AI In Product Lifecycle Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

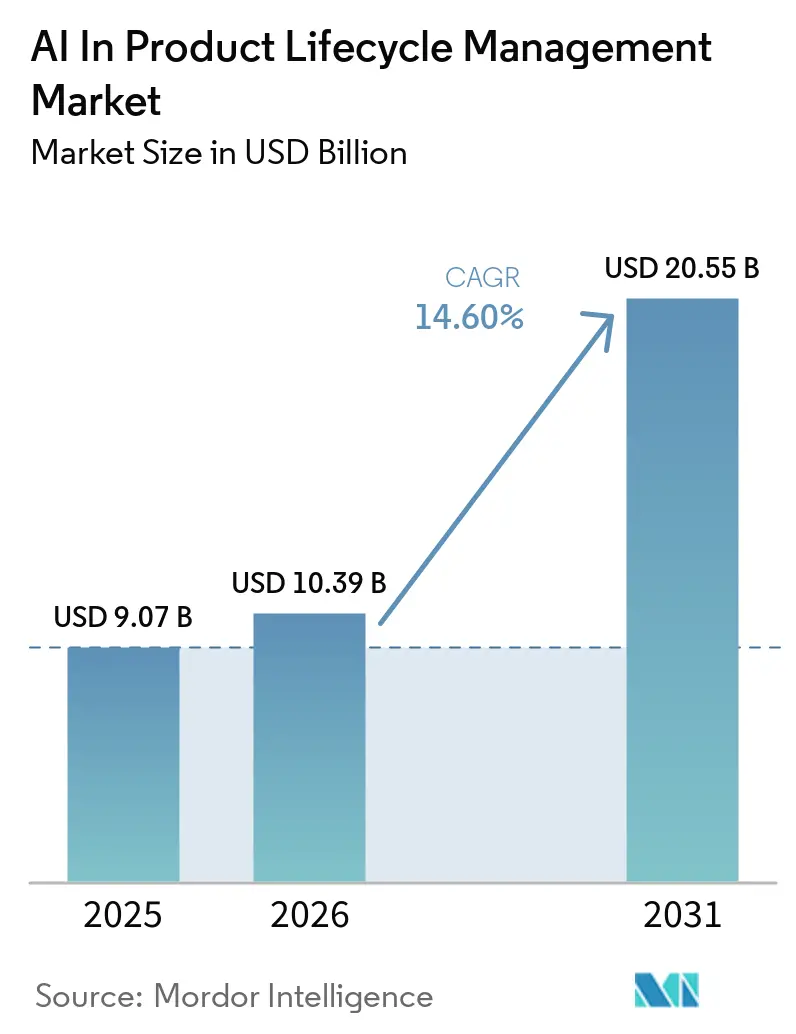

| Market Size (2026) | USD 10.39 Billion |

| Market Size (2031) | USD 20.55 Billion |

| Growth Rate (2026 - 2031) | 14.60% CAGR |

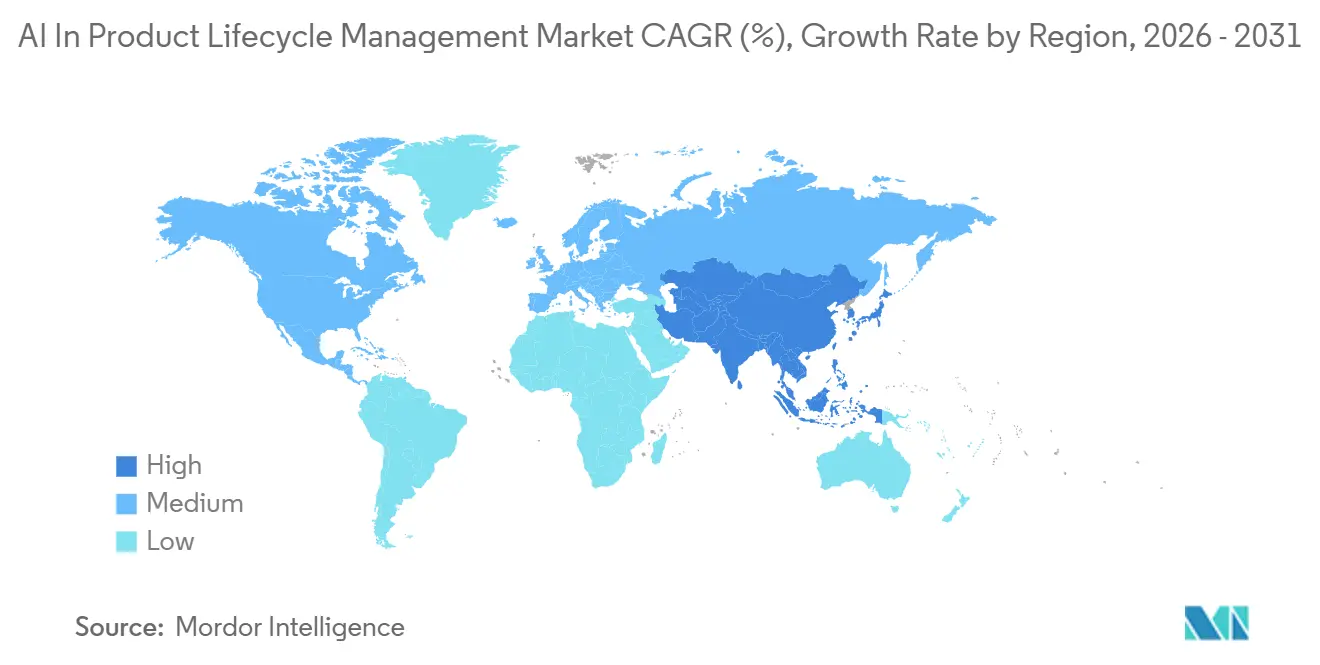

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Product Lifecycle Management Market Analysis by Mordor Intelligence

The AI In Product Lifecycle Management Market size is projected to expand from USD 9.07 billion in 2025 and USD 10.39 billion in 2026 to USD 20.55 billion by 2031, registering a CAGR of 14.60% between 2026 to 2031.

Growing product complexity, rapid migration to cloud-native platforms, and the embedding of generative AI copilots into engineering workflows keep spending momentum high across industrial sectors. Enterprise budgets that once followed multi-year upgrade cycles now shift toward continuous subscription payments for AI layers that deliver measurable value in months rather than years. Vendors respond by bundling outcome-based AI services alongside core PLM seats, encouraging broader adoption even among cautious late movers. North American manufacturers remain the early majority, yet the fastest incremental growth is emerging in Asia-Pacific where electric-vehicle and electronics supply chains scale quickly. These dynamics sustain double-digit expansion and reinforce the centrality of data-driven engineering across the global AI in product lifecycle management market.

Key Report Takeaways

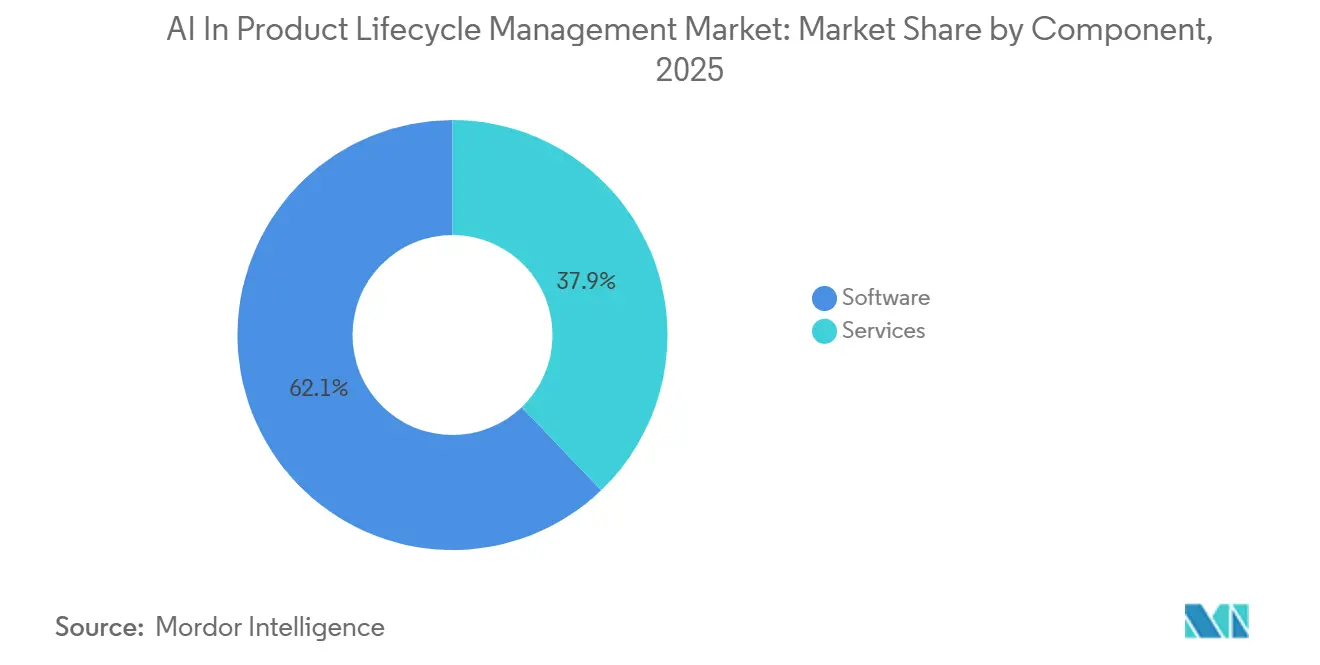

- By component, software led with 62.15% of the AI in product lifecycle management market share in 2025, while services recorded the highest projected CAGR at 15.95% through 2031.

- By deployment mode, cloud/SaaS captured 54.15% of the AI in product lifecycle management market size in 2025 and is forecasted to expand at a 16.15% CAGR between 2026 and 2031.

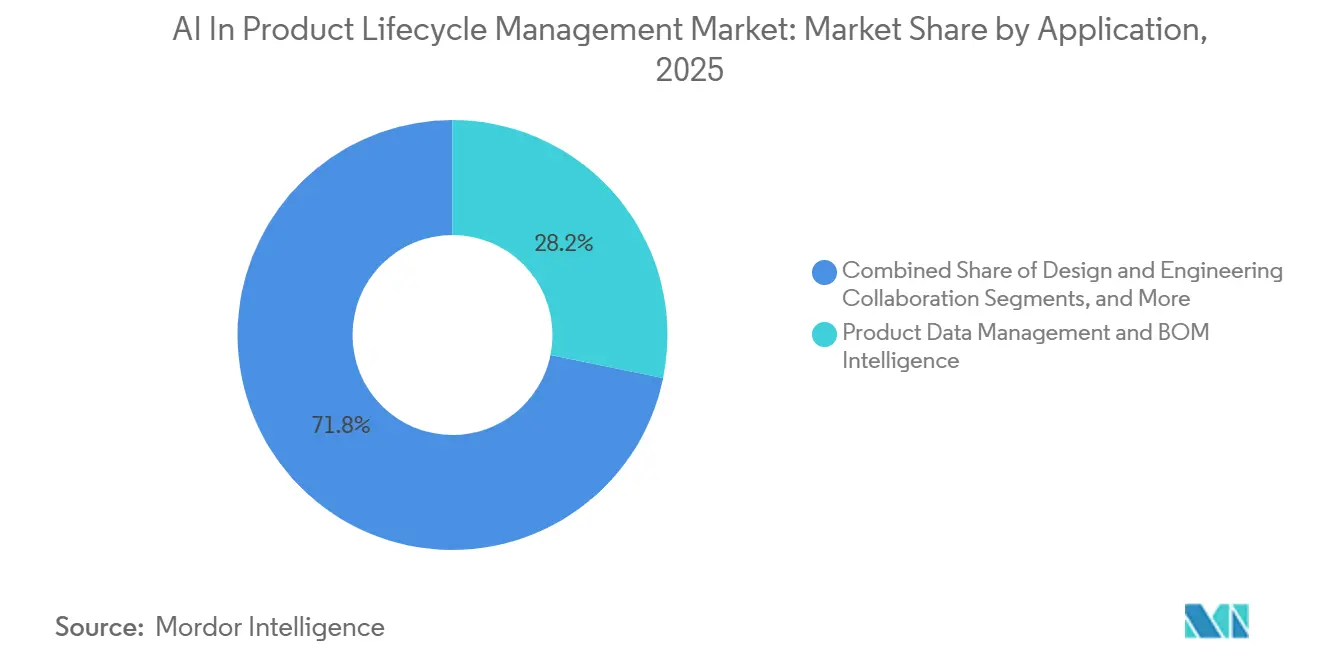

- By application, quality, compliance, and traceability posted the fastest growth at a 15.75% CAGR to 2031; product data management held 28.2% of the AI in product lifecycle management market share in 2025.

- By end user, automotive and transportation accounted for 22.62% of the 2025 revenue base, whereas healthcare and medical devices are expected to grow at 16.45% CAGR to 2031.

- By geography, North America accounted for 38.65% of the 2025 revenue base, whereas healthcare and medical devices are expected to grow at 16.50% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Product Lifecycle Management Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising product complexity and multi-domain engineering | +2.5% | Global, concentrated in automotive and aerospace | Long term (≥ 4 years) |

| Shorter time-to-market and change-cycle latency | +2.0% | Global, strongest in North America and Europe | Medium term (2–4 years) |

| Cloud/SaaS PLM modernization and digital thread buildout | +2.8% | Global, advanced in North America and DACH | Short term (≤ 2 years) |

| Compliance automation, traceability, and quality needs | +2.3% | Healthcare and aerospace hubs | Medium term (2–4 years) |

| AI-powered sustainability and LCA inside PLM | +1.8% | Europe and North America | Long term (≥ 4 years) |

| AI conversion of legacy engineering documents | +1.4% | Global, large OEM estates | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Cloud/SaaS PLM Modernization and Digital Thread Buildout

Cloud-native infrastructure enables compute-intensive tasks, such as large-scale BOM semantic searches and real-time visual similarity checks, which are integral to AI in product lifecycle management. Over half of new Aras Innovator deployments now operate as SaaS, including defense-grade GovCloud instances that meet ITAR and CMMC requirements. This shift reduces entry barriers for mid-sized firms by eliminating significant upfront server investments. It also ensures standardized security updates and performance enhancements, allowing engineering teams uninterrupted access to the latest AI models. Vendors are increasingly introducing usage-based AI micro-services, priced separately from core PLM licenses, driving additional revenue growth beyond traditional user-based metrics.

Compliance, Traceability, and Quality Automation Needs

Regulators now require manufacturers to maintain comprehensive digital audit trails that document every requirement, design decision, and validation artifact. The U.S. FDA's Quality Management System Regulation, effective February 2026, expands oversight to include AI-enabled production software, making AI-native PLM essential for compliance in the med-tech industry.[1]U.S. Food and Drug Administration, “Computer Software Assurance for Production and Quality Management System Software,” fda.gov In response, PTC has introduced Codebeamer AI assistants that automatically generate test cases aligned with industry standards, reducing manual traceability efforts by nearly 50%. Similar functionalities are being integrated into the portfolios of other vendors, such as Dassault Systèmes and Siemens, as they embed risk-scoring logic into engineering workflows. These advancements streamline validation cycles across life-sciences supply chains and allow quality engineers to focus on higher-value analytical tasks.

Rising Product Complexity and Multi-Domain Engineering

Software-defined vehicles, electrified propulsion systems, and additive manufacturing are creating new interdependencies among mechanical, electrical, and software components. A 2026 survey revealed that 59% of respondents identified multidisciplinary coordination as the primary risk to project schedules.[2]Siemens AG, “Digital Engineering Trends Survey 2026,” siemens.com AI tools capable of analyzing diverse CAD, ECAD, and MBSE data now suggest design corrections before release, significantly reducing rework. Venture-backed companies like SPREAD AI are transforming legacy datasets into graph structures, enabling rapid root-cause analysis across complex subsystem interactions. These innovations result in fewer late-stage changes and shorter prototype cycles, sustaining demand for AI-driven product lifecycle management solutions.

Need to Shorten Time-to-Market and Change-Cycle Latency

Achieving a competitive advantage often depends on launching a product one quarter ahead of competitors. AI-powered ECO impact analysis accelerates approval processes by providing engineering managers with risk-ranked action plans based on historical change data. PTC's Windchill AI Parts Rationalization has demonstrated up to a 60% reduction in manual duplicate searches since its launch in January 2026.[3]PTC Inc., “Windchill AI Parts Rationalization Launch,” ptc.com Systems integrators report similar efficiencies when PLM data integrates seamlessly with ERP and MES systems, ensuring procurement and shop-floor operations are updated with the latest revisions on an hourly basis rather than weekly. This reduction in cycle times drives revenue growth and supports platform upgrade investments, even during periods of economic uncertainty.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Legacy integration and fragmented data models | −1.8% | Global, acute in long-lived OEM estates | Medium term (2–4 years) |

| IP security, governance, and explainability requirements | −1.5% | Aerospace, defense, and semiconductor clusters | Medium term (2–4 years) |

| Copilot-in-a-silo across PLM / ERP / MES / ALM Ecosystems | −1.2% | Enterprises with heterogeneous stacks | Medium term (2–4 years) |

| Governance embedding and stale lifecycle context | −0.9% | Hybrid on-prem and cloud estates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy System Integration and Fragmented Data Models

Many large manufacturers, having acquired multiple PLM instances through mergers, face challenges with inconsistent part numbering systems and revision methodologies. Consolidating these disparate systems into a unified semantic layer requires significant investment in mapping processes, which is essential for AI to generate actionable and traceable insights. On average, data-conversion projects at automotive Tier-1 suppliers now take approximately 18 months to complete and account for 4% of annual engineering IT budgets. While graph-based knowledge layers offer a viable solution, most Fortune 500 OEMs anticipate this transition extending into their next planning cycle.

IP Security, Governance, and Explainability Requirements

Product source files, geometry tolerances, and simulation parameters are critical intellectual property assets. As a result, executives demand cryptographically secure access logs and transparent AI systems capable of justifying design recommendations. In recent years, advancements in compliance credentials have positioned companies to meet stringent procurement requirements in industries such as aerospace. Additionally, explainable AI tools now provide clear, human-readable rationales for part substitution recommendations, aligning with regulatory standards in sectors like medical devices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Anchors Platform Consolidation

In 2025, software held a 62.15% revenue share in the AI-driven product lifecycle management market. This dominance is primarily due to AI capabilities integrated into major PLM suites, including Siemens' Teamcenter, Dassault Systèmes' 3DEXPERIENCE, and PTC's Windchill. Features such as voice-driven BOM navigation, generative design sketches, and automated requirement summarization not only ensure seat renewals but also drive expansion into new accounts.

While service revenue is smaller in absolute terms compared to licenses, it is growing at a faster pace. Systems integration specialists focus on re-platforming historical data, managing cloud migrations, and optimizing large-language-model prompts to align with client-specific taxonomies. These services often extend beyond the initial implementation phase, evolving into managed service subscriptions aligned with the customer’s AI model refresh cycles. This trend supports a 15.95% CAGR for services, surpassing overall market growth while reinforcing the dominance of established platforms.

By Deployment Mode: Cloud-Native Platforms Unlock AI at Scale

In 2025, cloud and SaaS deployments accounted for 54.15% of total spending, with this share expected to grow as compute-intensive tasks increasingly rely on elastic infrastructures. The market size for AI in product lifecycle management driven by cloud deployments is projected to grow at a 16.15% CAGR through 2031. Multitenant architectures enable vendors to deliver weekly model updates without disrupting customer operations, a capability that is challenging to replicate on self-hosted servers.

Hybrid strategies, commonly adopted by Japanese and German OEMs, combine local control for sensitive files with on-demand GPU resources for tasks such as simulation and generative design. Tesla’s use of Dassault Systèmes' 3DEXPERIENCE in a containerized on-premises instance highlights how high-volume manufacturers prioritize low latency and consistent throughput. Over time, software vendors are introducing secure edge appliances that synchronize only non-sensitive data to the public cloud, gradually encouraging conservative users to adopt broader SaaS solutions and expanding the market.

By Application: Product Data Management Anchors the AI Foundation

Product data management accounted for 28.2% of 2025's revenue, emphasizing its critical role as the foundation for downstream AI tasks. Reliable metadata enables engineers to efficiently source interchangeable fasteners or perform cost roll-ups across global BOMs, reducing decision-making time and minimizing rework. As organizations transition from pilot projects to enterprise-wide implementations, the market size for product data management in AI-driven lifecycle management continues to grow steadily.

Applications focused on quality, compliance, and traceability are experiencing faster growth, with a projected CAGR of 15.75%. Regulatory bodies now emphasize the importance of validating software changes through AI-enabled traceability matrices that link requirements to tests in real time. Engineers in aerospace and defense face similar compliance pressures. As vendors integrate exportable evidence packs into PLM reports, adoption rates increase, driving the overall market growth trajectory.

By End User: Automotive Leads in Volume, Healthcare in Urgency

In 2025, the automotive and transportation sectors accounted for 22.62% of spending, driven by the scale of global model platforms and the need for synchronized updates. Leading OEMs are leveraging enterprise-private LLM projects to transform tacit knowledge into searchable formats. This innovation reduces change-approval cycles from days to hours, anchoring the market in automotive innovation hubs.

The healthcare sector, driven by new regulatory requirements, is experiencing the highest growth rate with a 16.45% CAGR. These regulations place digital evidence management at the core of regulatory approvals. Smaller device manufacturers, previously slower to adopt PLM, now prioritize AI-ready PLM systems as a critical factor for investor confidence. This urgency is channeling investments into advanced cloud solutions and increasing demand for specialized consultancy services, further expanding the market into previously underserved segments.

Geography Analysis

In 2025, North America commanded a dominant 38.65% share of global revenue, spearheaded by sectors such as aerospace, defense, semiconductors, and electric vehicles, all of which prioritize stringent engineering change controls. Federal procurement policies favoring digital-thread maturity, combined with the FDA's 2026 release of the Computer Software Assurance guidance, establish a foundational compliance standard. This standard ensures project funding continuity and provides a buffer during broader economic slowdowns. Additionally, the region's robust presence of cloud hyperscalers accelerates the realization of value from generative AI pilots, solidifying its lead in the AI-driven product lifecycle management arena.

Europe, while currently holding the second spot in spending, is on a rapid ascent. This surge is largely attributed to the EU's impending Digital Product Passport and Ecodesign regulations, which are seamlessly integrating lifecycle assessments into design processes. The DACH region, already home to some of the densest Product Lifecycle Management (PLM) systems globally, stands to gain significantly. By infusing AI intelligence into these existing systems, they can expect immediate reductions in cycle times. Notably, Dassault Systèmes highlighted an 8% year-on-year growth in its European Industrial Innovation software revenue for Q3 2025, a surge directly tied to AI-driven license upgrades.

Asia-Pacific is set to be the powerhouse of the AI-driven product lifecycle management market, boasting a projected CAGR of 16.50%. In China, battery-electric vehicle manufacturers are swiftly adopting AI-centric PLM strategies to expedite model iterations. Japanese OEMs are navigating data residency challenges, opting for a phased cloud strategy. They often choose hybrid models, retaining geometry data onshore while leveraging regional data centers for intensive computational tasks. In India, engineering service firms are developing PLM-AI tools, streamlining migration processes for Western clients. This not only underscores India's significance as a PLM adopter but also as a key exporter of PLM expertise.

Competitive Landscape

Siemens, Dassault Systèmes, PTC, and SAP dominate the market, collectively accounting for over half of the global license revenue. These industry leaders are embedding generative copilots into design authoring, issue resolution, and compliance reporting, thereby strengthening their competitive advantages. in 2024, Dassault Systèmes introduced a new monetization strategy with its outcome-based "Virtual Twin as a Service" model, which separates AI services from traditional seat licenses. Similarly, PTC launched its "Windchill AI Assistant" in April 2026, combining conversational search with agents designed for parts rationalization.

There's potential in cross-system orchestration, where emerging startups are integrating data from PLM, ERP, MES, and ALM into unified knowledge graphs. In April 2026, SPREAD AI and Synera each secured over USD 30 million in Series B funding to develop low-code connectors, streamlining data migration. Instead of building in-house, major software firms are forming partnerships: IBM's acquisition of Cognitus in October 2025 enhanced its consulting division with industry-specific AI services. This trend highlights a moderate consolidation in the market: while established PLM vendors maintain platform dominance, the focus is shifting toward specialized AI services, fostering a dynamic competitive environment in AI-driven product lifecycle management.

AI In Product Lifecycle Management Industry Leaders

Oracle

SAP

Wipro

Capgemini

Accenture

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Synera raised USD 40 million in Series B funding led by Revaia and Capgemini to scale its agentic AI engineering platform, which links over 80 tools including Siemens and PTC suites.

- April 2026: SPREAD AI secured USD 30 million in Series B financing led by OTB Ventures and Salesforce Ventures to expand its product twin ontology across automotive and aerospace accounts.

- April 2026: PTC introduced Windchill AI Assistant, adding natural-language product data search and summarization to its PLM suite, with future extensions into change-management automation.

- April 2026: Oracle released Design-to-Source Workspace within Fusion Agentic Applications, employing AI to translate engineering intent into supplier proposals while simulating cost-lead-time tradeoffs.

- March 2026: Dassault Systèmes demonstrated AI-powered virtual twins at NVIDIA GTC, advancing an industrial AI platform that marries accelerated computing with domain-specific world models.

Global AI In Product Lifecycle Management Market Report Scope

As per the scope of the report, AI in Product Lifecycle Management (PLM) is the integration of machine learning and automation into PLM systems to enhance decision-making, speed up product development, and manage data from conception to end-of-life. It transforms static systems of record into dynamic systems of intelligence, enabling generative design, predictive maintenance, and optimized supply chains.

The AI in Product Lifecycle Management market is segmented by component, deployment mode, application, end-user, and geography. By component, the market includes software and services. By deployment mode, the market is segmented into cloud/SaaS, on-premises, and hybrid. By application, the market is categorized into product data management & BOM intelligence, design & engineering collaboration, change, release & workflow automation, quality, compliance & traceability, digital twin, simulation & lifecycle analytics, portfolio, program & requirements management, and manufacturing handoff & closed-loop feedback. By end-user, the market is segmented into automotive & transportation, aerospace & defense, industrial equipment & heavy machinery, semiconductor & electronics, healthcare & medical devices, consumer goods, fashion & retail, chemicals & materials, and energy, utilities & infrastructure. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Software |

| Services |

| Cloud / SaaS |

| On-Premises |

| Hybrid |

| Product Data Management & BOM Intelligence |

| Design & Engineering Collaboration |

| Change, Release & Workflow Automation |

| Quality, Compliance & Traceability |

| Digital Twin, Simulation & Lifecycle Analytics |

| Portfolio, Program & Requirements Management |

| Manufacturing Handoff & Closed-loop Feedback |

| Automotive & Transportation |

| Aerospace & Defense |

| Industrial Equipment & Heavy Machinery |

| Semiconductor & Electronics |

| Healthcare & Medical Devices |

| Consumer Goods, Fashion & Retail |

| Chemicals & Materials |

| Energy, Utilities & Infrastructure |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment Mode | Cloud / SaaS | |

| On-Premises | ||

| Hybrid | ||

| By Application | Product Data Management & BOM Intelligence | |

| Design & Engineering Collaboration | ||

| Change, Release & Workflow Automation | ||

| Quality, Compliance & Traceability | ||

| Digital Twin, Simulation & Lifecycle Analytics | ||

| Portfolio, Program & Requirements Management | ||

| Manufacturing Handoff & Closed-loop Feedback | ||

| By End User | Automotive & Transportation | |

| Aerospace & Defense | ||

| Industrial Equipment & Heavy Machinery | ||

| Semiconductor & Electronics | ||

| Healthcare & Medical Devices | ||

| Consumer Goods, Fashion & Retail | ||

| Chemicals & Materials | ||

| Energy, Utilities & Infrastructure | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the AI in product lifecycle management market today?

The AI in product lifecycle management market size reached USD 10.39 billion in 2026 and is forecast to climb to USD 20.55 billion by 2031 at a 14.6% CAGR.

Which segment is expanding fastest within the market?

Quality, compliance, and traceability applications are advancing at a 15.75% CAGR through 2031 as regulatory bodies tighten digital audit requirements.

What share of spending comes from software versus services?

Software generated 62.15% of 2025 revenue, while services, though smaller, are growing at a 15.95% CAGR as organizations seek data-engineering and model-monitoring support.

Which region is seeing the highest growth rate?

Asia-Pacific is projected to expand at 16.45% through 2031, driven by electric-vehicle manufacturing in China and engineering-services expansion in India.

How consolidated is vendor competition?

The four largest vendors hold around 60% of revenue, yielding a moderate concentration that still leaves room for cloud-native and AI-orchestration challengers to gain share.

What is the principal barrier to AI deployment in PLM?

Legacy data fragmentation remains the toughest hurdle; large OEMs must harmonize multi-decade BOM structures before AI can deliver reliable insights, keeping integration projects on the critical path.

Page last updated on: