On-demand Wellness Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

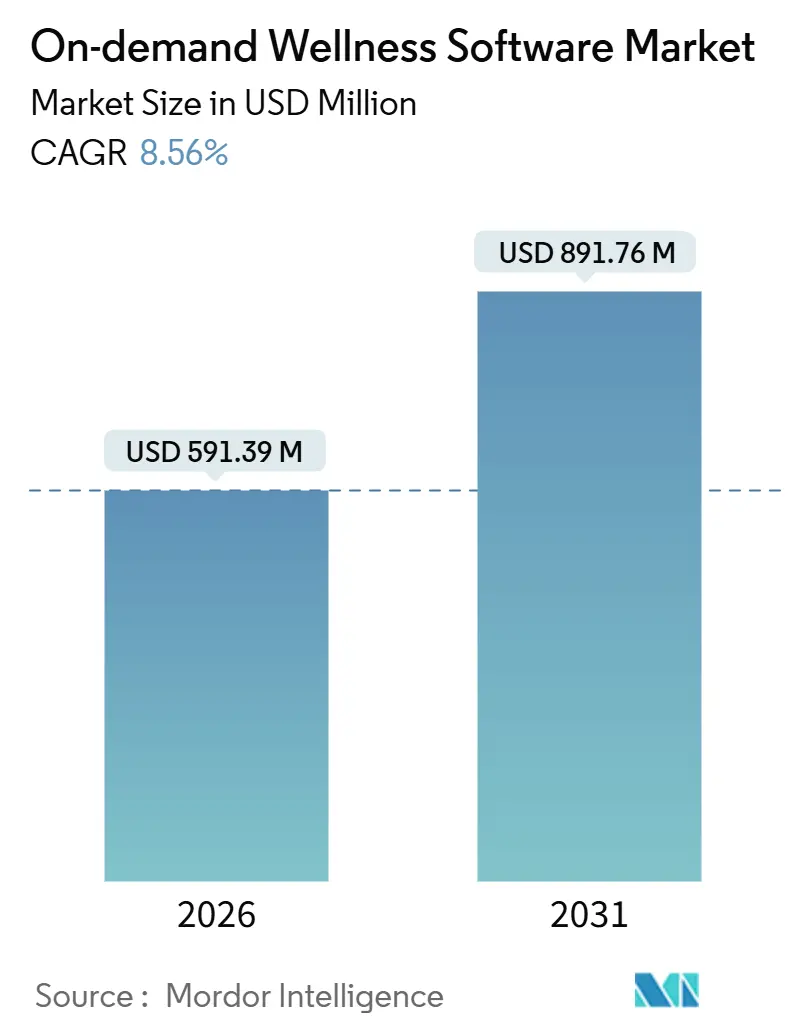

| Market Size (2026) | USD 591.39 Million |

| Market Size (2031) | USD 891.76 Million |

| Growth Rate (2026 - 2031) | 8.56% CAGR |

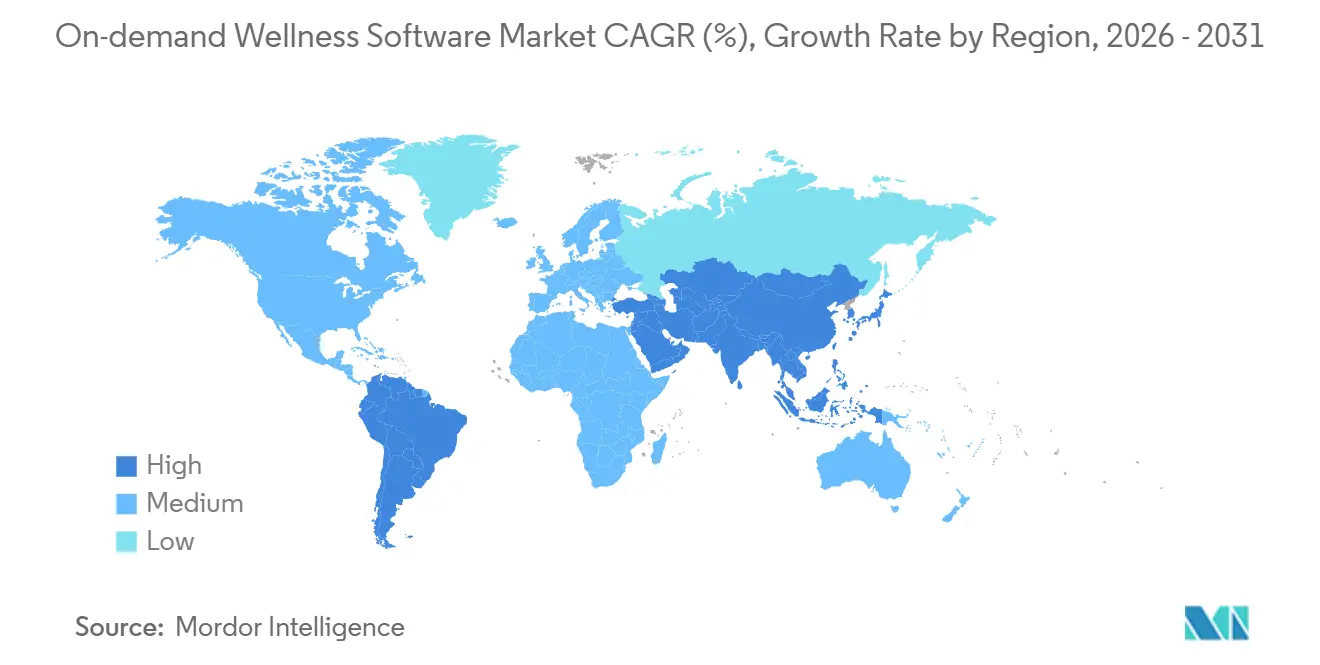

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

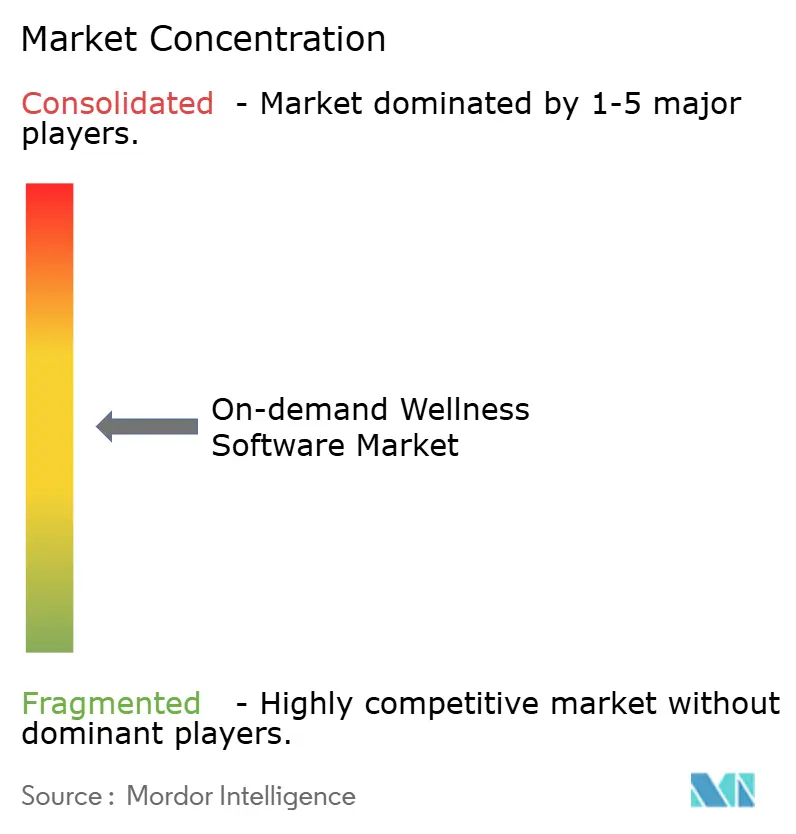

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

On-demand Wellness Software Market Analysis by Mordor Intelligence

The On-demand Wellness Software Market size is estimated at USD 591.39 million in 2026, and is expected to reach USD 891.76 million by 2031, at a CAGR of 8.56% during the forecast period (2026-2031).

It reflects a healthy expansion in the on-demand wellness software market. Rapid cloud adoption, aggressive enterprise spending on bundled wellness benefits, and investor appetite for vertically integrated SaaS stacks are the leading growth catalysts. Cloud deployment already accounts for two-thirds of global revenues, while analytics layers that convert raw booking data into pricing and retention insights have become the new competitive frontier. In parallel, employer wellness budgets have shifted from discretionary perks to measurable cost-containment levers—an evolution that favors platforms capable of quantifying reductions in absenteeism, turnover, and healthcare costs. Private-equity sponsors continue to reward vendors that bundle scheduling, payments, CRM, and AI capabilities into one stack, reinforcing consolidation momentum. Against this backdrop, the Asia-Pacific region is scaling faster than any other geography, thanks to smartphone ubiquity and the ability to aggregate fragmented practitioner bases at low marginal cost.

Key Report Takeaways

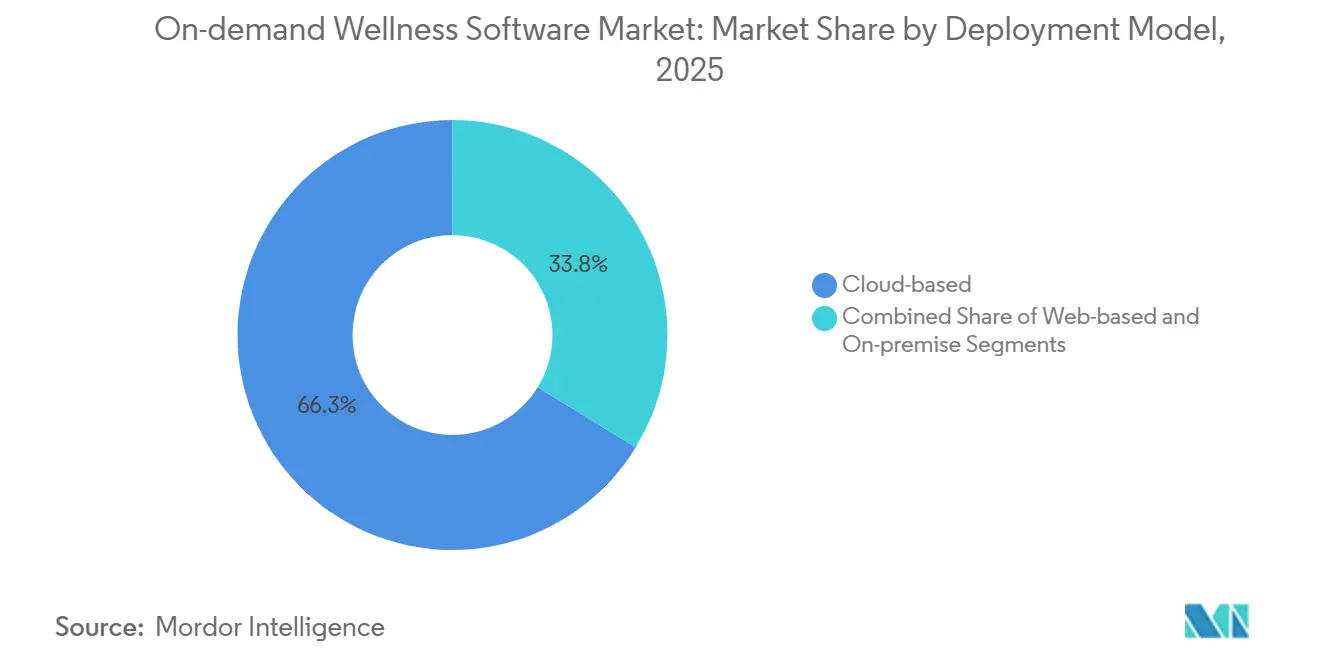

- By deployment model, cloud-based solutions led with 66.25% of the on-demand wellness software market share in 2025, and the same segment is projected to expand at a 12.63% CAGR to 2031.

- By subscription model, recurring monthly memberships captured 53.53% revenue share in 2025, while freemium tiers are forecast to record the fastest 11.55% CAGR through 2031.

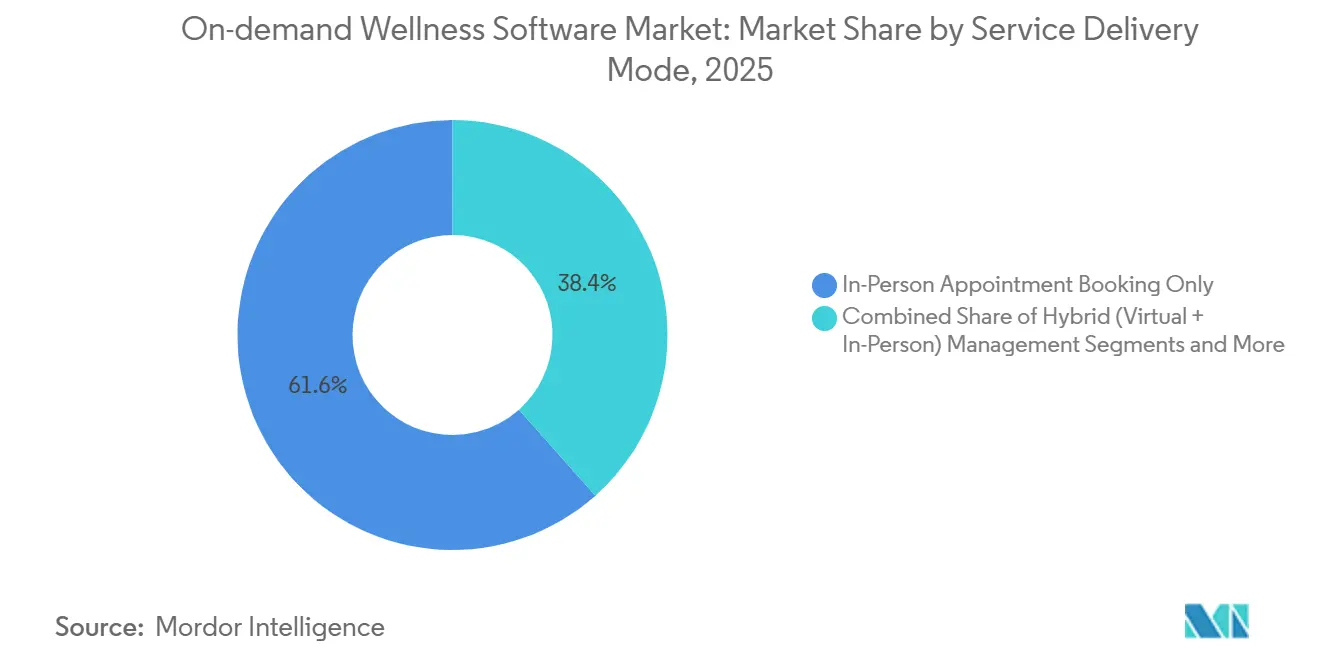

- By service-delivery mode, in-person appointments accounted for 61.57% of 2025 spending, whereas pure virtual streaming is advancing at the quickest 10.23% CAGR over the forecast period.

- By core functionality, booking and scheduling modules held 34.71% of 2025 revenue, but analytics and benchmarking are set to grow at the highest 11.45% CAGR to 2031.

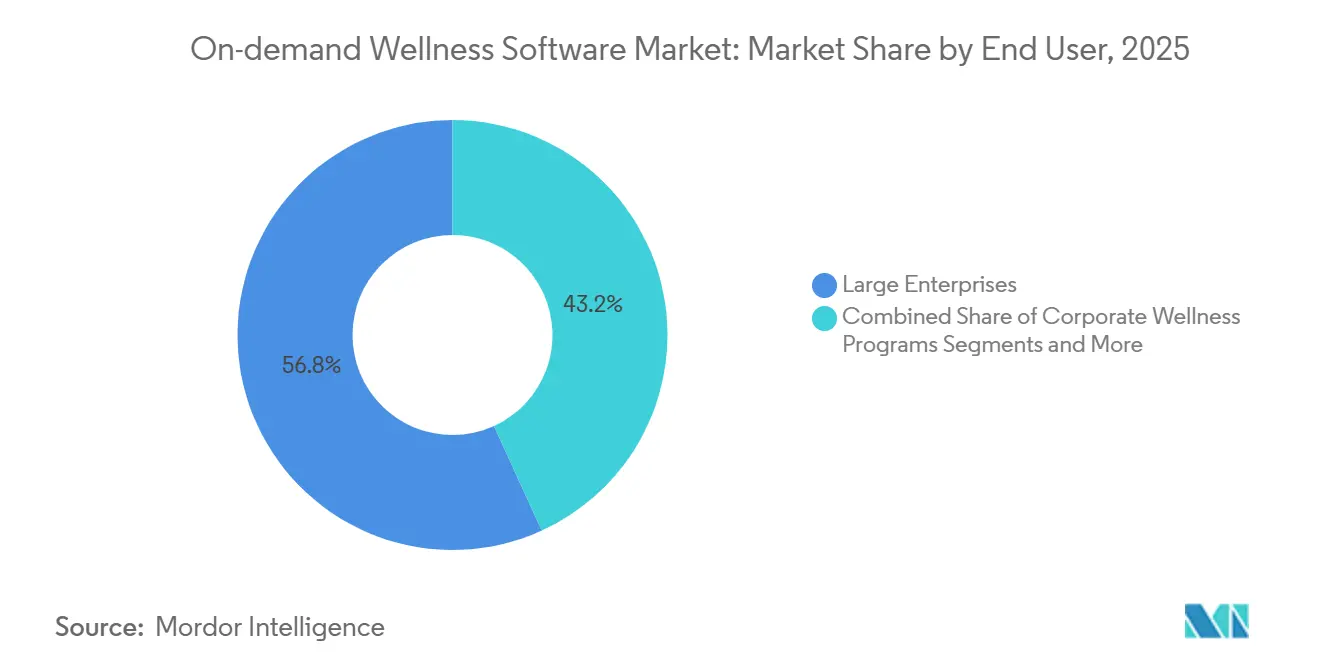

- By end-user, large enterprises represented 56.82% of 2025 sales, yet corporate wellness programs are projected to climb at the leading 10.42% CAGR through 2031.

- By geography, North America dominated with a 39.64% share in 2025, while Asia-Pacific is poised for the fastest 11.02% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global On-demand Wellness Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone-First Self-Service Booking Surge | 1.8% | Global, with APAC leading adoption | Short term (≤ 2 years) |

| Digitization of Spa/Salon Workflow | 1.5% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Employer Spending on Corporate Wellness SaaS | 2.1% | North America, Europe, GCC | Medium term (2-4 years) |

| AI Receptionists Convert Missed Calls | 1.3% | Global, early adoption in North America | Short term (≤ 2 years) |

| Dynamic-Pricing Engines for Yield | 0.9% | North America, Europe | Medium term (2-4 years) |

| Embedded Merchant-Financing Tools | 0.8% | North America, select APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Smartphone-First Self-Service Booking Surge

Mobile devices have replaced phone calls as the default channel for booking beauty and fitness sessions. Urban Company recorded 6.8 million mobile-only users across India, the UAE, Saudi Arabia, and Australia, proving that intuitive apps trump call centers in both convenience and conversion.[1]Urban Company, “Draft Red Herring Prospectus,” Securities and Exchange Board of India, sebi.gov.in GCC nations reinforce this trend: 5G coverage exceeds 90% and data plans cost less than 1% of monthly income, enabling real-time inventory visibility that eliminates no-shows and boosts utilization. Platforms optimized for sub-three-second load times win share, while legacy vendors reliant on desktop experiences watch churn climb. As smartphone penetration crosses 90% in most growth markets, mobile-first UX has shifted from differentiator to baseline expectation.

Digitization of Spa/Salon Workflow

Rising labor costs and slim margins are forcing salon and spa owners to abandon paper logbooks. Zenoti’s cloud suite integrates scheduling, POS, CRM, inventory, and payroll for 12,000 businesses worldwide, giving chains like European Wax Center and Massage Heights a single pane of glass for daily operations.[2]Zenoti, “Zenoti Raises $160 Million in Series D Funding Round Led by Advent International, Surpassing $1 B Unicorn Valuation,” Zenoti Press, zenoti.com Pandemic-era mandates for contactless check-in accelerated adoption, and Europe’s ePA requirement from October 2025 further pushes providers toward systems that can exchange HL7-FHIR data. Vendors that ship GDPR-ready consent modules and automated product reordering shrink administrative load and protect thin margins.

Employer Spending on Corporate Wellness SaaS

CFOs now treat wellness apps as cost-containment tools rather than perks. Wellhub, rebranded from Gympass in 2025, services 15,000 employers and 20 million employees, claiming 35% healthcare savings when users check in five-plus times each month.[3]Wellhub, “Gympass Is Now Wellhub: Let’s Make Every Company a Wellness Company,” Wellhub Press Release, wellhub.comThe platform aggregates 50,000 gyms, studios, and digital services under one fee, simplifying procurement and consolidating reporting. Because budgets reside in HR and Finance rather than Office Perks lines, contracts survive hiring freezes and deliver multi-year recurring revenue streams for vendors.

AI Receptionists Convert Missed Calls

Missed calls equal lost revenue. AI receptionists embedded in Zenoti parse natural-language requests, check real-time schedules, and upsell aromatherapy add-ons at booking, lifting after-hours bookings by as much as 30%. Beyond convenience, these algorithms function as yield-management engines that recommend optimal time slots based on historic demand. Early adopters report double-digit increases in average ticket size, demonstrating that AI reduces idle capacity and improves cash flow without adding headcount.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy & Security Compliance Burden | -1.2% | Global, acute in EU and select US states | Medium term (2-4 years) |

| Fragmented Practitioner Regulations | -0.9% | North America, Europe, select APAC markets | Long term (≥ 4 years) |

| High SMB Customer-Churn Costs | -1.4% | Global, pronounced in North America | Short term (≤ 2 years) |

| Scarcity of Vertical-AI Engineering Talent | -0.7% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy & Security Compliance Burden

Wellness platforms collect protected health information, card data, and geolocation, exposing vendors to Europe’s GDPR, California’s CPRA, and Brazil’s LGPD. BfArM demands robust security audits before German reimbursement approval, while Squarespace’s Acuity Scheduling restricts HIPAA BAAs to premium tiers, highlighting the cost of compliance for smaller firms. Fines can reach 2% of global revenue, turning privacy into both a moat and a minefield. Vendors investing early in SOC 2 and ISO 27001 audits secure enterprise RFPs others cannot touch.

High SMB Customer-Churn Costs

Small studio closures, cash-flow shocks, and aggressive competitive offers drive SMB churn. Beachbody’s SEC filing showed a USD 87.6 million loss on falling revenue despite 1.4 million digital subscriptions, underlining the fragility of volume-based models. For software vendors, every departing salon erases acquisition and onboarding spend, forcing a pivot either upmarket toward enterprises or toward faster payback periods on SMB accounts. Elevated churn heightens the imperative for retention tools such as loyalty programs and embedded financing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Maturity Outstrips On-Premise Holdouts

Cloud platforms captured 66.25% of 2025 revenue, expanding at a 12.63% CAGR as CIOs prioritize uptime, feature velocity, and global reach. Hyperscalers now operate 39 data centers in the UAE and 33 in Saudi Arabia, giving Middle-East operators low-latency access to cloud stacks. This dominance means the on-demand wellness software market size tied to cloud is set for outsized growth, while on-premise systems face inevitable decline. Regulatory carve-outs—such as Germany’s ePA landmark—still sustain a niche for hybrid setups, but even those must interoperate with cloud APIs to pass reimbursement hurdles.

Cloud leaders like Zenoti leverage aggregated transaction histories to train AI engines that power dynamic pricing and predictive scheduling. These capabilities become stronger with every new customer, creating feedback loops that browser-only or on-premise deployments cannot match. Yet data-localization rules in Brazil and China force vendors to negotiate local partnerships and build regional compliance layers, adding operational complexity but also raising competitive barriers.

By Subscription Model: Predictable Memberships Trump Pure Freemium

Monthly memberships account for 53.53% of 2025 revenue, proving that predictable cash flow outweighs one-off transactions for both investors and operators. Square Appointments follows this logic: a free tier hooks users, then Plus and Premium plans monetize advanced reporting and integrations. When executed well, freemium delivers viral growth, but Beachbody’s 25% revenue drop shows the perils of low conversion. Class packs remain attractive for occasional users, yet high transaction fees erode studio margins unless paired with upsells.

Enterprise seat-based contracts dominate corporate wellness, insulating vendors from seasonality and consumer churn. Wellhub’s per-employee pricing shifts usage risk onto the platform while granting CFOs budget certainty. BNPL integrations, such as Square’s Afterpay, boost conversion for high-ticket wellness bundles by splitting costs into installments. As interest-rate volatility subsides, embedded finance will likely extend beyond BNPL into longer-term merchant advances, deepening customer lock-in.

By Service Delivery Mode: Hybrid Delivery Wins Post-Pandemic

In-person services held 61.57% of 2025 spending because massages, facials, and haircuts remain inherently physical. Still, virtual streaming is growing at a 10.23% CAGR as remote work normalizes. The on-demand wellness software market size for hybrid models is poised to accelerate, combining in-person scheduling with tele-consultations on a single platform. Germany’s reimbursement mandate requires physiotherapists to integrate virtual visits into treatment records, catalyzing hybrid workflows in regulated segments.

Pure-virtual providers face engagement hurdles. Beachbody slashed its annual digital fee to maintain subscribers, confirming that user fatigue follows the novelty of at-home workouts. Corporate APIs, meanwhile, let employers plug curated wellness catalogs into HR portals, repositioning distribution as a differentiator. Platforms embedded in HRIS dashboards capture user attention at the point of need, while standalone apps struggle with notification overload.

By Core Functionality: Analytics Becomes the Engine of Retention

Booking modules still generated 34.71% of 2025 revenue, but analytics is the fastest climber at an 11.45% CAGR. Zenoti’s dashboards benchmark service-mix, labor productivity, and customer lifetime value against anonymized peers, making weekly performance reviews data-driven. Once executives integrate such metrics into incentive plans, switching vendors becomes costly, anchoring retention.

Subscription management automates failed-payment retries and tiered pricing, supporting the investor-preferred recurring model. Payments, although commoditized, deliver high-margin interchange fees that subsidize free plan tiers. CRM and marketing automation combat churn through targeted offers, while embedded outcome-tracking is becoming necessary in Europe’s evidence-centric reimbursement climate.

By End-User: Enterprises Fuel the Fastest Growth

Large corporations commanded 56.82% of 2025 revenues, yet corporate wellness programs will rise at a 10.42% CAGR, the quickest among all user groups. Employer contracts underpin the most resilient slice of the on-demand wellness software market, with Wellhub reporting 35% healthcare savings for highly engaged employees. At per-employee fees of USD 6-10, the potential annual spend eclipses smaller studio budgets.

SMB studios still supply volume but at the cost of higher churn. Equinox’s USD 1.8 billion refinancing revealed the capital intensity of brick-and-mortar fitness, a risk that software vendors inherit through operator instability. Consequently, many platforms now pursue a barbell approach: enterprise accounts for margin stability and SMB tailwinds for user-base scale, using embedded capital and loyalty tools to soften the volatility of the long-tail segment.

Geography Analysis

North America contributed 39.64% of global revenue in 2025, underpinned by established salon chains and generous corporate benefits budgets. Zenoti’s USD 1 billion valuation and Advent-led funding round show continued investor confidence, but saturation means growth will decelerate as penetration levels rise. Vendors differentiate through AI yield tools and merchant financing—Vagaro Capital funds up to USD 500,000 within 48 hours—enhancing retention among cash-constrained operators. Tightening privacy laws, notably CPRA amendments, are raising baseline compliance costs, tilting the playing field toward well-capitalized providers.

Asia-Pacific is expanding at an 11.02% CAGR, the fastest worldwide. Urban Company’s USD 137 million revenue and 38% annual growth validate a marketplace model that unifies 47,800 independent professionals across India and the Middle East. Local platforms thrive on fragmented supply and high smartphone adoption, whereas overseas entrants struggle with data-localization rules and super-app dominance in markets such as China. Japan’s modest 37% telehealth uptake, despite robust digital infrastructure, reminds vendors that cultural dynamics can delay virtual care adoption.

Europe’s trajectory is dictated by regulatory milestones. Germany’s ePA mandates HL7-FHIR interoperability from October 2025, rewarding platforms that invested early in compliant APIs. The BfArM DiGA fast track offers three-month reimbursement approval for evidence-backed apps, prompting an R&D arms race focused on clinical validation. Meanwhile, GDPR enforcement removes under-capitalized vendors unable to bankroll security audits.

The GCC spearheads Middle-East momentum, targeting a USD 4 billion digital-health market by 2026, with 90% 5G coverage and widespread digital ID adoption. Platforms benefit from instant payment rails like UAE Pass that reduce onboarding friction. Urban Company’s entry into Dubai and Riyadh highlights the region’s affluent, convenience-seeking consumer base and investor-friendly free-zone regimes.

South America offers scale but demands patience. Brazil’s ConecteSUS network links most states, yet patchy broadband and uneven LGPD enforcement complicate nationwide rollouts. Currency volatility and fragmented procurement make low-cost mobile-first solutions preferable to feature-rich enterprise suites. Vendors prepared to localize pricing and support offline workflows will capture early mover advantages as infrastructure improves.

Competitive Landscape

The market remains fragmented; no player exceeds a double-digit global share. Zenoti’s 12,000-business footprint captures only a small fraction of the potential salon and spa universe, underscoring ample headroom. Vendors cluster into three playbooks: all-in-one enterprise suites such as Zenoti and Mindbody, SMB freemium platforms like Square Appointments and Fresha, and corporate wellness aggregators led by Wellhub. White-space niches persist in teletherapy, medical aesthetics, and integrative medicine, each requiring specialized compliance or clinical features.

AI is the new moat. Zenoti’s AI Receptionist and dynamic pricing engines leverage data at scale, making feature parity difficult for smaller platforms. Embedded finance deepens stickiness; Vagaro Capital ties working capital to continued platform usage, dissuading defections during loan repayment. Regulatory integration forms another barrier: vendors first to link with Germany’s ePA or Brazil’s RNDS lock in early adopters who fear migration headaches.

Consolidation looms as private equity seeks operating leverage through roll-ups. Past precedent includes Vista Equity’s USD 1.9 billion purchase of Mindbody, which created a global footprint overnight. Similar transactions are expected as investors chase synergies in compliance, R&D, and go-to-market motions. Until then, intense price competition at the SMB tier offsets premium pricing in the enterprise cohort, keeping margins in check for most incumbents.

On-demand Wellness Software Industry Leaders

Zenoti

Fresha

Mindbody

Vagaro

Booksy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: purelyIV expanded its concierge IV therapy platform in Metro Detroit, added a Fullscript supplement store, and revamped membership tiers.

- September 2025: Spark Biomedical and Velentium Medical launched OhmBody, a non-invasive neuromodulation product aimed at menstrual symptom relief.

- August 2025: Hapbee Technologies secured investment from Smile Group to launch its digital wellness platform in Singapore and India.

Global On-demand Wellness Software Market Report Scope

On-demand wellness software is a digital platform that provides instant, 24/7 access to personalized health and lifestyle services, including virtual fitness, meditation, therapy, and nutrition consultations, often enhanced by wearable data, AI insights, and booking features.

The On-demand Wellness Software Market Report is segmented by Deployment Model, Subscription Model, Service Delivery Mode, Core Functionality, End User, and Geography. By Deployment Model, the market is segmented into Cloud-based, Web-based, and On-premise. By Subscription Model, the market is segmented into Recurring Monthly, Class Packs, Pay-As-You-Go, Freemium, and Enterprise Contract. By Service Delivery Mode, the market is segmented into Pure Virtual, Hybrid, In-Person, and Corporate API. By Core Functionality, the market is segmented into Booking, Membership, POS, Marketing, and Analytics. By End User, the market is segmented into Large Enterprises, SMEs, Wellness Centers, Gyms, and Corporate Programs. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Cloud-based |

| Web-based |

| On-premise |

| Recurring Monthly Memberships |

| Class/Session Packs |

| Pay-As-You-Go (One-off Purchases) |

| Freemium + In-App Upsells |

| Enterprise Contract (Per-Seat / Per-Employee) |

| Pure Virtual / On-Demand Content Streaming |

| Hybrid (Virtual + In-Person) Management |

| In-Person Appointment Booking Only |

| Corporate Wellness API / White-Label Integrations |

| Booking & Scheduling |

| Membership / Subscription Management |

| POS & Payments |

| Marketing & CRM Automation |

| Analytics & Benchmarking |

| Large Enterprises |

| Small & Medium Enterprises (SMEs) |

| Wellness Centers & Spas |

| Gyms & Fitness Studios |

| Corporate Wellness Programs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Deployment Model | Cloud-based | |

| Web-based | ||

| On-premise | ||

| By Subscription / Pricing Model | Recurring Monthly Memberships | |

| Class/Session Packs | ||

| Pay-As-You-Go (One-off Purchases) | ||

| Freemium + In-App Upsells | ||

| Enterprise Contract (Per-Seat / Per-Employee) | ||

| By Service Delivery Mode | Pure Virtual / On-Demand Content Streaming | |

| Hybrid (Virtual + In-Person) Management | ||

| In-Person Appointment Booking Only | ||

| Corporate Wellness API / White-Label Integrations | ||

| By Core Functionality | Booking & Scheduling | |

| Membership / Subscription Management | ||

| POS & Payments | ||

| Marketing & CRM Automation | ||

| Analytics & Benchmarking | ||

| By End-user | Large Enterprises | |

| Small & Medium Enterprises (SMEs) | ||

| Wellness Centers & Spas | ||

| Gyms & Fitness Studios | ||

| Corporate Wellness Programs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What was the global revenue of on-demand wellness software in 2026?

The market reached USD 591.39 million in 2026.

How fast will cloud-based deployment grow through 2031?

Cloud revenue is projected to expand at a 12.63% CAGR.

Which region is expanding the quickest?

Asia-Pacific is advancing at an 11.02% CAGR through 2031.

Why are employers investing heavily in wellness software?

Platforms such as Wellhub show up to 35% healthcare-cost savings when employees engage regularly.

What feature area is rising fastest in vendor roadmaps?

Analytics and benchmarking modules are growing at 11.45% CAGR as operators demand decision intelligence.

Page last updated on: