Textured Pea Protein Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.62 Billion |

| Market Size (2031) | USD 0.87 Billion |

| Growth Rate (2026 - 2031) | 7.76% CAGR |

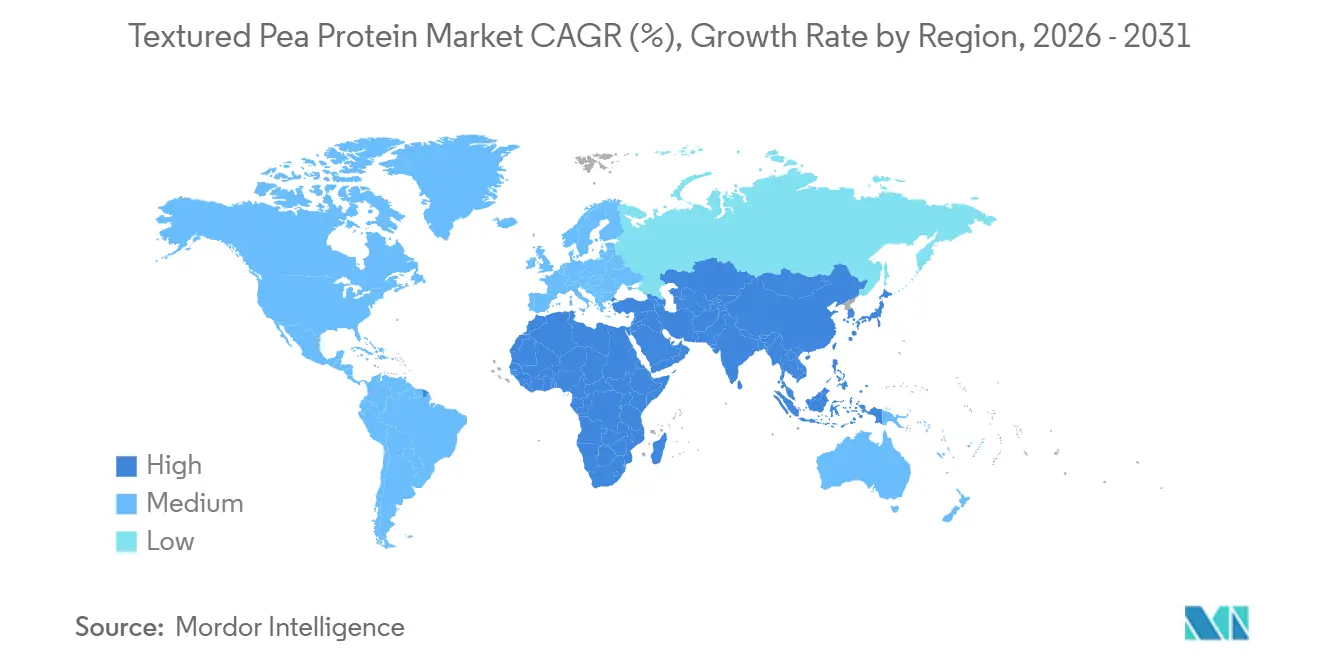

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Textured Pea Protein Market Analysis by Mordor Intelligence

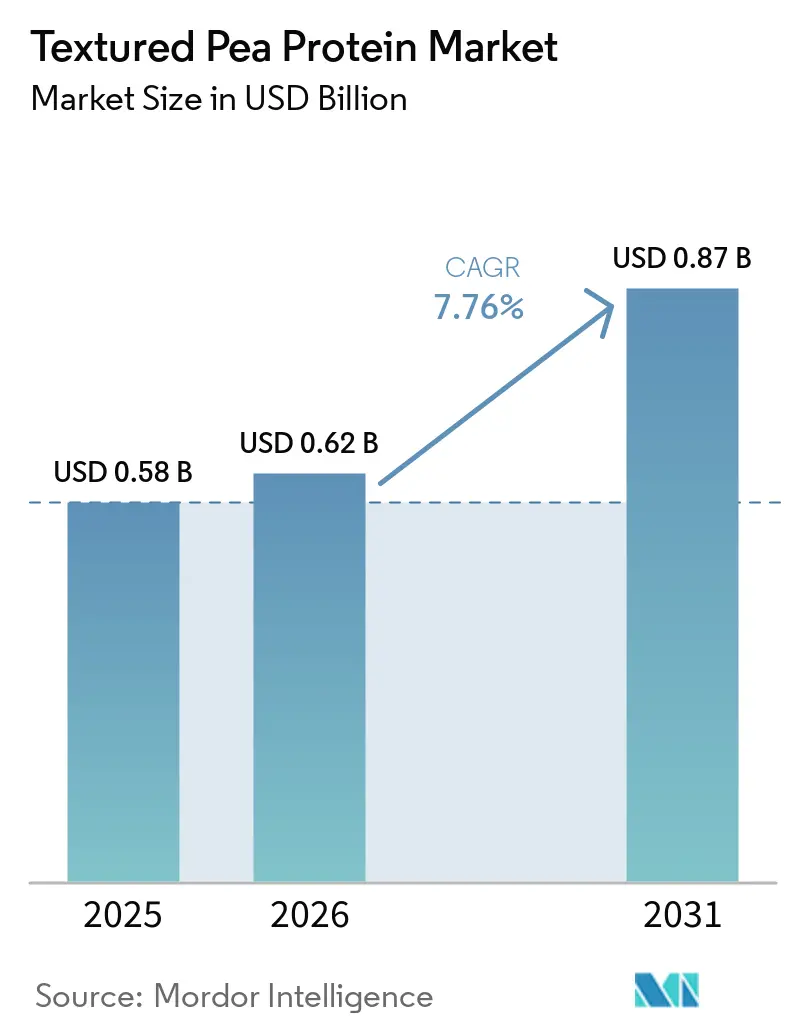

The textured pea protein market size was valued at USD 0.58 billion in 2025 and is estimated to grow from USD 0.62 billion in 2026 to reach USD 0.87 billion by 2031, at a CAGR of 7.76% during the forecast period (2026-2031). Continuing decarbonization pledges from multinational food groups, widening trade barriers that favor North-American and European processors, and rapid scale-up of high-moisture extrusion lines are combining to push the textured pea protein market toward sustained mid-single-digit growth. Yellow peas retained cost leadership through 2025, while green-pea variants are gaining a premium foothold in organic channels because of their milder flavor. Format preferences are bifurcating: powders still dominate bulk food manufacturing, yet chunks and minces are securing incremental demand from quick-service chains that want ready-to-use meat analogues. Regionally, North America benefits from domestic anti-dumping duties on Chinese imports, and the Asia-Pacific is accelerating capacity investment to localize value addition. Competitive intensity is moderate; the top five suppliers can lock in multi-year raw-material contracts but remain vulnerable to weather-induced price swings and new entrants commercializing faba-bean isolates.

Key Report Takeaways

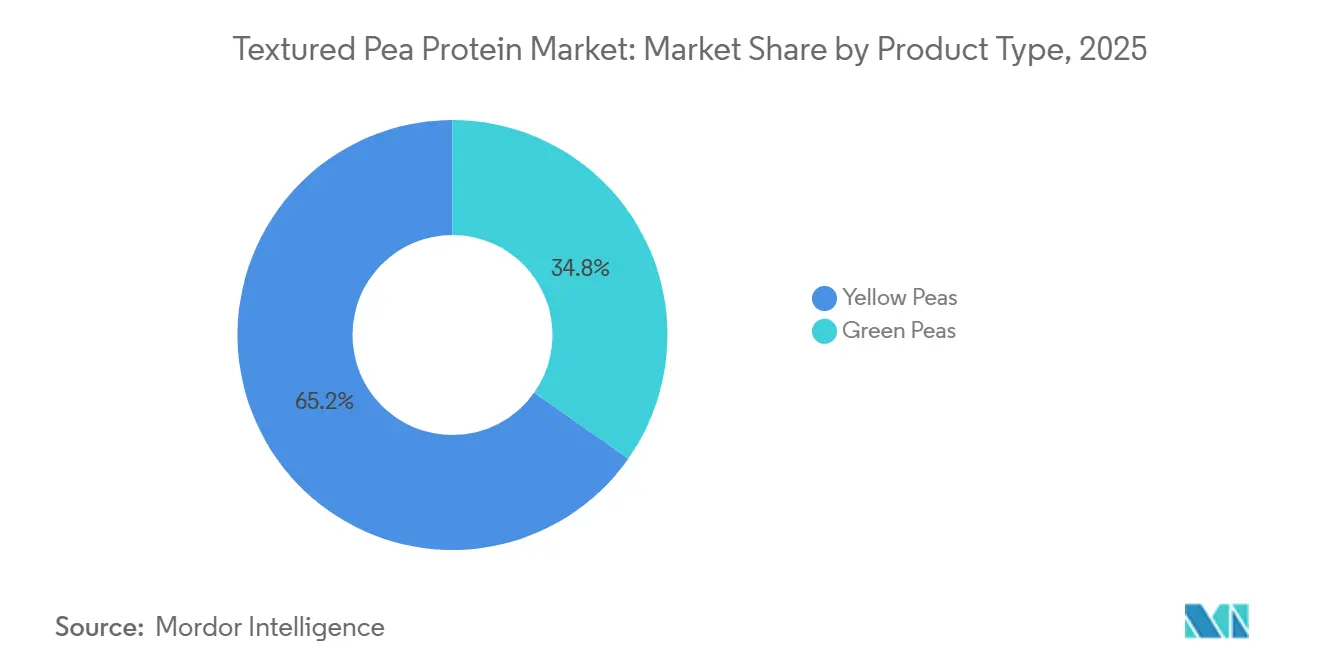

- By product type, yellow peas delivered 65.23% of 2025 revenue, while green peas are projected to expand at an 8.23% CAGR through 2031, the fastest rate in the category.

- By form, powders commanded 60.21% share in 2025, and chunks and minces led growth at a 9.02% CAGR for 2026-2031.

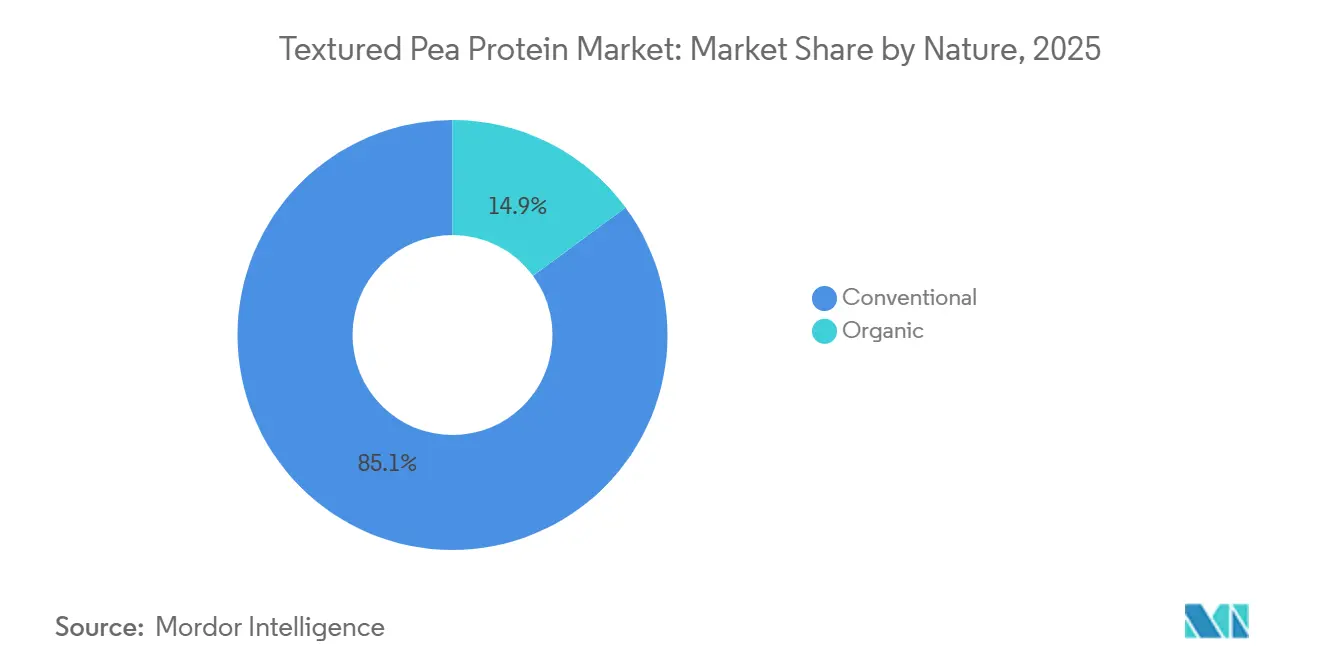

- By nature, conventional variants supplied 85.11% of the 2025 volume; organic products will rise at an 8.13% CAGR.

- By application, food and beverages accounted for 57.43% revenue in 2025, whereas animal food is forecast to advance at 7.65% CAGR.

- By geography, North America held 38.67% of global sales in 2025, yet Asia-Pacific is set to record the strongest regional CAGR at 8.21% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Textured Pea Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for plant-based meat alternatives | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Rising preference for clean-label and allergen-free products | +1.2% | North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Expansion of extrusion production capacity by leading manufacturers | +1.5% | North America, Europe, and China | Short term (≤ 2 years) |

| Growing adoption of private-label products across North America and Europe | +0.9% | North America and Western Europe | Medium term (2-4 years) |

| Increasing use of high-moisture extrusion technology in Asia | +1.0% | China, India, Japan, with spillover to Southeast Asia | Medium term (2-4 years) |

| Corporate Scope-3 emission reduction targets supporting pea-based formulations | +0.8% | Global, led by multinational food corporations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Plant-Based Meat Alternatives

Quick-service chains and retail grocers are consolidating around pea protein because it delivers the functional trifecta of binding, water retention, and thermal stability without triggering the top-8 allergen disclosures required for soy or wheat gluten. Meat-analogue formulations now routinely blend 15% to 25% textured pea protein with methylcellulose or konjac to achieve pull-apart fibers that mimic whole-muscle chicken or beef, a technical threshold that eluded first-generation veggie burgers. The shift is quantifiable: PURIS commercialized its Organic Pea Protein 2.0 in late 2025, targeting brands that require both USDA Organic and high-gel-strength specs for plant-based sausage casings. Regulatory tailwinds reinforce adoption; the European Food Safety Authority maintains pea protein on its positive list for novel foods, exempting it from the pre-market authorization burden that delays faba-bean and lupin isolates from EFSA. This regulatory clarity is steering R&D budgets toward pea-centric platforms, even as sensory gaps persist.

Rising Preference for Clean-Label and Allergen-Free Products

Institutional buyers, schools, hospitals, and corporate cafeterias are rewriting procurement specs to exclude the 14 EU-recognized allergens, a mandate that disqualifies soy protein isolate in roughly 30% of tenders and elevates pea protein to default status. Ingredion's October 2024 launch of VITESSENCE Pea 200 D, engineered for rapid dispersion in ready-to-mix beverages, exemplifies the pivot toward minimally processed formats that carry no E-number additives. The clean-label imperative extends to extraction: organic-certified processors such as NOW Sports employ cold aqueous extraction at 30°C to 45°C, preserving native protein structure and avoiding hexane residues that trigger non-GMO decertification. Compliance frameworks such as ISO 22000 and Global Food Safety Initiative benchmarks are becoming table stakes, particularly for European private-label contracts where retailers audit upstream to the farm gate. This dynamic favors vertically integrated suppliers capable of tracing yellow-pea lots to individual fields, a capability that mid-tier toll manufacturers lack.

Expansion of Extrusion Production Capacity by Leading Manufacturers

Capital deployment into twin-screw extrusion lines accelerated in 2025, with cumulative announced investments exceeding USD 300 million across North America and Europe. Ingredion's November 2024 partnership with Lantmännen commits EUR 100 million (approximately USD 108 million) to a Swedish facility designed to process 50,000 metric tons of locally sourced yellow peas annually by 2027, insulating the supply chain from transatlantic freight volatility. Axiom Foods expanded its North American production beyond 2,000 metric tons in January 2025 and announced plans to double capacity within 12 months, a direct response to the February 2026 U.S. anti-dumping duties that rendered Chinese imports uneconomical. High-moisture extrusion, operating at 50% to 70% moisture and 110°C to 180°C barrel temperatures, is the technical differentiator, yielding anisotropic fiber structures that replicate the shear resistance of animal muscle. Burcon NutraScience's June 2025 commissioning of its Galesburg, Illinois, facility added another 20,000 metric tons of annual pea-protein capacity, targeting co-manufacturing agreements with branded meat-alternative startups.

Growing Adoption of Private-Label Products Across North America and Europe

Retail private-label penetration in plant-based proteins reached 42% in Western Europe and 38% in North America by the end of 2025, as grocers such as Tesco, Carrefour, and Kroger launched house-brand meat analogues priced 20% to 30% below national brands. These programs prioritize cost-effective powder formats over premium chunks, a procurement pattern that sustained the 60.21% powder share in 2025 despite faster growth in extruded forms. OPW Ingredients, a European toll manufacturer, reported minimum order quantities of 500 kilograms for private-label pea-protein blends in 2025, with lead times compressed to 4 weeks, half the duration required for custom soy-protein formulations. The shift is margin-accretive for retailers, which capture 35% to 40% gross margins on private-label plant proteins versus 18% to 22% on branded equivalents, creating a structural tailwind for textured pea protein as the lowest-cost allergen-free base. Certification requirements remain stringent; Tesco mandates British Retail Consortium Global Standard audits for all pea-protein suppliers, a compliance threshold that excludes smaller Asian exporters lacking third-party accreditation.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility in yellow pea supply chains | -1.3% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Flavor and sensory challenges associated with beany taste profiles | -1.1% | Global, most pronounced in Western markets | Medium term (2-4 years) |

| Limited texturizing expertise among mid-sized OEM manufacturers | -0.7% | Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Intensifying competition from emerging faba bean-based TVP products | -0.6% | Europe, with early adoption in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Volatility in Yellow Pea Supply Chains

Canadian yellow-pea spot prices spiked 40% between January and March 2025 after China imposed a 100% retaliatory tariff on Canadian pulse imports, a trade action that removed 1.2 million metric tons of annual demand and forced growers to redirect volumes into already-saturated North American and European markets, according to Statistics Canada[1]Source: Statistics Canada, “Production of Principal Field Crops 2025,” statcan.gc.ca. The whipsaw continued: by June 2025, prices had collapsed 25% below the prior-year average as excess inventory flooded processing channels, eroding margins for vertically integrated players such as AGT Food and Ingredients that had locked in forward contracts at peak levels. Weather volatility compounds the risk; Saskatchewan's 2024 growing season saw spring frosts reduce yields by 18%, tightening supplies precisely when U.S. anti-dumping duties, ranging from 127% to 286%, curtailed Chinese imports in February 2026. Processors lacking multi-origin sourcing strategies face acute exposure; a single-origin reliance on North American peas subjects formulators to basis-risk swings of 30% to 50% within a crop year, a volatility band that private-label retailers refuse to absorb through price adjustments.

Flavor and Sensory Challenges Associated with Beany Taste Profiles

Off-flavor compounds, primarily hexanal, heptanal, and lipoxygenase-derived aldehydes, remain the principal barrier to mainstream consumer acceptance, despite enzymatic and thermal mitigation techniques. Roquette's February 2026 launch of NUTRALYS Pea 850F incorporates a proprietary debittering step that reduces hexanal concentrations by 60%, yet blind taste panels still rank pea-based burger patties below mycoprotein and soy analogs in overall liking scores. The sensory gap is most pronounced in minimally seasoned applications, plain protein shakes, and unflavored chunks, where beany notes cannot be masked by spices or umami enhancers. Kerry Group's 2024 patent filing (WO2024018028A1) for a pea-protein fat-replacement emulsion acknowledges the challenge, specifying 7% to 22% protein loads to balance mouthfeel against off-flavor perception.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Green Peas Gain Premium Traction

Green peas are projected to expand at 8.23% CAGR during 2026-2031, outpacing yellow peas despite the latter's 65.23% revenue dominance in 2025. The growth differential stems from green peas' milder flavor profile and higher chlorophyll content, attributes that command 15% to 20% price premiums in organic and Non-GMO Project Verified channels. Axiom Foods' March 2026 launch of Vegotein N Neutral, an 80% protein isolate derived from green peas, targets beverage formulators seeking neutral-tasting bases for ready-to-drink shakes, a segment where yellow-pea isolates struggle due to residual earthiness. Yellow peas retain structural advantages in cost-sensitive applications; their higher starch content (45% to 50% versus 40% to 43% in green varieties) yields better binding in extruded chunks, making them the default choice for private-label meat analogues where price points must undercut animal protein by at least 20%. Regulatory compliance remains uniform; both variants meet FDA Generally Recognized as Safe status and EU Novel Food exemptions, eliminating approval delays that hinder alternative pulses such as lentils or chickpeas.

Organic certification is reshaping product-type dynamics. Green peas accounted for 62% of USDA Organic-certified pea-protein volume in 2025, driven by their association with premium positioning and consumer perception of "cleaner" processing, according to the USDA National Organic Program[2]Source: USDA Agricultural Marketing Service, "National Organic Program", ams.usda.gov. The product-type split is also geographic; North American processors favor yellow peas due to established Saskatchewan and Montana acreage, while European players are diversifying into green peas sourced from France and Poland to satisfy local-origin preferences. Breeding advances may narrow the gap; Equinom's ultra-high-protein yellow-pea varieties, under development since 2022, aim to deliver 28% to 30% protein content versus the current 23% to 25%, potentially offsetting green peas' sensory edge through improved functionality

By Form: Chunks and Minces Capture Foodservice Demand

Chunks and minces are forecast to grow at 9.02% CAGR during 2026-2031, the fastest rate among form-based segments, as quick-service restaurants and meal-kit providers prioritize plug-and-play formats that require no additional texturization. Powders held 60.21% of form-based revenue in 2025, anchored by their versatility in bakery, beverage, and private-label applications, where cost per functional unit remains the decisive procurement criterion. The chunks-and-minces surge reflects the technical maturation of high-moisture extrusion; processors can now achieve anisotropic fiber alignment and 40% to 50% shear strength, metrics that replicate pulled pork or shredded chicken, by tuning barrel temperature, screw speed, and die geometry. MGP Ingredients commercialized its ProTerra textured pea protein in Q4 2025, securing a multi-year contract with a large multinational customer for use in frozen entrées, a validation that extruded chunks can meet industrial-scale consistency requirements.

Flakes occupy a niche position, favored in breakfast cereals and granola bars for their visual appeal and crunch retention, yet they represented less than 10% of form-based volume in 2025 due to higher processing costs and limited functional advantages over powders in most applications. Roquette's June 2025 introduction of NUTRALYS T PEA 700XC, a flake optimized for cold extrusion into protein bars, illustrates targeted innovation, but adoption remains confined to premium snack brands willing to absorb the 12% to 15% cost premium over commodity powders. Regulatory considerations are minimal across forms; all three formats share identical GRAS and Novel Food clearances, shifting competitive dynamics entirely to functionality and price. The chunks-and-minces trajectory suggests a bifurcation: powders will continue to dominate cost-driven bulk applications, while extruded forms capture margin-rich foodservice and branded-product segments where texture authenticity justifies higher ingredient costs.

By Nature: Organic Certification Drives Fastest Growth

Organic textured pea protein is expanding at 8.13% CAGR during 2026-2031, nearly double the 4.5% growth rate of conventional variants, propelled by institutional procurement mandates and consumer willingness to pay 25% to 35% premiums for USDA Organic and EU Organic certifications. Conventional products commanded 85.11% of nature-based volume in 2025, reflecting their cost advantage and sufficient functionality for mainstream meat-analogue applications where certification adds no performance benefit. The organic premium is justified by traceability requirements; certified processors must document non-GMO seed sourcing, pesticide-free cultivation, and segregated handling from farm to finished ingredient, a compliance burden that excludes most mid-tier toll manufacturers. NOW Sports and Nutra Food Ingredients exemplify the organic positioning, offering 80% to 85% protein isolates with ISO 22000 and HACCP certifications that satisfy European retail audits.

The organic growth trajectory is geographically skewed; North America and Western Europe accounted for 78% of certified organic pea-protein consumption in 2025, while Asia-Pacific remains dominated by conventional products due to lower consumer awareness and fragmented certification infrastructure. Cold aqueous extraction, operating at 30°C to 45°C to preserve native protein structure, is the preferred processing route for organic variants, avoiding hexane residues that trigger decertification and aligning with clean-label positioning Journal of Food Engineering. Conventional processors retain scale advantages; Ingredion's VITESSENCE Pea 100 HD, launched in July 2024, uses alkaline extraction to achieve 85% protein purity at 20% lower cost than organic equivalents, a trade-off that private-label retailers accept when certification is not contractually mandated Ingredion Incorporated. The nature-based split will likely persist, with organic capturing premium channels and conventional dominating volume-driven segments, unless regulatory shifts, such as EU Farm to Fork sustainability labeling—impose de facto organic requirements on mainstream products.

By Application: Animal Food Emerges as Growth Frontier

Animal food applications are forecast to grow at 7.65% CAGR during 2026-2031, the fastest rate among end-use segments, as aquaculture producers and premium pet-food brands substitute pea protein for fishmeal and poultry by-products to address cost volatility and sustainability pressures. Food and beverages held 57.43% of application revenue in 2025, anchored by meat alternatives, bakery fortification, and dairy-analog beverages, yet the segment's maturity and intense price competition are compressing margins. Within animal food, aquafeed represents the highest-growth subsegment; pea-protein concentrate delivers 65% to 70% crude protein with balanced amino-acid profiles for tilapia and salmon, achieving feed-conversion ratios within 5% of fishmeal at 30% to 40% lower cost. European aquaculture operations are leading adoption, driven by EU regulations that cap fishmeal inclusion to promote marine-stock sustainability.

Pet food is the second pillar of animal-food growth, with premium brands such as those supplied by Lam Tak Industrial incorporating 8% to 12% pea protein in grain-free dog kibble to meet Association of American Feed Control Officials protein minimums without triggering grain sensitivities. The application shift is margin-accretive; animal-food customers accept 10% to 15% lower protein purity (60% to 70% versus 80% to 85% for human food) and less stringent organoleptic specs, reducing processing costs and expanding addressable markets for lower-grade pea fractions. Meat alternatives and analogues, the largest food-and-beverage subsegment, continue to drive absolute volume, yet their 6.5% CAGR lags the overall market due to consumer fatigue with first-generation products and retailer SKU rationalization that eliminated underperforming plant-based brands in 2025. Breakfast cereals, snacks, and dairy alternatives collectively represent 20% to 25% of food-and-beverage volume, offering stable but low-growth outlets for textured pea protein in fortification roles.

Geography Analysis

In 2025, North America contributed 38.67% to global sales. The imposition of U.S. anti-dumping duties, which will reach up to 286% on Chinese imports starting February 2026, has redirected demand toward domestic suppliers such as PURIS and Axiom. Canadian growers, who were displaced from Chinese markets due to a 100% tariff introduced in March 2025, shifted 40% of their export volume to Europe by the fourth quarter of 2025. Private-label products achieved a penetration rate of 38%, reinforcing the role of powders in large-batch processing applications.

Regulations promoting clean-label products, which discourage the use of soy and require clear allergen labeling, are driving the increased adoption of pea protein. Additionally, the EU's Corporate Sustainability Reporting Directive, which mandates Scope-3 emissions disclosures, is favoring low-carbon pea-based ingredients. While BENEO's EUR 50 million investment in faba isolates could challenge pea protein's market position, Ingredion's Swedish extrusion facility, scheduled to become operational in 2027, will process 50,000 tons of locally sourced yellow peas. This initiative not only meets the demand for origin-labeled products but also capitalizes on price premiums of up to 8% associated with such labeling.

The Asia-Pacific region is positioned as the fastest-growing market, with a robust CAGR of 8.21% projected for the 2026-2031 period. China's retaliatory tariff on Canadian peas has accelerated investments in domestic crushing facilities, with BIOWAY leveraging low-cost extruders to enable rapid capacity expansion. In India, the introduction of a 30% tariff on imported concentrates has spurred the development of at least three extrusion projects, all of which are expected to commence operations by 2027. According to the Government of India Ministry of Commerce, greenfield projects in Gujarat and Punjab are also underway, with three facilities targeting a 2027 launch[3]Source: Government of India, Ministry of Commerce and Industry, "Annual Report", commerce.gov.in/. These facilities aim to support the growing domestic meat-analogue industry while also catering to export markets in Southeast Asia. Although high humidity levels in the region increase packaging costs by approximately 10%, the expanding urban population and the growth of foodservice channels continue to drive market expansion. While South America and the Middle East & Africa currently account for smaller shares of the market, these regions are expected to benefit from Brazil's expanding meat-analogue sector and the UAE's strategic food-security initiatives by 2031.

Competitive Landscape

The textured pea protein market demonstrates a moderate concentration level. Roquette, Puris, Ingredion Incorporated, Axiom Foods, and GEMEF Industries dominate the top tier. Roquette’s integrated operations, spanning pea farming, fractionation, and application labs, provide cost efficiencies and pre-flavored ingredient systems that accelerate customer development timelines. In Europe, Cosucra utilizes proprietary wet fractionation and continuous texturization to serve private-label clients. Axiom Foods focuses on allergen-free certifications to establish a foothold in medical-nutrition channels, while Burcon employs patented extraction methods to improve solubility. MycoTechnology works with contract extruders to bring fermented variants to market, addressing off-notes effectively.

Strategic initiatives emphasize capacity expansion, patent filings for extrusion configurations, and joint development agreements with major consumer packaged goods (CPG) companies. For example, Roquette’s Manitoba facility includes customer-innovation suites that enable rapid prototyping of meat-analogue concepts. Meanwhile, pet-food opportunities attract new entrants developing specialized nutrient blends. Faba-bean players, leveraging EU grants, are piloting hybrid meat analogues, intensifying competition while fostering cross-licensing discussions for complementary proteins.

Smaller OEM processors encounter challenges related to knowledge and certification. Retailers demand compliance with standards such as BRCGS, ISO 22000, and HACCP, creating barriers that many plants in Asia and Latin America are not yet equipped to overcome. As policy changes, such as tariffs and sustainability mandates, become more frequent, scale and geographic flexibility are expected to drive further consolidation, positioning mid-sized toll manufacturers as acquisition targets for larger ingredient companies.

Textured Pea Protein Industry Leaders

-

Roquette Frères

-

PURIS

-

Ingredion Incorporated

-

Axiom Foods, Inc.

-

GEMEF Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Food tech startup Prot introduced Prot Block, a pea protein-based ingredient block designed as a versatile "middle-ground" solution between highly processed meat analogs and conventional plant proteins like texturized soy. Prot Block delivers 15g protein and 10g fiber per 100g, making it ideal for everyday Indian, Asian, and global dishes such as stir-fries, curries, sandwiches, salads, and snacks.

- June 2025: Roquette has unveiled NUTRALYS® T PEA 700XC, a textured pea protein crafted for robust dishes. This pea protein, ideal for plant-based ready meals and classic dishes like goulash and bourguignon, reportedly maintains its bite, juiciness, and visual appeal post-cooking or reheating.

- November 2024: According to a provincial media release, Roquette's pea processing plant in Manitoba is set to double its current production capacity. Both the Manitoba and federal governments unveiled their joint funding for the expansion, among other significant capital infrastructure and investment projects. This funding comes through the Sustainable Canadian Agriculture Partnership (Sustainable CAP).

Global Textured Pea Protein Market Report Scope

| Yellow Peas |

| Green Peas |

| Flakes |

| Powders |

| Chunks and Minces |

| Conventional |

| Organic |

| Food and Beverages | Meat Alternatives and Analogues |

| Bakery and Confectionery | |

| Breakfast Cereals | |

| Snacks | |

| Dairy Alternatives | |

| Other Food and Beverages | |

| Animal Food | |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| Product Type | Yellow Peas | |

| Green Peas | ||

| Form | Flakes | |

| Powders | ||

| Chunks and Minces | ||

| Nature | Conventional | |

| Organic | ||

| Applications | Food and Beverages | Meat Alternatives and Analogues |

| Bakery and Confectionery | ||

| Breakfast Cereals | ||

| Snacks | ||

| Dairy Alternatives | ||

| Other Food and Beverages | ||

| Animal Food | ||

| Other Applications | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Ow large will the textured pea protein market be by 2031?

The textured pea protein market size is projected to reach USD 0.87 billion by 2031 at a 7.76% CAGR.

Which segment grows fastest in textured pea protein applications?

Animal food, led by aquafeed and premium pet nutrition, is forecast to grow 7.65% per year through 2031.

What drives Asia-Pacific demand for textured pea protein?

New high-moisture extrusion projects in China and India, combined with tariffs that encourage local processing, fuel an 8.21% regional CAGR.

Why are green-pea proteins gaining share?

Green peas offer a milder taste and align with organic, clean-label positioning, supporting an 8.23% CAGR that outpaces yellow-pea growth.

Page last updated on: