Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

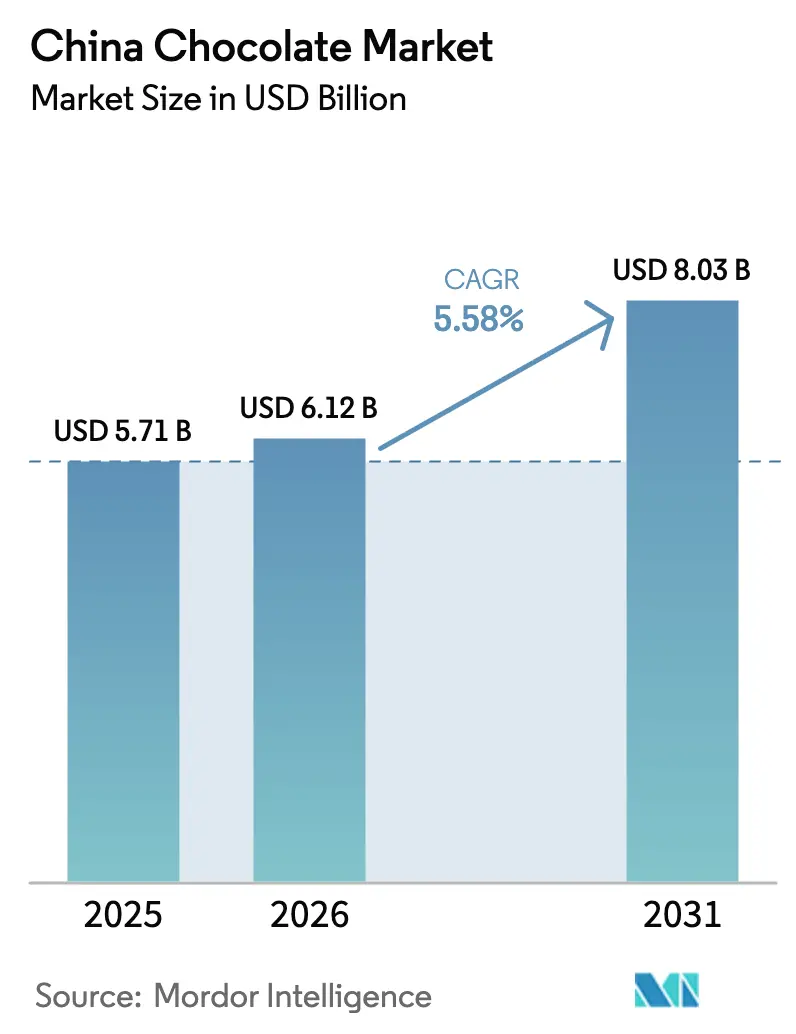

| Base Year Market Size (2025) | USD 5.71 Billion |

| Market Size (2026) | USD 6.12 Billion |

| Market Size (2031) | USD 8.03 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Chocolate Market Analysis by Mordor Intelligence

The China chocolate market size stood at USD 5.71 billion in 2025, USD 6.12 billion in 2026, and is forecast to reach USD 8.03 billion by 2031, advancing at a 5.58% CAGR over the period. Despite facing margin pressures from volatile cocoa prices, which peaked at GBP 9,425 per tonne in early 2025 before stabilizing, the chocolate market is buoyed by strong demand for premium gifting, expanding convenience-store footprints, and innovative ingredient trends. While consumption is predominantly centered in Tier-1 cities, a notable 14,550-unit increase in convenience outlets in 2024 is pushing deeper penetration into lower-tier markets. The consumer base is further expanding thanks to cross-border e-commerce, quicker last-mile deliveries, and the entry of luxury brands, highlighted by Louis Vuitton’s chocolate boutique in Shanghai. Current ingredient trends include single-origin cacao, plant-based dairy, and cocoa-free alternatives. Additionally, ongoing investments in cold-chain infrastructure and OEM capacity in Guangdong and Fujian are bolstering scalable distribution for China's chocolate market.

Key Report Takeaways

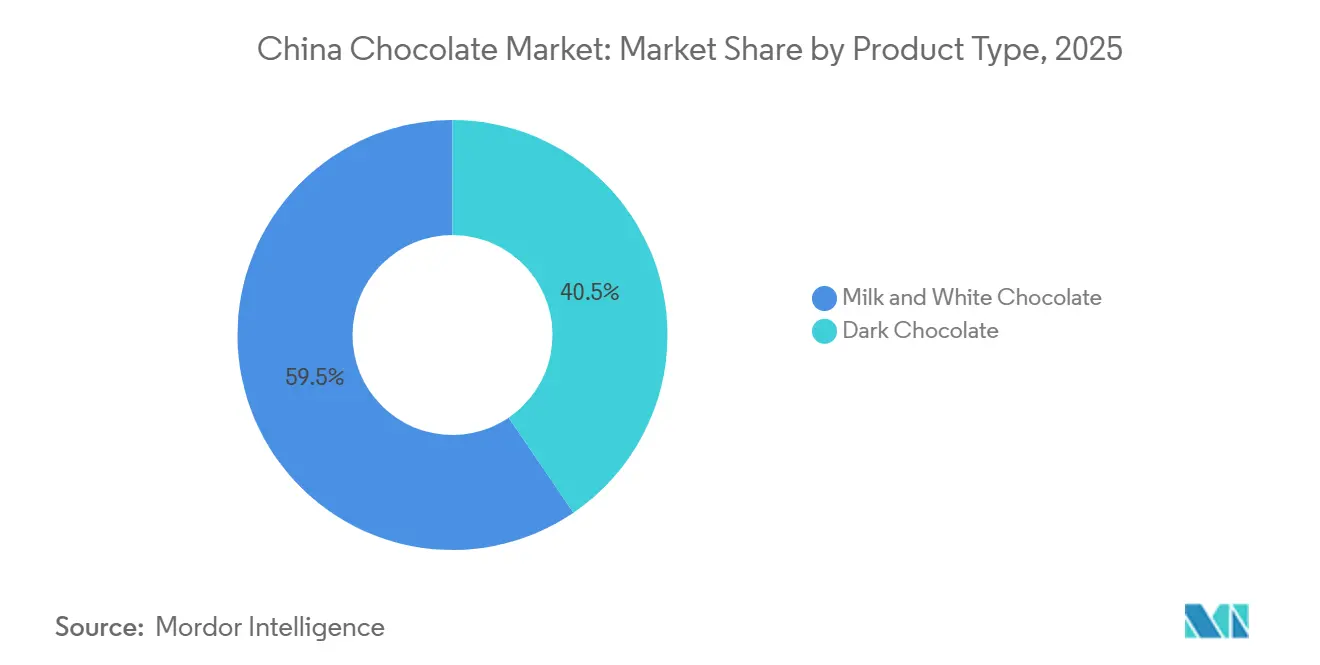

- By product type, milk and white chocolate captured 59.51% in 2025, while dark chocolate is poised for the fastest 6.13% CAGR to 2031.

- By form, tablets and bars held a 43.21% share in 2025; pralines and truffles are projected to deliver the highest 6.18% CAGR.

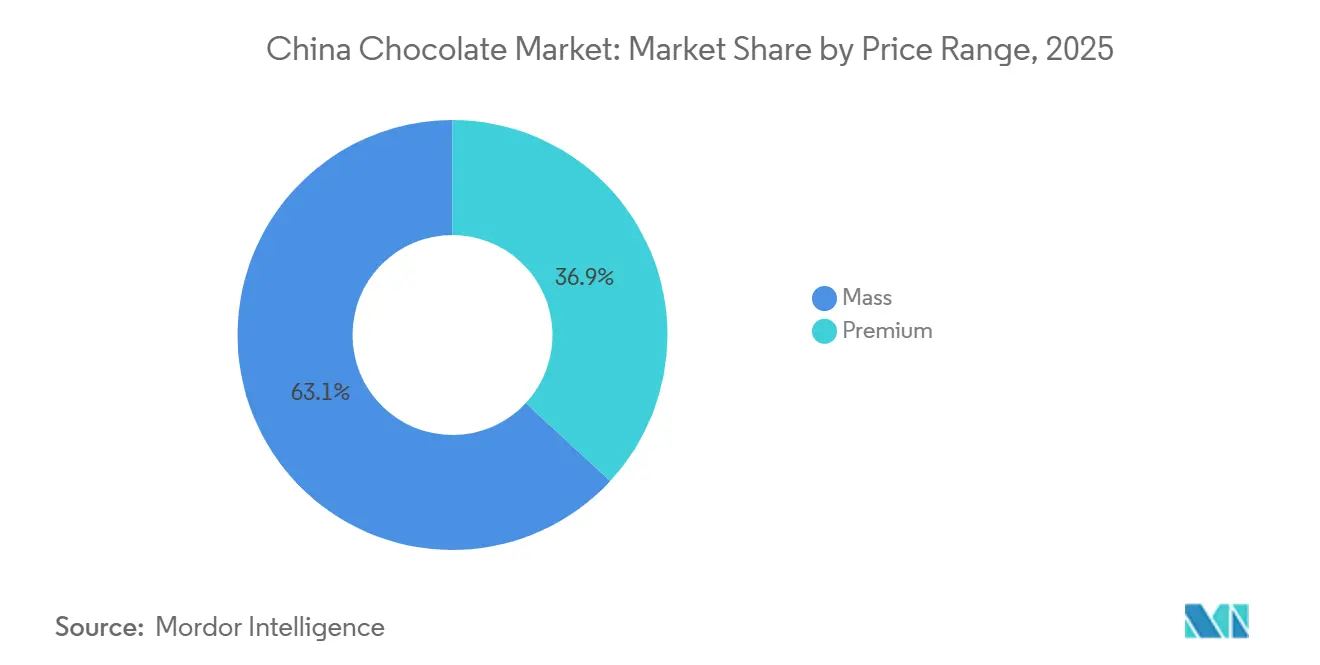

- By price range, mass-market stock kept 63.11% in 2025, yet the premium tier is forecast to expand at 7.72% CAGR.

- By ingredient type, dairy-based recipes accounted for 77.18% in 2025, whereas single-origin variants are set to register a leading 9.15% CAGR.

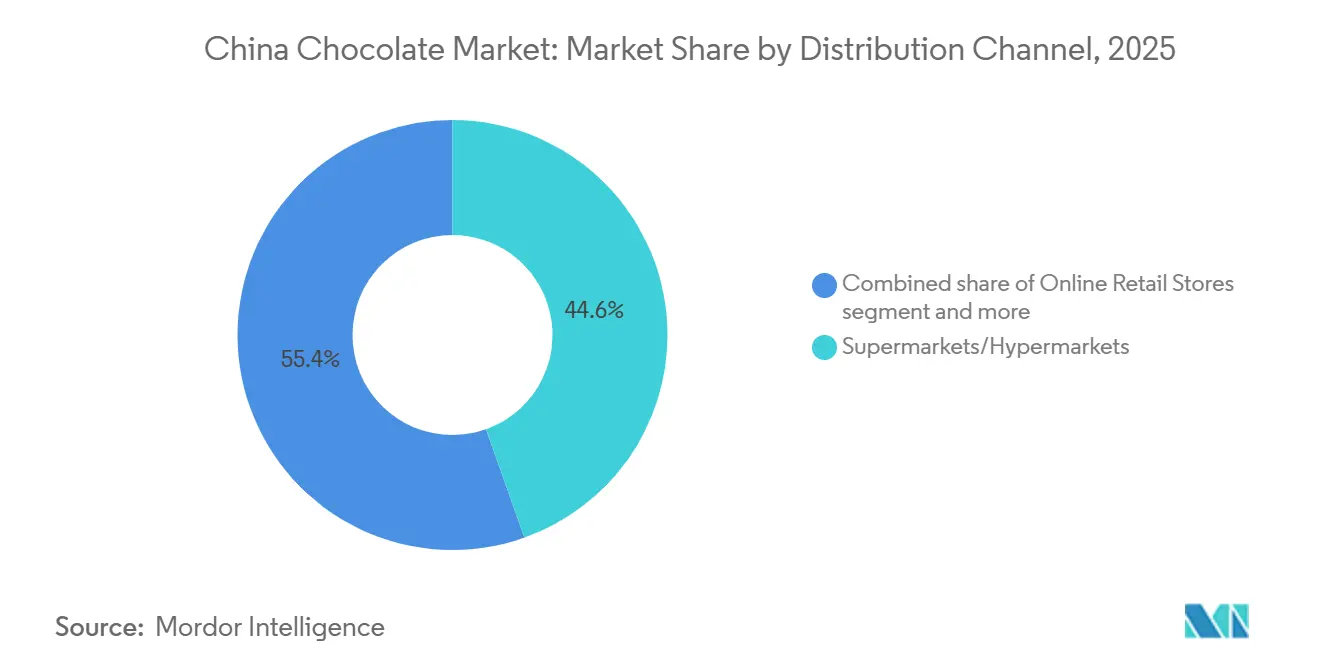

- By distribution channel, supermarkets and hypermarkets commanded 44.57% of 2025 sales, but online retail is primed for the fastest 7.17% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumisation of gifting culture | +0.8% | Nationwide, first movers Beijing, Shanghai, Guangzhou | Medium term (2-4 years) |

| Expansion of convenience-store networks | +0.7% | Tier-2 to Tier-4 cities, spillover from coastal hubs | Medium term (2-4 years) |

| Cross-border e-commerce imports surge | +0.6% | Bonded-warehouse zones in Tier-1 cities | Short term (≤ 2 years) |

| Functional chocolate with nutraceuticals | +0.5% | Urban health-focused cohorts in Tier-1 and Tier-2 cities | Long term (≥ 4 years) |

| “Chocolate + Tea” hybrids favored by Gen Z | +0.4% | Urban centers with dense Gen-Z populations | Medium term (2-4 years) |

| OEM capacity expansion in Fujian and Guangdong | +0.3% | Fujian and Guangdong manufacturing clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premiumization of gifting culture

High-profile festivals like the Spring Festival and Qixi contribute to the majority of China's annual chocolate turnover, highlighting the significant role of cultural events in driving sales. Louis Vuitton's exclusive boutique in Shanghai underscores chocolate's transformation from a mere treat to a lifestyle emblem, reflecting its growing association with luxury and status. In response, domestic brands are launching single-origin and artisanal chocolate lines, targeting the 25- to 40-year-olds, a demographic that leads in luxury spending and seeks unique, high-quality products. Innovative retail formats, including tasting bars and customization kiosks, are fostering a trend of 'trading up' in the Chinese chocolate market by offering consumers engaging and personalized experiences. This trend bolsters the pricing power of premium SKUs, even amidst broader economic uncertainties, as consumers continue to prioritize premium offerings that align with their evolving preferences.

Expansion of convenience-store networks into lower-tier cities

In 2024, chain operators expanded their footprint by adding 14,550 stores, with a notable 80% of these openings situated beyond Tier-1 locales. This expansion reflects a strategic move to tap into the growing demand in less saturated markets. Convenience venues, adept at capitalizing on impulse sales, have strategically secured shelf space for one-bite tablets, a staple in the Chinese chocolate market and a key driver of sales in quick-purchase scenarios. As disposable incomes rise inland, now exceeding USD 10,000 per capita in several provinces, the potential for larger purchases, especially chocolate multipacks, becomes evident[1]Source: National Bureau of Statistics of China, " Per capita gross domestic product (GDP) in China in 2024", data.stats.gov.cn. This increase in income levels has also led to a shift in consumer preferences toward premium and value-added chocolate products. Membership clubs, including Sam’s Club and Costco, further fuel this trend by offering family-value formats that cater to bulk-buying households. Additionally, partnerships with platforms like Meituan for instant deliveries are bridging the last-mile gap, especially for temperature-sensitive products, ensuring that consumers receive fresh and high-quality items promptly.

Surge in cross-border e-commerce imports

In 2024, cross-border retail transactions surged to CNY 2.6 trillion, thanks to tariff reforms and expedited customs clearances. These reforms have significantly streamlined the import process, making it easier for international brands to enter the Chinese market. Bonded warehouses in Hangzhou, Shanghai, and Guangzhou, now operating with a swift 48-hour lead time, are promoting the trial of limited-edition SKUs that may not be viable for domestic production due to scale constraints. This reduced lead time allows businesses to test niche products more efficiently, minimizing risks associated with inventory holding. Overseas chocolatiers are leveraging direct-to-consumer storefronts on Tmall Global and JD Worldwide to gauge demand before committing to factory investments. This strategy not only cultivates early-stage brand equity but also protects suppliers from the conventional distribution margins prevalent in China's chocolate market, enabling them to offer competitive pricing. Moreover, updated bilingual-labeling regulations have lightened compliance challenges, leading to a quicker SKU turnover and facilitating smoother market entry for foreign brands.

Growing demand for functional chocolate with nutraceutical additives

This trend underscores a growing consumer inclination towards blending indulgence with wellness. Dark chocolate bars, boasting a cacao content of 70% or more, are now infused with probiotics, collagen, and adaptogens, emphasizing their antioxidant benefits and catering to health-conscious consumers seeking functional snacks. Furthermore, plant-based launches, appealing to China's 50 million vegetarians, gain momentum with vegan certification under T/CGDF 00030-2022, ensuring compliance with stringent dietary standards. Collaborations between domestic formulators and nutraceutical experts are on the rise, ensuring adherence to clean-label claims and addressing consumer demand for transparency in ingredient sourcing. In the evolving landscape of China's chocolate market, the fusion of functionality and traceability is carving out premiumization pathways, offering products that align with both health and ethical considerations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-sensitive consumers | -0.6% | Nationwide, strongest in Tier-3 and Tier-4 locales | Short term (≤ 2 years) |

| Cocoa price volatility | -0.9% | Global supply chain, domestic pass-through | Short term (≤ 2 years) |

| Traditional sweets competition | -0.4% | Lower-tier cities with candy heritage | Medium term (2-4 years) |

| Fragmented cold-chain logistics | -0.5% | Tier-2 to Tier-4 distribution corridors | Long-term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price-sensitive consumers and cocoa price volatility

In early 2025, cocoa prices peaked at GBP 9,425 per tonne, then retreated to GBP 5,302. Yet, the annual average still marked a 131% increase, reflecting significant cost pressures on the supply chain. In response to surging costs, manufacturers employing cost-plus pricing strategies hiked retail prices to maintain margins. This led consumers to downsize their purchases, gravitating towards smaller packs and biscuits as more affordable options. Barry Callebaut observed a volume decline in China for FY 2024/25, with 63.11% of the category's volume remaining in the mass-market segment, indicating a shift in consumer preferences towards lower-priced products. With youth unemployment surpassing 15% and ongoing challenges in the property sector, discretionary spending took a hit, especially in lower-tier cities where economic recovery remains sluggish. To mitigate potential future shocks and ensure supply chain resilience, companies like Barry Callebaut are diversifying their sourcing strategies, exemplified by their establishment of a new 40,000-tonne warehouse in Malaysia, which is expected to enhance regional supply capabilities.

Traditional sweets competition and cold-chain fragmentation

Brands like White Rabbit have launched sugar-reduced candies, pricing them lower than comparable dark bars, effectively undercutting chocolate for calorie-conscious shoppers. These products cater to the growing demand for healthier confectionery options, appealing to consumers who prioritize reduced sugar intake. Nestlé's complete acquisition of Hsu Fu Chi in 2025 paves the way for cross-promoting traditional candies and chocolates across 3,000 of its proprietary outlets, leveraging its extensive distribution network to strengthen its market presence. Dali Foods balances its research and development investments equally between chocolate and traditional snack staples, a strategy aimed at hedging margin risks while ensuring innovation across both segments. While China's 14th Five-Year Plan set a goal of 180 million m³ for refrigerated warehousing by 2025, rural areas still lag behind urban counterparts by a significant 60%, highlighting the need for infrastructure development to support market growth. Additionally, spoilage rates of 10-15% for pralines in Tier-3 regions continue to hinder diversification efforts within China's chocolate market, limiting the ability to introduce new product formats effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dark Chocolate Gains on Wellness Wave

In 2025, milk and white chocolate claimed a dominant 59.51% share, led by mass-market brands such as Dove, Snickers, and Orion's Choco Pie. Leveraging decades of brand equity and a nationwide distribution network, these brands have solidified their leadership position. The segment's growth has slowed to a 5.2% CAGR, attributed to saturation in Tier-1 cities and a notable shift towards premiumization. Consumers are now gravitating towards single-origin or functional chocolate variants, rather than simply driving up overall revenue. Additionally, regulatory frameworks, specifically GB 9678.2-2014, mandate cacao content labeling[2]Source: National Food Safety Standard, "GB 9678.2-2014 PDF English", chinesestandard.net. This regulation aids in distinguishing between compound and genuine chocolate, further supporting the segment's evolution.

Meanwhile, dark chocolate not only holds a significant share of the revenue but is also expanding at a robust 6.13% CAGR. This growth outpaces the broader market, driven by urban millennials and Gen-Z's increasing preference for health narratives emphasizing antioxidants and reduced sugar content. Further underscoring the industry's evolution, Mars made a significant announcement in December 2024, committing to a segregated cocoa supply chain by 2030. This move not only emphasizes traceability as a key differentiator in the mass segment but also aims to bridge the price gap between milk and dark chocolate options.

By Form: Tablets and Bars Lead, Pralines Surge on Gifting

Tablets and Bars captured a dominant 43.21% share of China's chocolate market in 2025. Their appeal thrives on impulse purchases at convenience stores and supermarkets, especially at checkout aisles where single-serve formats reign. These formats cater to consumers seeking quick indulgence or on-the-go snacking options, making them a staple in high-traffic retail environments. Molded Blocks, typically found in multi-packs at membership giants like Sam's Club and Costco, are witnessing steady growth. This surge is attributed to these retailers' expansion into Tier-2 cities, targeting value-driven households that prioritize cost-per-gram over aesthetics. The affordability and bulk-buying appeal of Molded Blocks resonate with families and budget-conscious shoppers. Despite fluctuations in other segments, this trend remains robust, supported by consistent consumer demand for accessible and economical chocolate options.

Pralines and Truffles are leading the charge with a 6.18% CAGR, outpacing their previous 4.8% growth rate from 2020-2025. This uptick is buoyed by a post-pandemic rebound in disposable incomes and a resurgence in corporate gifting. Their luxury branding positions them as coveted lifestyle accessories, a sentiment echoed by Louis Vuitton's July 2024 boutique launch in Shanghai and Läderach's "Hermès of chocolate" moniker. These premium products often serve as status symbols, appealing to affluent consumers who associate them with exclusivity and sophistication. While festival seasons fuel their demand, cold-chain challenges lead to a 10-15% spoilage rate in Tier-3/4 cities, confining their growth primarily to coastal regions. Meanwhile, niche "Other Forms" like spreads and novelties are making waves, with collaborations like Moutai x Dove on Tmall showcasing their innovative spirit. These niche products often attract younger demographics and experimental consumers, further diversifying the chocolate market landscape.

By Price Range: Premium Gains Share Despite Macro Headwinds

In 2025, mass-market products commanded a dominant 63.11% share, underscoring the price-sensitive nature of Chinese consumers and the widespread distribution of well-established brands such as Dove, Snickers, and Hsu Fu Chi. These brands have successfully penetrated the market by leveraging extensive supply chains, competitive pricing strategies, and strong brand recognition. The mass-market segment continues to thrive due to its ability to cater to the everyday needs of a broad consumer base, particularly in lower-tier cities where affordability and accessibility remain key purchasing drivers.

Meanwhile, the premium segment is experiencing significant growth, with a robust 7.72% CAGR, outpacing the mass market by a notable 2.1 percentage points. This growth is driven by the increasing purchasing power and evolving preferences of affluent Tier-1 shoppers, who are seeking high-quality products that emphasize brand heritage, single-origin cacao, and artisanal craftsmanship. Premium brands such as Lindt, Godiva, and Le Conte are capitalizing on this trend by offering unique value propositions that resonate with discerning consumers. Additionally, cross-border e-commerce platforms like Tmall Global and JD Worldwide are playing a pivotal role in expanding access to premium European imports. These platforms enable Tier-2 consumers to explore and purchase high-end products, albeit at a 20-30% premium, thereby democratizing access to luxury offerings and further fueling the growth of the premium segment.

By Ingredient Type: Dairy Dominates, Single-Origin Surges

In 2025, dairy formulations captured a dominant 77.18% share in China's chocolate market. This dominance is largely attributed to a deep-rooted preference for creaminess and recipes from heritage brands, which continue to resonate strongly with traditional consumer tastes. Meanwhile, research and development efforts focusing on A2 milk and reduced-sugar variants are helping to mitigate losses due to changing demographics, such as younger consumers seeking healthier options. As lactose intolerance rises and more consumers gravitate towards plant-based options, there's a noticeable surge in non-dairy products, such as oat milk and coconut cream bars, which cater to evolving dietary preferences. Furthermore, stringent import regulations now require precise allergen labeling, bolstering transparency across diverse chocolate formulations and ensuring compliance with international standards.

Among various ingredient segments, single-origin chocolate is witnessing the fastest growth at a 9.15% CAGR. This surge is driven by a premiumization trend, drawing parallels to the narratives surrounding specialty coffee, where consumers are willing to pay a premium for quality and authenticity. Marketing strategies that emphasize origin resonate deeply with culinary enthusiasts and foodie subcultures, who value the unique flavors and stories tied to specific regions. Concurrently, sustainability initiatives not only ensure traceability for farmers but also foster consumer trust by addressing ethical concerns in the supply chain. Since 2022, vegan certifications have spurred a wave of product launches aimed at flexitarian consumers, who are increasingly seeking plant-based alternatives without compromising on taste. Additionally, the emergence of cocoa-free prototypes, utilizing fermentation or sunflower substrates, hints at a potential disruption in the market's long-term landscape, offering innovative solutions to address sustainability and supply chain challenges.

By Distribution Channel: Online Retail Outpaces Traditional Formats

In the China chocolate market, supermarkets and hypermarkets, leveraging festival promotions and a nationwide presence, accounted for 44.57% of sales in 2025. These outlets benefit from their ability to cater to a broad consumer base, offering a wide variety of products under one roof. Close behind, convenience stores, with a 7% growth rate, are making inroads into sub-tier urban areas by providing easy accessibility and quick purchase options for consumers. Specialty boutiques, positioned in prime locations, are capitalizing on high-margin premium sales by focusing on exclusivity and personalized customer experiences, while duty-free channels benefit from a resurgence in tourism, attracting international and domestic travelers. Despite the digital trend, physical stores continue to thrive, offering sensory experiences such as product sampling and visually appealing displays that drive impulse purchases.

Online retail is the fastest-growing segment, boasting a 7.17% CAGR. This surge is fueled by innovations like live-streaming, which engages consumers in real-time, rapid 30-minute deliveries that cater to convenience, and targeted marketing of niche products such as sugar-free pralines and vegan bars, which appeal to health-conscious and environmentally aware consumers. Direct-to-consumer platforms are not just selling; they're testing stock-keeping units (SKUs) with dynamic pricing and swift feedback loops, enabling brands to adapt quickly to market demands. Meanwhile, instant apps are pairing chocolates with beverages, enhancing overall basket values and encouraging complementary purchases. Cross-channel loyalty programs are amassing data, refining product launches, and seamlessly integrating online and offline shopping experiences through technologies like scan-and-go, which provide a frictionless shopping journey for consumers.

Geography Analysis

In 2025, the demand for chocolate, driven by a premium bias, a strong gifting culture, and dependable cold-chain networks. Residents in these cities consume nearly 1.5 kg of chocolate per capita annually, a figure that's about three times the national average. Meanwhile, lower-tier markets, with per-capita consumption just under 0.5 kg, are rapidly catching up, thanks to a surge in convenience stores and the expanding reach of e-commerce. Coastal provinces, notably Guangdong and Fujian, leverage their manufacturing hubs and port access, not only bolstering OEM exports but also catering to the domestic chocolate demand.

Inland provinces like Sichuan, Henan, and Hubei, starting from a modest base, are witnessing significant percentage growth. This surge is facilitated by bonded-warehouse shipping, which slashes delivery times to just 48 hours. The chocolate market in these inland regions is further energized by instant-delivery services, bypassing traditional retail hurdles. Inventory from cross-border shipments, once parked in Hangzhou or Guangzhou, is now reaching shoppers in Chengdu and Wuhan within a mere two days. While food-safety standard enforcement varies across provinces, Tier-1 cities maintain rigorous audits, encouraging multinational companies to invest in compliance. Looking ahead, while Tier-1 cities are expected to see their CAGR moderate to 5.0%, lower-tier markets might experience a boost, climbing towards a 6.5% growth rate as infrastructure and income levels align.

Nationally, cold-chain capacity boasts a volume of 180 million m³, yet rural areas still face challenges in praline distribution[3]Source: New Development Bank, "Jiangxi Urban and Rural Cold Chain Logistics Project", ndb.int. Third-party operators, such as SF Express, are expanding their refrigerated fleets, although their coverage predominantly favors the eastern seaboard. On a positive note, the rise of convenience stores and the establishment of highway logistics parks are curbing spoilage losses. This geographic shift not only aims to bridge the consumption gap between urban and rural areas but also seeks to introduce premium chocolate lines more deeply into the Chinese market.

Competitive Landscape

In the China chocolate market, a moderate fragmentation is evident. International giants like Mars, Ferrero, Mondelez, Nestlé, and Hershey compete head-to-head with domestic frontrunners such as Shanghai Golden Monkey, Hsu Fu Chi, and Yake. In a strategic move, Nestlé acquired the remaining 40% of Hsu Fu Chi in February 2025, gaining access to a vast 3,000-store network for promoting both chocolate and traditional candy. Meanwhile, Mondelez bolstered its position by taking a majority stake in Evirth, adding three factories for versatile co-manufacturing of frozen and chocolate products. After a 29-year journey, Orion finally turned profitable in China, celebrating its first dividend repatriation in 2024, backed by a robust revenue of 602.2 billion KRW.

Ferrero exemplifies the industry's premiumization trend, having reclaimed control of its Tmall flagship in mid-2023 to bolster its online brand equity. Localization strategies are also in play; for instance, Orion tweaked the weight of its Choco Pie to cater to Chinese palates. The realm of functional chocolate is drawing in newcomers with nutraceutical expertise, while OEM players in Fujian and Guangdong are capitalizing on e-commerce by selling private-label bars. Competitive edges are being sharpened through supply-chain digitization, as seen with Barry Callebaut's real-time shipment tracking, a feat achieved through a partnership with Microsoft. Mars is making waves with its USD 1 billion initiative to segregate cocoa sources, positioning itself as a leader in traceability amidst tightening regulations.

Mergers and acquisitions continue to be a pivotal strategy for scaling in the industry. The last two years witnessed a surge in cross-border investments, plant expansions across Asia, and significant warehousing milestones, highlighted by the establishment of Barry Callebaut and Maersk's 40,000-tonne hub in Malaysia. Domestic players are leveraging nimble online marketing and competitive pricing to carve out niches. As premium offerings gain traction, success in the competitive landscape will rely on compelling storytelling, innovative ingredients, and adeptness in navigating the complexities of the cold chain across China's expansive chocolate market.

China Chocolate Industry Leaders

-

Chocoladefabriken Lindt & Sprüngli AG

-

Ferrero International SA

-

Mars Incorporated

-

Nestlé SA

-

Yildiz Holding

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Nestle SA introduced its premium DAMAK chocolate to the Chinese market. DAMAK is a luxurious blend of silky milk chocolate and premium pistachios sourced from Turkey's Antep region, offering a delightful nutty and creamy taste.

- November 2025: Dove, in collaboration with Dong-A E-Jiao, unveiled its latest creation: E-Jiao dark chocolate. This innovative chocolate is crafted from pure cocoa butter and Dong-A E-Jiao's instant powder, utilizing a patented technology.

- September 2025: GODIVA teamed up with THE MONSTERS' LABUBU for a limited-edition launch in China. Their fantasy-themed offerings include chocolates and ice creams. The ice creams combine dark chocolate and hazelnut, topped with crunchy pecans and LABUBU inserts, while the milkshakes feature handmade rolls. The chocolate selection boasts praline-filled sets, 3D LABUBU sculptures in both 70% dark and milk chocolate, and themed tins adorned with raspberry stars and heart shapes.

- September 2025: Lindt marked its 180th anniversary with a special launch in China: panda-shaped chocolates. Collaborating with the Chengdu Research Base of Giant Panda Breeding, Lindt aimed to promote panda conservation. The exclusive series features mini packs of panda milk chocolates and the "Bamboo Forest Secret Realm" gift box, both showcasing adorable panda designs and a rich cocoa flavor with smooth, melt-in-mouth milk notes.

China Chocolate Market Report Scope

The chocolate market encompasses the global industry involved in the production, distribution, and sale of chocolate products derived from cocoa beans.

The China chocolate market is segmented by product type, form, price range, ingredient type, distribution channel, and geography. Based on product type, dark chocolate, milk, and white chocolate. Based on form, the market is segmented into tablets and bars, molded blocks, pralines and truffles, and other forms. Based on price range, the market is segmented into mass and premium. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, online retail stores, convenience stores, and other distribution channels.

The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

By Product Type

| Dark Chocolate |

| Milk and White Chocolate |

By Form

| Tablets and Bars |

| Molded Blocks |

| Pralines and Truffles |

| Other Forms |

By Price Range

| Mass |

| Premium |

By Ingredient Type

| Dairy-based |

| Plant-based |

| Single-origin |

By Distribution Channel

| Supermarket/Hypermarket |

| Convenience Store |

| Online Retail |

| Other Distribution Channels |

| By Product Type | Dark Chocolate |

| Milk and White Chocolate | |

| By Form | Tablets and Bars |

| Molded Blocks | |

| Pralines and Truffles | |

| Other Forms | |

| By Price Range | Mass |

| Premium | |

| By Ingredient Type | Dairy-based |

| Plant-based | |

| Single-origin | |

| By Distribution Channel | Supermarket/Hypermarket |

| Convenience Store | |

| Online Retail | |

| Other Distribution Channels |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms