Belgium Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

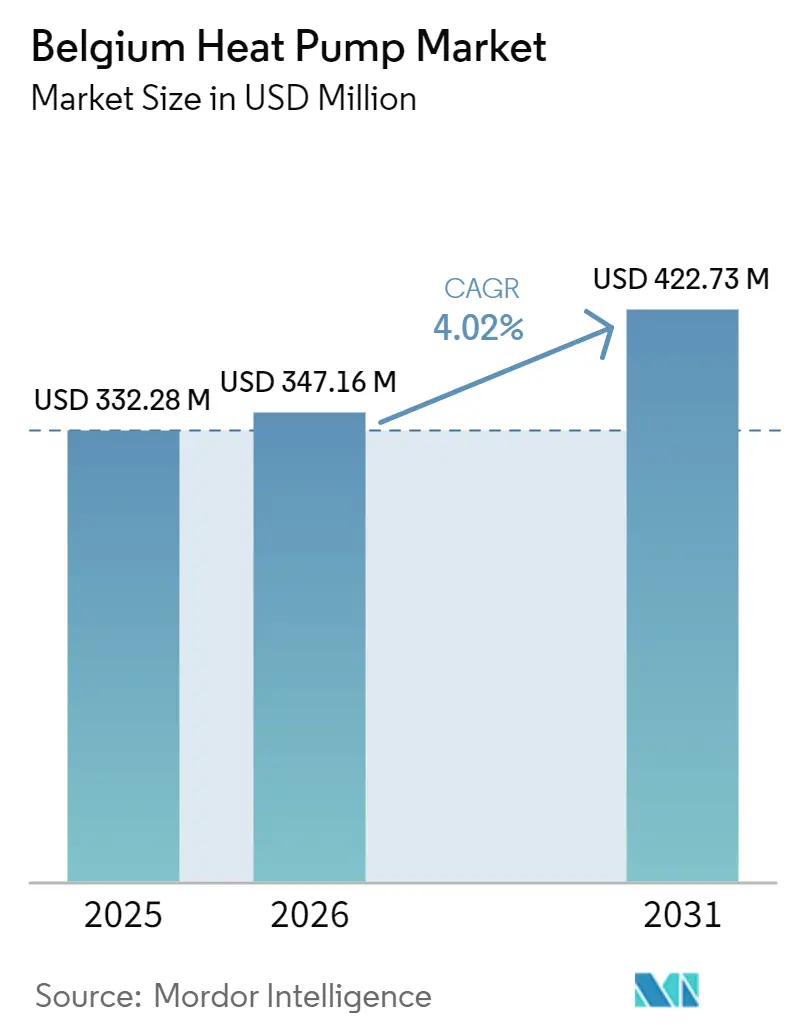

| Base Year Market Size (2025) | USD 332.28 Million |

| Market Size (2026) | USD 347.16 Million |

| Market Size (2031) | USD 422.73 Million |

| Growth Rate (2026 - 2031) | 4.02% CAGR |

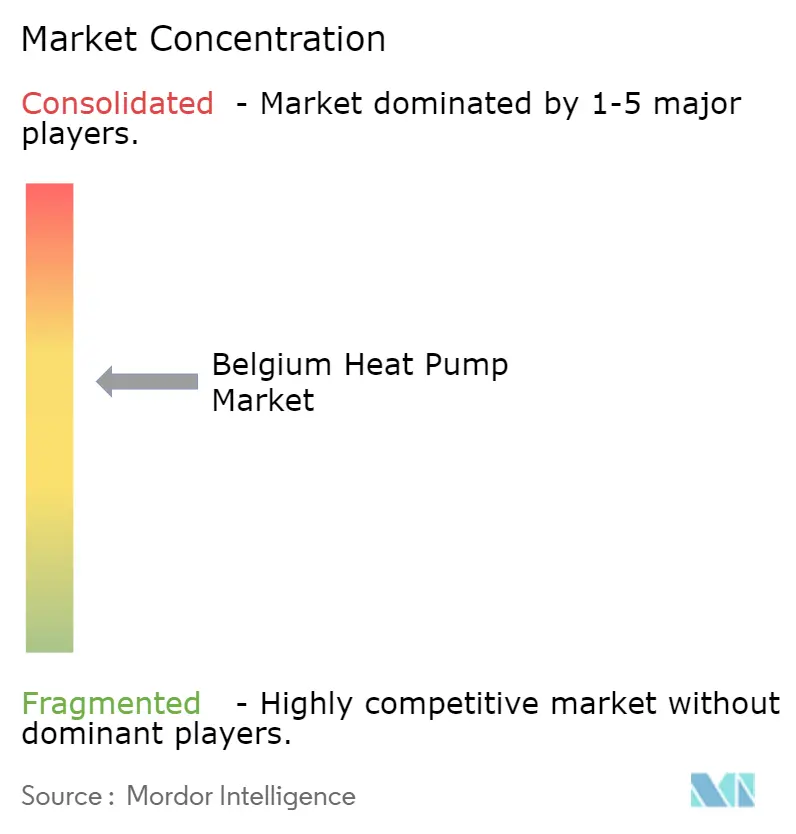

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Belgium Heat Pump Market Analysis by Mordor Intelligence

The Belgium heat pump market size is expected to grow from USD 332.28 million in 2025 to USD 347.16 million in 2026 and is forecast to reach USD 422.73 million by 2031 at 4.02% CAGR over 2026-2031. Subsidy reform that cuts VAT on heat pumps to 6%, an accelerating regional ban on new oil boilers, and corporate demand for low-carbon heat in industrial zones are steering households and factories toward electrified systems even while the national electricity-to-gas price ratio remains Europe’s highest. Manufacturers are localizing research and production to fast-track R290 refrigerant designs that meet EU F-gas rules and to shorten lead times for booming retrofit demand. Growing interest in demand-response revenues, data-center waste-heat integration, and renewable-heat power-purchase agreements underpins steady order books for mid-scale (50-200 kW) units. Hybrid air-source designs that automatically switch to integrated gas back-up during peak-tariff windows are gaining share as a transitional choice for Belgium’s poorly insulated pre-1970 housing stock.

Key Report Takeaways

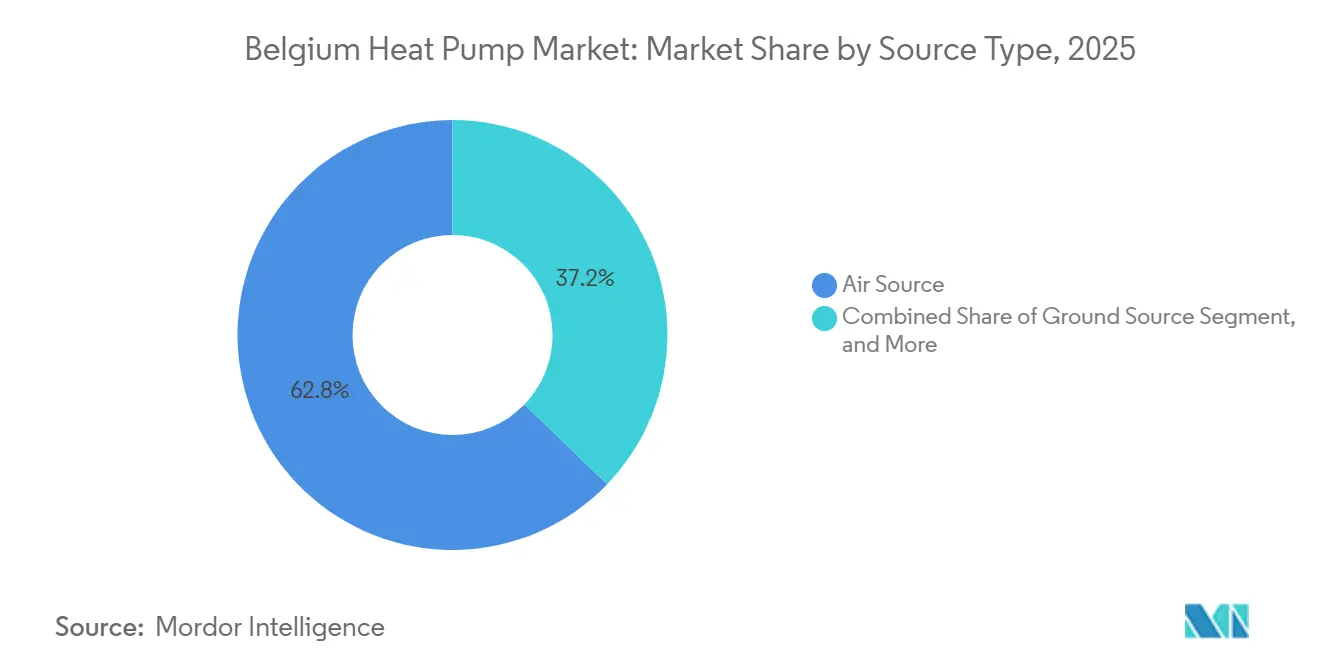

- By source type, air-source systems captured 62.78% of Belgium heat pump market share in 2025, while hybrid systems are projected to post the fastest 5.13% CAGR through 2031.

- By technology, air-to-water technology led with 52.41% share in 2025, and ground-to-water units are forecast to expand at 4.86% CAGR to 2031.

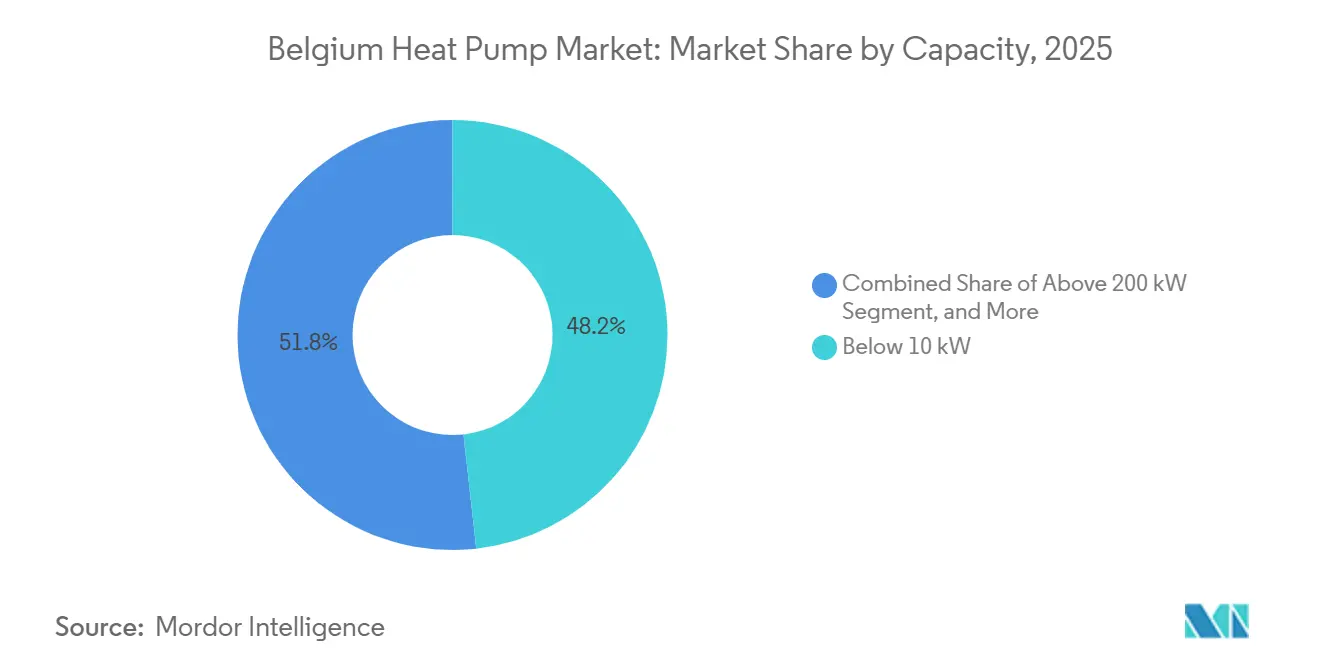

- By capacity, the below-10 kW bracket accounted for 48.23% of 2025 installations, whereas the 50-200 kW class is set to grow at 4.42% CAGR, the quickest among capacity bands.

- By application, space heating represented 41.82% of 2025 demand, yet industrial and process heat is on track for the highest 4.63% CAGR over the outlook period.

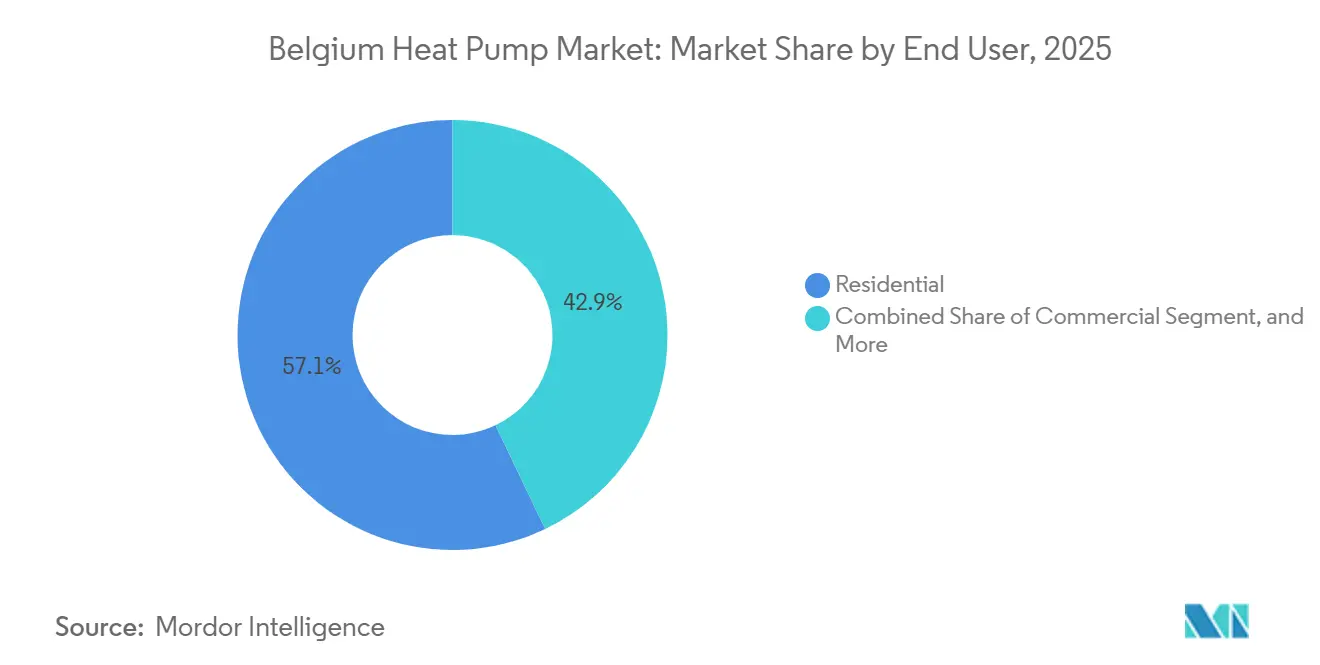

- By end user, residential end users held 57.09% share in 2025, but the industrial segment is forecast to rise at a 4.28% CAGR, outpacing all other customer groups.

- By installation type, new builds dominated with 64.43% share in 2025, while retrofits are expected to record a 4.12% CAGR as subsidy bundles mature.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Belgium Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heat-Pump Subsidy Surge Under Belgium’s 2030 NECP | +1.2% | National, higher uptake in Flanders and Brussels | Short term (≤ 2 years) |

| Mandatory Phase-Out of Oil-Fired Boilers in Flanders by 2026 | +0.9% | Flanders enforced 2022, Wallonia new builds 2026 | Short term (≤ 2 years) |

| Data-Center Waste-Heat Integration | +0.8% | Wallonia and Brussels | Medium term (2-4 years) |

| Expansion of Corporate Renewable-Heat PPAs | +0.6% | Industrial zones in Antwerp and Liège | Medium term (2-4 years) |

| Shift Toward Electrified Process Heat Below 120 °C | +0.5% | National, early adoption in Flemish Brabant and Hainaut | Long term (≥ 4 years) |

| Grid-Balancing Revenues Via Demand-Response Aggregators | +0.3% | National, Elia pilot programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heat-Pump Subsidy Surge Under Belgium’s 2030 NECP

Federal and regional authorities target 2.3 million cumulative units by 2030, a six-fold jump from 2025 installations, and back this goal with grants of up to EUR 8,000 (USD 9,040) in Flanders and VAT relief that trims a typical residential system’s upfront cost by about EUR 1,500 (USD 1,695).[1]Energy-Cities, “Belgium to Cut VAT on Heat Pumps and Raise It on Fossil Fuel Boilers,” energy-cities.eu Wallonia’s Rénopack links heat-pump aid to insulation upgrades, shrinking payback time to seven-nine years. Brussels adds a means-tested premium for low-income households, broadening access. Together, these incentives lower capital barriers, accelerate installer order books, and lift short-term demand ahead of the 2030 milestone.

Mandatory Phase-Out of Oil-Fired Boilers in Flanders by 2026

Flanders banned new oil boilers in 2022 and Wallonia extended the restriction to new buildings from 2026, eliminating roughly 60,000 units of annual replacement potential for fossil systems.[2]EURACTIV Staff, “Belgium Court Upholds Flanders' Oil Boiler Ban,” euractiv.com Court validation in 2024 removed legal uncertainty, so homeowners now face an electrification default when aging boilers fail. The policy sharply lifts near-term demand for air-source and hybrid units sized below 10 kW, while driving installer retraining and R290 product roll-outs.

Data-Center Waste-Heat Integration

Revised environmental permits oblige hyperscale operators to supply excess server heat to municipal networks. Google’s Farciennes campus already heats 5,000 homes and offsets 12,000 t of CO₂ a year.[3]Data Center Dynamics Staff, “Google Data Center in Belgium to Provide Waste Heat to Local District Heating Network,” datacenterdynamics.com Microsoft’s planned 10 MW array at Charleroi will replicate the model, signaling a pipeline across 15 operational Belgian hyperscale sites that today recover only a fraction of their 200 MW thermal output. Heat pumps are essential for lifting 30 °C exhaust to 70 °C district-heating grade, creating a medium-term equipment windfall.

Expansion of Corporate Renewable-Heat PPAs

Industrial buyers are locking in 10-15-year electricity contracts at EUR 60-70 per MWh, well below 2025 spot averages, to underwrite electrified process-heat retrofits. Borealis signed multi-hundred-gigawatt-hour PPAs that underpin heat-pump deployment at Antwerp steam crackers.[4]Borealis Press Office, “Borealis Signs Renewable Electricity Agreements in Belgium,” borealisgroup.com AB InBev’s Leuven brewery cut gas use by 18% after commissioning a 2 MW air-to-water unit. These deals provide price certainty and carbon visibility, accelerating industrial orders across chemical and food clusters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Capital Cost | -0.9% | National, acute in Brussels and Wallonia low-income zones | Short term (≤ 2 years) |

| Electricity-to-Gas Price Disparity | -1.1% | National, most severe in Brussels and Wallonia | Medium term (2-4 years) |

| Skilled-Labor Shortage Among Heat-Pump Installers | -0.6% | National, critical in rural Wallonia and West Flanders | Medium term (2-4 years) |

| Performance Challenges in Pre-1970 Housing Stock | -0.5% | National, concentrated in Brussels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electricity-to-Gas Price Disparity

Belgium’s 3.9 electricity-to-gas price ratio in May 2025, nearly double the EU mean, erodes operating savings, leaving a typical household paying EUR 1,450 (USD 1,639) a year for heat-pump electricity versus EUR 1,350 (USD 1,526) for gas. The 2026 tax shift trims, but does not close, the gap. Consumers hedge by choosing hybrid units that switch to gas during peak-tariff hours, dampening demand for all-electric systems until wholesale pricing converges.

High Up-Front Capital Cost

Residential air-to-water systems cost EUR 12,000-15,000 (USD 13,560-16,950) before subsidies, quadruple a condensing gas boiler, and low-income applicants wait up to nine months for reimbursement, stretching household cash flow. Leasing models account for only 2% of 2025 installations, far below Dutch and French penetration, indicating an underdeveloped financing ecosystem that slows mass adoption despite robust policy support.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Hybrid Systems Bridge the Transition

Hybrid configurations blending air-source heat pumps with integrated gas boilers are forecast to record the fastest 5.13% CAGR, while air source retained 62.78% Belgium heat pump market share in 2025. Homeowners favor hybrids because smart controls shift load to gas during the costliest electricity hours, preserving comfort in sub-zero weather and cutting annual bills. Manufacturers such as Daikin market R290 hybrid packages that link to smart-meter APIs, automatically optimizing the fuel mix. Ground and water source alternatives remain niche, constrained by drilling permits and site-specific water access.

Belgium’s pre-1970 housing, roughly 70% of dwellings, has limited insulation, so full electrification would oversize compressors. Hybrids lower capacity requirements by 25-30%, shaving capital cost and avoiding fuse-box upgrades, which explains their accelerating take-up in suburban Flanders. However, as electricity levies fall and envelope retrofits spread, hybrids may serve mainly as a stepping-stone toward all-electric dominance in the next decade.

By Technology: Air-to-Water Dominates While Ground-to-Water Accelerates

Air-to-water systems supplied 52.41% of 2025 shipments, thanks to ready compatibility with radiator loops and domestic hot-water tanks. Ground-to-water units are expected to expand at 4.86% CAGR, the swiftest across technologies, because they hold a coefficient of performance above 4.5 year-round and match passive-house and zero-emission office projects that demand predictable efficiency. Water-to-water designs monetize industrial effluent or river heat but remain site limited.

Developers in Brussels and Wallonia increasingly specify borehole exchangers where building tenure exceeds 25 years, accepting higher up-front drilling expense in return for lower lifetime energy outlays. Air-to-air units stay marginal in Belgium’s mild summers, leaving room for suppliers to push high-temperature air-to-water innovations with R290 refrigerant that approach 75 °C output for retrofit radiator compatibility.

By Capacity: Mid-Scale Band Captures Commercial Retrofits

Units below 10 kW captured 48.23% of 2025 installations, serving single-family homes with modest load profiles. The 50-200 kW class is forecast to increase at 4.42% CAGR and is pivotal for hotels, offices, and supermarkets replacing aging boilers. Manufacturers offer modular packages that couple multiple 100 kW R290 modules to minimize downtime and phase capex.

Belgium heat pump market size for the mid-scale band is reinforced by building-performance mandates that compel owners to cut carbon intensity below 50 kg CO₂/m² by 2030. Government loan guarantees shorten payback to six years for retail centers, while Elia’s demand-response pilots add EUR 50-80 per MWh revenue for flexible mid-scale arrays, nudging facility managers to approve projects.

By Application: Industrial Process Heat Gains Momentum

Space heating still led with 41.82% share in 2025, yet low-temperature industrial process loads are projected to generate the highest 4.63% CAGR. Food and beverage plants retrofitting fryers, pasteurizers, and CIP circuits below 120 °C represent the largest pocket of untapped demand. The EXQUISHEAT study found 60% of sub-120 °C needs in Belgian food factories are technically electrifiable.[5]VITO Research Team, “EXQUISHEAT Project Demonstrates Heat Pump Potential in Food Industry,” vito.be

Google, AB InBev, and Tiense Suiker showcase how waste-heat capture and high-temperature ammonia systems shrink gas burn by up to 80%, helping corporates meet Scope 1 and Scope 2 pledges. As EU carbon prices exceed EUR 110 (USD 125) per ton, factories gain an internal carbon shadow price that materially improves heat-pump economics, widening the Belgium heat pump market size for process-heat applications.

By End User: Industry Outpaces Households

Households still accounted for 57.09% of 2025 demand, but industrial users will grow faster at 4.28% CAGR through 2031. Corporations leverage accelerated depreciation and long-dated PPAs to electrify steam loops, while residential adoption tapers after early adopter saturation. Belgium heat pump industry financiers now see multi-megawatt arrays as mainstream, with petrochemical and beverage plants signing turnkey engineering, procurement, and construction contracts that bundle maintenance.

For homeowners, rising electricity tariffs offset subsidy gains, leaving hybrid units as a compromise. Social-housing agencies in Brussels pilot shared heat-pump rooms for apartment blocks, but fragmented ownership slows roll-out, tempering residential momentum relative to industrial uptake.

By Installation: Retrofits Narrow the Gap

New builds contributed 64.43% of 2025 installations as regional codes require heat pumps in nearly all post-2023 permits. Retrofit demand is set to expand at 4.12% CAGR as subsidy bundles cover envelope upgrades and radiators. Belgium heat pump market share for retrofits rises when owners combine Wallonia’s Rénopack or Flanders’ Mijn VerbouwPremie with low-interest renovation loans, closing a financing hole that historically stalled older-home projects.

Installer capacity is the pinch-point: certified crews number only 4,000 nationally, so manufacturers run fast-track academies in Ghent and Herstal. Retrofit performance still lags new builds, averaging a seasonal performance factor of 3.2, yet analytics-enabled commissioning and variable-speed compressors are narrowing this gap each heating season.

Geography Analysis

Regional deployment mirrors policy vigor and grid economics. Flanders delivered about 65% of 2025 installations owing to its 2022 oil-boiler ban, EUR 8,000 (USD 9,200) grants, and digital permitting that releases funds within 90 days. Average distribution tariffs of EUR 0.08 (USD 0.09) per kWh keep operating costs below Wallonia and Brussels, reinforcing adoption momentum among middle-income detached-home owners.

Wallonia captured roughly 30% of 2025 volume and will accelerate following the 2026 oil-boiler prohibition for new buildings and the envelope-tied Rénopack scheme. Rural communes confront transformer constraints that cap single-phase connections at 3 kW, steering residents toward hybrid units unless they co-finance grid upgrades costing up to EUR 8,000. Industrial clusters in Liège and Hainaut gain from demand-response payments that sweeten payback on 10 MW arrays.

Brussels contributed only 5% of 2025 sales, hampered by dense multi-family housing where collective decisions delay retrofits 18-24 months. The region’s EUR 0.11 (0.13) per kWh distribution charge, highest nationwide, erodes heat-pump savings unless paired with group purchasing or municipal bulk-heat networks. Means-tested premiums of EUR 6,000 (USD 6,900) target the 30% of residents in energy poverty, yet language and awareness hurdles slow disbursement. Pilot district-heating loops that blend data-center waste heat with central heat-pump stations could unlock metropolitan scale in the next decade.

Competitive Landscape

The top five vendors controlled an estimated 55-60% of 2025 revenue, indicating moderate concentration. Daikin leads by coupling its Ghent R&D hub with installer schooling, shortening product cycles for R290 lines and seeding loyalty among installers. Vaillant emphasizes A+++-rated systems with weather-compensation algorithms, while NIBE, BDR Thermea, and Bosch compete on modular scalability and demand-response integration.

Strategic moves center on vertical integration and high-temperature innovation. Nordic Climate Group acquired Climanova to secure distribution reach, mirroring Daikin’s direct-sales pivot. Armstrong International doubled Belgian capacity to 100 MW by 2027 after securing an EU grant, targeting the underserved 50-200 kW commercial segment. Bosch’s IDS range embeds flexibility software that caps compressor draw during tariff spikes, aligning with Elia’s grid-service tenders.

F-gas Regulation 2024/573 tightens the refrigerant landscape, so vendors racing to R290 differentiate on safety valves and leak-detection kits. Manufacturers with proprietary training centres gain an edge as installer licensing tightens, raising barriers for pure-play importers. White-space remains in multi-megawatt industrial arrays where only 15-20 projects exceed 1 MW, leaving opportunity for EPC consortia that bundle financing, performance guarantees, and carbon-credit aggregation.

Belgium Heat Pump Industry Leaders

Daikin Industries, Ltd.

Vaillant Group

Carrier Global Corporation

NIBE Group

BDR Thermea Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Building Technology Group acquired Vrints, an HVAC installer with EUR 18 million (USD 20.3 million) revenue, adding 4,500 service contracts in Flanders and Brussels.

- February 2026: Daikin expanded its Stylish air-to-air line with R32 models up to 7 kW, aimed at the residential replacement market.

- February 2026: The federal government cut VAT on heat-pump installations to 6% and lifted VAT on fossil boilers to 21%, lowering average heat-pump upfront expense by EUR 1,500 (USD 1,695).

- January 2026: Wallonia enforced a ban on new oil-boiler installations in residential and commercial buildings effective 1 January 2026.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts every new, factory-built electric heat-pump unit, air, water, or ground-source rated below 1 MW that is installed in Belgian homes, commercial premises, public institutions, and light industrial buildings for space heating, cooling, or sanitary hot-water service.

Scope exclusion: Vehicle heat-pump HVAC modules for electric cars, buses, and trucks lie outside this assessment.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed regional installers, distributor networks, and policy officers in Flanders, Wallonia, and Brussels. Discussions confirmed typical selling prices, subsidy uptake ratios, and the split between retrofit and new-build demand, closing gaps left by public data.

Desk Research

We began with Statbel building-stock data, Access2Markets import-export records, and tariff series from Belgium's federal energy regulator; these clarified equipment flow, price bands, and adoption context. Insights were layered with European Heat Pump Association statistics, Belgian Climate & Energy reports, and peer-reviewed COP studies. Company filings gathered through D&B Hoovers and news from Dow Jones Factiva completed the competitive picture. The sources named are illustrative; many additional references informed the work.

Market-Sizing & Forecasting

A top-down construct anchors the market starting from national sales and stock figures and average system ASPs. Supplier shipment samples and channel checks serve as a bottom-up sense check, with adjustments applied where variances exceed a specified threshold. Five market fingerprints, electricity-to-gas price ratio, renovation permits, regional grant budgets, segment share, and bore-hole drilling capacity, drive a multivariate regression that projects values through the forecast period. Scenario analysis tests the impact of VAT reversals or grant exhaustion on uptake.

Data Validation & Update Cycle

Outputs face automated anomaly flags, peer review, and senior analyst sign-off. We refresh models annually and issue interim updates when subsidy rules or fuel price shocks would shift forecasts materially.

Reliability of Mordor's Belgium Heat Pump Baseline

Estimates published by different firms rarely converge because each applies its own scope, price assumptions, and refresh rhythm. Our disciplined boundary setting and recurring cross-checks make Mordor's figure the dependable anchor for planning.

Typical gap drivers: some publishers price only 'heat pumps other than air-conditioning machines,' others publish unit counts without revenue, and several fold Belgium into broader Benelux totals, masking local subsidy effects.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 332.4 M (2025) | Mordor Intelligence | - |

| USD 114 M (2024) | Regional Consultancy A | Excludes hybrid and DHW units; trade-value model only |

| 31.4 k units (2024) | Industry Association B | Reports volume, not value; counts hydronic space heaters only |

The comparison shows that our Belgium-specific, revenue-based baseline, grounded in transparent variables and a clear update cadence, provides decision-makers with the most balanced starting point.

Key Questions Answered in the Report

What is the Belgium heat pump market size in 2026 and what value is it projected to reach by 2031?

The sector is valued at USD 347.16 million in 2026 and is projected to climb to USD 422.73 million by 2031.

Which subsidies can Belgian homeowners tap to lower the upfront cost of a residential heat pump?

Flanders offers up to EUR 8,000 (USD 9,040), Wallonia's Rénopack bundles as much as EUR 6,000 (USD 6,780) for the unit plus envelope upgrades, and the federal VAT rate on installations is cut to 6%.

Which region currently installs the highest number of heat pumps?

Flanders leads with roughly 65% of national installations, helped by its 2022 oil-boiler ban, higher disposable incomes, and quicker digital permitting.

Why are hybrid heat-pump systems particularly popular in Belgian homes built before 1970?

Smart controls let hybrids switch to the integrated gas boiler during peak electricity-tariff hours or very cold spells, avoiding expensive fuse-box upgrades and trimming annual energy bills.

Within commercial properties, which capacity band is expanding most rapidly?

Units rated between 50 kW and 200 kW are forecast to grow at a 4.42% CAGR as hotels, offices, and supermarkets replace aging gas boilers.

How does waste heat from hyperscale data centers influence future Belgian heat-pump installations?

Revised permits oblige operators to supply server exhaust to district networks, so multi-megawatt heat-pump arrays that lift 30 °C waste heat to 70 °C are set to power thousands of additional household connections over the next decade.

Page last updated on: