Biofilter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.5 Billion |

| Market Size (2031) | USD 5.38 Billion |

| Growth Rate (2026 - 2031) | 8.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biofilter Market Analysis by Mordor Intelligence

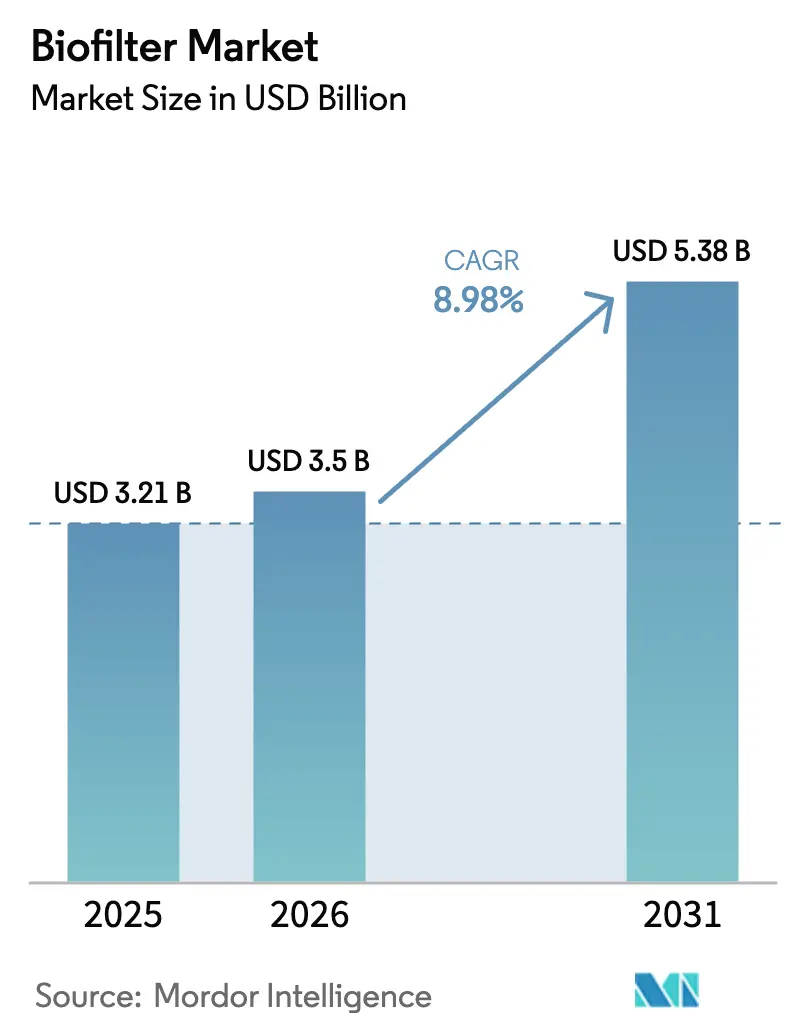

Biofilter market size in 2026 is estimated at USD 3.5 billion, growing from 2025 value of USD 3.21 billion with 2031 projections showing USD 5.38 billion, growing at 8.98% CAGR over 2026-2031. A tightening global regulatory framework, soaring adoption of biological air- and water-treatment technologies, and the growing emphasis on sustainable resource management anchor this growth trajectory. Government directives such as the European Union’s Urban Wastewater Treatment Directive 2024/3019, effective January 2025, oblige municipal and industrial plants to install advanced quaternary treatment, placing biofiltration at the center of compliance strategies. In the United States, the Environmental Protection Agency’s Subpart OOOOb zero-emission standards for new oil and gas facilities, effective May 2024, are widening the addressable opportunity for biofilter-based VOC and methane abatement.[1]U.S. Environmental Protection Agency, “Small Entity Compliance Guide for Oil and Natural Gas Sector: Emission Standards for New, Reconstructed, and Modified Sources,” U.S. EPA, epa.gov Rapid industrialization across Asia-Pacific, coupled with intensifying aquaculture activity, helps the region consolidate a 41.34% biofilter market share in 2024.[2]Xiang Li, “Shrimp Industry in China: Overview of the Trends in the Production, Imports and Exports During the Last Two Decades, Challenges, and Outlook,” Frontiers in Sustainable Food Systems, frontiersin.org Vendors are responding with larger-scale, modular, and carbon-valorizing solutions that promise lower lifecycle costs and additional revenue streams from captured gases.

Key Report Takeaways

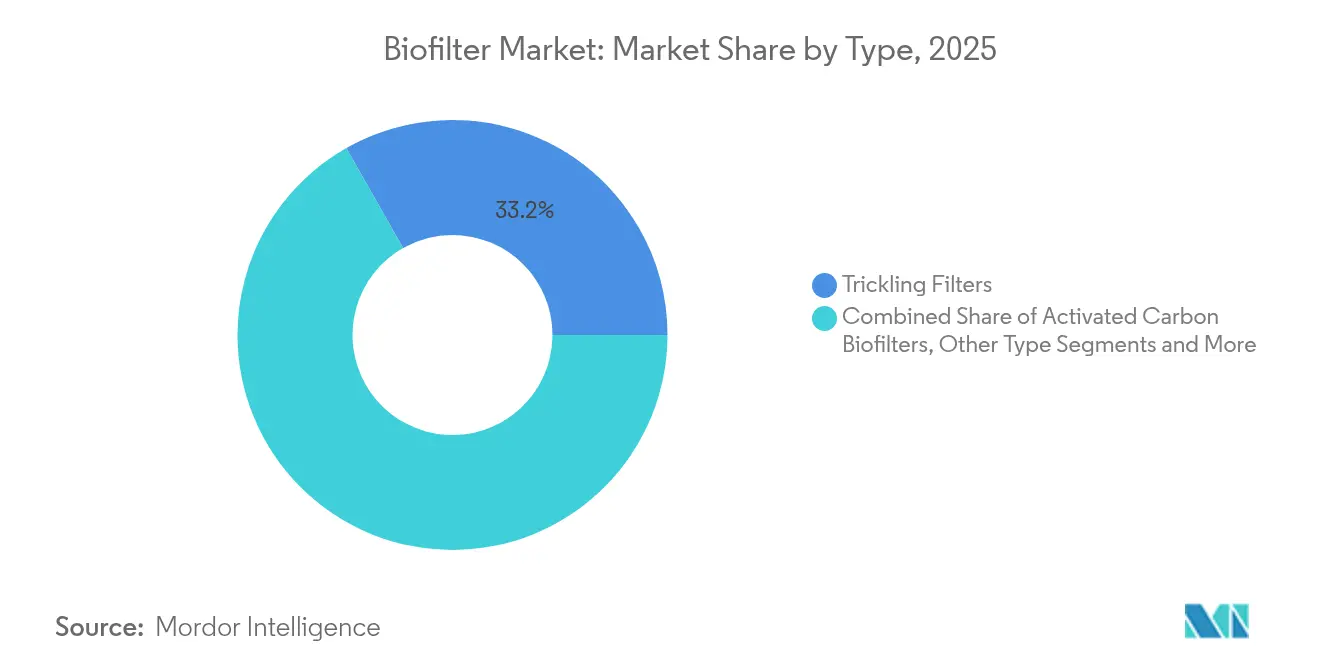

- By type, trickling filters led with 33.22% revenue share in 2025, whereas denitrification systems are projected to advance at a 13.37% CAGR through 2031.

- By filter media, moving bed media commanded 39.18% of the biofilter market size in 2025 and is forecast to grow at an 11.57% CAGR.

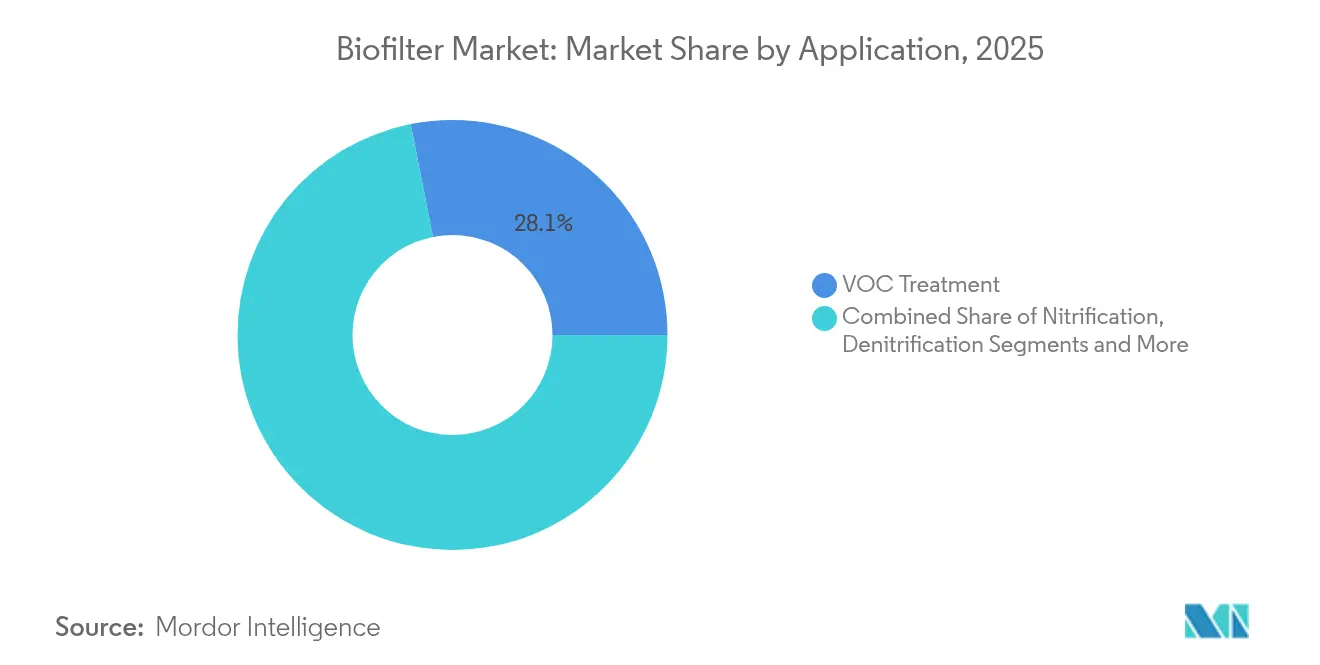

- By application, VOC treatment accounted for 28.12% of the biofilter market size in 2025 and is set to expand at a 13.02% CAGR to 2031.

- By end user, aquaculture held 25.11% share of the biofilter market in 2025, while the biopharma segment is poised for an 11.23% CAGR.

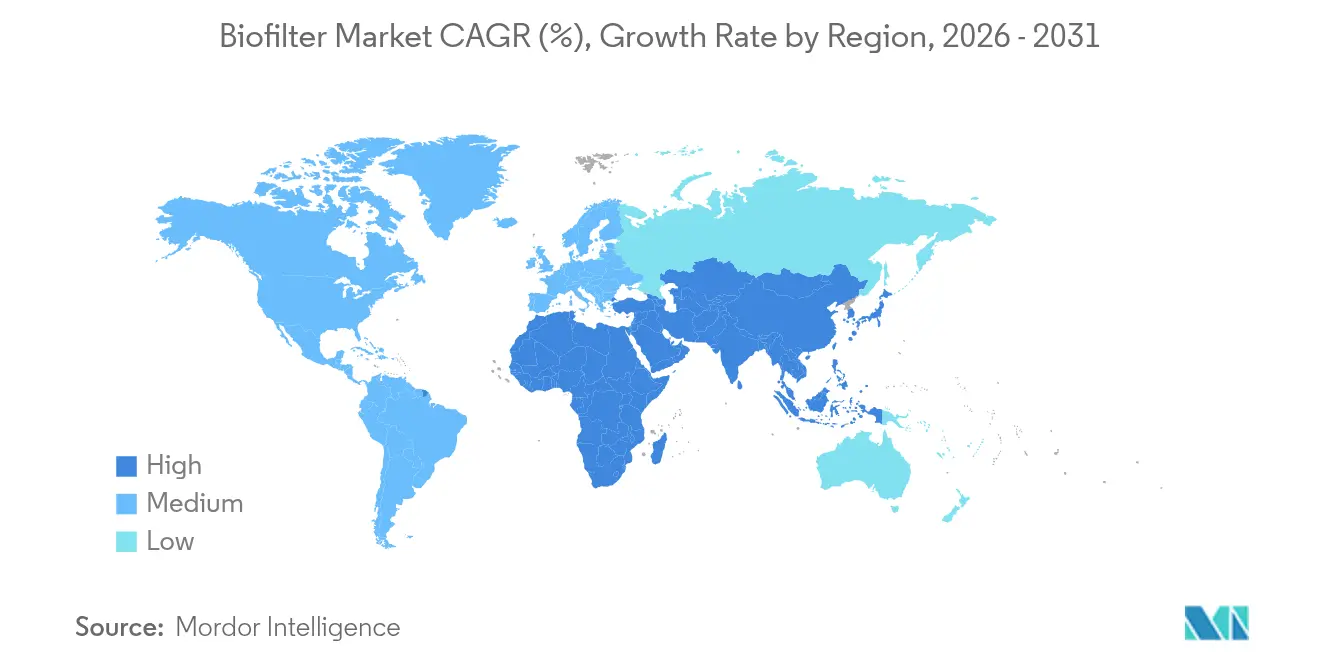

- By geography, Asia-Pacific dominated with 41.02% revenue share in 2025; the region is expected to post a 10.08% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biofilter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent environmental regulations on air & water quality | 2.8% | Global, with strongest impact in EU & North America | Medium term (2-4 years) |

| Growing demand for sustainable waste & odor-control solutions | 2.1% | Global, particularly APAC industrial corridors | Long term (≥ 4 years) |

| Expansion of recirculating aquaculture (RAS) facilities | 1.9% | APAC core, spill-over to Americas | Medium term (2-4 years) |

| Rising adoption in VOC abatement for advanced manufacturing | 1.6% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Modular biofilter platforms for mobile/decentralized treatment | 1.2% | Global, with early adoption in remote locations | Long term (≥ 4 years) |

| Biofilter-enabled carbon valorization from off-gas microbes | 0.8% | North America & EU pilot projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental Regulations on Air & Water Quality

Tighter statutes in major economies are reshaping purchasing decisions. The EU directive compels quaternary treatment for agglomerations above 100,000 population equivalents, shifting pharmaceutical and chemical producers toward biofilters that handle micropollutant loads with minimal energy draw.[3]European Commission, “New Rules for Urban Wastewater Management Set to Enter into Force,” European Commission, environment.ec.europa.eu In parallel, Subpart OOOOb obligates zero-emission technologies for new pneumatic controllers in U.S. oil and gas installations, leading operators to specify biofilters for methane-rich vent streams. Because both air- and water-stream rules now carry extended-producer-responsibility clauses, companies are financially motivated to invest in high-performance biological systems that also qualify for environmental tax credits.

Growing Demand for Sustainable Waste & Odor-Control Solutions

Corporate ESG goals elevate biofilter adoption from a compliance necessity to a brand differentiator. Food and beverage plants in Northern Europe report quantifiable reductions in sulfur-bearing odors after installing compact biofilter cabinets, thereby safeguarding nearby communities and brand equity. The technology’s ability to transform waste gases into beneficial by-products—such as compost precursors—further improves internal rates of return. Researchers document 92% methane removal in integrated livestock systems, with solid end-products suitable for soil amendment.

Expansion of Recirculating Aquaculture (RAS) Facilities

Land-based shrimp and finfish farms depend on biofilters to maintain near-closed-loop water quality. China, producing 58.1 million t of aquatic products in 2024, demonstrates scale: more than 70% of its shrimp farms now run biofloc-based RAS modules. Trials that combined ozone nanobubbles with moving bed biofilm reactors achieved 99.5% Vibrio pathogen reduction and 82% postlarval survival.[4]Jie Zhang, “Integration of Biofloc and Ozone Nanobubbles for Enhanced Pathogen Control in Prenursery of Pacific White Shrimp,” MDPI, mdpi.com Because water treatment accounts for up to 40% of RAS operating costs, performance gains in media design and dissolved-oxygen delivery translate directly into profit margins.

Rising Adoption in VOC Abatement for Advanced Manufacturing

Semiconductor fabs and pharmaceutical plants require ultra-clean exhaust management. Modern biofilter modules remove mixed VOC streams at 90%+ efficiency while consuming 30–50% less energy than thermal oxidizers. As Asia-Pacific builds new chip foundries, engineering teams increasingly specify biological systems to align with carbon-neutral corporate roadmaps. Membrane-aerated biofilm reactors now demonstrate simultaneous reductions of organics and nitrogen in high-strength effluents, simplifying treatment trains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & O&M costs | -1.8% | Global, particularly affecting SMEs | Short term (≤ 2 years) |

| Limited technical expertise & market awareness in EMs | -1.2% | Emerging markets in APAC, MEA, Latin America | Medium term (2-4 years) |

| Media fouling from PFAS & micro-plastics reduces lifespan | -0.9% | Global, concentrated in industrial applications | Long term (≥ 4 years) |

| Regulatory uncertainty over large-scale biofilter bio-aerosols | -0.6% | EU & North America regulatory jurisdictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & O&M Costs

Industrial biofilter installations range from USD 50,000 to USD 500,000 and demand annual operating budgets that can reach 25% of capex for media replacement and energy. Although modular, plug-and-play skids shorten construction schedules, payback periods often remain beyond three years for small emitters. Build-operate-transfer contracts from large integrators help mitigate the burden, yet financing hurdles persist where green-loan frameworks are still nascent.

Limited Technical Expertise & Market Awareness in Emerging Markets

Effective biofilter operation relies on microbiology and process-control know-how that is scarce in many developing regions. The Water Research Foundation is investing USD 4 million in guideline programs to bridge this gap. Parallel moves by OEMs to embed remote monitoring and automated nutrient dosing are gradually reducing skill barriers, but limited awareness still delays first-time purchases among municipal utilities and SMEs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Trickling Filters Lead Despite Denitrification Surge

Trickling filters held a 33.22% revenue lead in 2025, underpinned by decades-long municipal use and low maintenance profiles. Their share of the biofilter market remains strong in retrofit programs where existing basins can be upgraded with optimized media. Denitrification units, however, are accelerating at a 13.37% CAGR because regulators now limit total nitrogen to single-digit milligram levels in sensitive waters. Hybrid systems—such as AquaPoint’s Bioclere OH that merges moving bed reactors with trickling stages—illustrate the emerging convergence of technologies. The biofilter industry anticipates further crossover designs that cut footprints while lifting kinetics.

Second-generation media refinement reinforces both segments. Ceramic ceramsite with 55.8% porosity delivers 87.8% nitrate removal and 0.82 kg TN m³-d volumetric rates, surpassing conventional pumice by wide margins. Suppliers that patent such formulations stand to capture premium margins as utilities weigh lifecycle performance over initial price.

By Filter Media: Moving Bed Dominance Accelerates

Moving bed carriers achieved a 39.18% slice of the biofilter market in 2025 and are growing at 11.57% CAGR. Micro-structured surfaces on Veolia’s AnoxKaldnes Z-MBBR sustain homogeneous biofilm thickness, cutting back-washing frequency. On the cost-sensitive end, Evolution Aqua’s K1 Micro offers 950 m² m³ protected area and superior solids handling, making it attractive for medium-scale RAS facilities. Enhanced oxygen transfer and shearing forces combine to delay media fouling, extending bed lifespans well past the five-year mark.

High-temperatures and aggressive chemicals in semiconductor exhaust streams have also pushed demand for specialty ceramic rings that maintain structural integrity above 120 °C. Suppliers tout lower pressure drops and compact reactor designs, aligning with fab operators’ high air-change frequencies. As product differentiation grows, strategic partnerships between media innovators and system integrators are likely to intensify.

By Application: VOC Treatment Leads Dual Growth

VOC treatment captured 28.12% of the 2025 biofilter market and is on track for a 13.02% CAGR. Electronics, coatings, and pharmaceutical manufacturing sectors regard biofilters as the lowest total-cost solution for mixed hydrocarbon plumes. Benchmarks reveal 90%+ VOC removal and single-digit ppmv outlet concentrations without supplemental fuel. Nitrification and denitrification applications remain important in municipal upgrades, but growth tempering reflects already high penetration in developed regions.

Carbon valorization pilots point to future upside. Studies converting CO₂ and methane into acetate and biofuels within electrically assisted biofilter reactors report 85% CO₂ capture alongside power generation. If scaled, such dual-service units could reposition biofilters from compliance devices to profit centers, amplifying addressable revenues.

By End User: Aquaculture Dominance Faces Biopharma Challenge

Aquaculture retained 25.11% of revenue in 2025 as Asian operators upgraded to land-based RAS and biofloc modules that recycle more than 90% of process water. Intensifying disease-prevention targets in shrimp hatcheries demand ammonia and pathogen control best supplied by multi-stage biofilters. In parallel, the biopharma segment is registering an 11.23% CAGR; cGMP clean-room expansions worldwide require ultra-high-purity water and fume treatment, both areas where biological systems now match or outperform physical-chemical alternatives.

Chemical processing and food-and-beverage operations continue steady adoption for odor and nutrient removal, reinforced by ESG scorecards. Emerging storm-water installations leverage biofilter trenches that remove 50% of total phosphorus in peri-urban catchments, hinting at municipal infrastructure diversification.

Geography Analysis

Asia-Pacific commanded 41.02% of the biofilter market in 2025 and is set for a 10.08% CAGR as industrial output and protein demand rise. China’s strategy to elevate domestic shrimp capacity beyond 7 million t depends on thousands of new RAS units, each fitted with multi-stage biofiltration. Local authorities subsidize such systems to curb coastal discharge, accelerating adoption across Guangdong and Guangxi provinces. Japanese firms add technological depth: Asahi Kasei’s sewage-born biogas scrubber in Kurashiki yields pipeline-grade methane, demonstrating region-specific innovation.

North America reports mid-single-digit growth anchored in regulatory compliance and asset renewal cycles. Oil-and-gas operators retrofit aging compressors with biofilter skids that meet Subpart OOOOb methane limits while improving ESG ratings. Municipal consent orders in the United States likewise push nutrient-retrofitting of existing clarifiers using denitrification biofilters, often financed through state revolving funds.

Europe’s regulatory leadership ensures continuous capital expenditure. The Urban Wastewater Treatment Directive mandates quaternary treatment rollouts that will span the decade, making biofilters integral to meeting micropollutant targets. Early-stage projects in Germany and France already report 70–80 mg/L reductions in APIs after adding biological aerated biofilters. Meanwhile, the Middle East, Africa, and South America are emerging as longer-term demand centers. Scarcity-driven desalination hubs in the Gulf are testing biofilter pretreatment to extend membrane life, and Brazilian pulp-and-paper mills are integrating trickling units in effluent lines to meet updated national standards.

Competitive Landscape

The biofilter market shows moderate fragmentation. Veolia tops revenue charts with an integrated service model covering design, financing, and O&M; its Delaware PFAS facility exemplifies the pivot toward high-margin contaminants of emerging concern. CECO Environmental acquired DS21 Co. in South Korea to reinforce its Asian water-treatment portfolio, signaling regional consolidation.

Technology differentiation is the chief competitive lever. Biorem’s USD 60.5 million backlog demonstrates the commercial pull of energy-efficient odor abatement systems. Patenting activity concentrates on media porosity control, automated nutrient dosing, and hybridizer modules that handle varying loads without operator intervention. Smaller specialists leverage standard modular designs to compete for decentralized projects where footprint and cost sensitivity dominate.

Partnerships between OEMs and industrial end-users are deepening. Veralto’s USD 15 million investment in Axine underscores a trend: large corporates source disruptive electro-chemical aids to pair with biofilters for persistent pollutant removal. Supply-chain integration is likewise visible; Greenlane Renewables’s landfill gas upgrades rely on in-house carrier media, keeping margins internal. The landscape is expected to tilt toward players that bundle remote analytics, performance guarantees, and circular-economy pathways for captured gases.

Biofilter Industry Leaders

Biorem Inc.

Veolia Water Technologies

Pentair Aquatic Eco-Systems

Xylem

De Nora TETRA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Biorem Inc. secured more than USD 8 million in new orders, lifting its order backlog to USD 60.5 million

- February 2025: Asahi Kasei inaugurated a biogas purification demonstration in Kurashiki City, Japan, with commercialization planned for 2027

- January 2025: BioLargo Inc. announced commercial PFAS treatment projects and product line expansions

Global Biofilter Market Report Scope

As per the scope of the report, a biofilter is a type of device that purifies harmful air, water, and other common substances. It is used across various industries and applications to control pollution and odor. The biofilter market is segmented by type, filter media, application, end user, and geography. By Type, the market is segmented into biological aerated biofilter systems, denitrification biofilter systems, activated carbon biofilters, trickling filters, submerged filters, and other types. By filter media, the market is segmented into ceramic rings, bio balls, moving bed filter media, and other filter media. By application, the market is segmented into VOC treatment, nitrification, denitrification, odor abatement, and other applications. By end-user, the market is segmented into storm water management, water & wastewater collection, chemical processing, food & beverage, aquaculture, biopharma industry, and other end users. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers a value (USD) for the above segments.

| Biological Aerated Biofilter Systems |

| Denitrification Biofilter Systems |

| Activated Carbon Biofilters |

| Trickling Filters |

| Submerged Filters |

| Other Types |

| Ceramic Rings |

| Bio Balls |

| Moving Bed Filter Media |

| Other Filter Media |

| VOC Treatment |

| Nitrification |

| Denitrification |

| Odor Abatement |

| Other Applications |

| Storm Water Management |

| Water & Wastewater Collection |

| Chemical Processing |

| Food & Beverage |

| Aquaculture |

| Biopharma Industry |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Biological Aerated Biofilter Systems | |

| Denitrification Biofilter Systems | ||

| Activated Carbon Biofilters | ||

| Trickling Filters | ||

| Submerged Filters | ||

| Other Types | ||

| By Filter Media | Ceramic Rings | |

| Bio Balls | ||

| Moving Bed Filter Media | ||

| Other Filter Media | ||

| By Application | VOC Treatment | |

| Nitrification | ||

| Denitrification | ||

| Odor Abatement | ||

| Other Applications | ||

| By End User | Storm Water Management | |

| Water & Wastewater Collection | ||

| Chemical Processing | ||

| Food & Beverage | ||

| Aquaculture | ||

| Biopharma Industry | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the biofilter market and how fast is it growing?

The market is valued at USD 3.5 billion in 2026 and is forecast to grow at a 8.98% CAGR to reach USD 5.38 billion by 2031.

Which segment holds the largest biofilter market share?

Trickling filters led with 33.22% revenue share in 2025, reflecting widespread municipal and industrial use.

Why is Asia-Pacific the fastest-growing region in the biofilter market?

Rapid industrial expansion, the prevalence of RAS aquaculture, and supportive environmental regulations give the region a projected 10.08% CAGR through 2031.

How do biofilters compare to thermal oxidizers for VOC control?

Modern biofilters achieve 90%+ VOC removal while consuming 30–50% less energy, lowering total cost of ownership for manufacturers.

What are the main barriers to wider biofilter adoption?

High capital and operating costs, along with limited technical expertise in emerging markets, remain key obstacles, though modular systems and remote monitoring are mitigating factors.

Can biofilters contribute to carbon capture and utilization strategies?

Yes. Pilot projects demonstrate 85% CO₂ removal with simultaneous conversion into valuable biofuels, repositioning biofilters as both compliance and revenue-generating assets.

Page last updated on: