Children's Wear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

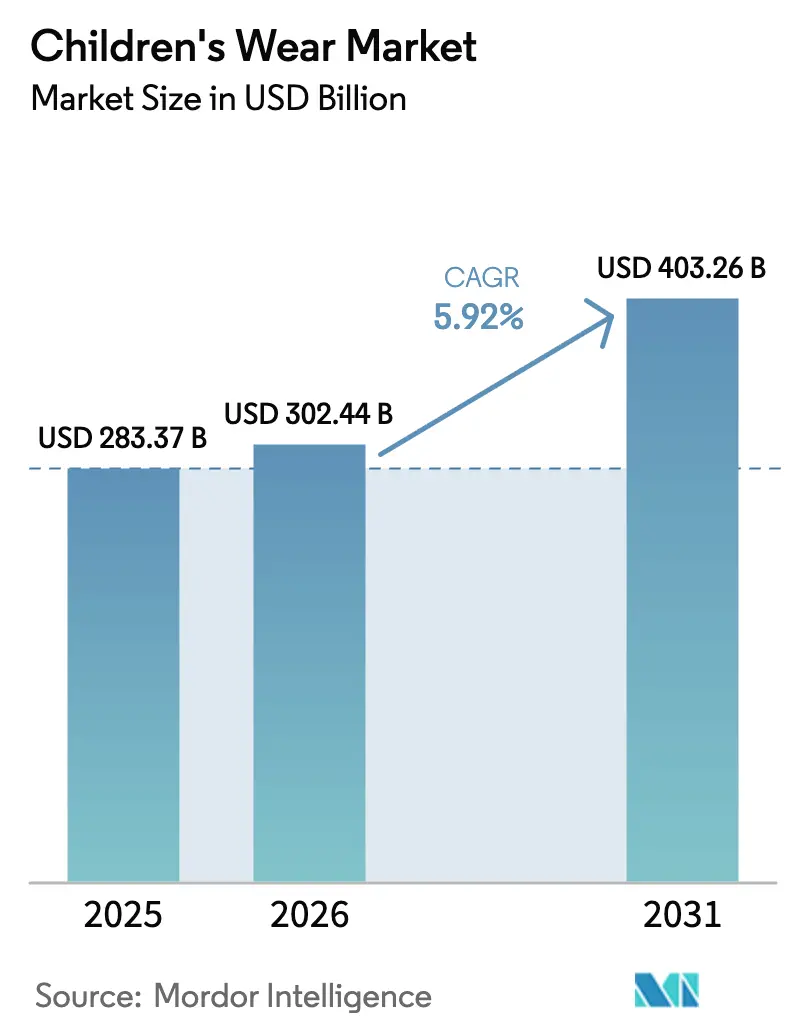

| Market Size (2026) | USD 302.44 Billion |

| Market Size (2031) | USD 403.26 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

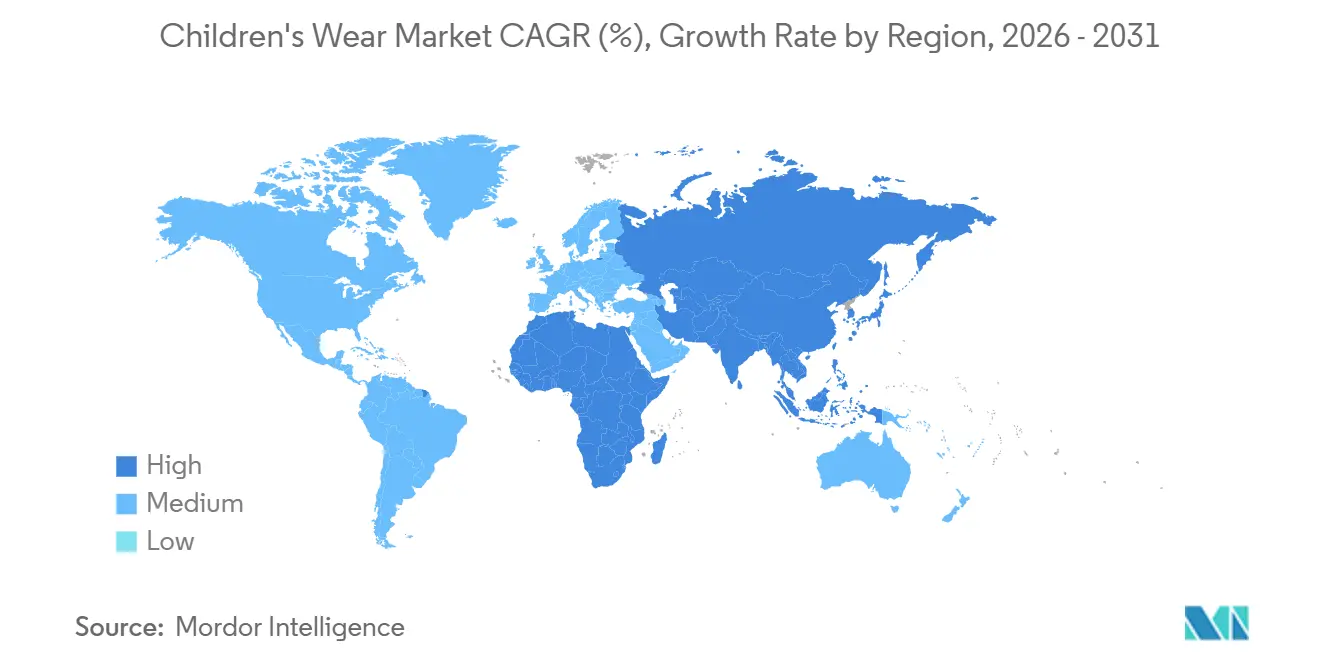

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Children's Wear Market Analysis by Mordor Intelligence

The children's wear market stands at 283.37 in 2025, to reach USD 302.44 billion in 2026 and is projected to reach USD 403.26 billion by 2031, representing a CAGR of 5.92%. Frequent replacement cycles foster inelastic demand, ensuring a steady market for products that require regular updates. Sustainability mandates are driving brands to prioritize traceability, rewarding those that align with these evolving consumer and regulatory expectations. AI-driven production models have significantly reduced lead times, compressing them from 12 weeks to just 3 weeks, enabling faster time-to-market and improved operational efficiency. Parents are increasingly moving away from disposable fast fashion, opting instead for durable garments certified by Global Organic Textile Standard (GOTS) and International Association for Research and Testing in the Field of Textile and Leather Ecology (OEKO-TEX), which ensure higher quality and adherence to environmental standards. Additionally, adaptive-fit footwear and gender-neutral collections are broadening the addressable market by catering to diverse consumer needs and preferences. While fragmented competition and low barriers to digital entry allow direct-to-consumer newcomers to scale rapidly, the European Union's Corporate Sustainability Due Diligence Directive is raising the bar for supply-chain transparency, compelling companies to adopt more stringent practices to meet regulatory requirements.

Key Report Takeaways

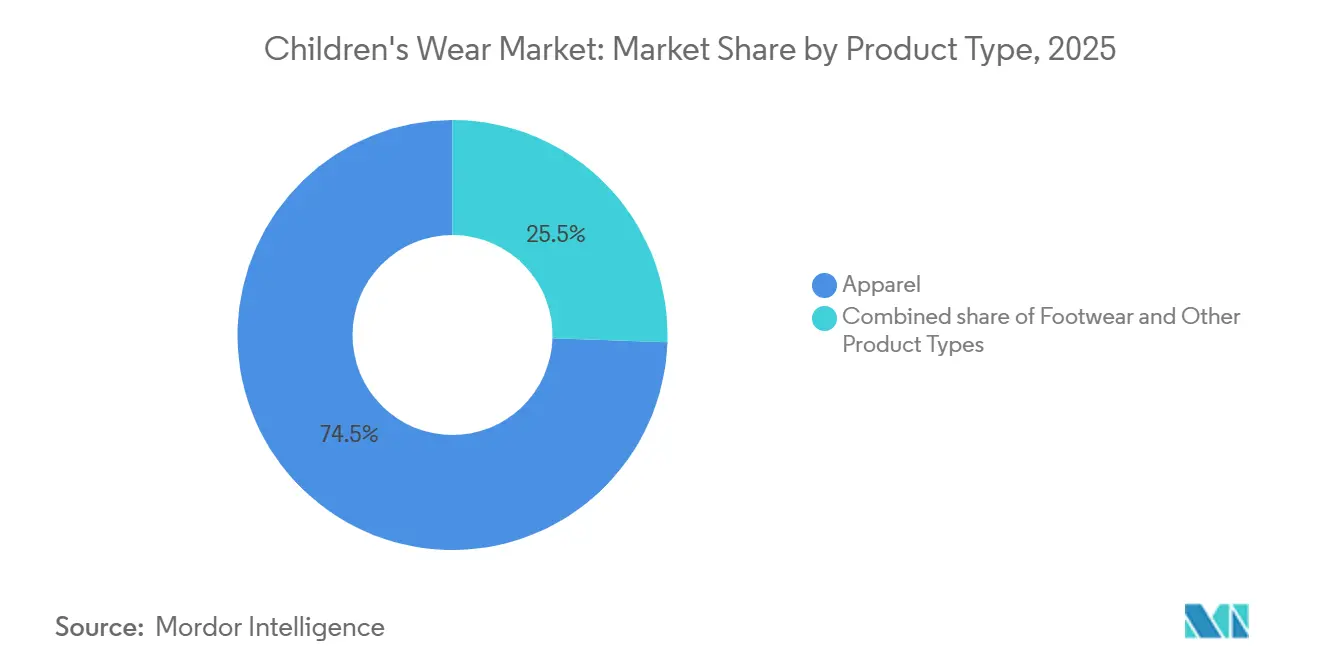

- By product type, apparel led with 74.47% of revenue in 2025 and footwear is forecast to grow at a 6.32% CAGR to 2031.

- By age group, the kids/children held 77.58% share in 2025 while the infant/toddler segment is advancing at a 6.57% CAGR to 2031.

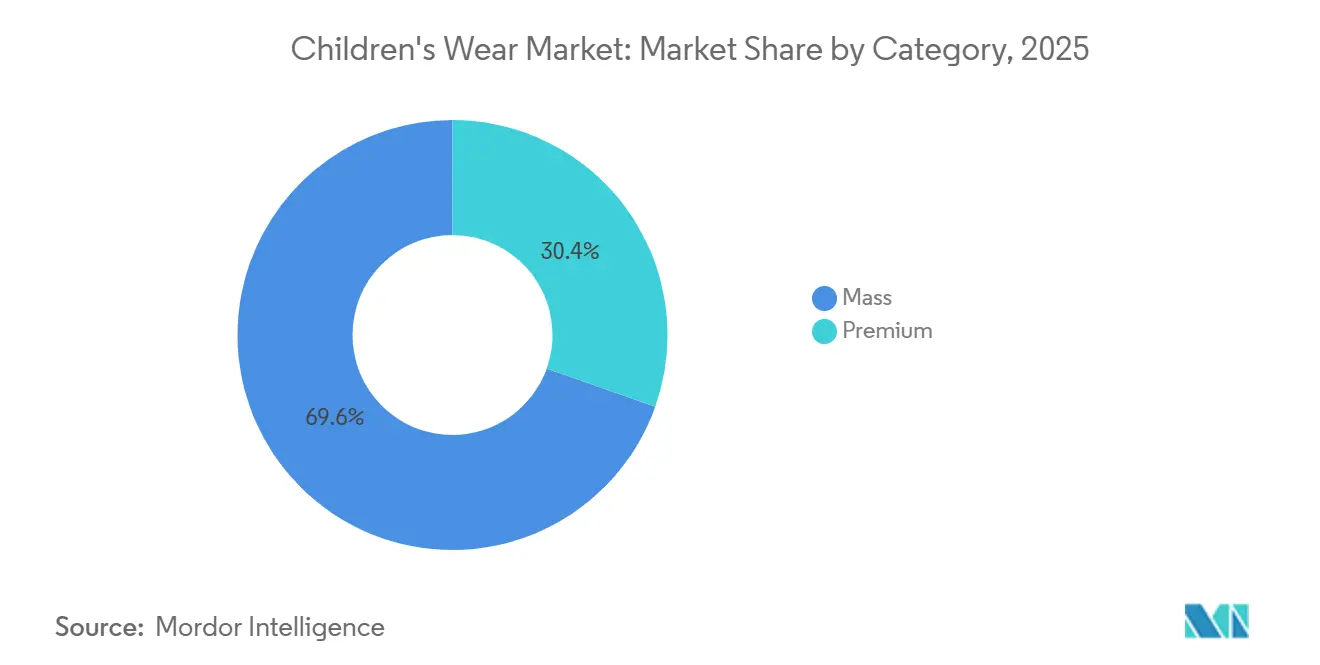

- By category, mass-market lines captured 69.58% of spending in 2025, but premium offerings are set to expand at a 6.95% CAGR through 2031.

- By distribution channel, offline stores retained 81.90% share in 2025; online sales will rise at a 7.42% CAGR through 2031.

- By geography, Asia-Pacific accounted for 40.69% of the market share in 2025 and is the fastest-growing territory at a 7.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Children's Wear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Frequent replacement cycle due to rapid growth and wear | +1.2% | Global, with higher intensity in Asia-Pacific | Short term (≤ 2 years) |

| Rising focus on quality, durability, and comfort | +0.9% | North America, Europe, premium segments in Asia-Pacific | Medium term (2-4 years) |

| Growing demand for sustainable and eco-friendly fabrics | +1.1% | Europe, North America, urban centers in Asia-Pacific | Long term (≥ 4 years) |

| Emergence of AI-driven micro-sizing and on-demand production | +0.7% | Global, led by North America and China | Medium term (2-4 years) |

| Expansion of kidswear rental, subscription, and resale ecosystems | +0.6% | Europe, North America, emerging in urban Asia-Pacific | Long term (≥ 4 years) |

| Growth of casual, gender-neutral, and adaptive apparel lines | +0.8% | North America, Europe, progressive urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Frequent replacement cycle due to rapid growth and wear

Children typically outgrow clothing every 6 to 9 months, resulting in shorter product life spans and requiring parents to frequently repurchase essentials such as T-shirts, jeans, and sneakers throughout the year. This inherent obsolescence creates a consistent demand that helps stabilize the category against economic fluctuations. However, this frequent replacement cycle also highlights the importance of durability and quality. Brands that incorporate features like reinforced knees, adjustable waistbands, and abrasion-resistant toe caps can extend product usability by 20% to 30%, reducing the overall cost of ownership and fostering customer loyalty. The emergence of "grow-with-me" designs, including extendable cuffs and modular sizing, reflects a shift from planned obsolescence toward longevity. This approach aligns with parental budget considerations and sustainability priorities. This trend is particularly evident in the Asia-Pacific region, where rising middle-class incomes and smaller family sizes encourage parents to prioritize fewer, higher-quality garments over disposable fast fashion.

Rising focus on quality, durability, and comfort

Parents are increasingly prioritizing fabrics that can endure repeated laundering, maintain shape retention, and provide moisture-wicking properties, particularly for activewear and school uniforms. Brands incorporating performance technologies such as Nike's Dri-FIT moisture management and Adidas's Primeknit seamless construction are gaining traction in the premium segment. Comfort has become an essential attribute, especially post-pandemic, as remote schooling popularized athleisure and elastic-waist joggers over traditional denim. The implementation of the United States Consumer Product Safety Commission's FY 2024 Operating Plan has introduced more stringent safety requirements for children's products, including apparel, directly impacting consumer purchasing decisions and manufacturer compliance standards[1]Source: "United States Consumer Product Safety Commission, Operating Plan FY 2024", cpsc.gov. Durability also plays a key role in resale value; garments that maintain structural integrity after 10 to 15 washes fetch higher prices on secondhand platforms like Vinted and ThredUp, reinforcing a cycle that benefits quality-focused brands. The focus on comfort extends to footwear, where features such as adjustable closures, cushioned insoles, and breathable mesh uppers are now standard in children's sneakers from brands like Puma and Under Armour.

High production costs for sustainable and safe materials

Higher costs associated with certified organic, recycled, and safety-compliant materials restrict market access, especially in price-sensitive segments and emerging markets where cost remains the primary purchasing factor. The procurement of sustainable materials requires specialized supply chains and certification processes that increase operational complexity and expenses. Additionally, safety-compliant materials must undergo rigorous testing, extending product development timelines and costs. The European Union's REACH regulations on hazardous substances in textiles, require mandatory compliance testing, which increases production costs while ensuring child safety[2]Source: "REACH Regulation ", environment.ec.europa.eu. Companies must balance sustainability initiatives with price competitiveness, particularly when competing against lower-priced alternatives that may not meet equivalent environmental or safety requirements. The price gap between traditional and sustainable materials creates market divisions where premium brands can incorporate higher material costs, while mass-market manufacturers face challenges maintaining affordable pricing, which may restrict widespread adoption of sustainable practices in the children’s wear industry.

Emergence of AI-driven micro-sizing and on-demand production

Artificial intelligence is driving advancements in hyper-personalized fit recommendations and just-in-time manufacturing, leading to shorter inventory cycles and reduced overproduction waste. Bold Metrics' body-scanning algorithms, utilized by several kidswear brands, create size profiles from smartphone photos, reducing return rates by 30% to 40%. Browzwear's 3D virtual-prototyping software enables designers to digitally iterate on patterns, cutting sample production by 50% and reducing time-to-market from 12 weeks to 3 weeks. On-demand production models, adopted by brands like Shein Kids and PatPat, use real-time sales data to initiate micro-batch runs of 100 to 500 units, thereby minimizing unsold inventory and markdown pressures. However, the high capital requirements for AI infrastructure for mid-sized brands pose challenges for smaller players, potentially driving market consolidation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly changing fashion trends and seasonality | -0.5% | Global, with higher volatility in fast-fashion hubs | Short term (≤ 2 years) |

| High production costs for sustainable and safe materials | -0.7% | Europe, North America, premium segments globally | Medium term (2-4 years) |

| Increasing regulatory scrutiny on chemical safety standards | -0.4% | Europe, North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Supply-chain traceability demands burdening SME brands | -0.3% | Global, acute for SMEs in South Asia and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapidly changing fashion trends and seasonality

The kidswear market experiences compressed trend cycles, with micro-seasons influenced by social media influencers and licensed-character collaborations that can rise and decline within 8 to 12 weeks. This volatility compels brands to maintain higher safety stock levels and accept markdowns on unsold inventory, negatively impacting gross margins. Fast-fashion companies like Shein Kids and Zara Kids address this risk with ultra-short lead times, while traditional wholesale brands, dependent on 6-month advance orders, face challenges in adapting to real-time demand signals. Seasonality further intensifies these issues, as winter outerwear and back-to-school apparel account for 40% to 50% of annual revenue within concentrated 8-week periods, creating significant cash-flow fluctuations that strain working capital. The emergence of year-round capsule collections and seasonless basics such as layering tees and versatile joggers, provides a partial solution. However, this approach requires brands to shift consumer behavior from impulse-driven trend purchases to wardrobe-building strategies.

High production costs for sustainable and safe materials

Organic cotton, recycled polyester, and non-toxic dyes command higher cost premiums over conventional inputs, compressing margins unless brands can pass increases to consumers or achieve scale efficiencies. Global Organic Textile Standard (GOTS)-certified organic cotton trads at higher, compared to conventional lint. Chemical-safety compliance such as eliminating azo dyes, phthalates, and formaldehyde, requires third-party testing , adding to landed costs for small and mid-sized brands. The EU's REACH regulation restricts over 2,000 substances, and China's GB 31701 standard mandates pH-neutral finishes for infant garments, necessitating reformulation investments that can exceed USD 1 million for diversified product lines European Chemicals Agency. Brands that vertically integrate or form buying consortia can negotiate volume discounts on sustainable materials, but Small and Medium Enterprises (SMEs) lacking scale face a structural cost disadvantage that limits their ability to compete on price while maintaining quality and compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Footwear Outpaces Apparel on Innovation

In 2025, apparel accounted for 74.47% of the market share, driven by everyday essentials such as T-shirts, jeans, and school uniforms, which benefit from frequent replacement cycles. Within the apparel segment, casualwear and athleisure are growing faster than formalwear, influenced by the rise of remote learning and hybrid schooling, which emphasize comfort over traditional dress codes. H&M Kids reported a 25% increase in jogger and hoodie stock-keeping units (SKUs) in 2025, reflecting this trend. Additionally, gender-neutral clothing lines are gaining popularity, with brands like Primary.com and Tootsa MacGinty offering unisex basics that simplify inventory management and appeal to progressive households.

Conversely, footwear is expected to grow at a compound annual growth rate (CAGR) of 6.32% from 2026 to 2031, surpassing the category average. This growth is attributed to the rapid adoption of adaptive-fit technologies and sustainable materials. Footwear brands are increasingly incorporating recycled rubber outsoles and bio-based foams. For instance, Puma's RE:SUEDE sneaker, designed for industrial composting, highlights circular-design principles that appeal to eco-conscious parents.

By Age Group: Infant Safety Standards Drive Toddler Growth

The Kids/Children segment, covering ages 2 to 14 years, accounted for 77.58% of the market share in 2025. This dominance is attributed to the longer wear period, higher unit consumption, and a wider range of product offerings compared to the Infant/Toddler segment. The Kids/Children segment's larger market share is due to its broader age range, which includes preschoolers, elementary students, and pre-teens, each with unique style preferences and activity requirements. Growth in this segment is further supported by increasing participation in organized sports and extracurricular activities. According to the National Sporting Goods Association, nearly all youth team sports (ages 7-17) saw increased participation in 2024 compared to their three-year averages. Flag football led with a 21% increase, followed by basketball and tackle football, each growing by 12%[3]Source: "NSGA Annual Sports Participation Study Shows Encouraging Youth Team Sports Growth", nsga.org.

However, the Infant/Toddler cohort, comprising children under 2 years, is projected to grow at a CAGR of 6.57% from 2026 to 2031. This growth is driven by increased parental emphasis on chemical-free fabrics and adherence to stringent safety regulations. Products such as organic cotton bodysuits and GOTS-certified sleep sacks, are witnessing year-over-year sales growth as millennial and Gen-Z parents prioritize health and sustainability. While the Infant/Toddler segment has a smaller base, its faster growth rate highlights opportunities for brands focusing on organic materials, safety certifications, and gifting-oriented packaging.

By Category: Premium Segment Captures Aspirational Spend

Mass-market offerings accounted for 69.58% of revenue in 2025, driven by value-conscious families purchasing everyday basics from retailers like H&M, Zara, and Target. The mass-market segment's dominance reflects its accessibility, wide distribution through hypermarkets and e-commerce, and rapid trend responsiveness. Fast-fashion players like Shein Kids and Zara Kids leverage 2- to 3-week lead times to capitalize on viral social-media trends, offering licensed-character collaborations and influencer-endorsed styles at price points 50% to 70% below premium competitors. However, the mass segment faces margin pressure from rising input costs and markdown intensity.

The premium segment is set to grow at 6.95% CAGR from 2026 to 2031, as rising household incomes in Asia-Pacific and Latin America enable trading up to heritage brands that signal quality, durability, and resale value. The segment's growth is also fueled by the secondhand market; premium garments retain 40% to 60% of original value on resale platforms like Vinted and The RealReal, making the initial investment more palatable, as noted by Vogue Business.

By Distribution Channel: Online Gains Share Through Personalization

Brick-and-mortar stores accounted for 81.90% of the market share in 2025, driven by parents' preference to assess fabric quality and fit in person. These stores provide a tactile shopping experience that online platforms cannot replicate, making them a preferred choice for many consumers. In India, retailers such as FirstCry continue to expand into tier-2 cities, where in-store shopping remains a common practice due to its convenience and trust factor. Physical retail also encourages impulse purchases of accessories, supports instant exchanges, and fosters customer loyalty through personalized service.

Online sales are expected to grow at a CAGR of 7.42%, supported by augmented reality (AR) try-on tools and artificial intelligence (AI) size guidance, which help reduce return rates and enhance the online shopping experience. The buy-online-pick-up-in-store model now constitutes 22% of Nike’s North American digital orders, combining the convenience of online shopping with the immediacy of in-store pickup. Subscription rental services, such as Bundlee, distribute wardrobe costs through monthly fees, offering an affordable alternative to outright purchases. These services also appeal to sustainability-conscious parents by promoting the reuse of clothing and reducing waste.

Geography Analysis

Asia-Pacific accounted for 40.69% of the global market share in 2025 and is projected to grow at a CAGR of 7.92% from 2026 to 2031, the fastest growth rate among all regions. China's live-streaming commerce ecosystem, driven by platforms like Douyin and Tmall, facilitates real-time product demonstrations and flash sales. In India, the expansion of organized retail, led by brands such as FirstCry and Gini, and Jony, is penetrating tier-2 cities like Pune, Jaipur, and Coimbatore. Rising household incomes and nuclear families are driving demand for branded kidswear. Japan's aging population supports premium kidswear sales, as grandparents allocate discretionary spending to grandchildren. In Southeast Asia, markets like Indonesia, Thailand, and Vietnam are experiencing rapid e-commerce adoption.

Europe and North America markets are together driven by premiumization and sustainability mandates. The EU's Corporate Sustainability Due Diligence Directive, effective from 2027, requires brands to disclose supply-chain labor practices and environmental impacts. Germany, the United Kingdom, and France lead in organic cotton adoption, with GOTS-certified garments accounting growing market shares in 2025. In North America, the United States market is consolidating around omnichannel leaders such as Target, Walmart, and Amazon, which leverage scale to negotiate favorable supplier terms. In Canada, bilingual labeling requirements and demand for insulated outerwear create niche opportunities for brands like Canada Goose Kids and Helly Hansen Junior. Mexico's proximity to United States manufacturing and its role in nearshoring supply chains position it as a cost-effective sourcing hub.

In South America, Brazil's large youth population and a growing middle class support steady demand, though economic volatility constrains purchasing power. In Argentina, inflation challenges have shifted consumer preferences toward durable, multi-season garments. Chile's stable economy and high urbanization rate support organized retail expansion. In the Middle East, the United Arab Emirates and Saudi Arabia exhibit high per-capita spending on kidswear, driven by young populations and elevated disposable incomes. Turkey acts as a bridge between Europe and Asia, with domestic brands exporting to neighboring markets. In Africa, South Africa's formal retail sector is the most developed, while Nigeria and Egypt present growth opportunities as urbanization and internet penetration increase.

Competitive Landscape

The children's apparel and footwear market is significantly fragmentated, with no single player holding more than a major global market share. This structure is driven by regional brand preferences, varied price segments, and low barriers to entry, particularly for digital-native disruptors. Established players such as Nike, Adidas, H&M, and Inditex compete by leveraging global supply chains and omnichannel distribution networks to achieve cost efficiencies and respond quickly to emerging trends. Traditional wholesale-centric models face increasing margin pressures from direct-to-consumer brands like PatPat and Shein Kids. These entrants bypass intermediary markups and utilize AI-driven demand forecasting to reduce overproduction.

Additionally, rental and resale platforms such as Bundlee, The Little Loop, and Circos are introducing a new competitive dimension by focusing on product longevity rather than unit sales, appealing to sustainability-conscious parents. Opportunities remain in underdeveloped segments such as adaptive apparel, gender-neutral lines, and on-demand micro-sizing, where mainstream brands have been slow to invest despite rising consumer interest. Technology is becoming a critical factor in gaining a competitive edge. Brands adopting tools like Bold Metrics' body-scanning algorithms or Browzwear's 3D virtual prototyping can reduce design-to-market cycles from 12 weeks to just 3 weeks. This minimizes inventory risks and supports test-and-learn approaches for trend validation. Nike, for instance, holds over 1,200 active patents related to adaptive closures, sustainable materials, and performance fabrics, creating barriers to imitation as documented by the United States Patent and Trademark Office (USPTO).

Smaller players are leveraging regulatory arbitrage by manufacturing in countries like Bangladesh and Vietnam, benefiting from lower labor costs. However, these brands face increasing scrutiny under the EU's due-diligence directive, which requires supply-chain audits and living-wage verification. The market's fragmented nature suggests potential for consolidation, with well-capitalized incumbents likely to acquire digital-native brands to gain access to customer data and agile operating models. Meanwhile, niche players achieving certifications such as Global Organic Textile Standard (GOTS) and International Association for Research and Testing in the Field of Textile and Leather Ecology (OEKO-TEX), can command premium pricing and differentiate themselves from commoditized offerings.

Children's Wear Industry Leaders

-

Carter's Inc.

-

Gap Inc.

-

Nike, Inc.

-

Adidas AG

-

Hennes & Mauritz AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Paragon, a prominent Indian footwear retailer introduced FreshFeet, a new line of children's shoes incorporating its proprietary Dual Fit Tech technology. This technology is claimed to be designed to adapt to the growing feet of children through adjustable fit mechanisms. The innovation addresses a significant challenge in the children's footwear market providing shoes that accommodate rapid foot growth, reducing the need for frequent replacements and offering improved value and sustainability.

- April 2025: Rag & Bon launched viral sweatpants jeans for kids, featuring their Miramar line that is claimed to be made from ultra-soft, breathable cotton terry fabric with hyper-realistic denim prints. According to the brand, these kid-friendly styles, including joggers and wide-leg pants, offer the comfort of loungewear with the appearance of denim, making them ideal for playdates and family outings.

- March 2025: Vogue Williams launched the Gen kidswear brand on M&S and Next digital platforms, offering a unisex collection for ages 2-8 that emphasizes versatility, durability, and timeless design with bold colors and fun prints.

- March 2025: Reebok launched a playful Sesame Street sneaker collection for kids, featuring five unique styles inspired by beloved characters like Elmo, Cookie Monster, Abby Cadabby, and Big Bird, with prices ranging from USD 50 to USD 60. According to the brand, the collection includes vibrant designs such as the Club C Revenge and Classic Nylon Elmo, blending comfort, educational elements, and whimsical details like character badges and themed sock liners.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the childrenswear market as all new clothing and footwear items purpose-designed for infants, toddlers, and children up to 14 years, quoted in retail value terms at the first point of sale to the consumer. Fabric, styling, and safety features appropriate for play, rest, and school life are included, which allows Mordor Intelligence to capture mass and premium price tiers across apparel and footwear.

Scope Exclusion: School uniforms supplied through institutional tenders and performance team sports kits sold under licensing contracts are excluded.

Segmentation Overview

-

By Product Type

- Apparel

- Footwear

- Other Product Types

-

By Age Group

- Infant/Toddler

- Kids/Children

-

By Category

- Mass

- Premium

-

By Distribution Channel

- Offline Stores

- Online Stores

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Nigeria

- Egypt

- Morocco

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Desk Research

We begin with wide-ranging desk work. Public datasets such as UN Comtrade shipment codes for HS 61-62, UNICEF live-birth statistics, WTO Consumer Price reports, and national household expenditure surveys give foundational volume and spend baselines. Trade association briefs from the American Apparel & Footwear Association, EU Kids Fashion Federation, and China National Garment Association enrich material mix and channel split insights. Company 10-Ks, IPO filings, and D&B Hoovers snapshots clarify brand revenues, while news flows on Dow Jones Factiva help trace pricing actions. These sources, among many others, provide the scaffold before deeper validation.

Primary Research

Mordor analysts conduct layered interviews with fabric mills, branded childrenswear buyers, regional distributors, and large online platforms across Asia-Pacific, North America, Europe, and the GCC. Short surveys with parents and store managers further test size curves, average selling prices, and return rates, helping us close data gaps that pure desk work cannot cover.

Market-Sizing & Forecasting

A top-down build draws total retail spend for 0-14 year olds from household surveys, then splits it by penetration rates for apparel and footwear, which are then adjusted for channel mark-ups. Select bottom-up checks, supplier roll-ups, and sampled ASP × units from leading chains anchor the totals. Key variables include annual live births, disposable income per child, cotton and synthetic fiber price indices, online channel share, and fashion cycle frequency. We forecast through multivariate regression that links these drivers to historical spend, followed by scenario analysis for currency moves and inflation. Where supplier data are sparse, our team interpolates using comparable markets and variance caps discussed with interviewees.

Data Validation & Update Cycle

Outputs pass three reviews: automated anomaly flags, peer analyst sense checks, and a senior consultant sign-off. We align figures with independent signals such as customs import tallies and birth cohort sizes before release. The dataset refreshes every twelve months, with interim revisions if material events, such as currency shocks, tariff changes, or major recalls, occur; clients therefore receive an up-to-date viewpoint.

Why Mordor's Children's Wear Market Baseline Commands Reliability Today

Published estimates often diverge because firms vary in product scope, price conversion points, and update cadence.

Key gap drivers in childrenswear stem from whether footwear is counted, how far the age band stretches into teen years, the treatment of currency inflation, and the frequency at which e-commerce mark-ups are refreshed.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 284.68 B (2025) | Mordor Intelligence | |

| USD 250 B (2024) | Regional Consultancy A | Omits footwear and premium capsules, uses historic FX rates |

| USD 211.57 B (2024) | Global Consultancy B | Limits scope to apparel only, conservative channel margins |

| USD 324.32 B (2024) | Industry Association C | Extends age band to 17 years and folds in licensed sports kits |

These comparisons show that by selecting a clear age ceiling, excluding institutional uniforms, and triangulating both apparel and footwear values with current exchange rates, Mordor delivers a balanced, transparent baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the projected value of the children's apparel and footwear market by 2031?

The sector is expected to reach USD 403.26 billion by 2031 on a 5.92% CAGR trajectory.

Which product line is expanding fastest?

Footwear is forecast to grow at a 6.32% CAGR from 2026 to 2031 due to adaptive-fit and circular-design innovations.

Which age bracket is delivering the highest growth?

The Infant/Toddler segment is rising at a 6.57% CAGR, driven by safety regulations and organic-cotton demand.

Which region offers the fastest sales momentum?

Asia-Pacific leads with a 7.92% CAGR to 2031, propelled by China’s live-streaming commerce and India’s expanding organized retail. . . . . . . . Ne

Page last updated on: