Life Sciences BPO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

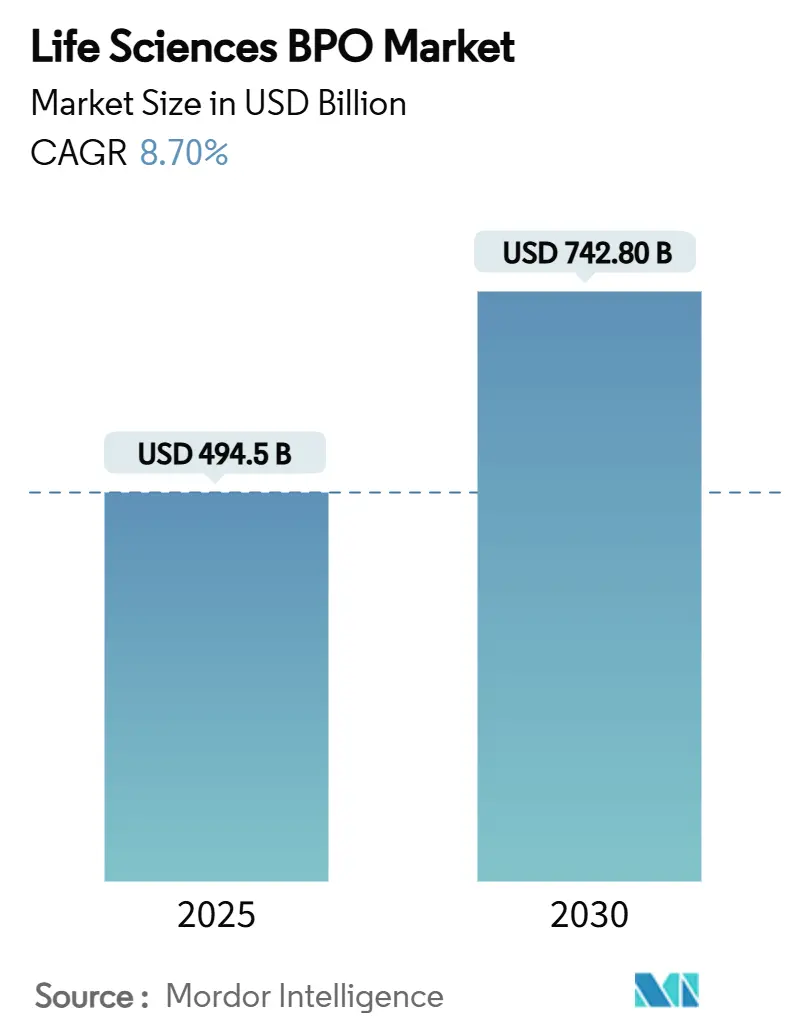

| Market Size (2025) | USD 494.5 Billion |

| Market Size (2030) | USD 742.80 Billion |

| Growth Rate (2025 - 2030) | 8.70% CAGR |

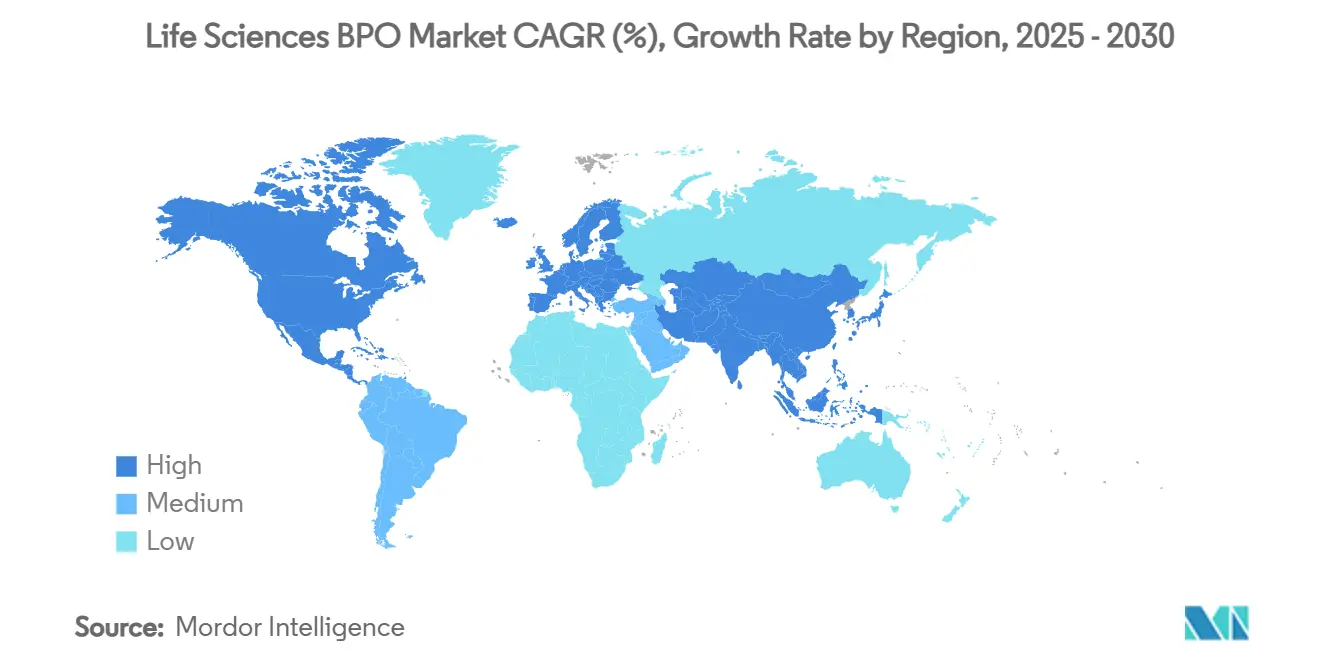

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Life Sciences BPO Market Analysis by Mordor Intelligence

The life sciences BPO market size stood at USD 494.5 billion in 2025 and is forecast to reach USD 742.8 billion by 2030, translating into an 8.70% CAGR over the period. This strong trajectory reflects how asset-light operating models, rising drug-pricing pressure, and complex R&D pipelines are converting outsourcing from a tactical cost lever into a structural requirement for life sciences companies. Contract research organizations (CROs) continue to serve as the backbone of externalized clinical development. Yet, contract development and manufacturing organizations (CDMOs/CMOs) are scaling faster as biologics, antibody-drug conjugates, and cell-gene therapies push demand for specialized capacity. Integrated full-service partnerships dominate today’s deal structures, but functional service provider (FSP) contracts are gaining favor when companies want sharper control over critical tasks. Regionally, North America anchors the market, while Asia Pacific is closing the gap on the back of India’s growing CDMO ecosystem and China-plus-one diversification. Consolidation—typified by Novo Holdings’ USD 16.5 billion takeover of Catalent—has intensified the competitive environment and raised questions about future capacity availability.

Key Report Takeaways

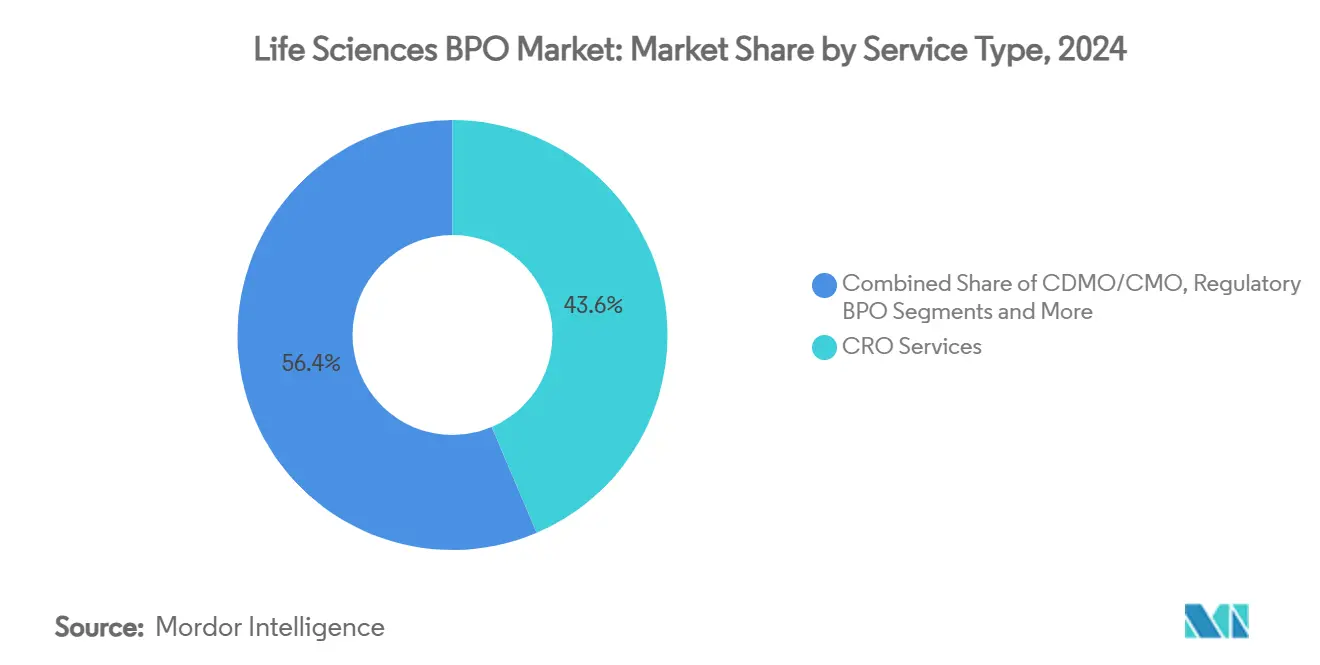

- By service type, CRO services led with a 43.6% share of the life sciences BPO market in 2024. CDMO/CMO services are projected to expand at an 11.3% CAGR through 2030, the fastest among service categories, as biologics scale drives manufacturing outsourcing.

- By end user, Pharmaceutical companies accounted for 57.1% of the life sciences BPO market size in 2024, whereas biotechnology companies are forecast to grow at an 8.4% CAGR to 2030.

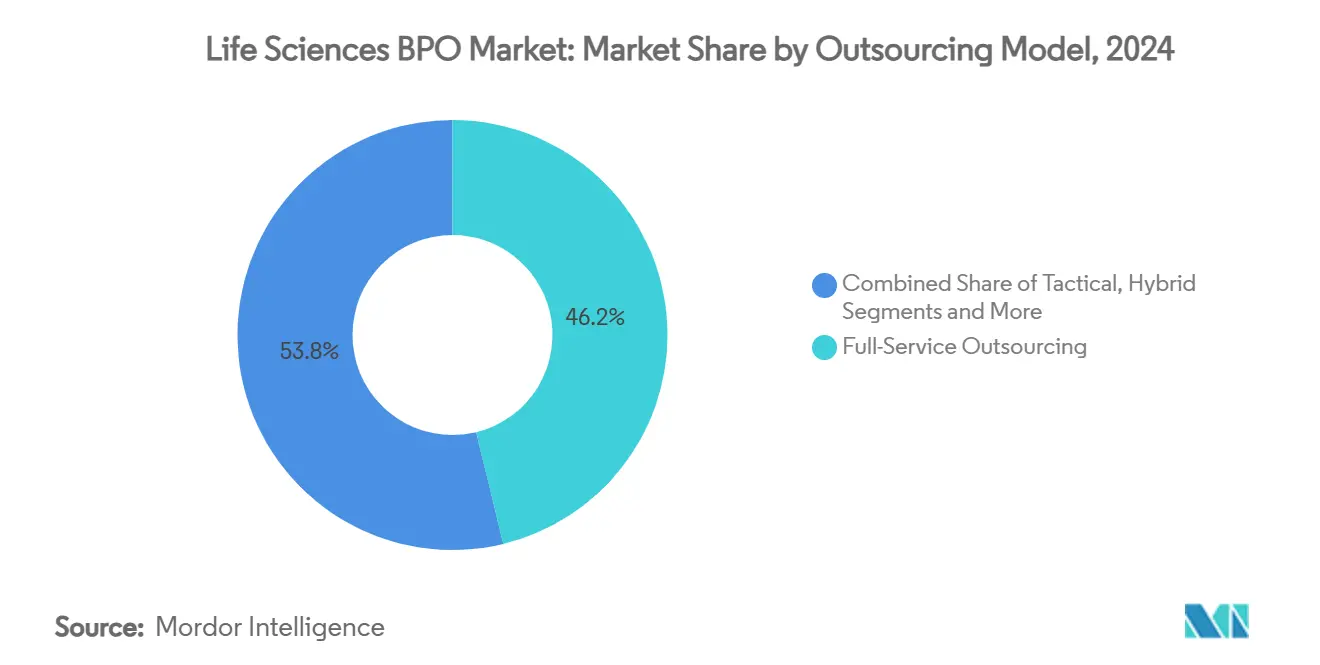

- By outsourcing model, Full-service outsourcing retained 46.2% of the life sciences BPO market share in 2024, while the FSP model is projected to post a 9.8% CAGR to 2030.

- Geographically, North America captured 41.6% revenue in 2024; Asia Pacific is set to grow at an 8.5% CAGR to 2030 as India and Southeast Asia expand capacity.

Global Life Sciences BPO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising R&D spend and trial complexity | +2.10% | US, EU, global | Medium term (2-4 years) |

| Drug-pricing pressure driving cost-efficient outsourcing | +1.80% | US, EU | Short term (≤ 2 years) |

| Biologics & CGT pipeline needs specialised CRO/CDMO capacity | +2.30% | North America, EU, APAC | Long term (≥ 4 years) |

| Regulatory-compliance outsourcing surge (eCTD v4.0, IDMP) | +1.20% | Global, EU-led | Medium term (2-4 years) |

| Mid-cap biotech IPO boom favouring flexible FSP contracts | +1.40% | North America, EU | Short term (≤ 2 years) |

| Generative-AI-enabled protocol design accelerating modular BPO | +0.90% | US early adoption, global roll-out | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising R&D Spend & Trial Complexity

Drug development now averages USD 2.3 billion per asset, and study timelines often exceed 12 years, magnifying the appeal of external expertise. Oncology illustrates the challenge: biomarker-driven designs demand narrow patient pools, real-world evidence, and tumor-specific analytics that a specialized CRO can deliver more efficiently than internal teams. At the same time, the Inflation Reduction Act’s pricing provisions incentivize companies to preserve margins through operational efficiency, propelling deeper outsourcing commitments. Advanced modalities—such as antibody-drug conjugates or autologous cell therapies—require cleanrooms, single-use systems, and regulatory know-how few sponsors possess, further embedding service providers into the development value chain. Collectively, these realities keep the life sciences BPO market on an upward path.

Drug-Pricing Pressure Driving Cost-Efficient Outsourcing

Legislation in the United States and heightened European health technology assessments have tightened reimbursement corridors, forcing sponsors to scrutinize cost structure. Outsourcing now extends beyond traditional manufacturing into pharmacovigilance, regulatory affairs, and even commercial operations, where large multi-functional vendors achieve 15–25% cost savings relative to entirely in-house execution. Venture-backed biotechs, more attuned to cash-burn rates, increasingly choose milestone-based FSP deals that match cost to progress while preserving strategic autonomy. This pivot adds momentum to FSP adoption yet simultaneously elevates competition among providers vying for smaller, targeted work packets. As cost containment intensifies, integrated vendors with scale and technology will consolidate share within the life sciences BPO market.

Biologics & CGT Pipeline Needs Specialized CRO/CDMO Capacity

Contract manufacturers are slated to control 54% of global biologics capacity by 2028, up from 43% in 2024, signaling a decisive shift to outsourced production. In parallel, the cell-and-gene therapy market is creating an acute need for viral-vector suites, personalized supply chains, and regulatory mastery. Large pharma firms lack readiness for these modality-specific demands, resulting in long-term dependency on CDMOs with high-grade cleanrooms and qualified personnel. Powerhouses such as Samsung Biologics and WuXi Biologics continue to expand Asian footprints, although potential disruptions from the proposed BIOSECURE Act highlight jurisdictional risk. The combination of capacity constraints and specialized know-how assures sustained double-digit growth in this slice of the life sciences BPO market.

Regulatory-Compliance Outsourcing Surge (eCTD v4.0, IDMP)

eCTD v4.0 migrations, Identification of Medicinal Products (IDMP) mandates, and evolving post-marketing safety obligations have made compliance workloads heavier and more technical. Sponsors without dedicated regulatory operations teams increasingly tap specialist vendors that offer automated document management, AI-enabled submission analytics, and global health-authority liaison support. For many mid-cap and emerging biotechs, outsourcing regulatory affairs has shifted from an option to a necessity because internal expertise is scarce and retaining it is expensive. Large, well-capitalized service providers also benefit as the burden of continuous system upgrades weeds out smaller competitors. The net effect is a steady compliance-driven inflow of projects, reinforcing top-line stability for the life sciences BPO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-security & IP-leakage concerns | -1.30% | US, EU, global | Short term (≤ 2 years) |

| Evolving data-privacy laws (GDPR, HIPAA 2026 update) | -0.80% | EU-centric, global impact | Medium term (2-4 years) |

| Offshore cost advantage eroded by currency & wage inflation | -1.10% | APAC core, global | Medium term (2-4 years) |

| ESG-driven reshoring pressure in US/EU | -0.90% | North America, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Security & IP-Leakage Concerns

Cyberattacks on life sciences companies cost an average USD 4.82 million per breach in 2023—well above cross-industry levels, making data protection a board-level issue. BPO engagement introduces additional risk vectors because proprietary protocols, patient data, and manufacturing blueprints traverse multiple IT environments.[1]Emma Stoye, “The Unfulfilled Dream of Drug Reshoring,” Chemical & Engineering News, cen.acs.org The rise of cloud-hosted eClinical platforms and AI engines widens the threat surface, forcing providers to adopt zero-trust architectures and aggressive third-party risk-assessment regimes. These necessities inflate operating expenses and can deter smaller sponsors worried about IP leakage. While robust security can become a competitive differentiator, the overall effect moderates the growth trajectory of the life sciences BPO market.

Evolving Data-Privacy Laws (GDPR, HIPAA 2026 Update)

The European Health Data Space Regulation and Germany’s Health Data Use Act add new layers of consent, anonymization, and data-transfer requirements. Parallel US reforms expected in the 2026 HIPAA update will likely extend protections to AI-derived insights, compelling substantial system upgrades across sponsor and provider landscapes. Coordinating compliance across jurisdictions raises overhead, erodes some offshore cost benefits, and disqualifies vendors lacking global regulatory capability. Yet for large service providers, the complexity acts as a barrier to entry, consolidating mid- to long-term revenue. As regulations proliferate, the life sciences BPO market must balance faster digital workflows with rigorous privacy safeguards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Manufacturing Momentum Reinforces Growth

The life sciences BPO market size for CRO services equaled 43.6% of overall revenue in 2024, underscoring the segment’s maturity. However, CDMO/CMO services are advancing at an 11.3% CAGR, buoyed by capital-intensive biologic and cell-therapy programs that require sterile suites, viral-vector lines, and single-use bioreactors. Sponsors outsource to avoid multi-billion-dollar plant investments and to access regulatory know-how around complex modalities. Meanwhile, regulatory-medical affairs outsourcing is benefiting from eCTD v4.0 adoption, which demands metadata-rich submissions that many internal teams cannot support.[2]ISACA Research Team, “Cloud Security Challenges in the Pharmaceutical Industry,” ISACA, isaca.org

Pharmacovigilance BPOs are integrating AI for triage and signal detection, yet must navigate intensifying regulatory scrutiny, tempering growth against higher compliance costs. Commercial outsourcing shows uneven momentum as virtual engagement reduces field-force demand, whereas cold-chain logistics and serialization are thriving on the back of personalized therapies. Taken together, manufacturing-oriented services will remain the primary engine driving expansion within the life sciences BPO market.

By End User: Biotech Appetite Outpaces Big Pharma

Pharmaceutical companies accounted for 57.1% of revenue in 2024, but their growth is moderating as many have already externalized a considerable portion of non-core functions. Biotechnology companies, by contrast, are scaling at an 8.4% CAGR as venture-backed firms transition into capital-efficient development models that rely heavily on external CRO, CDMO, and regulatory partners. Asset-light biotech strategies dovetail with the FSP and modular outsourcing formats, granting these sponsors control over key decisions while mitigating fixed-cost exposure.

Medical-device players are increasingly applying pharma-style outsourcing to combination products, digital therapeutics, and software-as-medical-device solutions where clinical evidence expectations mirror drug standards. Academic institutes represent a niche yet influential customer cohort, often pioneering novel trial designs and AI-assisted data analysis. The rise of fully virtual life sciences companies—organizations that own IP but outsource every operational function—further broadens the demand base and secures long-term relevance for the life sciences BPO market.

By Outsourcing Model: Functional Services Gain Ground

Full-service arrangements still contribute the most significant share, 46.2% in 2024 because sponsors prize single-vendor accountability across complex programs. Yet the FSP model is climbing at a 9.8% CAGR as companies search for agility, pricing flexibility, and granular control over high-value tasks. FSP contracts now extend beyond monitoring and statistics into specialized functions such as cell-therapy supply-chain management or AI-driven data-science pods. Tactical, project-based outsourcing is fading due to coordination inefficiency, whereas hybrid-captive strategies are resurfacing for modalities that demand dedicated infrastructure but still benefit from vendor skill sets. Outcome-based contracts—where providers assume milestone or approval risk—remain nascent yet hold disruptive potential. The choice of outsourcing model increasingly aligns with therapeutic complexity, capital availability, and sponsor risk tolerance, reinforcing dynamic segmentation in the life sciences BPO market.

Geography Analysis

North America held 41.6% of life sciences BPO revenue in 2024, underpinned by an extensive clinical-trial ecosystem, deep regulatory expertise around FDA pathways, and USD 160 billion of planned biomanufacturing investment for 2025. The venture-funding rebound boosts SME pipelines that almost exclusively depend on outsourcing. Nevertheless, proposed US legislation—the BIOSECURE Act—could curb reliance on certain Chinese suppliers, forcing contingency planning in sponsor supply chains.[3]Emma Stoye, “The Unfulfilled Dream of Drug Reshoring,” Chemical & Engineering News, cen.acs.org Canada also expands biologics capacity, leveraging government incentives to attract CDMO projects. While the region remains the nucleus for high-margin, complex outsourcing, cost pressure and geopolitical risk push sponsors to adopt multi-region vendor strategies, subtly re-balancing the life sciences BPO market.

Europe benefits from regulatory harmonization through the upcoming European Health Data Space, which simplifies cross-border clinical data transfer and attracts R&D stages once executed elsewhere. Germany’s Health Data Use Act centralizes datasets for research, giving CROs and data-analytics providers pre-authorized access to rich longitudinal information. Nearshoring to Eastern Europe is gathering pace as sponsors blend geographical proximity with moderate cost advantages. At the same time, ESG imperatives encourage low-carbon production footprints, nudging some CDMO projects back into Western Europe despite higher operating expenditures. Overall, Europe preserves its role as a hub for complex regulatory and late-phase work, adding resilience to the life sciences BPO market.

Asia Pacific posts the fastest growth at an 8.5% CAGR through 2030, driven by India’s ambition to double its CDMO export revenue within five years and by China’s entrenched biomanufacturing infrastructure. Samsung Biologics and WuXi Biologics continue multi-billion-dollar expansions, although geopolitical headwinds create uncertainty around US-bound supply lines. Southeast Asian nations provide back-office pharmacovigilance and data-management hubs, capitalizing on English-speaking talent and favorable wage structures. Currency appreciation and wage inflation are narrowing the pure-cost delta, yet the region remains essential for scale-intensive activities. As sponsors pursue China-plus-one strategies, countries such as Vietnam and Malaysia are securing a larger slice of the life sciences BPO market.

Competitive Landscape

Consolidation is reshaping the sector’s structure. Novo Holdings’ USD 16.5 billion purchase of Catalent erased a major independent player and spurred fears of capacity bottlenecks for fill-finish operations. Scale players such as IQVIA, Labcorp, and Thermo Fisher Scientific leverage integrated platforms—merging laboratory, data science, and manufacturing services—to defend share. Mid-tier specialists differentiate through deep therapeutic focus, nimble project governance, and AI-augmented workflows, positioning for carve-out work as megaprojects concentrate under conglomerates.

Strategic partnerships and risk-sharing contracts are now mainstream. Sponsors routinely structure milestone-dependent fees and outcome bonuses, compelling providers to align incentives and internal quality systems. Technology adoption is another battleground: firms with proprietary AI engines for site selection, protocol generation, or automated submission authoring claim measurable cycle-time advantages that resonate with fast-moving biotech customers. Capacity investments—for example, Samsung Biologics’ multi-train bioreactor campus and Thermo Fisher’s mRNA facility build-outs—signal long-range confidence in biologics demand. These moves, together with selective M&A, reinforce provider positioning and propel the life sciences BPO market forward.

Yet competitive risk remains. Wage inflation in core offshore locations compresses margin, while regional data-sovereignty laws raise compliance costs. Smaller vendors could become M&A targets as they struggle to meet escalating security and privacy requirements. Overall, the market exhibits moderate concentration: the combined top-five revenue share approximates 35%, leaving room for specialist challengers and regional champions. Innovation, execution quality, and regulatory credibility will determine relative gains as the life sciences BPO market grows through 2030.

Life Sciences BPO Industry Leaders

IQVIA

Labcorp (Covance)

Thermo Fisher Scientific (PPD)

Parexel

ICON plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Novo Holdings completed its USD 16.5 billion acquisition of Catalent, the largest life sciences BPO transaction in history, consolidating the CDMO market and triggering capacity concerns among pharmaceutical clients.

- July 2024: Agilent Technologies acquired contract service provider Biovectra for USD 925 million, expanding its biopharma solutions portfolio and adding sterile fill-finish and mRNA manufacturing capabilities to its BPO offerings.

- February 2024: Labcorp Drug Development (Fortrea) established a new clinical trial site network in Eastern Europe, adding 25 investigator sites to enhance patient recruitment capabilities for global studies

Global Life Sciences BPO Market Report Scope

| Contract Research (CRO) |

| Contract Development & Manufacturing (CDMO/CMO) |

| Regulatory & Medical Affairs BPO |

| Pharmacovigilance / Safety BPO |

| Commercial, Sales & Marketing Support |

| Supply-Chain & Logistics BPO |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Medical-Device Companies |

| Academic / Research Institutes |

| Full-Service Outsourcing (FSO) |

| Functional Service Provider (FSP) |

| Tactical / Project-based |

| Hybrid & Captive Models |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Contract Research (CRO) | |

| Contract Development & Manufacturing (CDMO/CMO) | ||

| Regulatory & Medical Affairs BPO | ||

| Pharmacovigilance / Safety BPO | ||

| Commercial, Sales & Marketing Support | ||

| Supply-Chain & Logistics BPO | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Medical-Device Companies | ||

| Academic / Research Institutes | ||

| By Outsourcing Model | Full-Service Outsourcing (FSO) | |

| Functional Service Provider (FSP) | ||

| Tactical / Project-based | ||

| Hybrid & Captive Models | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the life sciences BPO market?

The life sciences BPO market size reached USD 494.5 billion in 2025 and is set to climb to USD 742.8 billion by 2030 at an 8.70% CAGR.

Which service category is growing fastest?

CDMO/CMO services are pacing the field with an 11.3% CAGR through 2030 as biologics and cell-gene therapies demand capital-intensive manufacturing capacity.

Why are biotechnology companies outsourcing more than pharmaceutical firms?

Biotech companies typically operate asset-light models and rely on external expertise to progress clinical programs, resulting in an 8.4% CAGR for their outsourcing spend.

How will new data-privacy laws affect outsourcing contracts?

GDPR updates, the European Health Data Space, and the expected HIPAA 2026 revision will increase compliance complexity, favouring large BPO vendors with advanced security infrastructure.

What impact did the Catalent acquisition have on market dynamics?

Novo Holdings’ USD 16.5 billion Catalent deal removed a major independent CDMO from the market, intensified capacity concerns, and underscored the trend toward large-scale consolidation.

Page last updated on: