears around 2,000 L, where the recurring spend on consumables may eclipse amortized stainless-steel depreciation. Continuous production can magnify this gap because bags require replacement at every campaign, increasing cost of goods for high-titer molecules. Some mature monoclonal antibody programs therefore adopt hybrid architectures that keep single-use upstream but switch to hard-piped downstream purification to balance cash outlays. Rising resin prices and foreign-exchange swings tighten budgets in cost-sensitive geographies, temporarily slowing conversion for legacy blockbusters. Nonetheless, as suppliers optimize multilayer resins and extend bag lifetimes, the cost curve is projected to narrow over the planning horizon, tempering long-term drag on the bioprocess bags market.

Extractables & Leachables in Downstream Purification

Updated FDA guidance from April 2024 obliges firms to characterize every contact layer chemically and toxicologically, intensifying scrutiny of complex multilayer bag films[3]U.S. FDA CDER, “ANDA Submission: Risk-Based Extractable and Leachable Quality Information,” fda.gov. Transition away from USP <88> Class VI toward USP 665 by May 2026 triggers widespread requalification, adding time and expense for change control. Advanced LC-MS/MS mapping can uncover dozens of oligomers at parts-per-billion thresholds, forcing suppliers to maintain vast spectral libraries and offer toxicological risk assessments. Smaller producers lacking analytical depth may hesitate to switch bag vendors, slowing competitive churn. Although these hurdles are transient, they temporarily dilute growth velocity inside segments reliant on downstream disposable modules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: 3D Formats Anchor Growth Momentum

Single-use 3D bags captured 45.08% of the bioprocess bags market share in 2025 on the back of superior gas-liquid mixing that accelerates high-cell-density cultures. Market preference for deep square or cylindrical geometries reflects the push toward fed-batch perfusion, where oxygen transfer and shear control dictate protein quality attributes. Cryogenic and freeze-thaw bags clock a 20.63% CAGR, driven by autologous therapies demanding seamless transitions between ultra-low storage and rapid thaw stages. Suppliers now bundle temperature-graded tubing sets and bag welders as turnkey kits, creating ecosystem stickiness that reinforces the bioprocess bags market trajectory. Regulatory recognition of closed, presterilized film assemblies adds another adoption catalyst, especially for sites running parallel investigational new drug trials.

Traditional 2D pillow bags remain vital for process development units that value fast set-up and minimal footprint, offering an entry route for smaller firms into the bioprocess bags industry. Rocker and wave bags service shear-sensitive insect or stem-cell lines, while multi-use autoclavable bags hold a niche in academic labs where budget cycles favor reusable gear. Innovation is shifting toward smart films embedded with humidity or pressure sensors, signalling how digital process analytics could further expand the bioprocess bags market. Although rigid containers persist for solvent-heavy steps, ongoing polymer R&D continually erodes their domain. End users therefore plan capital projects with a baseline assumption that bag technology will satisfy most upstream and an increasing share of downstream unit-operations through 2030.

By Volume Capacity: Large-Scale Adoption Gains Credibility

The 20–200 L cohort commanded the largest slice of the bioprocess bags market size at 36.12% in 2025, balancing ease of handling with commercial-scale batch output. Multiproduct plants value this range because bag swaps can happen within day-shift windows, keeping downstream skid idle time low. Recent launches of radial-flow sparger designs have boosted oxygen transfer coefficients, allowing titers comparable to fixed reactors, a milestone that underpins confidence in middle-volume formats.

1,000 L assemblies represent the fastest-growing bracket, advancing at 19.21% CAGR as reinforced film laminates alleviate rupture concerns under high hydrostatic pressure. Hybrid stainless-steel exoskeletons now encase extra-large bags, merging structural rigidity with disposability, a design that broadens the practical ceiling of the bioprocess bags market. Demand also persists in the sub-20 L micro-bioreactor space for clone screening, where micro-architecture mirrors production-scale mixing patterns, shrinking scale-up risk. Flexibility to toggle capacity bands via common control systems encourages end users to standardize on single supplier platforms, deepening wallet share per facility.

By Material: Polyethylene Dominance Endures Amid Barrier Film Innovation

Conventional polyethylene (LLDPE, HDPE, ULDPE) constituted 71.05% of the bioprocess bags market size in 2025, favored for predictable weldability and gamma stability. Layered structures blend different PE grades to fine-tune tensile strength and impact resistance without compromising permeability specs. Additive packages such as hindered amine light stabilizers extend shelf life in environments exposed to sporadic UV during warehouse handling.

High-barrier fluoropolymers and EVOH-containing laminates chart an 18.36% CAGR thanks to low oxygen transmission rates vital for stem-cell culturing. Improved wettability and lower extractable profiles push these films into previously stainless-steel-dominated downstream ultrafiltration modules, expanding addressable acreage for the bioprocess bags market. EVA continues to serve ultra-flexible cryogenic roles, while mixed PE/PA/PP composites trade raw-material cost for elevated puncture resistance in logistics chains. Suppliers investing in cradle-to-cradle verification anticipate future recycling mandates that could reshape procurement criteria beyond 2027.

By Application: Upstream Procedures Retain Volume Leadership

Upstream processing occupied 48.11% share of the bioprocess bags market in 2025, mirroring entrenched adoption of disposable seed and production bioreactors. Sterile, pre-welded harvest lines limit operator intervention, helping manufacturers satisfy Annex 1 contamination control directives without costly retrofits. Nutrient-rich perfusion regimes are increasingly supported by bag-based depth-filtration hold tanks, extending disposability beyond the reactor shell.

Downstream unit-operations chalk a 18.62% CAGR as chromatography buffers and viral inactivation pools shift into single-use storage, limiting clean-in-place correlations. Media and buffer prep relies heavily on 2D tote bag assemblies that collapse post-use, freeing floor space. Process development teams value rapid configuration swaps as they iterate design of experiments, an agility that keeps the bioprocess bags market at the core of innovation cycles. Storage and transport use-cases emphasize multilayer thermal insulation films, a specification growth point tied to cell therapy distribution networks.

By End User: Biopharma Firms Dominate While CDMOs Accelerate

Originator biopharma companies held 55.74% of the bioprocess bags market share in 2025, leveraging disposables to shorten clinical lot release times and derisk capacity planning. Internal pipeline diversification toward multi-specific antibodies fuels investment in modular, bag-centric suites capable of parallel product campaigns. Stringent change-control governance prompts brand owners to lock in preferred vendors early, sustaining recurring revenue streams for integrated suppliers.

CMOs/CDMOs post an 18.24% CAGR because flexible bag platforms allow them to juggle numerous client processes without stainless-steel retrofits. Academic consortia and government-funded pilot plants depend on off-the-shelf bag kits to achieve regulatory-grade sterility with limited capital outlay, feeding early-stage demand in the bioprocess bags industry. Cell and gene therapy developers procure cryo-bags featuring prevalidated leachable datasets to satisfy expedited review pathways, adding premium-margin sales. The aggregate pull from these end-user cohorts ensures order books remain robust through 2030.

Geography Analysis

North America retained 40.88% of the bioprocess bags market in 2025, underpinned by resilient biopharmaceutical pipelines and federal incentives such as the USD 17.5 million Resilience award that shores up domestic active ingredient output. Thermo Fisher’s USD 4.1 billion purchase of Solventum’s purification arm signals continued consolidation that deepens vertical integration. Canada’s push for mRNA vaccine self-sufficiency funnels new capital into single-use suites, while Mexico leverages USMCA logistics corridors to attract fill-finish projects that favor disposable equipment. Collective activity maintains the bioprocess bags market momentum across the continent.

Asia-Pacific is the fastest-growing region at 18.94% CAGR, led by China’s USD 4.17 billion commitment to expand biologics infrastructure in 2025. Samsung Biologics and MilliporeSigma both executed nine-figure investments in South Korea, raising regional supplier density and slashing lead times. Japan’s harmonized ATMP framework and Australia’s advanced-manufacturing grants further entice global sponsors to source bag systems locally, entrenching the bioprocess bags market in the Pacific corridor.

Europe balances stringent sustainability rules with well-funded life-science clusters, preserving its relevance as a premium demand base. Germany and the United Kingdom host multinationals that routinely pilot novel barrier films to satisfy impending circular-economy targets. Ireland’s National Institute for Bioprocessing Research and Training upskills operators on single-use assemblies, reinforcing local uptake. Concurrently, the phase-out of USP Class VI plastics by May 2026 positions European vendors with advanced extractable analytics to expand share, sustaining the bioprocess bags market as continental policies evolve.

Competitive Landscape

Thermo Fisher Scientific, Sartorius, and Danaher command sizeable installed bases yet the overall arena remains moderately fragmented, allowing niche innovators to coexist. Thermo Fisher’s USD 4.1 billion Solventum acquisition augments its downstream filtration capabilities, cementing a cradle-to-commercial bag portfolio that appeals to turnkey facility buyers. Danaher merged Cytiva and Pall into a USD 7.5 billion entity, creating scale economies across resin manufacturing and film extrusion that could shave lead times in an industry prone to material shortages.

Strategic partnerships intensify as firms court specialized expertise. Wacker Biotech and Expression Manufacturing unite lentiviral process know-how with high-barrier bag designs, a collaboration meant to de-risk large-scale gene therapy commercial runs. Qosina’s joint effort with Sealed Air to launch the NEXCEL BIO1250 film underscores how packaging giants are entering the bioprocess bags market with multilayer substrates proven in adjacent food-grade applications. These alliances collectively reduce time-to-market for complex formats like freeze-thaw assemblies.

Regulatory transitions act as competitive sorting mechanisms. Suppliers with robust extractables databases stand to capture incremental volume once USP 665 enforcement begins because buyers prefer partners that minimize additional toxicology testing. Sustainability credentials are emerging as a tiebreaker; Sartorius’s R&D expansion in France explicitly targets recyclable mono-material films, aligning with EU waste-reduction directives. Given these dynamics, integrated players continue to widen their moat, yet specialized firms retain avenues to thrive by solving narrow, high-value problems.

Bioprocess Bags Industry Leaders

Corning Incorporated

Avantor Inc.

Charter Medical, LLC

Danaher Corporation (Cytiva & Pall)

Entegris Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sartorius Stedim Biotech expanded manufacturing and R&D capacities for innovative bioprocess solutions in France.

- May 2025: Qosina and Sealed Air launched NEXCEL BIO1250, a co-extruded bioprocessing bag film targeting high-performance single-use workflows.

Global Bioprocess Bags Market Report Scope

As per the scope of the report, bioprocessing bags are a flexible and customizable solution used to safely handle liquids in bioprocess environments. Bioprocessing bags are used in small research and mass production. The bioprocess bags market is segmented by product, application, end user, and geography. By product, the market is segmented into single-use bioprocess bags and multi-use bioprocess bags. By application, the market is segmented into process development, upstream process, downstream process, media preparation, and others. By end user, the market is segmented into pharmaceutical and biotechnology companies, CMOs and CROs, and academic and research laboratories. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market size is provided in terms of value (USD).

| Single-use 2D Bioprocess Bags |

| Single-use 3D Bioprocess Bags |

| Cryogenic & Freeze-thaw Bags |

| Mixing & Rocker Bags |

| Multi-use (Autoclavable) Bags |

| Less Than or Equal 20 L |

| 20-200 L |

| 200-1000 L |

| Greater Than 1000 L |

| Polyethylene (LLDPE/HDPE/ULDPE) |

| Ethylene-vinyl Acetate (EVA) |

| Multilayer PE/PA/PP Blends |

| Fluoropolymer & High-barrier Films |

| Process Development |

| Upstream Process |

| Downstream Process |

| Media & Buffer Preparation |

| Storage & Transport |

| Biopharma & Biotechnology Companies |

| CMOs & CDMOs |

| Academic & Research Institutes |

| Cell & Gene Therapy Developers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Single-use 2D Bioprocess Bags | |

| Single-use 3D Bioprocess Bags | ||

| Cryogenic & Freeze-thaw Bags | ||

| Mixing & Rocker Bags | ||

| Multi-use (Autoclavable) Bags | ||

| By Volume Capacity | Less Than or Equal 20 L | |

| 20-200 L | ||

| 200-1000 L | ||

| Greater Than 1000 L | ||

| By Material | Polyethylene (LLDPE/HDPE/ULDPE) | |

| Ethylene-vinyl Acetate (EVA) | ||

| Multilayer PE/PA/PP Blends | ||

| Fluoropolymer & High-barrier Films | ||

| By Application | Process Development | |

| Upstream Process | ||

| Downstream Process | ||

| Media & Buffer Preparation | ||

| Storage & Transport | ||

| By End User | Biopharma & Biotechnology Companies | |

| CMOs & CDMOs | ||

| Academic & Research Institutes | ||

| Cell & Gene Therapy Developers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving the rapid CAGR in the bioprocess bags market?

The main catalysts are accelerating demand for personalized biologics, cost savings from eliminating cleaning validation, and record capacity expansions among CDMOs, all of which rely heavily on disposable bag systems for flexibility and speed.

Which product type dominates today’s sales?

Single-use 3D bioprocess bags hold 45.08% market share owing to superior gas exchange and scalability suited for high-density mammalian cell culture.

Why is Asia-Pacific the fastest-growing region?

Government investment programs, large-scale capacity additions by Samsung Biologics and MilliporeSigma, and favorable cost structures underpin the region’s 18.94% CAGR outlook.

How are new regulations affecting bag material choice?

The shift to USP 665 standards pushes suppliers to provide detailed extractable data, favoring high-barrier fluoropolymer or EVOH films with inherently low leachable profiles.

Are single-use bags economical for very large commercial volumes?

Cost benefits diminish beyond 2,000 L continuous runs; however, hybrid facilities that combine bag-based upstream modules with stainless-steel downstream skids can balance economics and flexibility.

Page last updated on: