Lentil Protein Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

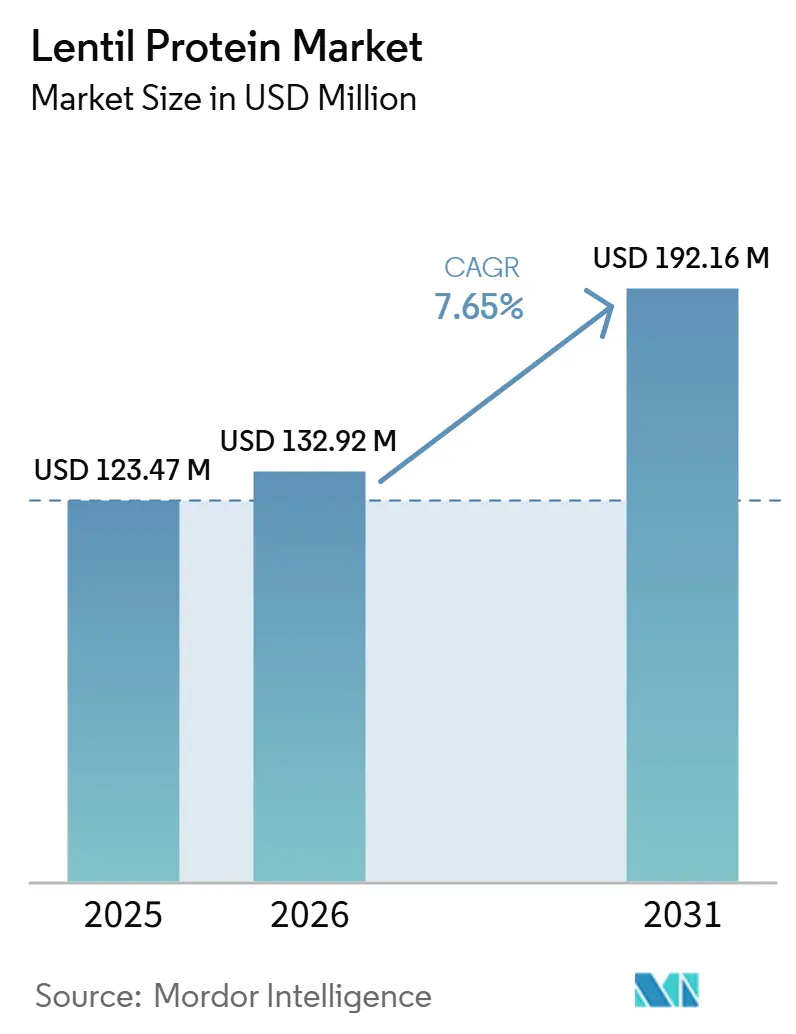

| Market Size (2026) | USD 132.92 Million |

| Market Size (2031) | USD 192.16 Million |

| Growth Rate (2026 - 2031) | 7.65% CAGR |

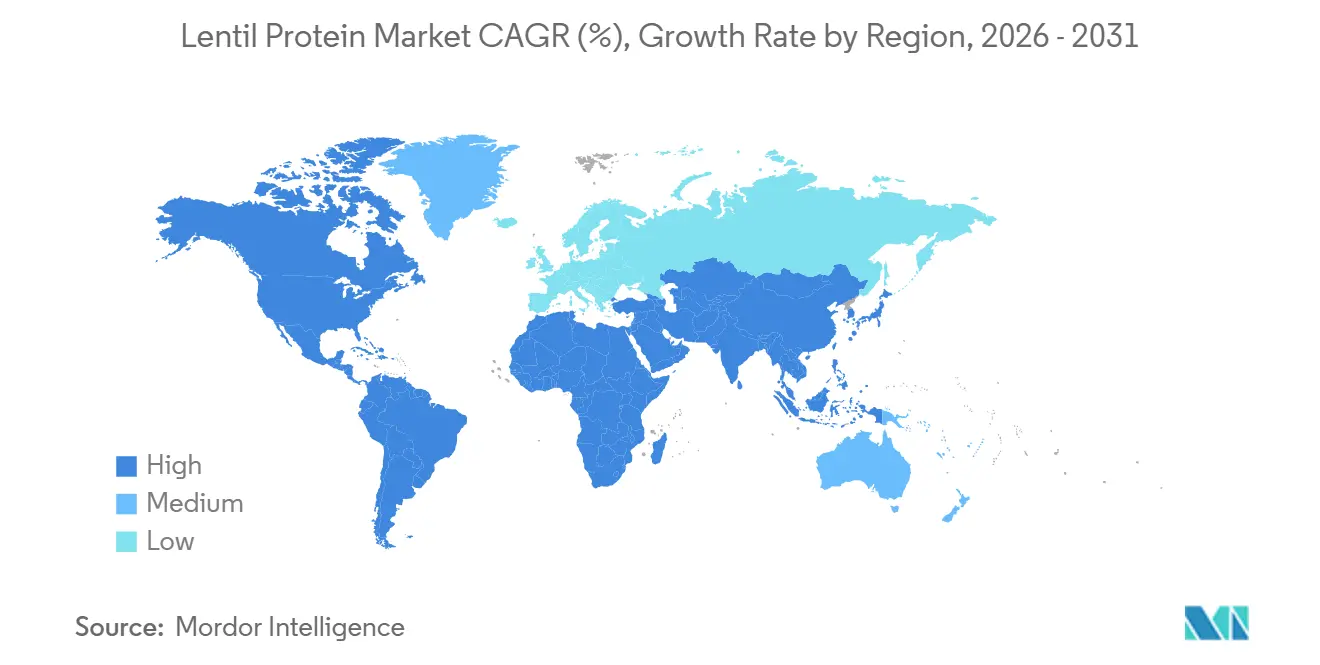

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Lentil Protein Market Analysis by Mordor Intelligence

The global lentil protein market is witnessing consistent growth, driven by the increasing preference for plant-based, sustainable, and nutritionally rich protein alternatives. The market was valued at USD 123.47 million in 2025, grew to USD 132.92 million in 2026, and is projected to reach USD 192.16 million by 2031, with a CAGR of 7.65% during 2026–2031. This growth is primarily attributed to the rising adoption of plant-based diets, increasing demand for allergen-free and clean-label ingredients, and the strong sustainability profile of lentil protein, which has a significantly lower environmental impact compared to animal-based proteins. Furthermore, advancements in processing and extraction technologies are improving the functional performance, taste, and consistency of lentil protein, enhancing its suitability for large-scale commercial applications.

Key Report Takeaways

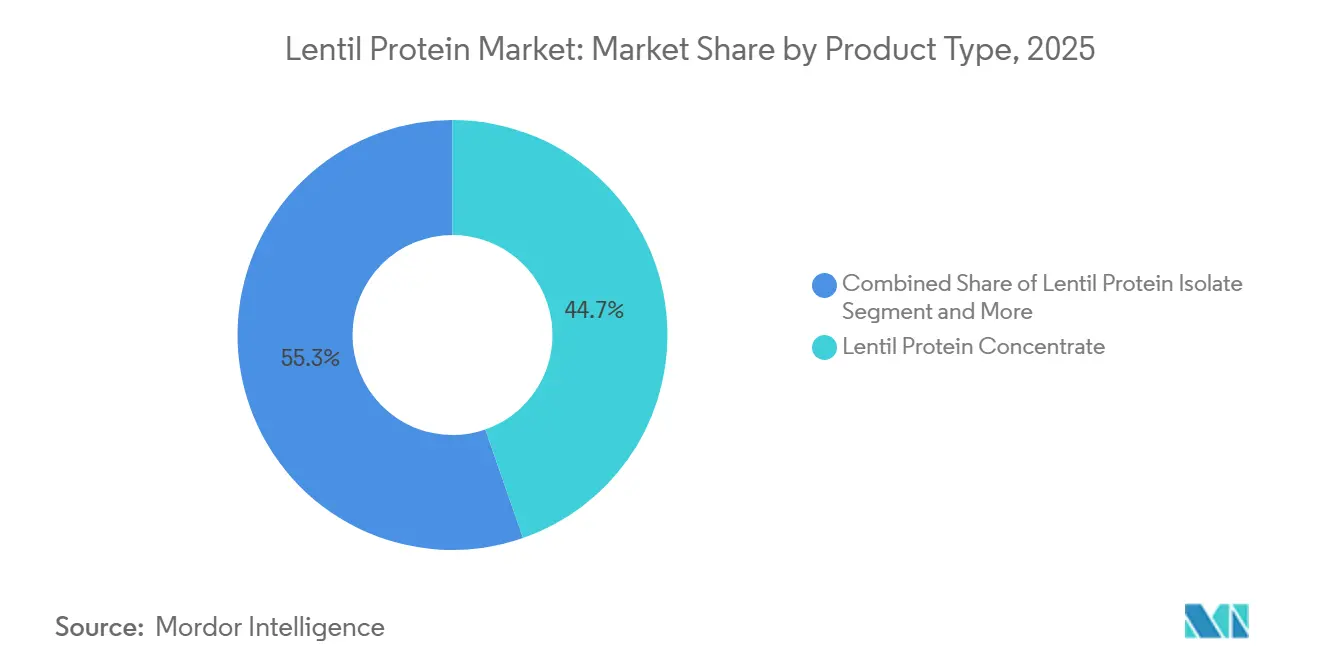

- By product type, lentil protein concentrate captured 44.68% of 2025 revenue, while lentil protein isolate is forecast to advance at a 7.89% CAGR to 2031.

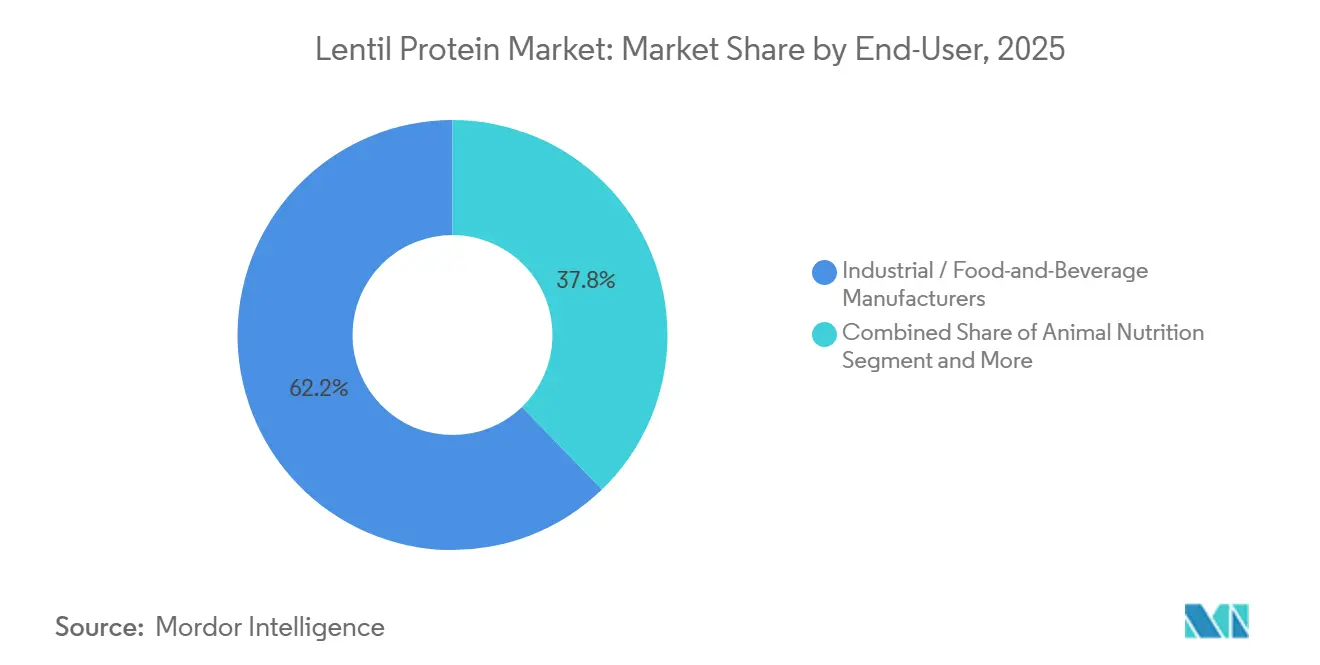

- By end-user, industrial and food-and-beverage manufacturers held 62.23% lentil protein market share in 2025; animal nutrition records the fastest projected expansion at 7.95% CAGR through 2031.

- By geography, North America dominated with 34.12% of 2025 revenue, whereas Asia-Pacific is forecast to climb at an 8.45% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lentil Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of plant-based diets | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growing demand for allergen-free proteins | +1.2% | North America and Europe, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Sustainability and low environmental footprint | +1.5% | Global, regulatory pressure strongest in Europe | Long term (≥ 4 years) |

| Rising demand for organic and conventional lentil proteins | +0.9% | North America and Europe premium segments | Medium term (2-4 years) |

| Advancements in processing technologies | +0.8% | Global, led by North America and Europe Research and Development (R&D) hubs | Long term (≥ 4 years) |

| Surge in functional food and beverage applications | +1.3% | Global, fastest uptake in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising adoption of plant-based diets

The growing adoption of plant-based diets is driven by consumer preferences for health, sustainability, and ethical considerations. This shift is prompting food manufacturers to incorporate alternative proteins, such as lentil protein, into their products to meet changing dietary demands. According to the Good Food Institute, 60% of United States households purchased plant-based foods in 2025, underscoring the mainstream acceptance of plant-based consumption [1]Source: Good Food Institute, "The plant-based food industry is evolving". gfi.org. This trend is increasing the demand for diverse and functional plant protein sources beyond traditional options like soy and pea. Lentil protein is emerging as a favorable alternative due to its nutritional benefits and clean-label attributes. As consumers seek variety and innovation in plant-based diets, food producers are broadening their ingredient portfolios to include emerging proteins that provide both nutritional and formulation advantages.

Growing demand for allergen-free proteins

The increasing demand for allergen-free proteins is a key factor driving the global lentil protein market. Consumers are progressively seeking dietary options that exclude common allergens such as dairy, soy, and gluten. Lentil protein, being naturally hypoallergenic compared to many traditional protein sources, is gaining popularity among consumers and manufacturers addressing rising sensitivities and dietary restrictions. According to the Centers for Disease Control and Prevention, 31.7% of adults in the United States were diagnosed with a seasonal allergy, eczema, or food allergy in 2024, highlighting the growing prevalence of allergic conditions [2]Source: Centers for Disease Control and Prevention, "Diagnosed Allergic Conditions in Adults", cdc.gov. This trend is encouraging food producers to reformulate products using allergen-friendly ingredients, thereby increasing the adoption of lentil protein as a dependable plant-based alternative.

Sustainability and low environmental footprint

The sustainability and minimal environmental impact of lentil protein are key factors driving market growth, as both manufacturers and consumers increasingly focus on environmentally responsible protein sources. Lentil protein production results in significantly lower greenhouse gas emissions compared to animal-based proteins, positioning it as a viable alternative in the shift toward sustainable food systems. On a lifecycle basis, lentil protein produces approximately 1 kg of CO₂-equivalent per kilogram of protein, which is a 98% reduction compared to beef protein, emitting around 50 kg of CO₂-equivalent per kilogram. This notable environmental benefit is prompting food producers to transition toward plant-based protein portfolios that align with corporate sustainability objectives and carbon reduction targets. Furthermore, the growing awareness among consumers about the environmental impact of their dietary choices is accelerating the adoption of lentil protein, as it offers a sustainable and nutritious option without compromising on quality or functionality.

Rising demand for organic and conventional lentil proteins

The demand for both organic and conventional lentil proteins is increasing, driven by the need for diverse sourcing options that address varying consumer and industrial requirements. Organic lentil protein is gaining popularity among health-conscious consumers who prioritize chemical-free, non-GMO, and sustainably cultivated ingredients, aligning with clean-label and premium product preferences. Meanwhile, conventional lentil protein remains in strong demand due to its cost-effectiveness, large-scale availability, and reliable supply, making it suitable for mass-market production and industrial applications. This dual demand structure enables manufacturers to cater to multiple consumer segments, ranging from premium organic product lines to cost-effective, high-volume offerings, thereby broadening the overall market reach.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Off-flavor and taste challenges | -0.60% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Limited consumer awareness | -0.40% | Emerging markets in Asia-Pacific, MEA, South America | Medium term (2-4 years) |

| Competition from established plant proteins | -0.70% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Supply chain and processing complexity | -0.50% | Emerging markets, seasonal impact in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Off-flavor and taste challenges

The off-flavor and taste issues associated with lentil protein serve as a significant restraint in the global lentil protein market, as sensory attributes are a critical factor influencing product acceptance. Lentil protein commonly exhibits a beany, earthy, or slightly bitter taste profile, which can be challenging to mask, especially in applications where flavor neutrality is crucial. These sensory limitations can significantly limit its use in products requiring a clean taste and smooth mouthfeel, creating substantial challenges for manufacturers striving to meet evolving consumer expectations. Furthermore, addressing these flavor concerns often necessitates additional processing steps, the use of flavor-masking agents, or blending with other ingredients, leading to increased formulation complexity, higher production costs, and potential delays in product development timelines.

Limited consumer awareness

The limited consumer awareness of lentil protein serves as a significant restraint in the global lentil protein market. Compared to more established plant-based proteins like pea and soy, lentil protein remains relatively less recognized. While lentils are commonly consumed as a whole food, their processed protein forms are not widely understood or familiar to mainstream consumers, which can impede their adoption in packaged and formulated products. This lack of awareness diminishes consumer-driven demand, making it difficult for manufacturers to position lentil protein as a preferred ingredient. Furthermore, the absence of robust marketing and branding efforts for lentil protein, compared to competing proteins, restricts its visibility in retail and foodservice channels. Consumers tend to favor well-known and trusted protein sources, creating challenges for newer or less-promoted alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Concentrates Maintain Scale While Isolates Accelerate

The lentil protein concentrate segment, projected to account for 44.68% of the global lentil protein market share in 2025, is driven by its balance of cost-effectiveness, nutritional value, and processing efficiency. Concentrates require less intensive processing compared to more refined variants, reducing production complexity while preserving more of the lentil's natural components. This aligns with the increasing consumer preference for minimally processed and clean-label ingredients. These attributes enable manufacturers to scale production while maintaining competitive pricing, thereby boosting adoption. Furthermore, lentil protein concentrate provides consistent protein content along with retained micronutrients, positioning it as a nutritionally balanced plant-based protein option.

The lentil protein isolate segment is anticipated to grow at a CAGR of 7.89% through 2031, driven by rising demand for high-purity, high-protein plant-based ingredients that meet evolving formulation and nutritional requirements. Isolates offer significantly higher protein content with reduced carbohydrates and fats, making them ideal for manufacturers focused on protein fortification and nutritional precision. This higher purity aligns with the increasing preference for protein-dense formulations and supports the development of products requiring strict macronutrient control. Additionally, lentil protein isolates provide enhanced functional performance, including improved solubility, emulsification, and dispersion, which increases their compatibility with advanced food processing systems and complex formulations.

By End-User: Animal Nutrition Outpaces Food Applications

The industrial and food-and-beverage manufacturers segment, expected to account for 62.23% of the global lentil protein market share in 2025, is a key driver of market growth. This is attributed to its large-scale procurement capacity and critical role in integrating ingredients into processed food systems. These manufacturers operate at high production volumes, necessitating consistent, scalable, and cost-effective protein ingredients. Lentil protein meets these requirements, making it a suitable option for industrial applications. Additionally, the segment benefits from the growing trend toward plant-based reformulation strategies, as companies increasingly replace or complement traditional protein sources with plant-derived alternatives to align with evolving product positioning and labeling standards.

The animal nutrition segment, anticipated to grow at a CAGR of 7.95% through 2031, is gaining traction as the feed industry shifts toward sustainable, plant-based protein alternatives. This transition aims to reduce reliance on traditional sources such as fishmeal and soybean meal. Lentil protein is becoming a preferred choice due to its balanced amino acid profile, digestibility, and plant-based origin, which support efforts to enhance feed efficiency and nutritional quality. As feed manufacturers focus on ingredient diversification and supply chain resilience, lentil protein provides a dependable alternative for incorporation into modern feed formulations.

Geography Analysis

North America is projected to hold 34.12% of the global lentil protein market share in 2025, maintaining its leadership due to a well-established plant-based protein ecosystem, advanced processing infrastructure, and strong innovation capabilities. The region benefits from a high concentration of ingredient manufacturers and food technology companies actively investing in protein extraction, fractionation technologies, and clean-label ingredient development. Additionally, the presence of a mature supply chain, particularly in countries like the United States and Canada—with Canada being one of the largest lentil producers globally—ensures raw material availability and supply stability. This integrated ecosystem supports efficient large-scale production and continuous product innovation, reinforcing North America’s dominant position in the market.

Asia-Pacific is emerging as the fastest-growing region, with a CAGR of 8.45% projected through 2031. This growth is driven by strong agricultural production, increasing processing capabilities, and rising adoption of plant-based protein ingredients. Countries such as India play a pivotal role, supported by robust domestic production. According to the Ministry of Agriculture and Farmers Welfare, India produced approximately 1.8 million metric tons of lentils during the 2024 rabi season, ensuring a steady raw material base for protein extraction [3]Source: Ministry of Agriculture and Farmers Welfare, "Production volume of lentils during Rabi season in India", agriwelfare.gov.in. The region is also witnessing growing investments in food processing infrastructure and ingredient standardization, enabling manufacturers to scale production and improve product quality. As regional players enhance processing technologies and integrate lentil protein into industrial applications, Asia-Pacific is becoming a key growth hub in the global market.

Europe, along with South America and the Middle East & Africa, is experiencing steady development in the lentil protein market, driven by regulatory support, sustainability initiatives, and the gradual expansion of plant-based ingredient ecosystems. In Europe, stringent regulatory frameworks promoting clean-label ingredients, transparency, and sustainable sourcing are encouraging manufacturers to adopt plant-based proteins such as lentil protein. Meanwhile, South America and the Middle East & Africa are benefiting from improving agricultural practices, increasing awareness of alternative proteins, and investments in food processing capabilities. Although these regions are at a relatively nascent stage, ongoing innovation is expected to gradually strengthen their position in the global lentil protein market.

Competitive Landscape

The global lentil protein market is moderately fragmented, with a mix of established ingredient companies and emerging plant-protein specialists competing on quality, functionality, and innovation. Key players such as AGT Food and Ingredients, Roquette Frères, Ingredion Inc., Puris Foods, and Avena Foods Limited hold significant positions, supported by robust raw material sourcing networks, processing expertise, and global distribution capabilities. These companies are actively expanding their plant-based protein portfolios, with lentil protein serving as a complementary option alongside pea and other pulse proteins.

Market competition is primarily driven by product quality, functional performance, and advancements in protein extraction and fractionation technologies. Leading companies are investing in research and development to address challenges such as solubility, taste neutrality, and consistency. Strategic initiatives, including capacity expansions, partnerships with food manufacturers, and vertical integration into pulse sourcing, are shaping the competitive dynamics. Additionally, clean-label positioning and sustainability credentials are becoming critical differentiators, influencing purchasing decisions among industrial buyers.

The market is also experiencing the entry of regional and niche players that leverage specialized processing techniques and localized sourcing advantages, intensifying competition at both global and regional levels. While large multinational companies benefit from economies of scale and established customer relationships, smaller players are competing through innovation and customized ingredient solutions. This balance between scale and specialization is expected to maintain the market’s moderate fragmentation. Ongoing advancements in plant protein technologies and growing demand for alternative proteins are likely to continue reshaping the competitive landscape.

Lentil Protein Industry Leaders

-

AGT Food and Ingredients

-

Roquette Frères

-

Ingredion Inc.

-

Puris Foods

-

Avena Foods Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: ECO Protein introduced its water lentil (duckweed) protein powder, offering a clean, sustainable, and nutritious alternative to traditional plant and dairy proteins. Water lentils require up to 10 times less land and water compared to conventional protein crops and grow directly on water without the need for farmland.

- April 2025: BENEO, a manufacturer of functional ingredients, has inaugurated its first pulse-processing plant following a construction period of one and a half years. The opening represents an investment of approximately EUR 50 million.

- September 2024: The French plant-based ingredients company, Ingood by Olga, has introduced LENGOOD, a fermented lentil powder designed for clean-label, egg-free bakery and pastry applications. The product is made from French green lentils and undergoes a natural, solvent-free fermentation process.

Global Lentil Protein Market Report Scope

Lentil protein is extracted from lentils to provide a concentrated source of plant-based protein with a neutral taste and smooth functionality. The lentil protein market is segmented by product type, end-user, and geography. Based on product type, the market is segmented into lentil protein isolate, Lentil Protein Concentrate, Lentil Protein Flour, and Textured Lentil Protein. Based on end-user, the market is market is segmented into Industrial / Food-and-Beverage Manufacturers, Animal Nutrition, and Pharmaceuticals and Dietary Supplements. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Lentil Protein Isolate |

| Lentil Protein Concentrate |

| Lentil Protein Flour |

| Textured Lentil Protein |

| Industrial / Food-and-Beverage Manufacturers | Meat Analogues | Dairy Alternatives | Bakery and Snacks |

| Beverages | |||

| Health and Sports Nutrition | |||

| Animal Nutrition | |||

| Pharmaceuticals and Dietary Supplements |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Type | Lentil Protein Isolate | |||

| Lentil Protein Concentrate | ||||

| Lentil Protein Flour | ||||

| Textured Lentil Protein | ||||

| By-End-User | Industrial / Food-and-Beverage Manufacturers | Meat Analogues | Dairy Alternatives | Bakery and Snacks |

| Beverages | ||||

| Health and Sports Nutrition | ||||

| Animal Nutrition | ||||

| Pharmaceuticals and Dietary Supplements | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Rest of North America | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| Italy | ||||

| France | ||||

| Spain | ||||

| Netherlands | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| India | ||||

| Japan | ||||

| Australia | ||||

| Rest of Asia-Pacific | ||||

| South America | ||||

| Middle East and Africa | ||||

Key Questions Answered in the Report

How large is the lentil protein market in 2025?

The lentil protein market size reached USD 123.47 million in 2025 and is forecast to grow at a 7.64% CAGR to 2030.

What is the current size of the lentil protein market?

It stood at USD 132.92 million in 2026 and is projected to reach USD 192.16 million by 2031.

Which region is growing fastest for lentil-based proteins?

Asia-Pacific, with an expected CAGR of 8.45% between 2026-2031, led by China, India, and Australia.

How do lentil proteins compare to soy and pea in allergen terms?

Lentil proteins are naturally free from the top eight FDA-listed allergens, unlike soy and some pea derivatives.

What drives the surge in animal-nutrition use of lentil protein?

Aquafeed and pet-food trials show up to 20% fishmeal or chicken-meal replacement without performance loss, lowering feed costs.

Page last updated on: