Inkjet Coders Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

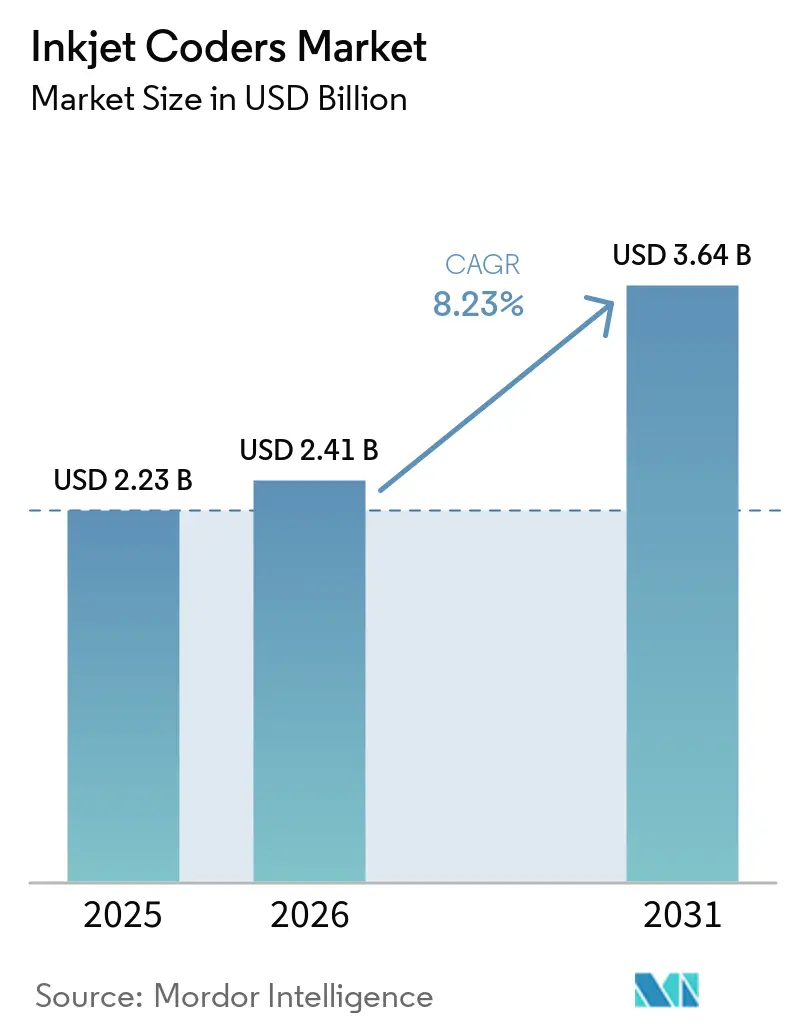

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 3.64 Billion |

| Growth Rate (2026 - 2031) | 8.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Inkjet Coders Market Analysis by Mordor Intelligence

The inkjet coders market size is expected to increase from USD 2.23 billion in 2025 to USD 2.41 billion in 2026 and reach USD 3.64 billion by 2031, growing at a CAGR of 8.23% over 2026-2031. Demand is rising as pharmaceutical serialization deadlines converge with faster FMCG line speeds and the deployment of Industry 4.0 execution systems that require real-time variable-data printing. Coders capable of ISO/IEC 15415-compliant 2D barcodes are rapidly replacing legacy batch printers, while adoption of UV-curable inks is accelerating under European and North American VOC mandates. Producers are also investing in predictive-maintenance algorithms to trim unplanned downtime and lengthen replacement cycles, tempering capital-expenditure risk even in recession-exposed segments.

Key Report Takeaways

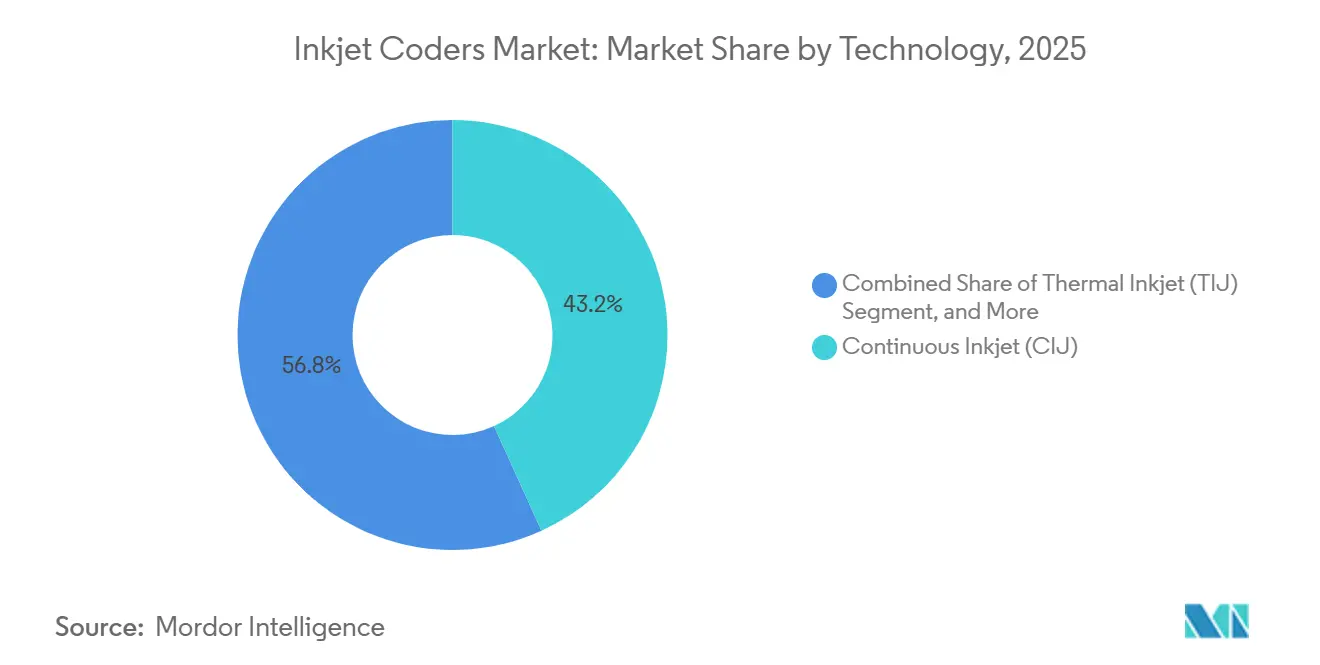

- By technology, Continuous inkjet commanded 43.2% of the inkjet coders market share in 2025, while thermal inkjet is projected to expand at a 9.9% CAGR through 2031.

- By end-use industry, Food and beverage accounted for 40.5% of the inkjet coders market in 2025, whereas pharmaceuticals and healthcare are set to grow at a 9.7% CAGR over 2026-2031.

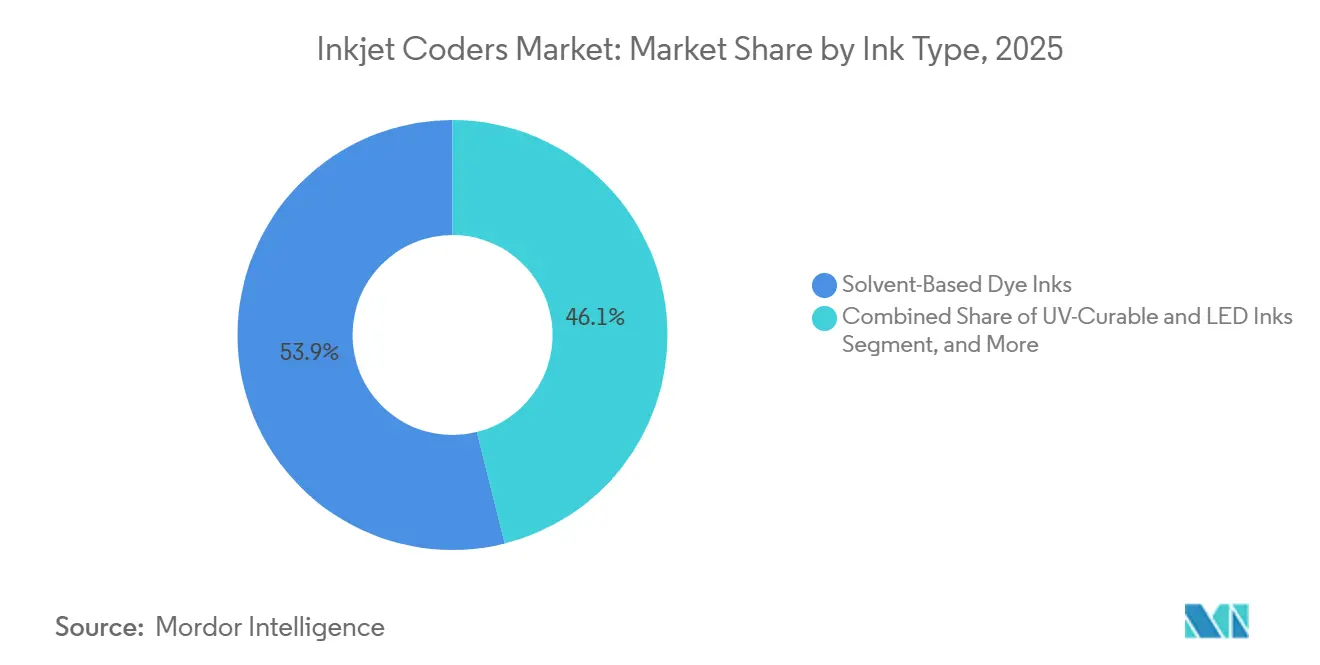

- By ink type, Solvent-based dye inks held 53.9% share of the inkjet coders market size in 2025, but UV-curable and LED inks are advancing at a 9.5% CAGR to 2031.

- By substrate material, plastic substrates captured 46.7% share of the inkjet coders market in 2025, yet flexible films and laminates are forecast to grow at a 10.4% CAGR through 2031.

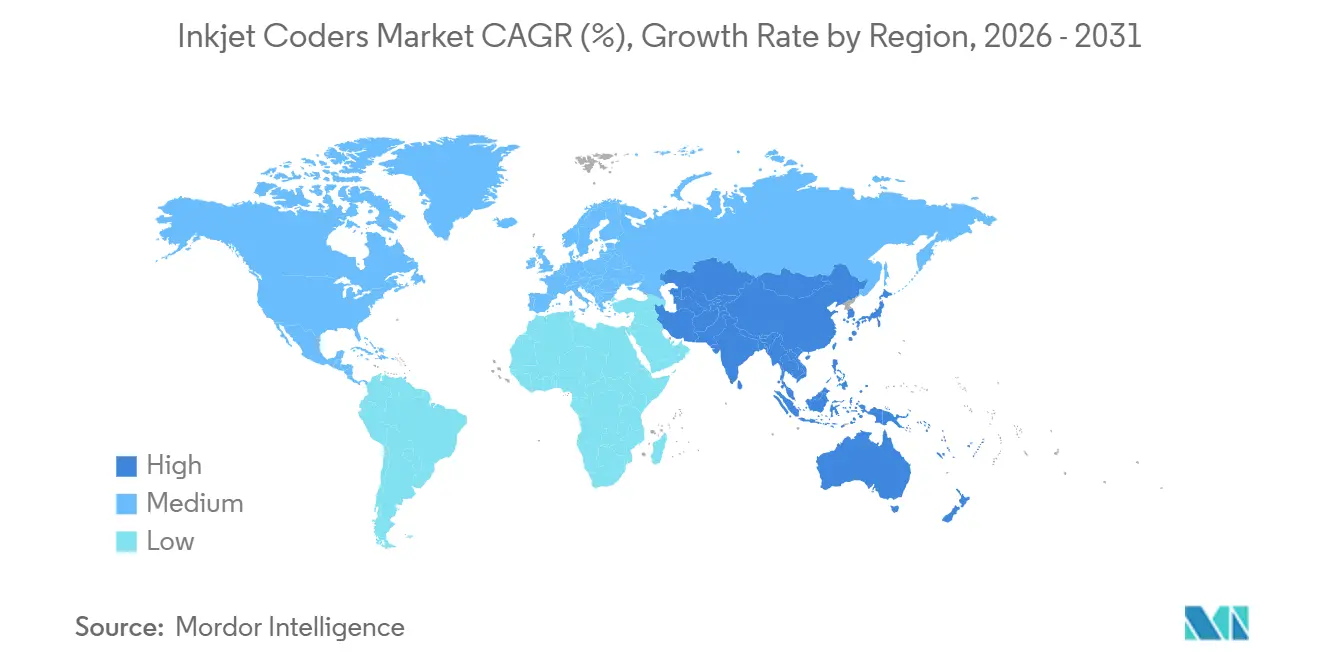

- By geography, North America led with 33.3% of the inkjet coders market, while Asia-Pacific is the fastest-growing region at a 9.1% CAGR for the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Inkjet Coders Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Serialization and Traceability Regulations | +2.1% | Global, peak in North America, Europe, China, India | Short term (≤ 2 years) |

| Proliferation of High-Speed FMCG Production Lines | +1.8% | Asia-Pacific beverage hubs, North American dairy clusters | Medium term (2–4 years) |

| Rapid Shift to Sustainable, Washable and Returnable Packaging | +1.4% | Europe and North America | Medium term (2–4 years) |

| Integration of CIJ/TIJ Heads into Industry 4.0 MES Stacks | +1.2% | Global, led by Germany, Japan, South Korea | Medium term (2–4 years) |

| Adoption of UV-Curable Inks for Counterfeit Mitigation | +1.1% | Global, strong in pharmaceuticals, electronics, and luxury goods hubs | Medium term (2–4 years) |

| AI-Enabled Predictive-Maintenance Algorithms for Print-Heads | +0.9% | Global, early adoption in North America, Europe, and advanced APAC markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Stringent Serialization and Traceability Regulations

Drug-supply-chain laws in the United States and the European Union now obligate every prescription pack to carry Data Matrix barcodes that pass ISO/IEC 15415 grade 1.5 or higher, pushing manufacturers to retrofit or replace coders for compliant high-resolution printing.[1]European Commission, “Commission Delegated Regulation (EU) 2016/161,” Official Journal of the European Union, EUR-LEX.EUROPA.EU China’s National Medical Products Administration and India’s iVEDA export program extended the same requirement to Asian producers, while Saudi Arabia’s dual-language mandate, effective October 2025, added multi-character-set capability to procurement checklists. Food traceability is moving in parallel, as the U.S. FSMA Rule 204 and the GS1 Sunrise 2027 initiative force high-risk foods to carry serialized 2D codes readable at retail. Collectively, these policies compress decision windows, making compliance-ready inkjet coders market solutions central to capital plans.

Proliferation of High-Speed FMCG Production Lines

Beverage, dairy, and snack plants now run at 1,200 units per minute, narrowing the print window to fractions of a second. Markem-Imaje’s 9750 thermal inkjet achieved 120,000 cans per hour in 2024 trials, highlighting throughput advantages over legacy continuous inkjet on small-character codes.[2]Markem-Imaje, “9750 Series Overview,” MARKEM-IMAJE.COM Domino’s Gx-Series meets similar speeds on flexible films, ensuring crisp, high-contrast marks on flow-wrap pouches.[3]Domino Printing Sciences, “Gx-Series Specification,” DOMINO-PRINTING.COM Asia-Pacific beverage hubs lead installations, while North American dairies retrofit HDPE jug lines. Cameras wired into reject stations verify every code in real time, safeguarding against recalls and penalties.

Rapid Shift to Sustainable, Washable and Returnable Packaging

The 2024 EU Packaging and Packaging Waste Regulation drives reusable glass and plastic containers that must survive multiple wash cycles without ink loss, yet remain removable during recycling.[4]European Parliament, “Packaging and Packaging Waste Regulation,” EUROPARL.EUROPA.EU UV-curable chemistries formulated for washable substrates now displace solvent inks in European bottling halls, and premium cosmetics adopt UV-LED on soft-touch cartons to meet durability rules. Water-based inks gain on paperboard, while mono-material films prompt low-temperature curing to avoid laminate delamination.

Integration of CIJ/TIJ Heads into Industry 4.0 MES Stacks

Modern coders ship with Ethernet, OPC-UA, and RESTful APIs that link directly to manufacturing-execution systems. Domino’s Dx-Series streams ink-level data and print jobs bi-directionally, enabling centralized recipe changes and remote diagnostics. Similar cloud dashboards from MapleJet and Cyklop U.S. allow predictive maintenance, cutting unplanned downtime and lowering the total cost of ownership. Automotive and electronics plants in Germany, Japan, and South Korea spearhead adoption, aligning with digital-twin traceability standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| VOC-Related Emissions Rules Limiting Solvent-Based Inks | -0.6% | Europe and North America | Short term (≤ 2 years) |

| Capital-Expenditure Freezes in Recession-Exposed Sectors | -0.5% | Global, focused on discretionary consumer goods and automotive | Short term (≤ 2 years) |

| Rising Competition from Laser Coders on High-Contrast Packs | -0.7% | Global, strong in developed markets (North America, Europe) | Medium term (2–4 years) |

| Supply-Chain Bottlenecks for Piezo Print-Head Components | -0.6% | Global, acute in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

VOC-Related Emissions Rules Limiting Solvent-Based Inks

California Air Resources Board caps and EU REACH limits on methyl ethyl ketone, toluene, and xylene force converters to replace solvent inks with UV-curable or water-based formulations. Although solvent inks still offer superior adhesion on HDPE and PP, new VOC thresholds accelerate UV-LED adoption that eliminates airborne pollutants and aligns with food-contact migration rules.

Capital-Expenditure Freezes in Recession-Exposed Sectors

Inflation and interest-rate volatility in 2025-2026 led automotive and discretionary goods producers to extend the life of installed coders rather than invest in advanced Industry 4.0 systems. Leasing, subscription, and retrofit kits partly offset the delay, yet overall inkjet coders market upgrades slowed until macro-economic visibility improved.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Thermal Inkjet Outpaces Yet Continuous Inkjet Retains Breadth

Thermal inkjet lines captured expanding beverage and dairy demand, pushing the segment toward a 9.9% CAGR, while continuous inkjet still held 43.2% of 2025 revenue. The inkjet coders market size for continuous inkjet remains buoyed by its non-contact versatility across plastics, films and corrugate. High-resolution piezo drop-on-demand platforms gained share in pharmaceutical serialization, printing Data Matrix codes at ISO/IEC grades that legacy systems cannot match. Adoption of valve-jet units stayed strong in construction and agro-chemical packaging where character height outweighs graphic fidelity. Ongoing R&D in high-viscosity piezo heads, exemplified by Kyocera’s 1,584-nozzle model able to jet 80 mPa·s fluids, will extend inkjet into decorative coatings and 3D molds.

Scaling lessons differ. Thermal heads excel where line speeds exceed 1,000 units per minute, yet nozzle lifespan and cartridge cost remain scrutinized. Continuous inkjet vendors counter with self-cleaning printhead diagnostics and lower per-code consumables, defending dominance in flexible packaging. Mixed-technology footprints are therefore common, allowing plants to allocate the right head to the right substrate without sacrificing uptime.

By End-Use Industry: Pharmaceuticals Accelerate While Food Anchors Volume

Food and beverage lines accounted for 40.5% of the revenue in 2025, driven by extensive SKU counts and retailer requirements for 2D barcodes. This segment remains dominant due to its broad application across various product categories. However, the pharmaceutical and healthcare sectors are experiencing the fastest growth, with a compound annual growth rate (CAGR) of 9.7%, fueled by global serialization initiatives. The inkjet coders market, primarily led by food companies, is expected to maintain its stronghold. At the same time, the increasing demand for high-resolution coding in injectable biologics, pre-filled syringes, and medical-device kits is creating opportunities for higher-margin unit volumes. Additionally, electronics manufacturers are adopting UV-curable and laser hybrid technologies to meet IPC traceability standards, while automotive and aerospace industries are integrating valve-jet coders for engine blocks and composite panels.

Cosmetics brands are also adapting to evolving requirements, particularly indelible batch-code regulations, by transitioning to UV-LED inks. These inks are specifically designed to bond seamlessly to soft-touch laminates without causing blemishes, ensuring compliance and maintaining product aesthetics. The growing emphasis on traceability and regulatory compliance across industries is driving innovation in coding and marking technologies. As a result, manufacturers are increasingly investing in advanced solutions to meet these demands while enhancing operational efficiency. This trend highlights the critical role of coding technologies in supporting industry-specific needs and addressing the challenges posed by stringent regulations and consumer expectations.

By Ink Type: UV-Curable Formulations Lead the Sustainability Shift

Solvent-based dye inks continue to dominate the market, accounting for 53.9% of the total market value in 2025. Their popularity stems from their fast-drying adhesion properties, particularly on materials like polyethylene (PE) and polypropylene (PP). However, UV-curable chemistries are emerging as a strong contender, projected to grow at a 9.5% CAGR. These inks offer significant environmental benefits by eliminating volatile organic compounds (VOCs) and curing instantly under LED lamps. The increasing adoption of UV-curable inks is also driven by their role in counterfeit mitigation, with companies like SICPA embedding covert markers within the polymer network to enhance product security. Meanwhile, water-based inks are gaining traction in applications involving paperboard and certain films that can accommodate slower drying times, further diversifying the market landscape.

Edible inks are another growing segment, driven by innovations such as Sun Chemical’s SensiJet line, which enables greater personalization in food manufacturing, particularly in confectionery and breakfast cereal production. Pigmented and specialty fluids are also carving out niche markets by addressing specific needs, such as printing on dark substrates and enabling temperature-trigger labels. These advancements create new revenue opportunities for formulators with expertise in specialized applications. Additionally, the demand for inks tailored to unique requirements, such as UV-LED inks for cosmetics packaging and high-resolution coding for pharmaceutical and healthcare products, is expanding. This trend underscores the market's shift toward innovative and sustainable solutions that cater to evolving industry needs while maintaining compliance with regulatory standards.

By Substrate Material: Flexible Films Surge on Recyclability Mandate

Plastics accounted for 46.7% of sales in 2025, but mono-material PE-based films and laminates experienced significant growth, registering a 10.4% CAGR. This growth is driven by brand owners transitioning to packaging designs that align with the 2030 EU recyclability targets. Flexible structures, such as these films and laminates, require low-temperature UV-LED curing to prevent laminate distortion while maintaining corona-treated bond lines. Paperboard cartons continue to be a key application area for water-based inks, which comply with FDA migration rules, making them suitable for food and beverage packaging. Additionally, glass and metal substrates are increasingly adopting laser or UV inks for permanent, tamper-evident markings that can endure harsh conditions such as autoclaving, pasteurization, and cold-chain logistics.

As legislative measures promoting reclaimed material loops gain momentum, the choice of substrate is becoming a critical factor in determining coder and ink selection. This trend underscores the importance of platform flexibility for manufacturers aiming to adapt to evolving regulatory and sustainability requirements. The demand for UV-LED curing technologies is expected to rise further, as they offer advantages such as energy efficiency and reduced environmental impact. Meanwhile, water-based inks are gaining traction in applications where slower drying times are acceptable, particularly in paperboard packaging. These developments highlight the growing need for innovative solutions that balance performance, compliance, and sustainability, positioning the market for continued growth and diversification.

Geography Analysis

North America contributed 33.3% of 2025 revenue on the back of DSCSA and FSMA Rule 204, spurring wide deployment of 2D-capable printers in pharmaceutical and high-risk food plants. Producers integrate coders with MES and ERP suites to automate variable data and remote diagnostics, reducing manual errors and labor overhead. California’s tougher VOC caps accelerate UV-LED conversions, although high capital cost tempers rollout among smaller processors.

Asia-Pacific registers the fastest 9.1% CAGR, fueled by China’s botulinum-toxin serialization, India’s GS1 QR mandates, and Saudi Arabia’s dual-language barcode rule that impacts exporters across the region. Investments include SATO’s USD 11.3 million Thai label plant that produces 7 million m² annually to service Southeast Asia. Local vendors such as Chengdu Kelier scale modular coders priced 30-40% below Western brands, capturing share in small-to-medium enterprises.

Europe sustains sizeable demand under the Falsified Medicines Directive Phase 2 and the 2024 Packaging Waste Regulation, which require reusable containers and VOC-free inks. Premium brands upgrade to UV-LED while cost-sensitive firms retrofit CIJ with eco-solvent blends. Germany, the U.K. and France spearhead Industry 4.0 coder integration, whereas Eastern Europe balances compliance needs against budget constraints. Additional momentum stems from Middle East and African serialization laws aligned with EU standards and Brazil’s digital drug passport now active across South America.

Competitive Landscape

The top five suppliers hold roughly 55-60% combined revenue, indicating moderate concentration and leaving opportunity for regional specialists. Consolidation intensified when Weber Packaging bought ATIP in March 2026, gaining ultra-high-speed thermal inkjet capability, and when Control Print purchased 50.49% of Codeology Group in April 2026 to extend U.K. service coverage. ProMach’s ID Technology absorbed KelCode in 2025, bolstering pharmaceutical track-and-trace expertise, while Kornit Digital’s PrintFactory deal integrated cloud workflow control into industrial platforms.

Strategic convergence centers on Industry 4.0 connectivity, predictive maintenance, and proprietary ink chemistry. Cyklop U.S. embeds IoT sensors that feed cloud dashboards, trimming on-site service calls. Kyocera’s high-viscosity piezo head positions the firm for decorative and additive-manufacturing verticals. Sun Chemical pioneers edible inks compatible with piezo and thermal heads, opening direct-food decoration revenue streams.

Price-sensitive buyers increasingly consider Chinese and Indian entrants offering modular coders at lower acquisition cost but comparable throughput. Incumbents respond with equipment-as-a-service contracts that bundle hardware, consumables and analytics. Patent filings in UV-curable covert-marker inks create technical moats that reward formulators with security-print know-how and raise entry barriers for ink-only upstarts.

Inkjet Coders Industry Leaders

Videojet Technologies, Inc.

Markem-Imaje SAS

Domino Printing Sciences plc

Hitachi Industrial Equipment Systems Co., Ltd.

Linx Printing Technologies Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Control Print acquired a 50.49% stake in Codeology Group for GBP 1 million (USD 1.27 million), enhancing its U.K. service footprint and serialization portfolio.

- April 2026: Kornit Digital bought PrintFactory to embed centralized workflow software across its industrial inkjet systems.

- March 2026: Weber Packaging Solutions purchased ATIP, adding high-speed thermal inkjet capability for beverage and dairy lines.

- March 2026: Pillsman Partners and Peninsula Capital acquired Printware, aiming to scale geographic reach and Industry 4.0 R&D.

Global Inkjet Coders Market Report Scope

The Inkjet Coding and Marking Systems Report is Segmented by Technology (Continuous Inkjet, Thermal Inkjet, Piezo Drop-on-Demand, Valve-Jet/Large-Character), End-Use Industry (Food and Beverage, Pharmaceuticals and Healthcare, Electronics and Electrical, Automotive and Aerospace, Cosmetics and Personal Care, Chemicals and Industrial Manufacturing), Ink Type (Solvent-Based Dye Inks, UV-Curable and LED Inks, Water-Based Inks, Food-Grade and Edible Inks, Pigmented and Specialty Inks), Substrate Material (Plastics, Paper and Paperboard, Glass, Metals, Flexible Films and Laminates), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Continuous Inkjet (CIJ) |

| Thermal Inkjet (TIJ) |

| Piezo Drop-on-Demand |

| Valve-Jet / Large-Character |

| Food and Beverage |

| Pharmaceuticals and Healthcare |

| Electronics and Electrical |

| Automotive and Aerospace |

| Cosmetics and Personal Care |

| Chemicals and Industrial Manufacturing |

| Solvent-Based Dye Inks |

| UV-Curable and LED Inks |

| Water-Based Inks |

| Food-Grade and Edible Inks |

| Pigmented and Specialty Inks |

| Plastics (HDPE, PET, PP) |

| Paper and Paperboard |

| Glass |

| Metals (Aluminum, Steel) |

| Flexible Films and Laminates |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Technology | Continuous Inkjet (CIJ) | ||

| Thermal Inkjet (TIJ) | |||

| Piezo Drop-on-Demand | |||

| Valve-Jet / Large-Character | |||

| By End-Use Industry | Food and Beverage | ||

| Pharmaceuticals and Healthcare | |||

| Electronics and Electrical | |||

| Automotive and Aerospace | |||

| Cosmetics and Personal Care | |||

| Chemicals and Industrial Manufacturing | |||

| By Ink Type | Solvent-Based Dye Inks | ||

| UV-Curable and LED Inks | |||

| Water-Based Inks | |||

| Food-Grade and Edible Inks | |||

| Pigmented and Specialty Inks | |||

| By Substrate Material | Plastics (HDPE, PET, PP) | ||

| Paper and Paperboard | |||

| Glass | |||

| Metals (Aluminum, Steel) | |||

| Flexible Films and Laminates | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the forecast value of the inkjet coders market by 2031?

The market is projected to reach USD 3.64 billion by 2031.

Which technology segment shows the fastest growth through 2031?

Thermal inkjet is expected to post the highest 9.9% CAGR between 2026 and 2031.

How large is the food and beverage share within the market?

Food and beverage held 40.5% of 2025 revenue, anchoring overall volume.

Which region is the quickest to expand during the forecast?

Asia-Pacific leads with a 9.1% CAGR through 2031, driven by serialization and FMCG capacity additions.

What inks are displacing solvent formulations?

UV-curable and LED inks are advancing at a 9.5% CAGR as firms seek VOC-free, migration-resistant options.

How concentrated is supplier power in this space?

The top five players command roughly 55-60% of revenue, placing overall concentration at a mid-range score of 6.

Page last updated on: