Lactated Ringers Injection Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

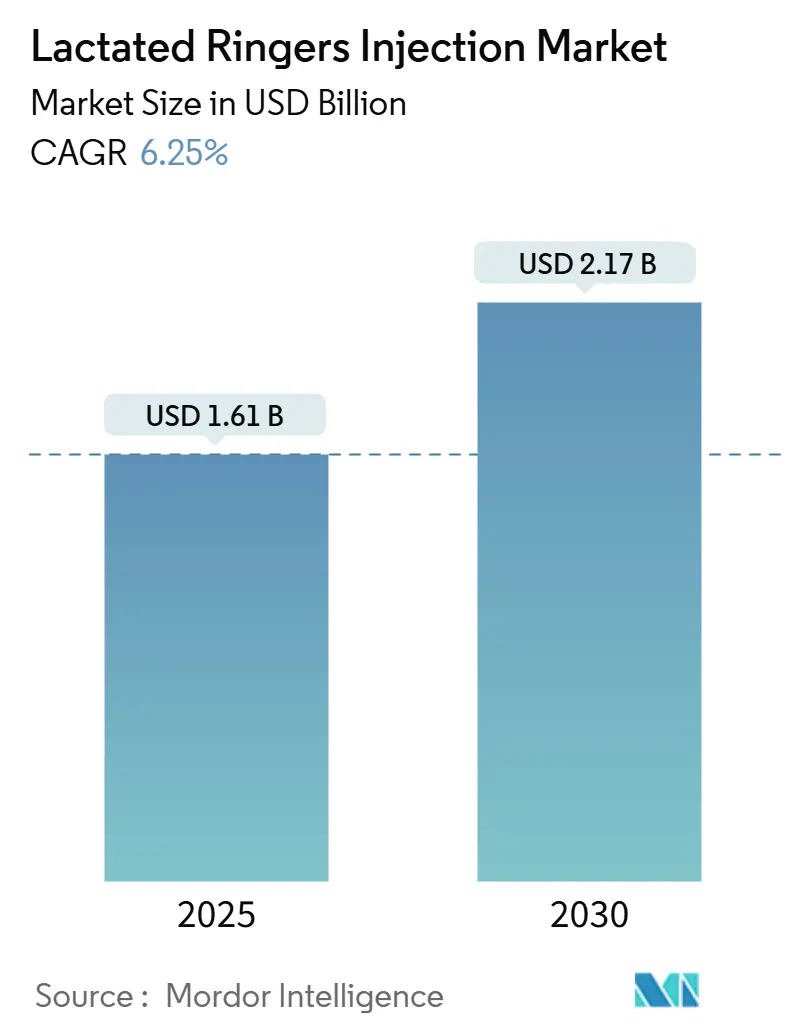

| Market Size (2025) | USD 1.61 Billion |

| Market Size (2030) | USD 2.17 Billion |

| Growth Rate (2025 - 2030) | 6.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lactated Ringers Injection Market Analysis by Mordor Intelligence

The Lactated Ringer's injection market size reached USD 1.61 billion in 2025 and is projected to climb to USD 2.17 billion by 2030, reflecting a 6.25% CAGR during the forecast period. Balanced crystalloid solutions are increasingly favored over saline for fluid resuscitation, and this preference—combined with rising surgical volumes, trauma cases, and home-based care adoption—underpins sustained growth. Intensifying emergency department capacity, coupled with hospitals’ tighter supply‐chain resilience mandates, is lifting procurement volumes even as conservation protocols become routine. Packaging innovation, especially the switch from PVC to non-PVC polyolefin bags, is reshaping vendor differentiation while global expansion of large-volume parenteral capacity, particularly across Asia-Pacific, is reinforcing supply security. At the same time, intermittent raw-material shortages, particulate recalls, and single-use‐plastic sustainability backlash temper the pace of market expansion.

Key Report Takeaways

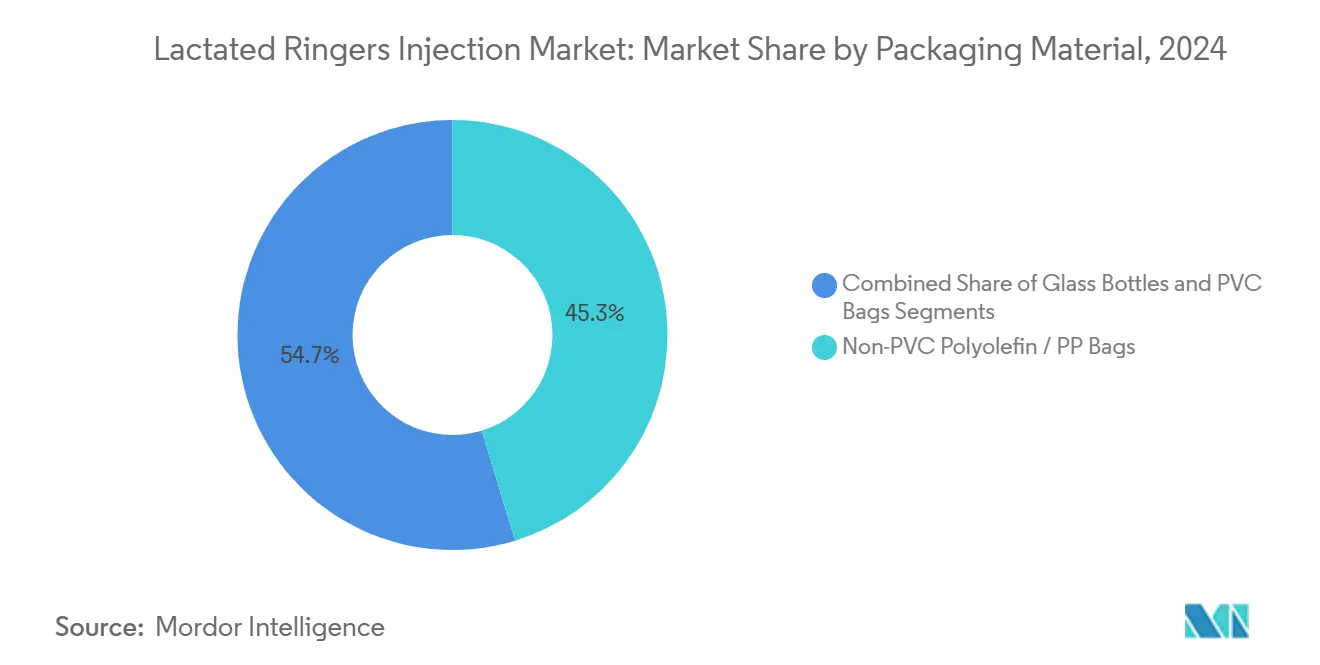

- By packaging material, non-PVC polyolefin/PP bags commanded 45.29% of the Lactated Ringer's injection market share in 2024.

- By container volume, 500-1000 mL formats accounted for 47.82% share of the Lactated Ringer's injection market size in 2024, while ≤250 mL packs advanced at a 9.42% CAGR through 2030.

- By end-user, hospitals captured 66.52% revenue share in 2024; home healthcare settings are forecast to grow at an 8.63% CAGR to 2030.

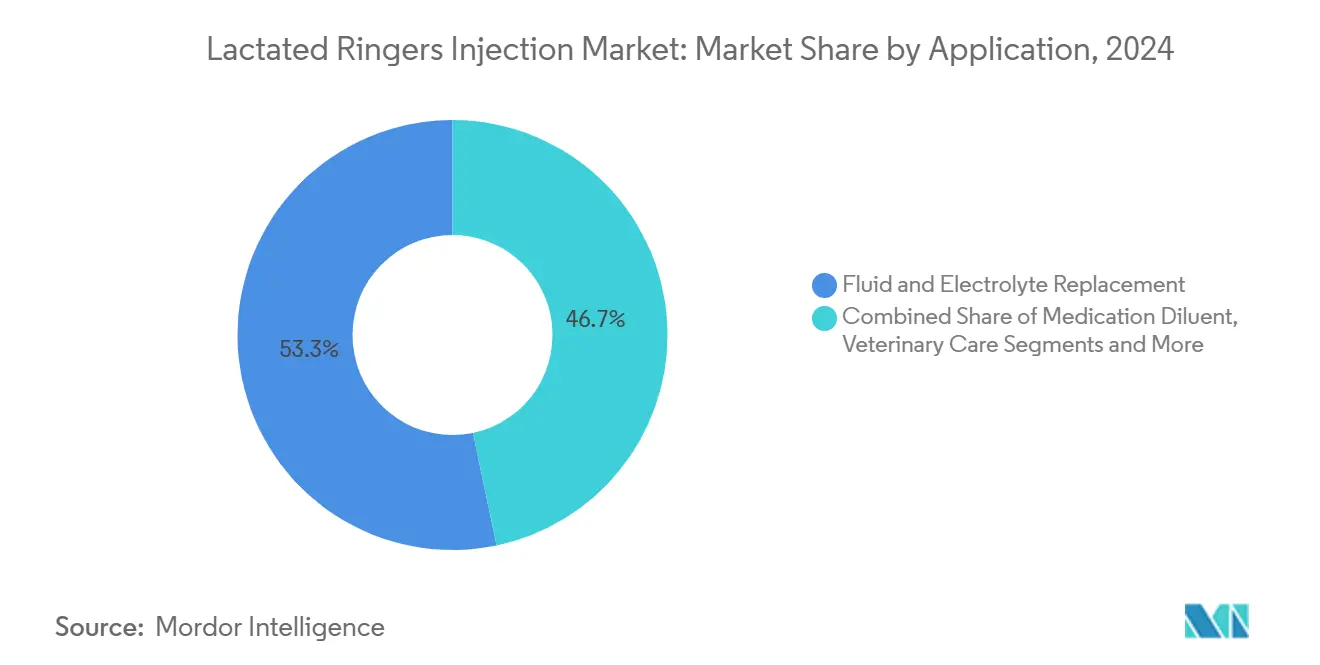

- By application, fluid and electrolyte replacement held 53.28% share of the Lactated Ringer's injection market size in 2024, with wellness IV therapy outpacing at a 9.54% CAGR through 2030.

- By distribution channel, hospital pharmacies held 69.72% revenue share in 2024, while online pharmacies are projected to post the fastest 10.89% CAGR through 2030.

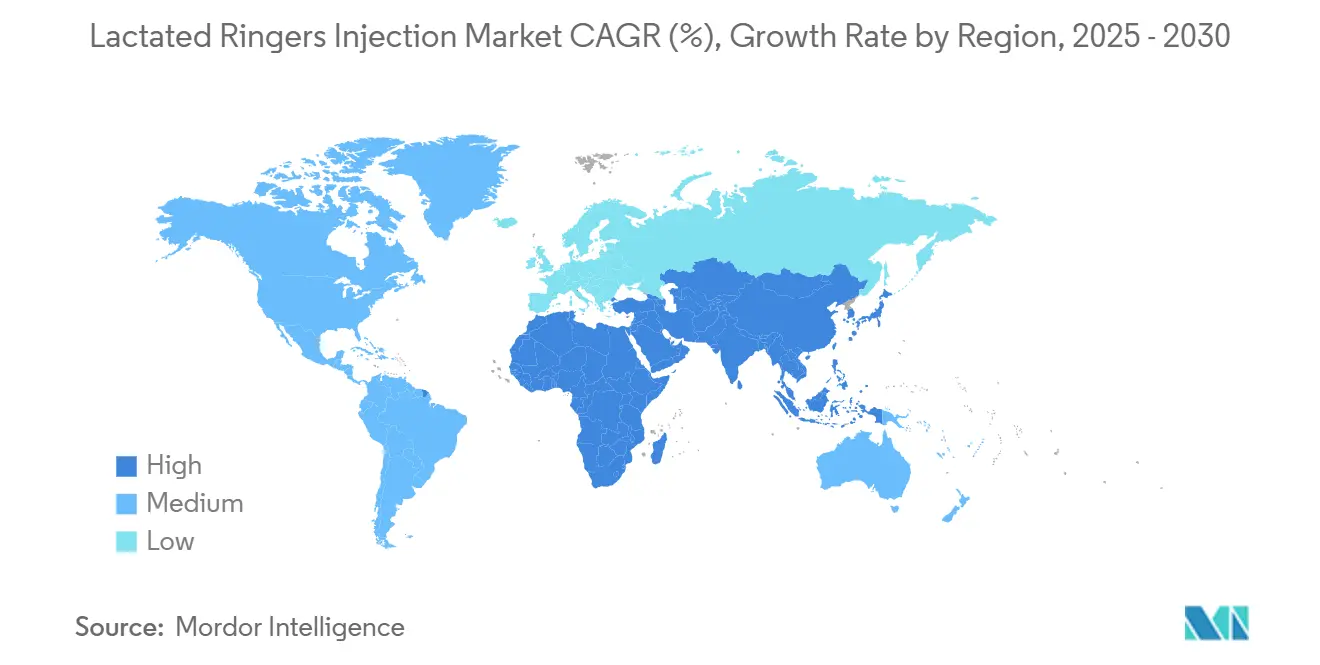

- By geography, North America led with 33.28% revenue share in 2024; Asia-Pacific is expected to post the fastest 8.41% CAGR to 2030.

Global Lactated Ringers Injection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hospital-driven IV fluid demand surge | +1.8% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Intensifying emergency & trauma cases | +1.2% | Global, higher impact in developed markets | Long term (≥ 4 years) |

| Growing preference for balanced crystalloids | +1.5% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Expansion of large-volume parenteral capacity in Asia | +0.9% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Shift to DEHP-free, non-PVC bags (ESG compliance) | +1.1% | Global, regulatory-driven in California & EU | Long term (≥ 4 years) |

| Home-based rehydration & wellness IV therapy | +0.7% | North America & EU, emerging in urban APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hospital-driven IV fluid demand surge

Hospitals worldwide face unprecedented inpatient volumes as elective surgeries rebound and aging populations drive higher admission rates. Typical facilities maintain only two to three days of IV fluid inventory, and the Hurricane Helene shortage exposed this vulnerability. Permanent inventory dashboards, diversified supplier contracts, and mandated strategic reserves are now standard procurement practices. These systemic shifts ensure steady purchasing cadence for Lactated Ringer’s injection market participants even during non-crisis periods. Integrated health networks also embed fluid-conservation protocols that balance cost control with patient-safety imperatives.

Intensifying emergency & trauma cases

Emergency departments are scaling bed counts and staffing to cope with rising trauma loads, mass-casualty preparedness programs, and climate-related disasters. The U.S. Veterans Health Administration found that every added ED clinic day per 10,000 enrollees deflected 48-61 external claims, proving the cost-saving value of capacity expansion.[1]Kertu Tenso, “Delivery System Emergency Department Capacity and Its Effect on Nonsystem Service Utilization,” Academic Emergency Medicine, wiley.com Military health systems likewise stockpile balanced crystalloids to support Role 4 definitive care across combat theaters.[2]Mason H. Remondelli, “Refocusing the Military Health System to Support Role 4 Definitive Care,” Journal of Trauma and Acute Care Surgery, lww.com These systemic investments elevate baseline demand for Lactated Ringer's injection market volumes across both civilian and defense channels.

Growing preference for balanced crystalloids

Large-scale trials, including the 15,802-patient SMART study, show a reduction in major adverse kidney events when balanced crystalloids replace saline.[3]Matthew W. Semler, “Balanced Crystalloids versus Saline in Critically Ill Adults,” New England Journal of Medicine, nejm.org Education campaigns and order-entry defaults pushed one U.S. network’s usage of Lactated Ringer’s from 28% to 75% within a year.[4]Joshua Bledsoe, “Order Substitutions and Education for Balanced Crystalloid Solution Use in an Integrated Health Care System and Association With Major Adverse Kidney Events,” JAMA Network Open, jamanetwork.comBecause cost parity with saline removes economic barriers, formulary committees increasingly designate Lactated Ringer’s as first-line therapy. This clinical shift locks in recurring demand and accelerates hospital contract conversions in the Lactated Ringer's injection industry.

Expansion of large-volume parenteral capacity in Asia

Governments from Australia to Japan are channeling grants and fast-track approvals to localize IV fluid production and reduce import reliance. Australia’s AUD 20 million expansion of Baxter’s Sydney plant will boost output to 80 million units annually by 2027. Standardized infusion-set specifications adopted by Japan’s PMDA improve manufacturing consistency and lower regulatory uncertainty. These initiatives stabilize global supply during natural disasters and position Asia-Pacific as the fastest-growing contributor to the Lactated Ringer's injection market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intermittent raw-material shortages | –1.4% | Global, concentrated impact in North America | Short term (≤ 2 years) |

| Product recalls linked to particulate contamination | –0.8% | Global, regulatory oversight varies by region | Medium term (2-4 years) |

| Cost pressure from saline price wars | –0.6% | Global, intensified in competitive markets | Long term (≥ 4 years) |

| Sustainability backlash against single-use plastics | –0.9% | Europe & North America, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intermittent raw-material shortages (polyolefins, lactate)

Sixty percent of U.S. generic drug inputs originate from China and India, leaving manufacturers exposed to geopolitical and logistics shocks. When polyolefin feedstocks tighten, smaller IV fluid producers struggle to secure allocations, prompting hospital buyers to favor larger vendors with multilayered supply networks. Diversification initiatives and on-shoring plans raise capital expenditures and pass-through costs, dampening the Lactated Ringer's injection market growth pace during shortage cycles.

Product recalls linked to particulate contamination

In 2024 and 2025, particulate contamination forced recalls of sodium chloride and Lactated Ringer’s batches from leading suppliers. Recalls trigger inventory scrapping, regulatory audits, and reputational damage, compelling manufacturers to invest in advanced filtration and inline optical inspection. While these upgrades bolster patient safety, they elevate production costs and complicate pricing negotiations with group-purchasing organizations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Material: Non-PVC Innovation Drives Market Transformation

Non-PVC polyolefin bags held 45.29% of the Lactated Ringer's injection market share in 2024 and are set to post a 10.45% CAGR to 2030. The Lactated Ringer's injection market size momentum stems from regulatory mandates, hospital sustainability pledges, and clinical preference to eliminate DEHP exposure. Supplier investments such as B. Braun’s USD 1.2 billion DEHP-free facilities support capacity scale-up and long-term contract locking. PVC bags continue servicing price-sensitive segments but confront declining volumes in regions with strict chemical regulations. Glass bottles remain a specialized choice where absolute barrier protection is paramount, sustaining niche demand in oncology and compounding pharmacies.

The transition to non-PVC packaging aligns with hospitals’ ESG scorecards. Baxter’s PVC recycling program diverted six tons of waste in pilot phases, convincing health systems to embed circular supply targets in tender documents. Because plastics account for 25% of the 34 pounds of medical waste each patient generates daily, sustainable packaging directly influences hospital accreditation and community relations. Consequently, suppliers champion life-cycle assessments and closed-loop take-back schemes as core differentiators in competitive bids.

By Container Volume: Large Formats Dominate While Small Volumes Accelerate

The 500-1000 mL category contributed 47.82% to the Lactated Ringer's injection market size in 2024, reflecting its suitability for routine fluid resuscitation and replacement therapy. Yet ≤250 mL packs exhibit a rapid 9.42% CAGR, propelled by ambulatory surgery, pediatrics, and home infusion protocols. These small formats reduce waste and align with precision dosing, vital in geriatric and pediatric care where fluid overload risks are pronounced.

Force-activated separation devices classified as Class II by the FDA in August 2024 enhance catheter integrity and enable safer administration of small-volume infusions. Ambulatory centers adopt barcode-linked pumps that preset infusion volumes, minimizing medication errors. Suppliers therefore bundle Lactated Ringer’s mini-bags with safety-engineered infusion sets, strengthening recurring revenue streams while positioning themselves as clinical-outcomes partners rather than commodity sellers.

By End-User: Hospitals Lead While Home Healthcare Emerges

Hospitals consumed 66.52% of global volumes in 2024, cementing their role as cornerstone purchasers of the Lactated Ringer's injection market. Large health systems negotiate multi-year supply contracts that hedge against displacement by saline. However, demographic shifts suggest home healthcare will record an 8.63% CAGR, reflecting payer incentives to move low-acuity care into residential settings.

Home infusion companies tout cost savings of up to 50% compared with inpatient delivery and report higher patient satisfaction rates. Technology platforms integrate e-prescribing, remote monitoring, and on-demand delivery, making Lactated Ringer’s logistics comparable to consumer e-commerce experiences. Veterinary hospitals, though smaller, illustrate cross-species product versatility, expanding addressable niches for human-grade manufacturers seeking portfolio adjacencies.

By Application: Fluid Replacement Dominates While Wellness Therapy Expands

Fluid and electrolyte replacement accounted for 53.28% of 2024 revenue and is projected to retain primacy throughout the forecast window. The Lactated Ringer's injection industry also benefits from surging wellness IV therapy, which is tracking a 9.54% CAGR as athletes, travelers, and wellness enthusiasts embrace hydration drips for performance and recovery.

Temporary FDA guidance that eased compounding restrictions during public-health emergencies catalyzed innovation in customized electrolyte and vitamin blends. Clinics market “immune boosts” and “jet-lag recovery” packages, each built on a Lactated Ringer’s base that mimics plasma electrolyte profiles. As clinical oversight tightens post-pandemic, providers with transparent sourcing and GMP-certified manufacturing stand to capture durable market share.

By Distribution Channel: Hospital Pharmacies Dominate While Online Channels Surge

Hospital pharmacies managed 69.72% of sales in 2024, leveraging integrated electronic health record systems to auto-replenish stock. Yet online pharmacies, advancing at a 10.89% CAGR, illustrate the sector’s digital pivot. CVS Health’s nationwide footprint and payer linkages enable same-day fulfillment of infusion supplies. In China, LBX Pharmacy’s 15,000-store network extends reach into rural locales, blending offline pickup with e-commerce ordering.

Direct-to-consumer portals partner with telehealth clinicians, letting patients schedule home IV sessions that include Lactated Ringer’s kits delivered by courier. This model circumvents traditional wholesalers, challenging incumbents to adopt omnichannel strategies that safeguard share across distribution silos.

Geography Analysis

North America retained 33.28% share in 2024, anchored by USD 4 trillion annual healthcare spending and entrenched clinical pathways that favor balanced crystalloids. Hurricane Helene’s damage to Baxter’s North Carolina plant, which previously supplied 60% of U.S. IV solutions, triggered Defense Production Act measures to prioritize domestic output and authorize emergency imports. Health systems implemented conservation dashboards that cut fluid consumption by up to 70% without compromising surgical caseloads, demonstrating operational agility.

Asia-Pacific is projected to record the highest 8.41% CAGR through 2030 as governments channel subsidies into local IV fluid manufacturing. Australia’s Baxter project alone will raise national output by 20 million units annually. China’s 310 million citizens aged 60 and above in 2025 drive baseline fluid demand, while Japan’s infusion-set standardization harmonizes quality expectations region-wide. Cross-border medical tourism in Thailand, Singapore, and India further accelerates Lactated Ringer's injection market growth as hospitals upgrade to U.S.-style trauma protocols to serve international patients.

Europe maintains mid-single-digit expansion underpinned by stringent EMA oversight and Green Deal sustainability targets that incentivize non-PVC adoption. New regulations require manufacturers to inform authorities of supply interruptions, curbing surprise shortages and promoting steady procurement cycles. South America and the Middle East & Africa register slower but steady uptake, buoyed by urban hospital construction and donor-funded emergency-care initiatives, though import tariffs and currency volatility continue to constrain penetration rates.

Competitive Landscape

The Lactated Ringer's injection market shows moderate concentration, with Baxter International, B. Braun Melsungen, Fresenius Kabi, and ICU Medical controlling a large share of global capacity. Baxter’s supply chain dominance became clear during the 2024 hurricane shortages, prompting hospitals to diversify vendors despite the company’s rapid recovery supported by federal intervention. B. Braun’s multi-billion-dollar shift to DEHP-free bags positions it as the ESG front-runner, while Fresenius Kabi leverages vertically integrated raw-material sourcing to safeguard uptime.

Strategic focus is migrating from price competition toward packaging sustainability, contamination control, and digital supply-chain transparency. Baxter’s closed-loop PVC recycling and B. Braun’s blockchain batch-tracking pilot resolve regulatory and consumer scrutiny over waste and provenance. Emerging players exploit veterinary and wellness niches by customizing formulations, whereas incumbents acquire specialty distributors to secure last-mile reach in home infusion. Investment in automated filling lines and inline particle detection reduces recall risks, converting quality assurance into a marketing asset that appeals to risk-averse hospital buyers.

Lactated Ringers Injection Industry Leaders

Becton Dickinson & Company (BD)

Baxter International Inc

B. Braun Melsungen AG

ICU Medical Inc.

Fresenius Kabi AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: B. Braun voluntarily recalled two lots of Lactated Ringer’s Injection USP 1000 mL and 0.9% Sodium Chloride Injection USP 1000 mL after detecting particulate matter inside the containers.

- March 2025: Nova-Tech issued a nationwide recall of Lactated Ringer’s 5 L veterinary solution (lot C2411061) due to fiber-like particles found during stability tests.

- October 2024: The Biden administration invoked the Defense Production Act to mitigate IV fluid shortages following Hurricane Helene and to expedite imports and domestic production recovery.

Global Lactated Ringers Injection Market Report Scope

| Glass Bottles |

| PVC Bags |

| Non-PVC Polyolefin / PP Bags |

| ≤250 mL |

| 251–500 mL |

| 501–1000 mL |

| Hospitals |

| Ambulatory Surgical Centers |

| Clinics |

| Home Healthcare Settings |

| Veterinary Hospitals |

| Fluid & Electrolyte Replacement |

| Acid–Base Management |

| Medication Diluent |

| Trauma & Burn Resuscitation |

| Veterinary Care |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Packaging Material | Glass Bottles | |

| PVC Bags | ||

| Non-PVC Polyolefin / PP Bags | ||

| By Container Volume | ≤250 mL | |

| 251–500 mL | ||

| 501–1000 mL | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Clinics | ||

| Home Healthcare Settings | ||

| Veterinary Hospitals | ||

| By Application | Fluid & Electrolyte Replacement | |

| Acid–Base Management | ||

| Medication Diluent | ||

| Trauma & Burn Resuscitation | ||

| Veterinary Care | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Lactated Ringer's injection market?

The Lactated Ringer's injection market size was USD 1.61 billion in 2025 and is forecast to reach USD 2.17 billion by 2030.

Which packaging material leads sales?

Non-PVC polyolefin/PP bags led with 45.29% share in 2024, buoyed by ESG regulations and hospital sustainability goals.

Why are ≤250 mL bags growing fastest?

Home healthcare, ambulatory surgery, and pediatric protocols prefer smaller volumes for dosing accuracy, driving a 9.42% CAGR.

Which region shows the highest growth?

Asia-Pacific is projected to expand at an 8.41% CAGR through 2030 as governments fund new IV fluid manufacturing lines.

How are suppliers tackling sustainability?

Leading vendors invest in DEHP-free materials, closed-loop PVC recycling, and blockchain traceability to meet hospital ESG criteria.

What impact did Hurricane Helene have on supply?

The storm disrupted 60% of U.S. IV solution production at Baxter’s facility, prompting federal action and hospital conservation measures.

Page last updated on: