EU AI Act HR Compliance Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.94 Billion |

| Market Size (2031) | USD 5.07 Billion |

| Growth Rate (2026 - 2031) | 21.18% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

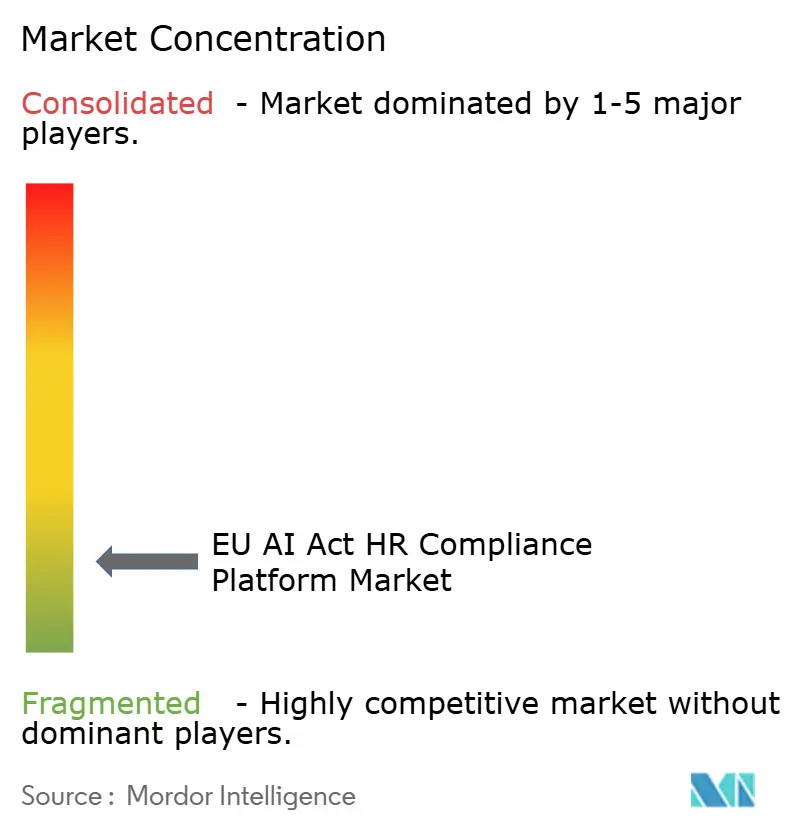

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

EU AI Act HR Compliance Platform Market Analysis by Mordor Intelligence

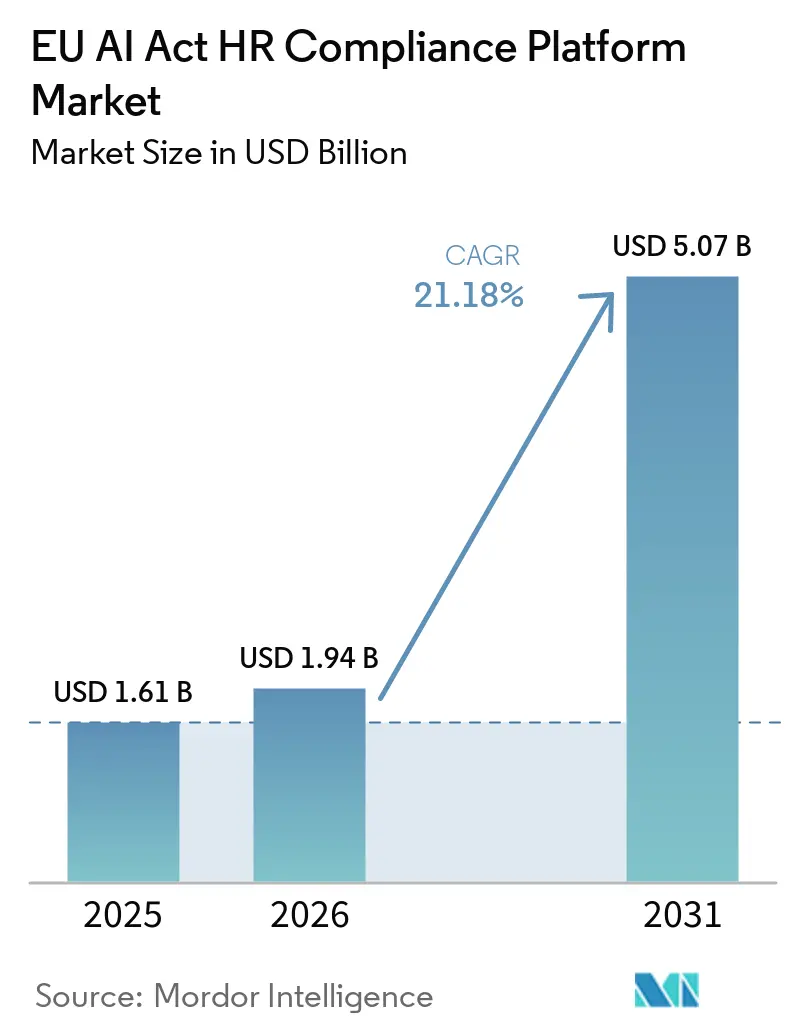

The EU AI Act HR compliance platform market size is projected to be USD 1.61 billion in 2025, USD 1.94 billion in 2026, and reach USD 5.07 billion by 2031, growing at a CAGR of 21.18% from 2026 to 2031. Regulation (EU) 2024/1689 moved HR-related AI use cases, such as recruitment, candidate screening, performance evaluation, task allocation via behavioral profiling, and workplace monitoring, into the high-risk category, making compliance spending a legal requirement rather than an optional software decision. Organizations that do not meet Article 26 obligations on human oversight, logging, incident reporting, and worker notification face penalties of up to EUR 15 million (USD 16.35 million) or 3% of global annual turnover, which has made preparation timelines much tighter across the European Union. The EU AI Act HR compliance platform market is also benefiting from the shift away from spreadsheet-based controls, as manual records are insufficient for automated logging, post-market monitoring, and fast incident reporting obligations. The EU AI Act HR compliance platform market is further supported by demand for cloud-delivered governance tools that can keep policies, controls, and evidence files aligned across cross-border HR operations where national interpretation may differ. The EU AI Act HR compliance platform market also has durable support from service-led implementation needs, supplier due diligence pressure, and the fact that worker notification and AI literacy obligations already apply even while some high-risk timelines remain under review.

Key Report Takeaways

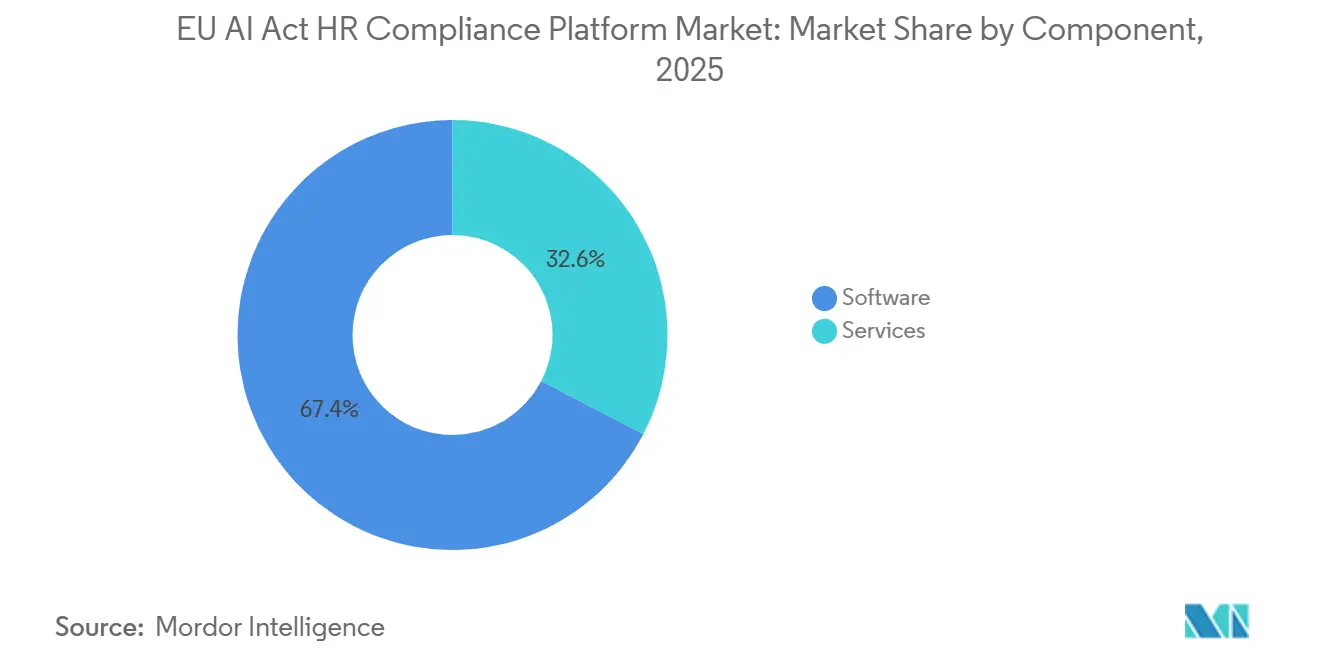

- By component, software held 67.39% of the EU AI Act HR compliance platform market share in 2025, while services are projected to expand at a 23.49% CAGR through 2031.

- By function, policy management and controls mapping accounted for 35.19% share in 2025, while bias and fairness testing is projected to grow at a 22.04% CAGR through 2031.

- By deployment mode, cloud captured 62.44% of the market in 2025, while hybrid deployment is projected to expand at a 23.12% CAGR through 2031.

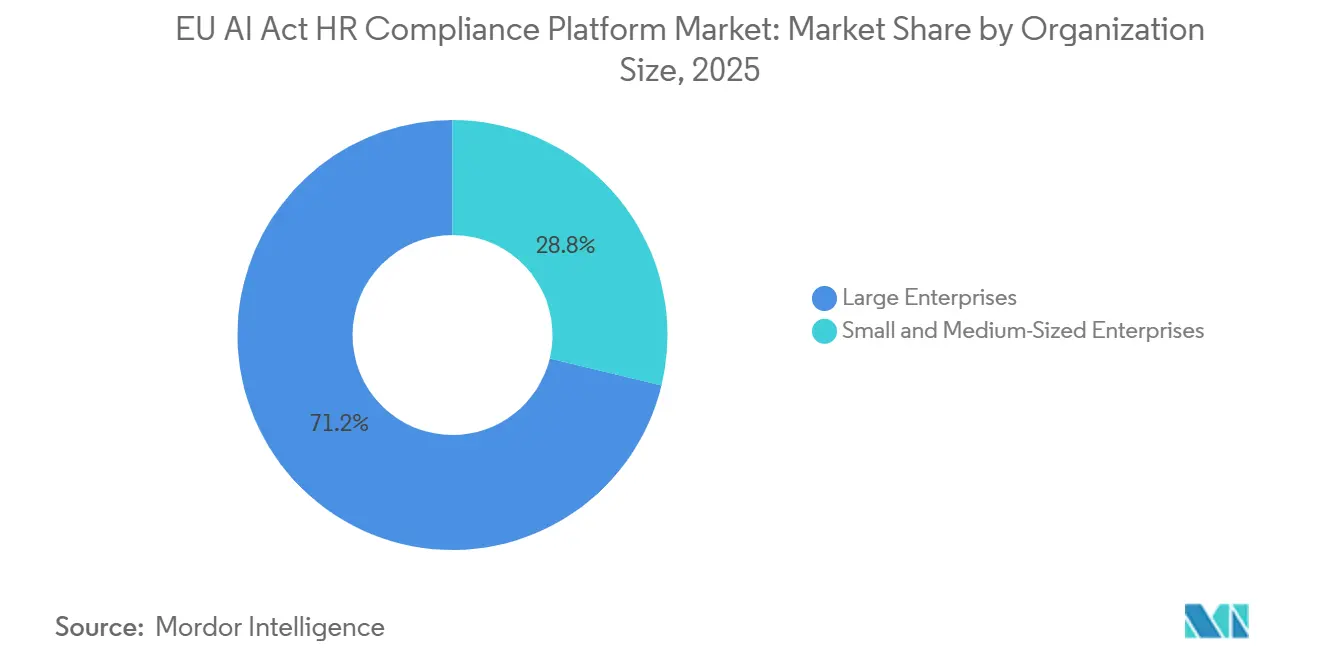

- By organization size, large enterprises held 71.22% share in 2025, while SMEs are projected to grow at a 23.85% CAGR through 2031.

- By end-use industry, IT and telecom led with a 29.31% share in 2025, while healthcare and life sciences are projected to advance at a 21.56% CAGR through 2031.

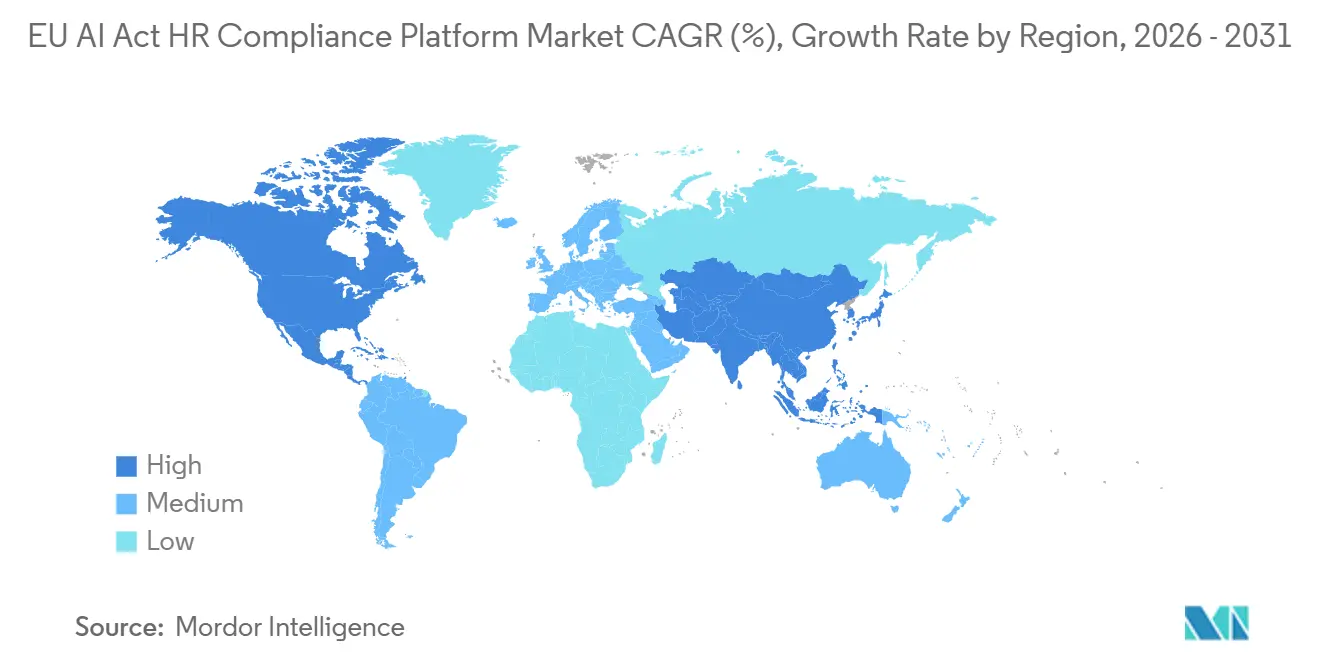

- By geography, Europe accounted for 38.71% share of the EU AI Act HR compliance platform market in 2025, while Asia-Pacific is projected to expand at a 22.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global EU AI Act HR Compliance Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU AI Act High-Risk HR Obligations Formalize Dedicated Compliance Budgets | +5.2% | Europe (core), North America and Asia-Pacific (multinationals) | Short term (≤ 2 years) |

| Off-the-Shelf Governance Suites Replace Spreadsheet-Based HR AI Controls | +3.8% | Global | Short term (≤ 2 years) |

| Bias Testing and Explainability Become Standard Buying Criteria in Hiring AI | +3.1% | Europe (core), Asia-Pacific and North America (secondary) | Medium term (2-4 years) |

| Cloud Delivery Speeds Regulatory Content Updates Across Multi-Country HR Deployments | +2.4% | Global | Short term (≤ 2 years) |

| Deployer-Side Vendor Assurance Burden Creates Demand for Shared Evidence Hubs | +1.9% | Europe and North America | Medium term (2-4 years) |

| Worker Consultation and Candidate Challenge Risk Raise Demand for Traceable Oversight Logs | +1.5% | Europe (national labor law overlay) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU AI Act High-Risk HR Obligations Formalize Dedicated Compliance Budgets

Annex III of Regulation (EU) 2024/1689 classifies AI systems used in recruitment, candidate evaluation, promotion and termination decisions, task allocation based on behavioral profiling, and performance monitoring as high-risk, placing a direct compliance burden on organizations that deploy these tools in HR settings.[1]European Parliament and Council of the European Union, “Regulation (EU) 2024/1689 of the European Parliament and of the Council on Artificial Intelligence,” Official Journal of the European Union, eur-lex.europa.eu The August 2026 enforcement baseline, together with penalties of up to EUR 15 million (USD 16.35 million) or 3% of global annual turnover, has pushed the EU AI Act HR compliance platform market into formal budget cycles rather than pilot-stage experimentation. The regulation matters even for companies that buy third-party HR AI software, because deployers still must maintain human oversight, logging, incident reporting, and worker notification records under Article 26 and related provisions. That design makes demand less dependent on who built the model and more on whether the employer can prove the model is used compliantly in daily operations. The European Commission’s guidance and timeline updates have reinforced that some obligations, including worker notification and AI literacy, already apply, thereby reducing the practical value of waiting for later enforcement milestones.

Off-the-Shelf Governance Suites Replace Spreadsheet-Based HR AI Controls

Organizations that still track HR AI systems through spreadsheets are finding that manual records do not satisfy Article 12 logging, Article 72 post-market monitoring, or the 15-day serious incident reporting window under Article 73, which is why the EU AI Act HR compliance platform market is shifting toward purpose-built software. This change is more than a software preference, because buyers now need structured evidence trails, role-based workflows, and repeatable controls that internal trackers usually cannot provide at scale. ISO/IEC 42001 has become part of that buying logic, and Microsoft’s compliance documentation noted that AI governance had become a standard line item in enterprise vendor questionnaires by the second half of 2025. Buyers increasingly prefer platforms that map controls across the EU AI Act, ISO/IEC 42001, and related frameworks into a single system, because the same governance investment can support multiple compliance programs. The EU AI Act HR compliance platform market, therefore, benefits from a procurement shift in which evidence automation, framework mapping, and audit readiness are replacing low-cost manual governance approaches.

Bias Testing and Explainability Become Standard Buying Criteria in Hiring AI

Articles 10(2)(f) and 10(2)(g) require providers of high-risk HR AI systems to examine training data for bias and implement measures to detect, prevent, and mitigate discriminatory outcomes, which has made fairness testing a core buying requirement in the EU AI Act HR compliance platform market. The pressure is greater because deployers also face individual accountability for explaining AI's influence on hiring or employment decisions, even when the underlying model documentation is with an outside vendor. A peer-reviewed legal analysis published in December 2025 noted that Article 86 creates practical tension for deployers who must explain outcomes without full access to provider documentation, thereby raising the value of platforms that preserve model-specific evidence and decision trails. Enterprise buyers are therefore asking for demographic performance reporting, explainability workflows, and third-party audit support during procurement rather than treating them as later enhancements. This change lifts the compliance baseline across the market and puts pressure on vendors whose offerings still stop at high-level fairness summaries without case-level traceability.

Cloud Delivery Speeds Regulatory Content Updates Across Multi-Country HR Deployments

The EU AI Act HR compliance platform market is seeing steady support from cloud delivery, as regulatory guidance, implementation details, and supervisory expectations have continued to evolve through 2026. Cloud-based governance suites can push updated policy packs, control maps, and evidence templates much faster than on-premises deployments, which depend on internal validation cycles and patch management. This matters for multinational employers because one HR AI deployment may need to satisfy multiple national interpretations while operating under a single corporate governance model. European data protection expectations do not remove the cloud case, because governance content, workflow orchestration, and evidence management can still be architected on European infrastructure with controlled handling of sensitive workforce data. As a result, the EU AI Act HR compliance platform market continues to favor delivery models that combine fast regulatory updates with centralized audit visibility across multiple countries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented National Interpretation Slows Product Standardization Across Europe | -2.1% | Europe | Short term (≤ 2 years) |

| Legacy Black-Box HR Models Limit Explainability and Remediation Readiness | -1.6% | Global | Medium term (2-4 years) |

| Standalone Platforms Depend on Upstream HR Tech Vendors for Critical Technical Evidence | -1.2% | Global | Medium term (2-4 years) |

| Limited Access to Representative Workforce Demographic Data Weakens Fairness Testing | -0.9% | Global, with acute impact in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented National Interpretation Slows Product Standardization Across Europe

The regulation required member states to set up national supervisory structures, but enforcement readiness has not progressed at the same pace across Europe, which makes the EU AI Act HR compliance platform market harder to standardize in the near term. Buyers do not just need a compliant product; they need confidence that their evidence files and workflows will be accepted across several jurisdictions with different operating practices. That pushes vendors to maintain country-specific policy packs, control mappings, and document templates rather than a single regional configuration. A strict common-denominator product can raise costs and operational burdens for buyers in less demanding settings, while a lighter product can expose them in stricter settings. This localization burden slows product standardization and favors vendors that can absorb ongoing regulatory interpretation work without weakening service quality.

Legacy Black-Box HR Models Limit Explainability and Remediation Readiness

Many enterprises still rely on vendor-supplied HR AI tools whose internal logic is not visible to the deploying organization, creating a structural limit on what the EU AI Act HR compliance platform market can solve through software alone. Article 14 requires qualified human oversight, but that obligation is harder to fulfill when deployers cannot inspect the model logic or trace how outputs were generated. The same gap affects explanation rights, because deployers may still need to provide meaningful explanations even when providers have not shared enough technical detail to support that process. If bias testing or monitoring reveals a serious issue, organizations may need to suspend use, negotiate remediation with the upstream vendor, or replace the system under tight reporting timelines. This dependence on upstream HR technology vendors slows adoption in environments where black-box models remain deeply embedded in existing recruiting and performance management workflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Demand Accelerates Beyond Core Software

Software held 67.39% of the EU AI Act HR compliance platform market share in 2025, which shows that buyers still prefer pre-built governance platforms over internal development for inventory management, automated policy mapping, and audit trail generation. This lead reflects the limits of general governance, risk, and compliance tools, which were not designed to capture the structured logging, technical documentation, and bias-testing records required under the AI Act. Service demand also remains strong because many buyers pursue ISO/IEC 42001 readiness alongside AI Act preparation, and those programs require competency frameworks, management reviews, and corrective action records that software alone cannot create.[2]Microsoft, “ISO/IEC 42001:2023 Artificial Intelligence Management System Standards,” Microsoft Learn, learn.microsoft.com In practice, the strongest vendors are those that can pair software depth with ongoing implementation and compliance management support, which makes component demand more balanced than the 2025 share split alone might suggest.

Services are projected to expand at a 23.49% CAGR from 2026 to 2031, putting this category ahead of the overall market pace and showing that buyers need more than software licenses to meet HR AI obligations. The main issue is execution, because platform deployment does not automatically produce compliant evidence files unless data feeds, user permissions, review steps, and documentation workflows are configured correctly across the HR technology stack. Many early programs were launched before dedicated governance platforms matured, so enterprises now face integration gaps between applicant tracking systems, HR information systems, performance tools, and the evidence structure required under the regulation. That has kept implementation, integration, and managed compliance work in demand, especially when companies want a single operating model across multiple countries and business units.

By Function: Policy Management Anchors Early Enterprise Deployments

Policy management and controls mapping accounted for 35.19% in 2025, reflecting how most organizations start by identifying covered AI use cases and linking them to specific obligations before investing in testing or incident workflows. That sequence has been common in the EU AI Act HR compliance platform market because companies first need to know what systems they use, why those systems may fall under Annex III, and what internal policies need to change before they can automate evidence gathering. Bias and fairness testing is projected to expand at a 22.04% CAGR in the EU AI Act HR compliance platform market size outlook through 2031, reflecting a later but sharper wave of spending as buyers shift from mapping obligations to proving technical compliance. The push is reinforced by academic and legal discussions that favor a more credible, audit-grade bias assessment over informal internal reviews, especially when employment decisions affect protected groups.

AI inventory and classification remain the practical foundation for every other module, because organizations cannot assign ownership, determine Annex III exposure, or maintain a current register of governed systems without it. Explainability and transparency management are also gaining weight because candidates and workers may request meaningful explanations of AI-assisted decisions, which require both technical evidence and user-facing communication workflows. Monitoring and incident management serve the post-market monitoring and rapid reporting obligations that arise once HR AI tools move into live production use. Other functions, such as conformity support, registration workflows, and structured filing preparation, become more important as deadlines draw closer, but early deployment still centers on policy mapping because it sets the logic for all downstream compliance work.

By Deployment Mode: Hybrid Architecture Emerges as Governance Sweet Spot

Cloud deployment held a 62.44% share in 2025, and that lead came from its ability to deliver fast content updates and consolidate evidence across multi-country HR operations. This matters in the EU AI Act HR compliance platform market because buyers often need a single control framework that can accommodate new guidance, evolving documentation requirements, and varying supervisory expectations without having to rebuild the whole system each time. On-premises deployment still retains demand among buyers in banking, financial services, insurance, government, and public sector environments where internal security rules or data sovereignty expectations remain strict. The practical outcome is that vendors gain an advantage when they can support cloud, on-premises, and hybrid models within a single governance framework, because deployment choices are increasingly shaped by sector conditions rather than a single technology preference.

Hybrid deployment is projected to grow at a 23.12% CAGR from 2026 to 2031, indicating that buyers increasingly want cloud-based regulatory orchestration without moving all sensitive HR data into a single centralized environment. This model meets a practical compliance need, as organizations often want cloud-delivered updates for policy packs, control libraries, and reporting templates while keeping workforce demographic data close to local systems used for bias testing and explanation workflows. The result is a split architecture in which governance content can be managed centrally while sensitive data processing remains near the operating environment that generated it. For many enterprises, that is not a temporary compromise but the most workable way to align HR AI compliance activities with broader employment, privacy, and internal security requirements.

By Organization Size: Large Enterprise Dominance Faces SME Disruption

Large enterprises commanded a 71.22% share in 2025, reflecting that cross-border employers typically face the widest HR AI exposure and the heaviest documentation burden under the regulation. Their HR environments often include multiple recruiting, screening, workforce planning, and performance systems, meaning a single company may need to govern several high-risk use cases simultaneously. That scale makes manual governance both expensive and legally fragile, especially when explanation rights, incident timelines, and audit expectations must be managed across several jurisdictions. Large enterprises also tend to face greater reputational risk when discriminatory hiring outcomes become visible, making the business case for structured governance platforms even stronger before penalties are considered.

SMEs are projected to expand at a 23.85% CAGR from 2026 to 2031, making this the fastest-growing segment of the EU AI Act HR compliance platform market. The European Commission’s evolving policy direction has acknowledged SMEs as a distinct compliance population, and the regulation itself does not remove deployer obligations simply because the employer is smaller. Another growth driver is commercial pressure from larger customers, as supplier due diligence increasingly includes AI governance attestations that can force smaller vendors to adopt formal controls before any direct enforcement action is taken against them. Vendors are responding with SaaS pricing tiers and pre-configured templates for major European jurisdictions, which lowers entry barriers and widens the addressable buyer base without changing the underlying compliance standard.

By End-Use Industry: Healthcare Challenges Information Technology's Market Lead

The information technology and telecom sector held a 29.31% share in 2025, reflecting its early use of AI in resume screening, coding assessments, interview scoring, and related hiring workflows that fit squarely within the regulation’s HR risk perimeter. Healthcare and life sciences are projected to grow at a 21.56% CAGR through 2031, as workforce management, clinical staffing, and sector-specific governance needs combine to create a broader compliance surface than many providers initially expected. Credo AI’s 2026 CHAI partnership also showed how vendors are tailoring governance offerings for healthcare organizations that need one framework spanning HR, operational AI, and sector-specific controls. That combination gives healthcare a strong growth path, even though IT and telecom remained the largest end-use buyer group in 2025.

BFSI remains an important customer group because many firms already run model risk governance programs, which lowers the hurdle for adopting HR AI compliance workflows but raises expectations for documentation quality and validation depth. ValidMind’s September 2025 update, adding EU AI Act support, is a good example of how vendors are adapting existing model governance products for financial institutions that want a single workflow to cover multiple obligations. Government and public sector organizations are also relevant because Article 27 requires a Fundamental Rights Impact Assessment when they deploy high-risk AI, thereby increasing demand for structured assessment workflows. Retail, manufacturing, and other end-use categories add demand as inventory exercises uncover AI-based scheduling, task allocation, and performance tools that were not initially treated as regulated systems but still fall into the HR compliance scope once reviewed more carefully.

Geography Analysis

Europe accounted for 38.71% share of the EU AI Act HR compliance platform market size in 2025, and that lead came from the regulation’s origin in the region and from earlier readiness spending among enterprises that expected HR AI obligations to move from policy debate into enforceable practice. The regional market also benefits from the fact that covered deployments within the European Union are subject to direct legal requirements for oversight, logging, transparency, and post-market monitoring, which gives buyers a stronger reason to invest earlier. The uneven pace of national implementation has also supported Europe’s position, because companies operating across several member states want a single platform layer to organize evidence before local supervisory practices settle into a stable pattern.[3]European Commission, “AI Act - Regulatory Framework for Artificial Intelligence,” European Commission, digital-strategy.ec.europa.eu That dynamic keeps the region at the center of current demand even when some enforcement details remain in motion.

North America held the second-largest regional position in 2025, driven mainly by multinational employers that need a single governance approach for EU operations and domestic HR AI use. For these buyers, the value of the EU AI Act HR compliance platform market extends beyond Europe, as controls for logging, fairness review, and explainability can also support overlapping employment and governance expectations in the United States and Canada. This has encouraged centralized AI governance teams to choose platforms that can map a single evidence model across multiple jurisdictions rather than maintain separate local processes. Mexico remained earlier stage, with demand tied more closely to export-oriented businesses and supply relationships with EU-connected customers than to domestic regulation alone.

Asia-Pacific is projected to expand at a 22.67% CAGR in the EU AI Act HR compliance platform market, making it the fastest-growing regional segment from 2026 to 2031. The main driver is not a single local law that mirrors the EU framework, but the spread of EU-aligned procurement standards through multinational vendor and supplier relationships. That has created demand in countries such as Japan, South Korea, India, Australia, and New Zealand, where employers and software vendors need to demonstrate governance readiness even when the legal trigger originated elsewhere. Middle East demand is being shaped by global banks, technology firms, and public entities seeking cross-framework governance support, while financial services and multinational operating footprints are driving African demand. South America remains nascent, centered on Brazil, with additional activity in Chile and Argentina, where EU-facing commercial contracts increasingly include compliance attestation requirements.

Competitive Landscape

The EU AI Act HR compliance platform market remained fragmented, with no single vendor holding a dominant position across all functional layers. Compliance-focused specialists such as Credo AI, Holistic AI, LatticeFlow AI, Enzai, and Modulos AG have competed on regulatory depth, pre-built policy content, and bias certification capabilities, while AI lifecycle and MLOps vendors such as DataRobot, Domino Data Lab, and H2O.ai have competed on integration breadth inside larger model management environments. This has created a split market in which some buyers prioritize evidence quality and regulatory recognition, while others prioritize how easily the platform connects to existing development and monitoring stacks. The EU AI Act HR compliance platform market, therefore, rewards vendors that can connect policy, technical testing, and operational workflows without forcing enterprises to rebuild the rest of their AI infrastructure.

A second competitive divide is visible in product scope. Some platforms are strongest in internal governance and audit readiness, while others are stronger in model observability, lifecycle controls, and technical evaluation at scale. That leaves clear whitespace in shared evidence hubs, candidate and worker transparency interfaces, and lighter self-service tooling for SMEs without dedicated AI governance teams. Vendors that can reduce the gap between internal compliance records and outward-facing explanation or attestation workflows are likely to strengthen their position as the market matures.

Several company moves from 2025 to 2026 showed how competition is evolving. Fiddler AI raised USD 30 million in January 2026 and framed continuous oversight as a response to AI Act logging and post-market monitoring duties, which shows how regulatory demand is shaping vendor capital narratives.[4]Fiddler AI, “Fiddler Raises USD 30M Series C to Deliver the First Control Plane for AI,” Fiddler AI Press Release, fiddler.ai LatticeFlow AI launched AI Atlas in April 2026 to connect governance frameworks with ready-to-run technical evaluations, thereby strengthening its position in evidence generation and technical credibility. Credo AI expanded through both IBM and Microsoft integrations and then moved into healthcare governance through its CHAI partnership, which shows how ecosystem alliances are being used to expand buyer reach and sector depth. ModelOp and Arthur AI also expanded their commercial access through AWS Marketplace and Google Cloud Marketplace listings, reflecting the importance of enterprise procurement channels in a category that still depends on rapid adoption within existing software budgets. These moves suggest that competitive advantage is now being built through distribution, sector specialization, and evidence automation rather than through simple claims of broad responsible AI coverage.

EU AI Act HR Compliance Platform Industry Leaders

Credo AI, Inc.

Holistic AI Limited

Fiddler AI, Inc.

ModelOp, Inc.

Monitaur, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Credo AI joined the Coalition for Health AI (CHAI) Partner Program, extending its governance platform's coverage to HIPAA, ONC HT-1, ISO 42001, and EU AI Act compliance for healthcare AI deployments. The partnership represents a deliberate vertical expansion into one of the market's fastest-growing end-use segments, targeting clinical AI governance needs that intersect HR, workforce management, and patient safety obligations simultaneously.

- April 2026: LatticeFlow AI launched AI Atlas, the first public registry of AI governance frameworks mapped to ready-to-run technical evaluations, enabling organizations to generate continuous automated compliance evidence for the EU AI Act, ISO 42001, and other regulatory frameworks. The platform targets the structural gap between static policy documentation and the verifiable technical evidence that regulators and enterprise auditors increasingly demand.

- April 2026: SD Worx, a European HR and payroll solutions provider with EUR 1.31 billion (USD 1.43 billion) in revenues in 2025, launched Legal Watch, an AI-driven regulatory monitoring platform developed in partnership with AI specialist Faktion. The initial rollout covers Germany, Luxembourg, Spain, Sweden, and the Netherlands, marking the entry of a major incumbent HR platform operator into the AI compliance software segment and signaling an intensification of competition for existing specialist vendors.

- February 2026: LatticeFlow AI published the first technical blueprint for governing Agentic AI in financial services, mapping FINMA guidance 08/2024 to measurable technical controls, including testing, monitoring, explainability, and model robustness. The blueprint targeted major European financial institutions, including Pictet, Julius Baer, and BNP Paribas, that operate on the Unique AI platform.

Global EU AI Act HR Compliance Platform Market Report Scope

The EU AI Act HR Compliance Platform Market comprises specialized platforms that enable organizations to comply with the European Union Artificial Intelligence Act's regulatory requirements in HR-related use cases. These platforms provide capabilities such as AI risk classification, transparency documentation, model monitoring, and audit reporting for AI systems used in recruitment, workforce management, and employee analytics. They ensure compliance with high-risk AI obligations, including those related to fairness, accountability, and human oversight. The market focuses on enabling organizations to deploy AI in HR securely and in accordance with EU regulatory standards.

The EU AI Act HR Compliance Platform Market Report is Segmented by Component (Software, and Services [Implementation and Integration Services, and Managed Compliance Services]), Function (AI Inventory and Classification, Policy Management and Controls Mapping, Bias and Fairness Testing, Explainability and Transparency Management, Monitoring and Incident Management, and Other Functions), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-Use Industry (Banking, Financial Services, and Insurance, Healthcare and Life Sciences, Government and Public Sector, Information Technology and Telecom, Retail and eCommerce, Manufacturing, and Other End-Use Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | |

| Services | Implementation and Integration Services |

| Managed Compliance Services |

| AI Inventory and Classification |

| Policy Management and Controls Mapping |

| Bias and Fairness Testing |

| Explainability and Transparency Management |

| Monitoring and Incident Management |

| Other Functions |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Banking, Financial Services, and Insurance |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Information Technology and Telecom |

| Retail and eCommerce |

| Manufacturing |

| Other End-Use Industries |

| North America | |

| South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | |

| Middle East | |

| Africa |

| By Component | Software | |

| Services | Implementation and Integration Services | |

| Managed Compliance Services | ||

| By Function | AI Inventory and Classification | |

| Policy Management and Controls Mapping | ||

| Bias and Fairness Testing | ||

| Explainability and Transparency Management | ||

| Monitoring and Incident Management | ||

| Other Functions | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-Use Industry | Banking, Financial Services, and Insurance | |

| Healthcare and Life Sciences | ||

| Government and Public Sector | ||

| Information Technology and Telecom | ||

| Retail and eCommerce | ||

| Manufacturing | ||

| Other End-Use Industries | ||

| By Geography | North America | |

| South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | ||

| Middle East | ||

| Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the EU AI Act HR compliance platform space?

The EU AI Act HR compliance platform market was valued at USD 1.61 billion in 2025, stood at USD 1.94 billion in 2026, and is projected to reach USD 5.07 billion by 2031 at a 21.18% CAGR.

What is driving adoption of HR AI compliance platforms in Europe?

Adoption is being driven by the AI Act’s high-risk classification for HR use cases, deployer obligations under Article 26, and penalties of up to EUR 15 million (USD 16.35 million) or 3% of global annual turnover.

Which component is growing faster, software or services?

Software led with a 67.39% share in 2025, but services are growing faster and are projected to expand at a 23.49% CAGR through 2031 because implementation and ongoing compliance management remain critical.

Which deployment model is most used for HR AI compliance tools?

Cloud led with a 62.44% share in 2025 because buyers need fast regulatory updates and centralized evidence management, while hybrid is growing fastest at a 23.12% CAGR.

Which type of customer is creating the most new demand?

Large enterprises led with a 71.22% share in 2025, but SMEs are the fastest-growing buyer group at a 23.85% CAGR as supplier due diligence and customer attestation demands spread through value chains.

Which regions and industries offer the strongest growth opportunities?

Europe led with a 38.71% share in 2025, while Asia-Pacific is projected to grow fastest at 22.67% CAGR. By end use, IT and telecom led with 29.31% share, while healthcare and life sciences is projected to grow fastest at 21.56% CAGR.

Page last updated on: