Compliance Training Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

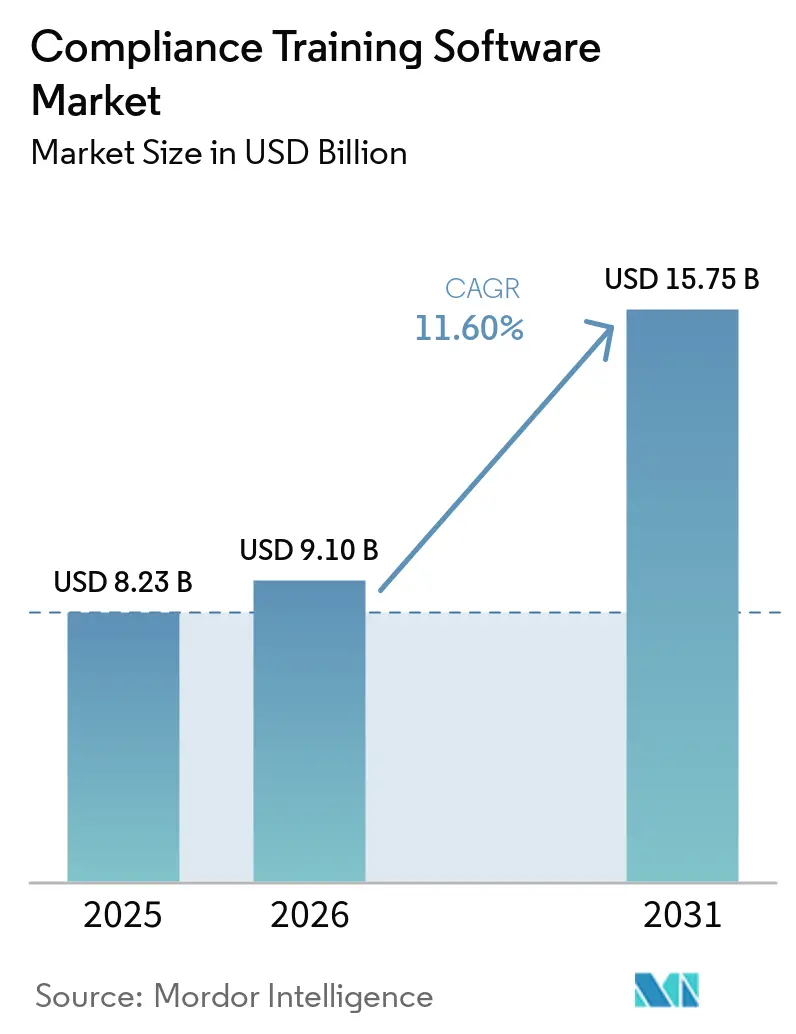

| Market Size (2026) | USD 9.10 Billion |

| Market Size (2031) | USD 15.75 Billion |

| Growth Rate (2026 - 2031) | 11.60% CAGR |

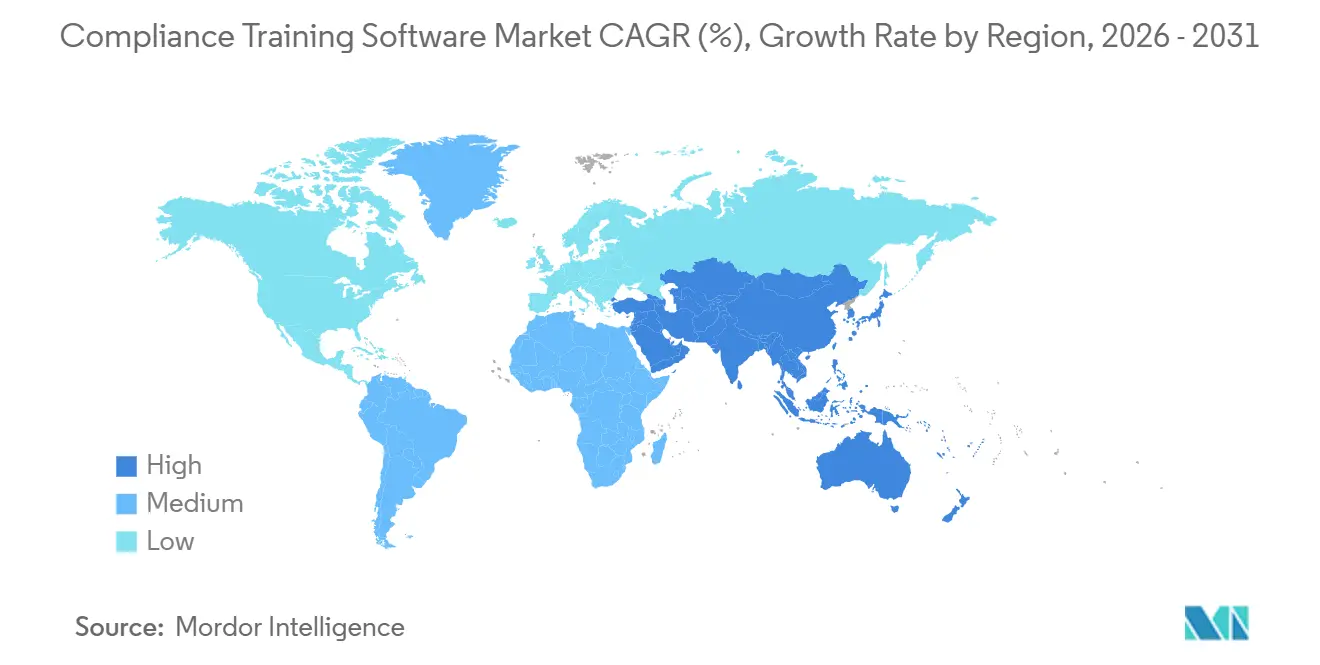

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

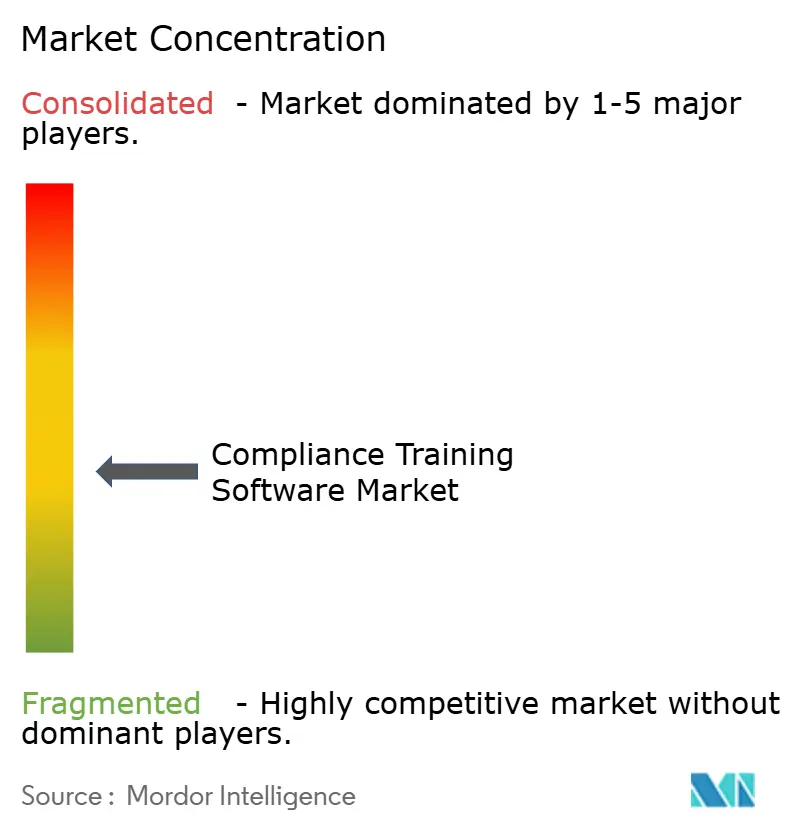

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compliance Training Software Market Analysis by Mordor Intelligence

The compliance training software market size is projected to be USD 8.23 billion in 2025, USD 9.10 billion in 2026, and reach USD 15.75 billion by 2031, growing at a CAGR of 11.60% from 2026 to 2031. Growth in the compliance training software market reflects a broader shift in how companies manage regulatory readiness, with training now treated as an ongoing risk-control rather than a periodic administrative task. Data privacy rules, workplace conduct requirements, cybersecurity obligations, and emerging AI governance standards are all pushing employers to use systems that can update content quickly, measure completion, and maintain clear records. The spread of cloud deployment has reduced delivery friction across the compliance training software market, while mobile-first learning design has made training easier to reach for frontline, remote, and shift-based workers. Vendors in the compliance training software market are also moving beyond static course libraries and investing in AI tools that turn internal policies into role-based learning content more quickly. At the same time, opportunities remain strongest where organizations need jurisdiction-specific assignment logic, audit-ready documentation, and easier adoption among mid-sized firms that still face tight compliance budgets.

Key Report Takeaways

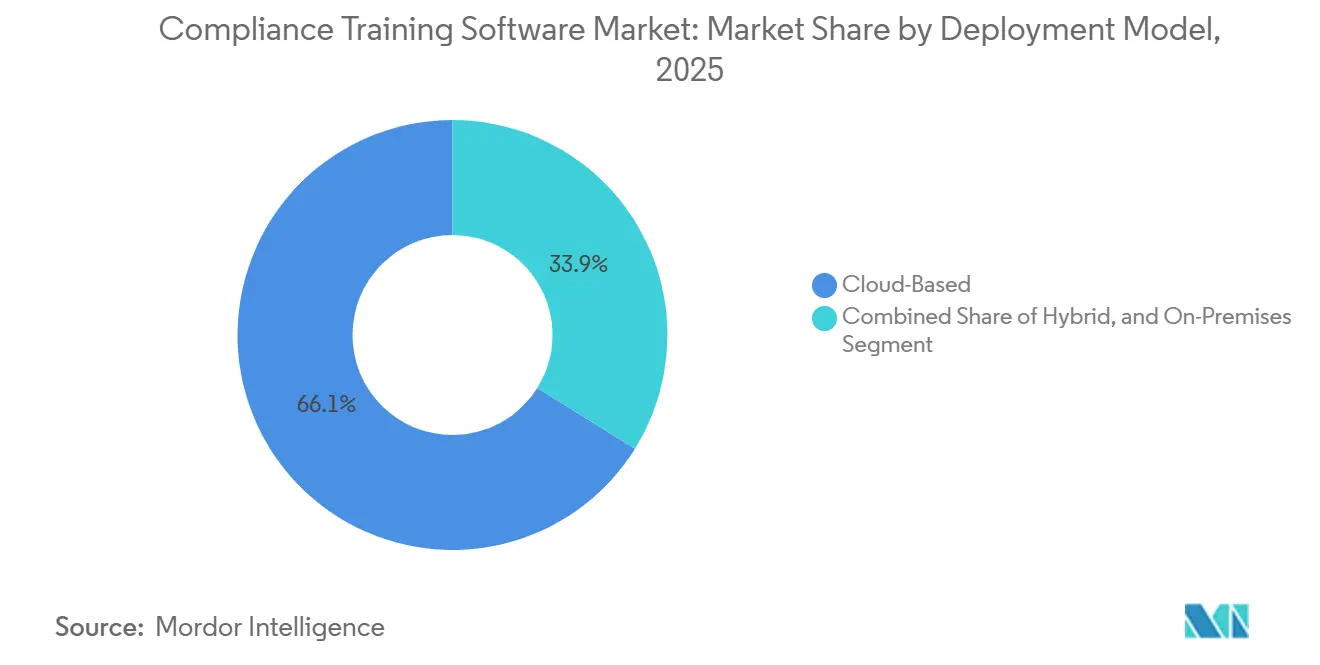

- By deployment model, cloud-based deployment held a 66.12% share of the compliance training software market in 2025, while hybrid deployment is projected to grow at a 14.67% CAGR from 2026 to 2031.

- By delivery mode, online delivery accounted for 72.74% of the market share in 2025, while blended learning is forecast to expand at a 13.84% CAGR through 2031.

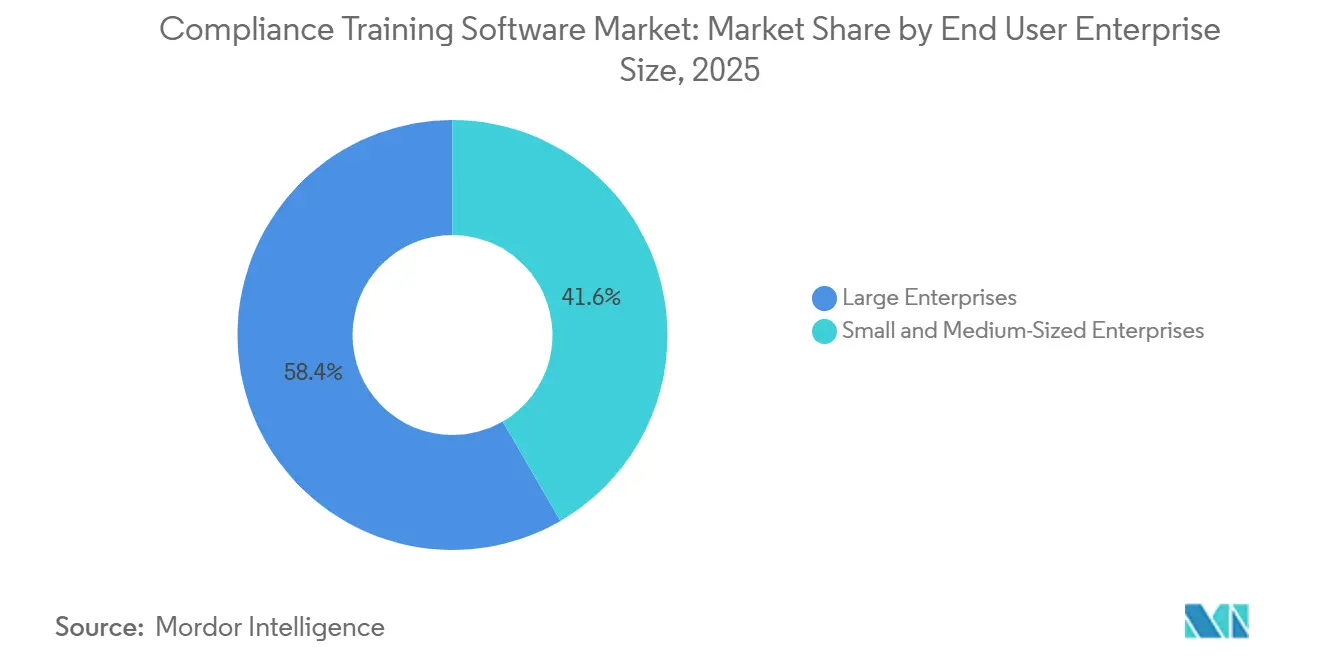

- By enterprise size, large enterprises held 58.37% share in 2025, while SMEs are projected to record the highest CAGR at 14.92% through 2031.

- By training type, cybersecurity and information security training led with 26.37% share in 2025, while data privacy and protection training is projected to grow at a 14.11% CAGR from 2026 to 2031.

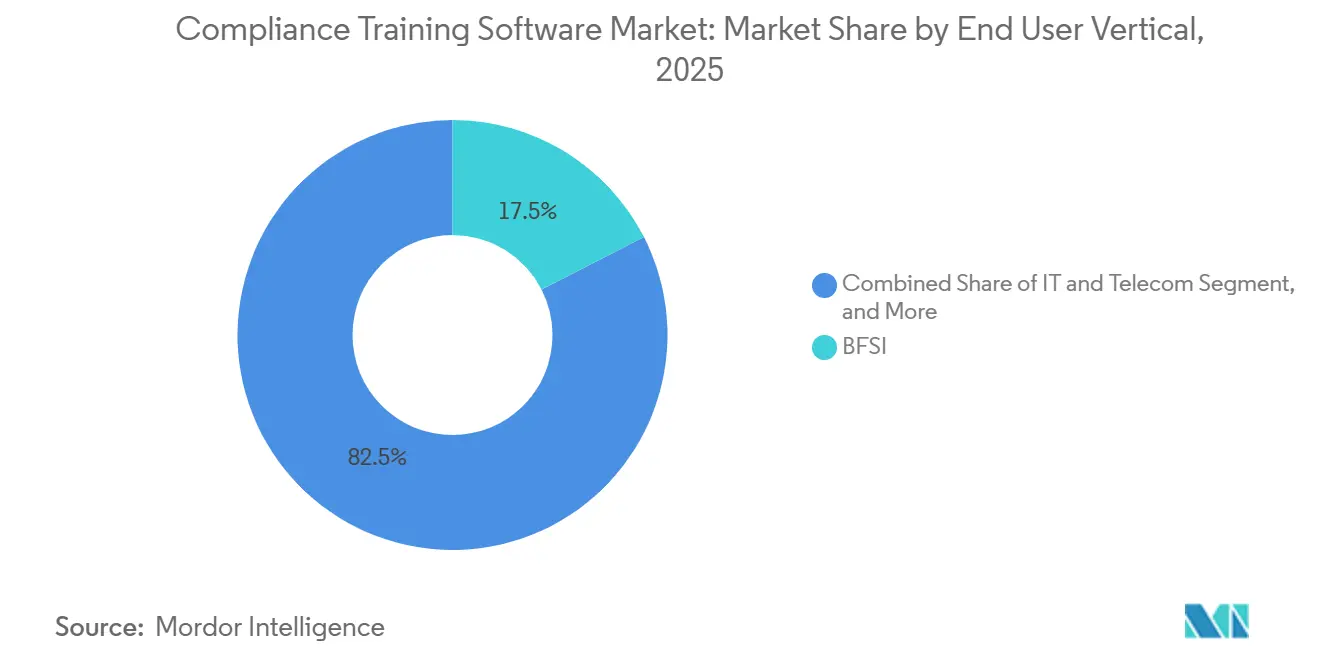

- By end-user vertical, BFSI captured 17.47% share in 2025, while IT and telecom are forecast to grow at a 13.76% CAGR through 2031.

- By geography, North America held 36.88% share in 2025, while Asia-Pacific is projected to expand at a 14.39% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Compliance Training Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Data Privacy And Cybersecurity Enforcement | +4.2% | Global, concentrated in North America and Europe, with growing enforcement in Asia-Pacific and the Middle East | Short term (≤ 2 years) |

| Expansion Of Mandatory Workplace Conduct And Harassment Training | +2.8% | North America and Europe core, spill-over to Asia-Pacific and South America | Medium term (2-4 years) |

| Shift Toward Cloud-Based And Mobile Learning Delivery | +2.4% | Global, rapid adoption in North America, Asia-Pacific core, with early gains in the Middle East | Short term (≤ 2 years) |

| Greater Need For Audit-Ready Tracking, Certification, And Reporting | +1.8% | Global, with core demand in North America and Europe, and early gains in Australia, Singapore, and the UAE | Short term (≤ 2 years) |

| Artificial Intelligence Literacy And Responsible Use Training Requirements | +1.5% | Europe, North America, spill-over to Asia-Pacific and South America | Medium term (2-4 years) |

| Workplace Violence Prevention Mandates Expanding Training Scope | +0.9% | North America core, early gains in Australia and Singapore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Data Privacy And Cybersecurity Enforcement

The compliance training software market is gaining momentum from the rapid expansion of privacy and cybersecurity enforcement across multiple jurisdictions. Twenty U.S. states had comprehensive privacy laws in effect as of January 2026, and 8 of those laws took effect in 2025, making the compliance environment harder to manage with static training programs alone.[1]O'Melveny and Myers LLP, “2026 Data Security and Privacy Compliance Checklist: Key US State Law Updates, AI Rules, COPPA Changes, and Global Data Protection Risks,” O'Melveny and Myers LLP, omm.com The U.S. Department of Defense formalized the Cybersecurity Maturity Model Certification final rule in November 2025, which extended cybersecurity training needs deeper into the defense supply chain and widened the pool of organizations that need structured programs. NIST Cybersecurity Framework 2.0 also expanded governance to a broader enterprise context, requiring training to reach legal, communications, operational, and executive roles rather than remaining within IT teams. As privacy regulators across states coordinate investigations more closely, the compliance training software market is benefiting from demand for platforms that can assign location-based content, track role-specific obligations, and document completion across multiple rule sets simultaneously.

Expansion Of Mandatory Workplace Conduct And Harassment Training

The broader adoption of mandatory workplace conduct and harassment training across U.S. jurisdictions also supports the compliance training software market. State obligations now cover employees in at least 14 jurisdictions, while many other states strongly encourage formal programs, which increases demand for systems that can handle different rules on timing, duration, and recordkeeping.[2]Jon Davis, “2026 Sexual Harassment Training Requirements by State,” OnPay, onpay.com Washington State expanded mandatory training to include isolated hotel, motel, retail, and security guard employees on January 1, 2026, demonstrating how training rules are becoming more sector-specific over time. The U.S. Equal Employment Opportunity Commission continues to receive more than 25,000 workplace harassment complaints annually, which keeps pressure on employers to demonstrate that training is structured and well-documented rather than occasional and informal. In this setting, the compliance training software market is seeing stronger demand for centralized platforms that can manage different jurisdictional rules, retain records, and support measurable training outcomes over time.

Shift Toward Cloud-Based And Mobile Learning Delivery

The compliance training software market has moved steadily toward cloud-based delivery because regulatory content changes too frequently for manual updates to remain practical. Cloud platforms can connect with HRIS and GRC systems, which lets training assignments respond quickly to new hires, role changes, or policy updates without long implementation cycles. Mobile delivery has expanded access across deskless and shift-based workforces in logistics, retail, healthcare, and manufacturing, where traditional learning formats often missed large employee groups. Harmony AI capabilities are designed to identify at-risk learners and reduce training gaps through more targeted remediation, reflecting the wider push toward context-aware learning in the compliance training software market. This shift favors cloud-native vendors that can combine automatic updates, broader accessibility, and scalable administration within a single environment.

Greater Need For Audit-Ready Tracking, Certification, And Reporting

The compliance training software market is also expanding because regulators increasingly look beyond whether training was assigned and ask whether records are secure, time-stamped, role-specific, and tied to the correct policy version. The proposed 2026 HIPAA Security Rule update would formalize annual training, extend record retention to 6 years, and require a stronger linkage between completion records and the relevant policy version. FDA-regulated environments already face strict expectations under 21 CFR Part 11, which makes manual recordkeeping much harder to defend during inspections. Cloud LMS deployments usually take 3 to 9 months, while on-premises projects often take 6 to 12 months, which highlights why organizations under regulatory deadlines are choosing faster, audit-ready systems. As a result, the compliance training software market is being shaped by demand for defensible records that help companies during audits, investigations, civil disputes, and insurance reviews.[3]LMS for Compliance Training: How to Track Completion, Prove Regulatory Compliance, and Choose the Right System,” Selleo, selleo.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Training Fatigue And Low Learner Engagement | -1.3% | Global | Short term (≤ 2 years) |

| Budget Constraints Among Small And Medium-Sized Enterprises | -0.8% | Global, pronounced in South America, Africa, and Southeast Asia | Long term (≥ 4 years) |

| Localization And Legal Review Bottlenecks Across Jurisdictions | -0.5% | Particularly in Asia-Pacific, Middle East, and Africa | Medium term (2-4 years) |

| Pushback On Sensitive Culture, Conduct, And Inclusion Content | -0.3% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Training Fatigue And Low Learner Engagement

The compliance training software market still faces a meaningful adoption challenge because many employees approach mandatory training as a legal requirement rather than a useful part of daily work. Research found that 72% of organizations cited learner engagement as their main challenge in virtual training, while only 27% viewed their virtual instructor-led training as highly effective.[4]eLearning Industry and Adobe Connect, “Addressing the Learner Engagement Gap in Virtual Training: How to Build an Action Plan and Leverage the Latest Technologies,” Adobe, adobe.com Completion rates on self-directed platforms can fall sharply when content feels disconnected from real work situations. This weakens both knowledge retention and the perceived value of software renewals, even when formal completion rates look acceptable on paper. The compliance training software market is responding with microlearning, gamified formats, and scenario-based tools, but learner fatigue remains a real drag on sustained program effectiveness.

Budget Constraints Among Small And Medium-Sized Enterprises

The compliance training software market also runs into budget pressure among smaller firms that face growing obligations without the staff or systems of larger employers. Small business compliance spending estimates for 2025 showed a much higher per‑employee burden at very small firms than at large enterprises, which helps explain why premium software adoption remains harder in this part of the market. Compliance‑related software costs had risen 45% since 2020, adding another layer of pressure for SMEs operating in regulated settings. Many of these organizations also lack dedicated compliance staff, legal review support, and internal IT resources, so the cost problem extends beyond license fees alone. This leaves the compliance training software market with a clear opening for lower‑touch, bundled, and per‑user models that can serve SME demand without requiring enterprise‑grade implementation effort.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud-Based Architecture Anchors Enterprise Adoption

Cloud-based deployment captured 66.12% of the compliance training software market in 2025, confirming that SaaS delivery had become the preferred model for organizations that need automatic updates, centralized administration, and integration with adjacent enterprise systems. In practical terms, this position reflects a market preference for faster regulatory content refreshes, greater scalability, and stronger workflow integration with HRIS and GRC environments. The cloud model also fits organizations that need to reach distributed employees without maintaining local infrastructure across several offices or regions. This advantage is becoming more visible as cybersecurity audit expectations become more formal and more documentation-heavy in the years ahead. The compliance training software market has therefore continued to shift toward hosted platforms that combine content delivery, reporting, and audit trails in a single managed environment.

On-premises deployment still retained relevance where data residency requirements, air-gapped operations, or internal security rules limited the use of shared cloud environments. Government agencies, defense contractors, and some large financial institutions remained the clearest examples of this pattern because they often operate under stricter control requirements than most commercial users. Hybrid deployment is projected to grow at a 14.67% CAGR from 2026 to 2031, making it the fastest-growing model in the compliance training software industry as organizations seek a balance between cloud flexibility and local control. The April 2026 release of the Companion browser extension and the Harmony AI search tools also showed how leading vendors are building on cloud-delivered, context-aware learning experiences rather than legacy deployment assumptions. That product direction supports a compliance training software market in which new demand is increasingly tied to usability in daily workflows rather than to basic content hosting alone.

By Delivery Mode: Blended Learning Extends Training Effectiveness

Online delivery accounted for 72.74% of the compliance training software market in 2025, making self‑paced digital learning the dominant format across enterprise sizes and end‑user groups. This share reflected the need for scale, repeatability, and easy access across geographically spread workforces. Online formats also gave employers greater control over completion tracking and easier deployment across multiple compliance topics at once. For many organizations, digital delivery has become the foundation of the compliance training software market because it enables faster rollouts than classroom‑led programs and works better with remote or shift‑based staffing models. That base has not removed the need for higher‑engagement formats, but it has established digital learning as the default delivery layer

Blended learning is projected to grow at a 13.84% CAGR from 2026 to 2031, which shows that many buyers now want stronger retention and behavioral reinforcement rather than certificate completion alone. The format combines self‑paced modules with live sessions, coaching, or scenario discussions, helping organizations address topics where policy understanding alone is not enough. Blended learning delivered 24% higher engagement than classroom‑only training and has seen wider adoption across organizations globally. In parallel, the January 2026 release of AI video simulations and prompt‑to‑scenario coaching tools aimed at making guided practice easier to scale within enterprise learning programs. These developments suggest that the compliance training software market is moving toward delivery models that connect formal completion with practical application in the workplace.

By Enterprise Size: Large Enterprises Lead While SME Demand Builds

Large enterprises held 58.37% of the compliance training software market share in 2025, supported by their greater capacity to fund platform integration, maintain internal legal teams, and manage obligations across multiple jurisdictions. They also have stronger demand for features such as multi‑tenant administration, role‑based assignment, automated enrollment, and tamper‑proof records. Because leading vendors often prioritize these needs in product development, large organizations continue to shape roadmap decisions and commercial design across the compliance training software industry. This has reinforced their leading position in spending even as smaller firms face growing regulatory pressure. The compliance training software market still depends heavily on large enterprise budgets for platform scale and long‑term vendor relationships.

SMEs are projected to grow at a 14.92% CAGR from 2026 to 2031, which makes them the fastest‑growing enterprise‑size segment despite budget constraints. Their growth is tied to the fact that many compliance obligations apply regardless of employer size, especially in workplace safety, harassment prevention, healthcare privacy, and sector‑specific training. Vendor strategies are adapting to this pattern through pre‑built course bundles and easier deployment models that reduce the need for a separate learning system. The October 2025 partnership that embedded more than 300 compliance courses into BambooHR’s HR platform showed how suppliers are packaging access for organizations that do not want a full standalone LMS purchase. This leaves the compliance training software market with a structural growth path in SMEs, but one that depends heavily on simple pricing, low setup effort, and bundled functionality.

By Training Type: Cybersecurity Leads While Data Privacy Accelerates

Cybersecurity and information security training accounted for 26.37% of the compliance training software market in 2025, making it the largest training category across the broader product mix. This position was supported by demand across defense, healthcare, finance, and other regulated sectors, where security awareness is directly tied to legal and operational requirements. The category also benefits from the fact that cybersecurity training is now expected across the workforce rather than only within technical teams. That broad user base has kept it central to vendor content libraries and enterprise program design across the compliance training software market. The category remains especially durable because new security rules often trigger recurring training updates rather than one-time course assignments.

Data privacy and protection training is projected to grow at a 14.11% CAGR from 2026 to 2031, making it the fastest-growing training type in the compliance training software market, according to forecast momentum. Growth is being driven by the combination of U.S. state privacy laws, the EU AI Act’s literacy obligations, India’s rollout of the Digital Personal Data Protection Act, and Australia’s automated decision-making disclosure requirements in December 2026. AI governance and responsible AI training are also becoming more visible as organizations translate regulatory expectations into practical guidance for employees. Internal Technologies cited Gartner data from April 2026 showing that only 8% of managers had effective AI skills at that time, underscoring the gap between new AI obligations and workforce readiness. Alongside this, ethics, anti-bribery, AML, KYC, ESG, and industry-specific compliance topics continue to support a compliance training software market where content depth across many risk areas is now a core competitive factor.

By End-User Vertical: BFSI Holds The Lead While IT And Telecom Expands Fastest

BFSI accounted for 17.47% of the compliance training software market in 2025, which made it the largest end-user vertical by revenue share. Its lead reflects a dense mix of anti-money laundering, know-your-customer, securities compliance, privacy, and cybersecurity obligations that require frequent and well-documented employee training. Financial firms also tend to need detailed audit trails, role-based content assignment, and platform integration with wider risk and governance systems. These requirements have made BFSI one of the most important anchor sectors for enterprise-grade providers across the compliance training software market. Docebo disclosed in its Q4 2025 results that a major U.S. financial services regulator selected its platform to replace a legacy solution, which illustrates how replacement demand is shaping vendor opportunities in this vertical.

Healthcare and life sciences also remained important because HIPAA obligations, accreditation needs, and medical device cybersecurity controls require structured workforce education and strong recordkeeping. Manufacturing, logistics, retail, construction, and energy continued to drive demand, with safety, operational readiness, and environmental compliance remaining critical. IT and telecom are projected to grow at a 13.76% CAGR from 2026 to 2031, making it the fastest-growing vertical as providers address cybersecurity maturity, AI governance, and data sovereignty obligations across multiple countries. This is one of the clearest signs that the compliance training software market is moving beyond legacy HR compliance topics toward more technical and product-linked obligations. The broader result is a market where vertical specialization, industry templates, and faster content adaptation matter more than generic course catalog scale alone.

Geography Analysis

North America held 36.88% of the compliance training software market share in 2025, making it the largest regional contributor. The region combines federal requirements such as HIPAA, OSHA, FINRA, the Cybersecurity Maturity Model Certification, and the DOJ Data Security Program with a large body of state privacy laws, creating one of the most layered training environments globally. That structure supports high demand for platforms that can automate assignment, retain records, and differentiate training by role, state, and business function. A USD 1,350,000 fine issued in California in September 2025 illustrated the high cost of compliance gaps. Canada is driving demand through provincially regulated food and workplace safety training, while Mexico is generating early demand for Spanish-language modules among multinationals managing operations across North America.

Europe remains structurally important because GDPR enforcement keeps employee handling of personal data under scrutiny and exposes firms to large penalties for weak controls. The EU AI Act added a new demand layer when Article 4 AI literacy obligations became enforceable in February 2025, with fuller compliance for high-risk systems required by August 2026. Research in 2026 found that only 1 in 4 employees had high generative AI fluency, even though more than half were already using AI tools, underscoring a sustained need for structured workforce education. Germany, the United Kingdom, and France remain the largest country markets in Europe due to their concentration of regulated financial, manufacturing, and life sciences activity. Asia-Pacific is projected to grow at a 14.39% CAGR from 2026 to 2031, making it the fastest-growing region as China, Hong Kong, India, and Australia advance cybersecurity, privacy, and AI requirements.

South America remains at an earlier stage, but Brazil’s data protection enforcement and Chile’s evolving framework are creating baseline demand for digital compliance delivery in Portuguese and Spanish. The Middle East is advancing as Saudi Arabia and the UAE put more structure in place for data protection, security safeguards, and cross-border transfer obligations, which increases the need for localized training content and better documentation. Africa is a longer-horizon opportunity, led mainly by South Africa’s Protection of Personal Information Act, while markets such as Nigeria and Egypt are still in earlier stages of regulatory development. Across these regions, vendor participation in the compliance training software market is still less mature, and demand often depends on localization capacity and the ability to adapt content to emerging national rules.

Competitive Landscape

The compliance training software market is moderately fragmented at the content and delivery levels, even as stronger positions are emerging among enterprise vendors that combine platform capabilities with broader compliance libraries. In 2026, the strongest competitive theme is the push to use generative AI to turn internal policy documents into role‑specific training modules with less production delay. This matters because buyers increasingly want training that reflects their own policies, workflows, and risk scenarios rather than only generic catalogs. Vendors that can shorten the time between a policy change and a deployable course are improving their ability to win regulated enterprise accounts. That shift is changing the compliance training software market from a library‑led model to a more adaptive content-infrastructure model.

AI capabilities have expanded to include machine‑translated content, integrated microlearning, and AI‑driven case summarization, demonstrating how training is being more closely connected to incident, policy, and case management workflows. Other strategies include acquisitions that bring regulatory intelligence and AI‑driven interpretation of legislative text into wider compliance management stacks. Security awareness vendors are also moving toward policy‑synchronized and AI‑generated training at scale. The competitive picture now includes growing interest in predictive risk signals, where behavior such as phishing failures, assessment performance, and training deferrals can help vendors identify risk hotspots before incidents occur. This is pushing the compliance training software market toward models where learner analytics and preventive action matter as much as course completion.

Trust signals are becoming more important because enterprise buyers now assess training vendors as part of their wider third‑party risk process. Certifications such as ISO 27001:2022 are one example of how providers are using their own security posture to support enterprise sales. At the same time, not every learning platform competes on equal footing in this space, because generalist tools are not as focused on regulatory compliance use cases as specialized providers. That distinction matters because the compliance training software market increasingly rewards specialized content, audit‑ready reporting, and jurisdiction‑aware design over broad course-creation flexibility alone. The overall result is a market where platform depth, content specialization, AI capability, and trust credentials are converging into a tighter set of competitive requirements.

Compliance Training Software Industry Leaders

Skillsoft Corporation

NAVEX Global, Inc.

SAI360 Inc.

LRN Corporation

360training.com, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Launched SAT Advanced and Foundation with AI-native training and a Content Creation Agent, enabling dynamic, multilingual compliance modules from internal policies, shifting away from static libraries.

- May 2026: Expanded AI translation for phishing simulations, allowing templates and landing pages in 13 languages, extending global reach of security awareness training for multinational organizations.

- May 2026: Achieved dual AWS Competency in Education and Non-Profit, validating enterprise-grade infrastructure, security, and technical architecture for organizations requiring robust compliance and training assurance.

- April 2026: Introduced AgentHub, Enterprise Knowledge, and Skills Intelligence, integrating AI-driven learning and compliance tools, with MCP Server beta linking to Claude, Copilot, and ChatGPT, GA planned July 2026.

Global Compliance Training Software Market Report Scope

The Compliance Training Software Market comprises digital platforms and solutions that deliver, manage, and track corporate compliance education across industries. It includes modules for cybersecurity, data privacy, ethics, ESG, workplace safety, and regulatory training, delivered via cloud, on-premises, or hybrid models. Serving enterprises of all sizes, the market supports risk mitigation, regulatory compliance, and workforce accountability while enabling organizations to streamline compliance processes, enhance employee awareness, and meet evolving global governance standards.

The Compliance Training Software Market is segmented by Deployment Model (Cloud-Based, On-Premises, and Hybrid), Delivery Mode (Online, Blended, and Classroom), Enterprise Size (Large Enterprises and Small and Medium-Sized Enterprises), Training Type (Cybersecurity and Information Security Compliance, Data Privacy and Protection Compliance, AI Governance and Responsible AI Compliance, Ethics and Corporate Governance, DEI, Anti-harassment and Workplace Conduct, Anti-bribery and Anti-corruption, AML, KYC & Financial Crime Compliance, Workplace Safety and EHS Compliance, ESG & Sustainability Compliance, Third-party and Vendor Risk Compliance, and Industry-specific Regulatory Compliance), Industry Vertical (IT and Telecom, Industrial Manufacturing, Healthcare and Life Sciences, Retail and Ecommerce, Energy and Utilities, Transportation and Logistics, BFSI, Construction and Engineering, and Government, Defense, and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD)

| Cloud-Based |

| On-Premises |

| Hybrid |

| Online |

| Blended |

| Classroom |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Cybersecurity and Information Security Compliance |

| Data Privacy and Protection Compliance |

| AI Governance and Responsible AI Compliance |

| Ethics and Corporate Governance |

| DEI, Anti-harassment and Workplace Conduct |

| Anti-bribery and Anti-corruption |

| AML, KYC and Financial Crime Compliance |

| Workplace Safety and EHS Compliance |

| ESG and Sustainability Compliance |

| Third-party and Vendor Risk Compliance |

| Industry-specific Regulatory Compliance |

| IT and Telecom |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Retail and Ecommerce |

| Energy and Utilities |

| Transportation and Logistics |

| BFSI |

| Construction and Engineering |

| Government, Defense, and Public Sector |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Delivery Mode | Online | |

| Blended | ||

| Classroom | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Training Type | Cybersecurity and Information Security Compliance | |

| Data Privacy and Protection Compliance | ||

| AI Governance and Responsible AI Compliance | ||

| Ethics and Corporate Governance | ||

| DEI, Anti-harassment and Workplace Conduct | ||

| Anti-bribery and Anti-corruption | ||

| AML, KYC and Financial Crime Compliance | ||

| Workplace Safety and EHS Compliance | ||

| ESG and Sustainability Compliance | ||

| Third-party and Vendor Risk Compliance | ||

| Industry-specific Regulatory Compliance | ||

| By End User Vertical | IT and Telecom | |

| Industrial Manufacturing | ||

| Healthcare and Life Sciences | ||

| Retail and Ecommerce | ||

| Energy and Utilities | ||

| Transportation and Logistics | ||

| BFSI | ||

| Construction and Engineering | ||

| Government, Defense, and Public Sector | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size and forecast for the compliance training software market?

The compliance training software market reached USD 8.23 billion in 2025, is projected at USD 9.10 billion in 2026, and is forecast to reach USD 15.75 billion by 2031 at an 11.60% CAGR.

Which region leads demand for compliance training software?

North America led with 36.88% share in 2025 because of its dense mix of federal, state, and sector-specific requirements tied to privacy, cybersecurity, workplace conduct, and financial regulation.

Which deployment model is most widely used in compliance training platforms?

Cloud-based deployment led with 66.12% share in 2025 because organizations prefer automatic content updates, centralized administration, and easier integration with HRIS and GRC workflows.

Which training category is growing the fastest in this space?

Data privacy and protection training is forecast to grow at 14.11% from 2026 to 2031, supported by expanding privacy laws, AI literacy mandates, and cross-border compliance obligations.

Which buyer group is expanding fastest for vendors in this market?

SMEs are expected to post the highest CAGR at 14.92% through 2031, even though adoption still depends heavily on simpler pricing, bundled content, and low-effort implementation.

Which end-user vertical offers the strongest growth opportunity?

IT and telecom is projected to grow at 13.76% through 2031 as providers address cybersecurity maturity requirements, AI governance needs, and data sovereignty rules across several jurisdictions.

Page last updated on: