Fava Bean Protein Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 310.22 Million |

| Market Size (2030) | USD 481.70 Million |

| Growth Rate (2025 - 2030) | 9.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fava Bean Protein Market Analysis by Mordor Intelligence

The fava bean protein market size stands at USD 310.22 million in 2025 and is projected to reach USD 481.7 million by 2030, reflecting a 9.2% CAGR and underscoring an accelerating global pivot toward sustainable, allergen-friendly plant proteins that can complement or replace soy and pea. Rising demand for clean-label formulations, a widening roster of sports-nutrition applications, and decisive regulatory clarity in both the United States and the European Union collectively fuel this expansion. Manufacturers are prioritizing dry-fractionation and hybrid extraction technologies that lower water and energy requirements, align with corporate net-zero targets, and improve cost structures[1]Center for Food Safety and Applied Nutrition, “Recently Published GRAS Notices and FDA Letters,” fda.gov. Europe benefits from the deepest installed processing base and favorable agri-policy support, yet Asia-Pacific delivers the highest incremental volume growth as Chinese pulse programs scale. North American players leverage a series of FDA GRAS notices to fast-track novel SKUs, while new capital projects in Germany and Canada provide proof points for scalable, zero-waste production.

Key Report Takeaways

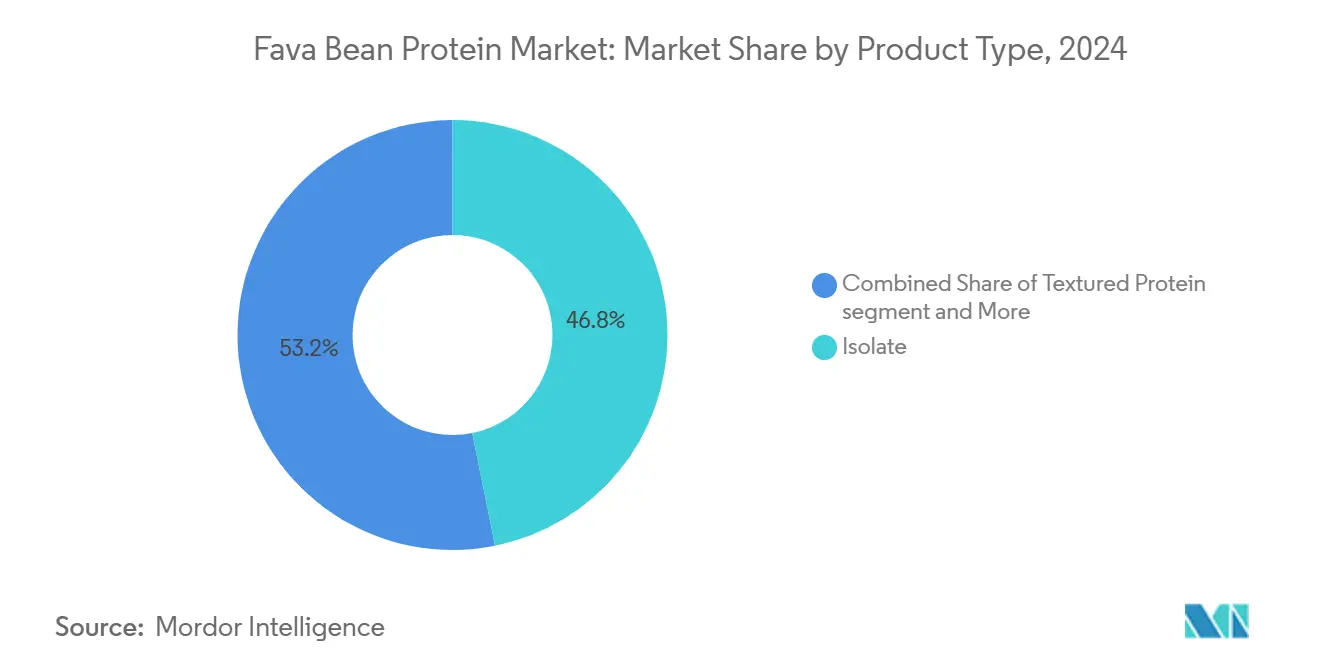

- By product type, isolates captured 46.84% of the fava bean protein market share in 2024, while textured protein is forecast to expand at a 9.27% CAGR through 2030.

- By nature, conventional grades held 81.62% share of the fava bean protein market size in 2024; organic grades are projected to grow at a 10.11% CAGR to 2030.

- By application, food and beverage manufacturers accounted for 57.83% of the fava bean protein market size in 2024, whereas animal nutrition is advancing at an 8.22% CAGR through 2030.

- By geography, Europe led with a 32.59% fava bean protein market share in 2024; Asia-Pacific posts the fastest regional growth at 9.04% CAGR to 2030.

Global Fava Bean Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plant-based diet mainstreaming in US and EU retail channels | +1.8% | North America & EU | Medium term (2-4 years) |

| Demand for allergen-friendly protein in sports-nutrition RTD beverages | +1.2% | Global | Short term (≤ 2 years) |

| Regulatory tailwinds: GRAS clearance and EU novel-food self-determinations | +2.1% | North America & EU | Short term (≤ 2 years) |

| Food-industry pivot to dry-fractionated proteins to cut water/energy use | +1.5% | Global | Medium term (2-4 years) |

| Corporate net-zero targets driving pulse-based ingredient sourcing | +1.3% | Global | Long term (≥ 4 years) |

| Rapid adoption of textured fava protein by global meat-analog manufacturers | +1.1% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Plant-based Diet Mainstreaming in US and EU Retail Channels

The institutionalization of plant-based diets across mainstream US and European retail channels creates unprecedented demand velocity for fava bean protein ingredients. Major food manufacturers are pivoting from niche health food positioning toward mass-market protein fortification, with fava bean protein emerging as a strategic alternative to saturated pea and soy protein markets. This shift is exemplified by HappyVore's plant-based ham alternative launch in March 2025, which achieved France's Saveur de l'Année award while incorporating bean protein concentrate as a core functional ingredient. The mainstream adoption accelerates as retailers demand diversified plant protein portfolios to reduce supply chain concentration risks, positioning fava bean protein as a critical portfolio component[2]Bev Betkowski, “Research Is Making Faba Beans a Better Source of Protein,” University of Alberta Folio, ualberta.ca for food manufacturers seeking competitive differentiation in the expanding flexitarian market segment.

Demand for Allergen-Friendly Protein in Sports-Nutrition RTD Beverages

Sports nutrition manufacturers increasingly prioritize allergen-friendly protein sources to capture the growing population of athletes with dietary restrictions, creating substantial market pull for fava bean protein ingredients. Clinical validation of PeptiStrong, a fava bean protein hydrolysate, demonstrated significant improvements in muscle strength recovery and bone mineral content in healthy adults, providing scientific substantiation for premium sports nutrition positioning. This clinical evidence enables sports nutrition brands to command premium pricing while avoiding common allergens associated with dairy and soy proteins. The trend accelerates as regulatory bodies increasingly scrutinize allergen labeling requirements, making fava bean protein's hypoallergenic profile a strategic competitive advantage in ready-to-drink beverage formulations.

Regulatory Tailwinds: GRAS Clearance and EU Novel-Food Self-Determinations

Regulatory momentum reached a critical inflection point with multiple FDA GRAS determinations for fava bean protein and protein hydrolysates (GRN 1151, 1166, 879), eliminating the primary commercialization barrier that historically constrained market entry. The regulatory clarity enables food manufacturers to incorporate fava bean protein ingredients without lengthy approval processes, accelerating product development timelines and reducing regulatory compliance costs. European markets benefit from established legume protein precedents under Novel Food Regulation (EU) 2015/2283, though manufacturers must navigate evolving allergenicity assessment requirements that emphasize proteomics-based allergen screening. This regulatory foundation creates competitive moats for early market entrants while establishing clear pathways for scaling commercial production.

Food-Industry Pivot to Dry-Fractionated Proteins to Cut Water/Energy Use

Sustainability mandates are driving food manufacturers toward dry-fractionation processing technologies that eliminate water-intensive alkaline extraction methods, creating structural demand advantages for fava bean protein suppliers who utilize air classification and electrostatic separation. University of Alberta research has demonstrated that hybrid dry-wet fractionation processes can achieve protein concentrates with up to 94% purity while reducing water consumption by 90% compared to conventional, chemical-intensive methods. BENEO's USD 65 million German processing facility exemplifies this technological shift, employing zero-waste dry fractionation to produce faba bean protein concentrate while generating valuable co-products, including starch-rich flour and fiber-rich hulls[3]Ophélie Gautheron et al., “Exploring the Impact of Solid-State Fermentation on Fava Bean Flour,” MDPI, mdpi.com. This processing evolution enables manufacturers to achieve sustainability targets while maintaining competitive cost structures, positioning dry-fractionated fava bean proteins as preferred ingredients for environmentally conscious brands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price premium vs. soy and pea proteins | -2.3% | Global | Short term (≤ 2 years) |

| Limited large-scale fractionation capacity outside Europe and Canada | -1.8% | Asia-Pacific & MEA | Medium term (2-4 years) |

| Vicine/convicine liability in G6PD-deficient populations | -1.4% | Mediterranean, Sub-Saharan Africa, SE Asia | Long term (≥ 4 years) |

| Low DIAAS score without complementary amino-acid blending | -1.1% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Premium vs. Soy and Pea Proteins

Fava bean protein ingredients command significant price premiums compared to established soy and pea protein alternatives, creating adoption barriers for cost-sensitive food manufacturers and limiting market penetration in price-competitive segments. Mid-2024 commodity data from Milan and Bologna exchanges indicated domestic fava beans traded at EUR 340-350 per ton compared to soybeans at EUR 440-450 per ton, yet processed fava bean protein isolates require substantially higher processing costs due to limited economies of scale. The pricing disadvantage intensifies for high-purity isolates exceeding 90% protein content, where specialized extraction processes and lower production volumes create cost structures that can exceed pea protein isolates by 30-50%. This premium pricing constrains adoption in mass-market applications while limiting fava bean protein to premium and specialized food segments where functional benefits justify higher ingredient costs.

Limited Large-Scale Fractionation Capacity Outside Europe and Canada

Processing infrastructure constraints create significant supply bottlenecks for fava bean protein ingredients, particularly in high-growth Asia-Pacific markets where demand increasingly outpaces regional production capacity. Current large-scale fractionation facilities concentrate primarily in Europe (BENEO Germany, Cosun Netherlands) and Canada (Roquette Manitoba), creating supply chain vulnerabilities and elevated logistics costs for manufacturers in emerging markets. The capacity constraints intensify as European facilities prioritize domestic and North American markets, leaving Asia-Pacific manufacturers dependent on costly imports that erode competitive positioning against locally produced soy and pea proteins. Infrastructure development requires substantial capital investments exceeding USD 50 million per facility, creating entry barriers that perpetuate regional supply imbalances and constrain global market expansion potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Isolates Lead While Textured Proteins Accelerate

The isolates' slice of the fava bean protein market size reached 46.84% in 2024, affirming manufacturers’ quest for ≥90% protein purity and a near-white organoleptic profile. Wet-fractionation assets built for pea can sometimes be retrofitted for fava beans, easing scale-up when functionally equivalent. Bakery, beverage, and infant-nutrition formulators cite high solubility and low polyphenol content as a rationale for selecting isolates. Roquette’s NUTRALYS Fava S900M consistently meets 90% protein and sub-1.5% fat specifications, unlocking premium listings in global non-dairy beverages. Isolates also carry self-affirmed allergen-free claims in multiple jurisdictions, appealing to health-care-oriented SKUs.

Textured formats represent the fastest value-gain opportunity, expanding at 9.27% CAGR as meat-analog developers pivot toward whole-muscle analog forms that require longer fiber strands and firmer bite. Extrusion partners invest in twin-screw systems calibrated to fava’s starch ratio, enabling expansion volumes above 3x while preserving tensile strength. Blends of fava and chickpea textured proteins achieve cleaner flavor profiles than corresponding pea-soy mixes, reducing reliance on masking agents. Category adoption in chilled and frozen ready meals compresses go-to-market timelines, while culinary teams embrace neutral taste that pairs with global spice kits. As more co-man facilities qualify fava matrices, textured volumes will materially lift the overall fava bean protein market.

Fava Bean Protein Market: Market Share by Product Type

| Isolate | 46.84% |

| Source: Mordor Intelligence | |

By Nature: Conventional Dominance with Organic Acceleration

Conventional grades dominated the fava bean protein market share at 81.62% in 2024, buoyed by large acreage in Canada, France, and Australia, where agronomic economics favor standard input regimes. Major processors prefer conventional feedstock to secure year-round plant utilization and hedge price volatility through futures or option overlays. Food manufacturers in mainstream bakery and snack categories accept conventional inputs as long as supply chains maintain full traceability and allergen segregation.

Organic supply, although only 18.38% by value today, is marching forward at 10.11% CAGR as niche beverage, baby food, and premium sports-nutrition brands commit to USDA and EU organic seals. Top Health Ingredients’ certified-organic AdvantaFava grades illustrate the commercial viability of achieving 90% purity without synthetic solvents. Retailers in Germany and Scandinavia allocate expanding shelf space to organic-positioned SKUs, validating consumer willingness to absorb a 20% price uplift. Organic acreage expansion in Eastern Europe and Western Canada could alleviate supply bottlenecks by 2027, lowering price premiums and broadening addressable markets.

By Application: Food Manufacturers Lead While Animal Nutrition Surges

Food and beverage manufacturers commanded 57.83% of the fava bean protein market size in 2024. Dairy-alternative formulators appreciate fava protein’s neutral color, which minimizes bleaching steps. Yeast-raised bakery applications use concentrates for dough strengthening and moisture retention, bridging the performance gap between wheat gluten and soy isolate. Beverage powder blends employ hydrolysates to improve dispersibility and mouthfeel. Clinically backed functional claims elevate fava protein into performance nutrition, adding incremental margin layers for brand owners.

Animal nutrition, while smaller in absolute terms, is the fastest-growing application at 8.22% CAGR. Poultry feed trials document feed-conversion-ratio improvements when fava substitutes for soybean meal at inclusion levels up to 20%, provided vicine and convicine are reduced through thermal treatment. In aquaculture, fava bean protein concentrate mitigates off-flavor in flesh and supports robust weight gain. BENEO integrates food-grade protein production with feed co-products, enhancing whole-bean profitability. Emerging pet-food formulations further diversify demand, positioning animal nutrition as an enduring growth pillar for the fava bean protein market.

Geography Analysis

In 2024, Europe maintained its leadership in the fava bean protein market with a 32.59% share, supported by a strong network of fractionators and Common Agricultural Policy incentives. German, French, and Dutch processors rely on locally sourced, zero-GMO feedstock, ensuring cost-effective traceability aligned with EU Green Deal goals. France’s ANSES introduced safety guidelines mandating vicine-convicine labeling, with swift industry compliance avoiding market disruptions. Scandinavian countries expanded acreage to diversify crops, improve soil health, and reduce fertilizer imports. With mature distribution channels and high consumer acceptance, Europe remains the primary volume hub for fava bean protein.

Meanwhile, Asia-Pacific is the fastest-growing region, with a 9.04% CAGR through 2030. China drives demand through government initiatives for protein self-sufficiency, supported by provincial subsidies for pulse rotation, though processing infrastructure lags. Japanese manufacturers source Canadian isolates for quality and low odor, while Australia targets premium exports to Southeast Asia, diversifying supply and mitigating weather risks. As regional fractionation capacity develops, the Asia-Pacific could rival Europe in market size by the next decade.

North America combines large-scale pulse farming with advanced extraction facilities, positioning itself as a hub for innovation in the fava bean protein market. Roquette’s Manitoba facility supplies isolates and concentrates for food and sports nutrition, leveraging abundant prairie harvests and favorable trade routes into the U.S. FDA GRAS notices provide a clear legal framework, accelerating product development for domestic food companies. Research into enzymatic treatments aims to enhance flavor neutrality, potentially reducing cost barriers and increasing adoption in bakery segments. With supportive policies and strong venture capital investment, North America continues to drive technological advancements in the market, solidifying its strategic importance in the global fava bean protein industry.

Competitive Landscape

The fava bean protein market exhibits a moderate concentration, with the top five suppliers holding an estimated 60-70% combined share. Roquette leverages proprietary wet-extraction expertise and an extensive B2B distribution network to retain lead customer share in beverage and meat-analog sub-segments. BENEO follows with dry-fractionation technology that aligns with EU sustainability mandates and produces integrated starch and fiber co-products that improve plant economics. Ingredion differentiates through customized texturates and regional application labs that optimize formulations in local cuisines. Cosun Protein and Atura Proteins round out the top tier with specialized functional concentrates that target gluten-free bakery and snack-bar applications.

Emerging challengers focus on patented solid-state fermentation and enzymatic hydrolysis that unlock higher digestibility scores and bioactive peptide fractions. Burcon NutraScience’s 2025 launch of FavaPro demonstrates scale-up success in 90%-pure isolates using low-pH extraction systems, opening doors to medical-nutrition applications. Canadian and European farmer-cooperatives explore co-ownership models for new plants, aiming to capture more margin at the farm gate. Overall, technology innovation and geographic expansion into Asia-Pacific remain dominant strategic thrusts, underscoring an evolving yet opportunity-rich competitive landscape.

Fava Bean Protein Industry Leaders

Roquette

Ingredion

BENEO

ADM

AGT Food & Ingredients

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Burcon NutraScience Corporation has officially launched FavaPro™, a next-generation, high-purity fava protein isolate with over 90% protein content, produced using a proprietary extraction and purification process from nutrient-rich, environmentally friendly fava beans.

- May 2024: Roquette, a global leader in plant-based ingredients, has launched NUTRALYS® Fava S900M, its first fava bean protein isolate, in Europe and North America. With a protein content of 90%, this innovative ingredient features a clean taste, light color, and exceptional functional properties, making it ideal for diverse applications such as meat substitutes, non-dairy alternatives, and baked goods.

Global Fava Bean Protein Market Report Scope

| Isolate |

| Concentrate |

| Textured Protein |

| Organic |

| Conventional |

| Food & Beverage Manufacturers | Meat and Fish Analogues |

| Dairy Alternatives | |

| Bakery & Snacks | |

| Sports & Clinical Nutrition | |

| Beverages | |

| Animal Nutrition | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Isolate | |

| Concentrate | ||

| Textured Protein | ||

| By Nature | Organic | |

| Conventional | ||

| By Application | Food & Beverage Manufacturers | Meat and Fish Analogues |

| Dairy Alternatives | ||

| Bakery & Snacks | ||

| Sports & Clinical Nutrition | ||

| Beverages | ||

| Animal Nutrition | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current valuation of the fava bean protein market?

The fava bean protein market is valued at USD 310.22 million in 2025 and is projected to reach USD 481.7 million by 2030 at a 9.2% CAGR.

Which region leads global demand?

Europe holds the largest share at 32.59% on the back of extensive processing infrastructure and supportive policy frameworks.

Which product format is growing fastest?

Textured fava protein is expanding at 9.27% CAGR as meat-analog brands seek improved texture and neutral flavor.

How do regulatory approvals influence commercialization?

FDA GRAS notices and streamlined EU novel-food procedures significantly shorten time to market and lower compliance costs.

What factors limit broader adoption?

A price premium over soy and pea, plus limited fractionation capacity outside Europe and Canada, remain chief constraints.

Page last updated on: