Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

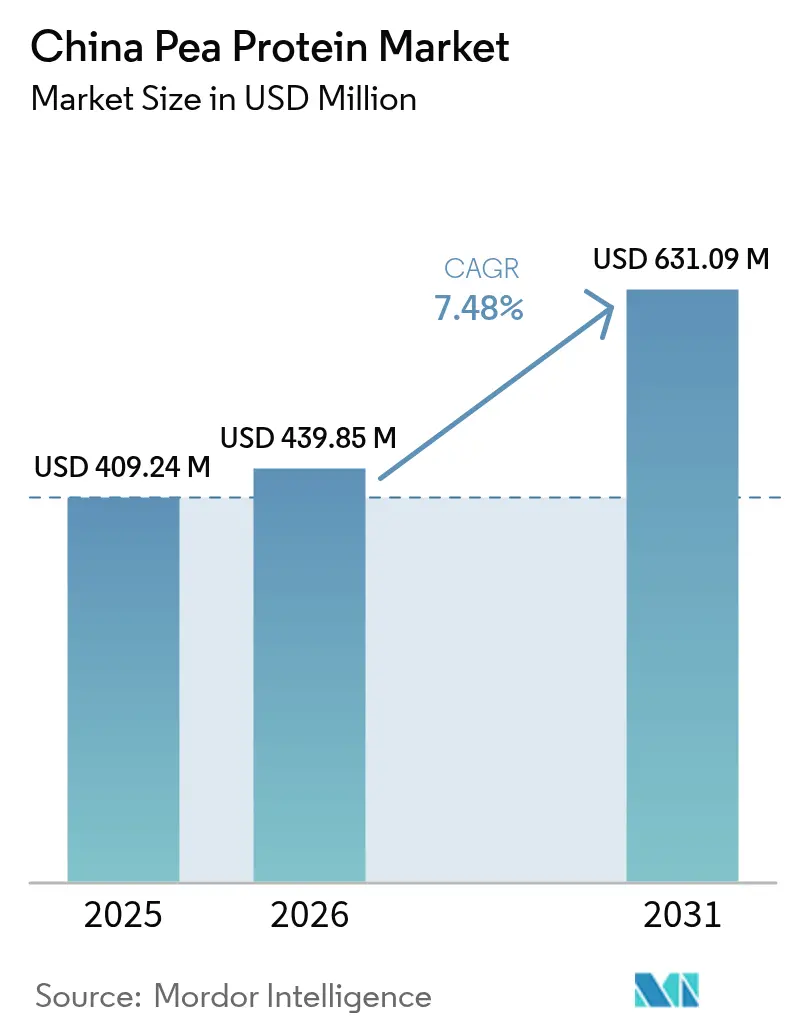

| Base Year Market Size (2025) | USD 409.24 Million |

| Market Size (2026) | USD 439.85 Million |

| Market Size (2031) | USD 631.09 Million |

| Growth Rate (2026 - 2031) | 7.48% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Pea Protein Market Analysis by Mordor Intelligence

The China pea protein market size was valued at USD 409.24 million in 2025 and estimated to grow from USD 439.85 million in 2026 to reach USD 631.09 million by 2031, at a CAGR of 7.48% during the forecast period (2026-2031). This growth is primarily fueled by the Chinese government's policy to reduce national meat consumption by 50% by 2030, encouraging consumers to adopt protein-diversified diets. Additionally, food processors are increasingly incorporating pea protein into widely consumed products, further driving demand. The rapid pace of urbanization is expanding the consumer base, while advancements in extraction technologies are improving product quality and yield. These technological breakthroughs are creating a positive feedback loop, reducing costs and enabling broader applications of pea protein. Export challenges, such as anti-dumping duties imposed by the United States and Canada, are redirecting supply to domestic markets. However, this shift is supported by government initiatives under the 14th Five-Year Plan, which are fostering research and development as well as capacity expansion. These combined factors are positioning the China pea protein market as a critical component of the country's food-security strategy, ensuring sustainable growth and resilience in the coming years.

Key Report Takeaways

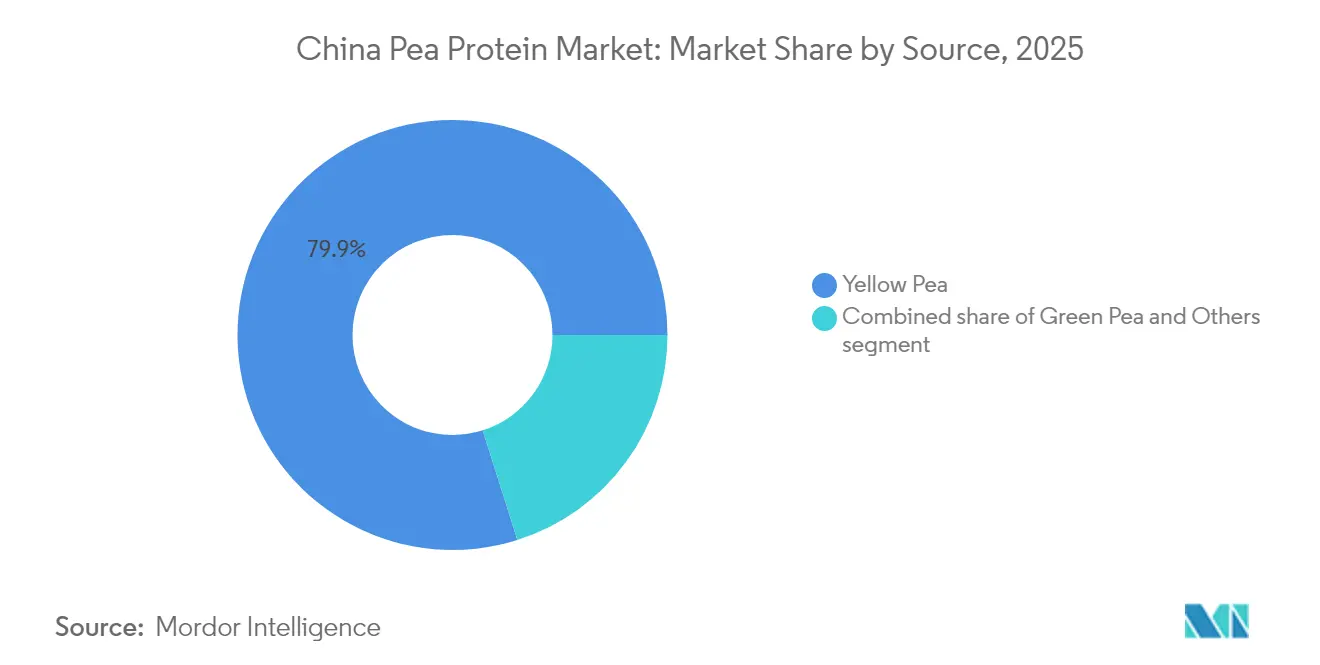

- By source, yellow pea led with 79.88% revenue share in 2025; green pea is projected to expand at an 8.28% CAGR through 2031.

- By form, isolates captured a 49.35% share of the China pea protein market in 2025, while textured/hydrolysed products are forecast to grow at a 8.01% CAGR to 2031.

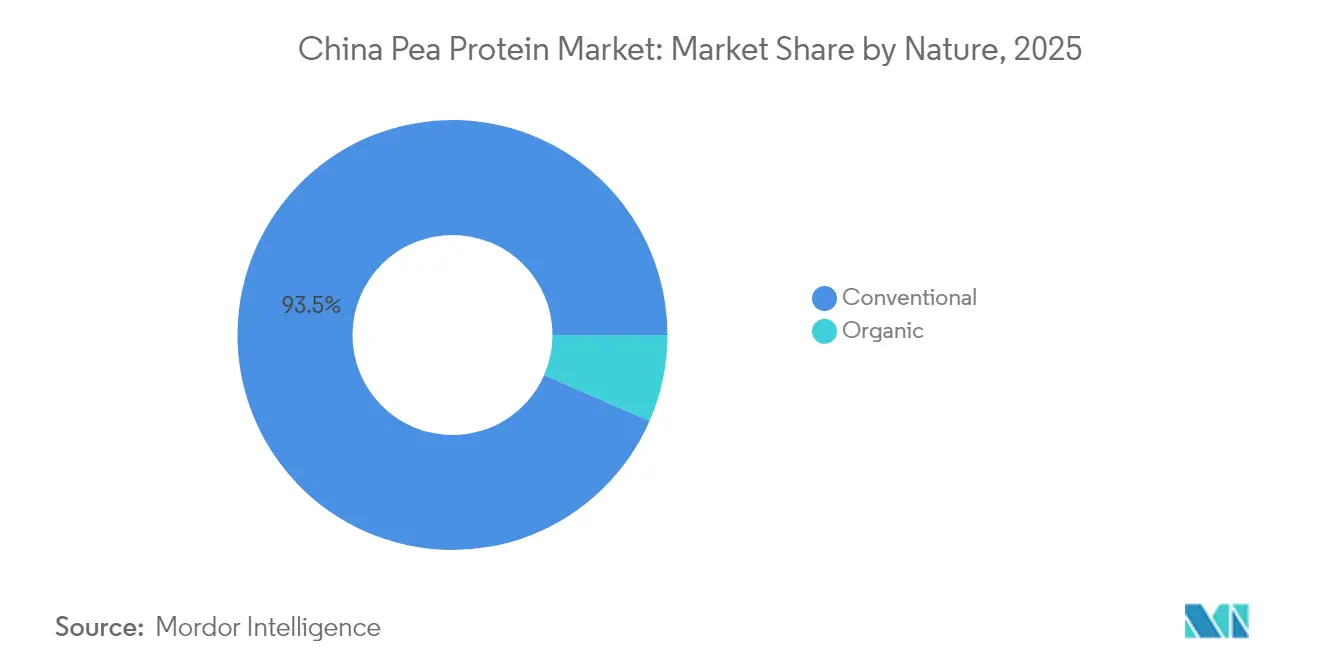

- By nature, conventional products commanded a 93.45% share of the China pea protein market in 2025; organic offerings headline a swift 8.42% CAGR to 2031.

- By application, food and beverage accounted for a 55.12% share of the China pea protein market in 2025 and is advancing at a 7.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Pea Protein Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift in consumer preference for plant-based high-protein foods | +2.8% | Urban centers in China, with higher intensity in tier-1 cities | Medium term (2-4 years) |

| Increased applications in food and beverage industry | +2.2% | Nationwide, with concentration in manufacturing hubs | Short term (≤ 2 years) |

| Technological advances in pea protein extraction | +1.8% | Manufacturing centers in Eastern China | Medium term (2-4 years) |

| Major soybean production and low input costs | +1.4% | Agricultural regions in Northeast and North China | Long term (≥ 4 years) |

| Policies promoting plant-based diets are supporting market growth | +1.6% | National, with early implementation in urban areas | Medium term (2-4 years) |

| The expanding vegan and vegetarian demographic in china is driving demand for pea protein. | +1.5% | Urban centers, particularly tier-1 and tier-2 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift in consumer preference for plant-based high-protein foods

China has overtaken the United States in total protein consumption, yet it boasts a notably higher intake of plant-based proteins. This dietary pivot is bolstered by government initiatives, notably a target to cut meat consumption in half by 2030. Such moves have opened up significant market avenues for pea protein, heralded as a sustainable alternative. The shift in consumer preferences isn't limited to the conventional vegetarian crowd; it's now embraced by health-focused urbanites. A 2024 survey underscores this trend, revealing a pronounced interest among Chinese consumers in amplifying their plant-based food consumption. Additionally, the rising awareness of environmental sustainability and the health benefits associated with plant-based diets are further driving this transition. Interestingly, while Chinese consumers don't see plant-based meat alternatives as mere meat stand-ins, they regard them as added protein sources. This perspective carves out a distinct market landscape, promoting the fusion of pea protein into both age-old Chinese dishes and modern culinary creations. Furthermore, the growing investments in research and development by domestic and international players are expected to enhance the quality and variety of pea protein-based products, further fueling market growth.

Increased applications in food and beverage industry

In China, the food and beverage industry is significantly expanding the applications of pea protein, transitioning from its conventional use in meat substitutes to innovative products tailored to local dietary preferences. STARFIELD, a leading domestic player in the plant-based market, is actively broadening its product portfolio by introducing snack lines fortified with pea protein, showcasing the ingredient's versatility and growing consumer appeal. Manufacturers are capitalizing on the opportunity to incorporate pea protein into traditional Chinese dishes, enhancing nutritional value while preserving the authentic flavors that resonate with consumers. Recent advancements in high-moisture extrusion technology have further propelled the development of plant-based meat alternatives, delivering improved texture and sensory experiences that address prior consumer concerns. Moreover, the introduction of hybrid protein blends, such as the combination of pea protein isolate and whey protein, is enabling the production of meat analogs with superior hardness, cohesiveness, and fibrous structures, closely replicating the characteristics of animal-based products. This evolution underscores the growing potential of pea protein in meeting both nutritional and sensory demands in the Chinese market.

Technological advances in pea protein extraction

In China, breakthrough extraction technologies are reshaping the economics and quality of pea protein. Innovations in cavitation technologies are notably boosting protein recovery rates and enhancing functional properties. Studies reveal that the ultrasonic probe (US-probe) and hydrodynamic cavitation (HDC) methods achieve protein recovery rates of 52.53 g/hg and 56.85 g/hg, respectively. Notably, HDC stands out for its industrial scaling potential. These cutting-edge extraction techniques not only maintain the primary structure of pea proteins but also strategically modify secondary and tertiary structures to boost functionality. This addresses earlier challenges related to solubility and sensory attributes. Meanwhile, mild fractionation techniques are emerging as a sustainable substitute for conventional wet fractionation. They not only safeguard the native protein structure but also enhance the interfacial performance of pea protein in emulsions. This enhancement is vital for applications that demand better lubrication and mouthfeel. The Beijing Academy of Food Sciences underscores the importance of these processing innovations. They play a pivotal role in boosting the nutritional and sensory attributes of plant-based meat alternatives, underscoring technological advancement as a primary catalyst for market growth.

Major soybean production and low input costs

China's Ministry of Agriculture is spearheading a strategic pivot in livestock feeding practices, aiming to curtail soybean meal usage. This move not only underscores the nation's commitment to diversifying its feed sources but also heralds a golden opportunity for alternative proteins, notably pea protein, to carve a niche in both human and animal nutrition. The "Three-Year Action Plan for Reducing Soybean Meal in Feed" sets an ambitious target: trim the soybean meal content in feed from the current 14.5% to under 13% by 2025. Achieving this could slash consumption by a staggering 6.8 million tonnes, leaving a lucrative market gap for alternative proteins to fill. Companies are already heeding the call, with many reporting marked reductions in soybean meal usage. Some have even fine-tuned their feed formulations, integrating alternative proteins to achieve levels as low as 5.7%. Meanwhile, the USDA's projections for China's soybean landscape in MY 25/26 stand at a production of 19.8 million metric tons (MMT) and a hefty import figure of 106 MMT[1]United States Department of Agriculture, "Report Name: Oilseeds and Products Annual", www.apps.fas.usda.gov. This underscores the enduring significance of protein crops in China's agricultural narrative. Furthermore, China's robust infrastructure and deep-seated expertise in soybean cultivation and processing not only bolster its agricultural landscape but also pave the way for a burgeoning pea protein industry. As the demand for diverse protein sources surges, this foundation promises efficient knowledge transfer and resource optimization, ensuring the industry scales seamlessly.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from other plant-based proteins | +0.9% | Nationwide, with higher intensity in urban markets | Medium term (2-4 years) |

| Sensory challenges (beany flavor) limiting adoption | +0.7% | Urban centers with sophisticated consumer base | Short term (≤ 2 years) |

| Fluctuating pea prices | +1.1% | National, with higher impact on manufacturing regions | Short term (≤ 2 years) |

| Ensuring a consistent supply of quality peas is difficult | +0.8% | Agricultural and manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from other plant-based proteins

In China, the alternative protein market faces stiff competition from traditional plant-based sources. These traditional sources, like tofu and wheat gluten (seitan), not only enjoy cultural familiarity but also come at significantly lower price points than their novel counterparts. Deeply rooted in Chinese culinary traditions, tofu and seitan are priced much lower than imported or newly developed pea protein products. This pricing gap poses a substantial hurdle for the adoption of pea protein, especially in segments sensitive to price changes. Adding to the competitive landscape, the Chinese government, through its agricultural five-year plan, has thrown its weight behind a broad spectrum of alternative proteins, endorsing both plant-based and cultivated meat initiatives. This backing amplifies the competitive stakes for pea protein, which now needs to carve out clear advantages over both established and emerging protein sources. Moreover, the market is further complicated by consumer preferences that lean towards products resonating with local tastes and dietary habits. This necessitates significant product adaptation and localization efforts for pea protein to effectively challenge the dominance of traditional sources.

Sensory challenges (beany flavor) limiting adoption

In China, where culinary traditions and taste preferences run deep, the persistent beany off-flavors in pea protein are curtailing its market potential. Research published by Science Direct in 2023 pinpoints that these off-flavors stem from volatile compounds, produced during processing via lipoxygenase and hydroperoxide lyase pathways, posing hurdles to consumer acceptance, especially in flavor-sensitive applications. This challenge resonates strongly in China. A study highlighted that for Chinese consumers, taste, alongside nutritional value and caloric content, plays a pivotal role in purchasing decisions regarding meat substitutes. The repercussions of these sensory hurdles are underscored by the struggles of international plant-based brands like Beyond Meat in China. Despite rolling out adaptations like pork-flavored meatballs, the brand has found it tough to make inroads, underscoring the paramount importance of flavor in achieving market success. While there's ongoing development of innovative processing techniques and flavor-masking strategies, scaling these solutions commercially proves daunting, especially for domestic manufacturers with constrained R&D resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Yellow Pea Dominates Production Landscape

In 2025, yellow pea, with an 79.88% market share, solidifies its position as the backbone of China's pea protein industry, thanks to its superior protein content and well-established cultivation practices. China's heavy reliance on imported yellow peas, predominantly sourced from Canada, underscores this dominance, with imports hitting 2.6 million tons in 2023, as highlighted by the China Pea Conference and Plant-Based Congress. Major Chinese manufacturers, such as Shandong Jianyuan Bioengineering Co., Ltd. and Yantai Shuangta Food Co., Ltd., have set up a robust processing infrastructure, fine-tuning their extraction processes specifically for yellow pea varieties. Meanwhile, other segments like green pea and specialty varieties, including split pea and marrowfat, carve out niche roles in the market, often leveraging their unique traits for specific applications.

Green pea is on the rise, boasting an 8.28% CAGR from 2026-2031, fueled by its unique nutritional benefits and growing use in premium protein products. Innovations in extraction technologies play a pivotal role, ensuring the preservation of green peas' distinct phytonutrients and antioxidants, bolstering the protein's health appeal. Comparative research on commercial pea proteins highlights notable differences in functional properties, influenced by both the source material and extraction techniques. Such insights are reshaping sourcing strategies for Chinese manufacturers, emphasizing the critical role of pea variety selection in enhancing product quality and application potential. This refined approach to sourcing signals a maturation phase for the Chinese pea protein industry, transitioning from mere commodity processing to the development of specialized, application-driven ingredients.

By Form: Isolates Lead with Functional Versatility

In 2025, isolates held a 49.35% market share, driven by their high protein content and versatility in applications like beverages and meat alternatives. Products from Chinese manufacturers, such as Shuangta Food Co., Ltd. and Shandong Jianyuan Bioengineering Co., Ltd., typically feature isolates with 76%-85% protein content, making them ideal for protein-rich products. Advances in extraction technologies, including ultrasonic probe and hydrodynamic cavitation methods, have improved protein recovery rates to 52.53 g/hg and 56.85 g/hg, enhancing yield and functionality. Concentrates and textured forms address specific needs: concentrates offer cost efficiency for less protein-sensitive uses, while textured forms provide the structure essential for meat analogs.

From 2026 to 2031, the textured/hydrolyzed segment is projected to grow at an 8.01% CAGR, fueled by high-moisture extrusion technology and rising demand for advanced meat alternatives. Improvements in high-moisture extrusion (HME) have resolved texture and sensory issues in plant-based meats. Studies show blending pea protein isolate with complementary proteins enhances structural properties like hardness, cohesiveness, and fibrous texture, critical for meat analogs. These innovations are pivotal in China, where texture and mouthfeel drive consumer acceptance of plant-based meats. Chinese manufacturers are now producing authentic meat substitutes, expanding appeal from niche vegetarian products to mainstream alternatives.

By Nature: Conventional Production Scales While Organic Accelerates

In 2025, conventional pea protein commands a dominant 93.45% market share in China, bolstered by established supply chains, cost efficiencies, and widespread availability. These advantages position conventional pea protein as the cornerstone of China's industry. Manufacturers leverage the scale of this segment to set competitive price points, driving mainstream adoption across a spectrum of applications, from mass-market food products to animal feed formulations. Historically, the conventional segment has played a pivotal role in China's export-driven pea protein landscape, emphasizing high-volume production for global markets. Yet, a recent challenge has emerged: the U.S. and Canada have imposed anti-dumping duties on select Chinese pea protein products, ranging from a staggering 112% to 270%. This trade hurdle is nudging conventional pea protein producers to explore domestic avenues and seek alternative export markets, altering the industry's competitive dynamics.

The organic segment is on a growth trajectory, with an 8.42% CAGR forecasted for 2026-2031. This rise aligns with China's organic food market, growing at 30% annually. Urban consumers, especially in tier-one cities, are prioritizing health and environmental factors, driving demand for organic pea protein. Positioned as a premium product, it caters to the need for high-quality, traceable ingredients, enabling manufacturers to command higher prices and margins. With rising food safety concerns, consumers increasingly prefer certified organic products with transparent supply chains.

By Application: Food & Beverage Drives Innovation and Volume

In 2025, the food and beverage segment holds a 55.12% market share and is projected to grow at a 7.62% CAGR from 2026 to 2031, reinforcing its role as the key driver of China's pea protein market. This growth reflects pea protein's adaptability, spanning traditional Chinese dishes, plant-based innovations, and health-focused beverages. While coconut and soy milks dominate, pea protein-based alternatives are gaining ground due to their nutritional benefits and allergen-free appeal. The sector's growth aligns with evolving consumer preferences for nutrition, flavor, and calorie-conscious plant-based products.

Pea protein's applications are diversifying beyond traditional uses. Demand for specialized nutrition products is rising, with research highlighting its role in beverages targeting specific dietary needs. The Chinese government’s push for artificial meat to enhance food security and reduce environmental impact supports pea protein's integration into meat substitutes, despite consumer preference for conventional meats. Policy support is critical in addressing consumer hesitance through education and awareness. The animal feed industry is also expanding as companies adapt to policies reducing soybean meal usage. Meanwhile, the personal care and cosmetics sector is leveraging pea protein's unique properties in premium formulations, adding value to niche offerings.

Geography Analysis

China's domestic pea protein market is undergoing a significant transformation. Manufacturers, previously focused on exports, are now prioritizing local demand, driven by both necessity and opportunity. This shift aligns with the rapid expansion of the domestic market, supported by government policies that promote alternative proteins and aim to reduce meat consumption. The government's commitment to this sector is evident in the establishment of China's first fermentation and cultivated meat research center in Beijing. This USD 10.9 million initiative seeks to bridge the gap between laboratory research and industrial production, positioning alternative proteins as a vital component of the nation's food security strategy. Additionally, the government is actively encouraging innovation and investment in the alternative protein sector to meet the growing demand for sustainable food solutions.

Eastern China, particularly manufacturing hubs in provinces like Shandong, plays a pivotal role in pea protein production. These hubs benefit from well-established processing infrastructure and proximity to major urban markets, making them ideal for scaling production. The region's manufacturing capabilities are advancing with the adoption of cutting-edge extraction technologies. Recent research highlights significant improvements in protein recovery rates through innovations such as ultrasonic probe and hydrodynamic cavitation methods. These advancements not only enhance yield but also improve the quality of pea protein, addressing previous challenges related to functionality and sensory characteristics. However, the concentration of production in this region also brings challenges, particularly in sourcing raw materials. China remains heavily dependent on imported peas for protein production, with 2.6 million tons imported in 2023. Canada continues to be the largest supplier, underscoring the importance of maintaining strong international trade relationships despite the challenges in exporting finished protein products. Efforts to diversify raw material sources and enhance domestic pea cultivation are gaining traction to reduce reliance on imports.

Urban centers, especially tier-one cities like Beijing, Shanghai, and Guangzhou, dominate the consumption landscape for pea protein products. This trend is driven by higher disposable incomes, greater health consciousness, and a growing interest in sustainable food options among urban consumers. Research on Chinese consumer behavior indicates that individuals with higher income and education levels are more likely to purchase plant-based meat alternatives, creating a clear demographic profile of the typical consumer as urban professionals. This concentration of consumption in urban areas presents opportunities for premium product positioning and innovative formats, such as ready-to-eat meals and fortified snacks. However, expanding market penetration into lower-tier cities and rural areas remains a challenge due to higher price sensitivity and deeply ingrained traditional dietary habits. To address this, manufacturers are exploring cost-effective production methods and targeted marketing strategies to make plant-based products more accessible and appealing to a broader audience.

Competitive Landscape

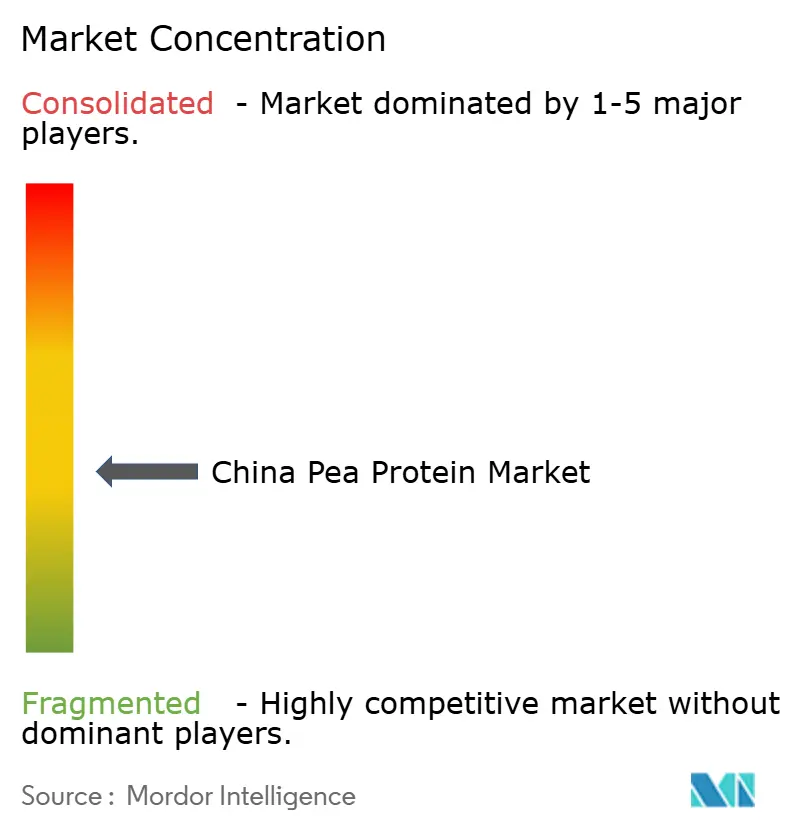

The China pea protein market is moderately fragmented, with local and international players competing for market share. Key companies include Archer Daniels Midland Company, Yantai Shuangta Food Co. Ltd, Shandong Jianyuan Health Industry Co., Ltd, Roquette Frères SA, and ETChem. Rising demand for vegan and plant-based foods is driving the need for plant-based ingredients. Companies are investing in R&D to develop innovative pea protein products and strengthen their market position.

Technological advancements are critical for competitive differentiation. Companies are improving extraction methods and processing technologies to enhance protein functionality and address sensory challenges. Comparative studies of commercial pea proteins from Chinese manufacturers show variations in protein content and functional properties, emphasizing the role of processing expertise in product quality. As competition grows, firms are focusing on proprietary technologies to improve protein recovery and sensory attributes, creating barriers for new entrants.

Supportive government policies are shaping the market. Initiatives like a USD 93 million investment in biomanufacturing research and the establishment of China’s first alternative protein innovation center are fostering industry-research collaborations. These efforts are expected to accelerate innovation and drive market growth, positioning China as a key player in the global alternative protein market.

China Pea Protein Industry Leaders

-

Archer Daniels Midland Company

-

Yantai Shuangta Food Co. Ltd

-

Roquette Frères SA

-

ETChem

-

Shandong Jianyuan group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Axiom Foods responded to steep U.S. tariffs on Chinese pea protein by launching large-scale production of Vegotein N, a highly neutral, allergen- and GMO-free pea protein that eliminates the need for flavor masking and offers 80% protein content. This move addresses supply chain disruptions and delivers a competitively priced, functional ingredient for manufacturers seeking local, high-quality plant protein.

- February 2024: Roquette expanded its Nutralys plant protein portfolio by introducing four new multi-functional pea proteins: NutralysPeaF853M (isolate), Nutralys H85 (hydrolysate), Nutralys T Pea 700FL (textured), and Nutralys T Pea 700M (textured). These ingredients, available globally, including in China, are tailored to help food manufacturers craft plant-based foods and high-protein nutritional products, such as nutritional bars, protein drinks, and alternatives to meat and dairy.

China Pea Protein Market Report Scope

Pea protein is a food product and protein supplement derived and extracted from yellow and green split peas, Pisum sativum.

The China pea protein market is segmented by source, form, nature, and application. By Source, the market is segmented into yellow pea, green pea, and others. Based on form, the market is segmented into protein concentrates, isolates, and textured/hydrolyzed protein. By nature, the market is segmented into conventional and organic. Based on application, the market is segmented into food and beverages, nutrition and health supplements, animal feed, personal care, and cosmetics. The food and beverage segment is further sub-segmented into the meat/poultry/seafood and meat alternative products, dairy and dairy alternative products, bakery, snacks and cereals, beverages, confectionery, and others. The nutrition and health supplements are further sub-segmented into sports/performance nutrition, infant & pediatric nutrition, clinical, and elderly nutrition. The Animal feed segment is further sub-segmented into aquafeed, petfood, and livestock feed.

The market sizing has been done in value terms in USD and for volume terms in volume in tons for all the abovementioned segments.

By Source

| Yellow Pea |

| Green Pea |

| Others (Split Pea, Marrowfat) |

By Form

| Isolate |

| Concentrate |

| Textured/Hydrolyzed |

By Nature

| Conventional |

| Organic |

By Application

| Food and Beverage | Meat/Poultry/Seafood and Meat Alternative Products |

| Dairy and Dairy Alternative Products | |

| Bakery | |

| Snacks & Cereals | |

| Beverages | |

| Confectionery | |

| Others | |

| Nutrition and Health Supplements | Sport/Performance Nutrition |

| Infant & Pediatric Nutrition | |

| Clinical & Elderly Nutrition | |

| Animal Feed | Aquafeed |

| Pet Food | |

| Livestock Feed | |

| Personal Care and Cosmetics |

| By Source | Yellow Pea | |

| Green Pea | ||

| Others (Split Pea, Marrowfat) | ||

| By Form | Isolate | |

| Concentrate | ||

| Textured/Hydrolyzed | ||

| By Nature | Conventional | |

| Organic | ||

| By Application | Food and Beverage | Meat/Poultry/Seafood and Meat Alternative Products |

| Dairy and Dairy Alternative Products | ||

| Bakery | ||

| Snacks & Cereals | ||

| Beverages | ||

| Confectionery | ||

| Others | ||

| Nutrition and Health Supplements | Sport/Performance Nutrition | |

| Infant & Pediatric Nutrition | ||

| Clinical & Elderly Nutrition | ||

| Animal Feed | Aquafeed | |

| Pet Food | ||

| Livestock Feed | ||

| Personal Care and Cosmetics | ||

Key Questions Answered in the Report

What is the current value of the China pea protein market?

The China pea protein market stands at USD 439.85 million in 2026 and is forecast to reach USD 631.09 million by 2031.

Which segment holds the largest share by source?

Yellow pea dominates with 79.88% revenue share in 2025, benefiting from mature supply chains and high protein yield.

Why are isolates preferred in beverage applications?

Isolates deliver 76-85% protein purity and superior solubility, essential for clear drinks and ready-to-mix powders.

What is the main barrier to wider consumer adoption?

Sensory issues such as beany flavour remain a hurdle, although enzymatic and filtration innovations are progressively mitigating this challenge.

Page last updated on: