Workflow Automation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

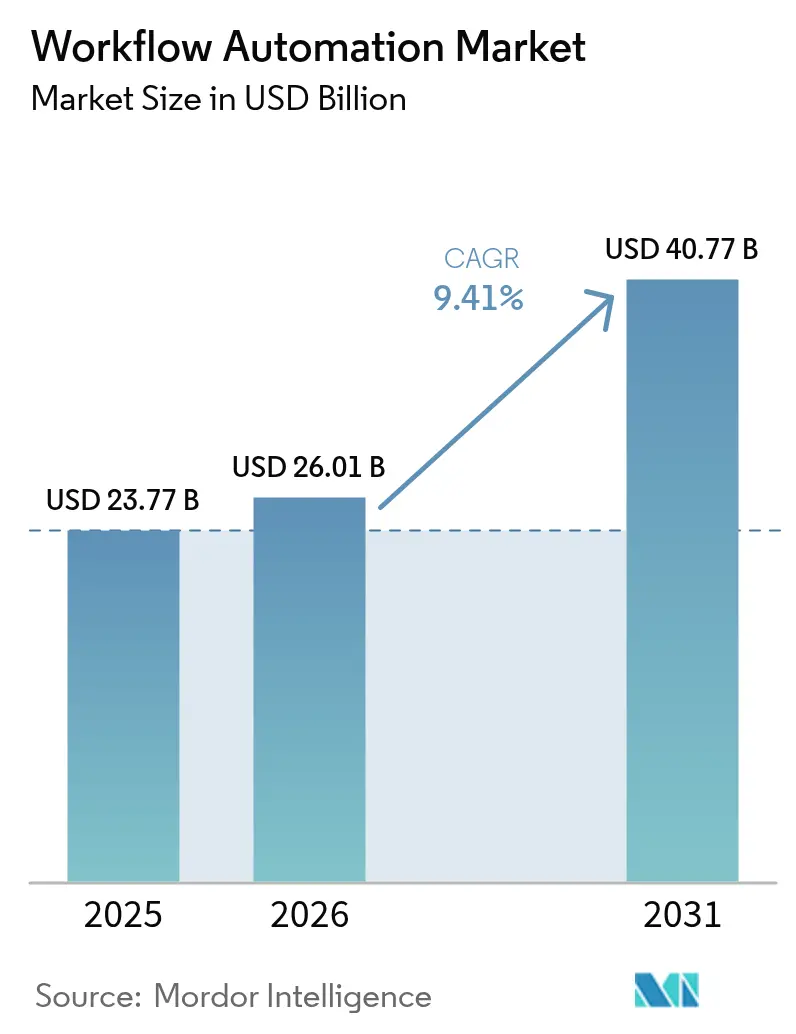

| Market Size (2026) | USD 26.01 Billion |

| Market Size (2031) | USD 40.77 Billion |

| Growth Rate (2026 - 2031) | 9.41% CAGR |

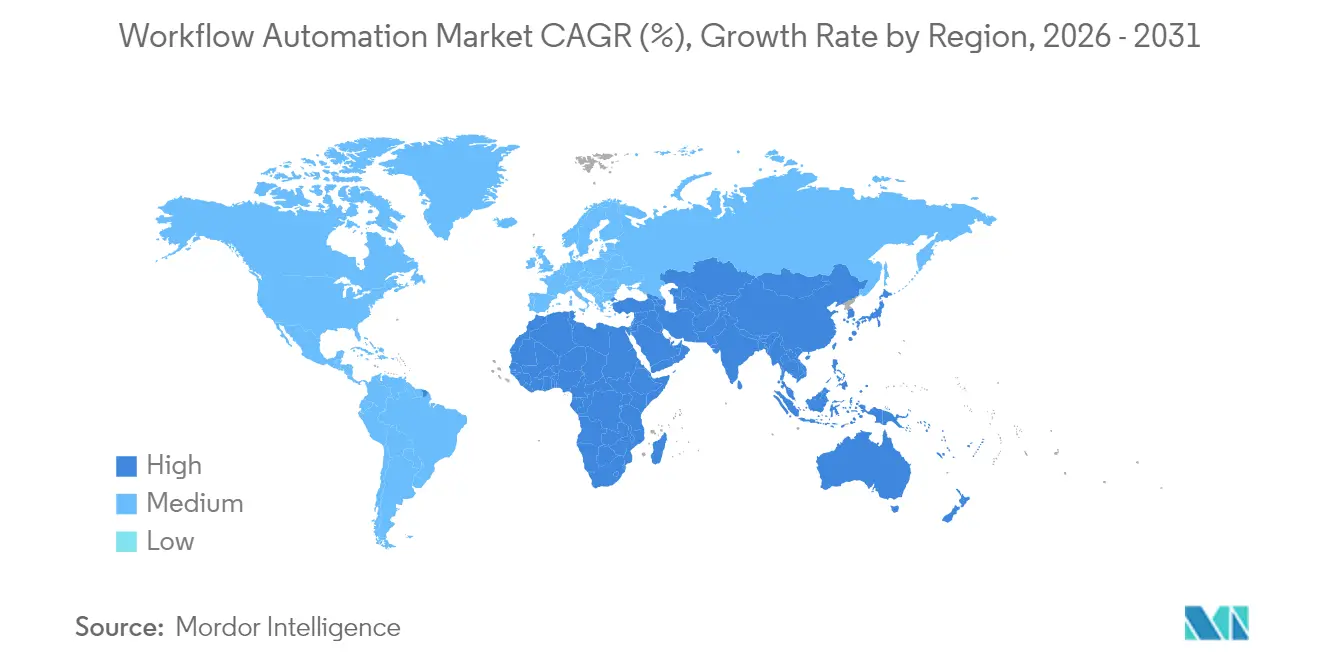

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Workflow Automation Market Analysis by Mordor Intelligence

The workflow automation market size was valued at USD 23.77 billion in 2025 and estimated to grow from USD 26.01 billion in 2026 to reach USD 40.77 billion by 2031, at a CAGR of 9.41% during the forecast period (2026-2031). Momentum stems from rising enterprise digitalization budgets, real-time edge workflows, and the fusion of artificial intelligence with robotic process automation. Vendors are packaging low-code design, process mining, and orchestration into unified suites, permitting faster deployments across finance, healthcare, and manufacturing. Cloud-first strategies remain dominant, but hybrid models are accelerating as regulators tighten data-sovereignty rules. Competitive intensity is steady: large platform providers defend share through vertical templates while specialist vendors target underserved edge and compliance niches.

Key Report Takeaways

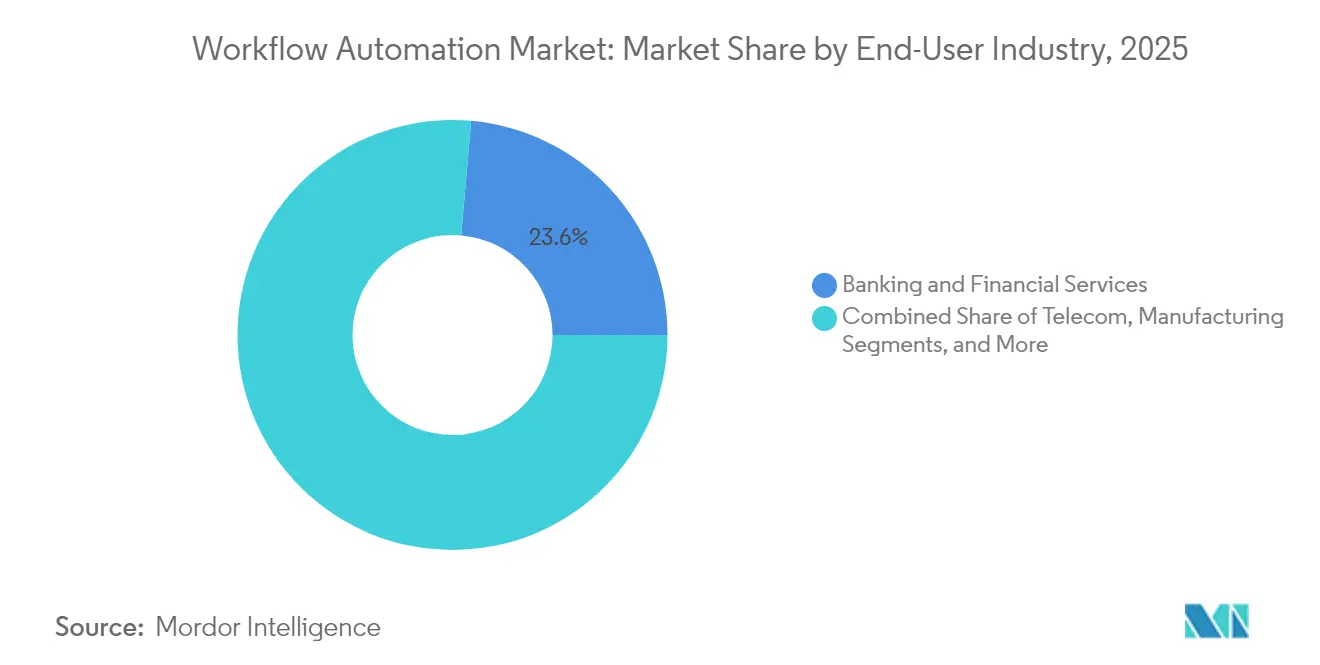

- By end-user industry, Banking and Financial Services held a 23.62% workflow automation market share in 2025, whereas Healthcare and Pharmaceuticals is projected to compound at an 11.22% CAGR through 2031.

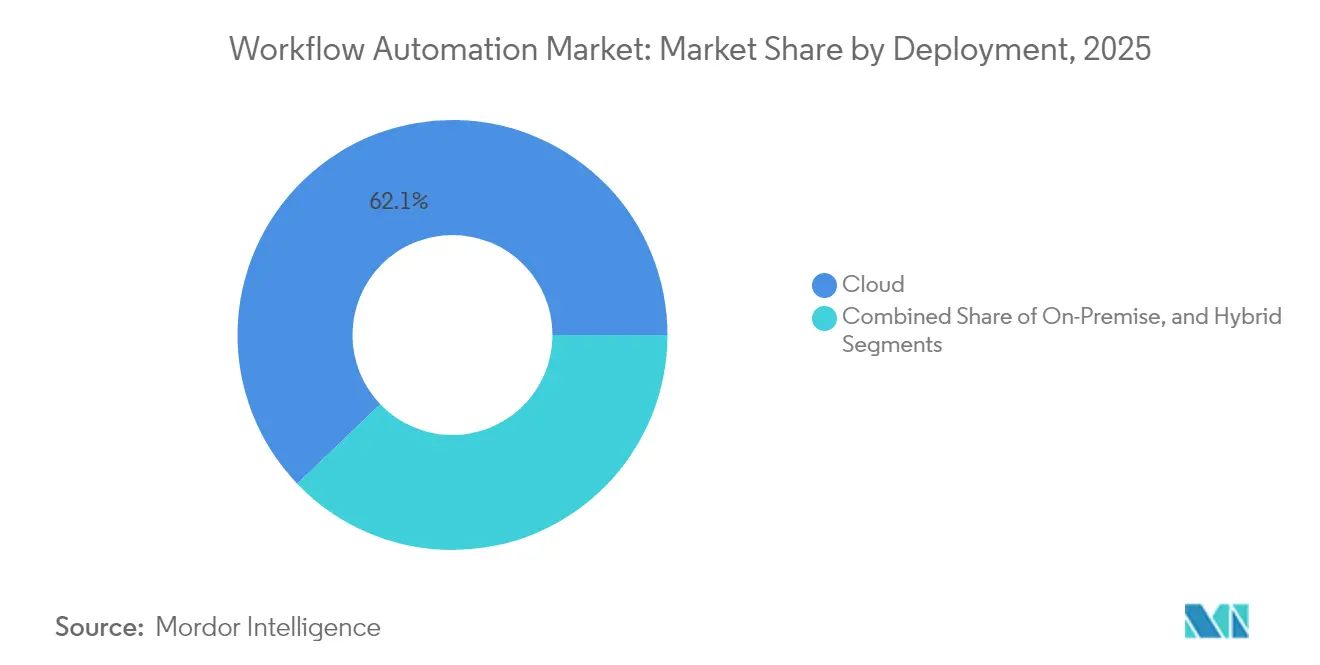

- By deployment, cloud captured 62.15% of the workflow automation market size in 2025, while hybrid configurations are expected to expand at a 10.08% CAGR between 2026-2031.

- By solution, software platforms commanded 66.55% revenue share of the workflow automation market size in 2025, and robotic process automation software is forecast to rise at a 9.95% CAGR through 2031.

- By organization size, large enterprises generated 71.05% of revenue in 2025, but small and medium-sized enterprises are on track for a 10.19% CAGR over the outlook period.

- By geography, North America contributed 34.22% of global revenue in 2025; Asia Pacific is expected to post the fastest regional CAGR at 9.92% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Workflow Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of IoT-enabled edge workflows | +2.1% | Global ⁄ early gains in North America and Asia Pacific hubs | Medium term (2-4 years) |

| Rise in implementation of robotic process automation in business process management | +1.8% | Global ⁄ strongest in North America and Europe finance | Short term (≤ 2 years) |

| Growing demand for low-code ⁄ no-code development platforms | +1.6% | Global ⁄ robust in SME segments | Short term (≤ 2 years) |

| Convergence of workflow automation with generative AI copilots | +2.3% | North America and Europe lead ⁄ Asia Pacific follows | Medium term (2-4 years) |

| Operational resilience mandates in highly regulated sectors | +1.4% | Europe, North America, Asia Pacific | Long term (≥ 4 years) |

| Expansion of 5G private networks enabling real-time industrial automation | +1.2% | Asia Pacific core, spill-over to other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of IoT-Enabled Edge Workflows

Real-time processing at the data source is removing latency barriers that previously hampered machine-critical automation. Manufacturers leverage local compute to analyze sensor streams in milliseconds, cutting scrap rates and scheduling predictive maintenance without waiting on centralized clouds. Mining operators deploy edge nodes that trigger automated safety shutdowns when gas or vibration thresholds spike, satisfying stringent IEC 61508 mandates. Logistics hubs combine 5G private networks with edge orchestration, letting autonomous mobile robots navigate dynamic warehouse layouts without connectivity delays. Healthcare providers embed edge analytics into bedside monitors so clinical alerts fire instantly, improving patient outcomes and easing nurse workloads. These gains reinforce capital investment in ruggedized gateways and containerized orchestration stacks that extend the workflow automation market deeper into operational technology footprints.[1]FlowForma, “The Automated Processes of the Mining Industry,” flowforma.com

Convergence of Workflow Automation with Generative AI Copilots

Generative AI is elevating automation from rule-based scripting to context-aware decision support. Financial institutions deploy copilots that parse regulatory bulletins, map clauses to business controls, and auto-configure approval chains, trimming weeks from compliance cycles while preserving auditability.[2]Microsoft Corporation, “Accelerating Copilot Across the Power Platform,” microsoft.comHospitals feed unstructured clinical notes into large language models that flag sepsis risk, launch care-path workflows, and redact protected health information to uphold HIPAA safeguards. Insurers use document understanding engines to extract key terms from multilingual policies, then route exceptions to underwriters only when human judgment adds value. Early pilots report 40-60% productivity boosts across knowledge tasks, but firms must enforce model-governance, bias-mitigation, and explainability frameworks before scaling beyond sandbox environments.

Growing Demand for Low-Code ⁄ No-Code Development Platforms

Citizen developers now design procurement, accounts-receivable, and HR workflows without deep programming skills, shrinking deployment cycles from months to days. Small manufacturers adopt subscription-based builders that bundle templates, connectors, and role-based access, eliminating hefty upfront licenses. Large enterprises encourage business units to prototype flows in sandboxes governed by IT-managed guardrails that enforce encryption, data-loss-prevention, and rollback controls. Vendors supplement drag-and-drop tooling with AI-guided suggestions that auto-generate integrations, further lowering barriers. These dynamics expand the workflow automation market into previously untapped long-tail use cases while shifting professional developers toward complex orchestration and governance work.[3]Kissflow Inc., “Workflow Automation for Small Business 2025,” kissflow.com

Rise in Implementation of Robotic Process Automation in Business Process Management

RPA has evolved from screen scraping into enterprise-grade orchestration capable of spanning legacy cores, SaaS suites, and mainframes. Banks employ attended bots that collect KYC evidence, cross-check sanctions lists, and populate onboarding systems, driving 70% cycle-time cuts and error rates below manual norms.[4]CFB Bots, “RPA for SME,” cfb-bots.comHealthcare providers automate claims adjudication, scheduling, and reporting, achieving 90% accuracy improvements. Integrating RPA with process-mining dashboards exposes bottlenecks, letting teams prioritize high-ROI candidates. Success hinges on robust exception handling, version control, and change-management programs that prevent unforeseen system updates from crippling automated processes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data security and privacy concerns within multi-tenant cloud | -1.8% | Global ⁄ acute in Europe and regulated verticals | Medium term (2-4 years) |

| Shortage of process-mining skill sets to scope automation projects | -1.5% | Global ⁄ most severe in North America and Europe | Short term (≤ 2 years) |

| Legacy system integration complexity in brownfield enterprises | -1.2% | Global ⁄ concentrated in mature IT landscapes | Long term (≥ 4 years) |

| Budget compression amid macro-economic uncertainty | -1.1% | Global with cyclical intensity | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Security and Privacy Concerns Within Multi-Tenant Cloud

Enterprises handling financial and health records face heightened breach risks when workflows run on shared stacks. European controllers demand GDPR alignment, compelling vendors to embed consent tracking, data-minimization, and erase-on-request functions. Financial institutions preparing for Digital Operational Resilience Act compliance insist on granular audit trails, encryption in transit and at rest, and continuous vulnerability scans. Many firms therefore adopt hybrid architectures that stage sensitive data on-premises while leveraging cloud analytics layers. Vendor roadmaps emphasize FedRAMP, ISO 27001, and SOC 2 certifications, plus region-specific data-residency options that place replicas inside sovereign clouds.[5]Relyance AI, “When Spending Money Will Save You Money,” relyance.ai

Shortage of Process-Mining Skill Sets to Scope Automation Projects

Process mining reveals hidden throughput gaps, yet qualified professionals who can extract logs, cleanse data, and interpret patterns remain scarce. Organizations struggle to build credible ROI cases, delaying funding approvals and narrowing project pipelines. Hospitals need analysts versed in both BPMN and clinical operations; manufacturers require expertise spanning ERP, MES, and Six Sigma. To bridge gaps, firms engage managed service partners or outsource diagnostics, but this can curb internal capability building and raise long-term costs. Vendors are releasing self-service discovery modules with AI-guided insights, though governance teams still need specialists to validate findings and prioritize initiatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Leadership Propels Hybrid Upswing

Cloud-hosted offerings generated 62.15% of revenue in 2025, underscoring the preference for elastic scaling and subscription pricing. Vendors bundle AI services and pre-built connectors, letting clients pilot flows in hours. Financial services, retail, and healthcare gravitate toward cloud to avoid hardware refresh cycles and to tap rapid innovation. Yet rising scrutiny from regulators and boards sparks a shift to hybrid, now pacing at a 10.08% CAGR. Here, sensitive data remains on-premises while orchestration tiers run in vendor clouds, balancing sovereignty with agility. The workflow automation market size for hybrid architectures is expanding as 5G edge nodes route latency-critical tasks locally, then sync analytics upstream. Vendors augment platforms with policy-based routing that assigns each process instance to cloud or edge based on data classification and performance targets.

Hybrid adoption broadens as public sector agencies and defense primes demand demonstrable control over encryption keys and audit logs. Integrated management dashboards unify visibility across zones, easing compliance reporting. On-premises deployments persist in nuclear, defense, and air-gapped plants where air-gap and zero-trust postures are mandatory. Edge appliances certified to ISO 27001 run containerized orchestration engines, letting factories maintain autonomous operations during network outages. Over the forecast span, workload portability, confidential computing, and sovereign-cloud alliances will embed flexibility, but cost-benefit analysis will continue to favor cloud for non-regulated workloads.

By Solution: Software Platforms Anchor RPA Innovation

Software platforms accounted for 66.55% of 2025 spending, bundling workflow orchestration, RPA, event streaming, and AI inference in cohesive suites. The segment’s dynamism lies in the infusion of large language models, enabling bots to comprehend free-text instructions and auto-generate API calls. This evolution positions RPA as the fastest-growing sub-segment, rising at 9.95% CAGR as enterprises revisit previously unautomatable exception handling. Vendors expose model ops consoles that monitor drift, retrain models, and enforce responsible-AI principles, features becoming purchase prerequisites for regulated buyers.

Services held 33.45% of value, anchored by system integration and change-management engagements that ensure cross-system data coherence. Process-mining assessments feed backlog roadmaps, while managed-service contracts guarantee outcome-based SLAs for clients lacking domain talent. Consulting arms increasingly verticalize offerings, delivering DORA compliance accelerators for banks or GMP-validated templates for pharmaceutical plants. As the workflow automation market grows, co-innovation partnerships between hyperscalers and boutique integrators will amplify, combining global reach with domain depth.

By End-User Industry: Finance Dominates, Healthcare Accelerates

Banking and Financial Services retained 23.62% revenue share in 2025, reflecting transaction volumes and stringent compliance overheads that favor automation. Institutions leverage bots for anti-money-laundering investigations, loan disbursements, and straight-through settlements. DORA preparation commands additional spend on continuity orchestration, cyber-event playbooks, and supplier-risk dashboards. The workflow automation market size for healthcare and pharmaceuticals is advancing the fastest, at 11.22% CAGR, as electronic health record mandates and clinical trial digitization intensify. Automated prior-authorization, e-signature capture, and pharmacovigilance reporting free clinicians to focus on patient care while meeting regulatory filing windows.

Manufacturing remains pivotal, integrating workflow engines with IoT sensors and quality-management systems to streamline shop-floor decisions. Retail, logistics, and utilities deploy automation to stabilize supply chains, respond to demand volatility, and comply with environmental reporting. Government agencies adopt citizen-service portals powered by back-office orchestration that slashes manual paperwork and accelerates benefit disbursements, yet they grapple with legacy interoperability constraints.

By Organization Size: SME Momentum Outpaces Enterprise Scale

Large enterprises delivered 71.05% of revenue in 2025, driven by cross-domain initiatives that weave workflows through finance, HR, ITSM, and customer experience platforms. Their deployments involve multi-year roadmaps, center-of-excellence governance, and complex change-management. However, the 10.19% CAGR logged by small and medium-sized enterprises through 2031 signals democratization. Low-code suites, pay-as-you-grow tiers, and template libraries enable SMEs to automate procure-to-pay, CRM updates, and compliance filings without large IT staff. Vendors court this base with usage-based pricing and managed-service bundles that guarantee uptime and security patching.

Partnership ecosystems with regional integrators and value-added distributors extend vendor reach into local markets, offering language localization and sector expertise. Government grant programs supporting digital adoption, such as Enterprise Singapore’s Enterprise Development Grant, offset capital barriers. As SMEs mature, they adopt hybrid governance, instituting light-weight approval gates to prevent runaway shadow IT and ensure audit readiness.

Geography Analysis

North America contributed 34.22% of global revenue in 2025 as enterprises accelerated cloud migration and AI adoption under stable regulatory oversight. Financial institutions implemented end-to-end onboarding workflows compliant with SOX and Dodd-Frank, while manufacturers embedded edge nodes to enhance production resilience. U.S. vendors anchor local ecosystems, offering early-access betas that encourage experimentation. Canada’s public sector digitization programs further underwrite regional demand, especially for citizen-service portals.

Asia Pacific is expanding at a 9.92% CAGR, propelled by manufacturing digitization, e-commerce growth, and favorable government incentives. China’s dual-circulation strategy drives factories to embed workflow engines for supply-chain visibility, whereas India’s Make-in-India campaign spurs SMEs to adopt low-code tools. Japan and South Korea prioritize 5G-enabled smart factories, integrating edge orchestration with industrial robots to curb labor shortages. Southeast Asian nations deploy cloud-native platforms hosted in regionally-compliant data centers, raising adoption among mid-market firms.

Europe ranks third by revenue but exhibits strong compliance-driven uptake. DORA’s 2025 deadlines catalyze bank spending on continuity orchestration, while GDPR fosters demand for built-in consent management. Germany’s Industrie 4.0 tailwinds support manufacturing workflows, and the United Kingdom’s NHS invests in process mining to optimize care pathways. Data-residency requirements encourage hybrid implementations, with sovereign-cloud regions from hyperscalers gaining traction. The Middle East and Africa and Latin America remain nascent but display rising interest as telecom operators roll out 5G and governments digitize public services.

Competitive Landscape

Competition is moderately concentrated, with the top five suppliers holding roughly 35% of global revenue. Microsoft, IBM, and ServiceNow embed workflow engines into broader cloud and productivity suites, leveraging install bases to defend share. UiPath, Celonis, and Automation Anywhere focus on RPA and process-intelligence depth, acquiring niche startups to widen capability gaps. Celonis’s 2024 purchase of PAF bolstered AI-driven mining, while UiPath’s multilingual document understanding adds vertical reach. Vendors differentiate via open APIs, BPMN-2.0 compliance, and multi-model AI orchestration that allows plug-in of third-party LLMs.

Strategic thrusts skew toward industry templates and compliance accelerators. Banks adopt DORA packs that pre-configure incident response workflows, while pharma clients seek GxP-aligned validation blueprints. Edge workflow enablement remains white space, with only a handful of providers offering containerized runtimes certified for rugged industrial PCs. Low-code vendors like Zapier and Kissflow target SMB sweet spots, combining ease-of-use and community-driven templates. Hyperscalers partner with specialist ISVs to co-sell domain solutions, while channel alliances with regional system integrators expand service wraparounds.

Pricing models migrate from user-based tiers to consumption or outcome-linked contracts. Clients increasingly evaluate total automation value delivered per hour saved rather than license counts. AI augmentation, governance toolkits, and analytical dashboards stand out as purchase criteria. Over the outlook horizon, consolidation is expected as platform breadth trumps point capabilities, yet innovative startups will persist by pioneering vertical micro-flows, privacy-preserving edge agents, and trust-layer overlays for regulated data.

Workflow Automation Industry Leaders

IBM Corporation

Oracle Corporation

Pegasystems, Inc

Xerox Corporation

Appian Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Nintex rolled out offline-capable mobile workflows for field teams in manufacturing and logistics scenarios.

- January 2025: Microsoft introduced Copilot AI features across Power Platform to enable natural-language workflow design, reducing build time for non-technical users.

- December 2024: Celonis finalized the acquisition of Process Analytics Factory, expanding process-mining depth and real-time insights.

- December 2024: IBM integrated Watson Orchestrate with its workflow suite, offering AI task recommendations for knowledge workers.

Global Workflow Automation Market Report Scope

Workflow automation tools allow a business function to automate repeatable tasks using a set of directives or workflows that form the basis of the operation. Over the last few years, the concept has evolved considerably with the emergence of RPA, BPM suites, Remote Desktop Automation, and custom scripting. The main objective is identifying repetitive tasks or any manual process that software, apps, or tech could handle better.

The workflow automation industry is segmented by solution (software and services), by end-user industry (banking, telecom, retail, manufacturing and logistics, healthcare and pharmaceuticals, energy and utilities, and other end-user industries), by deployment (cloud and on-premise), and by geography (North America, Europe, Asia-Pacific, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| On-premise |

| Cloud |

| Hybrid |

| Software | Workflow Orchestration Platforms |

| Business Process Management Suites | |

| RPA Platforms | |

| Services | Consulting and Advisory |

| Implementation and Integration | |

| Managed Services |

| Banking and Financial Services |

| Telecom |

| Retail and E-commerce |

| Manufacturing |

| Logistics and Transportation |

| Healthcare and Pharmaceuticals |

| Energy and Utilities |

| Government and Public Sector |

| Other End-user Industries |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Deployment | On-premise | |

| Cloud | ||

| Hybrid | ||

| By Solution | Software | Workflow Orchestration Platforms |

| Business Process Management Suites | ||

| RPA Platforms | ||

| Services | Consulting and Advisory | |

| Implementation and Integration | ||

| Managed Services | ||

| By End-user Industry | Banking and Financial Services | |

| Telecom | ||

| Retail and E-commerce | ||

| Manufacturing | ||

| Logistics and Transportation | ||

| Healthcare and Pharmaceuticals | ||

| Energy and Utilities | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the workflow automation market in 2031?

The market is forecast to reach USD 40.77 billion by 2031.

Which region is expected to witness the fastest growth through 2031?

Asia Pacific is projected to expand at a 9.92% CAGR, driven by manufacturing modernization and digital infrastructure investments.

Which deployment model is growing the quickest?

Hybrid deployment is rising at a 10.08% CAGR as enterprises balance data sovereignty with cloud scalability.

Why are healthcare organizations accelerating adoption?

Clinical digitization mandates and the need for compliant, patient-centric workflows are propelling hospital and pharmaceutical uptake at an 11.22% CAGR.

How are vendors differentiating their offerings?

Providers compete on integrated AI, process mining depth, vertical compliance templates, and low-code ease of use to shorten time-to-value.

What security features are enterprises demanding from vendors?

Buyers seek end-to-end encryption, granular audit trails, region-specific data residency, and certifications such as ISO 27001 and SOC 2 to satisfy regulatory mandates.

Page last updated on: