Lemonade Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

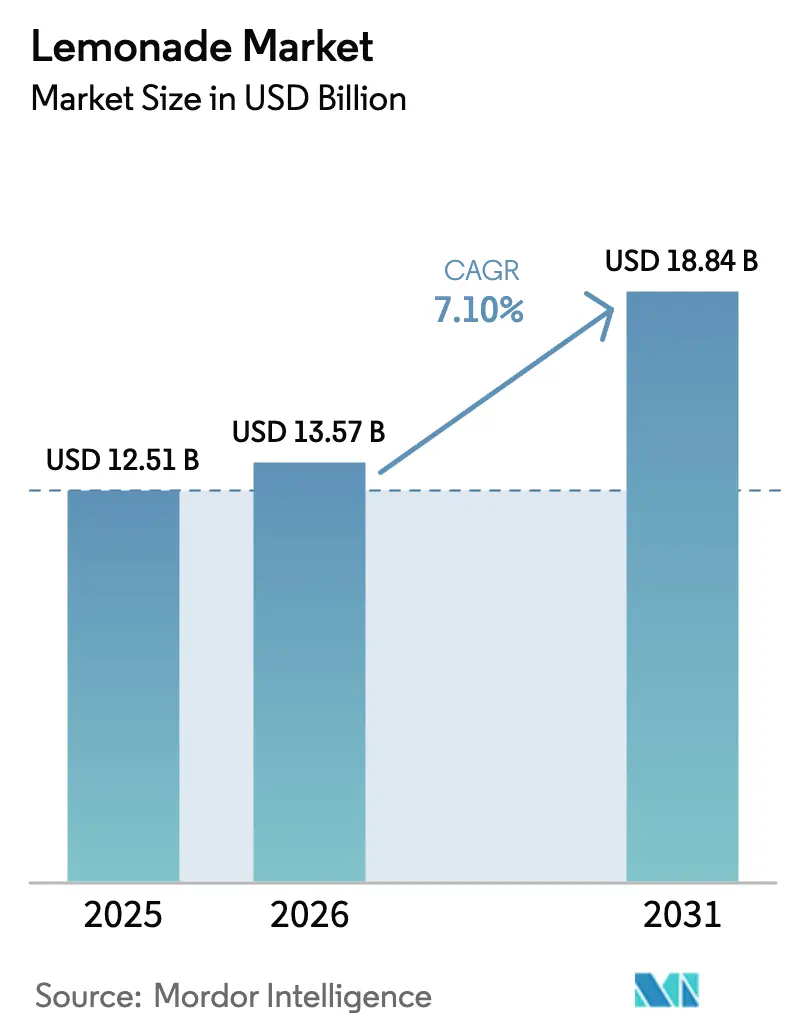

| Market Size (2026) | USD 13.57 Billion |

| Market Size (2031) | USD 18.84 Billion |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

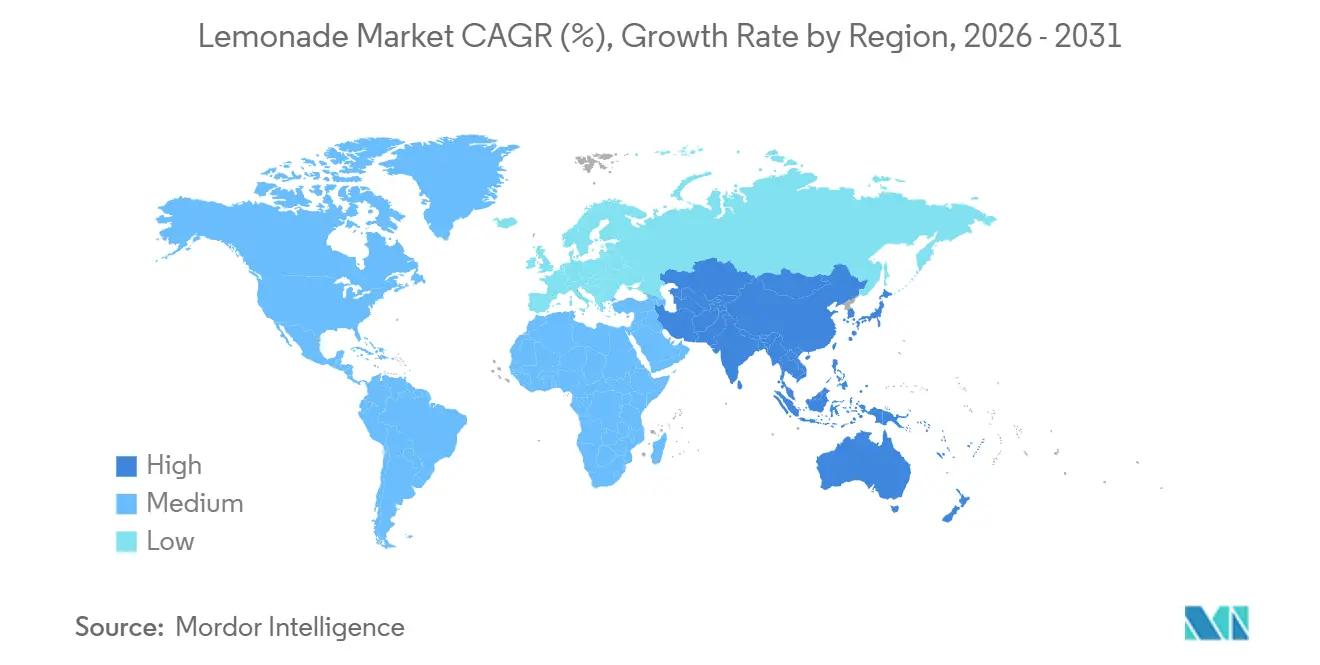

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Lemonade Market Analysis by Mordor Intelligence

The Lemonade Market size is projected to be USD 12.51 billion in 2025, USD 13.57 billion in 2026, and reach USD 18.84 billion by 2031, growing at a CAGR of 7.10% from 2026 to 2031. Rising demand for clean-label recipes, growing interest in immunity-linked functional beverages, and the convenience of single-serve packaging formats are steering formulation and distribution choices. Sugar-reduction targets published by regulators are accelerating the switch to stevia and monk fruit platforms, while cold-chain advances widen the range of premium, preservative-free products. Format innovation in frozen slush and sparkling extensions is expanding day-part consumption, and sustainability directives such as Europe’s proposed PPWR are reshaping material selection for bottles, cans, and pouches. Competitive intensity is heightening as global beverage multinationals defend legacy share against craft entrants funded by venture capital and celebrity investors.

Key Report Takeaways

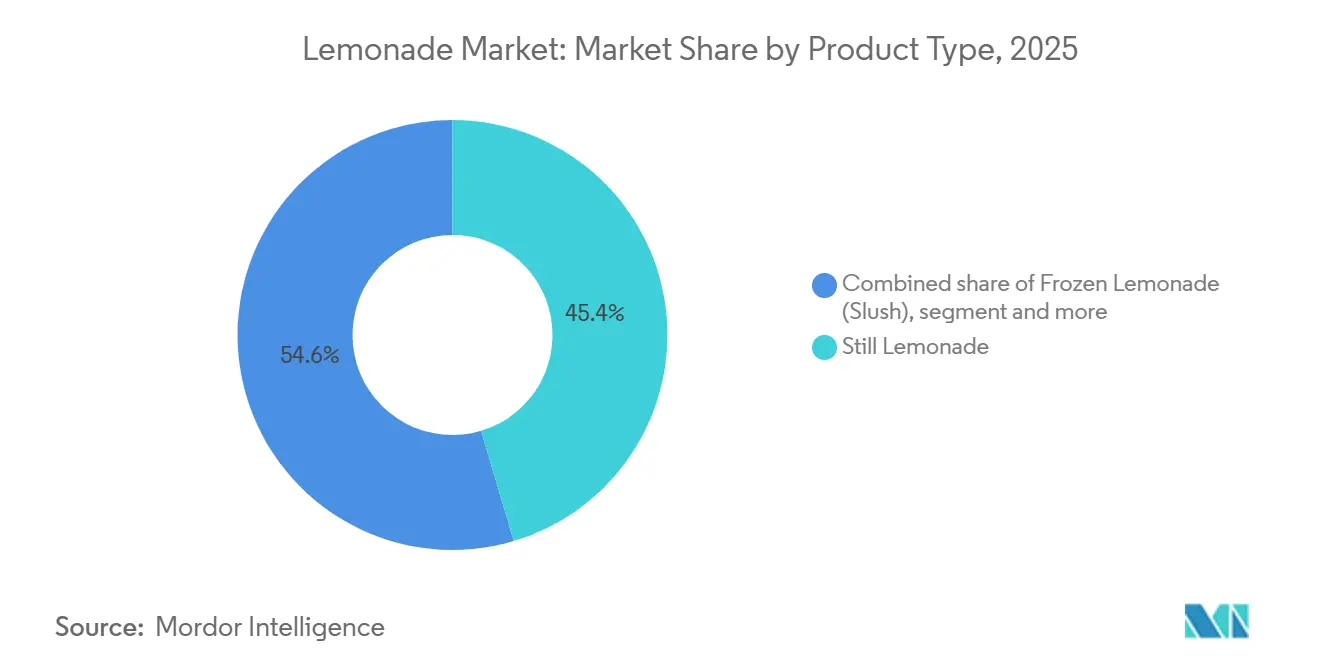

- By product type, still lemonade led with 45.39% of value in 2025, while frozen formats are projected to expand at an 8.56% CAGR through 2031, the fastest in the segment.

- By sweetener type, sugar-sweetened SKUs held 70.84% of the lemonade market share in 2025, yet natural non-nutritive alternatives are advancing at an 8.47% CAGR to 2031.

- By flavor, plain variants accounted for 55.02% of volume in 2025, while flavored extensions are forecast to post a 9.64% CAGR to 2031, outperforming the total lemonade market by 2.5 percentage points.

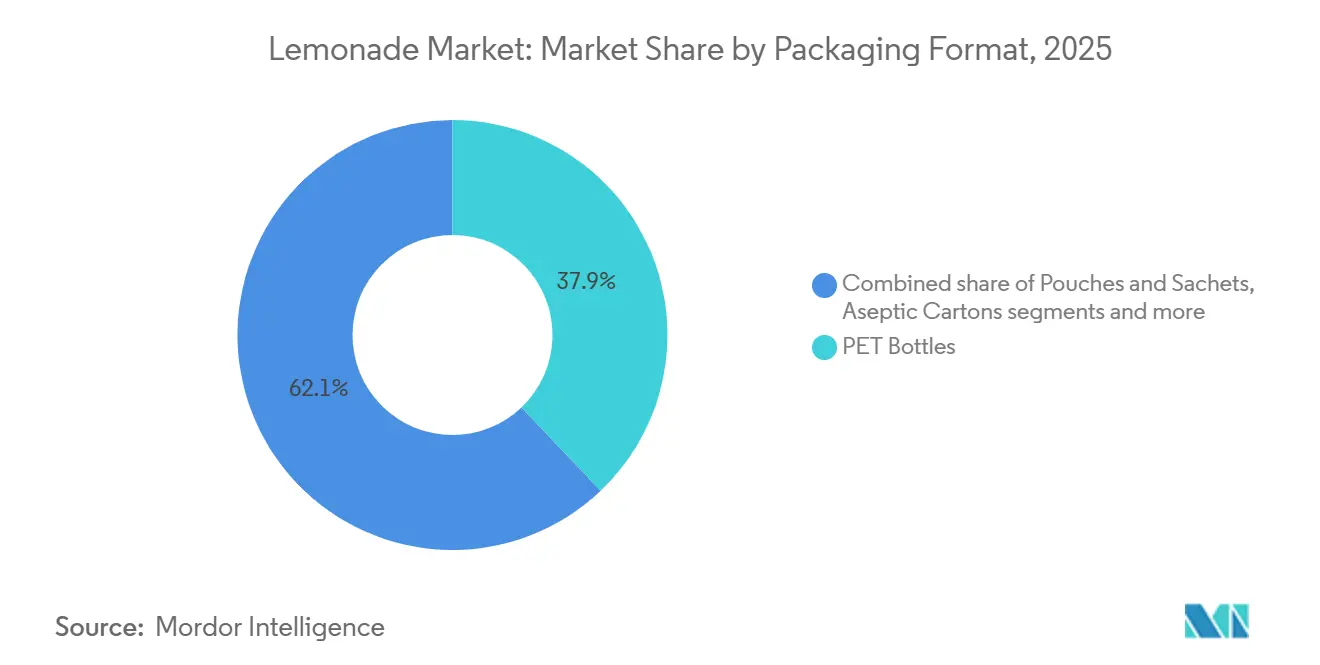

- By packaging format, PET controlled 37.89% value share in 2025, and pouches and sachets are on track for a 7.87% CAGR through 2031 as brands target logistics savings and lower carbon footprints.

- By distribution channel, off-trade retained 72.94% of sales in 2025, while on-trade venues are rebounding at an 8.69% CAGR to 2031 as foodservice recovers and experiential occasions multiply.

- By geography, North America contributed 34.12% of 2025 revenue, but Asia-Pacific is projected to climb at an 8.92% CAGR, outpacing every other region up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lemonade Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference for natural and organic lemonade | +1.2% | Global, with concentration in North America and Western Europe | Medium term (2-4 years) |

| Growing on-the-go RTD beverage consumption | +1.5% | Global, strongest in urban centers across North America, Asia-Pacific, and Europe | Short term (≤ 2 years) |

| Innovation in functional and fortified product offerings | +1.3% | North America and Asia-Pacific core, expanding to Europe and MEA | Medium term (2-4 years) |

| Craft micro-lemonade brands leveraging local citrus | +0.8% | Regional, with early gains in North America (California, Texas), Europe (Mediterranean), and select Asia-Pacific markets | Long term (≥ 4 years) |

| Sustainability and eco-friendly packaging | +1.0% | Europe (driven by PPWR), North America, and Asia-Pacific (Japan, South Korea) | Medium term (2-4 years) |

| Shift to non-carbonated and "better-for-you" drinks | +1.4% | Global, with pronounced adoption in North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Preference for natural and organic lemonade

Clean-label reformulation has transitioned from a niche strategy to a standard expectation in mainstream lemonade portfolios. This shift is largely fueled by heightened consumer scrutiny of ingredient lists and mounting regulatory pressures to simplify formulations. For instance, the Organic Trade Association reported that the consumption value of organic beverages in the U.S. reached a notable USD 2,802.5 million in 2025[1]Source: Organic Trade Association, "Organics Dashboard From Passport", ota.com. In response, brands are actively removing artificial colors, flavors, and preservatives. They're also placing a stronger emphasis on sourcing organic citrus and obtaining non-GMO certifications. Lemon Perfect's offering of zero-sugar, organic lemon water stands as a testament to the premium positioning brands can achieve when they prioritize certified organic inputs and minimal processing. However, this trend is complicating supply chains. Brands are now challenged to secure consistent volumes of organic lemons, especially given the tighter agricultural supply and price volatility highlighted by USDA crop reports. The strategic takeaway is evident: brands that commit to long-term organic citrus contracts and bolster their traceability infrastructure stand to gain margin premiums and foster consumer loyalty. In contrast, those leaning on spot markets expose themselves to potential cost surges and availability challenges.

Growing on-the-go RTD beverage consumption

Urbanization, longer commutes, and the decline of structured meal times are driving consistent demand for portable, single-serve ready-to-drink (RTD) formats. These formats provide convenience while maintaining a health-focused appeal. This trend is particularly prominent among individuals aged 21-44, who show a stronger preference for on-the-go consumption and digital-first discovery channels. A significant shift from home-prepared meals to RTD formats is highlighted by Coca-Cola's decision to discontinue Minute Maid frozen concentrate cans in February 2026, citing a clear consumer inclination toward fresh and RTD beverages over products requiring reconstitution. Brands are responding by expanding their single-serve SKU offerings, improving closure systems for resealability, and investing in packaging formats, such as aluminum cans, pouches, and aseptic cartons, that support mobile consumption. Additionally, the opportunity extends beyond product design to channel strategy. On-trade venues, including cafes, quick-service restaurants, and convenience stores, are expected to grow faster than off-trade channels. This growth emphasizes the importance of foodservice partnerships and the potential of fountain and dispensed formats to capture additional consumption occasions.

Innovation in functional and fortified product offerings

Brands are shifting functional beverage innovations from niche wellness channels to mainstream lemonade portfolios, infusing familiar citrus platforms with benefits like immunity, energy, hydration, and gut health. In February 2026, True Citrus introduced functional lemonade extensions, adding probiotics, prebiotics, and adaptogens to cater to consumer needs beyond mere refreshment. This move aligns with the growth of the broader functional beverage category, especially in modern soda and enhanced water segments, highlighting consumers' readiness to pay a premium for credible functional claims. Yet, the landscape is becoming more regulated. The FDA's revised definition of "healthy" claims and proposals for front-of-package labeling demand brands substantiate their functional claims and adhere to nutrient thresholds. Brands that prioritize clinical validation, obtain third-party certifications, and adjust formulations per FDA's evolving guidance will stand out in the crowded functional market. In contrast, those leaning on ambiguous wellness messaging risk enforcement actions and consumer doubt. The key strategy is to ground functional claims in tangible outcomes, like electrolyte replenishment, vitamin C levels, and probiotic CFU counts, and to ensure these benefits are clearly communicated through on-pack transparency and digital platforms.

Craft micro-lemonade brands leveraging local citrus

Regional craft lemonade brands are carving out unique niches by focusing on local citrus sourcing, artisanal production, and community storytelling, elements that multinational corporations find hard to replicate. In August 2025, Buda Juice, a Texas-based cold-crafted citrus brand, filed an S-1 registration statement, unveiling its innovative 35°F continuous cold-chain model. This model ensures the delivery of non-heat-treated, non-HPP lemonade, boasting an 8-12 day shelf life. Buda Juice's lemonade stands out due to its proprietary wash systems and food safety protocols validated by universities. The company is pursuing a three-hub geographic expansion strategy, setting its sights on Dallas, the Southeast (South Carolina), and the West (Arizona/Nevada). This approach aims for regional dominance by reducing transit times and logistics costs, all while prioritizing freshness. While other craft entrants can replicate this model, it demands a hefty capital investment of USD 5 million per hub and a disciplined approach to uphold cold-chain integrity. The real challenge for established brands isn't the scale but the authenticity that craft brands bring. These craft brands, by emphasizing provenance, transparency, and unique taste profiles, can command premium prices and secure coveted shelf space in natural and organic retail sections, something mass-produced lemonades struggle to achieve. In response, established brands like Tropicana Brands Group are eyeing acquisitions in the functional and craft beverage arena and are also rolling out premium line extensions that echo craft positioning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lemon supply seasonality and price volatility | -0.9% | Global, with acute pressure in North America (Florida, California) and Mediterranean Europe | Short term (≤ 2 years) |

| Stringent regulatory policies and sugar taxes | -0.7% | Europe (sugar taxes, PPWR), North America (FDA labeling), select Asia-Pacific markets (Singapore, Thailand) | Medium term (2-4 years) |

| Shelf-life limits for preservative-free lemonade | -0.5% | Global, particularly impacting craft and organic segments | Medium term (2-4 years) |

| Preference for freshly made lemonade | -0.4% | Regional, strongest in foodservice-heavy markets (North America, Europe) and emerging Asia-Pacific urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lemon supply seasonality and price volatility

Climate variability, disease pressures such as citrus greening (HLB), and geographically concentrated production expose citrus supply chains to structural vulnerabilities. These issues result in cost and availability risks, squeezing margins and disrupting production schedules. USDA agricultural data highlights significant seasonal variations in lemon yields and pricing, with spot prices rising sharply during off-seasons and adverse weather conditions. Florida's orange production has declined due to citrus greening, while lemon groves face similar challenges. As a result, brands have diversified their sourcing to include both domestic and international suppliers, such as those in Mexico and the Mediterranean. Buda Juice's S-1 filing indicates that approximately 50% of its citrus is sourced domestically, with the remainder coming from Mexico. This approach, while advantageous, exposes the company to risks like tariffs, currency fluctuations, and cross-border logistics complexities. Brands with long-term grower contracts, diversified sourcing geographies, and vertical integration into citrus processing are better equipped to handle volatility. Conversely, those relying on spot markets are more susceptible to margin compression during supply shocks. To enhance supply-chain resilience, the industry is adopting strategies like multi-sourcing, inventory buffering, and financial hedging. Furthermore, there is increasing investment in agricultural technology, including AI-driven disease detection and precision irrigation, to stabilize yields.

Stringent regulatory policies and sugar taxes

Regulatory frameworks are reshaping the landscape for food and beverage companies. New rules on sugar content, front-of-package labeling, and sustainable packaging are driving up compliance costs and hastening reformulation cycles. This trend is creating hurdles for smaller players and prompting strategic shifts for established companies. For instance, the FDA's proposed rule on front-of-package nutrition labeling mandates that added sugars, sodium, and saturated fats be prominently displayed. This change not only alters package design but could also sway consumer purchasing decisions. Similarly, sugar taxes in regions like Mexico, certain U.S. cities, and parts of Europe are levying charges on high-sugar beverages. This move is nudging companies to reformulate their products towards low- and zero-sugar alternatives. In Europe, the PPWR is setting stringent standards, including minimum recycled content and circularity targets. Brands are now tasked with redesigning their packaging systems and sourcing certified sustainable materials. While these regulatory demands tighten profit margins, due to costs like reformulation, research and development, and compliance documentation, they also present a silver lining. Brands that act swiftly, securing partnerships for cost-effective natural sweeteners like stevia and monk fruit, as well as sustainable packaging, can carve out a competitive edge. The overarching message is clear: regulatory compliance is evolving from a mere cost to a strategic differentiator. Brands that adapt early not only appeal to health-conscious consumers but also mitigate risks associated with future enforcement actions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Frozen Formats Gain Despite Still Dominance

In 2025, still lemonade accounted for 45.39% of the lemonade market, driven by its extensive retail availability, durability on both ambient and chilled shelves, and strong consumer familiarity. This format continues to play a pivotal role in multipack promotions and meal-deal collaborations, making it a reliable choice for retailers and consumers alike. On the other hand, carbonated lemonade caters to a niche audience seeking unique flavors, while powders and concentrates primarily attract budget-conscious shoppers. However, the demand for powders and concentrates is declining as they require additional preparation time, leading to reduced shelf space. Coca-Cola's strategic decision to discontinue frozen concentrate cans highlights this declining trend and reflects retailers' increasing inclination toward ready-to-drink (RTD) options, which offer greater convenience and align with evolving consumer preferences.

Frozen slush is anticipated to register a robust 8.56% CAGR between 2026 and 2031, emerging as the fastest-growing product format in terms of incremental volume. Innovative and experiential launches, such as SOUR PATCH KIDS Lemonade Fest Slush, illustrate how limited-time offerings can justify premium pricing in quick-service restaurants. By leveraging proprietary equipment and collaborating on unique flavor creations, chains can introduce new offerings on a quarterly basis, effectively capturing the attention of younger consumers and maintaining their engagement. However, the growth potential of frozen slush is moderated by its seasonal nature. Operators must ensure the consistent functionality of cold dispensers and refrigeration systems, which can lead to increased utility costs during periods of lower foot traffic, particularly in the winter months.

By Sweetener Type: Natural Alternatives Accelerate Amid Sugar Dominance

In 2025, sugar-sweetened SKUs accounted for 70.84% of the market's value. However, this significant share is gradually declining due to the implementation of stricter labeling regulations and an increasing emphasis on health consciousness among consumers. Reformulating products to reduce sugar content presents challenges, as sugar plays a vital role in providing the desired mouthfeel and ensuring microbial stability. As a result, processors are exercising caution to preserve taste consistency while transitioning to alternative sweeteners. Although artificial sweeteners continue to attract calorie-conscious consumers, they face ongoing challenges related to their image, primarily due to their association with synthetic chemical processes.

Natural, non-nutritive sweetener blends are experiencing the fastest growth trajectory, with a projected compound annual growth rate (CAGR) of 8.47% through 2031. These blends are gaining popularity among consumers who seek zero-calorie options derived from natural, plant-based sources. Brands that excel in utilizing reb M stevia and monk fruit masking techniques can successfully launch products that overcome the bitterness issues commonly associated with earlier stevia formulations. To address the growing demand for high-purity extracts, securing adequate supply has become a critical priority within the supply chain. Consequently, companies are increasingly entering into multi-year offtake agreements with ingredient suppliers to ensure consistent availability of these essential components.

By Flavor: Tropical and Functional Infusions Drive Flavored Surge

In 2025, plain lemonade led the market, accounting for 55.02% of the total liters sold. This highlights its significance as a versatile product, serving as a popular mixer, a preferred choice for children, and an accessible entry point into the lemonade category. The format performs particularly well in club packs and institutional food services, where affordability and cost per serving are critical factors. However, despite its strong presence, plain lemonade has started to underperform compared to the overall lemonade market, with the growth gap between the two continuing to widen.

Conversely, flavored lemonades are experiencing robust growth and are projected to expand at a compound annual growth rate (CAGR) of 9.64% through 2031. This growth is driven by the introduction of innovative flavors such as mango, berry, and botanical blends, which appeal to adult consumers seeking new and unique taste experiences. Additionally, the incorporation of functional ingredients like ginger and turmeric taps into the growing demand for wellness-oriented products. These additives not only enhance the health appeal of flavored lemonades but also enable brands to command premium pricing, particularly in natural and specialty retail channels. As retailers update their product assortments, there is a clear shift toward fast-moving tropical and fusion flavor profiles, which is expected to steadily increase the market share of flavored SKUs within the lemonade segment.

By Packaging Format: Sustainability Mandates Reshape Material Choices

In 2025, PET bottles contributed to 37.89% of total revenues, driven by their transparency, lightweight properties, and seamless compatibility with high-speed production lines. However, the decline in municipal recycling rates has placed PET under increased scrutiny from policymakers. This has compelled beverage companies to either enhance the recycled content in PET bottles or transition to alternative materials such as aluminum and paper-based solutions. Aluminum cans, which feature an impressive 73% average recycled content in North America, are gaining significant traction, particularly in sparkling and functional beverage categories, due to their sustainability and consumer acceptance.

The market for pouches and sachets is anticipated to grow at a robust CAGR of 7.87% through 2031. These packaging formats offer substantial environmental benefits by reducing transport emissions, as they are designed to be flat and lightweight. Additionally, advancements such as resealable spouts and puncture-resistant laminates address consumer needs for convenience and on-the-go usage while mitigating the risk of leakage. Brands that prominently display life-cycle impact data on their packaging can effectively differentiate themselves in environmentally conscious retail channels and proactively avoid potential future costs associated with Extended Producer Responsibility (EPR) levies.

By Distribution Channel: E-Commerce and On-Trade Rebound

In 2025, off-trade sales led the market, accounting for 72.94% of total sales. This dominance highlights the effectiveness of supermarket promotions, the convenience offered by store chillers, and the growing popularity of the click-and-collect model. Although the lemonade market size within digital retail channels remains relatively small, it is steadily expanding. Factors such as the increasing adoption of subscription bundles and the influence of social media-driven drop shipments are driving this growth, particularly among Gen Z households. Additionally, rising internet penetration is playing a crucial role in supporting online retail channels. For example, according to the International Telecommunication Union (ITU), 74% of the global population had internet access in 2025, compared to 71% in 2024[2]Source: International Telecommunication Union (ITU), "Individuals using the Internet", itu.int.

On the other hand, on-trade sales are projected to grow at a faster pace than grocery sales, with a robust CAGR of 8.69% during the same period. Quick-service restaurant chains, such as SONIC, have successfully demonstrated that introducing rotating frozen lemonade slush combinations can significantly increase foot traffic and generate buzz on social media. This, in turn, translates into higher beverage sales. While securing tap space or fountain nozzles often requires providing equipment subsidies, the investment is justified by the strong margins. Premium pricing of servings, compared to retail multipacks, further supports the profitability of this strategy.

Geography Analysis

In 2025, North America accounted for 34.12% of the market, driven by established RTD consumption habits, high per-capita beverage spending, and a mature retail infrastructure. This regional dominance highlights decades of category development by major players like PepsiCo, Coca-Cola, and Keurig Dr Pepper, along with premiumization trends favoring organic, functional, and craft lemonade segments. Regulatory changes, such as FDA's front-of-package labeling proposals and sugar taxes in certain municipalities, are accelerating the shift toward natural sweeteners and reduced-sugar variants. This transition creates significant opportunities for brands that act quickly and secure cost-effective ingredient supplies. Meanwhile, craft and functional challengers like Lemon Perfect and Buda Juice are capitalizing on market gaps through hyper-local sourcing, cold-chain innovations, and purpose-driven storytelling. Established players are responding with premium line extensions and mergers and acquisitions evaluations. Additionally, strong local lemon production supports the market, with the US Department of Agriculture reporting a production value of USD 698,343 thousand for lemons in the United States in 2024[3]Source: United States Department of Agriculture, "Citrus Fruits 2024 Summary", usda.gov .

Asia-Pacific is projected to grow at a CAGR of 8.92% from 2026 to 2031, surpassing the global average by 1.8 percentage points. This growth is attributed to rising disposable incomes, urbanization, and the increasing penetration of modern retail in China, India, Southeast Asia, and Oceania. The region's growth trajectory is supported by the expansion of convenience store networks, e-commerce platforms, and cold-chain infrastructure that facilitate RTD beverage distribution. Additionally, younger urban populations are increasingly adopting Western consumption patterns. For example, Minute Maid Zero Sugar's 2025 rollout in select Asia-Pacific countries demonstrates how multinational brands are adapting their product portfolios to align with regional health trends and regulatory requirements, driving value-share gains.

Europe reflects similar trends, with a focus on premiumization and sustainability. PPWR mandates are driving packaging innovations, while organic and natural positioning appeals to health-conscious consumers. South America, along with the Middle East and Africa, shows moderate growth driven by population increases, urbanization, and the gradual modernization of retail channels. However, infrastructure gaps and price sensitivity limit the penetration of premium segments. Brands looking to enter or expand in Asia-Pacific must navigate diverse regulatory frameworks, establish local distribution partnerships, and adapt product formulations, such as sweetness levels, flavor profiles, and packaging formats, to meet regional taste preferences and purchasing power.

Competitive Landscape

The lemonade market is characterized by moderate consolidation. Global multinational corporations are leveraging their financial resources, research and development capabilities, and robust marketing strategies to maintain a strong presence on retail shelves. At the same time, smaller, agile micro-brands are strategically targeting premium niches to establish their foothold. The recent partnership announced in July 2024 between Carlsberg and Britvic highlights the ongoing trend of consolidation, as major beverage companies seek to capitalize on synergies within the soft-drink sector. Additionally, PepsiCo's pep+ sustainability initiative reflects a broader industry shift, where environmental performance has become a critical factor for securing investor confidence and ensuring retail distribution opportunities.

To enhance operational efficiency and extend product shelf life, companies are increasingly adopting advanced technologies such as aseptic filling, high-pressure processing, and digital supply chain management systems. These innovations also help optimize maintenance processes, ensuring smoother operations. Smaller manufacturers are expanding their market presence by focusing on locally sourced ingredients, incorporating botanical elements, and developing low-sugar formulations that align with growing consumer preferences for healthier options. In contrast, larger manufacturers are prioritizing the implementation of automation technologies, introducing innovative packaging solutions, and improving labeling systems to enhance product traceability and accessibility. The growing demand for ready-to-drink formats and organic products continues to drive significant product development efforts within the lemonade market.

The lemonade market is also experiencing downward price pressures in the traditional still beverage category. However, premium segments, including frozen lemonade, functional beverages, and products with eco-friendly packaging, are helping to sustain overall profit margins. The increasing availability of high-quality private-label products from retailers is compelling established brands to innovate by updating their packaging designs, introducing new flavors, and refining their distribution strategies. To maintain competitiveness through 2030, the industry is leveraging economies of scale in production while simultaneously focusing on targeted product differentiation. This dual approach enables companies to effectively address evolving consumer demands and sustain their market position.

Lemonade Industry Leaders

-

The Coca-Cola Company

-

PepsiCo Inc.

-

Keurig Dr Pepper Inc.

-

Carlsberg A/S

-

Suntory Holdings Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Vita Coco unveiled Frosted Lemonade, a new coconut milk-based beverage in their indulgent "Treats" line, combining tart lemon with creamy coconut.

- April 2025: Carlsberg Britvic launched 7Up Pink Lemonade, a zero-sugar beverage that combined lemon, lime, and raspberry flavors. This addition to the brand's portfolio addressed consumer demand for new options in the flavored carbonates category, offering a refreshing alternative that does not compromise on taste.

- April 2025: BeatBox introduced a new line of three lemonade flavors: Lemon Squeeze, Watermelon Lemonade, and Blueberry Lemonade, with the latter developed in collaboration with Shaquille O'Neal. The beverages were packaged in 500ml resealable Tetra Pak cartons and contained 11.1% alcohol by volume (ABV). The products were gluten-free, low in sugar, shelf-stable, and formulated for various social occasions.

Global Lemonade Market Report Scope

Lemonade is a drink made from lemon juice and water sweetened with sugar. The lemonade market report is segmented by product type, sweetener type, flavor, packaging format, distribution channel, and geography. By product type, the market is segmented into still, carbonated, concentrates/powder mixes, and frozen slush. By sweetener type, the market is segmented into sugar-sweetened, low/no-calorie artificial, and natural non-nutritive. By flavor, the market is segmented into plain and flavored. By packaging format, the market is segmented into PET bottles, aluminum cans, aseptic cartons, pouches/sachets, and fountain/dispensed. By distribution channel, the market is segmented into on-trade and off-trade. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, the Middle East and Africa. For each segment market forecasts are provided in value (USD) and volume (tons).

| Still Lemonade |

| Carbonated Lemonade |

| Lemonade Concentrates and Powder Mixes |

| Frozen Lemonade (Slush) |

| Sugar-sweetened |

| Low/No-Calorie Artificial Sweeteners |

| Natural Non-nutritive Sweeteners (Stevia, Monk Fruit) |

| Plain |

| Flavored |

| PET Bottles |

| Aluminum Cans |

| Aseptic Cartons |

| Pouches and Sachets |

| Fountain/Dispensed |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Still Lemonade | |

| Carbonated Lemonade | ||

| Lemonade Concentrates and Powder Mixes | ||

| Frozen Lemonade (Slush) | ||

| By Sweetener Type | Sugar-sweetened | |

| Low/No-Calorie Artificial Sweeteners | ||

| Natural Non-nutritive Sweeteners (Stevia, Monk Fruit) | ||

| By Flavor | Plain | |

| Flavored | ||

| By Packaging Format | PET Bottles | |

| Aluminum Cans | ||

| Aseptic Cartons | ||

| Pouches and Sachets | ||

| Fountain/Dispensed | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the lemonade market in 2026?

The lemonade market size stands at USD 13.37 billion in 2026, on its way to USD 18.84 billion by 2031.

What CAGR is expected for lemonade between 2026 and 2031?

The category is forecast to grow at a 7.1% CAGR during the 2026-2031 period.

Which product format will expand the fastest?

Frozen lemonade slush is projected to post an 8.56% CAGR, outpacing still, carbonated, and powder segments.

Why are natural sweeteners gaining traction?

Regulatory sugar caps and health-conscious consumers favor stevia and monk fruit, driving an 8.47% CAGR for natural sweetened SKUs.

Page last updated on: