Bioprocess Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

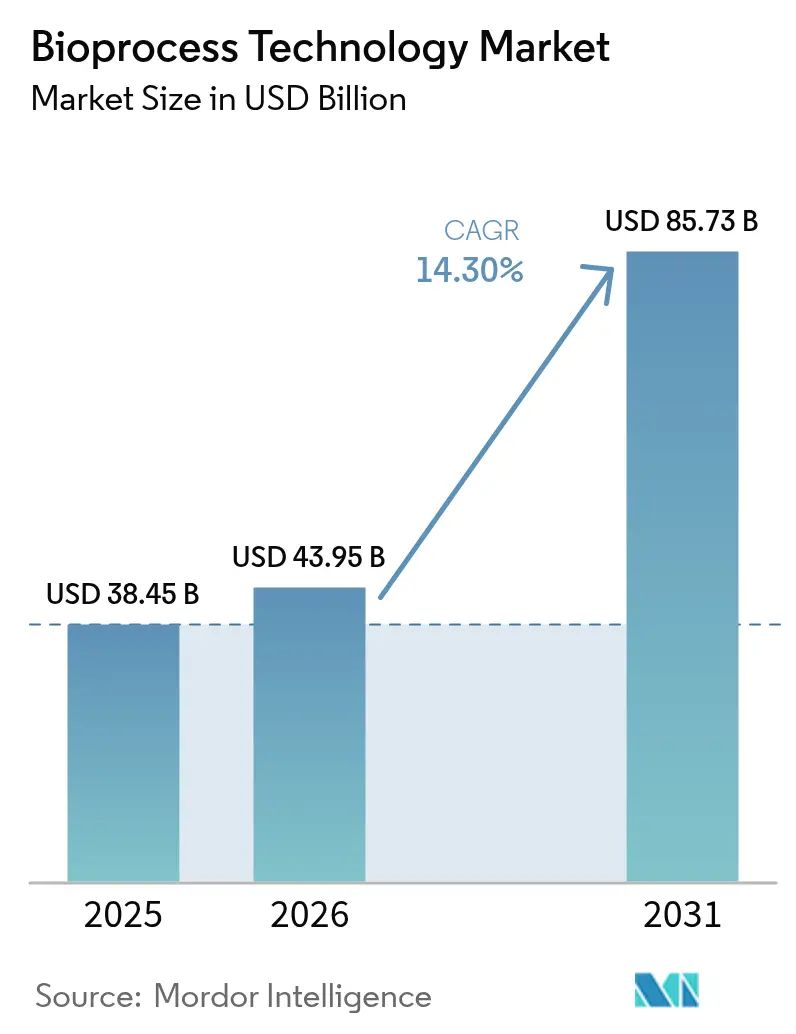

| Market Size (2026) | USD 43.95 Billion |

| Market Size (2031) | USD 85.73 Billion |

| Growth Rate (2026 - 2031) | 14.30% CAGR |

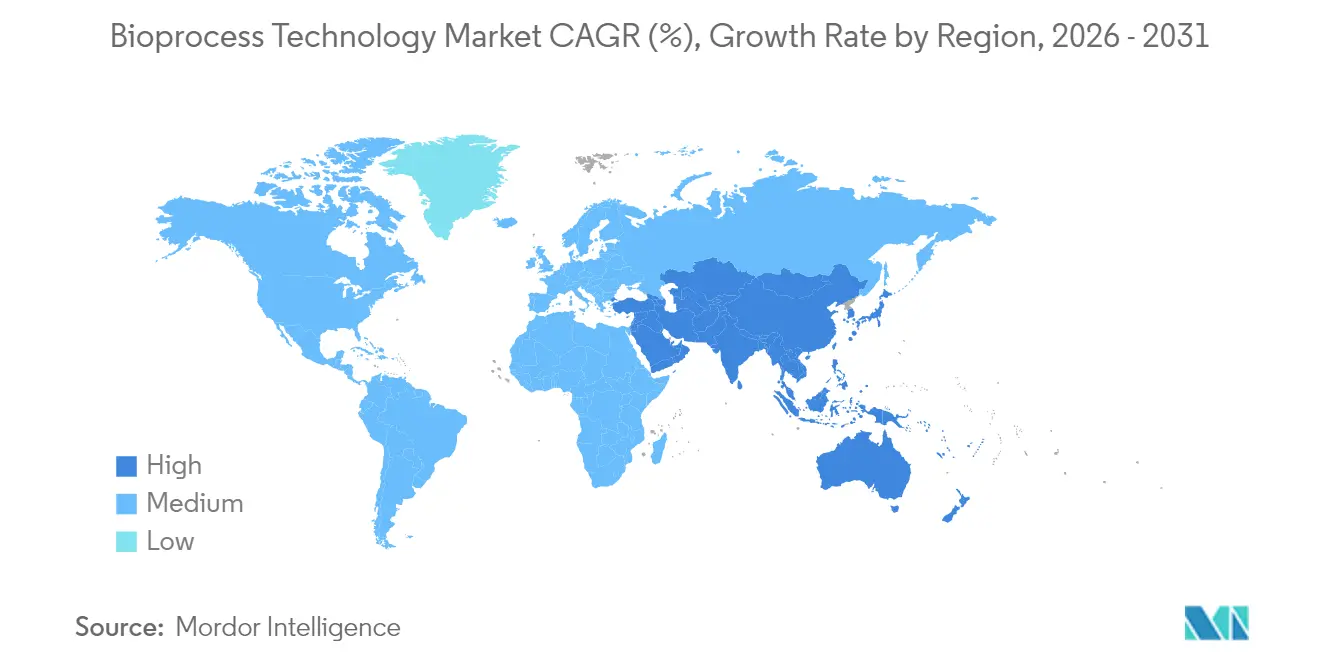

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

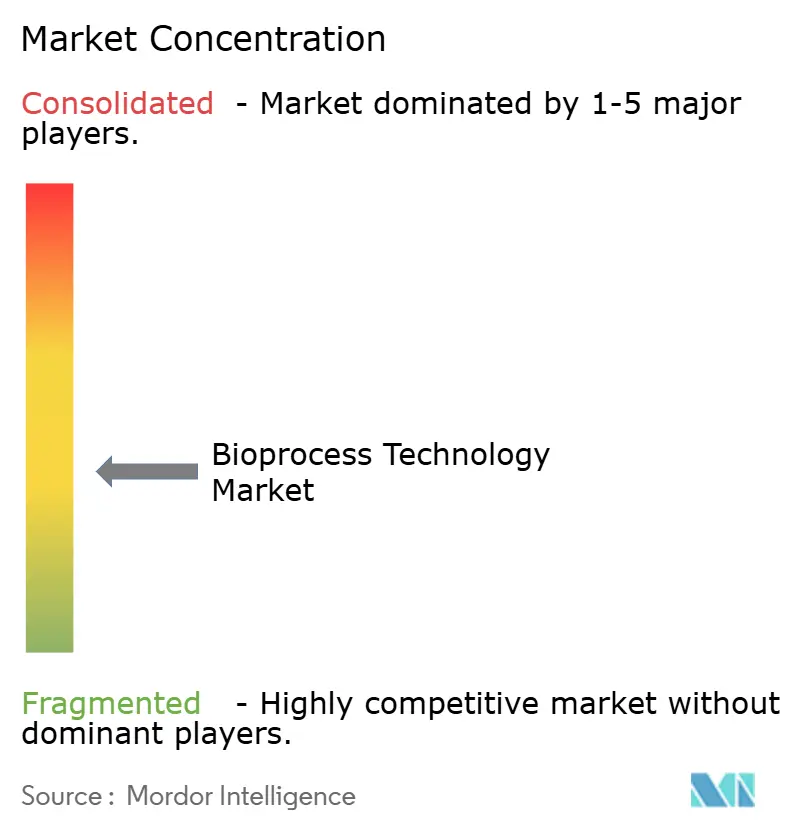

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioprocess Technology Market Analysis by Mordor Intelligence

Bioprocess Technology market size in 2026 is estimated at USD 43.95 billion, growing from 2025 value of USD 38.45 billion with 2031 projections showing USD 85.73 billion, growing at 14.3% CAGR over 2026-2031.

Capacity additions at contract development and manufacturing organizations (CDMOs) are accelerating as the share of global biologics production outsourced is set to climb by 2030, reshaping competitive dynamics and creating sustained demand for upstream and downstream solutions. Rising pipelines in cell and gene therapy (CGT) have intensified requirements for advanced manufacturing platforms, with growing demand for CGT manufacturing services. The dominance of single-use consumables, broader adoption of perfusion culture, and regulators’ growing comfort with continuous manufacturing are lifting productivity benchmarks across the bioprocess technology market. Regional momentum is polarized: North America retains infrastructure leadership, yet Asia-Pacific is expanding fastest on the back of Chinese and South Korean capacity investments.

Key Report Takeaways

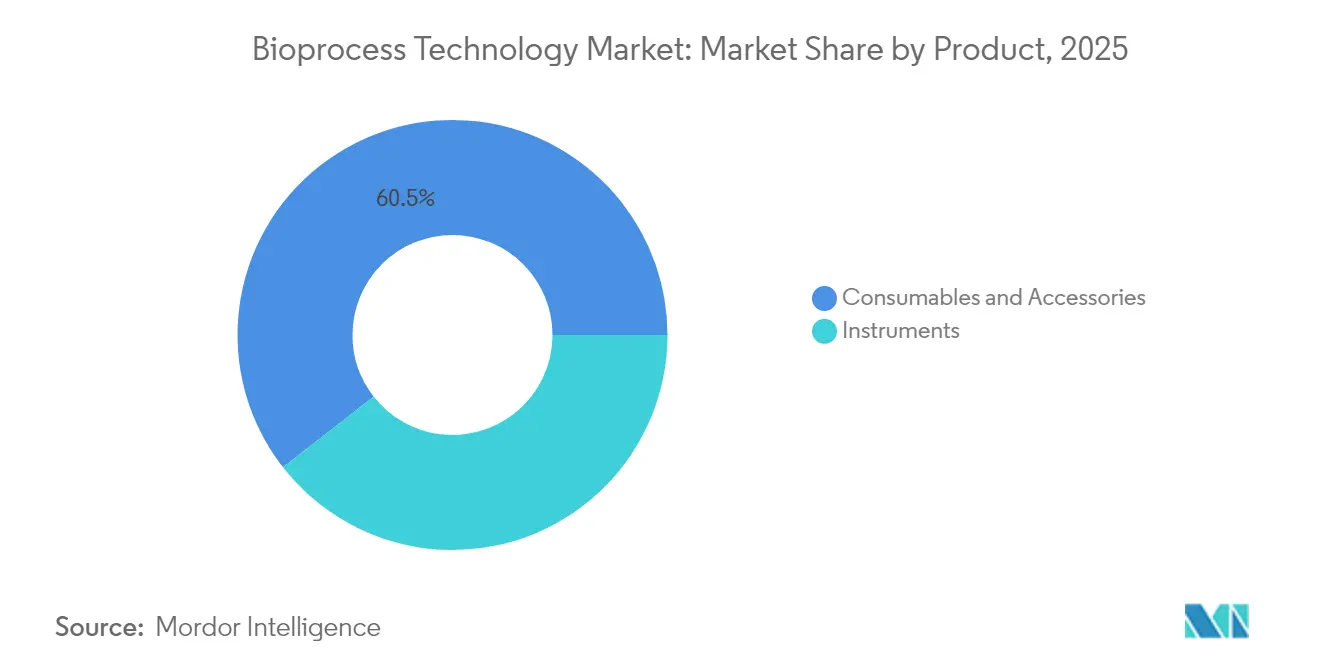

- By product, consumables and accessories led with 60.55% of the bioprocess technology market share in 2025 and it is projected to expand at a 16.42% CAGR to 2031.

- By process type, downstream processing held 51.20% share of the bioprocess technology market size in 2025; while upstream processing record the highest projected CAGR at 14.55% through 2031.

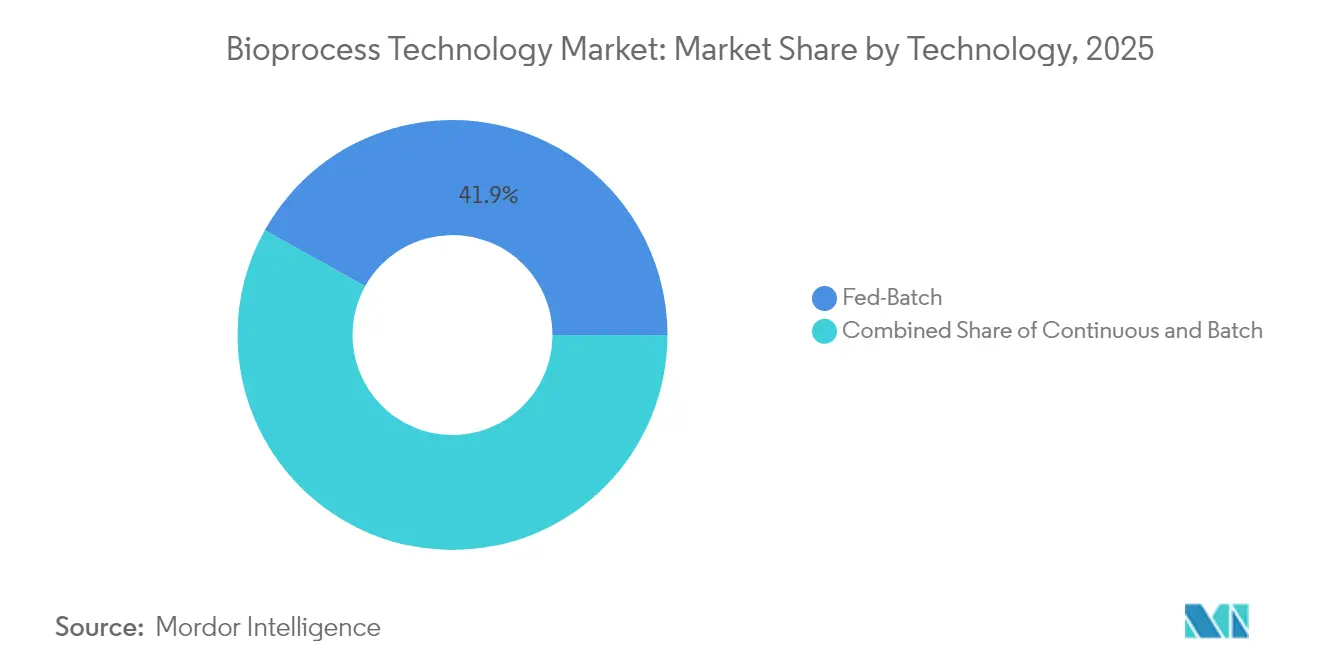

- By technology, fed-batch commanded 41.90% of the bioprocess technology market size in 2025, while continuous platforms recorded the highest CAGR at 14.10%.

- By application, monoclonal antibodies contributed 36.20% revenue in 2025; cell & gene therapy products registered the fastest 15.72% CAGR to 2031.

- By end user, biopharmaceutical companies accounted for 61.05% of demand in 2025, whereas CMOs expanded at a 14.75% CAGR.

- By geography, North America secured 38.90% share of the bioprocess technology market size in 2025; Asia-Pacific is on track for an 17.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bioprocess Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion in the Biopharmaceutical Industry | +2.8% | North America, EU lead | Medium term (2-4 years) |

| Growing Contract Development & Manufacturing Outsourcing | +2.1% | Global with APAC spill-over | Short term (≤ 2 years) |

| Surge in Cell & Gene Therapy Pipelines | +3.2% | North America, EU core, APAC rising | Long term (≥ 4 years) |

| Rising Demand for Single-Use Systems | +1.9% | Global | Short term (≤ 2 years) |

| Advent of Continuous & Hybrid Platforms | +1.7% | North America, EU focus | Medium term (2-4 years) |

| AI-Driven Bioprocess Optimization | +1.4% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion in the Biopharmaceutical Industry

Biopharmaceutical sales climbed lifting biologics’ contribution within overall drug spending from 41% in 2024 toward 45% by 2028. FDA projections of up to 20 CGT approvals annually from 2025 underline a new wave of complex modalities that require high-precision, GMP-compliant manufacturing suites. Samsung Biologics’ digital-twin deployment demonstrates how advanced modeling can compress validation timelines while maintaining data integrity.[1]Bioprocess International, “Digital Twins Transform Large-Scale Biologics Facilities,” bioprocessintl.com Capital-intensive upgrades are therefore migrating toward flexible, single-use configurations that accommodate multiple modalities without compromising regulatory expectations.

Growing Contract Development & Manufacturing Outsourcing

The biologics CDMO segment is on course, fueled by large pharma’s strategic divestment of non-core manufacturing assets. Samsung Biologics’ USD 1.4 billion Plant 5 expansion and Lonza’s USD 1.2 billion acquisition of Roche’s Vacaville site (330,000 L) illustrate an arms race for large-scale capacity.[2]CHEManager, “Samsung Biologics Breaks Ground on Plant 5,” chemanager.com Potential passage of the BIOSECURE Act could redirect outsourced volumes from Chinese providers to Western and Korean suppliers; 49% of executives surveyed in 2024 expected stronger contract services growth during 2025. The shift cements the bioprocess technology market as a pivotal enabler of global capacity realignment.

Surge in Cell & Gene Therapy Pipelines

Lonza’s commercial supply pact for CASGEVY, the first CRISPR-edited therapy, exemplifies demand for bespoke viral-vector suites and closed-system cell culture. Standardization remains elusive, yet automation and modular facilities are steadily reducing cost-of-goods. Gene therapy approvals like ELEVIDYS and ROCTAVIAN pushed the market, while the FDA's streamlined approval pathways encourage continued investment. Manufacturing challenges persist, with standardization gaps and workforce shortages creating bottlenecks, yet automation advances and platform process adoption are addressing scalability concerns. The shift from autologous to allogeneic therapies promises enhanced cost-effectiveness and treatment accessibility.

Rising Demand for Single-Use Bioprocessing Systems

Disposable technologies now dominate commercial biologics production workflows, offering reduced contamination risk and faster changeover versus stainless-steel installations. Thermo Fisher’s 5 L DynaDrive bioreactor boosts productivity by 27% while providing linear scalability up to 5,000 L. WuXi Biologics completed its first 5,000 L PPQ run in Hangzhou, cutting protein cost by 70% and raising yield 20%. Legacy players like GSK invested USD 120 million in Pennsylvania to deploy 2,000 L single-use reactors for complex biologics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Integrated Systems | -1.8% | Global, emerging markets sensitive | Medium term (2-4 years) |

| Stringent cGMP & Validation Requirements | -1.2% | Global, regional variability | Long term (≥ 4 years) |

| Chronic Skilled-Labor Shortages | -2.1% | Developed markets acute | Short term (≤ 2 years) |

| Upstream-Downstream Scale Mismatch | -0.9% | Process-specific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Integrated Systems

Up-front investments for state-of-the-art facilities can exceed USD 500 million, exemplified by Lonza’s planned Vacaville upgrades that target next-gen mammalian platforms. Inflationary pressures have lifted equipment and clean-room construction costs by double-digit percentages since 2023, forcing smaller biotech firms to lean on CDMOs for access to modern capacity.[3]Pharma Manufacturing, “Inflation’s Impact on Facility Projects,” pharmamanufacturing.com Continuous-manufacturing conversions are particularly capital heavy because parallel batch suites must stay online during validation, extending payback horizons. As a result, technology adoption cycles often hinge on demonstrable ROI and regulatory clarity, delaying penetration in cash-constrained geographies.

Chronic Skilled-Labor Shortages

Eighty percent of biomanufacturing sites reported hiring difficulties in 2024, and Cytiva’s resilience index dipped from 6.27 to 5.60 between 2021 and 2023, reflecting a shrinking specialist pool. Automation proficiency appears in 69% of advertised roles, yet academic curricula seldom provide hands-on exposure to GMP digital systems. The National Institute for Innovation in Manufacturing Biopharmaceuticals found that new hires require up to nine months of supplementary training, adding USD 100,000 per worker in opportunity costs. Employers are reducing degree requirements and introducing in-house academies, but retention remains problematic as industry demand outpaces supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Drive Revenue and Innovation

Consumables and accessories accounted for 60.55% of the bioprocess technology market share in 2025 and are forecast to advance at a 16.42% CAGR through 2031. This growth cements single-use bags, sterile connectors, and custom media as recurring revenue pillars within the bioprocess technology market. Culture media optimized for CGT has underscored value potential, with growing demand for gene-therapy media.

Instrument demand is comparatively steadier, underpinned by innovations such as the 5 L DynaDrive bioreactor and Sartorius’ BIOSTAT RM TX platform for automated cell expansion. Process analyzers are benefiting from heightened PAT adoption as facilities transition toward continuous workflows. The consumables boom embodies the larger structural shift away from stainless-steel dependencies, enabling faster turnarounds and lighter capital footprints across the bioprocess technology market.

By Process Type: Downstream Dominance with Upstream Acceleration

Downstream operations captured 51.20% of bioprocess technology market size in 2025, led by chromatography, filtration, and viral clearance solutions. Chromatography is evolving toward multi-column continuous formats that reclaim resin capacity and buffer efficiency. Upstream, perfusion culture adoption is propelling a 14.55% CAGR, as high cell-density systems cut bioreactor volume requirements while sustaining volumetric productivity.

Planova FG1’s seven-fold performance jump underscores the ongoing innovation race in virus filtration. Yet perfusion systems demonstrated at 2,000 L by Samsung Biologics embody upstream’s acceleration by offering steady-state cultures that pair seamlessly with continuous downstream platforms. These dynamics are tightening integration between unit operations, improving overall facility throughput across the bioprocess technology market.

By Technology: Fed-Batch Leadership with Continuous Processing Emergence

Fed-batch retained 41.90% share of the bioprocess technology market size in 2025 through its regulatory familiarity and extensive installed base. However, continuous setups are expanding at 14.10% CAGR as manufacturers chase smaller footprints and cost-of-goods gains.

ICH Q13 and FDA guidance have lowered adoption barriers, and multi-column chromatography is alleviating downstream bottlenecks in early adopters’ pipelines. Perfusion technologies serve as a pragmatic bridge, delivering continuous cell culture outputs while harvesting in batches to ease regulatory submissions. As more sponsors seek speed-to-clinic, continuous lines are expected to seize a larger slice of future capital budgets, pivoting the bioprocess technology market toward fully integrated, end-to-end continuous architectures.

By Application: Monoclonal Antibodies Lead with CGT Acceleration

Monoclonal antibodies contributed 36.20% of 2025 revenues, driven by expanding oncology and autoimmune portfolios and a steady trickle of biosimilar launches. CGT pipelines, however, are charting the steepest trajectory at a 15.72% CAGR through 2031, buoyed by the FDA’s expectation of approving up to 20 such products each year from 2025.

Lonza’s CASGEVY supply agreement illustrates escalating demand for CRISPR-enabled manufacturing know-how. Recombinant proteins and vaccines preserve diversified demand streams, yet their growth rates trail CGT’s explosive rise as regulatory pathways mature. Collectively, these trends underline the imperative for flexible platforms that can switch between high-titer monoclonal antibody runs and small-volume autologous CGT batches within the same facility footprint.

By End User: Biopharmaceutical Companies Dominate with CMO Growth

Biopharmaceutical sponsors controlled 61.05% of spending in 2025, leaning on internal networks for core franchises. Nonetheless, CMOs are expanding at a 14.75% CAGR as outsourced volumes climb, specifically for complex modalities requiring bespoke suites. Lonza’s integration of Roche’s Vacaville site now offers 330,000 L of capacity, signaling that big-ticket acquisitions remain a primary route to scale.

Academic institutes and government labs supply early-stage discovery work, often partnering with CDMOs for scale-up. The BIOSECURE Act could further pivot outsourcing to Western and Korean vendors, intensifying investment into greenfield builds and accelerating technology refresh cycles across the bioprocess technology market.

Geography Analysis

North America’s 38.90% market leadership is anchored by FDA regulatory depth and an ecosystem of established innovators. GSK’s USD 120 million single-use plant in Pennsylvania and Thermo Fisher’s pending Solventum deal reinforce domestic capacity commitments. Canada’s and Mexico’s cross-border supply chains complement United States strengths, leveraging USMCA provisions for frictionless component trade.

Europe maintains competitive parity through cohesive regulatory frameworks such as the EMA’s revised Annex 1 and upcoming ATMP guidelines, which advocate risk-based sterility assurance. Germany, the United Kingdom, and France provide dense biotech clusters, while Poland and the Czech Republic are capturing spill-over investments through favorable cost structures and EU funding.

Asia-Pacific is the growth pacesetter with an 17.65% CAGR, driven by China’s and South Korea’s extensive greenfield builds. WuXi Biologics’ 15,000 L single-use lines delivered 70% cost savings compared with stainless-steel incumbents. Cytiva’s new 6,100 m² filter plant in Incheon and Samsung Biologics’ digital-twin capacity expansion underscore South Korea’s vaccine hub ambitions. India is pivoting toward global GMP certification but faces infrastructure bottlenecks, prompting domestic firms to invest overseas rather than upgrade local sites. The Middle East, Africa, and South America remain emergent, with Saudi Arabia and Brazil leading nascent biomanufacturing initiatives.

Competitive Landscape

Sartorius, Thermo Fisher Scientific, and Danaher command a wide footprint that spans media, bioreactors, filtration, and analytics. Thermo Fisher’s USD 4.1 billion acquisition of Solventum’s purification business projected to contribute USD 1 billion in annual revenue—augments downstream depth while targeting USD 125 million in synergies within five years. Danaher’s consolidation of Cytiva and Pall yields a USD 7.5 billion bioprocess unit capable of one-stop solutions from cell line development to final fill-finish.

Sartorius continues to bulk up on consumables via its EUR 50 million purchase of Xell AG, solidifying its media and feed portfolio. White-space disruptors are carving niches in precision fermentation, automated CGT culture, and modular micro-factories that promise faster deployment. Digital transformation is now a decisive differentiator: Samsung Biologics’ CFD-based digital twin and Amgen’s data-driven run-rate optimization are tangible examples of operational superiority. Sustainable materials and closed-loop recycling schemes for single-use plastics are emerging as another battleground as regulators and clients scrutinize environmental footprints.

Bioprocess Technology Industry Leaders

Danaher Corporation

Sartorius AG

Bio-Rad Laboratories Inc.

Agilent Technologies Inc.

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thermo Fisher Scientific announced the USD 4.1 billion acquisition of Solventum's Purification & Filtration business, expected to generate approximately USD 1 billion in annual revenue and create significant value through enhanced biologics development and manufacturing capabilities, with the transaction anticipated to close by end of 2025.

- October 2024: Lonza completed the USD 1.2 billion acquisition of Roche's Vacaville biologics manufacturing facility, one of the world's largest with 330,000L bioreactor capacity, integrating 750 employees and planning CHF 500 million in facility upgrades for next-generation mammalian biologics therapies.

- October 2024: Lonza extended its collaboration with a major pharmaceutical partner for integrated commercial supply of antibody-drug conjugates, including construction of a new bioconjugation suite in Visp, Switzerland, operational by 2027 and creating approximately 100 jobs.

- September 2024: Lonza and Vertex signed a long-term commercial supply agreement for CASGEVY (exagamglogene autotemcel), the first CRISPR/Cas9 gene-edited cell therapy, with manufacturing at FDA, EMA, and MHRA-approved facilities.

Global Bioprocess Technology Market Report Scope

As per the scope of the report, bio-process is a specific process that uses complete living cells or their components to obtain desired products.

The bio-process technology market is segmented by product (instruments (bioprocess analyzers, osmometers, bioreactors, incubators, and other instruments), consumables, and accessories (culture media, reagents, and other consumables and accessories), application (recombinant proteins, monoclonal antibodies, antibiotics, and other applications), end-user (biopharmaceutical companies, contract manufacturing organizations, academic research institutes, and other end-users) and geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Instruments | Bioprocess Analyzers |

| Osmometers | |

| Bioreactors | |

| Incubators | |

| Other Instruments | |

| Consumables & Accessories | Culture Media |

| Reagents | |

| Other Consumables & Accessories |

| Upstream Processing |

| Downstream Processing |

| Batch |

| Fed-Batch |

| Continuous |

| Recombinant Proteins |

| Monoclonal Antibodies |

| Cell & Gene Therapy Products |

| Antibiotics |

| Other Applications |

| Biopharmaceutical Companies |

| Contract Manufacturing Organizations |

| Academic & Research Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Instruments | Bioprocess Analyzers |

| Osmometers | ||

| Bioreactors | ||

| Incubators | ||

| Other Instruments | ||

| Consumables & Accessories | Culture Media | |

| Reagents | ||

| Other Consumables & Accessories | ||

| By Process Type | Upstream Processing | |

| Downstream Processing | ||

| By Technology | Batch | |

| Fed-Batch | ||

| Continuous | ||

| By Application | Recombinant Proteins | |

| Monoclonal Antibodies | ||

| Cell & Gene Therapy Products | ||

| Antibiotics | ||

| Other Applications | ||

| By End User | Biopharmaceutical Companies | |

| Contract Manufacturing Organizations | ||

| Academic & Research Institutes | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the bioprocess technology market by 2031?

Forecasts place the bioprocess technology market at USD 85.73 billion by 2031, reflecting a 14.3% CAGR from 2026.

Which product category generates the highest revenue?

Consumables and accessories dominate with 60.55% revenue share in 2025 and continue to expand fastest on single-use demand.

How fast is the cell and gene therapy segment growing?

CGT applications are advancing at a 15.72% CAGR through 2031, driven by a pipeline of more than 1,200 active clinical studies.

Which region is exhibiting the fastest growth?

Asia-Pacific leads with an 17.65% CAGR through 2031, buoyed by Chinese and South Korean capacity additions.

What technology trend is reshaping future facilities?

Continuous manufacturing, underpinned by ICH Q13 guidance, is gaining momentum because it lowers cost-of-goods and boosts supply resilience.

Page last updated on: