Labor Law Compliance Automation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

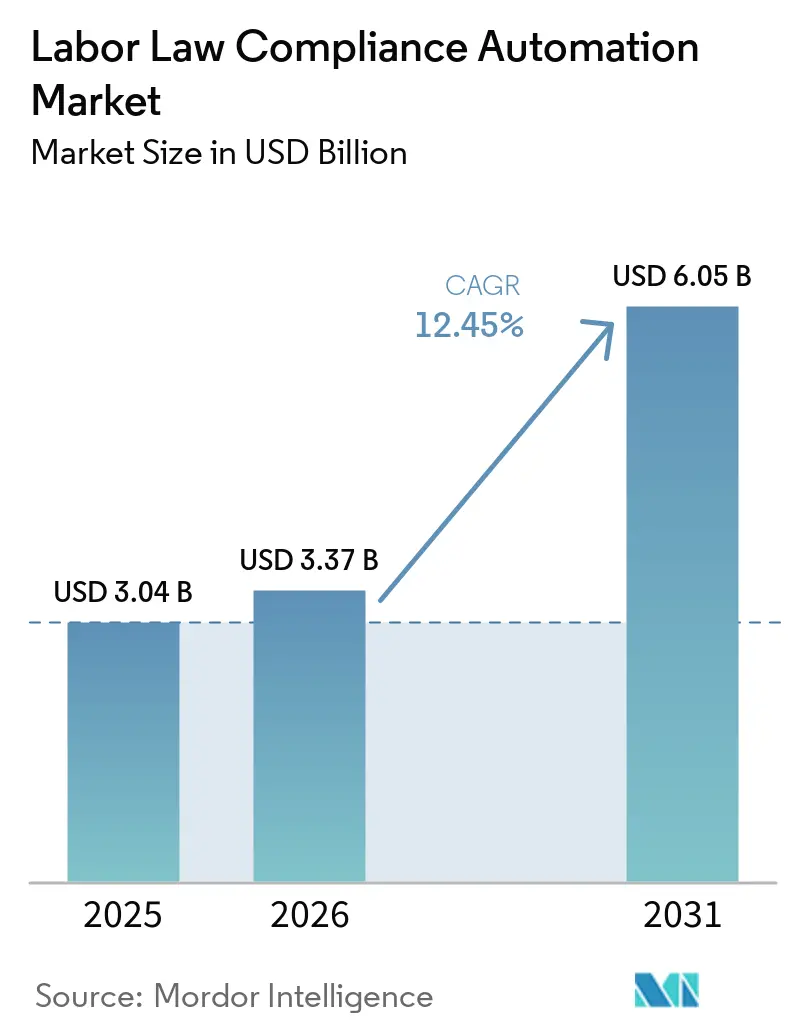

| Market Size (2026) | USD 3.37 Billion |

| Market Size (2031) | USD 6.05 Billion |

| Growth Rate (2026 - 2031) | 12.45% CAGR |

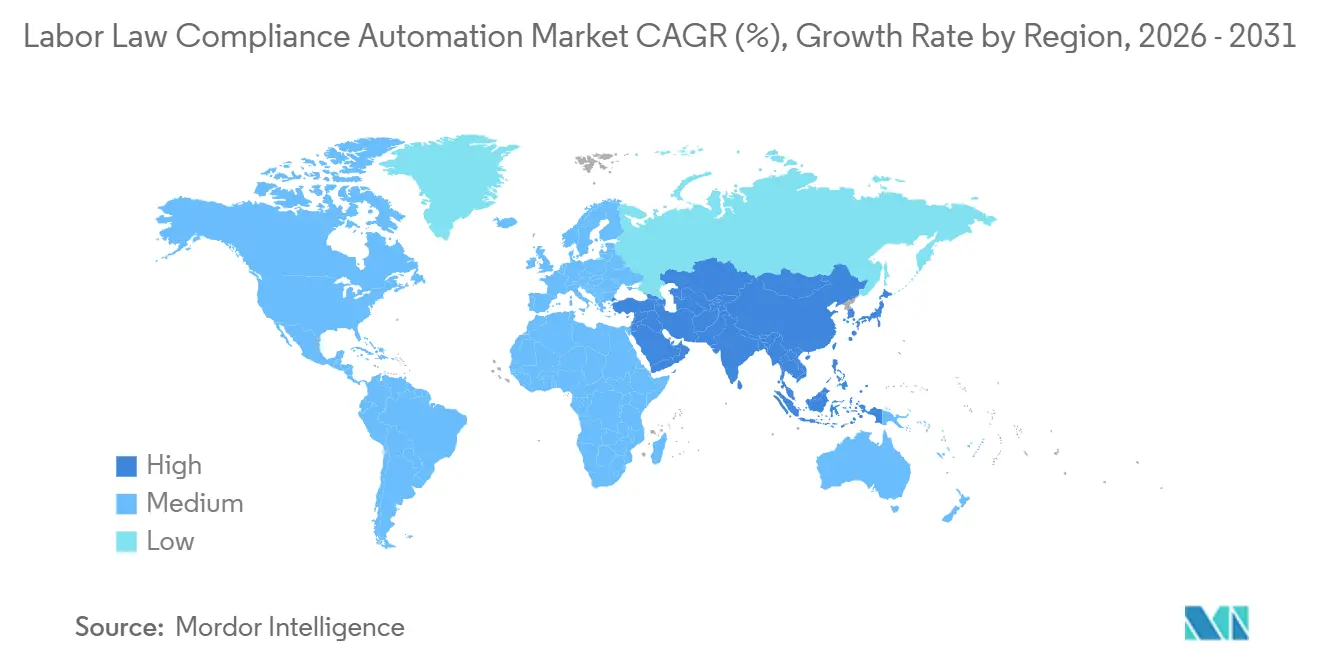

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Labor Law Compliance Automation Market Analysis by Mordor Intelligence

The labor law compliance automation market size is expected to increase from USD 3.04 billion in 2025 to USD 3.37 billion in 2026 and reach USD 6.05 billion by 2031, growing at a CAGR of 12.45% over 2026-2031. Employers are shifting compliance from a legal back-office task to a continuous operating process because rule changes now arrive across multiple jurisdictions simultaneously. This shift is being reinforced by the June 7, 2026, effect of the EU Pay Transparency Directive, the February 2026 U.S. proposal to rescind the 2024 independent contractor rule, and broader growth in gig and cross-border workforces, which are harder to manage with manual reviews. Demand is also supported by the need to document pay, classification, leave, and payroll decisions in a format that can withstand audit and litigation review. Vendor competition is widening between global employment platforms that package compliance into employer-of-record offerings and specialized vendors that focus on legal content, pay equity, and workflow automation. Even with uneven rule implementation across parts of Europe, buying intent remains strong because enterprises increasingly need systems that can demonstrate how workforce decisions were made, not just whether a policy exists.

Key Report Takeaways

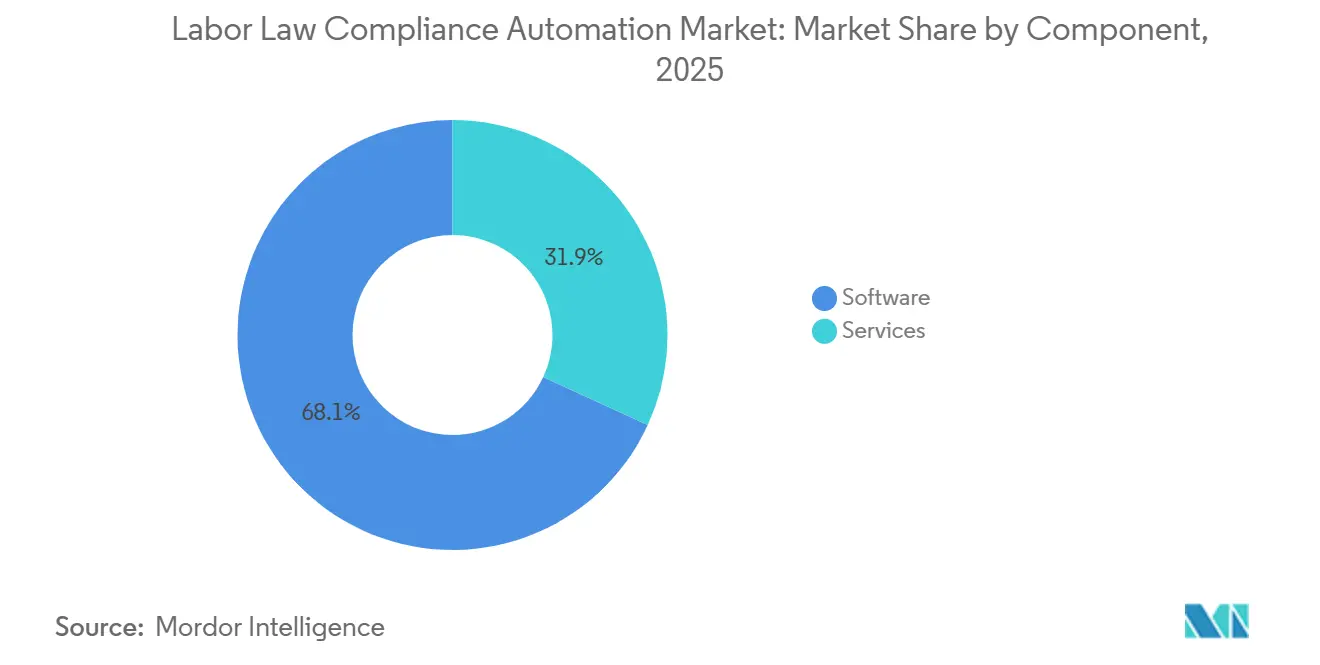

- By component, software led with a 68.12% revenue share in 2025, while services are projected to expand at a 14.46% CAGR through 2031.

- By functionality, wage, hour, leave, and payroll compliance accounted for a 41.22% share of the labor law compliance automation market in 2025, while worker classification and contractor compliance are projected to grow at a 13.12% CAGR through 2031.

- By deployment mode, on-premises accounted for 66.41% of revenue in 2025, while cloud is projected to grow at a 14.88% CAGR through 2031.

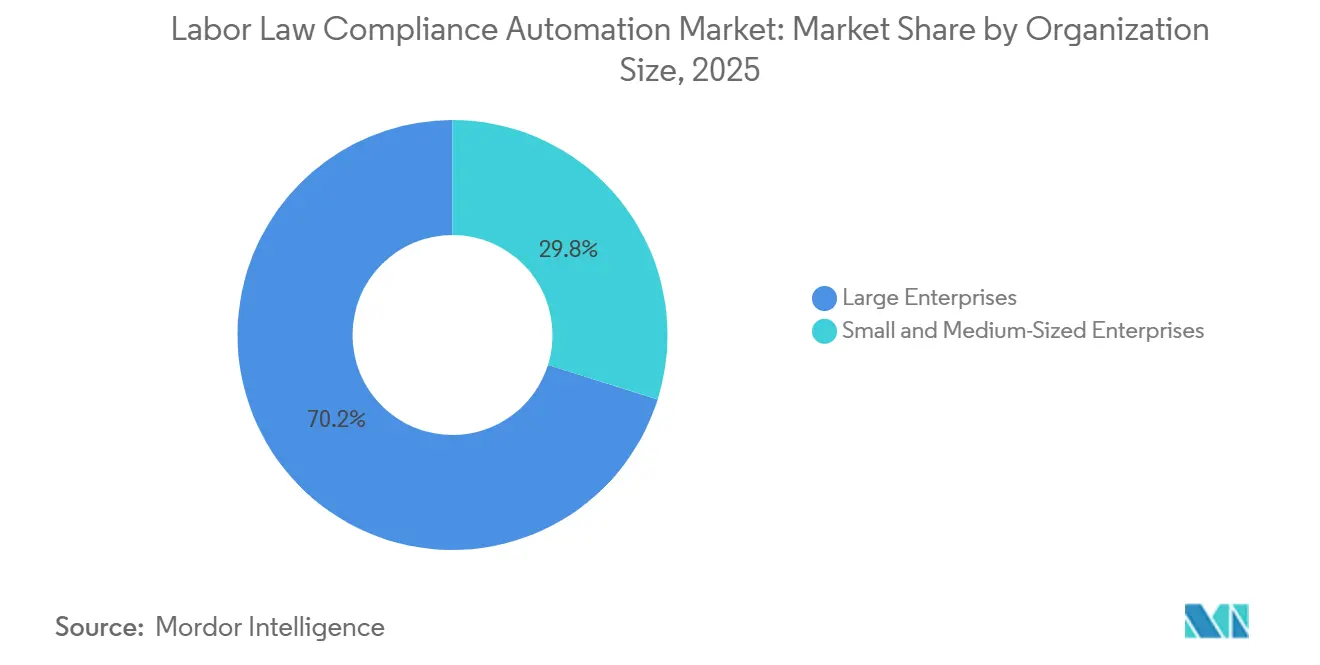

- By organization size, large enterprises held 70.16% of revenue in 2025, while SMEs are projected to expand at a 14.05% CAGR through 2031.

- By end-use industry, information technology and telecommunications led the labor law compliance automation market with a 36.21% share in 2025, while healthcare and life sciences are projected to grow at a 12.78% CAGR through 2031.

- By geography, North America held 38.51% of global revenue in 2025, while Asia-Pacific is projected to expand at a 13.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Labor Law Compliance Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Multi-Jurisdiction Labor Law Complexity | +3.2% | Global, with highest intensity in North America and EU | Short term (≤ 2 years) |

| European Union Pay Transparency Directive Readiness | +2.4% | EU core, spill-over to North America and APAC multinationals | Short term (≤ 2 years) |

| Growing Worker Classification and Contractor Compliance Risk | +2.0% | North America, EU | Medium term (2-4 years) |

| Need for Audit-Ready Payroll and Wage-Hour Controls | +1.5% | Global | Short term (≤ 2 years) |

| Expansion of Cloud-Based Human Resources and Payroll Compliance Stacks | +1.2% | Global, APAC core | Medium term (2-4 years) |

| AI-Driven Employment Decision Governance Requirements | +0.8% | EU and North America, with global spill-over | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Multi-Jurisdiction Labor Law Complexity

Multinational employers now manage live employment law changes across 90 jurisdictions, which pushes manual tracking well beyond a practical limit. Paul Hastings described regulatory fragmentation as the central global employer challenge in 2026, and that framing reflects how the labor law compliance automation market is moving toward continuous rule monitoring rather than periodic legal review. The issue is not simply that laws differ by country; it is that employers must translate those differences into operating rules for hiring, termination, leave, payroll, and documentation simultaneously. That pressure creates a demand floor for the labor law compliance automation market that does not depend on any single reform or court ruling. It also changes buying behavior, because platforms that push legal changes into templates, workflows, and audit logs are becoming part of core HR systems rather than optional legal tools. As that happens, vendor switching becomes harder because policy libraries, decision records, and jurisdiction rules become embedded in day-to-day operations.

European Union Pay Transparency Directive Readiness

The EU Pay Transparency Directive took binding legal effect on June 7, 2026, even though many member states had not completed national transposition by the deadline. Employers with EU operations, therefore, had to begin collecting data for the first reporting cycle before all local rules were fully settled, thereby heightening the urgency of automated payroll, reporting, and document controls. This timing mismatch is supporting the labor law compliance automation market because spreadsheet-driven pay analysis is harder to defend when disclosure and remediation duties begin before local implementation details stabilize. The directive also increases legal exposure when pay transparency duties are not met, because the burden of proof can shift in discrimination claims. KPMG also noted in 2025 that restrictions on pay confidentiality clauses were among the early requirements employers needed to address, which pushed contract and policy automation higher on the buying agenda. The result is that the labor law compliance automation market is benefiting not only from reporting needs but also from the need to align offer letters, employee communications, and internal pay-setting records across the EU.

Growing Worker Classification and Contractor Compliance Risk

Worker classification remains one of the strongest demand triggers in the labor law compliance automation market because the largest buyer regions are also the most active in changing classification rules. In the United States, the Department of Labor published a Notice of Proposed Rulemaking on February 26, 2026, to rescind the 2024 independent contractor rule and replace it with a revised approach under the FLSA.[1]U.S. Department of Labor, “Payroll Audit Independent Determination (PAID),” U.S. Department of Labor, dol.gov California still applies the ABC test to most contractor categories outside Proposition 22 carve-outs, which keeps classification exposure high for employers with flexible labor models. New Jersey also finalized its updated ABC-test framework in 2025, widening state-level enforcement pressure and making rule tracking more operational than theoretical. This instability matters more than a settled rulebook because employers need dynamic workflows that let them re-evaluate contractor populations whenever the legal standard shifts. That is why the labor law compliance automation market is being shaped by uncertainty itself, as unstable tests require continuous review rather than one-time policy updates.

Need for Audit-Ready Payroll and Wage-Hour Controls

Payroll and wage-hour exposure continues to support the labor law compliance automation market, as employers need systems that can demonstrate how every pay, overtime, leave, and classification decision was reached. The Department of Labor’s Payroll Audit Independent Determination program makes this especially important because employers can use that pathway only after they first identify likely violations through their own internal controls. That raises the value of tools that can flag exceptions early, preserve the decision trail, and connect wage-hour rules to the underlying employee record. This need is strongest in sectors with variable schedules, shift premiums, union rules, and complex leave accruals, where a routine input error can create a large downstream liability. The labor law compliance automation market is therefore seeing stronger demand for products that combine payroll logic, rule monitoring, and defensible documentation within a single workflow. It also explains why audit readiness is now being treated as an operating requirement, not simply a legal safeguard.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity Across Human Resource Information Systems, Payroll, and Legal Systems | -2.8% | Global | Short term (≤ 2 years), Medium term (2-4 years) |

| Sensitive Workforce Data Security and Localization Burdens | -1.8% | EU, APAC core, with spillover to North America | Medium term (2-4 years) |

| Regulatory Ambiguity in Worker Classification Rules | -1.2% | North America and EU | Medium term (2-4 years) |

| Persistent Need for Jurisdiction-Specific Human Legal Review | -0.9% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity Across Human Resource Information Systems, Payroll, and Legal Systems

Integration remains the clearest deployment barrier for the labor law compliance automation market because compliance decisions depend on data that spans HRIS, payroll, time-tracking, benefits, and legal content systems. When those systems use different field structures or update cycles, even a well-designed compliance engine can produce inconsistent outputs. This issue arises when employers operate across borders, as identity data, tax details, contract terms, right-to-work records, benefits data, and payroll inputs often flow through separate systems before a compliance decision is made. The labor law compliance automation market is therefore slowed not by weak demand, but by the time and cost required to connect old and new systems in a way that can withstand audit. Germany’s Federal Labor Court also clarified in late 2024 that company arrangements for employee data processing must still comply with the GDPR's purpose limitation and storage limitation requirements, which adds another layer to system design and documentation. That means many buyers still need service-heavy implementation plans before they can rely on automated compliance outputs at scale.

Sensitive Workforce Data Security and Localization Burdens

Data security and localization are also slowing the labor law compliance automation market because workforce compliance tools process some of the most sensitive employer records. The burden is multi-regional, with employers facing different rules on storage location, transfer mechanisms, permitted use, and access controls across Europe, Brazil, China, and other jurisdictions. Vendors, therefore, cannot always rely on one uniform cloud architecture, since some multinational customers need regional nodes, tighter sub-processor controls, and local governance layers before deployment can proceed. This makes the labor law compliance automation market even more complex for cloud vendors, even as customer demand rises. The EU AI Act adds another layer on August 2, 2026, for organizations using AI in HR settings, because technical documentation, conformity assessments, and risk-management systems become part of deployment obligations. As a result, buyers often move forward in phases, addressing privacy, residency, and AI governance requirements before expanding automation into more sensitive workflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate as Implementation Complexity Rises

Software held 68.12% of the labor law compliance automation market share in 2025, underscoring buyers' strong preference for platform-led regulatory monitoring and policy automation. That position reflected demand for scalable systems that could keep regulatory content current without manual legal review each time a rule changed. Large enterprises remained the core buyer group because they needed a single environment that could integrate policy generation, alerting, and classification analysis. In the labor law compliance automation market, software has also become the entry point for broader workflow redesign, as employers typically start with a rules engine before adding service layers.

Services are the fastest-growing component and are projected to expand at a 14.46% CAGR through 2031, underscoring the extent of implementation work still sitting at the software layer. This is not a sign of weak product maturithe ty. It reflects the growing effort required to configure rules across many jurisdictions, populate templates, and integrate with legacy payroll systems. The labor law compliance automation industry is therefore generating more service revenue per customer as legal coverage expands. SixFifty’s Employment Law Informatics Project, released in phases from November 2024, encoded more than 4,000 plain-language employment law summaries across all 50 U.S. states and major local jurisdictions, and that breadth naturally increases the need for configuration and adoption support. Security certifications such as ISO 27001 and SOC 2 Type II are also becoming part of implementation acceptance criteria, especially in regulated customer environments.

By Functionality: Wage and Hour Anchors the Market, Contractor Compliance Drives the Upside

Wage, hour, leave, and payroll compliance accounted for 41.22% of the labor law compliance automation market size in 2025, making it the main starting point for enterprise deployment. That leadership came from the steady exposure employers face over time, leave accrual, payroll accuracy, and wage rules across major jurisdictions. Companies often begin with these controls because they affect daily operations and carry immediate audit risk. In the labor law compliance automation market, this functionality acts as the gateway module that later supports adjacent adoption in documents, analytics, and monitoring.

Worker classification and contractor compliance are projected to grow at a 13.12% CAGR through 2031, supported by rule changes at both federal and state levels in the United States and related pressure in Europe. The category is expanding because employers can no longer assume that a one-time contractor review will remain valid for multiple years. Policy and document automation is also gaining weight as employers try to keep offer letters, handbooks, and separation documents aligned with shifting legal requirements. SixFifty stated in 2026 that its platform can automate 90% of routine employment law updates, underscoring why document-heavy workflows are entering the labor law compliance automation market faster than before.[2]SixFifty Technologies, “Labor Law Compliance Software,” SixFifty, sixfifty.com Audit trails and compliance analytics are also becoming more important as employers prepare for pay-setting documentation and defensible recordkeeping under European transparency rules, and Trusaic has been developing AI-led pay equity tools aligned with those needs.

By Deployment Mode: Cloud Accelerates as On-Premises Inertia Softens

On-premises deployment accounted for 66.41% of revenue in 2025, indicating that many large employers still relied on installed systems tied to data residency, internal controls, and long upgrade cycles. That installed base was especially strong in healthcare and financial settings where compliance software often sits close to payroll and identity systems. This share also reflected the slow replacement cycle of enterprise HR technology, where existing infrastructure tends to remain in use longer than buyer preference alone would suggest. The labor law compliance automation market, therefore, still carries a large legacy footprint even as new purchasing logic moves in another direction.

Cloud is the fastest-growing deployment mode, and this slice of the labor law compliance automation market size is projected to expand at a 14.88% CAGR through 2031. The reason is practical. Regulatory changes now arrive too quickly for quarterly or annual patch cycles to remain effective. The labor law compliance automation market is therefore favoring centrally maintained SaaS models that can push rule changes and policy updates in real time. Mordor Intelligence’s adjacent HRIS research noted that cloud subscriptions in that market grew at a 16.55% CAGR in 2025 and that 69% of employers had moved at least one core module to SaaS by 2025, which supports the same direction of travel here. Germany’s 2026 shift toward mandatory digital payroll record-keeping ahead of the January 1, 2027, archiving deadline is also reinforcing demand for systems that are easier to update and scale.

By Organization Size: SME Adoption Narrows the Enterprise-Only Narrative

Large enterprises accounted for 70.16% of revenue in 2025, reflecting their broader jurisdictional footprints, larger compliance teams, and greater capacity to evaluate complex software deployments. They were also better positioned to spend on systems that combine monitoring, documentation, and integration support. In the labor law compliance automation market, those factors kept enterprise buyers at the center of early adoption. Their scale also made compliance automation easier to justify because exposure was spread across more employees, more contractor relationships, and more countries.

SMEs are the fastest-growing segment, and this part of the labor law compliance automation market is projected to expand at a 14.05% CAGR through 2031. Lower SaaS pricing has opened the category to buyers who previously could not support enterprise-style implementation costs. Smaller employers also face acute classification risk because they often lack dedicated legal teams and cannot monitor frequent rule changes independently. New Jersey’s October 2025 ABC-test deadline and continued California AB5 exposure made automated classification records more relevant for both small and large businesses. The labor law compliance automation industry is therefore moving beyond its enterprise-only phase, and Paychex’s July 2025 acquisition of SixFifty directly supports that shift through a broader mid-market payroll and HR channel.

By End-Use Industry: Healthcare Presses the Acceleration Pedal, IT and Telecom Holds the Anchor

Information technology and telecommunications accounted for 36.21% of revenue in 2025, making it the largest end-use industry in the labor law compliance automation market. That position reflected cross-border hiring, contractor-heavy operating models, and frequent workforce changes linked to product cycles and project work. These employers often manage distributed teams across many jurisdictions, so classification and payroll compliance pressure is built into their operating model. As a result, the labor law compliance automation market continues to find a strong anchor in technology-led customer groups.

Healthcare and life sciences are projected to grow at a 12.78% CAGR through 2031, supported by complex shift premiums, union rules, and leave backlogs that need more systematic controls. The sector also faces higher documentation needs because regulators can review how staffing, leave, and pay decisions were applied to large groups of employees over time. Banking, financial services, and insurance remain an important secondary segment in which employment records feed into broader institutional audit readiness. Retail and e-commerce, manufacturing, logistics, industrial, and other end-use sectors add volume due to high hourly headcounts and frequent wage-hour exposure. Illinois also moved ahead with rules under the Use of AI in Employment Act for 2026, which adds notice, non-discrimination, and record-keeping obligations for employers using AI in hiring or performance decisions. That widens the reach of the labor law compliance automation industry across sectors that may not have viewed AI governance as part of workforce compliance until recently.

Geography Analysis

North America held 38.51% of the labor law compliance automation market share in 2025, making it the largest regional market. The region’s lead reflects the combined weight of federal wage and hour rules, state statutes, city-level mandates, and multi-agency enforcement across the United States. The Department of Labor’s February 26, 2026, proposal to rescind and replace the 2024 independent contractor rule adds to that pace of change and strengthens the case for dynamic classification tools. Canada and Mexico add demand through cross-border supply chains and payroll standardization needs. In the labor law compliance automation market, North American contracts also tend to be larger and more service-intensive because buyers often need deeper integration and configuration work.

Europe remains a core region because several major compliance changes now overlap in time. The EU Pay Transparency Directive became binding in 2026, while the EU AI Act introduces added obligations for HR-related AI deployments from August 2, 2026. Germany introduces a specific national catalyst through mandatory digital payroll record-keeping and archiving requirements that take effect on January 1, 2027. The labor law compliance automation market in Europe is also complicated by the expectation that some member states will apply stricter local thresholds than the directive baseline, which limits the usefulness of one standard pan-European configuration.

Asia-Pacific is the fastest-growing region, and this portion of the labor law compliance automation market size is projected to expand at a 13.56% CAGR through 2031. Government e-filing mandates, stronger labor-cost enforcement, and more cross-border hiring by technology exporters are supporting growth. Australia’s Fair Work Legislation Amendment, known as the Closing Loopholes Act 2024, signaled tougher enforcement on wage underpayment and raised the value of audit-ready payroll controls.[3]Staroplex, “Continuous Workforce Compliance to Keep You Audit Ready,” Staroplex, staroplex.com India, Japan, and South Korea also add momentum through wage, payroll, insurance, and record-digitization requirements that are harder to manage manually. The Middle East is building demand through wage protection and workforce quota systems, while Africa is still early in adoption and is largely led by multinational employer-of-record entry strategies.

Competitive Landscape

The labor law compliance automation market remains moderately fragmented, with competition split between global employment platforms and specialized compliance vendors. One group competes by embedding compliance into employer-of-record and global payroll ecosystems. This group includes Deel, Papaya Global, Remote, Globalization Partners, Multiplier, and Pebl (formerly Velocity Global). Their advantage comes from their geographic reach, owned-entity coverage, and the ability to connect hiring, payroll, and compliance workflows in a single stack. In the labor law compliance automation market, the integrated model appeals most to multinational employers seeking a single vendor relationship across many countries.

A second group competes through narrower but deeper functionality. SixFifty, GovDocs, and Trusaic focus more directly on legal content precision, documentation quality, and jurisdiction-specific outputs. SixFifty’s Employment Law Informatics Project encoded more than 4,000 employment law summaries across all 50 U.S. states and major local jurisdictions, which supports a content-led position in the labor law compliance automation market. Paychex strengthened that capability when it acquired SixFifty in July 2025, giving the combined offering a stronger route into payroll-connected compliance automation. Trusaic is also developing AI-led pay equity tools designed to meet EU transparency and AI governance needs, giving it a more focused position on defensible compensation compliance.

Strategic moves in 2025 and 2026 show how quickly the labor law compliance automation market is broadening beyond standalone software. Deel raised USD 300 million in Series E funding in October 2025 and said the capital would support acquisitions, AI development, and the expansion of native payroll to more than 100 countries by 2029. Remote expanded its infrastructure through the April 2026 acquisition of Bravas, while Papaya Global and Tech Mahindra allied in the same month to modernize workforce operations and payments. The labor law compliance automation market still has room for sector-specific orchestration, AI-governance documentation, and pay-equity analytics aligned with European rules. Buyers are also placing greater value on direct jurisdiction accountability, which can create a credibility gap for vendors that rely heavily on partner-led local coverage rather than owned entities. That keeps competitive pressure high even as the vendor field continues to widen.

Labor Law Compliance Automation Industry Leaders

Deel, Inc.

Papaya Global Ltd.

Remote Technology Services, Inc.

Atlas Technology Solutions, Inc.

Oyster HR, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: UKG unveiled agentic-powered UKG Pro Pay with Workforce AI at Payroll Congress 2026, introducing a Payroll Auditing AI that enables payroll teams to audit payrolls using natural language queries, alongside a Payroll Analyst Agent that surfaces root causes of payroll variances, materially advancing automated wage-hour audit capabilities for enterprise customers.

- April 2026: Remote Technology Services, Inc. completed the acquisition of Bravas, a French software company specializing in identity and device management, extending Remote's full employee lifecycle management platform and adding device provisioning and identity compliance capabilities across its global workforce operating system.

- April 2026: Papaya Global Ltd. and Tech Mahindra announced a strategic alliance targeting the modernization of global workforce operations and payments, with joint capabilities spanning automated onboarding, compliant cross-border payroll, and enhanced compliance governance through standardized controls for enterprise customers.

- April 2026: Multiplier Technologies Pte. Ltd. launched Global Payroll Payments, powered by Navro, completing its end-to-end Global Exchange for Work infrastructure spanning hiring, payroll, compliance, and payments across more than 150 countries.

Global Labor Law Compliance Automation Market Report Scope

The Labor Law Compliance Automation Market encompasses software and services that automate compliance with labor regulations, including wage laws, working hours, leave policies, and employee classification requirements. These platforms monitor regulatory changes, enforce compliance rules, and manage audit trails and reporting obligations. They primarily focus on operational compliance linked to workforce laws and statutory requirements. The market aims to reduce manual compliance efforts and ensure real-time adherence to evolving labor regulations.

The Labor Law Compliance Automation Market Report is Segmented by Component (Software, and Services [Implementation and Integration Services, and Support and Maintenance Services]), Functionality (Wage, Hour, Leave and Payroll Compliance, Worker Classification and Contractor Compliance, Policy and Document Automation, Labor Law Monitoring and Regulatory Change Management, Audit Trails and Compliance Analytics, and Other Functionalities), Deployment Mode (Cloud, and On-premises), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-Use Industry (Banking, Financial Services and Insurance, Information Technology and Telecommunications, Healthcare and Life Sciences, Retail and E-commerce, Manufacturing, Logistics and Industrial, and Other End-Use Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | |

| Services | Implementation and Integration Services |

| Support and Maintenance Services |

| Wage, Hour, Leave and Payroll Compliance |

| Worker Classification and Contractor Compliance |

| Policy and Document Automation |

| Labor Law Monitoring and Regulatory Change Management |

| Audit Trails and Compliance Analytics |

| Other Functionalities |

| Cloud |

| On-premises |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Banking, Financial Services and Insurance |

| Information Technology and Telecommunications |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Manufacturing, Logistics and Industrial |

| Other End-Use Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | Implementation and Integration Services | |

| Support and Maintenance Services | ||

| By Functionality | Wage, Hour, Leave and Payroll Compliance | |

| Worker Classification and Contractor Compliance | ||

| Policy and Document Automation | ||

| Labor Law Monitoring and Regulatory Change Management | ||

| Audit Trails and Compliance Analytics | ||

| Other Functionalities | ||

| By Deployment Mode | Cloud | |

| On-premises | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-use Industry | Banking, Financial Services and Insurance | |

| Information Technology and Telecommunications | ||

| Healthcare and Life Sciences | ||

| Retail and E-commerce | ||

| Manufacturing, Logistics and Industrial | ||

| Other End-Use Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of labor law compliance automation market?

The labor law compliance automation market was valued at USD 3.04 billion in 2025, is estimated at USD 3.37 billion in 2026, and is projected to reach USD 6.05 billion by 2031 at a 12.45% CAGR.

What is driving spending on labor compliance software in 2026?

Demand is being pushed by multi-country rule changes, EU pay transparency obligations, worker classification uncertainty, and the need for audit-ready payroll and documentation controls.

Which component leads revenue and which one is growing faster?

Software led with 68.12% of revenue in 2025, while services are forecast to grow faster at a 14.46% CAGR through 2031.

Why is contractor classification such a major buying trigger?

U.S. federal and state rules continue to shift, and employers need systems that can re-evaluate contractor status and preserve a defensible record of each decision.

Which regions matter most for future expansion?

North America remained the largest region with 38.51% of revenue in 2025, while Asia-Pacific is expected to grow fastest at a 13.56% CAGR through 2031.

Which customer groups and industries are expanding fastest?

SMEs are the fastest-growing organization size segment at 14.05% CAGR, and healthcare and life sciences is the fastest-growing end-use industry at 12.78% CAGR through 2031.

Page last updated on: