Life Science Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

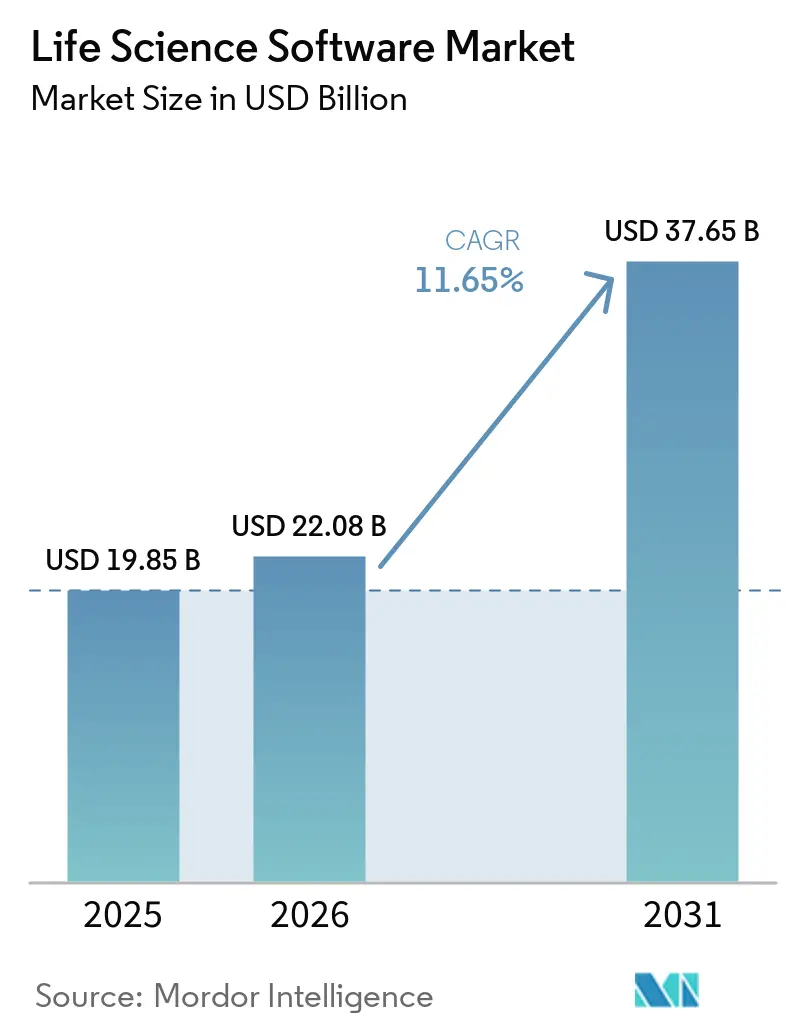

| Market Size (2026) | USD 22.08 Billion |

| Market Size (2031) | USD 37.65 Billion |

| Growth Rate (2026 - 2031) | 11.65% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Life Science Software Market Analysis by Mordor Intelligence

The Life Science Software Market size is expected to grow from USD 19.85 billion in 2025 to USD 22.08 billion in 2026 and is forecast to reach USD 37.65 billion by 2031 at 11.65% CAGR over 2026-2031.

The life science software market is growing as regulated companies demand improved data traceability across product development, manufacturing, quality, and submission workflows. The market is also benefiting from the adoption of AI-driven scientific processes, where laboratories and clinical teams require systems to manage larger data volumes with minimal manual effort. Real-time interoperability is gaining importance as sponsors, CROs, and CDMOs increasingly rely on shared systems and connected data flows to prevent delays and rework. Software spending in this market has become a strategic board-level decision, driven by validated, cloud-ready platforms that accelerate submission timelines and simplify change control. The market is shifting toward platforms that are not only functional but also robust enough to ensure compliance throughout their lifecycle.

Key Report Takeaways

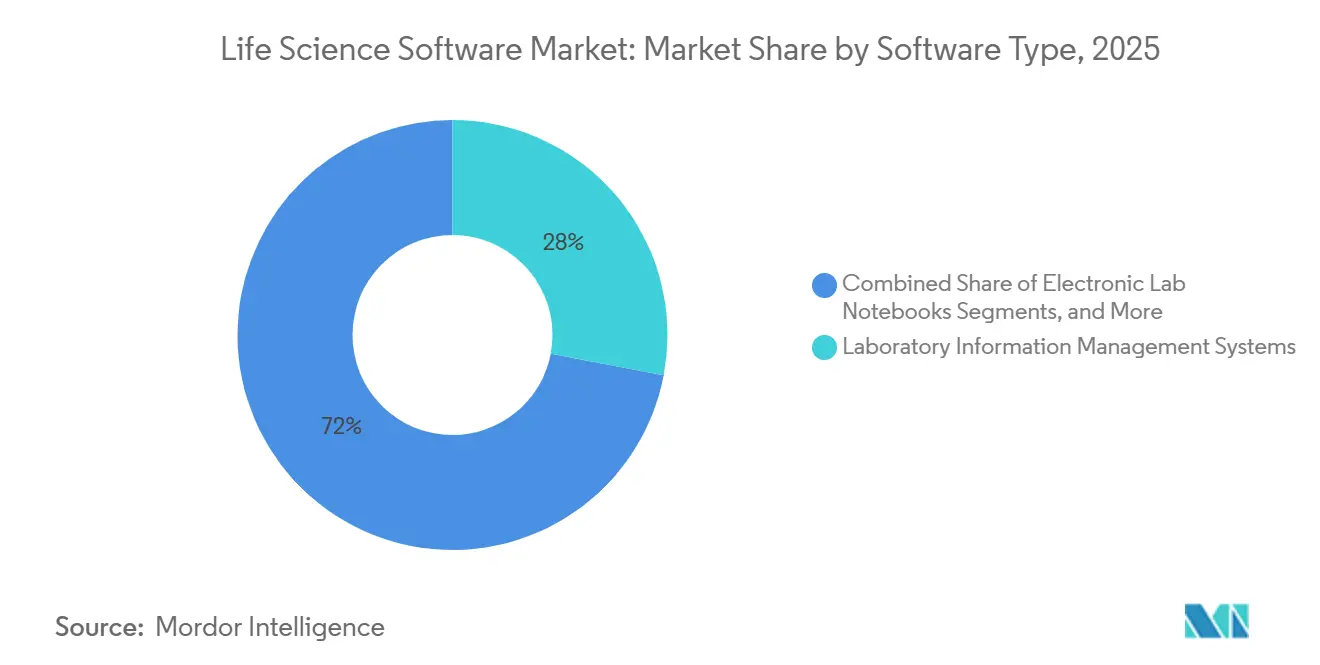

- By software type, laboratory information management systems led with 28.00% share in 2025, while clinical trial management systems are projected to grow at a 12.45% CAGR through 2031.

- By deployment, cloud represented 51.44% of the life science software market size in 2025, and cloud is expected to be the fastest-growing deployment model at a 12.77% CAGR through 2031.

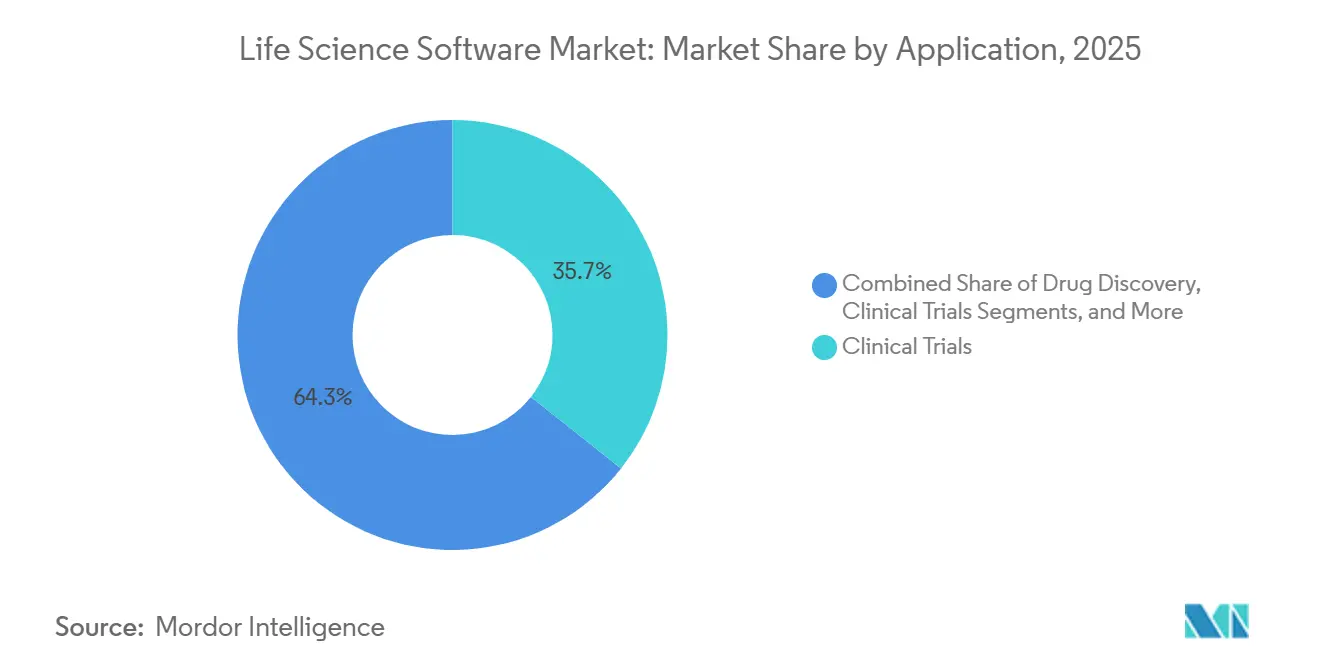

- By application, clinical trials accounted for 35.65% share of the life science software market size in 2025, while research and development is forecasted to expand at a 13.23% CAGR through 2031.

- By end user, biotechnology companies held 42.03% share in 2025, while biotechnology companies were expected to record the highest projected CAGR at 13.35% through 2031.

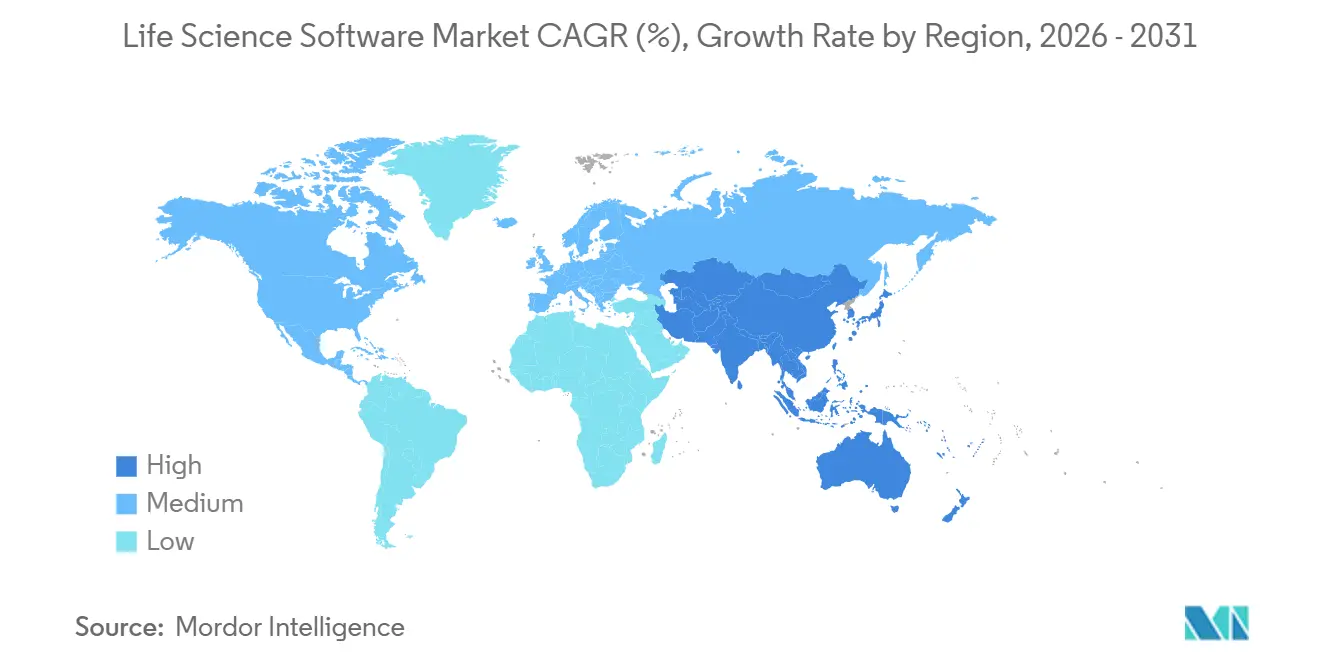

- By geography, North America held 38.99% of the life science software market share in 2025, while Asia-Pacific is forecasted to grow at a 12.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Life Science Software Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for regulatory-ready data traceability across the product lifecycle | +2.8% | Global | Short term (≤ 2 years) |

| Expansion of cloud-native and interoperable life science data architectures | +2.4% | North America & APAC core, spill-over to EU | Medium term (2-4 years) |

| AI-assisted scientific workflow automation and decision support | +2.1% | Global | Medium term (2-4 years) |

| Increased use of software to shorten validation and audit preparation cycles | +1.5% | North America & EU, early gains in key APAC hubs | Short term (≤ 2 years) |

| Integration pressure from partner, CRO, and CDMO ecosystems | +1.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Regulatory-Ready Data Traceability Across the Product Lifecycle

Traceability has become a critical design requirement in the life sciences software market, moving beyond a documentation task at the end of an audit cycle. Companies now demand systems that maintain data lineage across laboratory work, quality events, manufacturing records, and regulatory submissions while ensuring validation control. This shift is driving preference for platforms with robust audit trails, stringent user controls, and resilient change-management structures. Vendors embedding compliance into daily operations are gaining traction, as tools lacking comprehensive records of decisions, edits, and approvals are losing relevance.

AI-Assisted Scientific Workflow Automation and Decision Support

AI is now integral to the life sciences software market, particularly in clinical, commercial, and research workflows. IQVIA's launch of IQVIA.ai in 2026 demonstrated how vendors are embedding AI into enterprise platforms, supported by over 100 AI patents and 150+ intelligent agents. With 19 of the top 20 pharmaceutical companies already using IQVIA agents, AI adoption has moved beyond pilot stages.[1]IQVIA Holdings Inc., “IQVIA Unveils IQVIA.ai, a Unified Agentic AI Platform Powered by NVIDIA,” BusinessWire, businesswire.com Similarly, Benchling introduced Model Hub, integrating AI tools into validated R&D environments. These advancements highlight the growing demand for modern ELN, LIMS, and connected data platforms, as AI outputs in regulated settings require governance and traceability.

Expansion of Cloud-Native and Interoperable Life Science Data Architectures

Cloud adoption in the life sciences software market now focuses on seamless integration of commercial, clinical, quality, and research data. Major providers are building partnerships and embedding data services to retain customers within platform ecosystems. Salesforce partnered with AstraZeneca in 2025 to deploy Agentforce Life Sciences as a global customer engagement platform, following similar moves by Novartis and Takeda. SAP integrated Joule AI into life sciences workflows, emphasizing interoperability that combines data movement and AI usability. The market is shifting towards platforms with interconnected data architectures, sidelining those reliant on isolated models or limited API connectivity.

Increased Use of Software to Shorten Validation and Audit Preparation Cycles

The life sciences software market is prioritizing faster validation and simplified audit preparation with minimal manual effort. Buyers prefer platforms that reduce repetitive testing, centralize controlled records, and ensure sustained inspection readiness. Oracle’s 2026 update to Clinical One introduced EHR data import, ICH E2B(R3)-compliant safety integration, and enhanced adaptive randomization support, enabling more connected and audit-ready clinical operations. This trend is accelerating modernization decisions, particularly among mid-sized biotech firms, sponsors, and outsourced service providers.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| high switching costs from deep workflow embedding and data migration costs | -1.2% | Global | Short term (≤ 2 years) |

| validation burden and change-control risk in regulated environments | -0.9% | North America & EU | Medium term (2-4 years) |

| fragmented legacy stack across R&D, quality, and commercial teams | -0.7% | Global | Long term (≥ 4 years) |

| interoperability gaps across instruments, EHR adjacent systems, and external partners | -0.6% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Switching Costs From Deep Workflow Embedding and Data Migration Costs

Switching costs significantly hinder the life science software market. Core platforms are deeply integrated with validated workflows, linked records, and downstream systems, making transitions complex. Migration involves data mapping, retesting, user retraining, document updates, and managing historical records, transforming it into an operational challenge rather than a simple software installation. Larger companies plan migrations over multi-year cycles, while smaller firms often retain older systems until compliance demands force upgrades. Although the market is open to innovation, vendor displacement progresses slower than demand growth.

Validation Burden and Change-Control Risk in Regulated Environments

The life science software market faces delays due to the extensive review, documentation, and reapproval required for system changes in regulated environments. This impacts product releases for vendors and extends deployment timelines for clients, especially in GxP-relevant processes or AI-driven decision-making. AI-based medical products in the EU face overlapping compliance obligations under frameworks like the AI Act and MDR or IVDR, increasing complexity for organizations. Vendors must align product designs with varying governance expectations, while buyers incur higher adoption costs unless tools offer robust documentation, clear oversight, and streamlined updates. The market favors vendors with disciplined release management and innovative solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Software Type: LIMS Holds the Core Position While CTMS Delivers the Fastest Expansion

In 2025, laboratory information management systems (LIMS) held a 28.00% share of the software segment, reinforcing their critical role in the life science software market. LIMS platforms are indispensable, connecting sample tracking, instrument outputs, quality reviews, and regulated data management across laboratories. Their centrality in pharmaceutical quality control, bioanalytical labs, and contract research organizations (CROs) makes them difficult to replace. Clinical trial management systems (CTMS) are projected to grow at a 12.45% CAGR through 2031, driven by the increasing complexity and data demands of modern trial designs.

The industry is shifting toward platforms that streamline study coordination, site activities, transparency mandates, and patient data collection. Thermo Fisher Scientific’s acquisition of Clario in 2026 highlighted the strategic importance of CTMS capabilities. Electronic lab notebooks, regulatory information management systems, and scientific data management systems are gaining traction as organizations transition to integrated digital records. Bioinformatics and pharmacovigilance software are also becoming essential as AI-driven analytics are embedded into core workflows.

By Deployment: Cloud Moves Further Ahead as the Preferred Validated Model

In 2025, cloud deployment accounted for 51.44% of the market share, establishing its dominance in the life science software sector. It is projected to grow at a 12.77% CAGR through 2031, reflecting its leadership in adoption and future spending. Buyers now view cloud as a viable regulated architecture, supported by vendors offering preconfigured controls, integration capabilities, and specialized functionalities.

Salesforce’s Life Sciences Cloud and Agentforce platform gained enterprise adoption from major players like Takeda, Novartis, and AstraZeneca in 2025, showcasing confidence in cloud-native systems for regulated use. While on-premises systems remain relevant for specific needs like data residency and sensitive records, the market is increasingly favoring hybrid and cloud-first models for scalability, interoperability, and AI integration.

By Application: Clinical Trials Leads Current Spending While R&D Expands the Fastest

In 2025, clinical trials held a 35.65% share, making them the largest application in the life science software market. This reflects the software's critical role in trial operations, including data capture, randomization, monitoring, safety reporting, and remote coordination. Oracle’s enhancements to its Clinical One platform in 2026 addressed the need for more connected study execution. Research and development is expected to grow at a 13.23% CAGR through 2031 as laboratories adopt automation and AI-driven data environments. R&D spending is shifting from recordkeeping tools to platforms that integrate instruments, automation, scientific data, and model outputs.

Benchling’s launch of its automation platform in 2026 exemplifies this trend, creating a continuous data loop by connecting lab instruments and scientific records. Drug discovery tools are also gaining importance as vendors integrate informatics into early research programs. IQVIA’s acquisition of drug discovery assets in 2026 highlights the growing role of software in discovery initiatives. Applications in manufacturing, quality, and commercial sectors continue to expand as vendors integrate regulated operations with enterprise data and AI layers.

By End User: Biotechnology Companies Lead Demand and Sustain the Highest Growth

In 2025, biotechnology companies accounted for 42.03% of end-user demand, making them the largest buyers in the life science software market. They are projected to grow at a 13.35% CAGR through 2031, driven by advancements in biologics, cell and gene therapies, and mRNA developments. These modalities generate dense and diverse data, making traditional spreadsheet methods increasingly unfeasible. Biotech companies are adopting digital platforms earlier in their lifecycle, integrating informatics into core scientific processes. This demand for speed, flexibility, and scalable data governance is reshaping vendor priorities.

Veeva reported fiscal year 2025 revenue of USD 2.746 billion, with USD 2.284 billion from subscription services, and expanded its R&D solutions customer base to 1,125. While pharmaceutical companies influence feature standards through large procurement programs, CDMOs and CROs are becoming significant buyers as outsourced development and manufacturing grow. SAP’s partnership with Chanelle Pharma in 2026 reflects the trend of outsourced manufacturers investing in enterprise-grade software for regulated growth. Academic institutions and medical device firms also contribute to demand, though their purchasing patterns are more specialized and less consistent compared to biotech and pharmaceutical companies.

Geography Analysis

In 2025, North America held a 38.99% share of the life science software market, maintaining its position as the largest regional block. The region benefits from a high concentration of pharmaceutical, biotechnology, and medical device companies operating under strict digital documentation standards. A mature SaaS ecosystem and a strong base of funded biotech firms further drive software adoption. Microsoft's collaboration with Mayo Clinic in June 2026 to develop an advanced AI model for healthcare highlights North America's continued leadership in life sciences data infrastructure.

Europe remains a key player in the life science software market, with demand shaped by compliance timelines and formal process controls. Countries like Germany, France, and the UK anchor regional demand through strong pharmaceutical production, research capabilities, and regulated data management needs. The region is also fostering local specialists, particularly in submission and pharmacovigilance workflows, where regulatory specificity is critical. Ennov’s submission of one of four eCTD 4.0 test sequences to the EMA pilot program demonstrates the growing visibility of European-native vendors in high-control software segments.

Asia-Pacific is projected to grow at a 12.95% CAGR through 2031, making it the fastest-growing region in the life science software market. China and India drive this growth with increased clinical trial activity, outsourced research capacity, and digital regulatory processes. China's "AI+" pharmaceutical supervision initiative in April 2026 and the Biomedical New Technology Clinical Research Regulation effective May 2026 have strengthened the demand for compliant software systems.

Competitive Landscape

The life science software market is evolving from a fragmented landscape to a more structured competitive arena. Major players are broadening their horizons, moving beyond singular functions. They are now offering expansive product suites, integrated data solutions, and AI-driven services to retain their clientele. Key players like IQVIA, Veeva Systems, Microsoft, Salesforce, Oracle, SAP, and Dassault Systèmes are vying for dominance, each carving out a niche in the software spectrum. Today, competition in the life science software arena transcends mere product depth. Buyers are increasingly prioritizing platforms that promise long-term compliance, interoperability, and extensibility.

Recent strategic maneuvers underscore this shifting competitive landscape. In March 2026, IQVIA unveiled IQVIA.ai, bridging agentic AI with clinical, commercial, and real-world workflows, marking its transition from an analytics provider to a comprehensive operating platform. In the same month, Thermo Fisher bolstered its software capabilities by acquiring Clario, enhancing its services with significant clinical endpoint data capabilities. December 2025 saw Salesforce making waves when AstraZeneca chose Agentforce Life Sciences as its global customer engagement platform, a move echoed by other major pharmaceutical players.

While larger players dominate, smaller vendors still wield influence, particularly in R&D settings where user-friendliness and workflow integration take precedence over sheer breadth. For instance, Benchling’s April 2026 introduction of AI Connectors aims to seamlessly integrate scientific records with the broader AI ecosystem via the Model Context Protocol. Such innovations empower biotech users with a more flexible operating model, eliminating the need for an entire software stack overhaul.

Life Science Software Industry Leaders

IQVIA Holdings Inc.

microsoft corporation

oracle corporation

Salesforce, Inc.

Veeva Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Microsoft and Mayo Clinic announced a partnership to develop an advanced AI model for healthcare, accessible globally through Azure Foundry APIs. First Foundation Labs also collaborated with Microsoft Discovery to enhance the platform with clinical and translational AI reasoning, enabling systematic hypothesis generation in life sciences R&D.

- May 2026: Benchling launched three new products at for end-to-end antibody R&D, Benchling Automation for integrating lab instruments and scientific records, and a Data Analysis AI skill, strengthening its leadership in biotech R&D.

- May 2026: Benchling introduced Model Hub, allowing scientists to manage and track AI models alongside structured experimental data within a validated workflow.

- March 2026: IQVIA launched IQVIA.ai, an AI platform powered by NVIDIA Nemotron, featuring over 100 AI patents and 150+ deployed agents across clinical, commercial, and real-world domains. The company reported that 19 of the top 20 pharmaceutical companies have adopted its agents into their workflows.

- March 2026: SAP and Chanelle Pharma announced a strategic partnership to implement SAP S/4HANA Cloud Private Edition and SAP Business AI, targeting a late-2026 go-live as part of Chanelle’s investment in a GxP-compliant digital foundation.

Global Life Science Software Market Report Scope

As per the scope of the report, life science software refers to technology designed to help biotech, pharmaceutical, and healthcare organizations manage research, run clinical trials, and meet strict government rules. It organizes complex lab data and speeds up the process of creating new drugs and medical treatments.

The life science software market is segmented by software type, deployment, application, end-user, and geography. By software type, the market includes laboratory information management systems, electronic lab notebooks, clinical trial management systems, regulatory information management systems, scientific data management systems, bioinformatics software, pharmacovigilance software, quality management software, and other life science software types. By deployment, the market is segmented into cloud and on-premises. By application, the market is categorized into research and development, drug discovery, clinical trials, regulatory compliance, manufacturing operations, quality management, commercial operations and customer engagement, and other applications in life science software. By end-user, the market is segmented into pharmaceutical companies, biotechnology companies, contract research organizations, contract development and manufacturing organizations, academic and research institutes, medical device companies, and other end users in life science software. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Laboratory Information Management Systems |

| Electronic Lab Notebooks |

| Clinical Trial Management Systems |

| Regulatory Information Management Systems |

| Scientific Data Management Systems |

| Bioinformatics Software |

| Pharmacovigilance Software |

| Quality Management Software |

| Other Life Science Software Types |

| Cloud |

| On-Premises |

| Research and Development |

| Drug Discovery |

| Clinical Trials |

| Regulatory Compliance |

| Manufacturing Operations |

| Quality Management |

| Commercial Operations and Customer Engagement |

| Other Applications in Life Science Software |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Contract Research Organizations |

| Contract Development and Manufacturing Organizations |

| Academic and Research Institutes |

| Medical Device Companies |

| Other End Users in Life Science Software |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Software Type | Laboratory Information Management Systems | |

| Electronic Lab Notebooks | ||

| Clinical Trial Management Systems | ||

| Regulatory Information Management Systems | ||

| Scientific Data Management Systems | ||

| Bioinformatics Software | ||

| Pharmacovigilance Software | ||

| Quality Management Software | ||

| Other Life Science Software Types | ||

| By Deployment | Cloud | |

| On-Premises | ||

| By Application | Research and Development | |

| Drug Discovery | ||

| Clinical Trials | ||

| Regulatory Compliance | ||

| Manufacturing Operations | ||

| Quality Management | ||

| Commercial Operations and Customer Engagement | ||

| Other Applications in Life Science Software | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Contract Research Organizations | ||

| Contract Development and Manufacturing Organizations | ||

| Academic and Research Institutes | ||

| Medical Device Companies | ||

| Other End Users in Life Science Software | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the life science software market by 2031?

The life science software market is forecast to reach USD 37.65 billion by 2031, rising from USD 22.08 billion in 2026 at an 11.26% CAGR.

Which software type currently leads adoption in life sciences?

Laboratory information management systems led software type demand with 28.00% share in 2025 because they remain central to sample, instrument, and quality data management.

Why is cloud deployment gaining faster acceptance in regulated environments?

Cloud held 51.44% share in 2025 and is projected to grow at 12.77% CAGR through 2031 because buyers increasingly want validated, interoperable, and scalable platforms.

Which application area is growing the fastest through 2031?

Research and development is the fastest-growing application area, with a projected 13.23% CAGR, driven by AI-enabled laboratory workflows and connected scientific data systems.

Why are biotechnology companies the biggest buyers of these platforms?

Biotechnology companies held 42.03% share in 2025 and are also the fastest-growing end-user group because biologics, mRNA, and cell and gene therapy programs generate complex datasets that require stronger digital infrastructure.

Which region is expanding the fastest?

Asia-Pacific is projected to grow at a 12.95% CAGR through 2031, supported by clinical trial growth, regulatory digitalization, and rising software demand in China and India.

Page last updated on: