Leather Jackets Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

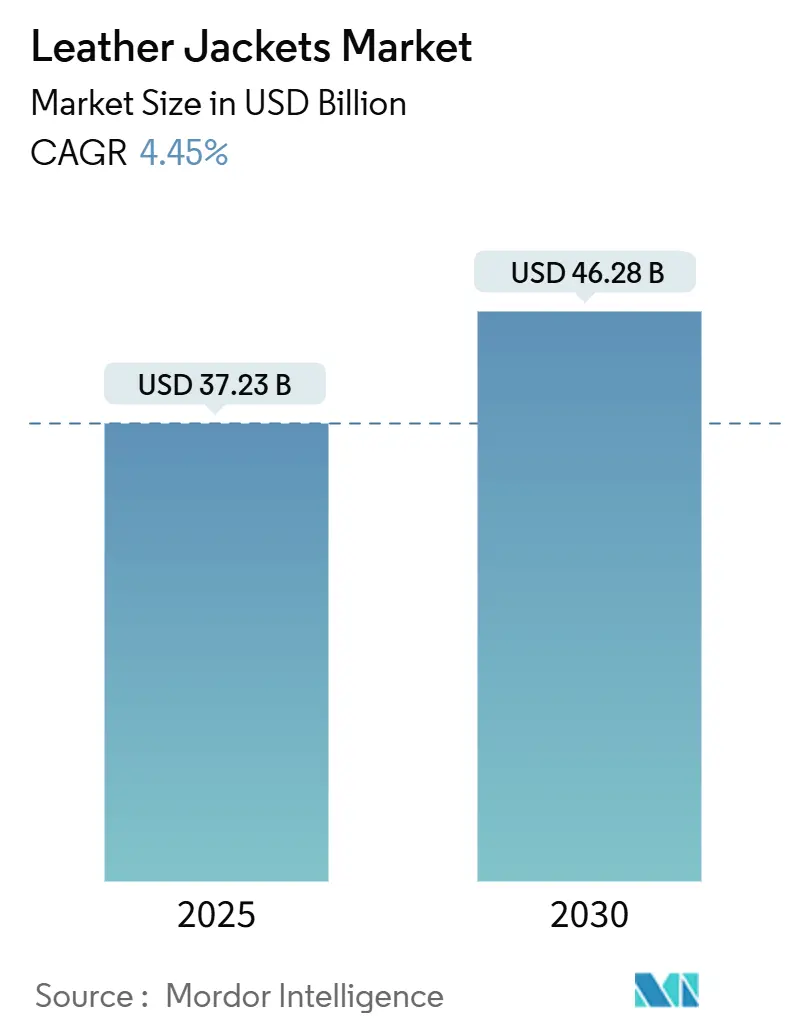

| Market Size (2025) | USD 37.23 Billion |

| Market Size (2030) | USD 46.28 Billion |

| Growth Rate (2025 - 2030) | 4.45% CAGR |

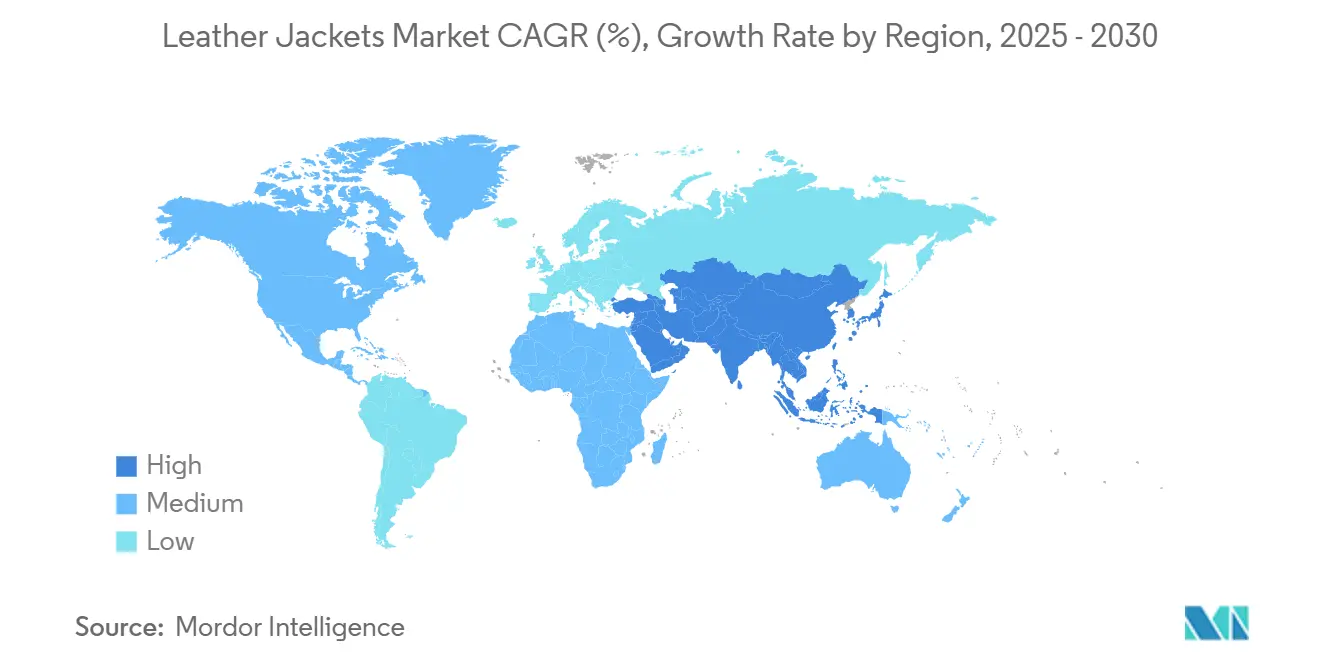

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

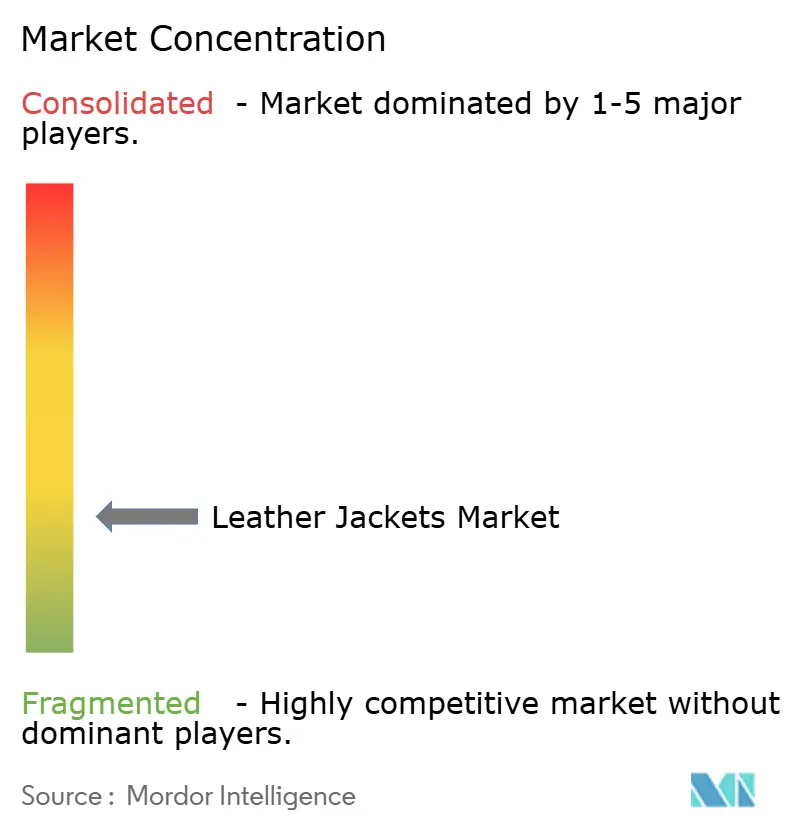

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Leather Jackets Market Analysis by Mordor Intelligence

In 2025, the leather jacket market size is valued at USD 37.23 billion and is expected to grow to USD 46.28 billion by 2030, registering a steady CAGR of 4.45% during the forecast period. This growth is driven by strong demand for premium outerwear and the versatile appeal of leather jackets as both functional protective wear and fashionable attire. Advancements in material innovation that avoid harsh chemicals, enhanced brand storytelling focused on sustainability, and the expansion of e-commerce channels enable manufacturers to maintain margins despite market maturity. Affluent consumers continue to view genuine leather as a durable and worthwhile wardrobe investment, while middle-income consumers increasingly opt for synthetic alternatives. Companies that adhere to traceability standards and establish vertically integrated supply chains are well-positioned to capitalize on emerging profit opportunities as regulatory frameworks become more stringent.

Key Report Takeaways

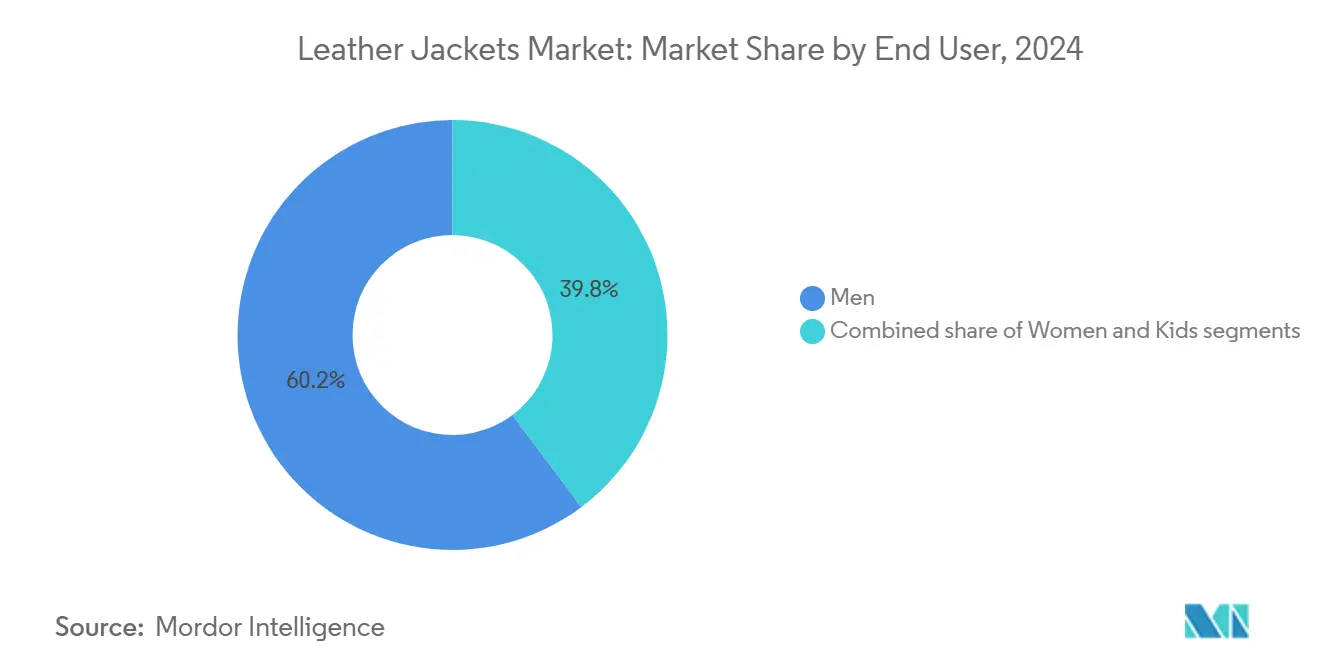

- By end user, men held 60.24% of leather jacket market share in 2024, while the kids segment is set to expand at a 7.80% CAGR to 2030.

- By material, conventional leather accounted for 81.23% of the leather jacket market size in 2024; synthetic/vegan materials are forecast to grow at a 9.20% CAGR through 2030.

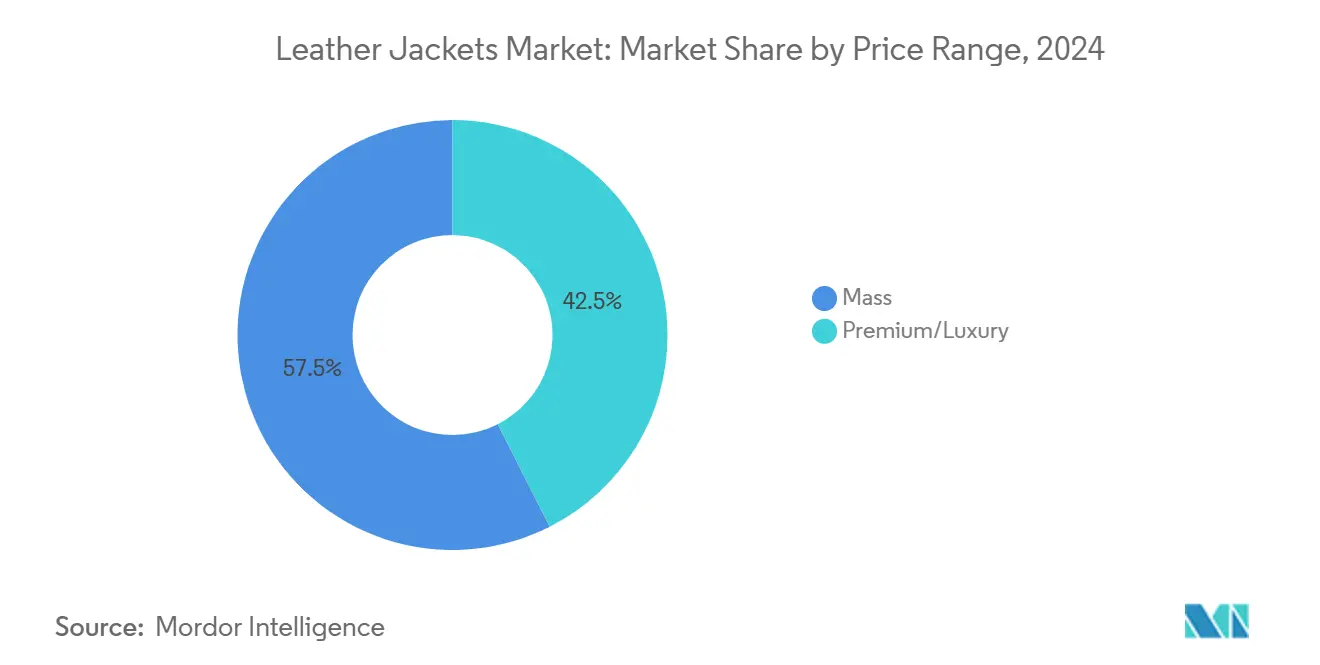

- By price range, mass market accounted for 57.48% of the leather jacket market size in 2024; premium/luxury are forecast to grow at a 7.10% CAGR through 2030.

- By distribution channel, online platforms commanded 45.26% revenue share in 2024, whereas offline retail is expected to post the fastest 8.50% CAGR to 2030.

- By geography, North America led with 32.46% of leather jacket market share in 2024; Asia-Pacific is projected to register a 9.60% CAGR through 2030.

Global Leather Jackets Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements in materials | +0.8% | Global, with concentration in Europe and North America | Medium term (2-4 years) |

| Cultural and lifestyle associations | +0.7% | North America and Europe core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of global e-commerce apparel platforms | +0.9% | Global, with strongest impact in Asia-Pacific and North America | Short term (≤ 2 years) |

| Influence of retro and vintage fashion | +0.6% | North America and Europe, emerging in Asia-Pacific urban centers | Medium term (2-4 years) |

| Growth in custom "made-to-measure" jackets | +0.5% | North America and Europe premium markets | Long term (≥ 4 years) |

| Traceable sustainable-leather certifications | +0.4% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technological advancements in materials

Material innovation is a critical factor driving market growth, delivering enhanced performance and ensuring adherence to environmental regulations. Evolved by Nature's Activated Silk L1 finishing system highlights the potential of biotechnology to replace harmful chemicals while maintaining the integrity and quality of leather. This breakthrough allows suppliers in developing markets to compete more effectively with well-established European producers. Furthermore, these advancements address stringent regulatory requirements and offer cost efficiencies for manufacturers transitioning to sustainable processing methods. The adoption of bio-based finishing systems also reduces dependence on chrome-tanning processes, which are subject to increasingly strict EPA regulations, capping total chromium discharge at a daily maximum of 12 mg/l[1]Code of Federal Regulations, "§ 425.15 Pretreatment standards for existing sources (PSES).", ecfr.gov.

Cultural and lifestyle associations

Leather jackets have consistently remained a timeless fashion staple across generations and regions, symbolizing style, rebellion, and status. Their enduring appeal stems from their strong association with iconic subcultures, such as bikers, rock musicians, and Hollywood celebrities, which has cemented their cultural significance. Furthermore, their versatility makes them suitable for both fashion-conscious individuals and those seeking practicality. With the growing influence of Western fashion trends and vintage aesthetics, particularly in emerging markets, leather jackets continue to resonate with a wide range of consumers. This sustained demand is driving the growth of the leather jackets market and facilitating its expansion beyond traditional boundaries.

Expansion of global e-commerce apparel platforms

Digital transformation is significantly expanding market reach and enhancing consumer accessibility, offering substantial advantages to niche brands and custom manufacturers. E-commerce platforms not only eliminate geographic barriers but also empower brands to establish direct-to-consumer relationships, effectively bypassing traditional retail markups. This strategic channel expansion is projected to drive the online segment's 45.26% market share in 2024, while simultaneously creating avenues for personalized, made-to-measure, and on-demand services. Furthermore, the integration of advanced technologies, such as AI and data analytics, is enabling brands to better understand consumer preferences and deliver tailored experiences. Moreover, the digital shift is improving transparency across supply chain practices, addressing growing consumer demands for traceable, ethical, and sustainable leather products.

Influence of retro and vintage fashion

In 2025, classic leather jacket styles, biker, bomber, and moto, are witnessing a significant revival, driven by their popularity among Millennials and Gen Z consumers. According to the United States Census Bureau, Millennials made up approximately 21.81% of the U.S. population in 2024, while Generation Z closely followed at 20.81 percent[2]US Census Bureau, "Population distribution in the United States in 2024, by generation", census.gov. Designers have redefined these iconic styles by introducing tailored fits, eco-friendly materials, and an expanded color palette to align with shifting consumer preferences. Drawing inspiration from the ‘70s, ‘80s, and ‘90s, they have incorporated elements such as distressed textures, retro-inspired hardware, and heritage silhouettes. This seamless integration of vintage aesthetics with modern innovation not only evokes nostalgia but also underscores the growing importance of storytelling and authenticity in fashion. Consequently, leather jackets remain timeless wardrobe staples, resonating with consumers who prioritize individuality, tradition, and sustainability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-hide price volatility and supply disruption | -0.9% | Global, with strongest impact in North America and Europe | Short term (≤ 2 years) |

| Shift toward vegan alternatives on animal-welfare grounds | -0.7% | Europe and North America, expanding to Asia-Pacific urban centers | Medium term (2-4 years) |

| Chrome-tanning effluent regulation tightening | -0.6% | Global, with strictest enforcement in Europe and North America | Long term (≥ 4 years) |

| Rise of second-hand/rental fashion platforms | -0.5% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-hide price volatility and supply disruption

Leather jacket manufacturers are grappling with increasing cost pressures due to ongoing supply chain instability. According to the Leather and Hide Council of America, the contribution of U.S. cattle hides to the total value of beef cattle has dropped sharply, decreasing from a historical range of 6-8% to approximately 1% as of 2024. This significant decline has forced manufacturers to implement flexible pricing strategies and diversify sourcing regions, potentially disrupting long-standing supply chains and supplier relationships. Additionally, the geographic concentration of hide production exacerbates supply risks, particularly as climate change, disease outbreaks, and other external factors continue to adversely affect cattle populations and overall hide availability.

Shift toward vegan alternatives on animal-welfare grounds

Growing consumer awareness of animal welfare and environmental concerns is driving a significant increase in demand for synthetic and plant-based leather alternatives, disrupting the dominance of the traditional leather market. The synthetic/vegan leather segment is expected to grow at a strong CAGR of 9.2% through 2030, reflecting a notable shift in consumer preferences, particularly among younger and urban populations. According to World Bank data, approximately 57.34% of the global population lived in urban areas in 2023[3]World Bank, "Share of the world's population living in urban or rural areas from 1960 to 2023", data.worldbank.org. This trend is pressuring traditional leather manufacturers to diversify into alternative materials, which could accelerate the commoditization of conventional leather products. In Europe, where sustainability and animal welfare are top priorities, conventional leather products face growing challenges. To remain competitive, manufacturers must implement comprehensive sustainability strategies that address material sourcing, production processes, and end-of-life considerations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Men's Market Leadership

In 2024, men account for 60.24% of the market share, emphasizing leather jackets' strong association with masculine fashion and motorcycle culture. This dominance is attributed to male consumers' higher spending on premium outerwear and their preference for durable goods with extended replacement cycles. Leather jackets are widely regarded as versatile and timeless, offering both practicality and style across professional and casual settings. For instance, LVMH's fashion and leather goods division, which contributed 78% of the conglomerate's profits in 2024, highlights the significant growth potential and profitability of the male-focused luxury leather market.

The children's wear segment is the fastest-growing demographic, with a projected CAGR of 7.8% through 2030. This growth is driven by evolving parental preferences for stylish, durable outerwear for children and a rising willingness to invest in premium-quality clothing. The trend toward premiumization in children's apparel is unlocking opportunities for large-scale production while emphasizing the importance of adhering to strict safety standards and offering customized sizing, which differentiate children's products from adult offerings.

By Material: Conventional Leather Dominance

In 2024, conventional leather holds a dominant 81.23% market share, including materials such as bovine, sheepskin, and goatskin. These materials benefit from well-established supply chains and strong consumer familiarity, showcasing leather's durability, comfort, and traditional aesthetics, qualities that synthetic alternatives often fail to replicate consistently. This segment's strength is supported by mature processing technologies and stringent quality standards. However, it faces growing regulatory challenges, particularly from environmental compliance requirements. For example, the Environmental Protection Agency's chrome-tanning regulations, which limit total chromium discharge to a daily maximum of 12 mg/l, have pushed conventional leather processors to adopt cleaner production technologies while maintaining high material quality. Additionally, the rising demand for sustainable practices has further pressured the segment to innovate while adhering to environmental standards.

Synthetic and vegan alternatives are experiencing the fastest growth, with a 9.2% CAGR projected through 2030. This growth is driven by increasing environmental awareness, concerns about animal welfare, and advancements in material performance technologies. Innovations in bio-based materials and recycled synthetics are enabling these alternatives to closely replicate the characteristics of traditional leather while addressing sustainability demands. For instance, Evolved by Nature's Activated Silk L1 finishing system represents a significant technological breakthrough, allowing synthetic alternatives to compete on quality while eliminating harmful chemicals associated with traditional leather processing. Furthermore, the segment benefits from reliable supply availability, potentially lower production costs compared to conventional leather, and growing consumer preference for eco-friendly products, particularly among younger, environmentally conscious demographics.

By Price Range: Mass Market Leadership

In 2024, mass market products hold a 57.48% share, highlighting the transformation of leather jackets from exclusive luxury items to widely embraced fashion staples, now appealing to a broader consumer base. This market dominance is fueled by advancements in manufacturing processes and supply chain optimization, which enable competitive pricing while maintaining acceptable quality standards. Moreover, the segment capitalizes on economies of scale in production and extensive retail distribution networks, ensuring broad product availability across diverse geographic regions.

In contrast, the premium and luxury segments are set to experience significant growth, with a projected 7.1% CAGR through 2030. This growth is driven by affluent consumers seeking unique, high-quality products and artisanal craftsmanship that justify premium pricing. The growing polarization of consumer preferences toward either value or premium offerings exerts competitive pressure on middle-market segments. The premium segment benefits from higher profit margins and strong brand loyalty, while luxury brands leverage their pricing power to shield themselves from fluctuations in commodity costs. For example, Prada's acquisition of a 10% stake in the Italian leather group Rino Mastrotto in June 2025 demonstrates luxury brands' strategic focus on ensuring quality control and securing their supply chains, further reinforcing their premium pricing strategies.

By Distribution Channel: Online Platform Leadership

In 2024, online channels hold a 45.26% share of the market, highlighting the ongoing digital transformation and consumers' increasing preference for convenience, variety, and competitive pricing in fashion retail. This dominance is driven by e-commerce platforms' ability to provide niche brands with global exposure, offer extensive product catalogs, and deliver personalized shopping experiences, advantages that traditional retail struggles to match economically. The shift in consumer shopping behavior, particularly among younger demographics who are comfortable with digital purchasing, further reinforces this trend. Additionally, these platforms enable direct-to-consumer relationships, eliminating traditional retail markups. In Europe, the digital transformation of the leather accessories market further accelerates the growth of online channels, as consumers increasingly prioritize transparency in supply chain practices and product authenticity.

Offline channels, however, demonstrate notable resilience, with a projected 8.5% CAGR through 2030. This growth is attributed to experiential retail strategies and the tactile nature of leather products, which often require physical evaluation before purchase. Strategic investments in enhancing in-store experiences and integrating omnichannel approaches combining the convenience of digital platforms with the tangible interaction of physical stores play a crucial role. This is particularly significant for premium and custom leather jacket purchases. Consumers' desire for immediate gratification and access to expert guidance not only justifies premium pricing but also fosters long-term loyalty. Supporting this offline retail growth, the Leather Working Group, which represents over 2,000 industry stakeholders, provides certification standards that ensure quality assurance and traceability, enhancing customer confidence during in-store purchases.

Geography Analysis

In 2024, North America leads the market with a 32.46% share, buoyed by its deep-rooted fashion culture, a strong presence of premium brands, and robust consumer spending. This dominance underscores the cultural importance of leather jackets in American fashion, bolstered by heritage brands that set global style trends. A well-established retail infrastructure, combined with consumers' willingness to embrace premium pricing, fortifies the region's market leadership. Furthermore, efficient supply chains guarantee product availability across various price segments. North America's edge is amplified by its closeness to major fashion hubs and the sway of celebrity endorsements, which accelerate global trend adoption.

Asia-Pacific is on a rapid ascent, projected to grow at a 9.6% CAGR through 2030. This surge is driven by rising disposable incomes, a burgeoning middle class, and a heightened awareness of fashion. Urbanization and a shift towards western fashion preferences, especially among the youth in major cities, fuel this growth. Countries like China and India, with their robust manufacturing capabilities, not only cater to domestic demands but also bolster export production. The region's vast diversity paves the way for tailored product development and pricing strategies, catering to distinct consumer tastes and economic landscapes.

Europe stands as a seasoned market, where premium positioning and sustainability take center stage. Here, luxury brands and artisanal manufacturers hold sway, thanks to a strong emphasis on quality, craftsmanship, and environmental stewardship. Such values not only justify premium pricing but also carve out unique brand identities. Moreover, the European Union's stringent regulations on deforestation and environmental standards set benchmarks that resonate globally. Coupled with a consumer base that prioritizes traceability and sustainability, these factors bolster Europe's premium positioning strategies.

Competitive Landscape

The leather jackets market is highly fragmented, with a wide range of international, regional, and local players competing across different price segments. Some of the key players in the market include LVMH Moët Hennessy Louis Vuitton SE, Kering S.A. (Gucci, Saint Laurent), Industria de Diseño Textil, S.A. (Inditex), Burberry Group plc, and H&M Group. These players include luxury fashion houses, fast-fashion retailers, and independent designers, each catering to specific consumer needs and preferences. This competitive environment fosters innovation in design, material sourcing, and sustainable practices.

Furthermore, the fragmented nature of the market creates opportunities for niche brands to differentiate themselves through personalized offerings and ethical manufacturing processes. Leading players are increasingly focusing on strategic consolidation to achieve vertical integration and enhance supply chain control. For instance, Prada acquired a 10% stake in Italian leather group Rino Mastrotto in June 2025, showcasing the efforts of luxury brands to secure premium-quality materials and strengthen their manufacturing capabilities.

Similarly, Gucci's complete acquisition of Colonna Group tannery demonstrates its vertical integration strategy aimed at ensuring consistent quality and reliable supply chains. These developments highlight the growing importance of supply chain management and material quality as competitive advantages, especially as sustainability regulations become stricter and consumers demand more transparency and ethical practices.

Leather Jackets Industry Leaders

-

LVMH Moët Hennessy Louis Vuitton SE

-

Kering S.A. (Gucci, Saint Laurent)

-

Industria de Diseño Textil, S.A (Inditex)

-

Burberry Group plc

-

H&M Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Urban Leather Jackets has expanded into the UK market with the launch of a dedicated website, offering a curated collection of men's leather jackets that blend style, durability, and comfort. According to the brand, its new range includes classic bombers and bold biker jackets designed for both urban environments and open-road adventures, appealing to fashion-conscious consumers seeking versatile outerwear.

- May 2025: Royal Enfield has launched the Phoenix Leather Jacket as part of its new urban outerwear collection, offering city riders a blend of style and advanced protection. According to the brand, the new Phoenix is crafted from 100% genuine leather, features CE Class “AA” certification, Safe Tech CE Level 2 protection for the back, shoulders, and elbows, titanium sliders, reflective elements, and mesh panels for breathability and flexibility.

- April 2025: AllSaints has continued its United Kingdom expansion by introducing two new stores: one at London’s St Pancras station, marking its second location in a major rail hub, and another at the Meadowhall shopping centre in Sheffield, which replaces and upgrades its previous store there. The St Pancras store features the brand’s signature urban aesthetic and brings AllSaints’ total London locations to ten, while the new Meadowhall shop offers a brighter, more premium space with an expanded product range, including iconic leather jackets and biker boots.

- January 2025: Inessa Maksutova has launched the “More Love” premium leather jacket collection, with each piece crafted from ethically sourced, high-quality Italian leather for exceptional comfort, durability, and sophistication. According to the brand, the new collection features a range of styles from classic to contemporary silhouettes, ensuring a tailored fit and luxurious feel.

Global Leather Jackets Market Report Scope

| Men |

| Women |

| Kids |

| Online |

| Offline |

| Conventional |

| Synthetic/Vegan |

| Mass |

| Premium/Luxury |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By End User | Men | |

| Women | ||

| Kids | ||

| By Distribution Channel | Online | |

| Offline | ||

| By Material | Conventional | |

| Synthetic/Vegan | ||

| By Price Range | Mass | |

| Premium/Luxury | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the leather jacket market?

The leather jacket market stands at USD 37.23 billion in 2025 and is set to reach USD 46.28 billion by 2030 at a 4.45% CAGR

Which region is growing the fastest for leather jackets?

Asia-Pacific is the fastest-advancing region with a projected 9.6% CAGR through 2030, powered by rising urban incomes and fashion awareness

Which distribution channel leads leather jacket sales today?

Online platforms hold a 45.26% share of global sales thanks to broad product variety and convenient returns

What material is gaining traction as an alternative to conventional leather?

Synthetic/vegan materials are expanding at a 9.2% CAGR by leveraging lower environmental footprints and improving aesthetics

Page last updated on: