Kimchi Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.45 Billion |

| Market Size (2031) | USD 6.94 Billion |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kimchi Market Analysis by Mordor Intelligence

The kimchi market size is expected to grow from USD 5.19 billion in 2025 to USD 5.45 billion in 2026 and is forecast to reach USD 6.94 billion by 2031 at 4.95% CAGR over 2026-2031. Cultural enthusiasm powered by the Hallyu wave continues to strengthen the kimchi market. The formal inclusion of kimchi in the U.S. Dietary Guidelines and record-high South Korean exports underscore the product’s shift from ethnic specialty to functional. Inflation-resistant demand for affordable fermented foods continues to support the kimchi market, alongside flavor-seeking younger consumers, supporting steady volume gains even as cabbage price volatility persists. Multinational retailers are deepening shelf presence, while smart-factory investments in Hungary and the United States signal a pivot toward localized vegetable sourcing and shorter cold chains. Product innovation across the kimchi market, including in single-serve pouches, vegan formulations, and fusion condiments, positions producers to capture incremental occasions across retail, e-commerce, and HoReCa.

Key Report Takeaways

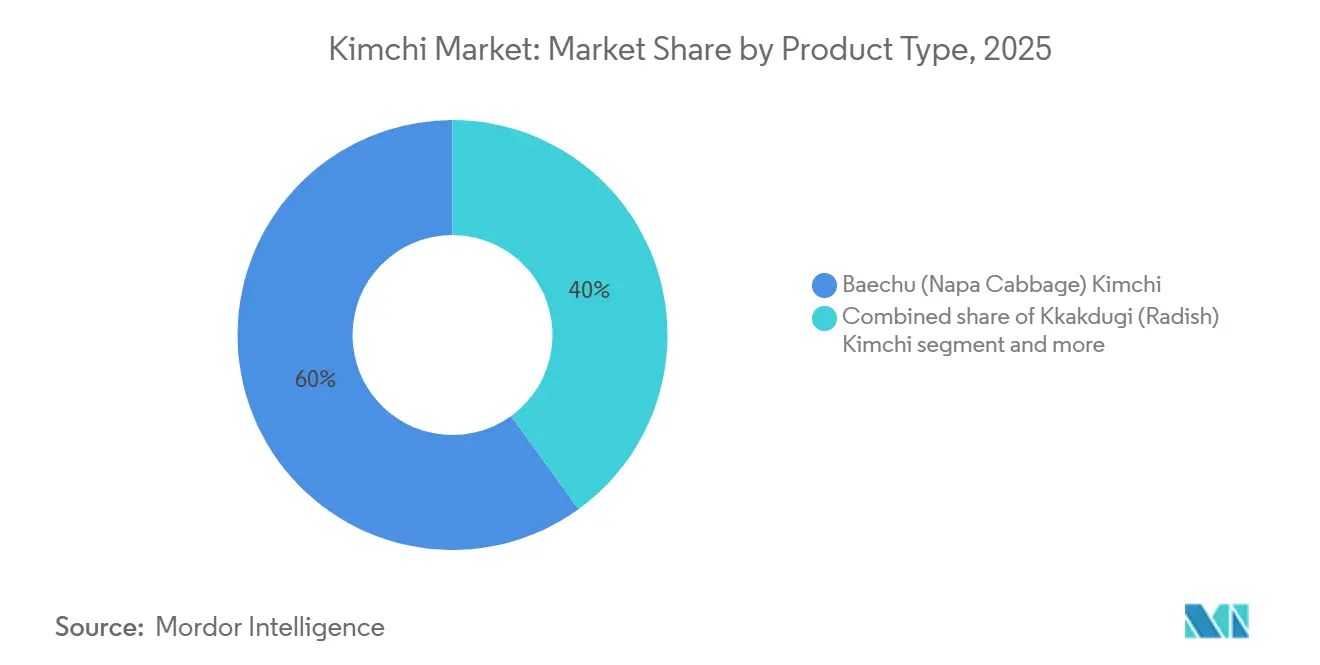

- By product type, baechu kimchi led with 59.97% of kimchi market share in 2025, whereas kkakdugi kimchi is forecasted to expand at a 5.69% CAGR through 2031.

- By packaging format, plastic tubs and buckets captured 40.11% share of the kimchi market size in 2025, yet pouches and sachets are projected to post the fastest 5.95% CAGR through 2031.

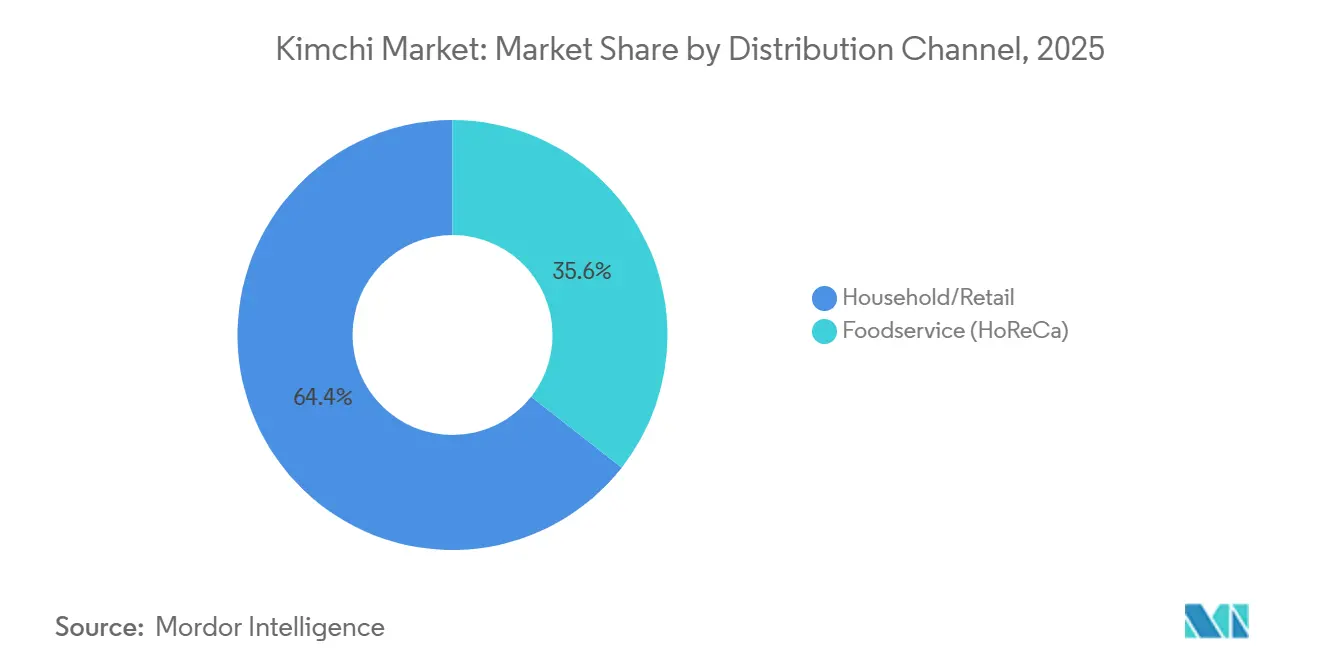

- By distribution channel, household and retail accounted for 64.41% of the kimchi market share in 2025, while HoReCa is poised at a 5.28% CAGR through 2031.

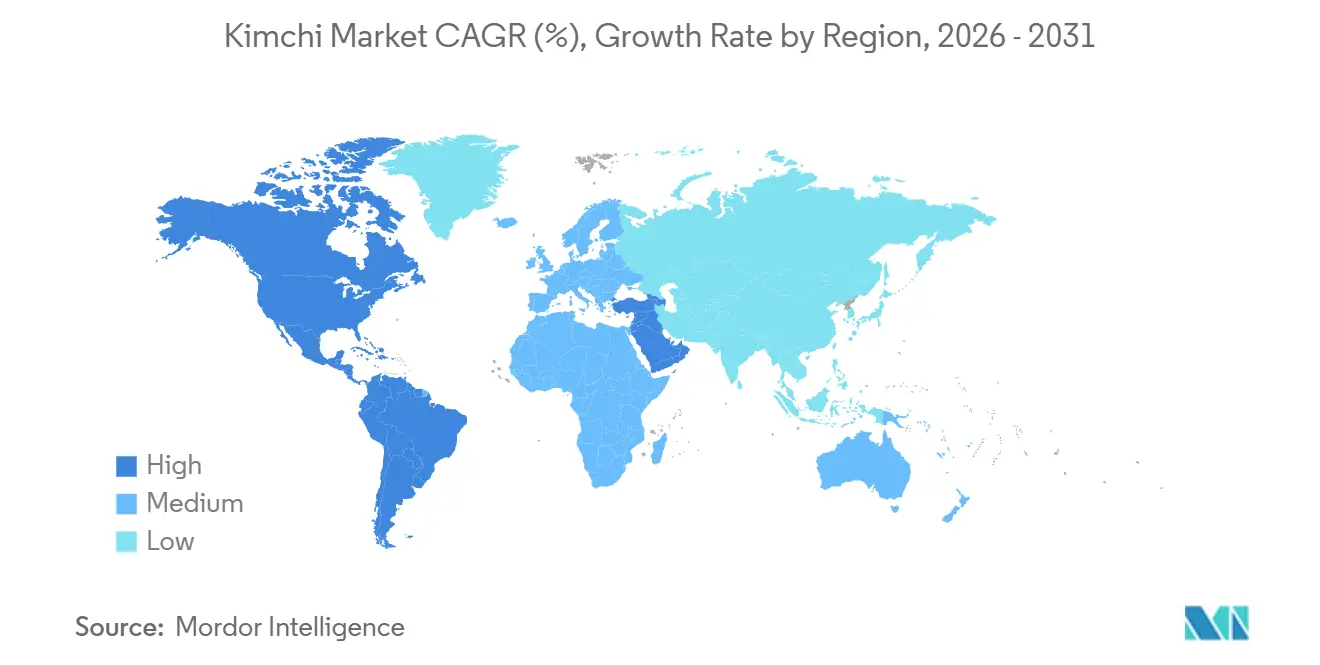

- By geography, Asia-Pacific retained 55.02% of kimchi market share in 2025; while South America is projected to grow at a 5.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Kimchi Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global popularity of Korean cuisine and cultural influence (Hallyu wave) | +1.2% | Global, with concentration in North America, Europe, Southeast Asia | Medium term (2-4 years) |

| Increasing consumer awareness of gut health and probiotics | +0.9% | Global, led by North America and Europe, expanding in Asia-Pacific urban centers | Long term (≥ 4 years) |

| Growing demand for fermented and functional foods | +0.8% | Global, particularly North America, Europe, and affluent Asia-Pacific markets | Long term (≥ 4 years) |

| Expansion of Asian foodservice restaurants and quick-service formats globally | +0.7% | North America, Europe, Middle East, with spillover to South America | Medium term (2-4 years) |

| Surging vegan and plant-based diet adoption | +0.6% | North America, Europe, Australia, urban Asia-Pacific | Medium term (2-4 years) |

| Product innovation in flavors, formats, and packaging | +0.5% | Global, with early adoption in North America, Europe, and South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising global popularity of Korean cuisine and cultural influence (Hallyu wave)

The rising global popularity of Korean cuisine, strongly influenced by the expansion of the Hallyu (Korean Wave), has emerged as a significant driver for the kimchi market. The worldwide success of Korean entertainment, including K-pop, K-dramas, and films, has heightened international curiosity and acceptance of traditional Korean foods such as kimchi. This cultural diffusion has translated into increased consumption across regions such as Southeast Asia, the Middle East, Europe, and North America. According to a 2025 government-commissioned survey, over 82.3% of global respondents reported a favorable perception of Korea and its culture, highlighting the extensive reach of Hallyu. Notably, the influence is particularly strong among younger demographics, with nearly 79% of teenagers expressing positive attitudes toward Korean culture[1]Source: The Korea Times, “K-culture lifts Korea's global image to record high”, koreatimes.co.kr. This growing cultural affinity has accelerated the adoption of kimchi in both retail and foodservice sectors worldwide. Furthermore, the association of kimchi with health benefits, authenticity, and premium Asian cuisine has strengthened its global positioning.

Increasing consumer awareness of gut health and probiotics

The growing emphasis on gut health and probiotic consumption is significantly contributing to the expansion of the kimchi market. Consumers are becoming more informed about the role of a healthy gut microbiome in supporting digestion, immunity, and overall well-being, leading to increased demand for naturally fermented foods. Kimchi, which contains beneficial live cultures formed during fermentation, is gaining recognition as an effective and natural probiotic source. This heightened awareness is particularly evident among health-focused consumers in the kimchi market seeking functional foods with added nutritional value. In addition, the rising preference for clean-label and minimally processed products has further strengthened kimchi’s market appeal. Scientific studies linking gut health to broader health outcomes, including metabolic and immune functions, are also influencing purchasing behavior. Consequently, food companies are increasingly promoting the probiotic benefits of kimchi and introducing diverse product variants to meet evolving consumer demand.

Expansion of Asian foodservice restaurants and quick-service formats globally

The global expansion of Asian foodservice restaurants and quick-service formats is playing a crucial role in driving the kimchi market. The rising popularity of Korean and broader Asian cuisines has led to a surge in the number of casual dining outlets, street-food concepts, and quick-service restaurants incorporating kimchi into their menus. International chains and independent operators alike are introducing kimchi-based dishes such as kimchi burgers, tacos, fried rice, and noodle bowls to cater to evolving consumer tastes. For instance, brands like Shake Shack have experimented with Korean-inspired menu items, while Wagamama integrates Asian flavors into mainstream dining experiences. Additionally, Korean quick-service chains such as Bibigo are expanding internationally, further popularizing kimchi-based offerings. The growth of food delivery platforms and urban dining culture continues to benefit the kimchi market has also accelerated the accessibility of such cuisines.

Surging vegan and plant-based diet adoption

The increasing adoption of vegan and plant-based diets is significantly contributing to the growth of the kimchi market worldwide. As consumers shift toward plant-forward eating habits for health, ethical, and environmental reasons, naturally plant-based and fermented foods like kimchi are gaining strong traction. Kimchi, traditionally made from vegetables and rich in nutrients, aligns well with vegan dietary preferences, especially when produced without fish-based ingredients. According to the Good Food Institute 2024 report, around 60% of U.S. households purchased some form of plant-based food, highlighting a major shift in consumption patterns[2]Source: Good Food Institute, “U.S. retail market insights for the plant-based industry”, gfi.org. Similarly, the ProVeg International 2024 report indicates that approximately 27% of Europeans identify as flexitarians, with nearly 40% of consumers in Germany following a flexitarian diet[3]Source: ProVeg International, “The new flexitarian consumer: insights from ProVeg's Veggie Challenge”, proveg.org. This widespread adoption is creating favorable conditions for kimchi as a clean-label, plant-based functional food. Furthermore, manufacturers are increasingly introducing vegan-certified kimchi variants to cater to this expanding consumer base. As a result, the convergence of plant-based trends and fermented food benefits is accelerating global kimchi demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong odor and taste profile limiting mainstream consumer acceptance | -0.6% | North America, Europe, Middle East, Africa | Medium term (2-4 years) |

| Short shelf life and storage challenges for fresh kimchi products | -0.5% | Global, particularly in regions with underdeveloped cold-chain infrastructure | Short term (≤ 2 years) |

| Supply chain complexities related to fresh vegetable sourcing | -0.4% | South Korea, North America, Europe (production hubs) | Short term (≤ 2 years) |

| Limited awareness in emerging markets outside Asia | -0.3% | Middle East, Africa, parts of South America, rural Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong odor and taste profile limiting mainstream consumer acceptance

A significant challenge restricting the wider adoption of kimchi is its strong aroma and bold, pungent flavor, which may be off-putting for consumers who are not accustomed to fermented foods. The distinctive smell, produced during lactic acid fermentation and from ingredients such as garlic and cabbage, can discourage first-time buyers, while the spicy and tangy taste can be polarizing in markets with a preference for milder flavors. This sensory intensity impacts both retail sales and foodservice incorporation, as hesitant consumers may avoid trying or regularly consuming kimchi. Despite increasing awareness of its health benefits and nutritional value, the pronounced odor and taste continue to limit mainstream appeal. To address this, manufacturers are developing milder variants, improved packaging solutions to reduce odor, and flavor-blended options, yet consumer resistance remains a notable restraint on market growth.

Short shelf life and storage challenges for fresh kimchi products

The short shelf life and storage requirements of fresh kimchi pose a significant restraint on the kimchi market growth. Being a naturally fermented product, kimchi continues to ferment even after packaging, which can lead to rapid changes in taste, texture, and acidity if not stored under proper refrigeration. Fresh kimchi typically requires cold-chain logistics and consistent low-temperature storage to maintain quality, making distribution and retail stocking more complex and costly, particularly in international markets. These factors can limit large-scale expansion, especially in regions with limited cold-storage infrastructure. Additionally, consumers may be hesitant to purchase larger quantities due to the risk of spoilage, further constraining sales. While innovations such as vacuum packaging, pasteurized kimchi, or fermented concentrates help extend shelf life, the inherent perishability of fresh kimchi remains a key challenge for manufacturers and retailers alike.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Baechu Dominance Meets Radish Momentum

Baechu kimchi, made primarily from napa cabbage, accounted for the largest share of the kimchi market in 2025, contributing 59.97% of total revenue. Its dominance is driven by its status as the most traditional and widely consumed form of kimchi, particularly in South Korea and across Asia-Pacific. The product’s versatility allows it to be consumed as a side dish, ingredient, or standalone meal component, further strengthening its market position. In addition, its well-established production processes and widespread availability across retail and foodservice channels support consistent demand. Consumers also associate baechu kimchi with authentic taste and proven health benefits, including probiotic properties. The segment continues to benefit from product innovations such as ready-to-eat packaging, low-sodium variants, and organic options, reinforcing its leadership in the global market.

Kkakdugi, a cubed radish-based kimchi, is projected to be the fastest-growing segment, expanding at a CAGR of 5.69% through 2031. Its growth is driven by increasing consumer interest in diverse kimchi varieties beyond traditional cabbage-based products. Kkakdugi offers a distinct crunchy texture and slightly sweeter flavor profile, making it appealing to both domestic and international consumers. The rising popularity of Korean cuisine globally has also contributed to greater exposure and adoption of this variant. Additionally, foodservice outlets and restaurants are incorporating kkakdugi into menus, boosting its visibility and consumption. Manufacturers are capitalizing on this trend by introducing packaged and flavored variations tailored to regional tastes.

By Packaging Format: Plastic Tubs Lead, Pouches Accelerate

Plastic tubs and buckets accounted for the largest share of the kimchi market in 2025, capturing 40.11% of total revenue. This dominance is primarily driven by their practicality within the kimchi market for storing fermented products, as they provide durability, airtight sealing, and ease of handling. These containers are widely used for both household consumption and bulk packaging, making them suitable for retail as well as foodservice applications. Their ability to preserve freshness and maintain fermentation quality over time further strengthens their preference among consumers and manufacturers. Additionally, plastic tubs and buckets are cost-effective and easily stackable, which improves logistics and storage efficiency across the supply chain.

Pouches and sachets are projected to be the fastest-growing packaging segment in the kimchi market, expanding at a CAGR of 5.95% through 2031. This growth is largely attributed to rising demand for convenience, portability, and portion-controlled packaging formats among modern consumers. These lightweight and flexible packaging options are particularly appealing to urban consumers and smaller households, where single-use or smaller quantities are preferred. In addition, pouches and sachets offer advantages such as reduced packaging material usage and lower transportation costs, supporting sustainability goals. Manufacturers across the kimchi market are increasingly adopting advanced pouch technologies, including resealable and vacuum-sealed designs, to enhance product shelf life and usability.

By Distribution Channel: Retail Dominance, HoReCa Acceleration

The household and retail segment dominated the kimchi market in 2025, accounting for 64.41% of the total market share. This leadership is primarily driven by the high frequency of at-home consumption, particularly in countries where kimchi is a daily dietary staple. Supermarkets, hypermarkets, convenience stores, and online retail platforms play a crucial role in ensuring widespread product availability and accessibility. Consumers prefer purchasing kimchi through retail channels due to the availability of multiple brands, pack sizes, and flavor variations. In addition, the growth of private-label offerings and promotional strategies by retailers has further strengthened this segment. The increasing demand for ready-to-eat and packaged food products also supports sustained growth in household consumption through organized retail networks.

The HoReCa (Hotels, Restaurants, and Cafés) segment is projected to be the fastest-growing distribution channel, expanding at a CAGR of 5.28% over the forecast period. This growth is fueled by the rising global popularity of Korean cuisine and the increasing presence of Korean restaurants and fusion dining concepts. Foodservice establishments are incorporating kimchi into a variety of dishes, including traditional meals, street food, and modern fusion recipes, thereby boosting demand. Additionally, the expansion of international tourism and dining-out culture is contributing to higher consumption through HoReCa channels. Restaurants and catering services are also sourcing kimchi in bulk, supporting volume growth in this segment.

Geography Analysis

Asia-Pacific dominated the kimchi market, accounting for 55.02% of the global share in 2025, driven primarily by South Korea, where kimchi is a daily dietary staple. The region benefits from deeply rooted cultural consumption, strong domestic production, and widespread availability across retail channels and the South Korea foodservice market. Countries such as China and Japan are also contributing to regional demand, supported by growing interest in fermented foods and cross-cultural culinary adoption. The dominance of Asia-Pacific is further reinforced by increasing exports of Korean food products, particularly through the global expansion of K-food trends. Rising urbanization and busy lifestyles have boosted demand for ready-to-eat and packaged kimchi across major cities. Additionally, health awareness regarding probiotics and gut health has encouraged higher consumption among younger consumers.

South America is emerging as the fastest-growing region in the kimchi market, projected to expand at a CAGR of 5.76% through 2031. This growth is largely driven by increasing awareness of global cuisines and the rising popularity of fermented foods among health-conscious consumers. Countries such as Brazil and Argentina are witnessing growing demand, particularly in urban areas where international food trends are rapidly adopted. The expansion of Asian restaurants and Korean cultural influence, including K-pop and K-dramas, has also contributed to consumer curiosity and trial. Furthermore, the region is experiencing growth in modern retail formats and e-commerce platforms, which are improving product accessibility. Importers and local distributors are introducing packaged kimchi in supermarkets and specialty health stores, catering to niche but expanding consumer segments.

North America and Europe represent steadily growing markets for kimchi, supported by increasing consumer awareness of probiotic-rich foods and the expanding popularity of Korean cuisine. In the United States and Canada, kimchi has transitioned from a niche ethnic product to a mainstream health food, widely available in supermarkets and organic stores. Similarly, European countries such as the UK, Germany, and France are witnessing rising demand, particularly among vegan and health-focused consumers. Meanwhile, the Middle East & Africa region is at a nascent stage but shows gradual growth due to urbanization, rising disposable incomes, and the expansion of international retail chains.

Competitive Landscape

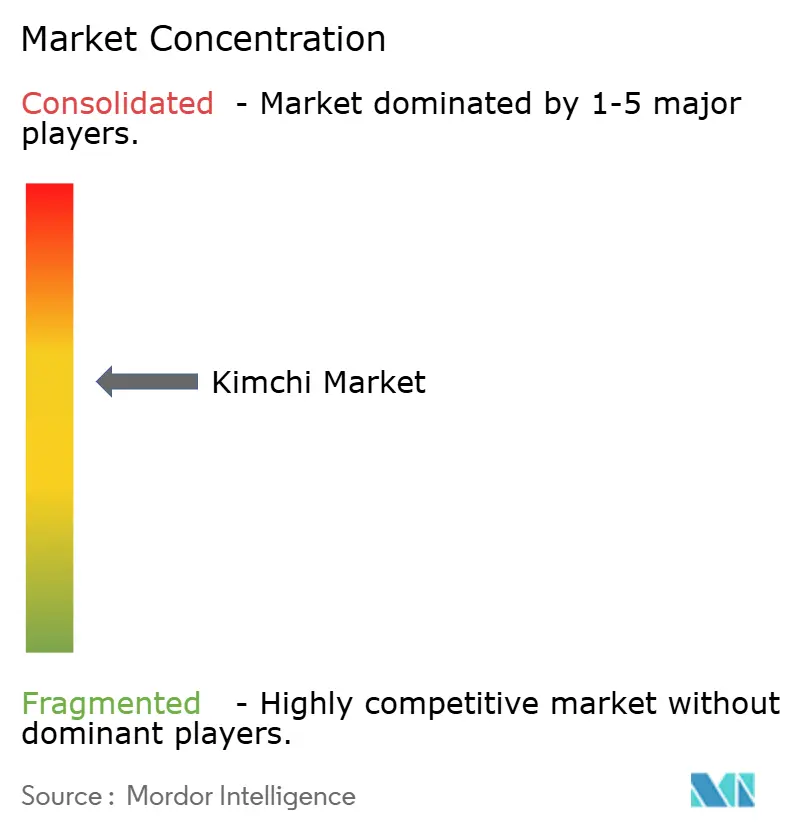

The kimchi market exhibits moderate fragmentation, characterized by the presence of a mix of large multinational food companies, regional producers, and numerous small-scale artisanal manufacturers. While a few established brands dominate organized retail and international exports, a significant portion of the market remains highly localized, particularly in South Korea where traditional and family-run businesses continue to thrive. This fragmented structure is driven by the cultural significance of kimchi, regional taste variations, and the widespread availability of locally produced options. As a result, no single player holds a dominant global market share, allowing multiple brands to coexist and compete across different price and quality tiers.

Large players such as CJ CheilJedang, Daesang Corporation, and Pulmuone have strengthened their positions through strong distribution networks, brand recognition, and product innovation. These companies focus on expanding into international markets, offering packaged, ready-to-eat kimchi tailored to global tastes, including vegan, low-sodium, and organic variants. For example, CJ CheilJedang’s Bibigo brand has successfully penetrated markets in North America and Europe, leveraging the global popularity of Korean cuisine. Meanwhile, Daesang and Pulmuone emphasize premium quality and health-focused offerings to differentiate themselves in both domestic and export markets.

At the same time, smaller and regional players play a critical role in maintaining market diversity and authenticity. Local producers often focus on traditional fermentation methods, unique regional recipes, and fresh, small-batch production, appealing to consumers seeking authentic and artisanal products. Additionally, private-label offerings from major retailers and the growth of online grocery platforms have intensified competition by increasing product accessibility and price transparency. This dynamic landscape encourages continuous innovation, packaging improvements, and strategic partnerships, as companies aim to capture a larger share of the growing global demand for fermented and probiotic-rich foods.

Kimchi Industry Leaders

Hansung Food Co., Ltd

CJ CheilJedang Corp.

Daesang Corporation

Pulmuone Co., Ltd.

Dongwon F&B Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Daesang Corporation launched two kimchi-based ramyun products under its O’Food brand, namely “Real Kimchi Ramyun Noodle Soup” and “Real Fiery Kimchi Stir-fried Ramyun,” across major retail channels in Canada and the United States. The products are differentiated by the inclusion of real fermented kimchi, reinforcing premiumization and authenticity in instant noodle offerings.

- November 2025: Vadasz, a brand under The Compleat Food Group, launched its first seasonal product, Sprout Kimchi, as a limited-edition offering in the United Kingdom. The product incorporates fermented Brussels sprouts combined with spring onion, garlic, ginger, chilli, and citrus zest, delivering a differentiated flavor profile that balances bitterness with spice and natural sweetness.

- August 2025: CJ CheilJedang launched an All-Purpose Kimchi Cooking Sauce targeting the global foodservice sector, with planned distribution across 12 countries including the United Kingdom, France, and Japan. The product leverages proprietary fermentation technology to deliver consistent flavor, extended shelf life, and operational convenience for restaurants, catering services, and hospitality providers, thereby supporting the global expansion of kimchi-based cuisine.

- August 2025: Jongga, a subsidiary brand of Daesang Corporation, entered into a strategic collaboration with Michelin-starred culinary partners to promote premium kimchi applications in haute cuisine, thereby strengthening brand positioning in the global fine-dining segment.

Global Kimchi Market Report Scope

Kimchi is a traditional Korean fermented food made primarily from vegetables most commonly napa cabbage and radishes, seasoned with a mix of spices and flavorings such as chili powder, garlic, ginger, and salted seafood. The kimchi market is segmented by product type, packaging type, distribution channel and geography. By product type, the market is segmented into baechu kimchi, kkakdugi kimchi, dongchimi kimchi, nabak kimchi, white kimchi and other product types. Based on packaging type, the market is segmented into plastic tubs and buckets, glass jars and bottles, pouches/sachets and cans. Based on distribution channel, the market is segmented into foodservice and retail. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million).

| Baechu (Napa Cabbage) Kimchi |

| Kkakdugi (Radish) Kimchi |

| Dongchimi (Radish Water) Kimchi |

| Nabak Kimchi (Sliced vegetable kimchi) |

| White (Baek) Kimchi |

| Other Product Types |

| Plastic Tubs and Buckets |

| Glass Jars and Bottles |

| Pouches/Sachets |

| Cans |

| Foodservice (HoReCa) | |

| Household/Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Baechu (Napa Cabbage) Kimchi | |

| Kkakdugi (Radish) Kimchi | ||

| Dongchimi (Radish Water) Kimchi | ||

| Nabak Kimchi (Sliced vegetable kimchi) | ||

| White (Baek) Kimchi | ||

| Other Product Types | ||

| By Packaging Format | Plastic Tubs and Buckets | |

| Glass Jars and Bottles | ||

| Pouches/Sachets | ||

| Cans | ||

| By Distribution Channel | Foodservice (HoReCa) | |

| Household/Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the kimchi market today and where is it headed?

The kimchi market size reached USD 5.45 billion in 2026 and is projected to climb to USD 6.94 billion by 2031 at a 4.95% CAGR.

Which product type is growing fastest?

Kkakdugi, the radish-based variant, is expected to post a 5.69% CAGR through 2031, outpacing the overall market.

What packaging formats are gaining traction?

Flexible pouches and sachets are the fastest-expanding format with a 5.95% CAGR, driven by single-serve convenience and e-commerce.

Why are U.S. imports falling despite rising interest?

Domestic artisanal producers have expanded, cutting reliance on refrigerated imports and tailoring flavors to local preferences.

Which region offers the highest growth potential?

South America shows the strongest trajectory at a 5.76% CAGR, thanks to diaspora influence and growing probiotic awareness.

Page last updated on: