Bovine Lactoferrin Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 724.58 Million |

| Market Size (2030) | USD 985.67 Million |

| Growth Rate (2025 - 2030) | 6.35% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bovine Lactoferrin Market Analysis by Mordor Intelligence

The bovine lactoferrin market size reached USD 724.58 million in 2025 and is forecast to climb to USD 985.67 million by 2030, reflecting a 6.35% CAGR. A confluence of infant-nutrition premiums, precision-fermentation breakthroughs, and expanding adult-health applications is broadening commercial horizons for the bovine lactoferrin market. Spray-dried formats continue to dominate volumes, yet freeze-dried and recombinant alternatives are narrowing the cost gap. Demand remains tightly linked to iron-absorption benefits, microbiome support, and antiviral positioning, while regulatory clarity in the US, EU, and key Asian economies sustains cross-border trade. Cost volatility in dairy inputs and purification bottlenecks still restrain short-term margins, but ongoing plant expansions and biotech scale-ups are poised to ease supply constraints. Market participants are repositioning product portfolios toward immune health, sports recovery, and plant-based functional foods, ensuring the bovine lactoferrin market retains multi-sector growth momentum.

Key Report Takeaways

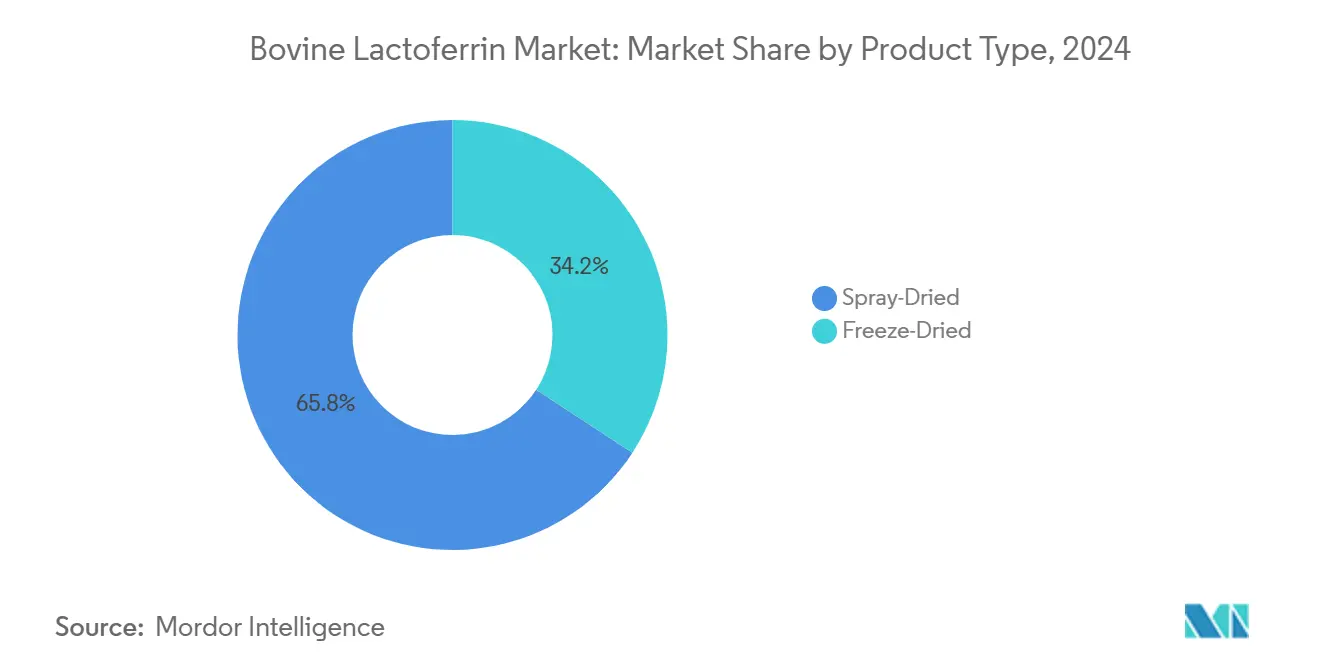

- By product type, spray-dried powders held 65.78% of the bovine lactoferrin market share in 2024, whereas freeze-dried grades are projected to expand at a 7.24% CAGR through 2030.

- By function, iron-absorption ingredients commanded 41.56% share of the bovine lactoferrin market size in 2024, while gut-flora protection is advancing at a 7.83% CAGR to 2030.

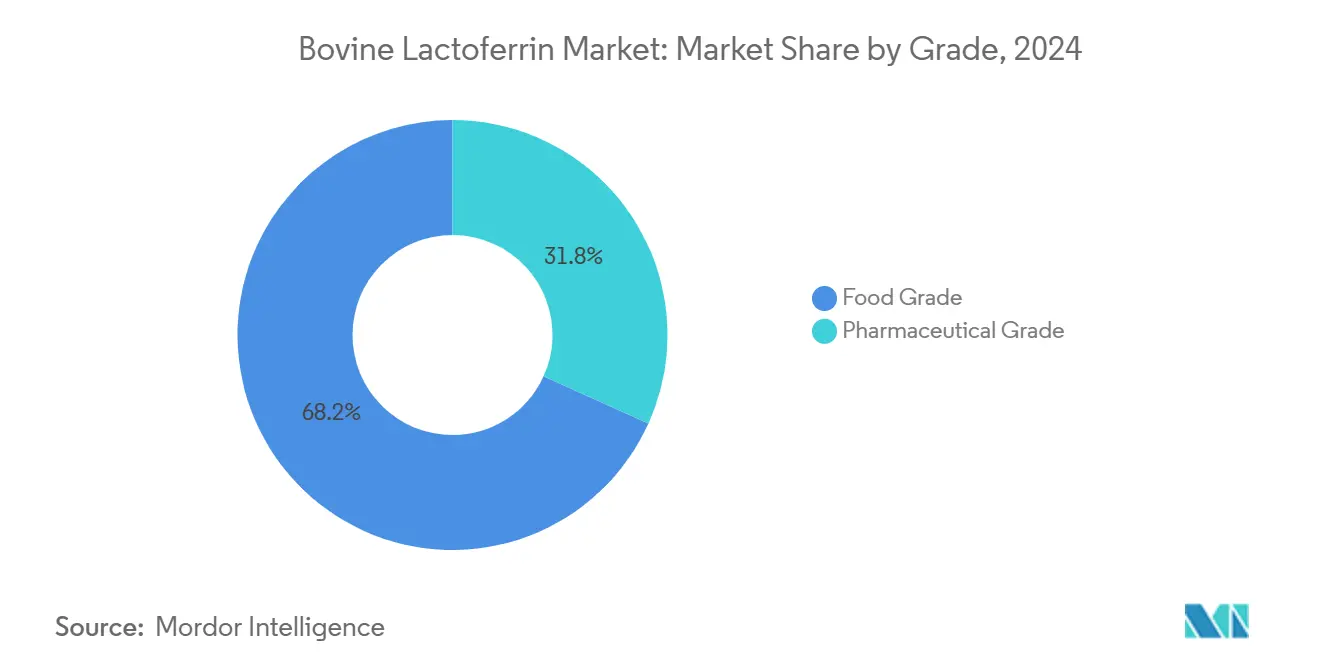

- By grade, food-grade offerings captured 68.24% share in 2024; pharmaceutical-grade revenue is forecast to rise at a 6.79% CAGR.

- By application, infant formula led with 48.39% of bovine lactoferrin market share in 2024, yet nutraceuticals are set to grow fastest at 6.95% CAGR.

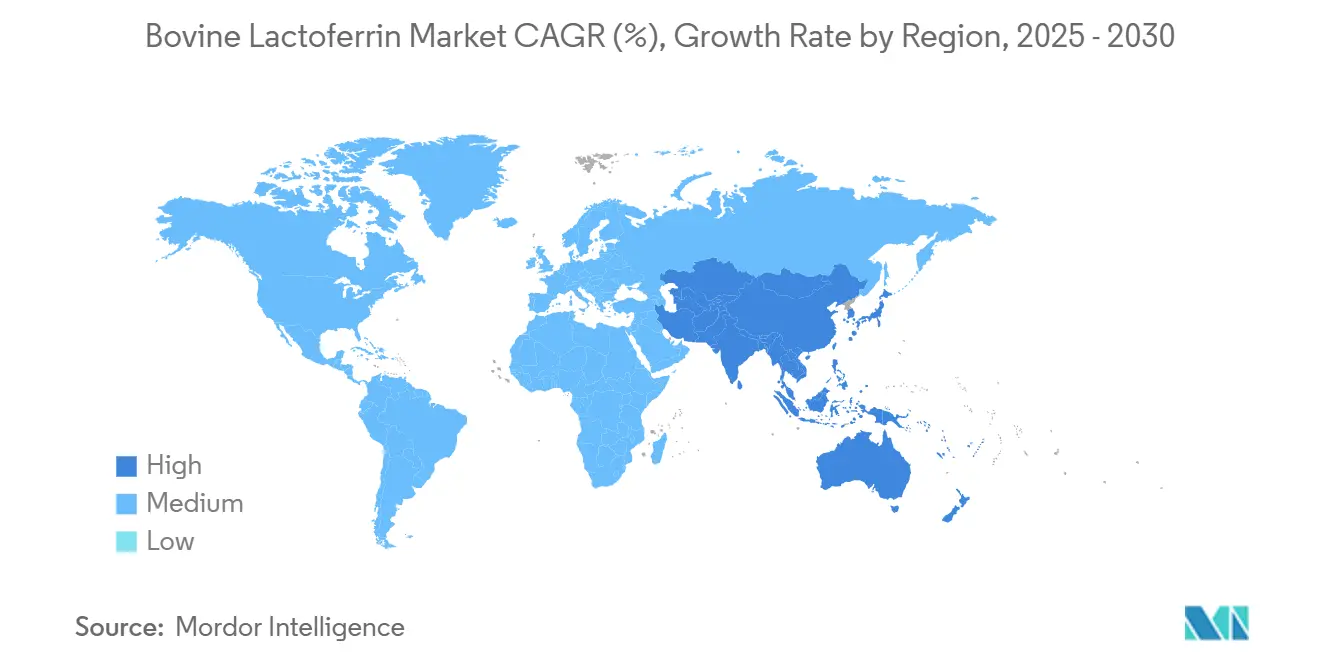

- By geography, North America accounted for 32.48% of 2024 revenue, whereas Asia-Pacific is on track for a 7.05% CAGR between 2025 and 2030

Global Bovine Lactoferrin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption in infant-formula industry | +1.8% | Global, with concentration in Asia-Pacific and North America | Long term (≥ 4 years) |

| Demand for anemia-targeted nutraceuticals | +1.2% | Global, particularly in developing markets with iron-deficiency prevalence | Medium term (2-4 years) |

| Precision-fermentation cost breakthroughs | +1.1% | Global, early uptake in North America, Europe, select APAC | Medium term (2-4 years) |

| Capacity expansions by dairy majors | +0.9% | North America & Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Broader regulatory clearances (GRAS, EFSA) | +0.7% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Post-pandemic antiviral positioning | +0.5% | Global, strong in regions with viral-outbreak history | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adoption in Infant-Formula Industry

Infant-formula manufacturers worldwide continue to integrate lactoferrin as a core differentiator, and nearly half of global demand flows into this channel. Multiple Generally Recognized as Safe (GRAS) notices in the United States and longstanding European Food Safety Authority (EFSA) opinions underpin regulatory confidence, enabling premium-tier brands to raise baseline inclusion levels. In China, lactoferrin-fortified formulations have shifted from niche to mainstream, reinforcing the bovine lactoferrin market as a foundational ingredient in “humanized” formulas.

Demand for Anemia-Targeted Nutraceuticals

Iron-deficiency anemia remains an unresolved public-health issue in many developing economies. Clinical research shows lactoferrin outperforming[1]Christofi MD, “ The effectiveness of oral bovine lactoferrin compared to iron supplementation in patients with a low hemoglobin profile: A systematic review and meta-analysis of randomized clinical trials,” PubMed, ncbi.nlm.nih.gov conventional ferrous salts in elevating hemoglobin, particularly in pregnant women and infants, spurring demand for capsules, sachets, and gummies. Affordable sachet formats tailored for low-income consumers[2]Elaine K. McCarthy, “Bovine Lactoferrin and Its Potential Use as a Functional Ingredient for Tackling the Global Challenge of Iron Deficiency,” Current Opinion in Food Science, sciencedirect.com illustrate how the bovine lactoferrin market is adapting formulations to address “hidden hunger.”

Precision-Fermentation Cost Breakthroughs

Companies such as FrieslandCampina with Triplebar Bio and TurtleTree have validated animal-free production routes that can cut cost per kilogram by more than half over the next decade. These advances promise new entries in plant-based yogurts, ready-to-drink beverages, and adult-nutrition shots, broadening the addressable base for the bovine lactoferrin market.

Capacity Expansions by Dairy Majors

Leading dairy processors are commissioning new extraction lines in Europe and Oceania, collectively adding several hundred tons of annual output. These projects hinge on membrane-chromatography upgrades that double yield per liter of whey, reducing reliance on multiple purification passes and trimming energy costs. As capacity comes onstream, the bovine lactoferrin market is expected to ease spot-price volatility in the mid-term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High purification & processing cost | -1.7% | Global, acute where dairy infrastructure is limited | Medium term (2-4 years) |

| Milk-supply volatility & price swings | -1.2% | North America, EU, downstream in Asia-Pacific | Short term (≤ 2 years) |

| Rise of plant-based immune ingredients | -0.9% | North America, Europe, spillover to APAC | Long term (≥ 4 years) |

| Tightening bio-active protein regulations | -0.8% | EU, Australia/New Zealand, select APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Purification & Processing Cost

Isoelectric points near neutral pH make lactoferrin susceptible to rapid fouling during extraction. Conventional multi-stage chromatography and ultrafiltration units incur high capital outlays and energy bills, keeping cost of goods elevated. Mixed-matrix and ligand-specific membranes are emerging, yet technology transfer to industrial scale remains slow, constraining penetration in price-sensitive supplements.

Milk-Supply Volatility & Price Swings

Extreme weather events, feed-cost inflation, and labor shortages have amplified raw-milk price volatility. Because lactoferrin is isolated from whey, any disruption to cheese or casein output tightens supply. This exposure to dairy-market cycles occasionally forces producers to ration spot volumes, challenging consistent downstream supply in the bovine lactoferrin market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Spray-Dried Retains Volume Dominance

Spray-dried variants commanded 65.78% of the bovine lactoferrin market size in 2024, illustrating how large-scale dryers and relatively low operating costs give this form a cost edge. Freeze-dried powders, while still niche, enjoy superior retention of tertiary protein structure and thus higher bioactivity, shaping demand in medical-nutrition formulas. Enhanced nozzle designs and closed-loop air systems are helping spray-dryers achieve tighter moisture control, reinforcing product stability. Conversely, low-temperature sublimation in freeze-dryers attracts premium price points that many clinical-nutrition buyers accept as a trade-off for bioactivity. Precision-fermented lactoferrin output is now entering the same value chain and is expected to augment spray-dried volumes rather than cannibalize them, as recombinant broth can be spray-dried directly. These dynamics ensure the bovine lactoferrin market continues to offer parallel growth paths for both formats.

The adoption of advanced drying and encapsulation technologies is enabling both formats to capture new use cases, particularly where product stability and bioactivity retention are mission-critical[3]Nika Kržišnik, “Enteric-Coated Lactoferrin Pellets Ensure Stability and Targeted Intestinal Delivery,” Pharmaceutics, mdpi.com. Production scale ups by European and Oceania facilities indicate that spray-dried lines will keep growing in absolute tonnage. Freeze-dried capacity, mostly concentrated in Japan and select US sites, is slated for double-digit expansion as pharmaceutical clients lock in supply. Continuous freeze-drying skid systems under pilot evaluation promise to narrow throughput differentials versus spray-drying. Should validation succeed, the bovine lactoferrin market size for freeze-dried grades may accelerate toward its forecast 7.24% CAGR through 2030.

By Function: Iron Absorption Anchors Demand

Iron-absorption ingredients represented 41.56% of the bovine lactoferrin market share in 2024, underscoring the protein’s well-documented ability to chelate and transport iron. Clinical-trial meta-analyses show faster hemoglobin recovery with lactoferrin relative to ferrous sulfate, bolstering medical-marketing claims. Growth in this function aligns with rising birth rates in emerging Asia and maternal-health supplementation protocols in Latin America. Concurrently, gut-flora support, spurred by microbiome research, is pacing at 7.83% CAGR as formulators combine lactoferrin with prebiotics and spore-forming probiotics. Immunomodulation, including modulation of cytokine balance, is attracting sports-nutrition and healthy-ageing brands. The bovine lactoferrin market is therefore diversifying its functional storyline beyond iron, mitigating dependency on a single benefit.

Scientific interest in antimicrobial action[4]Furkan Eker, “The potential of lactoferrin as antiviral and immune-modulating agent in viral infectious diseases,” Frontiers in Immunology, frontiersin.org—ranging from otitis media prevention to oral-care biofilm disruption—is also deepening. While these indications remain early-stage, they signal further addressable demand. Over the forecast horizon, iron-absorption SKUs will still dominate volumes, yet new health claims will progressively lift blended formats, keeping the bovine lactoferrin market on a trajectory of functionally segmented growth.

By Grade: Food Grade Drives Volume, Pharmaceutical Grade Accelerates

Food-grade powders accounted for 68.24% of the bovine lactoferrin market share in 2024, serving infant-formula, yogurt, and fortified-drink channels. Technological gains in pasteurization and low-endotoxin filtration have raised purity, enabling dual certification under food and supplement regulations. Pharmaceutical-grade output, however, is gaining traction, supported by 6.79% CAGR projections to 2030. Hospitals in Japan and select EU markets administer intravenous lactoferrin in post-surgical recovery protocols, driving premium pricing. Dermal formulations targeting wound-healing and acne are another emerging avenue. Because pharmaceutical-grade batches must pass stringent endotoxin and microbiological limits, only a handful of facilities currently qualify, which keeps barriers to entry high. Investment plans by Morinaga Milk Industry to retrofit reactors with clean-room isolation highlight supply diversification. These shifts suggest the bovine lactoferrin market will witness a gradual erosion of food-grade dominance as pharma-grade demand climbs.

Regulatory harmonization is also smoothing cross-border trade. A pending monograph under the Japanese Pharmacopoeia and ongoing discussions for inclusion in the European Pharmacopoeia will standardize assay methods, facilitating multinational procurement. As such norms crystallize, the bovine lactoferrin market size allocated to pharmaceutical-grade material is poised to escalate.

By Application: Infant Formula Retains Share, Supplements Accelerate

Infant formula captured 48.39% of the bovine lactoferrin market size in 2024, reflecting lactoferrin’s alignment with biomimicry trends. China’s revised GB standards stipulate higher lactoferrin inclusion, further entrenching demand. Premium tier SKUs in the United States and Europe now list lactoferrin on front-of-pack panels, reinforcing brand equity. Nutraceuticals, projected at 6.95% CAGR, are diversifying beyond capsules into gummies and stick packs aimed at adult immunity. Sports-nutrition applications leverage lactoferrin’s role in iron metabolism to mitigate “sports anemia” among endurance athletes. Functional beverages, while nascent, are testing stable micro-encapsulated inclusions. Personal-care and cosmetic brands are incorporating lactoferrin into serums for skin-barrier reinforcement, broadening application scope within the bovine lactoferrin market.

Technological convergence with precision-fermentation is easing supply concerns for non-dairy sectors. Plant-based yogurt and milk analog makers can now integrate recombinant protein without allergen-labeling constraints tied to bovine milk, opening incremental channels. This adaptability ensures the bovine lactoferrin market maintains application-led growth resilience.

Geography Analysis

North America obtained 32.48% of the bovine lactoferrin market size in 2024, underpinned by mature regulatory frameworks and broad application diversity. GRAS determinations have encouraged formulators to expand use beyond infant nutrition into cereal bars, gummies, and throat lozenges, sustaining consumption even as US birth rates plateau. Precision-fermentation ventures headquartered in California and Colorado have secured venture capital injections exceeding USD 300 million, signaling long-term supply assurance for the bovine lactoferrin market.

Asia-Pacific is the fastest-growing territory at 7.05% CAGR to 2030. China, which mandates higher fortification thresholds in infant formula, remains the epicenter of volume growth. Japanese researchers continue to pioneer clinical-grade applications, including lactoferrin-conjugated liposomes for metabolic syndrome intervention, further deepening regional sophistication. Limited indigenous extraction capacity, especially in Southeast Asia, necessitates imports from New Zealand and Europe, reinforcing inter-regional trade flows within the bovine lactoferrin market.

Europe exhibits a 6.04% CAGR outlook, with demand concentrated in premium infant nutrition and medical-nutrition segments. Widespread adoption of membrane-chromatography upgrades signals producer commitment to traceability and purity. However, stringent bio-active protein directives anticipated under the forthcoming EU Novel Food Regulation revision may require additional toxicology data, potentially slowing novel-format clearances. Investment in alternative protein facilities, such as precision-fermentation hubs in the Netherlands and Denmark, aims to buffer dairy-supply risks. Beyond the three core markets, the Middle East & Africa and South America register CAGRs of 6.68% and 6.26%, respectively. Growing awareness of fortified milks and anemia-focused supplements is lifting baseline demand, although logistics and consumer-price sensitivity temper acceleration.

Competitive Landscape

The competitive topology is transitioning from moderate concentration toward controlled fragmentation. Glanbia, FrieslandCampina, and Morinaga Milk Industry collectively command a sizable slice of installed extraction capacity, yet biotech entrants are redrawing boundaries. TurtleTree and Triplebar Bio deploy precision-fermentation systems with titers exceeding 3 g/L, achieving cost parity scenarios not feasible five years ago. Strategic collaborations, such as FrieslandCampina’s expanded tie-up with Triplebar Bio, underscore incumbents’ intent to hedge supply via dual pathways. Capital-expenditure disclosures indicate more than USD 1 billion earmarked for new membranes, chromatography resins, and stainless reactors worldwide, anchoring future throughput gains.

Patent landscapes reveal a shift toward affinity-ligand columns and ion-exchange membranes aiming to trim endotoxin levels below 0.05 EU/mg without diminishing yield. Dairy majors are also exploring smart manufacturing, integrating inline mass-spectrometry for real-time purity feedback. Meanwhile, precision-fermentation startups court plant-based dairy producers, positioning their animal-free lactoferrin as an ethical upgrade. As regulatory approvals widen, multiple production modes will coexist, intensifying pricing dynamics within the bovine lactoferrin market.

Emerging white-space encompasses adult-immunity chewables, antimicrobial oral-care rinses, and dermal patches for post-surgical healing. Cross-licensing deals between dairy incumbents and biotech newcomers are likely as each side seeks access to complementary IP and distribution. Overall, competitive pressure is expected to heighten, yet the diversity of technological platforms allows players to specialize, preserving margin pools across distinct value-chain nodes of the bovine lactoferrin market.

Bovine Lactoferrin Industry Leaders

Bega Cheese Ltd.

Fonterra Co-operative Group

FrieslandCampina Domo B.V.

Glanbia Plc

MILEI GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Daisy Lab achieved multi-gram-per-liter bovine lactoferrin titers in a yeast host, marking a critical scale-up milestone.

- May 2025: TurtleTree’s LF+ received a “no questions” GRAS letter from the FDA, opening broad US food and supplement use.

- April 2025: DeNovo Foodlabs and Earth First Food Ventures formed a venture targeting 300 tons of precision-fermented lactoferrin output annually, aiming to slash market prices by over 40% in ten years.

- May 2024: FrieslandCampina Ingredients and Triplebar Bio deepened their precision-fermentation partnership to counter global supply shortages and lower costs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the bovine lactoferrin market as all commercially purified proteins extracted from cow's whey or skim-milk streams and sold in powder or liquid form for use in infant formula, nutraceuticals, pharmaceuticals, functional foods, personal-care items, and related R&D applications. Only first-sale product revenues (ex-factory, any purity grade) are counted; downstream finished goods are outside the boundary.

Scope exclusions include animal-feed additives, recombinant or plant-derived lactoferrin, and bulk whey protein concentrates that contain trace lactoferrin and are not included.

Segmentation Overview

- By Product Type

- Spray-Dried

- Freeze-Dried

- By Function

- Iron Absorption

- Immune Modulation

- Antimicrobial

- Gut-Flora Protection

- Other Functions

- By Grade

- Food Grade

- Pharmaceutical Grade

- By Application

- Pharmaceuticals

- Infant Formula

- Nutraceuticals & Dietary Supplements

- Functional Foods & Beverages

- Personal-Care & Cosmetics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed dairy processors, ingredient distributors, formulation specialists, and regional food-safety officials across North America, Europe, Oceania, and East Asia. These conversations validated purification yields, typical contract prices by purity band, and emerging demand triggers such as China's GB-standard updates and precision-fermentation pilots, filling the gaps left by desk work.

Desk Research

We began by mapping global supply using public sources such as FAOSTAT dairy output, USDA-NASS milk-yield statistics, UN Comtrade export codes 350790 and 292219, Codex Alimentarius infant-formula standards, and EFSA/US FDA GRAS filings that cap lactoferrin inclusion levels. Trade-association white papers from the International Dairy Federation, plus peer-reviewed journals tracking purity-linked pricing, helped us benchmark extraction yields. Company filings, 10-Ks, and investor decks disclosed capacity additions, while news archives in Dow Jones Factiva and firm financial snapshots in D&B Hoovers grounded cost curves. Patent families retrieved via Questel illustrated technology diffusion. Many other open-source datasets were also referenced to triangulate volumes, prices, and regulatory milestones.

Market-Sizing & Forecasting

A top-down build starts with raw-milk availability, whey-stream split ratios, average lactoferrin yield per ton of whey, and weighted-average selling price. Outputs are stress-tested through selective bottom-up checks, sampled supplier shipments, and ASP multiplied by volume indications from channel partners before adjustments. Key model drivers include live-birth rates, infant-formula penetration, per-capita nutraceutical spend, purity-linked price spreads, and announced capacity pipelines. Multivariate regression coupled with ARIMA smoothing projects these variables to 2030, while scenario analysis gauges policy or technology shocks. Gaps where bottom-up evidence is thin are bridged by regional analogs reviewed with industry experts.

Data Validation & Update Cycle

Every model iteration passes anomaly screens, variance checks against historical series, and second-analyst review. Findings are then re-checked with at least one primary source before sign-off. Reports refresh yearly, and mid-cycle updates are triggered by material events such as factory start-ups, regulation changes, or price swings, ensuring clients get the latest view.

Why Mordor's Bovine Lactoferrin Baseline Commands Reliability

Published estimates often differ because firms pick varying product scopes, purity thresholds, and refresh cadences, or they rely on unvetted yield factors.

Key gap drivers include whether colostrum-derived or recombinant volumes are folded in, the choice of infant-formula versus total-nutrition demand pools, currency conversion dates, and the extent to which unofficial price quotes inflate revenue estimates. Mordor's model fixes scope to bovine-derived material only, applies audited yield coefficients, and updates exchange rates quarterly, yielding a balanced midpoint.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 724.6 Mn (2025) | Mordor Intelligence | - |

| USD 676.2 Mn (2024) | Global Consultancy A | Includes recombinant volumes and uses 2022 ASPs without currency re-base |

| USD 695.5 Mn (2024) | Industry Association B | Excludes pharmaceutical-grade material and applies constant infant-formula penetration |

| USD 755.1 Mn (2025) | Market Forecaster C | Assumes higher extraction yields based on pilot-plant data yet to scale |

Taken together, the comparison shows how disciplined scope setting, live price auditing, and annual refreshes enable Mordor Intelligence to deliver a dependable, decision-ready baseline for planners who cannot afford opaque assumptions.

Key Questions Answered in the Report

Why are infant-formula companies prioritizing bovine lactoferrin in new product lines?

Brands use lactoferrin to mimic breast-milk bioactives that support iron uptake and immunity, letting them position formulas as closer to human milk and command premium shelf placement.

How is precision fermentation reshaping the competitive landscape?

Recombinant production offers a dairy-free supply that lowers input costs and attracts plant-based food makers, allowing biotech start-ups to challenge long-established dairy processors.

What role do regulatory approvals play in accelerating adoption?

Clear GRAS opinions in the US and long-standing EFSA safety assessments in Europe give formulators confidence to include lactoferrin across foods, beverages, and supplements without lengthy novel-food hurdles.

Which functional benefits beyond iron absorption are gaining traction?

Formulators increasingly promote gut-microbiome balance and antiviral support, tapping research that links lactoferrin to beneficial shifts in gut flora and inhibition of certain respiratory viruses.

What supply-chain risks still concern manufacturers?

Dependence on whey streams exposes producers to milk-price swings and seasonal dairy yields, so companies diversify with precision fermentation and multi-region sourcing contracts.

How are pharmaceutical and personal-care sectors influencing demand patterns?

Clinical research into wound healing, metabolic syndrome, and skin-barrier protection is encouraging drug and cosmetics firms to secure pharmaceutical-grade lactoferrin, expanding use beyond traditional nutrition channels.

Page last updated on: