Backpack Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 23.12 Billion |

| Market Size (2031) | USD 31.96 Billion |

| Growth Rate (2026 - 2031) | 6.69% CAGR |

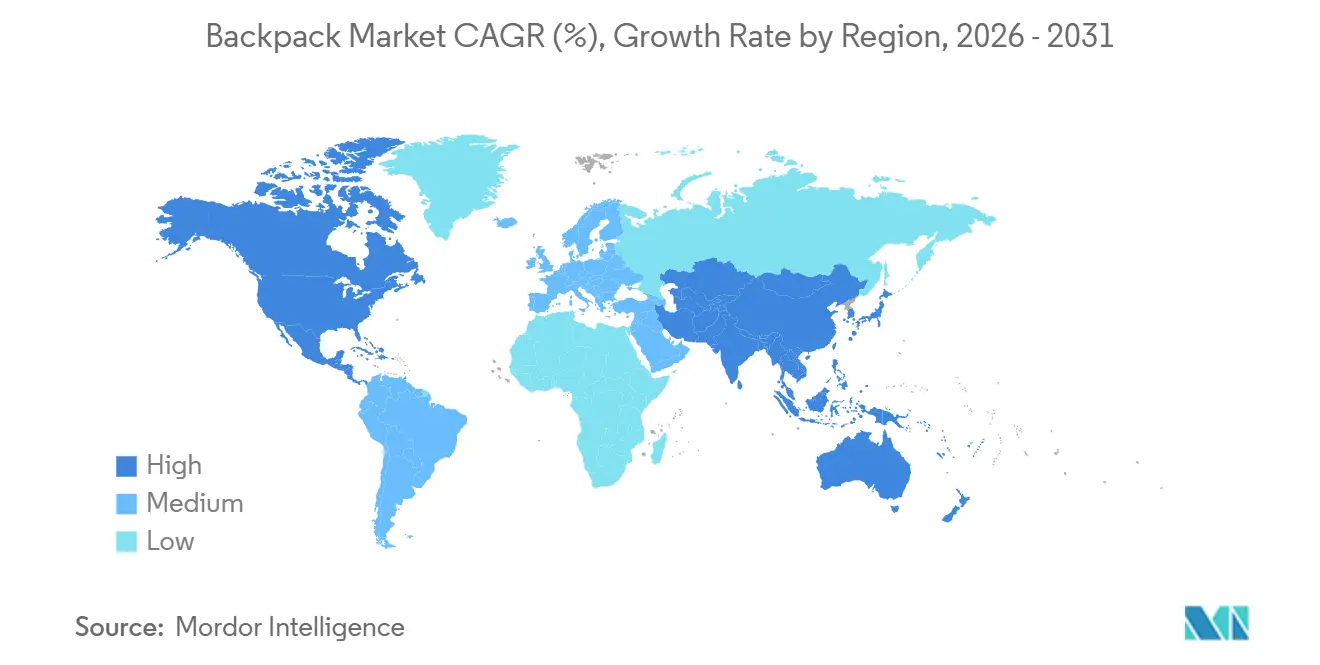

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

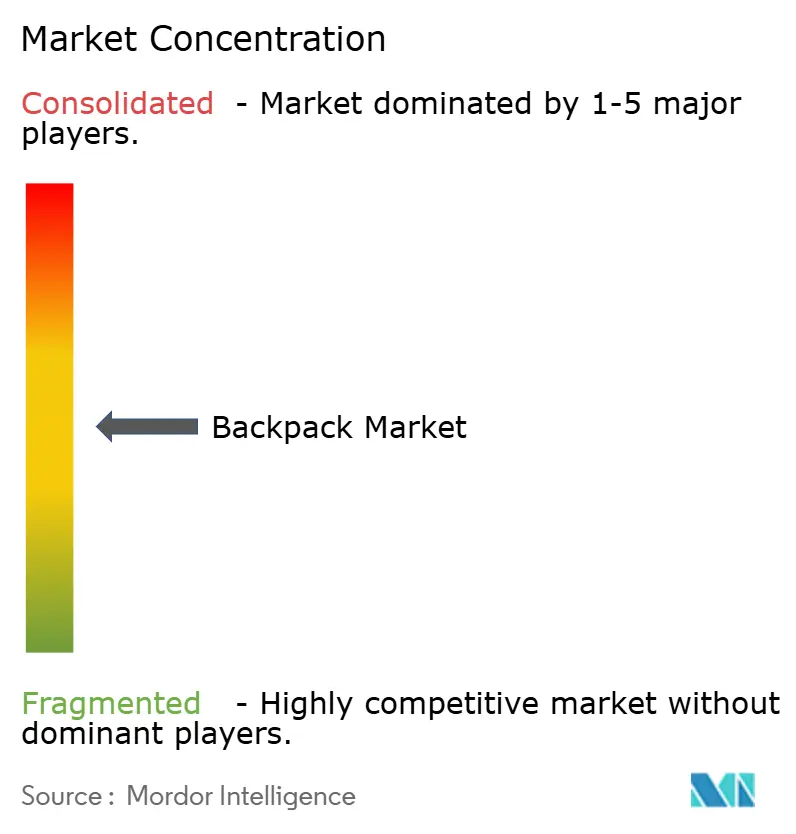

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Backpack Market Analysis by Mordor Intelligence

The Backpack Market size is expected to increase from USD 21.74 billion in 2025 to USD 23.12 billion in 2026 and reach USD 31.96 billion by 2031, growing at a CAGR of 6.69% over 2026-2031. This growth is driven by three primary factors: the resurgence of outdoor recreation in 2025, which boosted technical pack sales; sustainability initiatives from governments and major retailers promoting circular-economy designs; and the expansion of direct-to-consumer e-commerce, which has increased the global presence of niche brands. Athletic-inspired designs dominated revenue in 2025, but casual packs are rapidly gaining popularity due to the shift in urban mobility trends, as hybrid work encourages shorter city trips instead of gym-to-office commutes. The Asia-Pacific region leads in both production and consumption, while North America faces challenges from counterfeit products that undermine brand value. Premium models priced above USD 150 are capturing a growing market share, as features like solar panels, biometric locks, and modular inserts enable brands to sustain margins despite fluctuations in nylon prices and rising tariff expenses.

Key Report Takeaways

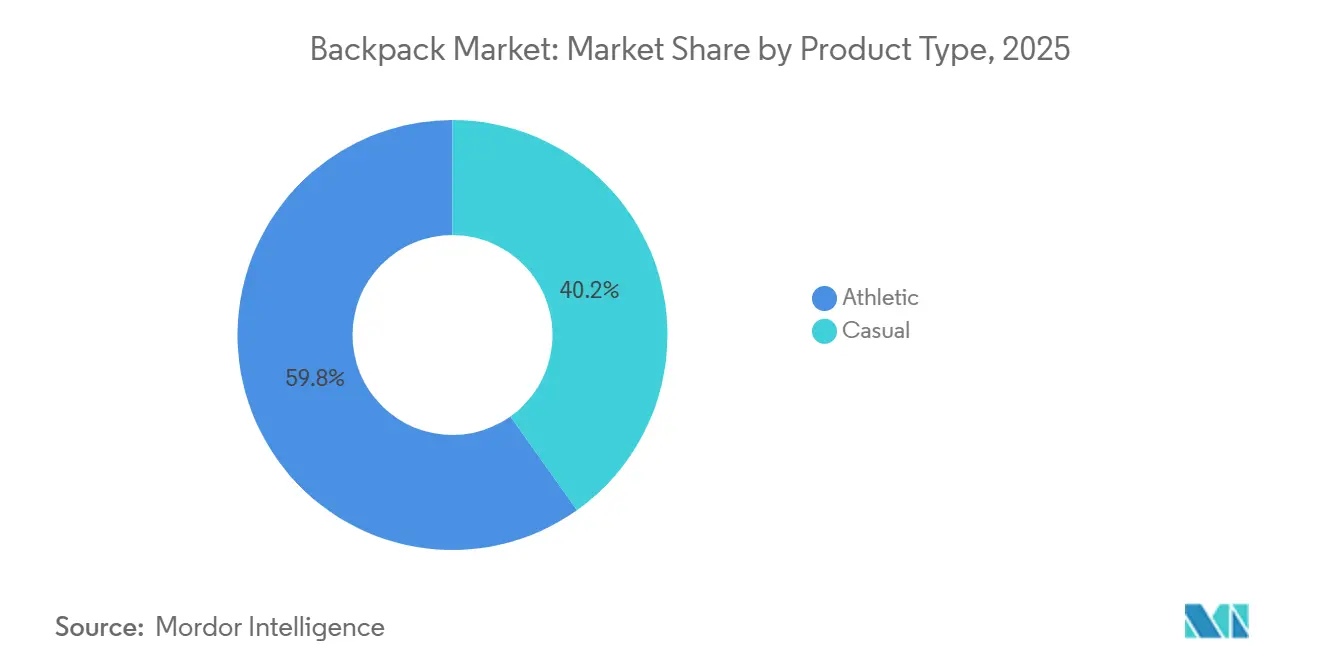

- By product type, athletic backpacks held 59.84% of 2025 revenue, while casual variants are projected to advance at an 8.96% CAGR through 2031.

- By price point, economy lines captured 55.02% backpack market share in 2025; premium models above USD 150 are forecast to expand at a 9.15% CAGR through 2031.

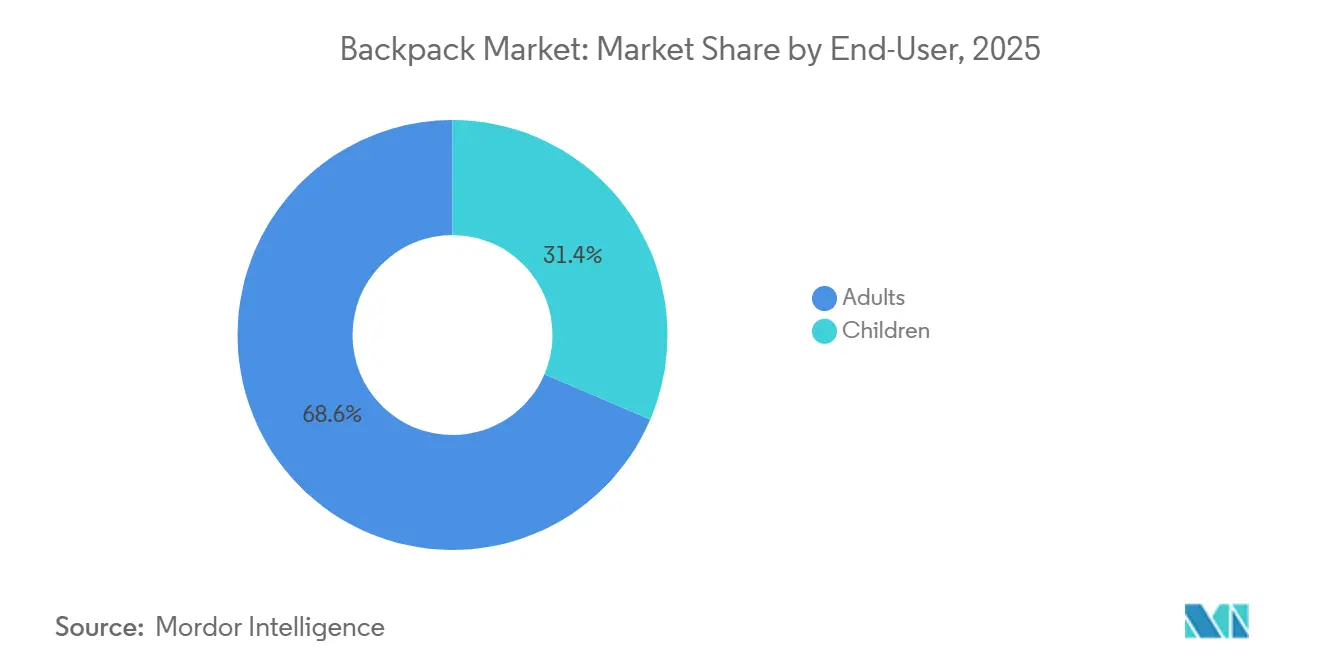

- By end-user, adults accounted for 68.56% of 2025 sales, yet children’s packs are set to grow at a 9.57% CAGR to 2031 as ergonomic standards tighten.

- By distribution channel, offline retail stores commanded 64.97% of 2025 turnover, whereas online outlets are poised for a 9.47% CAGR through 2031.

- By geography, Asia-Pacific generated 38.48% of the 2025 value and is forecast to climb at 9.68% CAGR, outpacing every other region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Backpack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in outdoor recreation and adventure tourism | +1.2% | North America, Europe, Asia-Pacific (China, India, Australia) | Medium term (2-4 years) |

| Sustainability-driven material innovation | +0.9% | Global, with early adoption in Europe and North America | Long term (≥ 4 years) |

| Urbanization and working population growth | +1.5% | Asia-Pacific core (China, India, Indonesia), spill-over to Middle East | Long term (≥ 4 years) |

| Athleisure-inspired fashion influence | +0.8% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Demand for multifunctional and smart backpacks | +1.1% | North America, Europe, affluent Asia-Pacific metros | Medium term (2-4 years) |

| Lightweight and ergonomic product innovation | +0.7% | Global, regulatory push in Asia-Pacific (Thailand, Japan) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in outdoor recreation and adventure tourism

In 2024, the Outdoor Industry Association recorded a 4.1% rise in outdoor participation, reaching an all-time high of 175.8 million participants, or 57.3% of Americans aged six and older[1]Source: Outdoor Industry Association, "2024 Outdoor Participation Trends Report", outdoorindustry.org. This growth has significantly driven the demand for backpacks. Trail-specific backpacks, featuring hydration compatibility, load-bearing frames, and weather-resistant materials, are priced 20-30% higher than standard urban daypacks. Osprey Packs' collaborations with Houdini on the Allt backpack and Carryology on the Archeon 30 illustrate a growing trend: brands are jointly developing specialized products for multi-day trekkers, focusing on circular design and modular attachment systems. The expansion of adventure tourism in the Asia-Pacific region, supported by China's government-backed five-year plans for outdoor sports infrastructure, has created a mutually reinforcing cycle: improved trail access increases backpack sales, which in turn fund research and development for lighter and more durable materials. The shift from occasional weekend users to committed year-round enthusiasts has shortened product replacement cycles. Increased usage accelerates wear on components such as zippers, buckles, and waterproof membranes, driving aftermarket and warranty-related revenue streams.

Sustainability-driven material innovation

Brands are integrating circular-economy principles into their product designs to stay ahead of regulatory requirements and attract environmentally conscious consumers. FREITAG's Mono backpack, made from mono-material nylon, supports complete mechanical recycling without requiring chemical breakdown. This approach addresses the industry's previous reliance on mixed-fiber composites, which often end up in landfills. VAUDE, in partnership with Covestro, has implemented thermoplastic polyurethane lamination, which eliminates harmful perfluorinated compounds and reduces water usage by 40% during production. Cotopaxi's Allpa and Del Día collections use repurposed deadstock fabrics, turning supply-chain waste into unique SKUs that appeal to Gen Z consumers, who frequently verify sustainability claims through third-party certifications. Deuter plans to incorporate recycled polyester into 90% of its 2025 lineup, showcasing how established brands can adopt eco-materials without compromising durability or color retention. Although these eco-innovations increase factory-level costs by 15-20%, brands recover these expenses through premium pricing and reduced risk from future carbon-border adjustments. This is particularly relevant as the EU's Carbon Border Adjustment Mechanism prepares to extend its textile coverage after 2026.

Urbanization and working population growth

In 2024, the World Bank reported that 64% of the population in East Asia and the Pacific lived in urban areas[2]Source: World Bank, Urban population (% of total population) - East Asia and Pacific, worldbank.org. These urban residents are increasingly concentrated in megacities, often facing daily commutes exceeding 90 minutes. Their dependence on multimodal transportation, such as subways, bike shares, and walking, emphasizes the need for versatile carry solutions. This demographic shift has driven a growing demand for backpacks. Features like padded laptop sleeves, RFID-blocking pockets, and quick-access compartments cater to the modern urban lifestyle, allowing seamless transitions between office, gym, and errands. In 2025, Samsonite's India segment achieved USD 210 million in revenue. To strengthen its position in both domestic and export markets, the company's Nashik facility expanded its capacity to produce 700,000 units per month. The rise of flexible work arrangements has unexpectedly supported backpack sales. Hybrid employees, who alternate between home, co-working spaces, and client meetings, prefer backpacks that adapt effortlessly to different settings. Similar trends are observed in Indonesia and Vietnam, where motorcycle commuting drives demand for backpacks with reinforced straps and reflective panels to meet informal safety requirements. Urbanization is also fueling premiumization, as city dwellers increasingly allocate discretionary income to bags that reflect professional status. This is evident in the market, with Peak Design's X-Pac backpack priced at USD 259 and NOMANZ's DIRAC Dyneema model retailing for USD 439.

Athleisure-inspired fashion influence

Backpack designs are evolving as brands combine athletic and casual aesthetics. Inspired by performance sportswear, they incorporate features like breathable mesh panels, compression straps, and ergonomic contouring into everyday designs. Nike is set to make an impact with its February 2026 relaunch of All Conditions Gear. By opening a flagship store in Beijing and showcasing Team USA kits during the Olympics, Nike is merging technical outdoor gear with lifestyle fashion, bridging the gap between trail and street. Similarly, Adidas is addressing the needs of modern athletes with its Combat Sports USA National Line 2-in-1 Backpack/Duffle, priced at USD 89.77. This adaptable bag includes stowable shoulder straps and a ventilated shoe garage, catering to athletes who require hybrid functionality for tournaments and travel. The rise in SKU proliferation is evident as brands release seasonal colorways and limited-edition collaborations. For example, VF Corporation's Eastpak has expanded through marketplace partnerships, offering exclusive prints that change quarterly. Athleisure's influence extends beyond aesthetics to materials. Moisture-wicking fabrics and antimicrobial treatments, once limited to gym bags, are now common in commuter packs, particularly in humid climates where odor control is essential. Additionally, premium features are becoming more accessible. Mid-tier brands are adopting the sleek minimalism and monochrome palettes once associated with luxury labels, increasing competition by narrowing the price-to-feature ratio.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit and low-quality products | -0.6% | Global, concentrated in North America and Europe enforcement zones | Short term (≤ 2 years) |

| Market saturation in developed economies | -0.4% | North America, Western Europe | Long term (≥ 4 years) |

| Volatility in high-performance textile prices | -0.5% | Global, acute in nylon-dependent premium segment | Short term (≤ 2 years) |

| Import tariffs on technical components | -0.8% | North America (Section 301/122), Europe (post-Brexit adjustments) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit and low-quality products

In fiscal 2024, U.S. Customs and Border Protection reported the seizure of 32 million counterfeit items, according to the U.S. Chamber of Commerce[3]Source: U.S. Chamber of Commerce, "Shop Smart", uschamber.com. In the UK, authorities conducted coordinated raids, confiscating over 800 counterfeit items and emphasizing the global scale of intellectual property violations. These counterfeit goods, priced 50-70% lower than authentic products, undermine legitimate brands. Additionally, they are made from inferior materials, failing safety tests for flammability, strap tensile strength, and zipper durability. The U.S. Trade Representative's Notorious Markets List identifies online platforms and physical markets in Southeast Asia and Eastern Europe as ongoing infringement hotspots. To combat this, brands are adopting blockchain-based authentication tags and serialized QR codes, enabling consumers to verify product authenticity. Counterfeits not only affect sales but also damage brand equity. For example, when a fake North Face pack deteriorates within three months, it negatively impacts consumer perceptions of the genuine product. Enforcement efforts remain uneven: developed markets invest in advanced customs technology and cross-border collaboration, while emerging economies often lack the resources to inspect high-volume e-commerce shipments. This imbalance creates opportunities for counterfeiters to route goods through regions with weaker controls.

Market saturation in developed economies

As household backpack ownership approaches saturation, North America and Western Europe are experiencing slower unit growth. Enhanced product quality is extending lifespans, leading to longer replacement cycles. For example, a premium backpack purchased in 2020 with a lifetime warranty remains usable through 2026, delaying repurchase. To address this saturation, brands are diversifying their SKUs by launching specialized packs for activities like cycling, photography, and travel, focusing on increasing wallet share among existing customers rather than acquiring new ones. Furthermore, the shift from ownership to rental models, driven by programs such as REI Co-op and Patagonia's Worn Wear, is reducing demand for new units as consumers opt to rent gear for specific trips. Demographic trends are adding to the saturation challenge. Declining birth rates in countries like Germany, Japan, and South Korea are shrinking the school-age population, which is a key driver of children's backpack sales. In response, brands are expanding into adjacent categories, such as rebranding diaper bags as "parenting backpacks" and designing laptop sleeves to fit larger 17-inch devices. However, these efforts are resulting in only marginal volume growth. Premiumization is offering some relief, as brands upsell existing customers to higher-margin smart or sustainable options. However, this strategy is concentrating revenue among affluent consumers while ceding mass-market share to low-cost imports.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Casual Variants Accelerate Despite Athletic Dominance

In 2025, athletic backpacks accounted for 59.84% of the market revenue, driven by trends in sports participation and their gym-to-office versatility. However, as remote work becomes more prevalent and consumers shift their focus to everyday aesthetics over performance, casual models are expected to grow at an 8.96% CAGR through 2031. Athletic backpacks, featuring moisture-wicking fabrics, ventilated back panels, and compression straps, appeal to fitness enthusiasts and commuters who cycle or jog to work. These features have maintained demand for athletic packs, even as gym memberships stabilize. Brands are leveraging the athleisure trend, evident in Nike's ACG relaunch and Adidas' innovative 2-in-1 convertible designs in their Combat Sports line, to blur product categories and attract cross-category purchases. However, athletic packs' dependence on synthetic performance textiles makes them susceptible to nylon price fluctuations, which can compress margins during feedstock cost spikes. In contrast, casual backpacks, often made with cotton-canvas blends and recycled polyester, offer cost stability and sustainability credentials that strongly appeal to urban millennials and Gen Z consumers.

The growth of the casual segment reflects changing mobility patterns. While hybrid work has reduced daily commutes, it has increased spontaneous trips, such as visits to coffee shops, co-working spaces, or running errands. These activities favor minimalist designs over the bulkier profiles of athletic packs. Brands like Herschel Supply Co. and Fjällräven's Kånken exemplify this trend, offering clean lines and heritage branding that seamlessly transition between professional and leisure contexts. The casual segment also benefits from lower barriers to entry. With simpler construction and fewer technical components, agile brands can introduce seasonal collections without significant research and development investments. This flexibility intensifies competition and accelerates style turnover. In contrast, athletic packs require extensive biomechanical testing, load-distribution engineering, and performance validation. These requirements create a competitive moat for established players like Osprey and Deuter but limit the speed of SKU turnover. The casual segment's rapid fashion cycles align well with e-commerce trends, where visual differentiation and influencer endorsements drive impulse purchases. On the other hand, athletic buyers are more deliberate, conducting thorough research and prioritizing functional specifications over aesthetics.

By Price Point: Premium Surge Challenges Economy's Volume Base

In 2025, economy-tier backpacks accounted for 55.02% of the market share, targeting price-sensitive students, budget travelers, and bulk institutional buyers. On the other hand, premium models priced above USD 150 are expected to grow at a 9.15% CAGR through 2031. This growth is driven by brands incorporating smart features and sustainable materials, which validate the higher price points. Economy packs, made with polyester fabrics and injection-molded plastic hardware, achieve retail prices below USD 50. They dominate the mass-market in Asia-Pacific and Latin America, where limited disposable incomes restrict discretionary spending. Brands such as Samsonite's American Tourister and Kamiliant lead this tier, leveraging the Nashik facility's 700,000-unit monthly output to outperform regional competitors. However, economy packs operate on thin margins, typically 8-12% at wholesale, leaving minimal room to absorb tariffs or material cost inflation. This forces brands to focus on volume-driven profitability rather than per-unit returns. Mid-range packs, priced between USD 50 and 150, offer a balance of features and affordability. However, they face challenges from both ends: premium brands are launching entry-level lines to attract aspirational buyers, while economy players are introducing superficial upgrades, like faux-leather accents and extra pockets, to justify slight price increases.

Premium backpacks, with gross margins of 40-50%, feature innovations such as solar panels, biometric locks, and modular compartments. These additions appeal to tech-savvy professionals and affluent outdoor enthusiasts. Buyers in the premium segment prioritize durability and warranty coverage, viewing backpacks as long-term investments rather than disposable items. This approach not only sustains aftermarket revenue through repairs and component replacements but also reinforces the brand's focus on quality. By adopting direct-to-consumer channels, brands retain full margins, bypassing wholesale markups. The resulting savings are reinvested into enhancing customer experience, offering benefits like free lifetime repairs, personalized monogramming, and carbon-offset shipping. The premium segment is experiencing accelerated growth in North America and Europe, where consumers are increasingly attentive to supply-chain ethics and carbon footprints. Brands that transparently share third-party sustainability audits and material traceability reports are gaining consumer trust. Notably, the premium segment has demonstrated resilience during economic downturns. Sales remained stable in 2024-2025, even amid inflationary pressures, underscoring the segment's ability to withstand cyclical demand shocks. Affluent buyers, it appears, continue to prioritize quality over price.

By End-User: Children's Segment Gains on Ergonomic Mandates

In 2025, adult backpacks represented 68.56% of the market revenue, driven by the commuting, travel, and recreational needs of working-age populations. However, children's backpacks are projected to grow at a 9.57% CAGR through 2031, supported by stricter ergonomic regulations and parents' growing focus on health-certified designs. Adult backpacks serve a wide range of purposes, including carrying laptops, gym gear, and weekend essentials. This versatility enables brands to segment their products by occasion and price, with offerings ranging from USD 30 daypacks to high-end USD 400 expedition models. Buyers who prioritize quality tend to use their backpacks for 5-7 years, which, while beneficial for the segment, limits unit sales in saturated markets like North America and Western Europe. To address this, brands are launching specialized SKUs, such as photography backpacks with padded dividers and cycling packs with helmet attachments, to encourage additional purchases from existing customers. Additionally, adult buyers are increasingly adopting smart backpacks. Professionals, in particular, value features like integrated USB charging, RFID-blocking pockets, and TSA-compliant laptop sleeves, which streamline airport security processes and daily activities.

Children's backpacks are experiencing growth due to two key factors: rising school enrollments in the Asia-Pacific and Africa regions, and increased regulatory focus on backpack weight relative to a child's body mass. The American Academy of Pediatrics recommends that a child's backpack should weigh no more than 10-15% of their body weight. This regulatory environment creates compliance challenges, favoring established brands with biomechanics testing capabilities. Furthermore, Polish research linking backpack weight to BMI percentiles has influenced EU-wide discussions on standardized load limits. These discussions could lead to formalized ergonomic requirements, potentially excluding non-compliant imports. In response, brands are developing backpacks with ultra-lightweight materials, such as 70-denier ripstop instead of the standard 210-denier, and incorporating load-distribution features like padded shoulder straps and adjustable sternum clips. Unlike adult backpacks, children's backpacks have shorter replacement cycles. Annual growth spurts and changing style preferences prompt parents to purchase new backpacks frequently, ensuring consistent revenue. The strongest growth for children's backpacks is concentrated in India, Indonesia, and Sub-Saharan Africa, where a growing middle class prioritizes education and invests in high-quality school supplies. In contrast, developed markets see slower growth, primarily driven by demographic trends and a shift toward premium products.

By Distribution Channel: Online Retail Narrows Offline's Lead

In 2025, offline retail stores commanded a dominant 64.97% share of the distribution landscape. This stronghold was bolstered by mono-brand flagships, multi-brand sporting goods chains, and department stores, all of which provided tactile product trials and immediate fulfillment. However, online channels are poised for a robust ascent, projected to grow at a 9.47% CAGR through 2031. This surge is attributed to deepening e-commerce penetration and the maturation of direct-to-consumer models. The steadfastness of offline retail can be attributed to the fit-sensitive nature of backpacks. Consumers often test adjustments like shoulder straps, back-panel contours, and weight distribution before making a purchase. Additionally, knowledgeable sales staff play a pivotal role, guiding selections for specialized uses, be it mountaineering or photography. Mono-brand stores, such as those operated by Samsonite, The North Face, and Patagonia, offer immersive brand experiences and premium services. These elements not only justify their higher price points but also enhance customer loyalty. On the other hand, multi-brand retailers like REI and Decathlon curate diverse assortments and provide price-matching guarantees, effectively attracting comparison shoppers. Yet, offline channels grapple with fixed costs—rent, labor, and inventory. These expenses can significantly compress margins, especially in bustling urban locales where lease rates are on the rise. To counteract the online competition, there's a noticeable shift towards experiential retail. Initiatives like in-store repair workshops and customization stations aim to set physical stores apart. However, these enhancements come with their own challenges: they demand capital investment and skilled labor, resources that many regional chains find hard to come by.

Platforms owned by companies, such as Nike.com and Patagonia.com, not only capture the full margins but also gather invaluable first-party customer data. This data empowers them to offer personalized recommendations and loyalty programs, significantly boosting repeat purchases. Meanwhile, third-party marketplaces like Amazon and Zalando, while providing an expansive reach and robust logistics infrastructure, come at a cost. They typically extract commissions ranging from 15-25% and impose limitations on brand control concerning pricing and product presentation. Eastpak, a brand under VF Corporation, has adeptly navigated this landscape. By collaborating with marketplaces to introduce rotating exclusive colorways and limited editions, they've harnessed the platforms' traffic while ensuring brand differentiation. A significant shift looms on the horizon: the August 2025 de minimis repeal. This change is set to redefine the contours of cross-border e-commerce. With tariffs now imposed on low-value shipments, international sellers face a choice: establish domestic warehouses or forge partnerships with fulfillment providers. While this raises entry barriers for smaller brands, logistics behemoths like Amazon stand to gain, effortlessly absorbing compliance costs at scale. The online retail surge is also a testament to the dominance of mobile commerce. With over 60% of e-commerce transactions occurring on smartphones, brands are racing to optimize checkout flows. Many are even integrating augmented-reality tools, allowing users to visualize pack dimensions right in their homes.

Geography Analysis

Asia-Pacific accounted for 38.48% of the revenue in 2025 and is expected to drive the backpack market with a 9.68% CAGR through 2031. In China, urban professionals increasingly prefer laptop-ready designs. Meanwhile, India utilizes a Samsonite plant producing 700,000 units monthly to address rising domestic and export demands. Motorcycle commuting in Indonesia and Vietnam is boosting demand for specialized products like weatherproof and reflective packs. Despite challenges such as exchange-rate fluctuations and intensified promotions impacting VF Corporation’s Q2 2026 APAC sales, multinational companies continue to reinvest. The advantages of cost-efficient factories and expanding digital marketplaces outweigh short-term market softness. Additionally, government investments in trail infrastructure and sports participation programs are driving outdoor-pack adoption, contributing to the growth of the backpack market across Southeast Asia.

In North America, the backpack market is experiencing slower unit growth due to market maturity. The seizure of 32 million counterfeit items in 2024 highlights progress in enforcement, though brand-equity risks persist. The repeal of the de minimis exemption has added USD 4-6 to the landed cost of economy packs, potentially shifting price-sensitive consumers toward domestic brands. Outdoor activities remain a key driver, with 63.4 million U.S. hikers supporting technical-pack sales, but longer replacement cycles are limiting volume growth. To stay competitive in a saturated market, brands are introducing subscription-based repair and rental services.

Europe’s backpack market benefits from strong demand for premium products, driven by eco-conscious consumers in Germany, France, and the Nordic countries. EU circular-economy directives and the upcoming Carbon Border Adjustment Mechanism are increasing transparency requirements, favoring companies like FREITAG and VAUDE that already emphasize material traceability. Aging demographics are prompting a shift in product development toward ergonomic features for seniors, partially offsetting the impact of declining birth rates on children’s product volumes. While Latin America and the Middle East and Africa currently contribute a smaller share to the global backpack market, urbanization and a growing middle class could significantly increase their combined market share by 2031, provided currency volatility and import duties stabilize.

Competitive Landscape

The backpack market demonstrates moderate fragmentation, highlighting a competitive environment where established brands compete with emerging players and direct-to-consumer disruptors. Prominent companies in the market include Samsonite Group S.A., Nike, Inc., Under Armour Inc., Adidas AG, and Columbia Sportswear Company. Traditional luggage leader Samsonite IP Holdings S.àr.l. capitalizes on its brand legacy and extensive distribution network while focusing on innovation and sustainability to align with shifting consumer preferences.

Athletic brands such as Nike and Under Armour are expanding their market presence by offering performance-oriented products featuring advanced materials and ergonomic designs. Similarly, outdoor brands like Patagonia and Arc'teryx secure premium positioning by emphasizing sustainability and technical innovation. To remain competitive, key players are increasingly adopting strategies centered on partnerships and product innovation. For example, in February 2025, JanSport, the iconic backpack brand known for its "Always With You" tagline, partnered with L2 Brands, a leader in collegiate and destination apparel. This collaboration aims to enhance JanSport's presence on college campuses nationwide, with a new collection of collegiate-branded backpacks set to launch in university bookstores in July 2025.

Companies that effectively navigate diverse distribution channels while maintaining brand consistency and delivering a superior customer experience are gaining a competitive advantage. Strategic acquisitions are also reshaping the competitive landscape. For instance, Anta Sports' USD 290 million acquisition of Jack Wolfskin, finalized on May 31, 2025, expands its outdoor product offerings and creates synergies in supply chain and product development. Technology integration is emerging as a critical differentiator, with companies investing in smart features, sustainable materials, and optimized manufacturing processes. These efforts are essential in an increasingly crowded market, as consumers increasingly favor brands that deliver authentic value propositions beyond basic functionality.

Backpack Industry Leaders

-

Nike, Inc.

-

Adidas AG

-

Columbia Sportswear Company.

-

Samsonite Group S.A.

-

Under Armour, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: YETI, renowned for its premium outdoor gear, unveiled the versatile Skala hiking backpack, now available in four sizes: 32L, 40L, 50L, and 60L.

- January 2026: Pelican revealed the Aegis 25L Tactical Backpack in a limited-edition MultiCam at SHOT Show 2026. Designed for tactical enthusiasts, competitive shooters, and off-duty professionals, the Aegis 25L was produced in an ultra-limited run of only 300 units in MultiCam, offering a one-time opportunity to purchase this exclusive product.

- June 2025: PD EDC, the design team behind several hit Kickstarter campaigns, launched its most ambitious project to date: VAULT3, a modular backpack engineered for tactical missions, photographers, travelers, adventurers, and everyday creators. The project, which went live on Kickstarter, generated excitement among gear enthusiasts for its revolutionary adaptability and all-terrain durability.

- April 2025: Kemp USA launched its new Ultimate EMS Mini Backpack. This pack maintained the legendary quality and smart organization of their bestseller but in a compact, grab-and-go format. Perfect for rapid deployment in space-constrained environments, the EMS mini backpack made the perfect addition to any rapid response kit.

Global Backpack Market Report Scope

Backpacks, typically made from fabric, canvas, or nylon, are designed to be carried on the back. Secured with two shoulder straps, they often come with frames to support heavier loads. The backpack market report is segmented by product type, price point, end-user, distribution channel, and geography. By product type, the market is segmented into casual and athletic. By price point, the market is segmented into economy, mid-range, and premium. By end-user, the market is segmented into adults and children. By distribution channel, the market is segmented into offline retail stores and online retail stores. By Geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, the market forecasts are provided in terms of value (USD).

| Casual |

| Athletic |

| Economy |

| Mid-Range |

| Premium |

| Adults |

| Children |

| Offline Retail Stores | Mono Brand Stores |

| Multi-Brand Stores | |

| Others | |

| Online Retail Stores | Company Owned Platform |

| Third Party Online Retailers |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Casual | |

| Athletic | ||

| By Price Point | Economy | |

| Mid-Range | ||

| Premium | ||

| By End-User | Adults | |

| Children | ||

| By Distribution Channel | Offline Retail Stores | Mono Brand Stores |

| Multi-Brand Stores | ||

| Others | ||

| Online Retail Stores | Company Owned Platform | |

| Third Party Online Retailers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global backpack market size and forecasted growth?

The backpack market size reached USD 21.74 billion in 2025, is projected at USD 23.12 billion in 2026, and is expected to climb to USD 31.96 billion by 2031, reflecting a 6.69% CAGR.

Which region will contribute most to future backpack sales?

Asia-Pacific already holds 38.48% of revenue and is forecast to expand at 9.68% CAGR through 2031, making it the dominant growth engine.

How fast are premium backpacks growing compared with economy lines?

Premium backpacks priced above USD 150 are projected to grow at 9.15% CAGR through 2031, outpacing economy models that nonetheless remain volume leaders.

What factors are driving adoption of smart backpacks?

Demand stems from mobile professionals seeking on-the-go charging, biometric locks, and modular inserts; these features command 40-60% price premiums despite representing fewer than 10% of units today.

Page last updated on: