Membrane Microfiltration Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

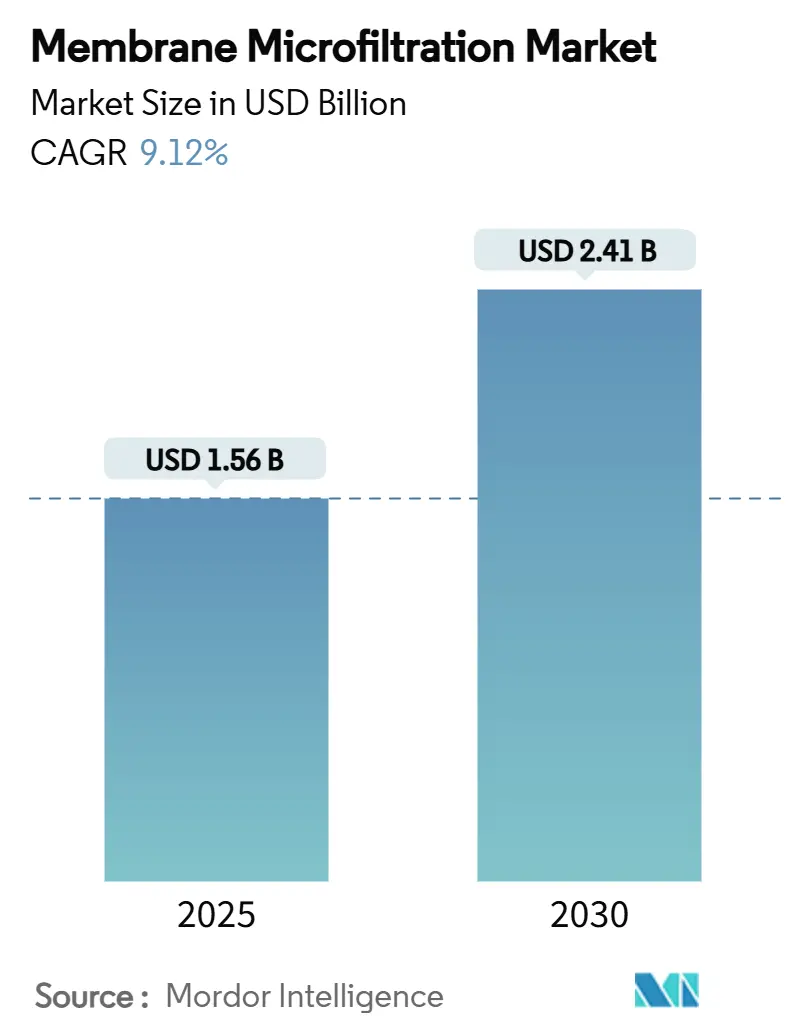

| Market Size (2025) | USD 1.56 Billion |

| Market Size (2030) | USD 2.41 Billion |

| Growth Rate (2025 - 2030) | 9.12% CAGR |

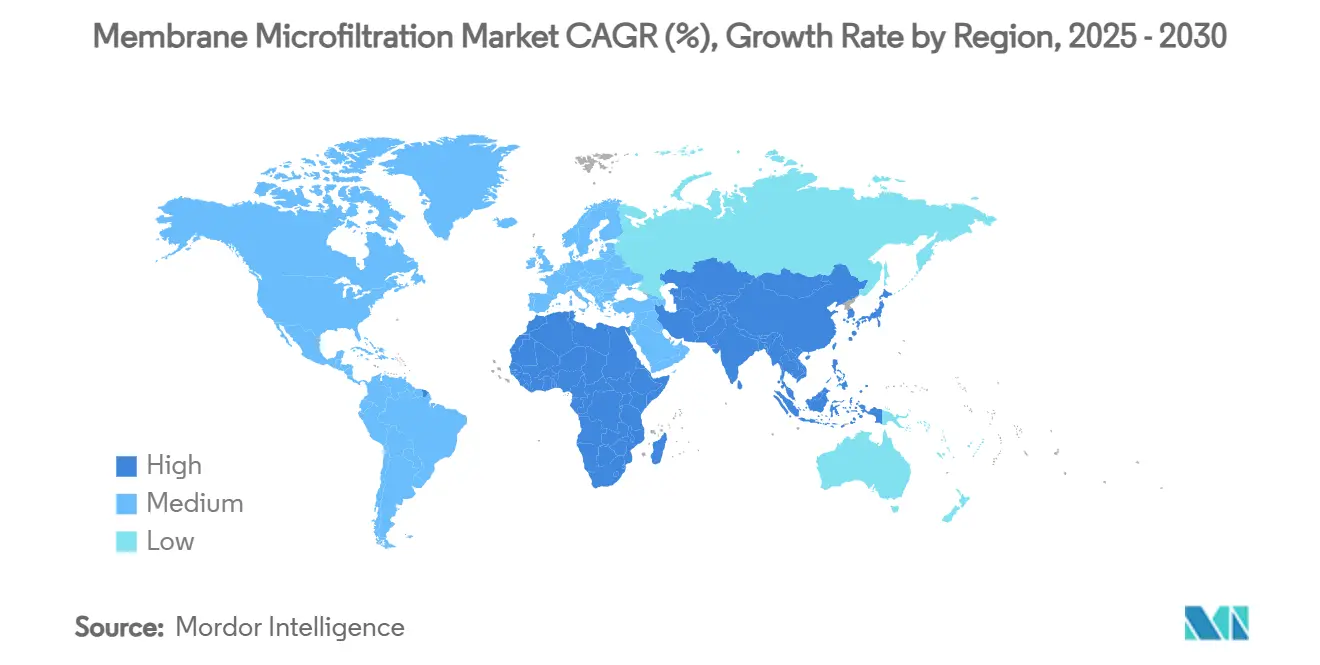

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Membrane Microfiltration Market Analysis by Mordor Intelligence

The membrane microfiltration market size stands at USD 1.56 billion in 2025 and is projected to rise to USD 2.41 billion by 2030, reflecting a CAGR of 9.12%. Rapid infrastructure upgrades, industrial water-reuse mandates, and premium biopharma filtration needs are the pivotal forces behind this momentum. Utilities replace aging sand and media filters with compact microfiltration units to tackle per- and polyfluoroalkyl substances (PFAS) and other emerging contaminants. Industrial operators, facing stricter zero-discharge directives, embed membrane stages in closed-loop systems to meet effluent ceilings for heavy metals and organics.[1]U.S. Environmental Protection Agency, “40 CFR Part 437 — The Centralized Waste Treatment Point-Source Category,” ecfr.gov Biopharmaceutical plants are scaling single-use sterile filters to protect advanced biologics while maintaining high flux and production flexibility. Material science breakthroughs—especially ceramic formulations with high heat and solvent tolerance—shave life-cycle costs despite higher upfront prices.

Key Report Takeaways

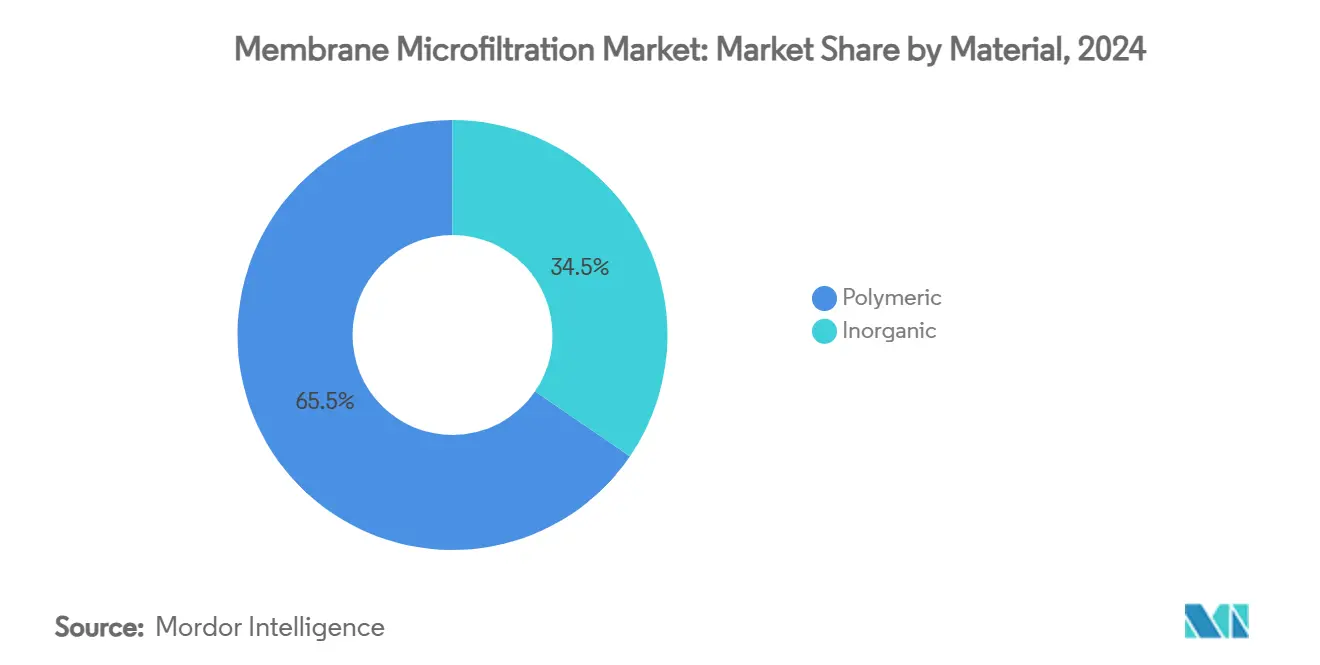

- By material, polymeric modules led with 65.47% of membrane microfiltration market share in 2024, whereas ceramic variants are forecast to expand at a 12.38% CAGR to 2030.

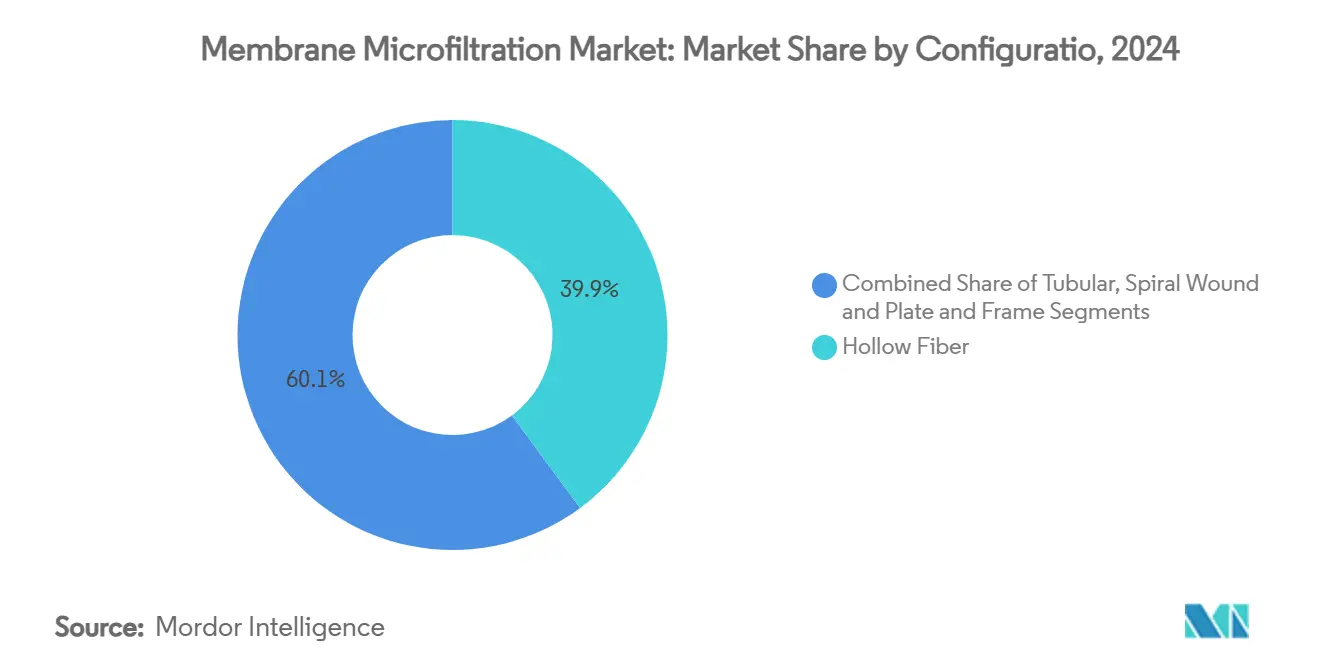

- By configuration, hollow fiber units held 39.87% of the membrane microfiltration market size in 2024 and spiral-wound systems are advancing at a 13.39% CAGR through 2030.

- By application, municipal water infrastructure accounted for 43.56% of revenue in 2024 while biopharmaceutical processing is registering the highest projected CAGR at 11.63% through 2030.

- By geography, North America dominated with 31.23% revenue share in 2024, and Asia-Pacific is poised for the fastest regional CAGR of 11.49% to 2030.

Market Trends and Insights

Drivers Impact Analysis of Membrane Microfiltration Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption Of Membrane-Based Water Purification In Municipal Upgrades | +2.1% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Stringent Global Wastewater Discharge Standards | +1.8% | Global, early adoption in EU & North America | Short term (≤ 2 years) |

| Biopharma Capacity Build-Out Boosting Sterile Filtration Demand | +1.5% | North America, EU, APAC core markets | Medium term (2-4 years) |

| Decentralized, Solar-Powered MF Units For Off-Grid Communities | +0.9% | APAC, MEA, Latin America rural regions | Long term (≥ 4 years) |

| Ceramic MF Membranes Enabling High-Temperature Chemical Processing | +1.2% | Global industrial centers, APAC manufacturing hubs | Medium term (2-4 years) |

| MF Pre-Treatment In Green-Hydrogen Electrolyzer Loops | +0.7% | EU, North America, select APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Membrane-Based Water Purification in Municipal Upgrades

Utilities are retrofitting legacy clarification trains with microfiltration to comply with lower turbidity and pathogenic requirements. Modeling platforms now simulate flux decline and chemical cleaning frequency, trimming engineering lead times and warranty risk. U.S. city councils cite PFAS removal success stories when approving bond issues for plant overhaul. Artificial-intelligence dashboards detect early fouling signatures, letting operators initiate backwash cycles proactively. Plants report up to 35% reductions in coagulant use, extending filter run length and lowering finished-water variability. Positive public-health outcomes reinforce ratepayer acceptance of capital surcharges.

Stringent Global Wastewater Discharge Standards

The revised EU Urban Wastewater Treatment Directive pushes quaternary treatment—including membrane stages—into projects serving towns above 100,000 residents. EPA zero-liquid-discharge rules for centralized waste processors amplify demand for high-rejection pre-filters that shield energy-intensive RO trains.[2] U.S. Environmental Protection Agency, “40 CFR 455.64 — Effluent Limitations Guidelines,” ecfr.gov Canada’s effluent regulation amendments employ risk scoring, nudging mills and refineries to adopt microfiltration for predictable solids removal.[3]Government of Canada, “Regulations Amending the Wastewater Systems Effluent Regulations,” canadagazette.gc.caIndustrial players in metals and chemicals are shifting to membrane-centric loops to safeguard permits, a trend mirrored in published capex budgets. Consultants note that project tender volumes grew 14% in 2024, setting a strong pipeline for integrators.

Biopharma Capacity Build-Out Boosting Sterile Filtration Demand

Blockbuster monoclonal antibody pipelines and next-generation gene therapies require sterile, virus-free process streams. Asahi Kasei’s high-flux Planova FG1 filter reduces required area by 60%, allowing smaller single-use assemblies. CMOs are ordering modular skids featuring interchangeable cassettes to support multi-product facilities. Validation packages now integrate bacterial challenge data and endotoxin retention curves, streamlining regulatory filings. Continuous-manufacturing blueprints embed microfiltration steps upstream of chromatography, cutting hold-up times and lowering contamination risk. Suppliers see margin expansion because biologics makers prize reliability more than price.

Ceramic Membranes Enabling High-Temperature Chemical Processing

Petrochem, pulp, and semiconductor facilities operate at temperatures and pH ranges that quickly degrade PVDF or PES. Alumina-titania composites tolerate 90 °C caustic and chlorine shocks without pore collapse. Ceramic modules last up to 15 years—over triple the lifespan of polymers—offsetting capex premiums. Pilot studies in fluoropolymer plants logged flux recovery rates above 98% after acid cleaning, validating opex benefits. Regulatory scrutiny of PFAS polymers accelerates the shift, and vendors highlight recyclability to bolster ESG scores. Capacity expansions by furnace makers suggest supply chain readiness for double-digit demand growth.

Restraints Impact Analysis of Membrane Microfiltration Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Membrane Fouling & Cleaning Costs | -1.4% | Global, particularly in high-fouling applications | Short term (≤ 2 years) |

| Price Pressure From Alternative UF/NF Technologies | -0.8% | Competitive markets in North America & EU | Medium term (2-4 years) |

| Limited Recyclability Of Polymeric Modules Affecting ESG Scores | -0.6% | EU, North America sustainability-focused markets | Medium term (2-4 years) |

| Shortage Of Skilled Membrane Technicians In Emerging Markets | -0.5% | APAC, MEA, Latin America developing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Membrane Fouling and Cleaning Costs

Surface cake formation remains the top operational headache. Full-scale beverage plants report productivity drops up to 35% before scheduled CIP events. Sodium hypochlorite-alkali sequences recover 90% flux but raise chemical expenses and labor. Nanoparticle-doped coatings are showing promise, with manganese ferrite layers delivering 2.6-fold flux gains in pilot rigs. OEMs embed AI algorithms to forecast fouling curves and shift cleaning from fixed intervals to data-driven triggers, yet adoption is uneven outside Tier 1 utilities.

Price Pressure From Alternative UF/NF Technologies

Ultrafiltration (UF) vendors tout similar removal efficiencies with lower footprint, forcing MF suppliers into value-engineering. In Europe, bundled UF/RO packages underbid MF tenders by 8–12%, especially for brackish water projects. Aggressive low-cost imports have compressed polymeric module margins below 15%. Some integrators pivot to hybrid skid offerings to defend share, but cost headwinds persist as high-pressure membranes gain scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Membrane Microfiltration Market Segment Analysis

By Material:

Ceramic Membranes Gain Traction Despite Cost PremiumIn 2024 polymeric media captured 65.47% of membrane microfiltration market revenue, but ceramic alternatives tapped rising demand for chemical toughness and PFAS-free credentials. Alumina and titania channels resist chlorine shocks up to 10,000 ppm, enabling in-place sterilization cycles that trim downtime. Halloysite-reinforced layers registered 126 L m² h flux at 99.4% particle rejection, widening the process window for semiconductor wastewater polishing. The membrane microfiltration market size for inorganic modules, underpinned by refinery, pulp, and electronics investments that demand high-temperature resilience. Vendors are building reactors that cut sintering temperatures, narrowing the price delta versus PVDF. As PFAS regulations tighten, buyers migrate from polymeric to ceramic designs, accelerating share gains.

Adoption accelerates in Southeast Asia where textile effluent complexity overwhelms standard polymers. European EPCs specify ceramic modules for zero-liquid-discharge loops to hit circular-economy KPIs. Leasing models, bundling maintenance with performance guarantees, lower entry barriers for cash-constrained clients. Producers highlight 95% recyclability rates versus near-zero for fluoropolymer cartridges, a persuasive argument in green-bond funded projects. In turn, polymer players respond with blend modifications and hydrophilic coatings to prolong service life and defend incumbency.

By Configuration:

Spiral-Wound Systems Capture Growth Through Surface-Area OptimizationHollow fiber units retained 39.87% revenue share in 2024 owing to dense packing and low-pressure operation across municipal retrofits. Yet spiral-wound formats are increasing installation speed lines, registering 13.39% CAGR as distillers and beverage firms seek higher recoveries. Re-engineered feed spacers diminish concentration polarization by 18%, boosting clean-water yield per module. Pilot runs in citrus-juice clarification report 10% higher permeate quality versus legacy flat-sheet stacks.

Second-generation spiral designs integrate pressure sensors in permeate collectors, enabling early blockage detection and condition-based maintenance. Fabricators adopt continuous casting to streamline layer lamination, lowering module price by 6% year on year. Tubular and plate-and-frame geometries preserve niche roles in viscous feed applications, particularly cocoa and gelatin where quick disassembly is vital for hygiene audits. Hybrid skids mixing hollow fiber pre-filters with spiral polishers gain traction in breweries pursuing 99.99% yeast removal without pasteurization.

By Application:

Biopharmaceutical Segment Drives Premium Technology AdoptionMunicipal water and wastewater projects held 43.56% of market turnover in 2024. Utilities employ microfiltration as both primary clarification and RO pretreatment to maximize reuse volumes. Upgrading to membranes delivers log-removal values often exceeding 6 for Cryptosporidium, eclipsing rapid-sand benchmarks and fulfilling tightened guidelines in North America. Facilities report chlorine dose cuts of 25%, bolstering residual taste profiles. The membrane microfiltration market size for biopharma is forecast to rise at 11.63% CAGR, reflecting pipeline expansions and pandemic-preparedness stockpiles.

Biologic drug makers prize single-use, gamma-sterilized modules that reduce cross-contamination risk. Virus-removal cassettes now incorporate QR codes storing lot-specific retention curves, streamlining QA audits. Food and beverage processors deploy membranes for cider haze reduction and dairy native whey protein capture, unlocking premium SKUs. Industrial coolant loops utilize microfiltration to extend fluid change-out intervals, saving on chemical costs and waste disposal. Emerging sectors—microelectronics, lithium-brine pretreatment, and pulp de-ink washing—are beginning to specify MF stages to address fine-particle burdens that undermine downstream processes.

Geography Analysis

North America Membrane Microfiltration Market

North America’s rigorously enforced discharge ceiling stimulates premium membrane penetration. U.S. plant operators leverage performance-based contracts, tying vendor compensation to permeate quality benchmarks. Energy-efficient hollow fiber skids outperform gravity sand filters on lifecycle economics once chemical and sludge disposal costs are tallied. Canada, integrating risk-based licensing, opts for membranes to ensure compliance margin across seasonal feed swings. Supply-chain robustness and trained labor pools shorten commissioning periods relative to other regions.

APAC Membrane Microfiltration Market

Asia-Pacific’s 11.49% CAGR stems from industrial growth matched with stricter resource-management statutes. Mega-plants in petrochemicals shift to internal water loops filtered via microfiltration to slice freshwater draws. Provincial incentives in China’s Yangtze and Pearl River basins subsidize PFAS remediation, a boon for ceramic unit suppliers. Indian smart-city schemes mix potable and reclaimed water lines, with MF modules serving as the microbiological safeguard. Regional OEMs adopt high-throughput sintering to crank out ceramic elements at cost points competitive with PVDF.

Europe Membrane Microfiltration Market

Europe’s steady demand is underpinned by ecological stewardship objectives. The circular-economy agenda pushes wastewater processors to recover phosphorus and nitrate, and membranes supply the fine separation step. Operators experiment with energy-positive plants where biogas offsets compression loads. Eligibility for EU innovation funds hinges on PFAS-free construction, sparking rapid R&D in fluorine-free polymers. Eastern European municipalities, accessing cohesion funds, increasingly leapfrog sand filtration stages altogether, specifying membrane trains in first-generation plants.

Competitive Landscape

Market structure is moderately fragmented. Top ten players account for an estimated 46% of shipments, leaving room for regional specialists. Thermo Fisher’s USD 4.1 billion purchase of Solventum’s purification arm widens single-use offerings and tightens supply integration. Danaher merged Cytiva and Pall into a USD 7.5 billion entity, combining depth and breadth in life-science filtration. Graphene-membrane start-ups like NematiQ target industrial niches with ultra-high flux at half the differential pressure of PVDF.

Vertical integration accelerates: module makers acquire skid fabricators to capture aftermarket chemicals and services. Patent filings concentrate on anti-fouling chemistry and intelligent monitoring. Partnerships between ceramic kiln operators and filter assemblers aim to secure raw-material continuity. Fabricators located near semiconductor hubs in Taiwan and South Korea ramp lines dedicated to ultrapure water. Meanwhile, polymeric giants diversify into recyclable blends to mitigate PFAS-phase-out risk. The intensity of R&D spend, measured at 6–8% of revenue for the top three players, remains a barrier for late entrants.

Membrane Microfiltration Industry Leaders

Danaher

Merck KGaA

Sartorius AG

SUEZ Water Technologies & Solutions

Alfa Laval

- *Disclaimer: Major Players sorted in no particular order

Membrane Microfiltration Market Companies Covered in this Report

- Danaher

- Merck

- Sartorius

- Koch Separation Solutions

- Pentair

- SUEZ Water Technologies & Solutions

- Alfa Laval

- GEA Group

- Donaldson Company

- Parker Hannifin

- Porvair Filtration

- MANN+HUMMEL (Microdyn-Nadir)

- TAMI Industries

- Novasep

- Graver Technologies

- SPX Flow

- Kubota Corporation

- Toray

- Lenntech

Recent Industry Developments in Membrane Microfiltration Market

- February 2025: Thermo Fisher Scientific agreed to acquire Solventum’s Purification & Filtration business for USD 4.1 billion, adding depth in bioproduction filtration.

- April 2024: GVS Japan expanded its hollow fiber tangential-flow filtration range, supporting scale-up from lab to industrial volumes.

Global Membrane Microfiltration Market Report Scope

Segmentation Overview

| Polymeric | PVDF |

| PES | |

| PP | |

| Others (PAN, PTFE) | |

| Inorganic | Ceramic (Al₂O₃, TiO₂) |

| Metallic & Others |

| Hollow Fiber |

| Tubular |

| Spiral Wound |

| Plate & Frame |

| Water & Wastewater Treatment |

| Food & Beverage Processing |

| Biopharmaceutical & Life-Science Manufacturing |

| Industrial Fluids & Coolants |

| Others (Microelectronics, Pulp & Paper) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Polymeric | PVDF |

| PES | ||

| PP | ||

| Others (PAN, PTFE) | ||

| Inorganic | Ceramic (Al₂O₃, TiO₂) | |

| Metallic & Others | ||

| By Configuration | Hollow Fiber | |

| Tubular | ||

| Spiral Wound | ||

| Plate & Frame | ||

| By Application | Water & Wastewater Treatment | |

| Food & Beverage Processing | ||

| Biopharmaceutical & Life-Science Manufacturing | ||

| Industrial Fluids & Coolants | ||

| Others (Microelectronics, Pulp & Paper) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current size of the membrane microfiltration market?

The market is valued at USD 1.56 billion in 2025 and is projected to reach USD 2.41 billion by 2030.

2. Which segment is growing fastest in the membrane microfiltration market?

Biopharmaceutical manufacturing posts the quickest trajectory at 11.63% CAGR, fueled by sterile filtration demand for biologics.

3. Why are ceramic membranes gaining popularity?

They tolerate high temperature and aggressive chemicals, last longer than polymers, and avoid PFAS concerns, which offsets their higher upfront cost.

4. Which region leads the membrane microfiltration market?

North America holds the largest share at 31.23%, thanks to strict discharge rules and infrastructure funding.

5. What are the main restraints hindering market growth?

Fouling-related cleaning costs, price competition from ultrafiltration, module recyclability challenges, and technician shortages in emerging regions all weigh on adoption.

Page last updated on: