Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

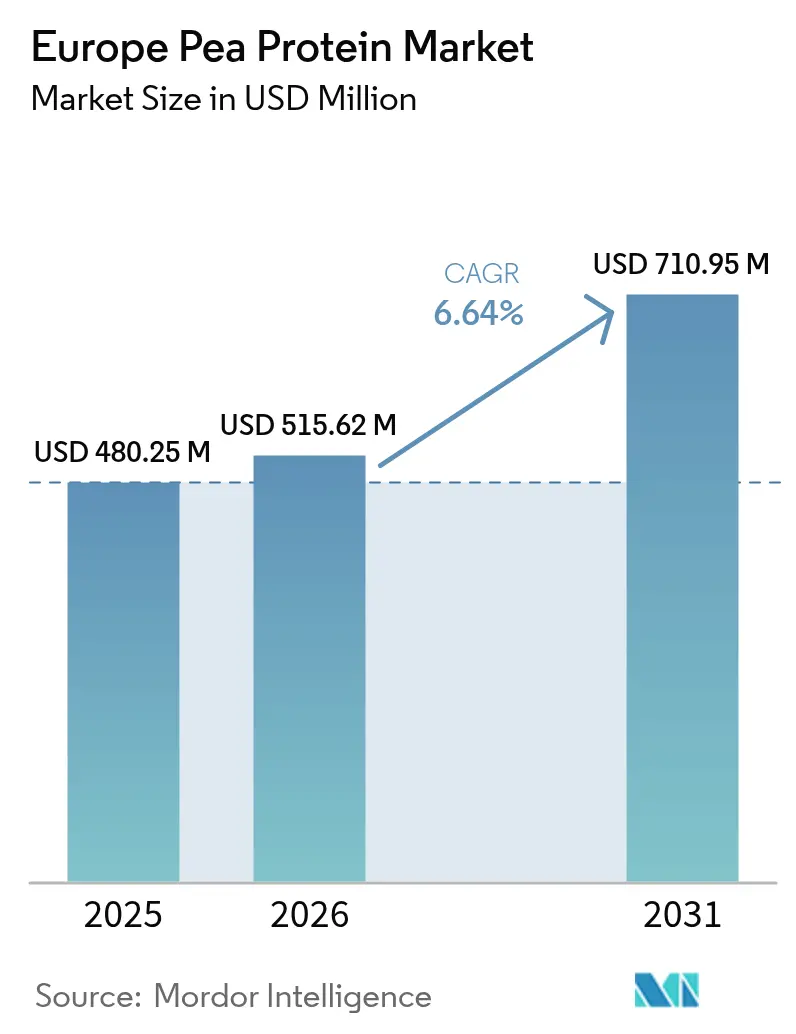

| Base Year Market Size (2025) | USD 480.25 Million |

| Market Size (2026) | USD 515.62 Million |

| Market Size (2031) | USD 710.95 Million |

| Growth Rate (2026 - 2031) | 6.64% CAGR |

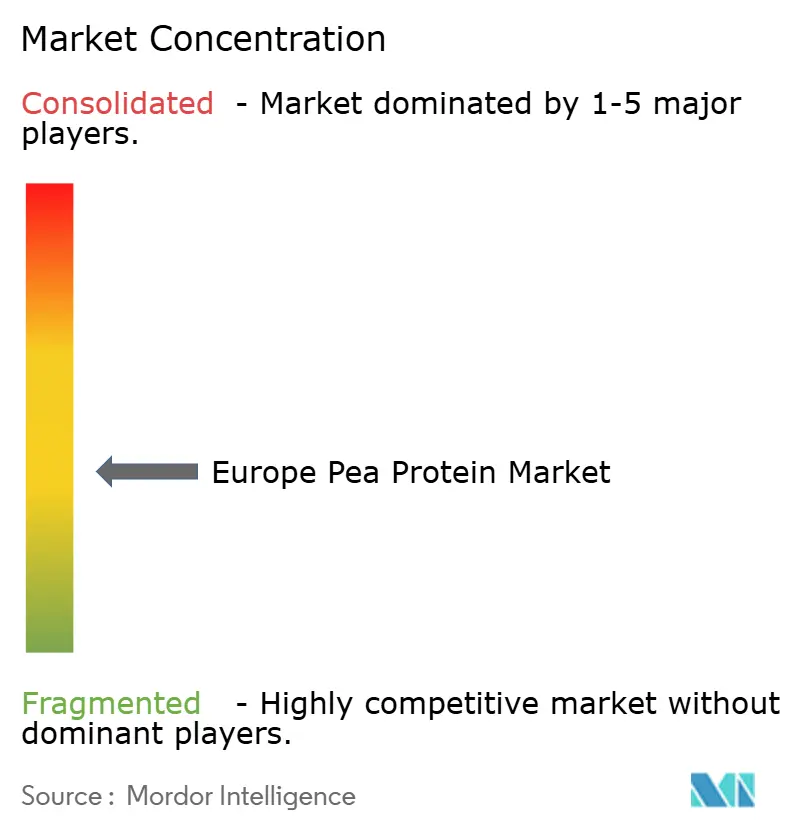

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Pea Protein Market Analysis by Mordor Intelligence

The Europe pea protein market size is projected to be USD 0.48 billion in 2025, USD 0.52 billion in 2026, and reach USD 0.71 billion by 2031, growing at a CAGR of 6.6% from 2026 to 2031. Cost compression driven by membrane-filtration retrofits, together with expanded crop contracts that reduce raw-material volatility, is bringing pea protein within reach of mainstream formulators. Government protein-transition programs across France, Germany, and the Netherlands continue to subsidize capacity additions, making Europe the fastest-growing regional hub for legume ingredients. Large food groups are speeding vertical integration. Kerry Group, Danone, and Nestlé each added dedicated European pea-protein lines in 2025 to secure traceable supply and sidestep freight shocks tied to imported soy. Meanwhile, retailers are using clean-label scorecards that favor short ingredient lists, a shift that directly benefits pea isolates, which need fewer masking agents than soy or wheat proteins

Key Report Takeaways

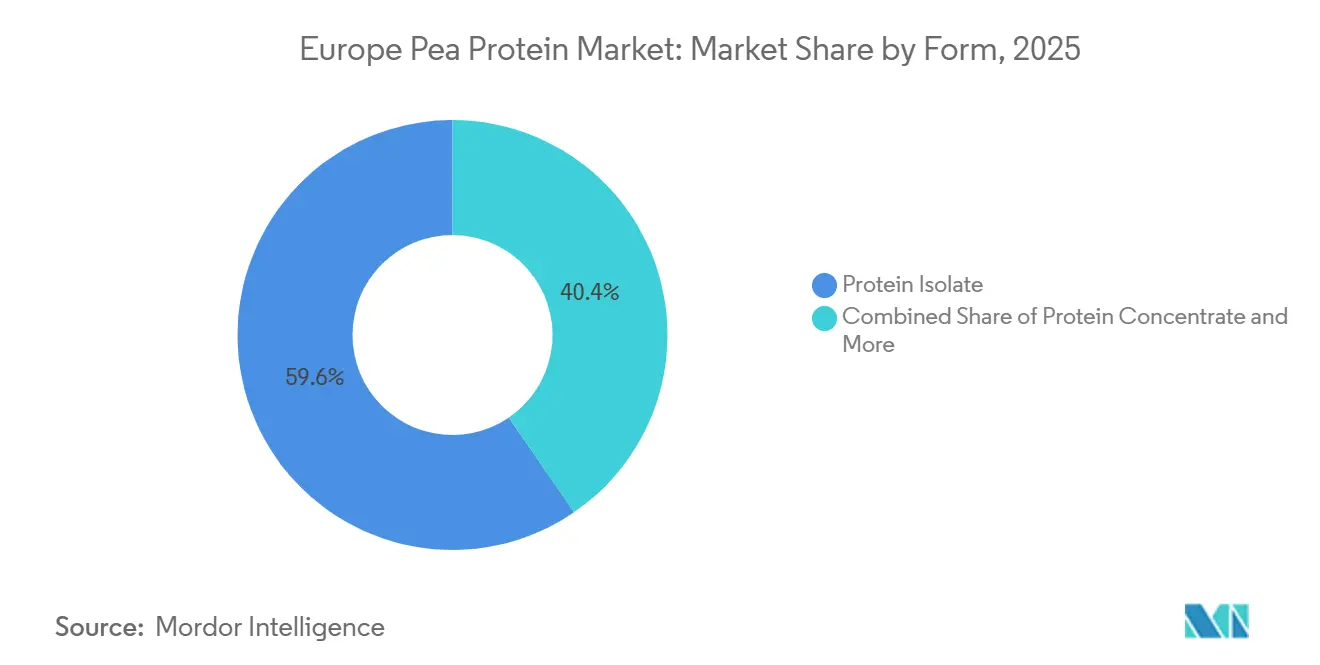

- By form, isolates held 66.1% Europe pea protein market share in 2025 and are forecast to expand at a 7.7% CAGR through 2031.

- By product category, conventional variants captured 85.4% of the Europe pea protein market size in 2025, while organic offerings are projected to grow at an 8.1% CAGR to 2031.

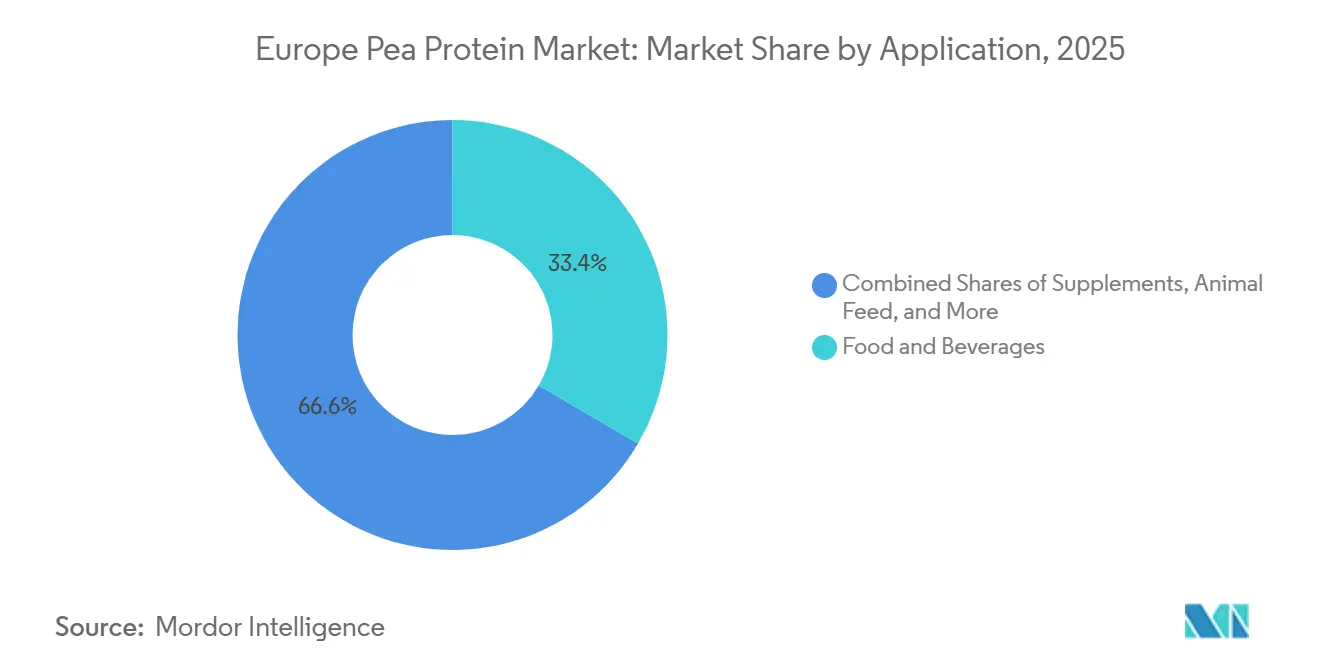

- By application, food and beverages led with 33.4% revenue in 2025; supplements are the fastest-rising use case, advancing at an 8.9% CAGR through 2031.

- By geography, Germany commanded 33.6% regional revenues in 2025, whereas France is on track for the fastest 9.0% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Pea Protein Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Plant-Based Food and Beverage Sectors | +1.8% | Germany, UK, Netherlands, France | Medium term (2-4 years) |

| Rising Veganism and Vegetarianism | +1.2% | UK, Germany, Sweden, Belgium | Long term (≥ 4 years) |

| Technological Advancements in Production | +0.9% | Germany, France, Netherlands | Short term (≤ 2 years) |

| Consumer Preference for Clean and Transparent Labeling | +0.7% | Germany, UK, France, Sweden | Medium term (2-4 years) |

| Investment in Research, Development, and Production Capabilities | +0.6% | Germany, France, Netherlands, Belgium | Long term (≥ 4 years) |

| Rising Demand for Sports Nutrition | +0.8% | UK, Germany, Spain, Italy | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Plant-Based Food and Beverage Sectors Drive Ingredient Demand

In 2025, Europe's plant-based meat sector recorded retail sales of EUR 3.6 billion (USD 3.9 billion). Pea protein accounted for approximately 40% of total protein inputs among leading brands, replacing soy due to its non-GMO status and favorable amino-acid profile for texturization. Unilever's Vegetarian Butcher and Nestlé's Garden Gourmet reformulated their core SKUs in 2025 to feature pea isolate as the primary protein. This decision was supported by consumer tests, which showed a 28% increase in repeat purchases when "pea protein" was prominently displayed on packaging compared to the generic "plant protein" label. This shift highlights the growing recognition of pea protein's benefits: its neutral taste and light color enable cleaner labels with only 3-4 masking ingredients, compared to the 8-10 typically required for soy-based products. This simplicity appeals to European consumers, who rank ingredient clarity as the second-most-important purchasing factor after taste. Dairy-alternative manufacturers are also adapting to this trend. In early 2026, Danone's Alpro brand launched pea-protein yogurt alternatives in Germany and France, targeting lactose-intolerant consumers who find almond and oat bases texturally inadequate. The beverage industry is also advancing in this direction. Ready-to-drink protein shakes are being reformulated to meet clean-sport certifications, which are increasingly scrutinizing whey supply chains for antibiotic residues—a concern absent in plant proteins.

Rising Veganism and Vegetarianism Reshape Protein Consumption Patterns

In 2025, approximately 10% of Germany's population identified as vegetarian or vegan, an increase from 8% in 2023. National dietary surveys show similar trends in the UK and Sweden, with 9% and 12% respectively. This change is most evident among urban millennials and Gen-Z, who are 3-4 times more likely than older generations to pay a premium for plant-based proteins. This has resulted in a segmented market where premium pea-isolate products coexist with more cost-effective concentrate options. Flexitarians, individuals reducing but not fully eliminating animal protein, make up a significant 30% of the European population and are the primary drivers of growth in hybrid products. These products combine pea protein with small amounts of dairy or egg to improve texture and reduce costs. Retail data from 2025 showed that in France and Spain, hybrid burgers containing 60% pea protein and 40% beef outsold 100% plant-based alternatives by a 2:1 margin. This suggests that pea protein's growth is driven more by incremental replacement of animal protein in mainstream diets than by converting committed vegans. As a result, ingredient suppliers are focusing on improving functionalities, such as enzymatic hydrolysis for enhanced emulsification, to make pea protein effective at lower inclusion rates. This approach reduces formulation costs and broadens market accessibility.

Technological Advancements Lower Costs and Improve Functionality

From 2023 to 2025, Roquette and Cosucra, which collectively manage 7 of Europe's 15 largest pea-protein facilities, achieved energy efficiency improvements of 18-22% in wet-fractionation processes used to isolate pea protein. These advancements were driven by membrane-filtration upgrades and the adoption of waste-heat recovery systems. Consequently, the cost gap between pea isolate and soy isolate narrowed from approximately USD 1.80 per kilogram in 2023 to USD 1.20 per kilogram in 2025. This price reduction is considered pivotal by food manufacturers for wider adoption in price-sensitive segments such as bakery and snacks. Concurrently, enzyme-modification methods have reduced off-flavors and enhanced gel-forming properties, expanding the range of applications for pea protein. Ingredion's 2025 launch of a pre-gelatinized pea isolate supports cold-process formulations in dairy alternatives, preserving heat-sensitive vitamins and colors by eliminating the need for thermal treatment. Moreover, patent filings for pea-protein processing methods in the EU Intellectual Property Office rose by 34% in 2024-2025, with German and Dutch applicants leading the way, highlighting continued R&D efforts[1]Source: Eurostat, “Industrial Energy Prices 2024-2025,” ec.europa.eu.

Consumer Preference for Clean and Transparent Labeling

In a 2025 survey of 12,000 respondents from Germany, France, the United Kingdom, and Spain, European consumers ranked "recognizable ingredients" as the most important factor in building trust in packaged foods, according to the BUEC[2]Source: BEUC, “Consumer Ingredient Trust Survey 2025,” beuc.eu. Notably, 68% of respondents reported avoiding products with more than five ingredients they could not identify. This preference benefits pea protein, which requires fewer co-ingredients for stabilization. In comparison, soy protein isolate often relies on additives like lecithin, carrageenan, or gums to mask its beany flavor and achieve a desirable texture. Retailers are leveraging this trend through private-label strategies. For example, Tesco's Plant Chef range in the UK reformulated 14 SKUs in 2025 to use pea protein exclusively. The packaging emphasized "just 4 ingredients," resulting in a 19% increase in sales velocity compared to earlier formulations. Organic certification provides an additional layer of differentiation, particularly in Germany and Austria, where organic foods account for over 12% of grocery spending. Although organic pea protein commands a 40-50% premium over conventional variants, its supply remains limited due to a shortage of certified acreage and the longer crop-rotation cycles required to maintain soil health without synthetic inputs. This supply-demand imbalance has driven interest in contract farming investments. For instance, Emsland Group has secured multi-year agreements for 8,000 hectares of certified organic pea cultivation in northern Germany and Poland, guaranteeing farmers a floor price indexed to conventional peas with an additional 25% premium.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher production costs compared to other proteins like soy or animal sources | -1.2% | Global; most acute in Western & Northern Europe where input and energy costs are elevated | Medium term (2–4 years) |

| Competition from established soy, rice, or other plant proteins | -0.9% | EU-wide; particularly intense in Germany, Netherlands, and Belgium where soy processing infrastructure is mature | Long term (≥ 4 years) |

| Consumer skepticism about novel proteins | -0.6% | Eastern Europe and Russia, with spill-over into Southern Europe (Italy, Spain) | Medium term (2–4 years) |

| Regulatory and labeling hurdles | -0.5% | EU-wide; driven by EU Novel Food Regulation (EC) No 2015/2283 and national-level labeling compliance requirements | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Production Costs Constrain Margin Expansion in Price-Sensitive Segments

In 2025, pea-protein isolate production costs in Europe averaged EUR 4.20-4.80 per kilogram (USD 4.55-5.20), about 35-40% higher than soy isolates and 60-70% above whey concentrates on a protein-equivalent basis. These elevated costs were due to lower extraction yields; protein recovery from raw peas is 18-22%, compared to 30-35% for soybeans, and higher energy consumption during drying and milling. This cost disadvantage limited adoption in high-volume, low-margin markets like bakery and confectionery, where ingredient costs must stay within 8-10% of the finished product price to maintain retailer margins. Rising energy costs worsened the situation. Industrial electricity rates in Germany and Belgium rose 12-15% during 2024-2025, despite broader energy market stabilization, straining processors without renewable energy sources, as noted by Eurostat[3]. Additionally, yellow-pea prices in France spiked 18% in early 2025 due to droughts in key growing regions, forcing processors to either absorb losses or pass costs to customers, which led to formulation shifts to soy in some private-label meat alternatives. Scaling up is critical for cost reduction, but achieving economies of scale similar to soy requires facilities with over 100,000 metric tons of annual capacity. Currently, only three plants in Europe meet this threshold, and reaching it requires capital investments of EUR 200-300 million (USD 215-325 million), deterring new entrants and consolidating the market around established players.

Competition From Soy and Emerging Plant Proteins Fragments Demand

In 2025, soy protein held a 45% share of Europe's plant-based protein ingredient market, driven by established supply chains, competitive pricing, and decades of formulation expertise that minimize trial and error for food manufacturers. Rice protein gained traction in Southern Europe, particularly in Spain and Italy, where local rice cultivation and cultural familiarity helped it capture 8% of the regional market. Its growth was notable in hypoallergenic applications like infant formula and medical nutrition. Faba-bean and chickpea proteins are emerging as strong contenders, with EU-funded research exploring their potential to rival or surpass pea protein's functionality while offering agronomic benefits such as improved soil structure and water retention. However, the rise of alternatives is fragmenting R&D efforts and slowing pea protein's market-share growth, despite increasing volumes. Hybrid formulations blending multiple plant proteins to optimize cost and functionality are further diluting single-ingredient demand. A 2025 analysis of 200 plant-based meat products from major European retailers showed 62% contained two or more plant proteins, with pea-soy blends being the most common.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Isolates Dominate Through Superior Functionality

In 2025, protein isolates accounted for 66.12% of the European pea protein market and are expected to grow at a 7.72% CAGR through 2031. Their 85-90% protein content and neutral organoleptic properties make them ideal for beverages, clinical nutrition, and infant formula, where off-flavors or grittiness are unacceptable. Isolates enable protein fortification up to 20 grams per serving without compromising mouthfeel, unlike concentrates, which require costly hydrocolloid systems. Textured pea protein, used in plant-based meat analogs, remains niche due to specialized processing and competition from soy-based alternatives.

Advancements in isolate production technology between 2024 and 2025, such as membrane-filtration systems, improved protein recovery by 8-12% and reduced water usage by 30-35%, per Cosucra's disclosures. These efficiencies are lowering isolate premiums over concentrates, driving adoption in mid-tier applications like nutrition bars and ready-to-drink shakes. Hydrolysed pea protein, a sub-segment of isolates, is gaining traction in clinical and infant nutrition for its reduced allergenicity and faster absorption. EFSA's 2024 approval of pea-protein isolate for infant formula, subject to purity and heavy-metal standards, further boosts demand in high-margin segments.

By Product Category: Conventional Dominates, Organic Accelerates

In 2025, conventional pea protein held 85.36% market share, reflecting the maturity of non-organic supply chains and price sensitivity across applications. Organic variants, growing at an 8.11% CAGR through 2031, benefit from premium positioning in retail and foodservice channels, where certification justifies 40-50% price premiums. Germany and Austria lead organic consumption, with organic food accounting for 12-14% of grocery spending, double the European average. However, limited certified acreage and 3-year crop rotations constrain organic supply, prompting investments in contract farming by Roquette and Emsland Group, securing 5,000-8,000 hectares in France, Germany, and Poland.

Organic certification imposes stricter processing standards, requiring dedicated production lines and non-GMO enzyme sources, increasing costs by 15-20% compared to conventional facilities. These costs are viable only at scale, concentrating organic pea protein production among 4-5 major European processors. Retail dynamics are shifting, with private-label organic meat alternatives gaining share as Lidl and Aldi expanded organic plant-based SKUs by 30-40% in 2025. This private-label growth pressures branded manufacturers to differentiate through functional claims like "high-protein" or "complete amino-acid profile" rather than relying solely on organic status.

By Application: Supplements Outpace Food and Beverages

In 2025, food and beverages accounted for 33.42% of Europe's pea protein applications, spanning bakery, meat extenders, supplements, beverages, snacks, confectionery, and infant nutrition. The supplements segment is growing at an 8.85% CAGR through 2031, driven by sports nutrition and meal replacements. Meat extenders and substitutes dominate, with pea protein used in 60% of plant-based burgers, sausages, and mince products launched in 2024-2025. Bakery applications grow slower due to pea protein's limited gluten-mimicking properties, which increase costs and development timelines.

Infant nutrition became a high-value niche after EFSA's 2024 approval of pea-protein isolate for formula use. Danone's Nutricia division launched a pea-based hypoallergenic formula in France and Germany in late 2025, targeting infants with cow's-milk protein allergy, affecting 2-3% of infants. Historically, this condition was managed with costly hydrolyzed dairy formulas. Animal feed applications are smaller but growing, as aquaculture and pet-food producers seek sustainable alternatives like pea protein, which reduces feed costs and maintains growth rates.

Geography Analysis

Germany captured 33.6% of market share in 2025 thanks to five large extraction plants, integrated rail logistics, and retail penetration of plant-based meats that hit 2.1 kg per-capita consumption—double the European mean. Mature adoption tempers growth to a 5.8% CAGR as core burger and sausage SKUs saturate shelves. Processors pivot to high-protein snacks and bakery to sustain momentum, while energy-price volatility motivates investment in on-site solar to protect margins.

France is the growth pacesetter with a forecast 9.02% CAGR through 2031. The Protéines France program poured EUR 100 million into local legume value chains, aligning farmer incentives with processor needs. Roquette’s Vic-sur-Aisne hub integrates 600 farms and slashes inbound transport costs 12-15%, positioning France as Europe’s isolated export base. Mandatory plant-protein options in public cafeterias from 2024 underpin volume, while urban millennials push retail penetration from 12% of households in 2023 to 18% in 2025.

The United Kingdom, Spain, the Netherlands, Belgium, Italy, and Poland collectively contribute to a significant market share. In the United Kingdom, retail volumes normalized post-pandemic, but Greggs, Pret, and Costa Coffee added pea-protein menu items, moving demand to foodservice. Spain and Italy see slower retail uptake yet rapid sports-nutrition expansion, aided by chain gyms and marathon culture. The Netherlands and Belgium benefit from port-centric logistics, with Avebe and Cosucra exporting isolates across the bloc. Poland’s low-cost sites lure capacity, though slower regulatory approvals and infrastructure gaps temper near-term growth.

Competitive Landscape

The European pea protein market is highly fragmented, with the top players, Roquette, Cosucra, Emsland Group, and Ingredion, collectively accounting for a significant market share. This leaves significant opportunities for smaller, niche players to establish themselves. Roquette relies on a network of 600 farms to ensure a consistent supply of traceable peas, reinforcing its commitment to quality and transparency. Emsland Group, on the other hand, focuses on securing organic farmland to maintain its position in the premium segment. Ingredion differentiates itself through enzymatic hydrolysis lines, which produce pre-digested peptides specifically designed for clinical nutrition applications. Meanwhile, Cosucra emphasizes water-efficient membrane processes, aligning with the preferences of environmentally-conscious and ESG-focused consumers.

Mid-tier processors are under increasing pressure as large food multinationals adopt backward integration strategies. For example, Kerry Group has expanded its operations by incorporating Dutch isolate production lines dedicated to its own meat-alternative brands. However, the company also markets its surplus capacity to third-party buyers, which has intensified price competition in the market. Similarly, Cargill has partnered with Puris to distribute U.S.-sourced isolates, leveraging its extensive distribution network to mitigate challenges posed by freight costs and logistics.

Start-ups are actively targeting untapped niche markets within the pea protein sector. Burcon NutraScience, for instance, has licensed its advanced 95%-purity extraction technology to Merit Functional Foods, although the production of commercial volumes remains limited at this stage. Patent filings in the sector have increased by 34% during 2024-2025, with innovations primarily focusing on energy-efficient filtration methods and flavor-masking enzymes. Regulatory expertise has emerged as a critical competitive advantage, as the cost of preparing EFSA dossiers can reach up to EUR 0.5 million. This financial barrier provides well-funded incumbents with a distinct edge, particularly in emerging segments such as infant formula.

Europe Pea Protein Industry Leaders

Ingredion Incorporated

Archer Daniels Midland Company

Roquette Frères S.A.

Cargill Inc.

Cosucra Groupe Warcoing SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Lasenor debuted VP-100, a texturizing pea protein developed with Meala FoodTech, to reduce egg use by 50-100% in bakery products like muffins and cakes. The ingredient enhanced aeration, produced softer crumbs, extended shelf life, and maintained volume and texture.

- June 2025: DSM-Firmenich partnered with Meala FoodTech to launch Vertis PB Pea, a clean-label texturizing pea protein for plant-based meat alternatives. This multifunctional ingredient replaces modified binders like hydrocolloids, enabling shorter ingredient lists while providing binding, gelation, emulsification, and protein enrichment.

- May 2024: In a strategic move to diversify its plant protein portfolio, Roquette launched NUTRALYS Fava S900M, a sustainable and high-quality bean protein isolate that complements its pea protein offerings. This product was asserted to be designed to provide balanced amino acid profiles and functional attributes suitable for clean-label nutritional supplements, beverages, and meat alternative products. The addition of this innovative ingredient highlights the company's commitment to expanding sustainable protein options for the growing European market.

- February 2024: Roquette introduced four innovative pea protein ingredients under its NUTRALYS brand that offer enhanced functionality and nutritional benefits. These new pea protein isolates and concentrates are engineered to improve texture, solubility, and emulsification properties, making them ideal for a wide range of plant-based food applications. The products target formulations in high-protein nutritional bars, beverage mixes, and dairy alternatives, enabling manufacturers to meet growing consumer demand for clean-label and plant-based protein options.

Europe Pea Protein Market Report Scope

Pea protein is a food product and protein supplement derived and extracted from yellow and green split peas, Pisum sativum.

The European pea protein market is segmented by form, application, and geography. Based on form, the market is segmented into protein isolate, protein concentrate, and textured protein. Based on application, the market is segmented into bakery, meat extender and substitute, nutritional supplement, beverage, snacks, and other applications. By geography, the market is segmented into Spain, the United Kingdom, France, Germany, Italy, Russia, and the Rest of Europe.

The market sizing has been done in value terms in USD and volume terms in tons for all the abovementioned segments.

By Form

| Protein Isolate |

| Protein Concentrate |

| Textured/Hydrolysed |

By Product Category

| Conventional Pea Protein |

| Organic Pea Protein |

By Application

| Food and Beverages | Bakery |

| Meat Extenders and Substitutes | |

| Nutritional Supplements | |

| Beverages | |

| Snacks | |

| Confectionery | |

| Infant Nutrition | |

| Animal Feed | |

| Supplements | |

| Other Applications |

By Geography

| Europe |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Russia |

| Sweden |

| Belgium |

| Poland |

| Netherlands |

| Rest of Europe |

| By Form | Protein Isolate | |

| Protein Concentrate | ||

| Textured/Hydrolysed | ||

| By Product Category | Conventional Pea Protein | |

| Organic Pea Protein | ||

| By Application | Food and Beverages | Bakery |

| Meat Extenders and Substitutes | ||

| Nutritional Supplements | ||

| Beverages | ||

| Snacks | ||

| Confectionery | ||

| Infant Nutrition | ||

| Animal Feed | ||

| Supplements | ||

| Other Applications | ||

| By Geography | Europe | |

| United Kingdom | ||

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the projected value of the Europe pea protein market in 2031?

The Europe pea protein market is expected to reach USD 710.95 million by 2031.

Which form leads regional demand?

Protein isolates dominate, holding 66.12% share in 2025 and expanding at a 7.72% CAGR to 2031.

Why is France the fastest-growing geography?

Government funding, new processing capacity, and mandatory plant-protein options in public catering drive a forecast 9.02% CAGR.

Which application segment is growing quickest?

Supplements, especially sports-nutrition powders and ready-to-drink shakes, are rising at an 8.85% CAGR through 2031.

Page last updated on: