Computational Biology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

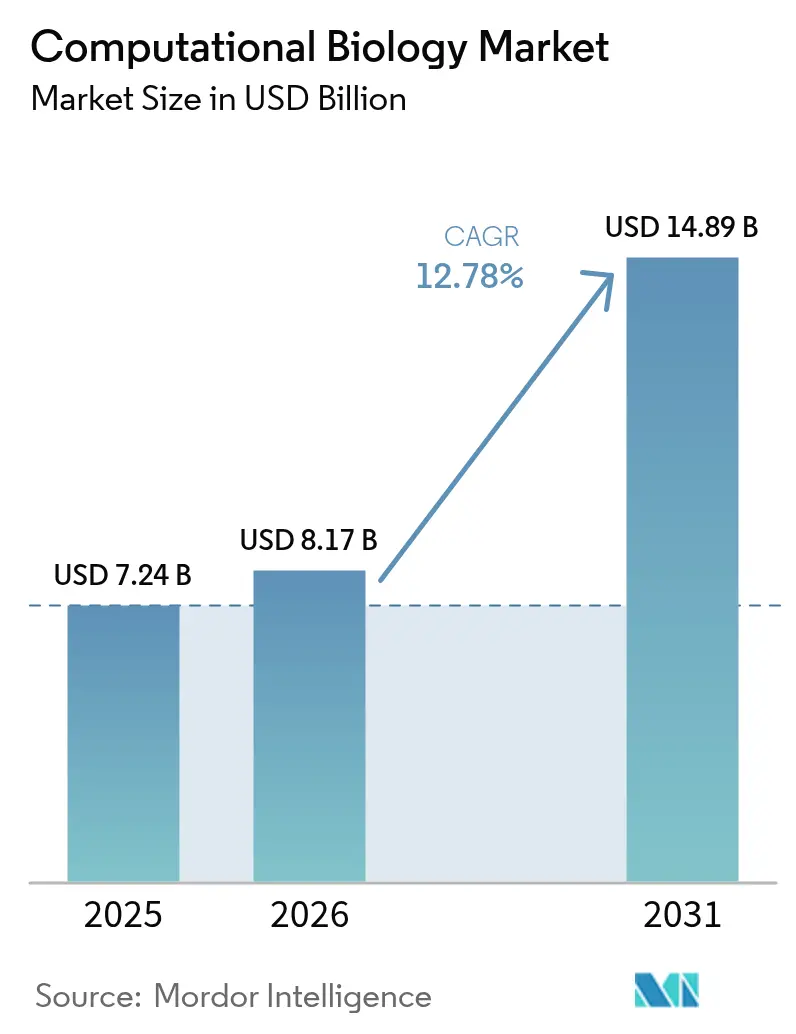

| Market Size (2026) | USD 8.17 Billion |

| Market Size (2031) | USD 14.89 Billion |

| Growth Rate (2026 - 2031) | 12.78% CAGR |

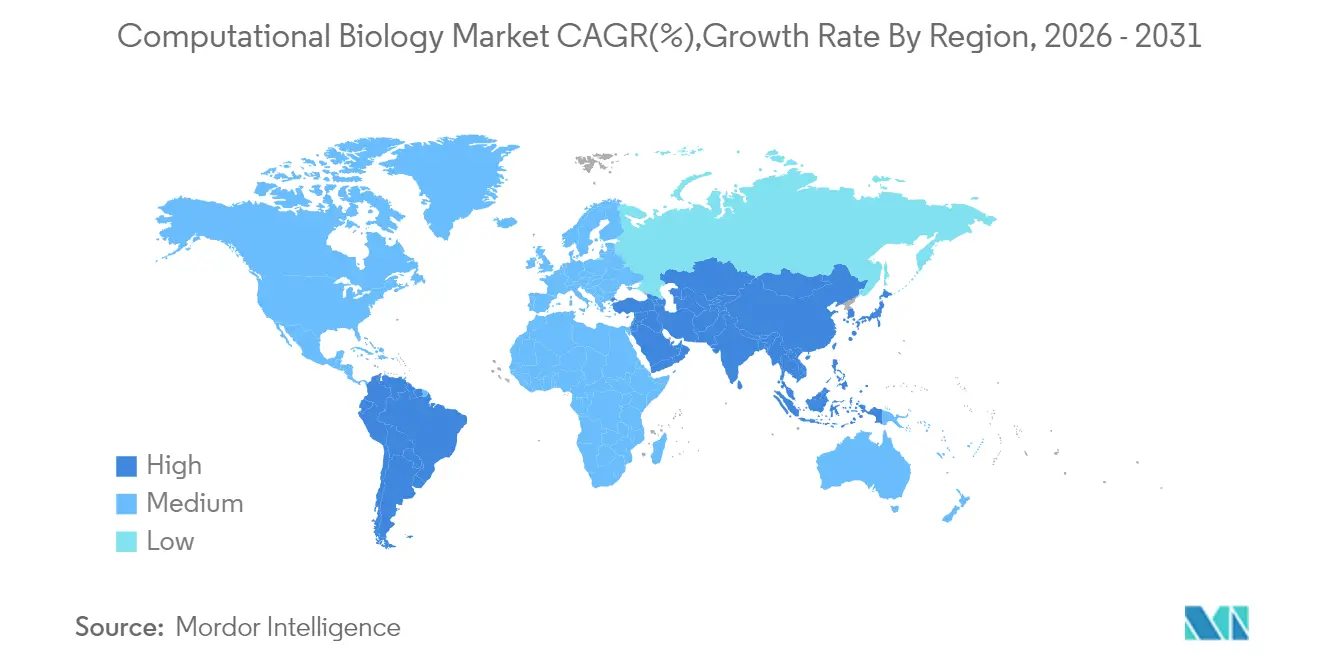

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

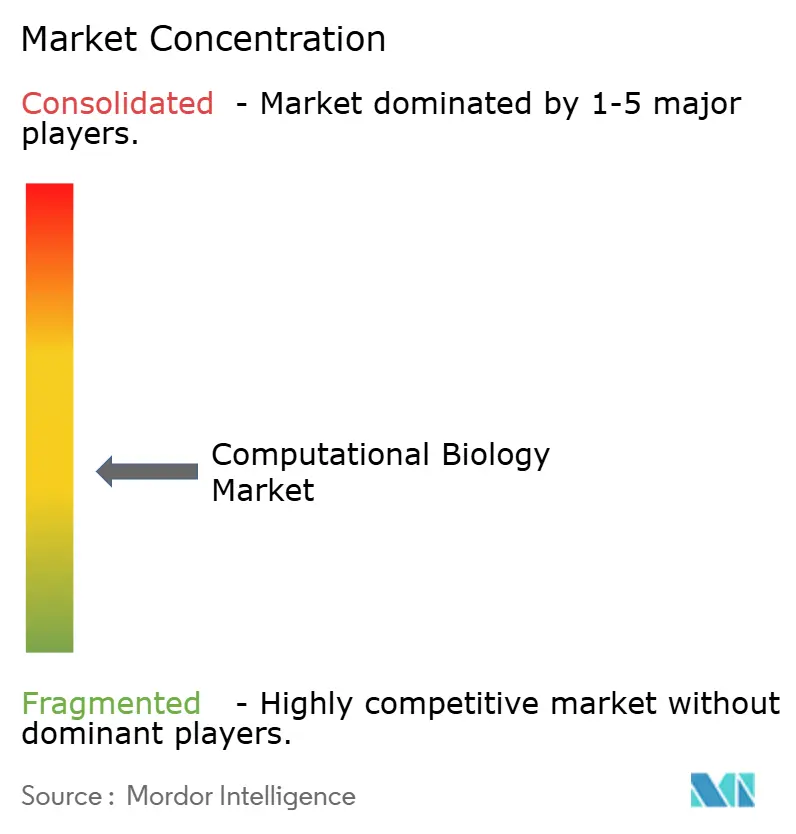

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Computational Biology Market Analysis by Mordor Intelligence

Computational biology market size in 2026 is estimated at USD 8.17 billion, growing from 2025 value of USD 7.24 billion with 2031 projections showing USD 14.89 billion, growing at 12.78% CAGR over 2026-2031. This outlook signals how transformer-based genome language models, synthetic-biology digital twins, and wider AI adoption now shape every application layer of the computational biology market. A sharp rise in multi-omics datasets, ongoing shifts toward contract research services, and the need for scalable cloud infrastructure keep fueling demand. North America still anchors the computational biology market thanks to mature biotech regulation, but Asia-Pacific’s supercomputer investments and expanding pharmaceutical manufacturing base are positioning the region as the next growth engine. Meanwhile, strategic acquisitions such as Siemens’ USD 5.1 billion deal for Dotmatics reflect intensifying platform consolidation inside the computational biology market.

Key Report Takeaways

- By application, cellular and biological simulation accounted for 32.10% of the computational biology market share in 2025, while drug discovery and disease modeling are forecast to grow at a 15.33% CAGR through 2031.

- By tool, databases held the largest 35.95% share of the computational biology market size in 2025; however, analysis software and services are expected to expand at a 14.49% CAGR through 2031.

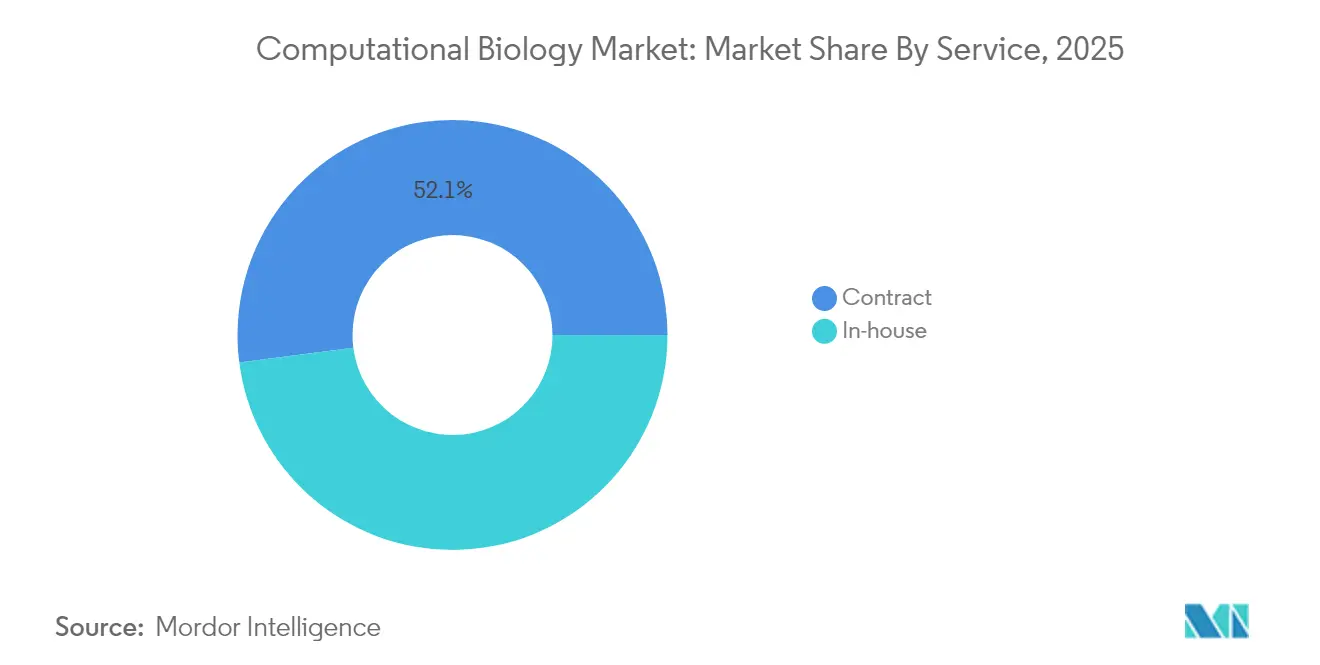

- By service model, contract arrangements accounted for 52.05% of the computational biology market share in 2025 and are projected to advance at a 15.72% CAGR through 2031.

- By end user, academia retained 44.10% revenue share in 2025, whereas industry and commercial users are projected to post a 14.27% CAGR to 2031.

- By region, North America led with a 42.30% computational biology market share in 2025; the Asia-Pacific region shows the fastest 16.02% CAGR outlook through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Computational Biology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising volume of omics data & bioinformatics research | +2.8% | Global, concentrated in North America and EU | Medium term (2–4 years) |

| Accelerated use in drug discovery & disease modeling | +3.1% | Global, led by North America, expanding to APAC | Short term (≤ 2 years) |

| Expansion of clinical pharmacogenomics & pharmacokinetics studies | +1.9% | North America and EU, emerging in APAC | Medium term (2–4 years) |

| Transformer-based genome language models enabling rapid annotation | +2.2% | Global, early adoption by research institutes | Short term (≤ 2 years) |

| Synthetic-biology digital twins for in-silico workflows | +1.7% | North America and EU, pilots in APAC | Long term (≥ 4 years) |

| Open-source single-cell lineage-tracing algorithms | +1.5% | Global, academic-led with industry uptake | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising volume of omics data & bioinformatics research

Terabyte-scale single-cell RNA-sequencing, multi-omics integration, and lower sequencing costs continue to expand data flows into the computational biology market. Advances in sequencing have cut RNA-seq costs by 50-70%, widening access to precision-medicine datasets. Large language models now automate 94% of common data-element mapping, driving interoperability.[1]Rodney Alan Long, Jordan Klebanoff, and Vince D. Calhoun, “A New AI-Assisted Data Standard Accelerates Interoperability in Biomedical Research,” medRxiv, medrxiv.orgThe resulting data network effects reinforce first-mover advantages for stakeholders controlling the largest repositories. Cloud bioinformatics platforms therefore have become mandatory infrastructure for organizations lacking on-premises high-performance computing.

Accelerated use in drug discovery & disease modeling

Protein language models, such as ESM-3, simulate evolutionary processes, creating novel protein candidates at a pace that drug developers could not achieve a few years ago. Hybrid AI–quantum systems, exemplified by Model Medicines’ GALILEO, now deliver 100% hit-rate antiviral screens.[2]Model Medicines Communications Team, “The Future of Drug Discovery: 2025 as the Inflection Year for Hybrid AI and Quantum Computing,” Model Medicines, modelmedicines.comDigital twins enable researchers to run millions of virtual experiments, thereby compressing hypothesis-testing cycles and reducing wet-lab costs. A 479,000-trial machine-learning benchmark provides unprecedented training data for trial-design optimization. M&A activity, such as the USD 688 million Recursion-Exscientia merger, shows incumbents racing to internalize these AI advantages and consolidate platforms.

Expansion of clinical pharmacogenomics & pharmacokinetics studies

Preemptive pharmacogenomics testing cut psychiatric adverse drug reactions by 34.1% and hospitalizations by 41.2%.[3]Maria Skokou, Konstantinos Tziomalos, and Georgios Papazisis, “Clinical Implementation of Preemptive Pharmacogenomics in Psychiatry,” eBioMedicine, thelancet.com Real-world panels show 60.4% of patients receive at least one actionable prescription. UCLA leveraged a 342,000-person biobank to identify 156 genes that modulate statin efficacy, providing proof that genetic diversity improves dosing accuracy. AI-enhanced PK/PD models now account for population-specific variants, a requirement as the adoption of pharmacogenomics in the Asia-Pacific region rises.

Transformer-based genome language models enabling rapid annotation

Open-source protein models deliver AlphaFold-class performance while requiring only commodity GPUs. Bidirectional DNA foundation models, such as JanusDNA, process 1 million base pairs without specialized hardware. Parameter-efficient fine-tuning methods, such as LoRA, reduce training costs while maintaining or improving downstream prediction accuracy. These gains democratize advanced analytics and lower barriers to entry, extending the computational biology market well beyond traditional bioinformatics centers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of multidisciplinary talent | -1.8% | Global, acute in North America and EU | Short term (≤ 2 years) |

| Interoperability & data-standardization gaps | -1.2% | Global, especially cross-border collaborations | Medium term (2–4 years) |

| Escalating cloud & compute costs | -0.9% | Global, strongest effect in cost-sensitive markets | Short term (≤ 2 years) |

| Biosecurity & dual-use regulatory scrutiny | -0.7% | Mainly North America and EU, expanding worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of multidisciplinary talent

The demand for professionals with expertise in biology, software engineering, and statistics outstrips the supply. Life-science employers anticipate a 35% shortfall by 2030, with hiring demand projected to grow at an annual rate of 11.75%. Salary inflation and project delays follow, particularly for mid-sized biotechs that compete with tech giants entering the field. Skills-based hiring, apprenticeships, and cross-industry recruitment are interim mitigation strategies.

Interoperability & data-standardization gaps

While Matrix and Analysis Metadata Standards (MAMS) begin to align single-cell datasets, broad harmonization remains elusive. Semantic mapping tools can integrate unstructured health records; however, implementation burdens slow their adoption. Federated-learning pilots protect privacy but still confront regulatory uncertainty, leaving multinational studies reliant on manual data cleaning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Drug discovery and disease modeling power next-generation workflows

Drug discovery and disease modeling already post the fastest 15.33% CAGR, whereas cellular and biological simulation retained a 32.10% stake in the computational biology market size by 2025. AI-enhanced target identification and lead optimization enable companies like Insilico Medicine to screen millions of compounds in silico. Preclinical teams now integrate genomic, proteomic, and metabolomic data sets to raise compound-to-clinic success odds. Clinical-trial operations utilize retrieval-augmented systems that achieve 97.9% eligibility-screening accuracy, thereby reducing recruitment bottlenecks. A growing number of investigators are exploiting digital twins to conduct virtual dose-response studies, thereby shrinking wet-lab timelines. Consequently, the computational biology market experiences deeper pharmaceutical engagement at every stage of R&D.

Human-body simulation software emerges as a high-potential sub-segment. Stanford’s AI-driven “virtual cell” illustrates how integrated multi-omics and biophysical models can map pathway perturbations for individualized therapy strategies. This development expands the computational biology market to frontline precision-medicine clinicians. As digital twin fidelity increases, insurers start evaluating reimbursement models for computer-optimized treatment plans, indicating potential opportunities for downstream revenue streams.

By Tool: Analysis software accelerates AI integration

Databases still account for 35.95% of the computational biology market share, but analysis software and services chart the fastest growth at 14.49% CAGR. Protein and genome language models are prompting organizations to invest in analytical capacity rather than maintaining static archives. Vendors embed multimodal data pipelines that fuse genomic, proteomic, and clinical streams. The shift also encourages academic-industry consortia to co-develop open-source stacks; Boltz-1’s AlphaFold-comparable accuracy on standard GPUs underscores how community innovation fuels wider adoption.

On-premises high-performance computing remains important for handling sensitive datasets; however, cloud cost curves and the maturity of managed services encourage migration. Providers differentiate by auto-scaling algorithms and security certifications. Database incumbents react by building analytics layers on top of repositories to defend their install base. The net effect increases competition yet lifts overall software quality, supporting sustained growth in the computational biology market.

By Service: Contract models dominate growth

Contract research services lead both share and velocity—52.05% in 2025 and a 15.72% CAGR outlook—as pharmaceutical companies outsource complex in-silico workflows. CROs now bundle genomic analysis, AI model development, and virtual screening in unified subscriptions. In-house teams retain core, IP-intensive algorithms but partner externally for computationally intensive simulations.

Hybrid service frameworks gain traction. Enterprises maintain data-governance nodes on premises while bursting to cloud-based CRO platforms for peak workloads. Strategic alliances distribute risk: clients pay usage-based fees, while providers guarantee service-level agreements that include regulatory support. As adoption increases, the computational biology market further integrates into traditional drug development value chains.

By End User: Industry adoption accelerates

Academia controlled 44.10% of the revenue in 2025, yet industry users captured momentum with a 14.27% CAGR through 2031. Declining sequencing costs, validated AI pipelines, and urgent therapeutic timelines drive pharmaceutical uptake. Enterprise buyers seek turnkey solutions that embed audit trails and comply with GxP regulations.

Academic institutions remain knowledge engines, pioneering algorithms later licensed commercially. To counter budget limits, universities are expanding partnership models where technology vendors provide compute credits in exchange for co-authorship and early access to feedback. This symbiosis sustains innovation funnels for the computational biology industry.

Geography Analysis

North America, commanding 42.30% 2025 revenue, benefits from deep biotech venture capital, mature regulator engagement, and a dense talent pool. The FDA’s evolving AI framework provides local firms with a more straightforward commercialization path than many of their peers. Thermo Fisher’s USD 2 billion multi-year domestic investment underscores confidence in infrastructure scalability; nonetheless, workforce shortages and rising cloud costs temper acceleration.

Asia-Pacific posts the highest 16.02% CAGR. Governments bankroll exaflop supercomputers—South Korea’s plan targets launch by 2025—while China’s distributed national centers already propel multi-omics projects. Regional pharmaceutical manufacturing booms, and genetic diversity research programs tailor AI models to local populations, creating edge-case data assets that are unavailable elsewhere. Decentralized clinical-trial pilots and mRNA platform build-outs reinforce long-term demand for computational biology market capabilities.

Europe maintains steady growth, anchored by cross-border consortia and robust data privacy safeguards. Ethical AI initiatives increase compliance overhead, yet also foster trust among payers and regulators. Digital-twin pilots align with public health goals to optimize resource utilization. Meanwhile, Latin America, Africa, and the Middle East are making progress as internet infrastructure and bioinformatics curricula expand. Partnerships with multinational pharmaceutical groups compensate for local funding gaps, ensuring gradual yet persistent market penetration in computational biology.

Regulatory Landscape

In the United States, the FDA has been formalizing expectations for AI-enabled computational methods used in drug and biologics development. In January 2025, the agency issued draft guidance on the use of artificial intelligence to support regulatory decision-making for drug and biological products, with emphasis on a risk-based credibility assessment for AI outputs used in submissions. The FDA also continues to advance New Approach Methodologies (NAMs), and in March 2026 released draft guidance on alternatives to animal testing, reinforcing regulatory acceptance pathways for validated in silico and other human-relevant approaches.

In Europe, AI governance and life-science policy initiatives are raising compliance requirements for computational biology platforms that handle sensitive biomedical data. The European Commission has been developing a broader biotechnology policy agenda, including the European Biotech Act initiative, while the EU AI regulatory framework adds lifecycle obligations around documentation, risk management, and data governance that can affect how computational models are developed and deployed in regulated workflows. In parallel, standard-setting momentum in the US, including proposed legislation directing NIST-linked work on definitions and frameworks for AI-ready biological datasets (H.R. 7907), highlights the role of data quality, provenance, and interoperability in multi-omics analytics that feed regulatory decisions.

Value Chain Analysis

The computational biology value chain starts with biological and clinical data generation (sequencing, proteomics, imaging, and real-world clinical data), followed by ingestion, curation, harmonization, and secure storage in repositories and data lakes. Model development and validation then depend on scalable infrastructure, including HPC clusters and cloud accelerators, plus specialized software layers such as workflow orchestration, analysis software, simulation engines, and domain databases. Outputs are packaged into enterprise workflows for drug discovery, disease modeling, pharmacogenomics, and clinical trial operations, delivered through licensed platforms, in-house teams, or contract service providers.

Downstream delivery increasingly hinges on integrated ecosystems that connect algorithms, compute, and governed data access. Partnerships such as Illumina and NVIDIA (January 2025) show how omics pipelines, including DRAGEN analytics, are being tied to accelerated computing stacks to reduce turnaround time for large multi-omics workloads. Key bottlenecks include data migration friction for terabyte-scale datasets, interoperability gaps between proprietary environments, and vendor lock-in risks when workflows are tightly coupled to specific cloud configurations, which can affect reproducibility and auditability in regulated settings.

Competitive Landscape

The computational biology market remains moderately fragmented, but it shows a clear trend of mergers and acquisitions (M&A). Siemens’ USD 5.1 billion Dotmatics acquisition integrates lab informatics with industrial digital twin offerings, reflecting buyers’ desire for end-to-end stacks. Danaher brought Genedata into its portfolio, mirroring the same logic. Illumina collaborates with NVIDIA to speed GPU-powered omics analytics, an example of tech–biotech convergence.

Start-ups leverage open-source communities to punch above their weight. EvolutionaryScale raised USD 142 million to commercialize protein-generating AI that competes directly with incumbents’ proprietary chemistries. Patent filings surrounding hybrid quantum-classical models and lineage-tracing algorithms suggest an intensification of IP battles. Competitive success will hinge on access to curated datasets, scalable compute, and integrated workflows that minimize switching costs.

Large vendors pursue ecosystem lock-in through subscription licensing and data-network effects. Mid-tier players differentiate themselves through vertical specialization—single-cell analytics, digital twin engines, or pharmacogenomics toolkits. Price competition is muted because accuracy, regulatory compliance, and turnaround speed remain decisive purchase factors.

Computational Biology Industry Leaders

Dassault Systèmes SE

Schrödinger Inc.

Certara

Simulation Plus Inc.

Illumina Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large, multi-year investments in building predictive, multimodal biology models are creating whitespace for platforms that can operationalize interoperable data pipelines, mechanistic simulation, and governed model reuse. In April 2026, Biohub announced a five-year USD 500 million Virtual Biology Initiative focused on predictive models of life using multi-modal datasets, which is increasing demand for tooling that can integrate multi-omics, preserve provenance, and support reproducible model development across institutions.

Clinical development modernization is also expanding opportunity for computational biology vendors offering secure cloud analytics, real-time monitoring, and traceable model outputs that fit submission-ready workflows. In April 2026, the FDA initiated a proof-of-concept clinical trial with AstraZeneca, UT MD Anderson, and the University of Pennsylvania to enable real-time endpoint monitoring in the cloud, raising the bar for scalable, governed data processing during trials. Standardization programs such as ARPA-H IGoR (announced May 2026) reinforce demand for reusable, verifiable experimental data and protocols, supporting tool providers that can embed interoperable metadata standards and validation into day-to-day computational workflows.

Recent Industry Developments

- May 2026: Veristat completed the acquisition of Certara's Regulatory and Medical Writing business, including the transfer of more than 200 regulatory experts. The transaction moves those capabilities into a specialist clinical and regulatory services provider, while Certara tightens focus on its core drug development software and model-informed decision support offerings.

- April 2026: Certara entered a definitive agreement to sell its Regulatory Writing and Medical Writing business to Veristat for up to USD 135 million. The divestiture reflects portfolio rationalization toward scalable computational platforms, and it also signals ongoing consolidation and specialization in outsourced regulatory services tied to data-heavy development programs.

- January 2026: Schrödinger partnered with Eli Lilly and Company to make the Lilly TuneLab AI platform available as a priority interface within Schrödinger's LiveDesign enterprise informatics platform. The integration approach increases stickiness of enterprise discovery workflows by embedding third-party AI capabilities inside established computational chemistry and biology environments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is counted as revenues earned from computational tools and services that help store, process, and model biological data for research and development work, including drug discovery, disease modeling, genomics, and proteomics.

Scope exclusions: We exclude free academic software and open-source code that is shared without a paid license, paid support, or a paid subscription.

Segmentation Overview

- By Application

- Cellular & Biological Simulation

- Computational Genomics

- Computational Proteomics

- Pharmacogenomics

- Other Simulations (Transcriptomics/Metabolomics)

- Drug Discovery & Disease Modelling

- Target Identification

- Target Validation

- Lead Discovery

- Lead Optimization

- Preclinical Drug Development

- Pharmacokinetics

- Pharmacodynamics

- Clinical Trials

- Phase I

- Phase II

- Phase III

- Human Body Simulation Software

- Cellular & Biological Simulation

- By Tool

- Databases

- Infrastructure (Hardware)

- Analysis Software & Services

- By Service

- In-house

- Contract

- By End-User

- Academics

- Industry & Commercials

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean fact base on life science R&D activity and data generation, and then mapping where computational biology spend typically sits inside that activity. We use public sources such as the National Institutes of Health funding databases, the US FDA and EMA public approvals and trial registries, NCBI and EMBL-EBI repository statistics, and OECD and World Bank science and technology indicators.

We also review peer-reviewed journals on computational methods adoption, patents to understand where new algorithms and workflows are being built, and company filings and investor presentations to identify revenue exposure and pricing logic. For cross-checks, a paid subscription focused on company financials and a paid patent database are used selectively to standardize peer sets and reduce the risk of missing private participants. These sources are not exhaustive, and we use additional public and paid references as needed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm what is being paid for and what is being used freely, which matters in computational biology. We spoke with solution providers, research leaders, and buyer-side managers across APAC, EMEA, and the Americas to validate adoption rates, typical contract sizes, and the split between software, services, and database access before the final assumptions were locked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 16% | APAC: 48% |

| Mid tier: 46% | Functional/Unit leaders: 25% | EMEA: 32% |

| Smaller Players: 20% | Managers: 59% | Americas: 20% |

Market-Sizing & Forecasting

Our sizing uses a top-down build that starts from life science R&D and clinical activity signals and then reconstructs the paid demand pool for computational biology by applying adoption and spend intensity factors. The totals are then checked through selective bottom-up approximations, including sample vendor revenue mapping, typical annual subscription or license price ranges, and volume checks using active user groups in research institutes and pharma settings.

Inputs we track include sequencing and omics data volumes (which lift compute and database needs), the number and mix of drug discovery programs and clinical trials, and the pace of AI and simulation use in discovery workflows. We also monitor cloud versus on-prem deployment mix and typical price progression for licenses and services as workloads scale. Where bottom-up signals are thin for smaller geographies, we apply region-specific adoption curves that were validated in interviews and then sanity-checked against funding and publication intensity.

For forecasting, we mainly rely on scenario analysis supported by multivariate regression checks, because the market moves with several drivers at the same time rather than one single series. Assumptions on funding, trial activity, and compute intensity are updated with expert consensus so the forecast stays practical and explainable.

Data Validation & Update Cycle

Results are validated through multiple cross-checks, so one data series does not overly drive the final value. We compare outputs against independent signals such as public research funding direction, trial activity trendlines, and disclosed revenue exposure from relevant participants, and then investigate any unusual jumps before internal sign-off.

If a major policy change, a sharp funding shift, or an acceleration in cloud migration is seen, experts are re-contacted to retest key assumptions and the model is recalculated. The report is refreshed annually, and material events can trigger interim updates, followed by a final pre-delivery review so clients receive the latest view.

Mordor Intelligence's Computational Biology Market Size Measured Against Other Published Estimates

Published market sizes for computational biology can look far apart because firms do not always count the same revenue streams, and they also pick different base years and growth windows. Differences in whether free research tools are treated as paid equivalents, and how software, services, and database access are grouped, are usually the biggest reasons.

The benchmark table shows a spread that is mainly explained by scope and timing, and in Mordor Intelligence's model the 2026 total counts paid software platforms, related services, infrastructure tools, and specialized databases, but it leaves out academic freeware and open-source code that is distributed without monetized support.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.17 B (2026) | |

| Industry Publisher A | USD 5.90 B (2024) | Uses an earlier base year and can mix paid revenues with broader research activity proxies, which typically undercounts later-stage commercial uptake and delays scale effects from cloud and AI-enabled workflows. |

| Industry Publisher B | USD 5.14 B (2025) | Starts from a different base year and commonly applies narrower commercial definitions around platform revenue, which can reduce the contribution from paid services and specialized database access that buyers often purchase alongside tools. |

When these differences are made explicit, the remaining variance becomes easier to interpret. Our approach stays traceable to clear paid-revenue boundaries and repeatable demand drivers, which helps decision-makers compare regions and time periods without mixing free usage with paid market value.

Key Questions Answered in the Report

What is the current size of the computational biology market?

The computational biology market generates USD 8.17 billion in 2026 and is on track to hit USD 14.89 billion by 2031.

Which application area is expanding fastest?

Drug discovery and disease modeling posts the highest 15.33% CAGR through 2031, driven by AI-enabled target identification and digital-twin workflows.

Why are contract research services growing rapidly?

Pharmaceutical firms outsource data-intensive modeling to specialized CROs, giving contract services a 52.05% share and a 15.72% growth rate.

Which region will contribute most to future growth?

Asia-Pacific leads with a 16.02% CAGR thanks to government supercomputer projects and rapidly expanding pharmaceutical manufacturing.

What is hindering wider adoption of computational biology platforms?

A shortage of multidisciplinary talent, rising cloud-compute costs, and evolving biosecurity regulations are the main constraints.

Page last updated on: