Orthopedic Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 439.01 Million |

| Market Size (2031) | USD 621.93 Million |

| Growth Rate (2026 - 2031) | 7.21% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Orthopedic Software Market Analysis by Mordor Intelligence

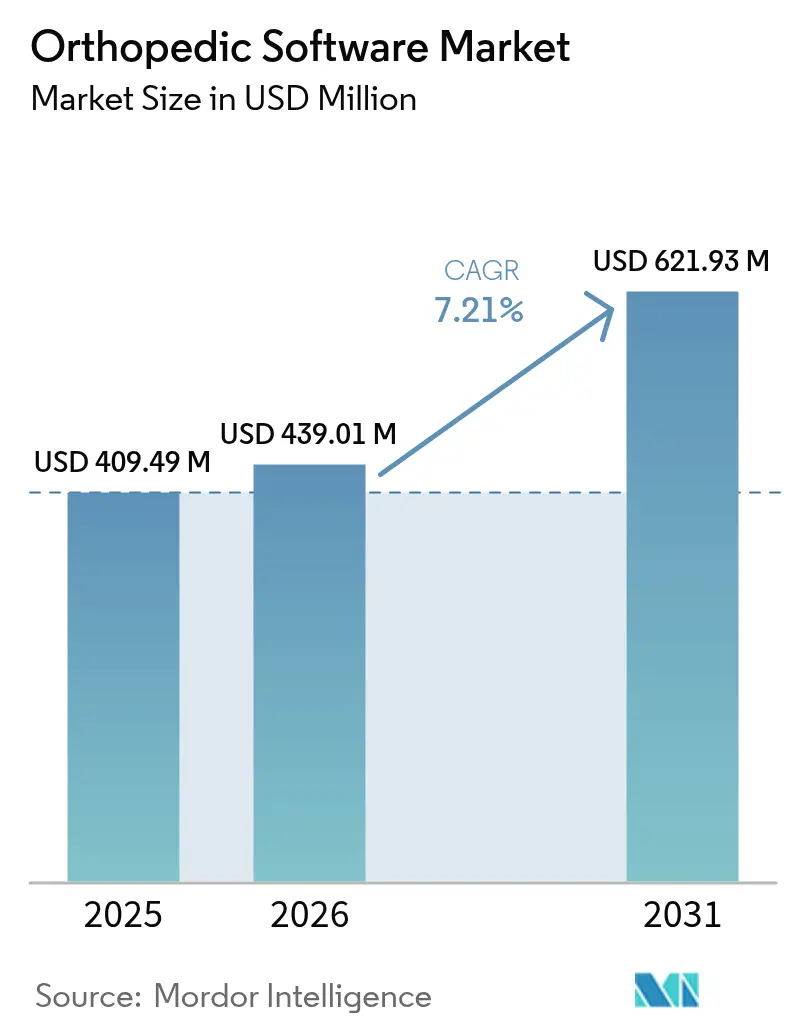

The Orthopedic Software market size is expected to grow from USD 409.49 million in 2025 to USD 439.01 million in 2026 and is forecast to reach USD 621.93 million by 2031 at 7.21% CAGR over 2026-2031.

Widespread digitization of orthopedic care, the rapid maturation of artificial intelligence (AI), and the enforcement of interoperability rules are pushing specialty clinics and large hospital systems toward integrated software ecosystems that manage imaging, surgical planning, and revenue-cycle tasks. Vendors that provide AI-driven decision support and secure cloud deployment continue to capture demand from practices looking to shorten operating-room time, lower revision rates, and tap new value-based reimbursement streams. Aging populations in high-income countries, surging ambulatory surgery center (ASC) volumes, and expanding use of robotic guidance further sustain double-digit growth in key sub-segments. Competitive intensity is rising as hardware majors enter software niches, yet the market remains fragmented, allowing mid-tier developers to gain share through niche innovations and regional partnerships.

Key Report Takeaways

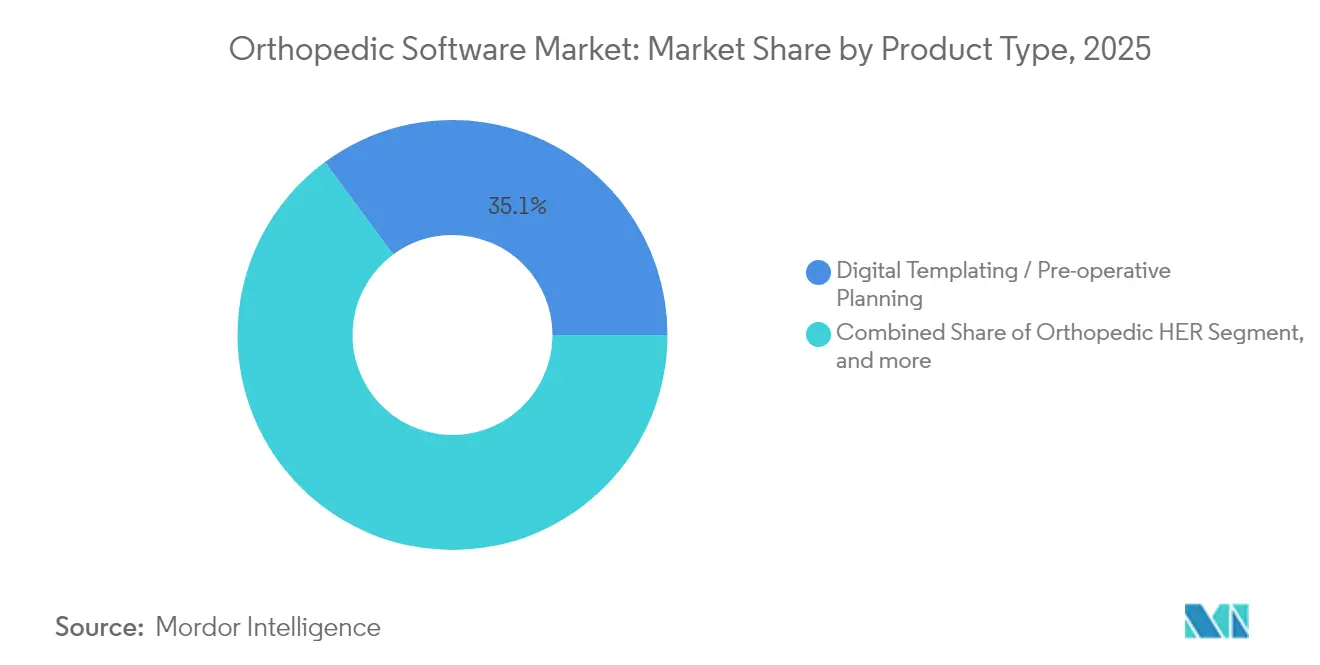

- By product type, digital templating captured 35.12% of orthopedic software market share in 2025, while orthopedic PACS is projected to expand at a 9.52% CAGR through 2031.

- By mode of delivery, cloud deployments commanded 58.74% share of the Orthopedic software market size in 2025, and the same model is forecast to grow at an 11.42% CAGR to 2031.

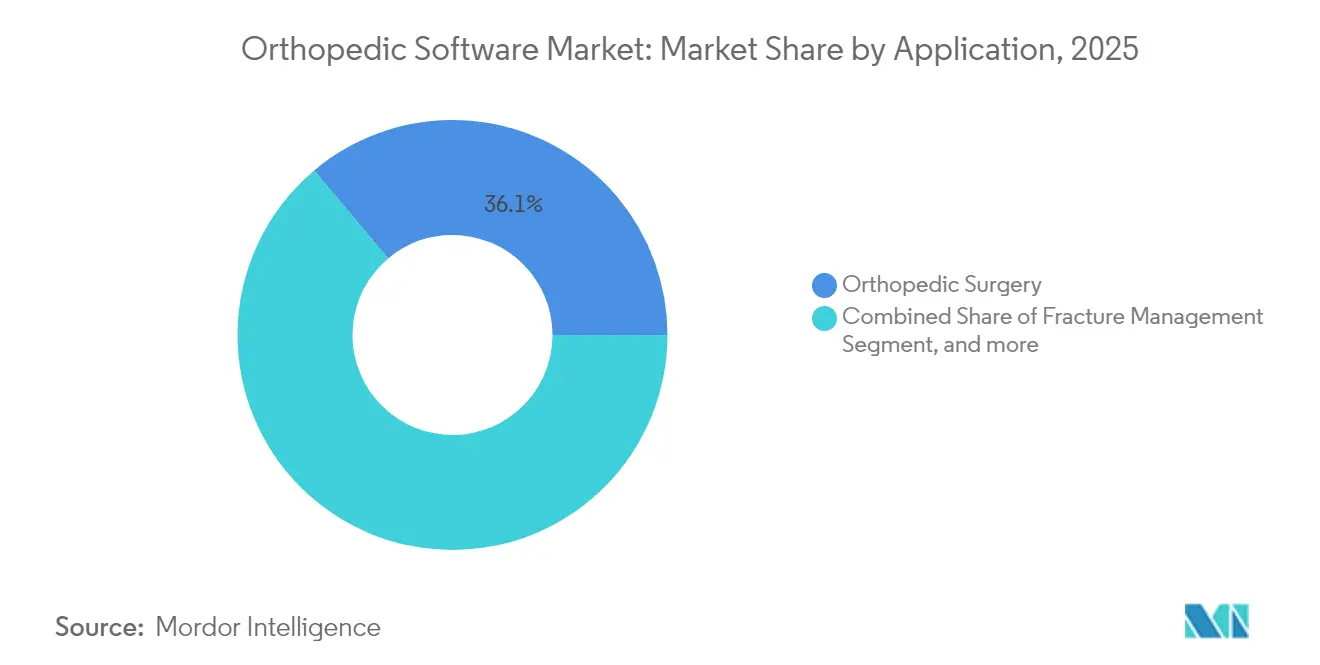

- By application, orthopedic surgery held 36.12% of the orthopedic software market size in 2025, whereas fracture management will record the fastest 12.04% CAGR between 2026-2031.

- By end user, hospitals accounted for 55.02% share of the orthopedic software market in 2025, while orthopedic clinics are poised for the highest 13.21% CAGR to 2031.

- By geography, North America led with 39.33% revenue share in 2025; Asia-Pacific is expected to post a 12.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Orthopedic Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population Boosting Osteoarthritis & Fracture Case-Load | +1.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Rapid Shift to Ambulatory & Minimally-Invasive Orthopedic Surgery | +1.5% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Mandatory EHR / PACS Interoperability | +1.2% | North America & EU regulatory zones | Short term (≤ 2 years) |

| 3-D Digital Templating Proven to Cut Implant Revision Rates | +1.0% | Global, early adoption in developed markets | Medium term (2-4 years) |

| AI Auto-Templating Reduces Sterile Tray Inventory | +0.8% | North America & Europe, pilot programs in APAC | Medium term (2-4 years) |

| Ortho-Software API Marketplaces Unlocking New SaaS Revenue for Clinics | +0.6% | North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population Boosting Osteoarthritis & Fracture Case-Load

Global populations aged 65+ continue to expand, driving up degenerative joint disease and fracture incidence that strain manual workflows. Digital templating decreases surgical time by 15-20% and improves implant placement accuracy, helping surgeons handle higher caseloads without compromising outcomes.[1]Journal of Clinical Medicine Editors, “Digital Templating in Total Hip Arthroplasty Improves Accuracy,” mdpi.com AI-driven imaging reaches over 90% diagnostic accuracy for early bone pathology detection, enabling proactive interventions that ease long-term cost pressures. Integrated revenue-cycle modules streamline complex geriatric billing, improving margin security for practices facing payer scrutiny.

Rapid Shift to Ambulatory & Minimally-Invasive Orthopedic Surgery

ASC volumes are climbing at 6.9% annually, with orthopedic outpatient procedures projected to grow 13% this decade. These settings require cloud-native software that supports rapid turnover, small operating suites, and tight capital budgets. CMS approval of shoulder replacements for outpatient reimbursement accelerates adoption of advanced planning tools. Only 54.6% of ASCs presently operate certified EHRs, signaling a sizable addressable market for specialty vendors.

Mandatory EHR / PACS Interoperability

The 21st Century Cures Act penalizes information blocking, forcing orthopedic groups to deploy standards-based solutions capable of exchanging clinical data across disparate systems.[2]U.S. Department of Health & Human Services, “21st Century Cures Act Information Blocking Final Rule,” hhs.gov Practices now prioritize FHIR-enabled platforms that integrate radiology images, operative notes, and billing details in a single record. Vendors offering turnkey APIs gain preference as clinics weigh compliance risk against cost.

3-D Digital Templating Proven to Cut Implant Revision Rates

Evidence shows 3-D planning reduces revision surgeries, which cost hospitals two to three times more than primary procedures. AI-assisted templating aligns pre-operative planning with intra-operative robotic guidance, delivering sub-millimeter precision. Economic payback strengthens when templating data feed custom implant workflows that reduce inventory waste and post-op complications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of orthopedic informatics & imaging IT specialists | -1.5% | Global — acute in rural and emerging markets | Long term (≥ 4 years) |

| High capital cost and workflow disruption during system migration | -1.2% | Global — smaller practices most affected | Short term (≤ 2 years) |

| Complex HIPAA / GDPR compliance for cloud data hosting | -0.8% | North America & EU regulatory zones | Medium term (2-4 years) |

| Soaring cyber-insurance premiums after ransomware incidents | -0.6% | Global — developed markets see largest hikes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Orthopedic Informatics & Imaging IT Specialists

Advanced EHR rollouts require up to 153,114 additional IT full-time equivalents worldwide, yet training pipelines lag demand. Specialty clinics in rural settings depend on vendor services, elevating deployment cost and elongating timelines. Vendors that bundle implementation, training, and managed services thus gain a strategic edge.

Soaring Cyber-Insurance Premiums after Ransomware Incidents

The February 2024 Change Healthcare breach compromised 190 million patient records and elevated cyber-insurance premiums by 25-50%.[3]Change Healthcare Cybersecurity Update, “Impact Analysis of the February 2024 Ransomware Event,” bankinfosecurity.com Small orthopedic groups struggle to finance coverage that now requires multi-factor authentication, zero-trust architectures, and vendor redundancy proofs. Software suppliers with robust encryption and certified security programs are increasingly specified in procurement tenders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Templating Sets the Benchmark for Clinical Precision

Digital templating held a 35.12% orthopedic software market share in 2025, reflecting its proven ability to lower revision rates and trim operating-room minutes. The sub-segment benefits from AI image-segmentation modules that learn from prior cases, yielding standardized implant plans and reducing inter-surgeon variability. Orthopedic PACS is projected to post a 9.52% CAGR, fueled by climbing MRI and CT volumes and regulatory moves to eliminate film. Revenue-cycle tools remain essential as value-based contracts rise, while integrated EHRs embed specialty decision support tailored to musculoskeletal workflows. Patient-engagement apps that sync rehab milestones into the clinical record close the feedback loop, supporting bundled-payment compliance.

Complementary modules converge around an open-API backbone that unifies scheduling, imaging, and OR inventory control. Vendors now deploy cloud functions for 3-D rendering, offloading compute workload from local servers. As digital templating exports structured data to robotics consoles, intra-operative adjustments shrink and post-operative alignment scores improve. The Orthopedic software market size tied to templating and PACS is forecast to expand at a steady 8-9% pace, underpinned by a backlog of elective cases deferred during pandemic years.

By Mode of Delivery: Cloud Dominance Accelerates Scalability

Cloud deployments comprised 58.74% of the orthopedic software market in 2025 and are tracking an 11.42% CAGR to 2031. Subscription pricing aligns with ASC cashflows and shields smaller clinics from large capital outlays. Vendors emphasize zero-downtime upgrades and encrypted edge-to-cloud sync, overcoming earlier fears of latency and data sovereignty. Hybrid models remain relevant for academic centers that house sensitive research images onsite while using cloud analytics for AI model-training.

On-premise systems persist where wide-area bandwidth is limited or data guardianship rules forbid offsite storage. Even here, suppliers offer modular gateways that mirror datasets to disaster-recovery clouds. As public cloud providers win HIPAA and GDPR attestations, holdouts are expected to convert. The Orthopedic software market size attributed to cloud software will likely exceed USD 407.8 million by 2031 if current adoption curves hold.

By Application: Fracture Management Leads Future Growth

Orthopedic surgery applications generated the largest revenue share at 36.12% in 2025, yet fracture management will lead expansion with a 12.04% CAGR. AI algorithms that spot subtle cortical disruptions on X-ray and quantify callus formation on follow-up CT foster earlier interventions and optimized fixation strategies. Joint-replacement modules harness robotic navigation to improve cup and stem orientation, while pediatric assessment tools automate bone-age scoring, supporting endocrine-orthopedic collaboration.

Sports-medicine clinics integrate wearable telemetry with postoperative dashboards, extending visibility into at-home rehabilitation. Such end-to-end datasets feed predictive analytics that flag patients at risk of delayed union or prosthesis loosening. The Orthopedic software market share linked to fracture management will widen as trauma volumes climb in rapidly urbanizing economies.

By End User: Clinics Outpace Hospitals in Percentage Growth

Hospitals represented 55.02% of 2025 spending, reflecting enterprise-wide rollouts that integrate imaging, operative, and billing workflows. Yet independent orthopedic clinics will see the fastest 13.21% CAGR through 2031 as they invest in specialty EHRs to secure payer recognition and compete with health-system-owned practices. ASC operators prize cloud deployment for rapid scaling into newly accredited procedure rooms. Academic institutes leverage open-source APIs for research analytics and AI validation, forging partnerships with software vendors to co-develop algorithms.

Smaller practices gravitate toward turnkey platforms bundling digital templating, practice management, and patient engagement in one contract. This reduces vendor sprawl and simplifies cyber-insurance compliance. The Orthopedic software market size derived from clinics is forecast to nearly double within five years, cementing them as a vital growth channel for suppliers.

Geography Analysis

North America accounted for 39.33% of total revenue in 2025 thanks to established reimbursement pathways and mature cloud infrastructure. U.S. Medicare policies reward digital documentation that supports quality metrics, encouraging practices to adopt integrated solutions. Canada’s provincial mandates for electronic data sharing further entrench demand, and cross-border vendor relationships ease technology transfers.

Asia-Pacific is registering the strongest 12.79% CAGR. China’s Healthy China blueprint funds digital health pilots, positioning provincial hospitals as early adopters. Japan utilizes robotics and AI to offset surgical labor shortages, while India’s public-private partnerships finance cloud EHRs in tertiary trauma centers. Regional heterogeneity favors modular, language-localised platforms that comply with divergent privacy statutes.

Europe’s steady adoption is led by Germany, where federal grants subsidize orthopedic digitization in clinics complying with stringent GDPR controls. The U.K.’s NHS Interoperability program specifies FHIR messaging for orthopedic referrals, giving vendors with proven data-exchange workflows a head start. France channels innovation budgets toward coordinated care networks that require real-time image routing from outpatient radiology to orthopedic wards. Across the bloc, evidence of lower revision rates is pivotal to investment sign-off, placing data-rich suppliers in an advantageous position.

Regulatory Landscape

In the United States, orthopedic software that functions as a medical device is being shaped by FDA guidance that clarifies quality expectations and the boundary between regulated and non-regulated clinical functionality. In February 2026, the FDA finalized guidance on Computer Software Assurance for production and quality management system software, reinforcing a risk-based approach to software used in quality processes that underpin compliant releases and post-market updates. In January 2026, the FDA also updated its Clinical Decision Support (CDS) Software guidance, clarifying which CDS functions can be excluded from the device definition under the 21st Century Cures Act, which affects how orthopedic planning and decision-support features are positioned and documented.

Regulatory requirements are tightening for software that supports patient-specific orthopedic workflows and for cybersecurity-ready submissions. In May 2026, the FDA issued final guidance on Patient-Matched Guides for Orthopedic Implants, which affects pre-operative planning and workflows that connect imaging, planning software, and patient-matched instrumentation. In Europe, the European Commission proposed EU MDR 2026 amendments that include fixed assessment timelines and digital submission mandates via EUDAMED, alongside proposed certificate extensions (Class IIa through December 2028 and Class IIb through December 2030), which impacts conformity planning and post-market data handling for SaMD-like orthopedic modules. Globally, IMDRF activity around SaMD lifecycle controls, including work on Predetermined Change Control Plans (PCCPs) targeted for a September 2026 submission, supports faster iteration pathways for AI-enabled planning software where updates are frequent but need structured change governance.

Competitive Landscape

Competitive rivalry is moderate. Top hardware incumbents leverage installed imaging bases to upsell software overlays, while independent developers win share in niche areas like pediatric templating. Stryker’s six acquisitions averaged USD 817 million in 2024, adding AI navigation to its Mako platform and broadening its software stack. GE HealthCare’s Genesis launch illustrates hardware-agnostic imaging SaaS, aiming to triple cloud-enabled modules by 2028. Brainlab’s planned EUR 200 million IPO underscores the shift toward subscription revenue and continuous feature rollout.

White-space gaps persist in low-resource markets and subspecialties such as limb deformity analysis. New entrants deliver API marketplaces where third-party apps plug into core records, creating an ecosystem effect that entrenches platform providers. Partnerships between device makers and cloud hyperscalers accelerate AI model training and global distribution, while cybersecurity remains a gating criterion for contract awards.

Orthopedic Software Industry Leaders

Materialise NV

GE Healthcare

Medstrat Inc.

IBM Corporation (Merge Healthcare Inc.)

Brainlab

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Provider demand is shifting from point solutions toward longitudinal, workflow-integrated platforms that connect pre-op planning, intraoperative assistance, and post-op monitoring. This creates openings for vendors that can deliver interoperable modules across settings such as ASCs and multi-site orthopedic groups. ModMed's June 2026 enterprise-wide rollout of its AI-Powered Practice across U.S. Orthopaedic Partners (over 55 locations and 300 providers) is a concrete sign of that platform consolidation, reflecting buyer appetite for standardized templates, documentation automation, and operational tooling deployed at scale. It also expands whitespace for orthopedic-specific EHR, scheduling, and revenue-cycle features that plug into imaging and planning, particularly as clinics look for turnkey deployment to offset the shortage of orthopedic informatics specialists.

Reimbursement and connected-care pilots are further broadening the addressable surface for software that supports recovery tracking and documentation. CMS implemented new and updated Remote Patient Monitoring billing codes in January 2026, strengthening the business case for orthopedic patient-engagement and monitoring workflows that can feed structured data back into the clinical record and billing. On the technology side, device and software ecosystems are incorporating AI to compress planning and navigation steps, illustrated by Johnson and Johnson MedTech's June 2026 launch of Velys Hip Navigation with AI Assistance in the United States after FDA 510(k) clearance; the reported workflow-time reduction claims support procurement interest in measurable efficiency outcomes. Together, these shifts increase opportunity for vendors offering open APIs, FHIR-ready interoperability, and security-forward cloud deployments that reduce migration friction while supporting integrated perioperative datasets.

Recent Industry Developments

- June 2026: GE HealthCare received US FDA 510(k) clearance for MIM Contour ProtegeAI+ 2.0, an AI-enabled auto-contouring software used in treatment planning workflows. The clearance included a Predetermined Change Control Plan, signaling a more structured path for iterative AI model updates and strengthening confidence in regulated AI software maintenance practices that influence broader imaging-software procurement.

- March 2025: GE HealthCare launched the Genesis portfolio, a cloud suite of enterprise imaging SaaS capabilities spanning edge data management, cloud storage, vendor-neutral archive, and AI-enabled data migration. The release supports orthopedic imaging modernization by lowering barriers to cloud adoption for image-intensive workflows that need scalable storage and cross-site access.

- March 2024: Pixee Medical announced the commercial availability of its Knee+ AR computer-assisted solution in the United States for ambulatory surgical centers, featuring real-time 3D positioning through smart glasses. Commercial availability in ASC settings strengthens the pull-through for preoperative planning and imaging-data preparation that must integrate efficiently with lightweight intraoperative guidance workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers software used to plan, document, manage, and bill orthopedic care, from pre-op templating and surgical planning through imaging, clinic workflows, and revenue cycle tasks across provider settings.

Scope exclusions: We exclude orthopedic-capable general hospital IT that is not configured or sold as an orthopedic-focused product, and we also exclude implant hardware, robotics, and navigation systems unless the revenue is clearly for software licenses or subscriptions.

Segmentation Overview

- By Product Type

- Digital Templating / Pre-operative Planning

- Orthopedic EHR

- Orthopedic Practice Management

- Orthopedic PACS

- Revenue Cycle Management

- Other Software

- By Mode of Delivery

- Cloud / Web-based

- On-premise

- By Application

- Orthopedic Surgery

- Fracture Management

- Joint Replacement

- Pediatric Assessment

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Orthopedic Clinics

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to pin down the demand backdrop for orthopedic care and the digital workflow intensity around it, which then shaped the market boundaries and input assumptions. We leaned on non-paywalled sources such as the US Centers for Medicare and Medicaid Services procedure and payment references, CDC utilization statistics, OECD health datasets, and World Bank macro indicators to keep volumes and affordability signals grounded.

To connect demand with software spending logic, we also reviewed sources such as clinical guideline publications in peer reviewed orthopedic journals, orthopedic society websites, and hospital annual reports and investor presentations that discuss digitization and productivity targets. A paid subscription for company financials and a general news and financials database helped verify business mix language, regional exposure, and acquisition activity that can shift reported revenue lines. The desk sources listed here are illustrative only, and many additional public references were also checked to clarify definitions and validate assumptions.

Primary Interviews and Surveys

Primary work focused on confirming what orthopedic providers actually buy, how modules are packaged, and how pricing tends to move between new sales and renewals, since these points are not fully visible in public data. We spoke with a mix of software suppliers, channel partners, hospital IT and orthopedic department stakeholders, and ambulatory orthopedic clinic operators across major regions. The goal was to pressure test adoption rates, deployment mix (cloud versus on-premise), and realistic upgrade cycles tied to care site operations.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 17% | APAC: 48% |

| Mid tier: 53% | Functional/Unit leaders: 29% | EMEA: 29% |

| Smaller Players: 17% | Managers: 54% | Americas: 23% |

Market-Sizing & Forecasting

Our model uses a top-down build that reconstructs the addressable software spend from orthopedic procedure volumes and the number of active care sites, which is then filtered by workflow digitization and module penetration. The result is then corroborated with selective bottom-up approximations, such as sampled vendor revenue disclosures, channel checks on typical subscription or license pricing, and sanity checks on installed base by care setting.

Inputs that mattered in this market included annual orthopedic surgery volumes (especially joint replacement and trauma), the split of cases handled in hospitals versus ambulatory surgical centers, the share of sites using orthopedic specific planning or imaging modules, cloud adoption rates and typical contract durations, and pricing progression for seats and modules when practices add surgeons or locations. Where vendor revenue is bundled across broader imaging or hospital IT lines, allocation was handled through stated product mix, triangulated with interview feedback and observed module attach patterns.

For forecasting, we relied on scenario analysis supported by trend lines in procedure growth, site expansion, and digitization intent, and then adjusted the yearly path based on expert views around reimbursement pressure, staffing shortages, and replacement cycles for legacy systems. The forecast was kept repeatable by tying every growth driver back to an observable indicator and documenting the assumption that links it to software spend.

Data Validation & Update Cycle

Validation is done through a set of cross checks that compare the model output with independent signals, such as procedure growth, provider count trends, and the pace of cloud migration discussed by buyers and implementers. When a variance shows up, the assumptions are reviewed step by step, and targeted follow ups are triggered with respondents who can explain whether the issue is scope, pricing, or adoption timing.

Before sign-off, the numbers go through internal analyst reviews focused on year to year continuity, currency consistency, and whether changes are explainable through the tracked variables. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory shifts, pricing model changes, or notable product consolidation. Right before delivery, a final check is done so clients receive the latest updated view.

Mordor Intelligence's Orthopedic Software Market Size Versus Other Published Estimates

It is normal to see different market size values for orthopedic software because each publisher draws the scope line differently and uses its own timing, pricing, and adoption assumptions. In this market, the largest swings usually come from what is counted as orthopedic specific software versus broader hospital IT, and whether services and implementation revenue are included in full.

By tracking procedure volumes, care site counts, and module level adoption, Mordor Intelligence keeps the model tied to provider demand signals, and then avoids inflating totals by separating orthopedic focused software revenue from adjacent imaging or general EHR spend that is not sold as an orthopedic product.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 439.01 M (2026) | |

| Global Consultancy A | USD 356.21 M (2024) | Uses an earlier base year and a broader segmentation that can blend orthopedic modules with general PACS or hospital IT lines, which can shift what gets allocated into the orthopedic software total. |

| Industry Publisher B | USD 419.50 M (2024) | Extends the forecast window and may apply a higher long-run pricing and adoption trajectory, and it is not always clear how implementation and support services are treated versus recurring software revenue. |

The comparison shows that timing, boundary choices, and how mixed revenue lines are handled explain most of the spread. When the scope is kept specific to orthopedic workflows and the growth path is anchored to observable demand and adoption indicators, the final number becomes easier to reproduce and easier for decision makers to use.

Key Questions Answered in the Report

What is the current size of the Orthopedic software market?

The Orthopedic software market is valued at USD 439.01 million in 2026 and is projected to reach USD 621.93 million by 2031.

Which product segment leads the Orthopedic software market?

Digital templating holds the top position with 35.12% share in 2025, owing to its success in cutting implant revision rates.

How fast is cloud deployment growing in orthopedic software?

Cloud-based solutions are expanding at an 11.42% CAGR and already account for 58.74% of 2025 revenue.

Why is fracture management software gaining traction?

AI algorithms detecting fractures with over 90% accuracy and rising trauma cases support a 12.04% CAGR in this application.

Which region offers the highest growth potential?

Asia-Pacific shows a 12.79% CAGR through 2031, fueled by government digitization initiatives in China, Japan, and India.

Page last updated on: