Cameroon Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

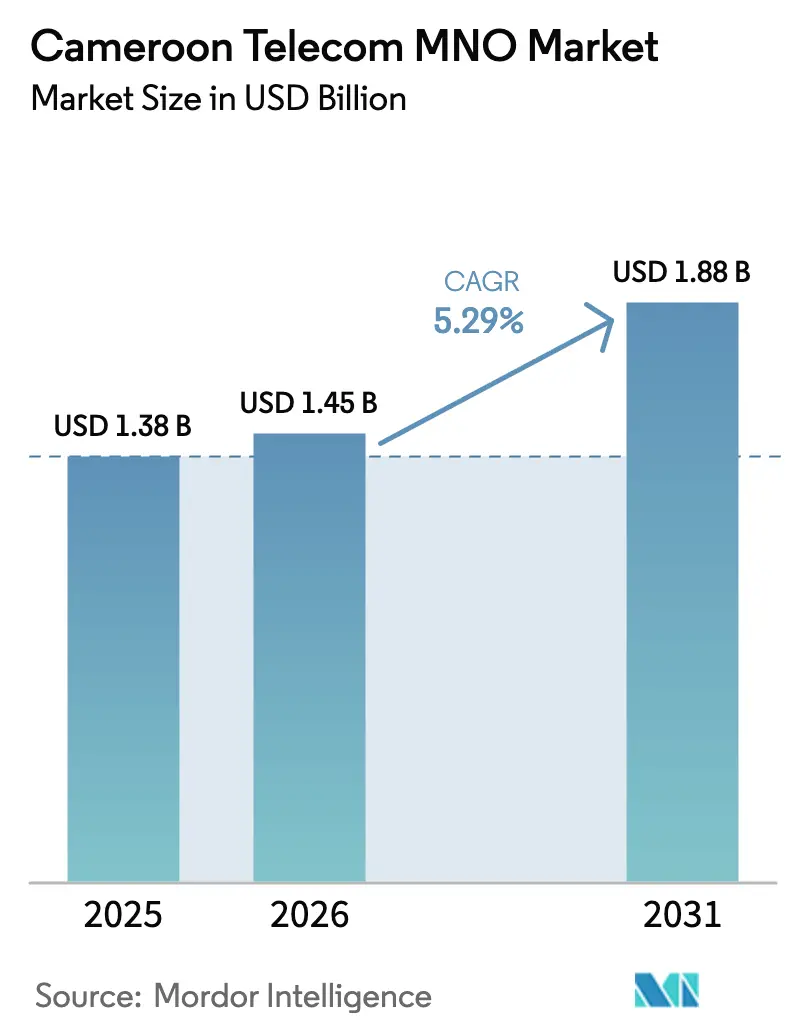

| Base Year Market Size (2025) | USD 1.38 Billion |

| Market Size (2026) | USD 1.45 Billion |

| Market Size (2031) | USD 1.88 Billion |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

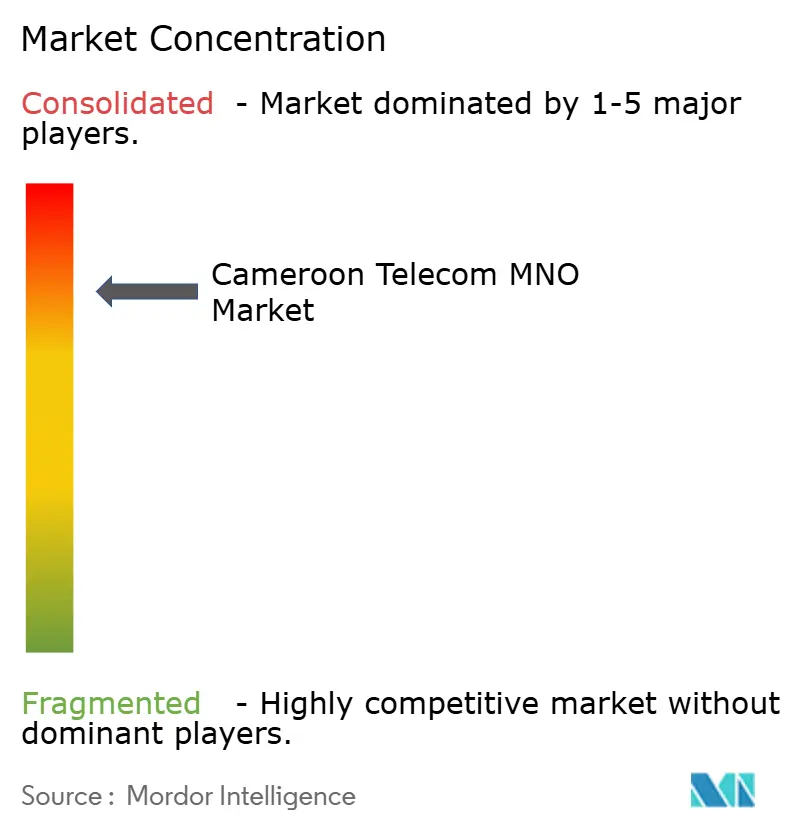

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cameroon Telecom MNO Market Analysis by Mordor Intelligence

Cameroon Telecom MNO Market size in 2026 is estimated at USD 1.45 billion, growing from 2025 value of USD 1.38 billion with 2031 projections showing USD 1.88 billion, growing at 5.29% CAGR over 2026-2031.

Robust capital expenditure from the two dominant operators, rising smartphone penetration, and aggressive government digitalization programs underpin this growth path. International bandwidth rose sharply after the South Atlantic Inter-Link (SAIL) cable activated 32 Tbps of capacity and positioned Kribi as a regional traffic gateway. Mobile money adoption fuels additional data usage, while enterprise connectivity demand benefits from a World Bank USD 100 million program that links broadband to agricultural productivity. Competitive intensity escalates as network-sharing agreements help smaller licensees extend rural reach without duplicating costly infrastructure. Ongoing fibre vulnerabilities and a heavy tax regime weigh on profitability but do not derail the overall upward trajectory of the Cameroon telecom market.

Key Report Takeaways

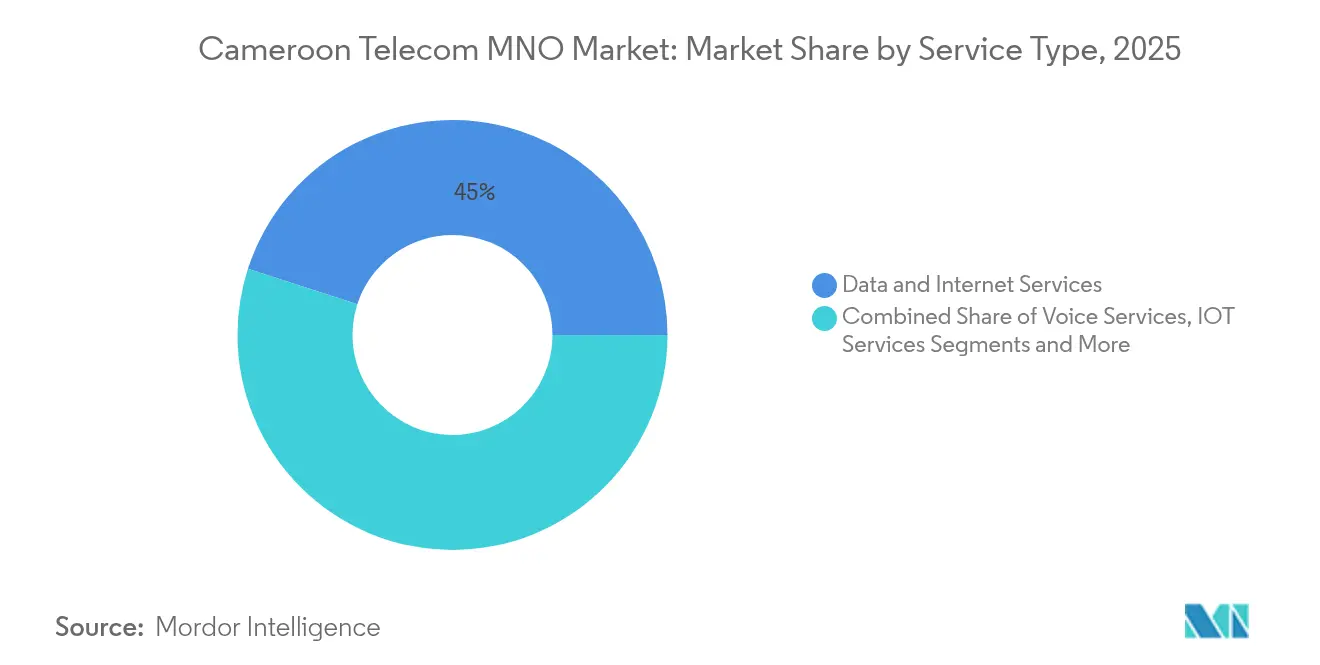

- By service type, data services captured 45.02% of the Cameroon telecom market share in 2025 and are projected to grow at a 5.39% CAGR through 2031.

- By end user, the consumer segment accounted for 69.55% share of the Cameroon telecom market size in 2025, while the enterprise segment records the highest projected CAGR at 5.57% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Cameroon Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aggressive 4G and imminent 5G CAPEX | +1.2% | National, urban focus | Medium term (2-4 years) |

| Mobile-money-led surge in data traffic | +0.9% | National, strongest in CEMAC region | Short term (≤ 2 years) |

| Government “Digital Cameroon 2030” projects | +0.8% | National, rural prioritization | Long term (≥ 4 years) |

| Cheaper Chinese smartphones | +0.6% | National, accelerated in rural markets | Short term (≤ 2 years) |

| Youth-driven OTT video and e-sports adoption | +0.4% | Urban and secondary cities | Medium term (2-4 years) |

| New subsea cables raising international capacity | +0.7% | National gateway effect from Kribi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aggressive 4G and Imminent 5G CAPEX by MTN and Orange

Operator investment cycles directly strengthen network quality and subscriber retention. MTN Cameroon registered 15.7% service revenue growth in Q1 2025 after heavy radio and fibre upgrades that lifted data revenues by 30.1% year on year[1]Telecom Lead, “MTN Q1 2025 Revenue, Capex, ARPU, Subscribers,” telecomlead.com. Orange’s Africa and Middle East arm added EUR 182 million in Q3 2024 revenue on the back of similar coverage enhancements. Both groups plan 5G pilots in Douala and Yaoundé, and Camtel signals a dual-vendor strategy to diversify beyond Chinese equipment. Better throughput mitigates churn triggered by recurrent backbone cuts, while the capital burden compresses near-term margins before translating into durable market-share advantages. Sustained CAPEX therefore supplies the largest single uplift to the Cameroon telecom market.

Mobile-Money-Led Surge in Data Traffic

Cameroon hosts 19.5 million active mobile-money accounts and processes CFA 40.6 billion (USD 67.7 million) in daily transactions, equal to 73.1% of CEMAC volumes[2]Business in Cameroon, “CEMAC: Cameroon Confirms Leadership in the Mobile Money Market,” businessincameroon.com. MTN lowered withdrawal fees by 25% in October 2024, which spurred transaction frequency and authentication data bursts. Orange Money’s tie-up with Mastercard widens acceptance networks and sparks higher cross-border usage. Fintech revenue climbed 27.4% at MTN Cameroon in H1 2024, a trajectory that mirrors a 19.2% uplift in data revenue. Financial inclusion thus becomes a virtuous driver for packet-based traffic that enlarges the Cameroon telecom market.

Government “Digital Cameroon 2030” Projects Lifting Enterprise Demand

The national strategy promotes e-government, biometric visas, and smart-agriculture pilots financed through a USD 100 million World Bank credit line. These programs obligate ministries and parastatals to procure secure cloud links, VPNs, and IoT connectivity that exceed ordinary broadband requirements. MTN responded by launching Chenosis, an application-programming-interface marketplace that helps enterprises digitize back-end processes. Predictable public-sector contracts offer multi-year revenue streams, but slow payment cycles challenge cash flow. Overall, policy coordination is unlocking a fresh enterprise addressable base inside the Cameroon telecom market.

Cheaper Chinese smartphones

Sub-USD 50 Android handsets from Transsion and Xiaomi now dominate informal retail channels, raising the active smartphone ratio to 43% of total SIMs in 2025. Feature-rich but affordable devices improve user experience, encourage app downloads, and shift rural customers toward data bundles. Operators benefit through higher average revenue per user even as handset subsidies remain minimal. The influx of low-priced smartphones therefore accelerates rural data adoption and expands the revenue pool.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Frequent fibre-cut outages | -0.8% | National, acute in rural corridors | Short term (≤ 2 years) |

| High sector-specific taxes | -0.6% | National, stronger rural impact | Medium term (2-4 years) |

| Slow 5G spectrum awards | -0.4% | Urban enterprise zones | Medium term (2-4 years) |

| Cash-dominant economy limits post-paid uptake | -0.3% | Rural areas, informal economy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Frequent Fiber-Cut Outages Eroding Quality of Service

MTN’s chief executive confirmed record backbone instability in August 2024, with repeated cuts on the Camtel-managed network. Cameroon ranks last among 93 countries on a fibre-readiness index despite having laid 15,000 km of cable by 2023. Outage risks force operators to invest in microwave or satellite back-ups that raise cost bases. Enterprise clients demand service-level agreements, so recurrent disruptions impair operator credibility and dilute the Cameroon telecom market growth impulse.

High Sector-Specific Taxes Keeping Tariffs Elevated

Excise duties, import levies on network gear, and multiple municipal fees inflate operator cost structures. These charges translate into tariffs that remain above regional medians, depressing broadband adoption among price-sensitive rural users. Operators then struggle to recoup CAPEX commitments, and policy makers face a trade-off between fiscal revenue and digital inclusion. Tax relief could release meaningful latent demand and accelerate the Cameroon telecom market, yet reforms remain slow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Data Services Drive Digital Transformation

Data services held 45.02% of the Cameroon telecom market share in 2025 and are on track for a 5.39% CAGR to 2031. This weight makes the segment the anchor of the Cameroon telecom market size expansion narrative. Rising smartphone ownership, the rollout of affordable 4G bundles, and enterprise digitization propel packet revenues. The World Bank-backed smart-agriculture initiative alone spans 100,000 potential IoT endpoints that rely on continuous data streams. MTN’s Chenosis marketplace supports application integration, signaling a shift from connectivity to solution-based engagement. On the consumer side, OTT video already accounts for more than half of peak-hour traffic in urban centers, pressuring operators to densify cell sites and reinforce fibre backhaul.

Data service momentum further benefits from fintech synergies. Each mobile-money authentication step consumes data, and transaction growth therefore maps onto volume-based billing curves. Operators leverage zero-rating strategies for specific banking apps, driving ecosystem stickiness without sacrificing revenue. The segment remains sensitive to backbone resilience, so accelerated splice protection and dual-path routing projects are vital to protect the Cameroon telecom market size gains.

Enterprise Segment Accelerates Digital Adoption

Enterprise clients represented 30.45% of 2025 revenue but are projected to lead growth with a 5.57% CAGR. Government IT modernisation, foreign direct investment inflows, and the French Development Agency’s CFA 721.55 billion (USD 1.2 billion) infrastructure loan pipeline all require scalable connectivity. Corporations demand secure MPLS, dedicated internet access, and managed security, enabling operators to upsell beyond basic bandwidth. MTN’s enterprise portfolio already spans cloud hosting and API gateways, while Orange Business Services offers hybrid-cloud orchestration. High compliance needs create switching costs and foster sticky contracts.

Long procurement cycles and payment delays do pose working-capital pressures. However, once contracts close, revenue visibility strengthens, and operators achieve higher average revenue per line. The enterprise surge therefore adds depth to the Cameroon telecom market size forecast.

Geography Analysis

Coastal landing points grant Cameroon a gateway role. Kribi connects four subsea systems, delivering over 200 Gbps of aggregate capacity and direct South Atlantic access. MTN GlobalConnect monetizes transit traffic to Chad and CAR, lowering unit costs for domestic users and broadening the Cameroon telecom market footprint. Reliable hydro power from the Nachtigal plant, fully online since March 2025, secures stable energy for data centers and reduces operating expenditure.

Regional cross-border fibre projects deepen integration. The 22 km optic link to Gabon carries 96-strand G652 cable with near-100 Tbps potential and supports e-health, e-learning, and wholesale resale markets. Google’s announced Umoja cable will further diversify routes, although timelines remain fluid. Concentrated infrastructure at Kribi does create single-point-of-failure risk, so secondary landing sites and inland redundancy corridors are priorities.

Urban-rural gaps persist. National 4G population coverage exceeds 80.37%, yet effective throughput drops sharply beyond provincial capitals. Only 170 of 2,000 planned Multipurpose Community Telecentres were built, highlighting execution hurdles. Terrain, conflict pockets in the Far North, and limited purchasing power slow rural rollout. The Digital Cameroon 2030 plan tasks public-private models to overcome these barriers, and network-sharing agreements already show promise.

Competitive Landscape

The market remains concentrated. MTN controls above 50% of subscribers, Orange hovers near 30%, Nexttel counts 5 million users, and Camtel leverages a new mobile license. MTN outperformed peers with a 30.1% data revenue jump in Q1 2025, capitalizing on coverage breadth. Orange counters with fintech differentiation via its Mastercard alliance. Nexttel banks on aggressive device-bundle promotions, while Camtel’s partnership with Orange opens rural corridors previously outside its reach.

Competitive focus is shifting from pure connectivity to ecosystems. MTN slashed mobile-money withdrawal fees, driving volume spikes and platform loyalty. Orange exploits international backbone ownership for superior latency, attracting premium corporate accounts. Equipment supplier strategies diversify as geopolitical risk mounts; operators increasingly source from multiple vendors to hedge sanctions exposure.

Regulation enforces structured competition. Authorities suspended Starlink in April 2024 to ensure licence compliance, protecting incumbents and asserting sovereignty. A USD 52 million debt recovery drive in April 2025 signals tougher oversight on financial discipline. The competitive narrative thereby blends high concentration with rising service-based rivalry that collectively shapes the Cameroon telecom market.

Cameroon Telecom MNO Industry Leaders

MTN Cameroon

Orange Cameroun

Nexttel Cameroon

Camtel Mobile (Blue)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The regulator launched a USD 52 million debt-recovery campaign aimed at outstanding dues from telecom operators.

- December 2024: Camtel signed a network-sharing pact with Orange to expand rural footprint and lift service quality.

- November 2024: Orange Africa and Middle East division posted 10.5% revenue growth, contributing EUR 182 million.

Cameroon Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

Which service type generates the largest revenue share?

Data services lead with 45.02% revenue in 2025 and maintain the fastest absolute growth.

How significant is mobile money to operator revenue?

Fintech income grew 27.4% at MTN Cameroon in H1 2024, showing strong linkage between financial services and data traffic.

What share do MTN Cameroon and Orange Cameroun hold together?

The two operators jointly account for more than 80% of subscribers, underpinning high market concentration.

Why is fibre instability considered a major restraint?

Recurrent backbone cuts degrade quality of service and impose redundancy costs that subtract 0.8% from forecast CAGR.

Page last updated on: