Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

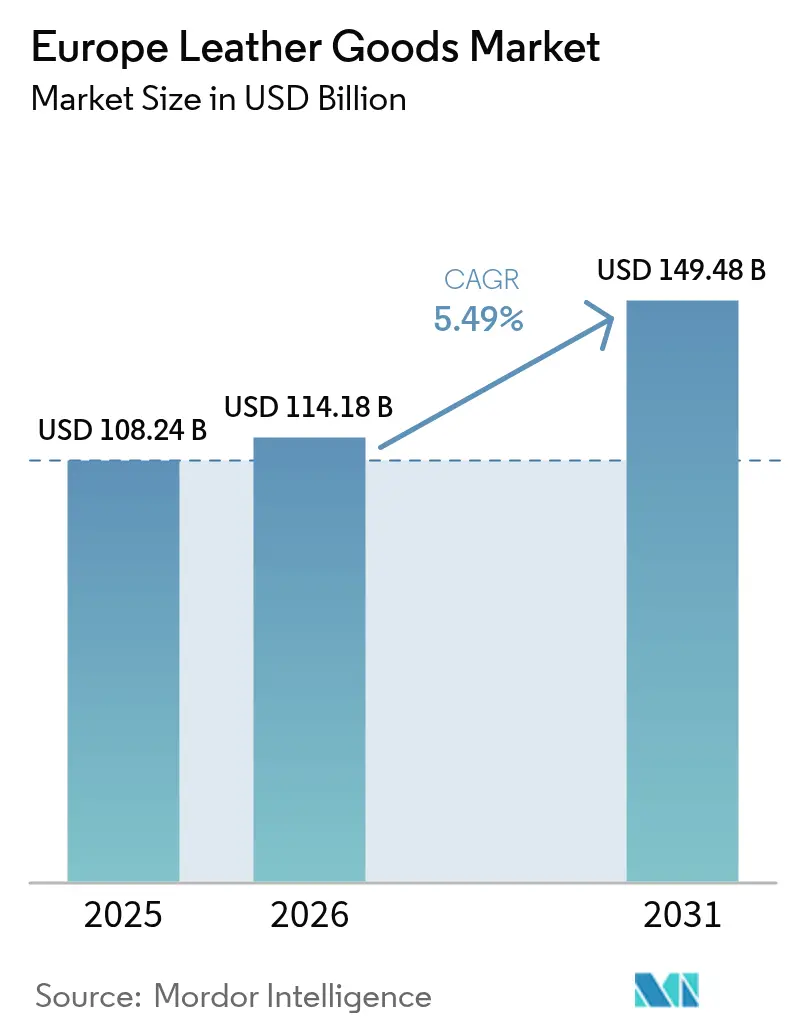

| Base Year Market Size (2025) | USD 108.24 Billion |

| Market Size (2026) | USD 114.18 Billion |

| Market Size (2031) | USD 149.48 Billion |

| Growth Rate (2026 - 2031) | 5.49% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Leather Goods Market Analysis by Mordor Intelligence

The Europe leather goods market size is expected to grow from USD 108.24 billion in 2025 to USD 114.18 billion in 2026 and is forecast to reach USD 149.48 billion by 2031 at 5.49% CAGR over 2026-2031. Sustained appetite for heritage craftsmanship, expanding premiumization among middle-income shoppers, and rising adoption of traceable, low-impact tanning technologies reinforce expansion across the Europe leather goods market. Germany’s leadership position is anchored in formidable manufacturing ecosystems and high disposable incomes, while Poland’s outperformance signals demand rotation toward Eastern Europe leather goods market opportunities. Handbags outpace footwear on growth momentum as consumers gravitate toward investment pieces that double as status symbols. Accelerating digital commerce, especially among Gen Z and millennial cohorts, reshapes the competitive field, even as flagship boutiques remain essential for luxury storytelling. Meanwhile, counterfeit suppression initiatives, ESG-linked financing for tanneries, and vertical integration strategies safeguard margins in the Europe leather goods market despite raw material volatility

Key Report Takeaways

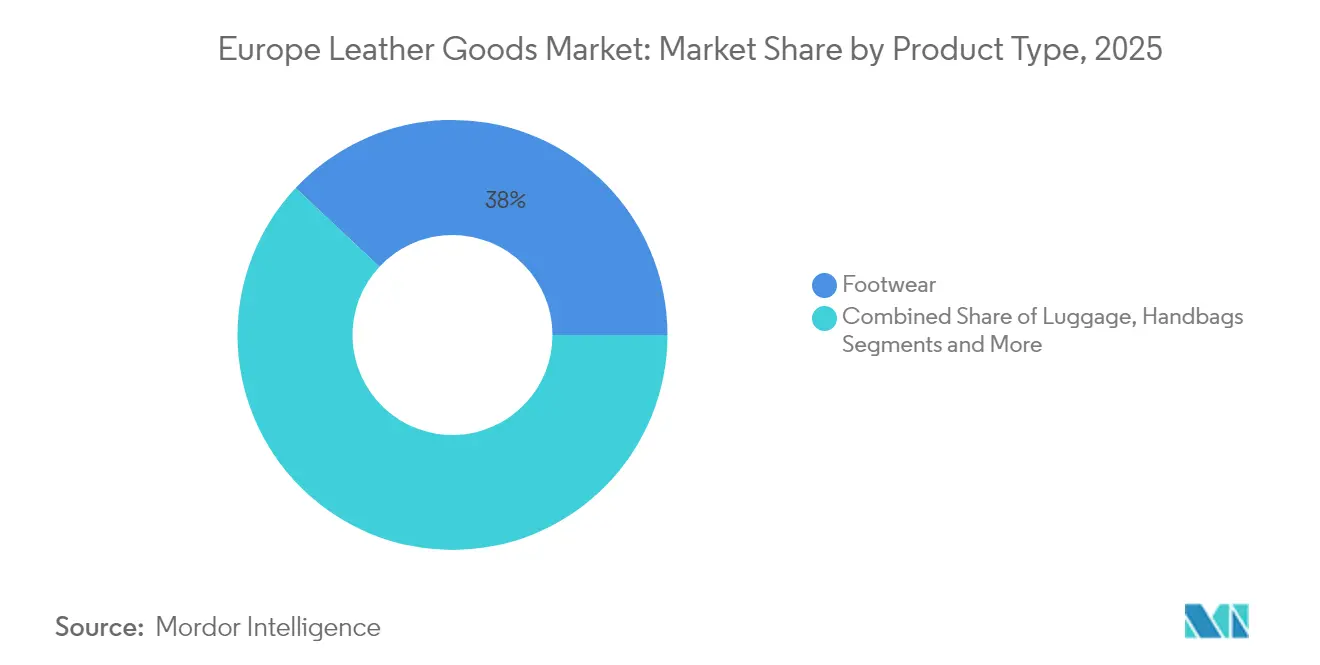

- By product type, footwear held 38.02% of Europe leather goods market share in 2025, whereas handbags are projected to log the swiftest 5.74% CAGR to 2031.

- By end user, male consumers accounted for 53.86% of Europe leather goods market share in 2025; female purchasers are set to register a faster 5.79% CAGR through 2031.

- By category, the mass segment captured 59.84% of the Europe leather goods market size in 2025, while premium offerings are on track for a 6.01% CAGR to 2031.

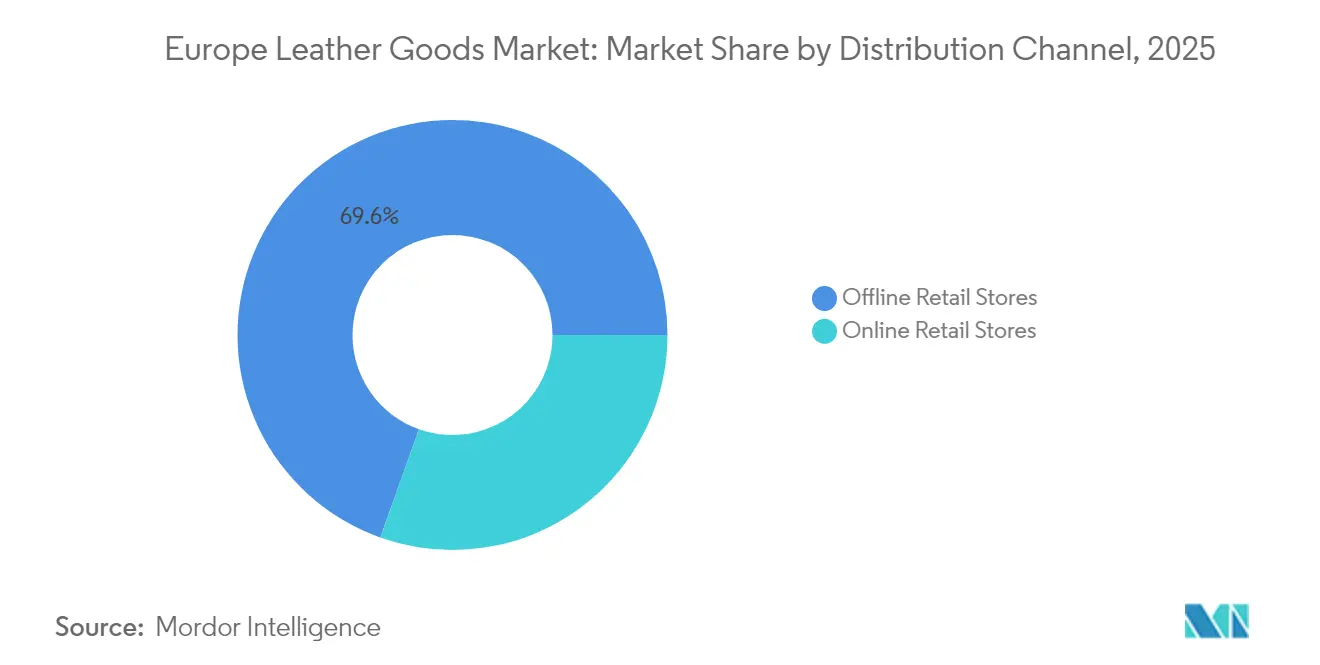

- By distribution channel, offline retail dominated with 69.55% revenue share in 2025; online channels are forecast to expand at a 6.73% CAGR by 2031.

- By geography, Germany led with 19.52% revenue share in 2025, yet Poland is poised for the highest 6.26% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Leather Goods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust growth of the luxury fashion industry | +1.2% | Western Europe, with spillover to Eastern markets | Medium term (2-4 years) |

| High consumer preference for premium, durable goods | +0.9% | Germany, France, Italy, United Kingdom | Long term (≥ 4 years) |

| Popularity of personalized and customized leather products | +0.7% | Urban centers across Europe | Short term (≤ 2 years) |

| Increasing travel and tourism fueling market growth | +0.6% | Major tourist destinations: France, Italy, Spain | Medium term (2-4 years) |

| Adoption of advanced technologies in leather processing | +0.5% | Italy, Germany, France manufacturing hubs | Long term (≥ 4 years) |

| Demand for sustainable and ethically produced leather | +0.8% | Northern Europe, with adoption across Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust growth of the luxury fashion industry

The robust growth of the luxury fashion industry serves as a critical driver for the Europe leather goods market, reinforcing demand for high-end leather accessories, footwear, and apparel. Europe, home to iconic fashion capitals like Milan, Paris, and London, boasts a luxury fashion market valued in the tens of billions of dollars, with steady year-on-year growth fueled by an expanding base of affluent consumers and increasing acceptance among younger demographics such as Millennials and Gen Z. This market growth is supported by a strong culture of craftsmanship, innovation, and brand heritage, with major luxury houses like Louis Vuitton, Gucci, and Burberry continuously launching new collections and expanding into experiential retail. The rise in disposable incomes and the cultural importance of fashion as a symbol of status further drive consumer spending on premium leather goods. Additionally, the luxury fashion sector’s focus on sustainability and exclusivity through limited editions and bespoke offerings enhances the appeal of leather accessories, creating a synergistic boost for the leather goods market across Europe.

High consumer preference for premium, durable goods

High consumer preference for premium, durable leather goods is a major growth driver in the Europe leather goods market, closely linked to the increasing influence of digital and social media marketing. A 2024 University of Portsmouth survey highlighted that 60% of consumers trust influencer recommendations, with nearly half of all purchasing decisions influenced by these endorsements [1]Source: University of Portsmouth, “New research unveils the ‘dark side’ of social media influencers and their impact on marketing and consumer behaviour,”port.ac.uk . This trend underscores how consumers place significant trust in lifestyle influencers and opinion leaders when selecting luxury leather products, emphasizing quality, craftsmanship, and brand prestige. As influencer marketing builds emotional connections and brand credibility, consumers are more inclined to invest in high-quality, long-lasting leather goods that symbolize status and personal value. This combination of premium product preference and trusted influencer guidance bolsters market demand and supports sustained growth within Europe's competitive leather goods sector.

Popularity of personalized and customized leather products

The growing popularity of personalized and customized leather products is a significant driver of the Europe leather goods market. Consumers increasingly seek unique and tailor-made leather items that reflect their individual styles and preferences, which has led brands to focus on offering customization options like monogramming, bespoke designs, and personalized hardware. This trend enhances the exclusivity and emotional connection customers have with their purchases, driving higher spending on premium products. Traditional craftsmanship, especially in key European markets such as Italy, continues to blend with modern technology to deliver these personalized offerings. Additionally, the emphasis on environmentally friendly and vegetable-tanned leather in customized products appeals to consumers who value sustainability alongside luxury, further propelling market growth.

Increasing travel and tourism fueling the market growth

Increasing travel and tourism is a significant driver fueling the growth of the Europe leather goods market. In 2024, the European Union experienced its best tourism year on record, with the total number of nights spent at tourist accommodation establishments exceeding 3 billion, marking a 2.2% increase (+65.4 million nights) compared to 2023 [2]Source: Eurostat, “EU tourism tops 3 billion nights in 2024 after strong Q4”, www.ec.europa.eu. This surge, driven largely by a strong final quarter and a notable 4.9% rise in international visitor stays, has heightened demand for high-quality travel accessories such as leather luggage, handbags, and wallets. Key tourism hubs like Spain, Italy, France, and Germany, which collectively accounted for over 61% of these overnight stays, have seen increased consumer spending on premium leather goods. Affluent travelers seek durable and stylish leather products that serve functional and luxury purposes. This tourism-driven demand, combined with rising disposable incomes and evolving fashion trends, is significantly accelerating market growth across Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in leather supply chains and raw material sourcing | -0.8% | Regional impact, particularly affecting Italian manufacturers | Short term (≤ 2 years) |

| Counterfeit products and brand dilution | -0.6% | Europe-wide, concentrated in online channels | Medium term (2-4 years) |

| Stringent government regulations on animal-derived leather | -0.4% | Europe regulatory framework, national variations | Long term (≥ 4 years) |

| Animal welfare concerns and activist opposition | -0.3% | Northern Europe, spreading across Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in leather supply chains and raw material sourcing

Volatility in leather supply chains and raw material sourcing acts as a key restraint to the growth of the Europe leather goods market, creating cost pressures and supply uncertainties for manufacturers. Fluctuations in raw hide availability, driven by livestock industry dynamics, trade restrictions, and environmental regulations, significantly impact the stability of supply and pricing. Additionally, geopolitical tensions, rising energy costs, and disruptions in global logistics further compound procurement challenges, often leading to delays in production and higher operational expenses. Growing concerns around sustainability and ethical sourcing also add complexity, as brands are increasingly required to balance consumer demand for responsible materials with the high costs and limited availability of certified sustainable leather. This volatility not only squeezes profit margins but also hinders the ability of companies to plan long-term strategies in a competitive and highly quality-sensitive market.

Counterfeit products and brand dilution

Counterfeit products and brand dilution remain a major restraint in the Europe leather goods market, eroding both brand equity and consumer trust. The rise of counterfeit handbags, footwear, and accessories, particularly through online platforms and unregulated markets, generates unfair price competition and diminishes the exclusivity that genuine leather brands depend on. Luxury and premium players are especially vulnerable, as imitation products weaken their perceived value and authenticity. According to research from the Intellectual Property Office, as of February 2024, 24% of male consumers influenced by social media endorsements are inclined to purchase counterfeit goods, compared to only 10% of female consumers [3]Source: Intellectual Property Office, "The impact of complicit social media influencers on counterfeit purchasing among male consumers in the UK," gov.uk, highlighting how digital marketing channels further fuel demand for counterfeits. This growing trend not only reduces consumer confidence in distinguishing authentic products but also exacerbates brand dilution, posing a significant challenge to sustainable market growth despite ongoing regulatory enforcement in Europe.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Footwear Dominance Faces Handbag Disruption

Footwear accounted for the largest share of the Europe leather goods market in 2025, holding 38.02% of the overall market. This dominance highlights the strong preference of European consumers for high-quality footwear that combines functionality with style. The category benefits from deeply ingrained cultural appreciation for craftsmanship, durability, and fashion-forward design. Footwear serves not only as a daily necessity but also as an important marker of personal style, especially in markets such as Italy, France, and Spain, where fashion heritage is significant. Premium and luxury footwear brands have also strengthened their market positions through expanded product lines, collaborations, and sustainability initiatives. The segment’s resilience makes it a key contributor to the overall revenue flow in the European leather goods industry, while aligning with consumers’ growing desire for products that offer both practicality and aesthetic distinction.

Handbags, on the other hand, are projected to be the fastest-growing segment in the Europe leather goods market, with a CAGR of 5.74% through 2031. This growth is primarily attributed to their position as accessible luxury items that appeal to a broad consumer base seeking both functionality and status. Unlike footwear, handbags are increasingly seen as versatile investment pieces that can be styled across multiple occasions while retaining long-term value. Rising demand for premium and designer handbags underscores a consumer shift toward products that embody luxury and identity, even among younger demographics. Moreover, the segment has significantly benefited from increasing online retail penetration, influencer-driven trends, and the popularity of entry-level luxury offerings. As consumer preferences evolve, handbags are poised to capture greater attention from brands and investors alike, cementing their role as a dynamic growth engine within the leather goods sector.

By End User: Gender Convergence Reshapes Market Dynamics

Male consumers represented the largest share of the Europe leather goods market in 2025, accounting for 53.86% of the total. This dominance is primarily driven by their traditional demand for business accessories, footwear, and luggage, categories that continue to see consistent purchases across both professional and travel-related needs. European men value durability, craftsmanship, and functionality, making them reliable customers for premium leather products. In addition, men are more likely to view leather goods such as luggage and formal shoes as long-term investments, which reinforces steady spending patterns. The corporate sector and frequent travel culture across Europe further sustain male-driven consumption, ensuring the segment’s stable revenue contribution. Even in evolving fashion trends, the male consumer base remains a cornerstone for the overall performance of the European leather goods industry.

The female consumer segment, however, is projected to be the fastest growing, expanding at a CAGR of 5.79% through 2031. Unlike the traditionally male-dominated categories, female demand spans a wider range of products, particularly handbags, wallets, and fashion-driven footwear. Women increasingly perceive leather goods as both essential accessories and lifestyle statements, fueling accelerated adoption across diverse income groups. Designer handbags and other premium accessories are emerging as aspirational purchases, supported by social media influence and global fashion trends. Younger female demographics are especially contributing to this growth, as they prioritize luxury consumption that aligns with identity, status, and self-expression. With brands introducing new collections targeted at women and emphasizing personalization, the female segment is set to reshape gender-based consumption patterns, making it a dynamic driver of market expansion in the coming years.

By Category: Premium Acceleration Challenges Mass Dominance

Mass category leather goods commanded the largest share of the Europe leather goods market in 2025, accounting for 59.84% of the total. This segment’s strength lies in its appeal to price-conscious consumers who prioritize affordability and practicality over exclusivity. Mass market products cater extensively to everyday use applications such as wallets, belts, footwear, and basic handbags, ensuring steady volume-driven demand. European consumers in this segment seek durability and accessible quality, making it an essential foundation of the wider leather goods industry. Additionally, established distribution through supermarkets, online platforms, and multi-brand stores further reinforces the segment’s widespread availability. Despite increasing interest in premium and luxury items, the mass category remains indispensable, as it supports broad-based adoption and sustains consistent revenue streams for manufacturers.

In contrast, the premium leather goods category is emerging as the fastest growing segment, anticipated to expand at a CAGR of 6.01% through 2031. This momentum reflects a clear shift in European consumer behavior toward luxury and semi-luxury purchases driven by rising disposable incomes and evolving fashion aspirations. Premium leather products, such as designer handbags, bespoke footwear, and branded accessories, are increasingly seen as symbols of status, individuality, and long-term value. Consumers are drawn to superior craftsmanship, sustainable materials, and exclusive designs that differentiate these goods from mass offerings. Social media influence and celebrity endorsements further amplify demand across younger demographics, strengthening premium positioning within the market. With such dual forces of aspiration and investment value, the premium segment is set to capture expanding market attention, shaping bifurcated demand patterns between mass adoption and elevated luxury consumption.

By Distribution Channel: Digital Transformation Accelerates Omnichannel Evolution

Offline retail stores captured the largest share of the Europe leather goods market in 2025, accounting for 69.55% of the total. This dominance is rooted in the importance of tactile product evaluation, as consumers continue to value the ability to physically inspect the quality, texture, and craftsmanship of leather items before purchase. Luxury leather goods, in particular, benefit from experiential retail environments such as flagship stores, boutiques, and department store outlets that provide personalized customer service and brand immersion. The offline channel also plays a critical role in reinforcing brand identity and sustaining exclusivity, both of which are vital in the premium and luxury segments. Moreover, in-store experiences create opportunities for upselling and cross-selling, contributing to higher average transaction values. Despite the rising prominence of e-commerce, offline retail remains the dominant distribution mode, as it aligns with consumer expectations of trust, authenticity, and engagement in the leather goods purchasing process.

The online retail channel, however, is projected to be the fastest growing segment, expanding at a CAGR of 6.73% through 2031. Growth in this space is strongly supported by enhanced digital shopping experiences that replicate aspects of in-store engagement through advanced tools such as virtual try-on technologies and 3D product visualization. Direct-to-consumer strategies adopted by leather goods brands are also reducing reliance on traditional intermediaries, enabling more competitive pricing while fostering closer customer relationships. Online platforms provide extensive product accessibility and convenience, particularly appealing to younger consumers who are highly digitally engaged. In addition, the integration of social media, influencer marketing, and seamless payment solutions has accelerated adoption and normalized luxury purchases through digital channels. As technology continues to transform customer interactions, the online channel is set to redefine market dynamics, becoming a central driver of growth and innovation in the European leather goods industry.

Geography Analysis

In 2025, Germany commands a dominant 19.52% share of the European leather goods market. This leadership is bolstered by Germany's robust manufacturing base, the high purchasing power of its consumers, and its strategic role as a distribution hub for luxury goods, catering to both Central and Eastern European markets. Germany's well-established infrastructure and advanced production technologies further enhance its competitive edge in the leather goods market. Additionally, the nation's strong automotive and business travel sectors fuel the demand for premium leather accessories, including high-quality luggage and car interiors. Furthermore, even amidst broader economic uncertainties, Germany's domestic consumption of luxury goods remains steadfast, supported by a culture that values premium craftsmanship and durability.

On the other hand, Poland is making waves as the market with the most rapid growth, boasting a 6.26% CAGR projected through 2031. This surge is attributed to Poland's swift economic advancement, rising disposable incomes, and an increasing allure of luxury brands among urbanites, who are increasingly drawn to Western lifestyle products. The growing presence of international luxury retailers in Poland's urban centers has significantly contributed to the market's expansion. Additionally, the younger demographic, with a preference for premium and branded leather goods, is driving demand. Poland's strategic location in Europe also positions it as a key market for regional distribution and trade.

France remains a key player in the European leather goods market, driven by its globally renowned luxury brands and a strong tradition of craftsmanship. The country benefits from a well-established luxury retail network and a steady influx of international tourists, which significantly contributes to the demand for high-end leather products. Italy, another major market, continues to thrive due to its reputation as a global fashion hub and its expertise in leather production. Italian leather goods are highly sought after for their quality and design, with exports playing a crucial role in the market's growth. Spain is also emerging as a notable market, supported by its growing fashion industry and increasing consumer preference for premium leather products. The country's focus on innovation and sustainability in leather manufacturing further enhances its market position.

Competitive Landscape

The European leather goods market, with a concentration score of 4, reflects a moderately fragmented competitive landscape. Established luxury conglomerates such as LVMH, Kering, and Hermès dominate the market by leveraging vertical integration strategies. These companies maintain control over the entire value chain, from raw material sourcing to retail distribution, ensuring quality and exclusivity. Alongside these leaders, mid-market players focus on niche positioning, emphasizing craftsmanship authenticity, regional heritage, and sustainable production methods. This diverse structure creates a dynamic environment where both established and emerging players compete for market share.

Technological advancements have become a critical factor in gaining a competitive edge within the market. Brands are increasingly adopting blockchain verification systems, NFC authentication chips, and AI-powered customer personalization platforms to combat counterfeiting and enhance customer engagement. Collaborative initiatives, such as the AURA Consortium, highlight the industry's collective efforts to implement blockchain-based product authentication. At the same time, individual companies are investing in proprietary anti-counterfeiting solutions to protect their brand integrity across digital and physical channels, ensuring consumer trust and loyalty.

Opportunities for growth in the European leather goods market lie in sustainable material innovation, circular economy business models, and direct-to-consumer platforms. These platforms allow brands to bypass traditional retail markups while maintaining premium positioning and delivering high-quality customer experiences. As European consumers increasingly prioritize sustainability and transparency, brands that align with these values through supply chain transparency initiatives and eco-friendly practices are well-positioned to capture market demand. This evolving landscape underscores the importance of differentiation through innovation and responsiveness to consumer preferences.

Europe Leather Goods Industry Leaders

-

Hermès International S.A.

-

Chanel SA

-

Capri Holdings Limited

-

Kering S.A.

-

LVMH Moët Hennessy Louis Vuitton SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Von Baer has launched a new UK website, vonbaer.co.uk, marking its expansion into the United Kingdom to offer premium full-grain vegetable-tanned Italian leather bags, briefcases, and accessories. The brand is known for affordable luxury, blending timeless style, sustainability, and high craftsmanship, targeting a gap in the UK market for high-end leather goods.

- April 2025: Hermès announced the opening of its 27th leather goods workshop in Colombelles, Normandy, scheduled for completion by 2028 with 260 artisan positions, representing a significant capacity expansion to meet global demand for luxury leather goods and reinforcing France's position as a premium manufacturing hub.

- August 2024: Von Baer, a renowned name in luxury leather bags and accessories, has unveiled its latest wallet collection. Crafted from Cuoio Superiore Leather, a premium and durable vegetable-tanned leather, these wallets epitomize the brand's dedication to merging sustainability with luxury.

- February 2024: Ermenegildo Zegna Group announced that it had unveiled plans for a luxury footwear and leather goods production facility in Sala Baganza (Parma). Scheduled for completion by the end of 2026, this facility was intended to boost the Group's production capacity and spotlight Italian craftsmanship.

Europe Leather Goods Market Report Scope

Leather goods are products made from tanning hides and the skin of animals, mainly from cattle. The Europe leather goods market is segmented by type, distribution channel, and geography. Based on type the market is segmented into footwear, luggage, and accessories. Based on distribution channels, the market is segmented into offline and online retail stores. Based on geography, the market is segmented into the United Kingdom, Germany, Spain, France, Italy, Russia, and the Rest of Europe. For each segment, the market sizing and forecasts have been done based on value (in USD Million).

By Product Type

| Footwear |

| Handbags |

| Luggage |

| Clothing |

| Accessories |

| Other Product Types |

By End User

| Male |

| Female |

By Category

| Mass |

| Premium |

By Distribution Channel

| Offline Retail Stores |

| Online Retail Stores |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Footwear |

| Handbags | |

| Luggage | |

| Clothing | |

| Accessories | |

| Other Product Types | |

| By End User | Male |

| Female | |

| By Category | Mass |

| Premium | |

| By Distribution Channel | Offline Retail Stores |

| Online Retail Stores | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe leather goods market in 2026?

The market is valued at USD 114.18 billion in 2026 and is forecast to reach USD 149.48 billion by 2031 at a 5.49% CAGR.

Which product type leads sales across Europe?

Footwear continues to dominate with 38.02% revenue share in 2025, though handbags are the fastest-growing segment.

Which country represents the fastest-growing demand?

Poland is projected to expand at a 6.26% CAGR between 2026 and 2031, outpacing all other European markets.

What role do online channels play in category growth?

E-commerce is expected to grow at a 6.73% CAGR, complementing flagship stores and underpinning omnichannel strategies.

What drives premium segment acceleration?

Rising sustainability awareness and consumer focus on craftsmanship quality push premium offerings toward a 6.01% CAGR through 2031.

Page last updated on: