Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

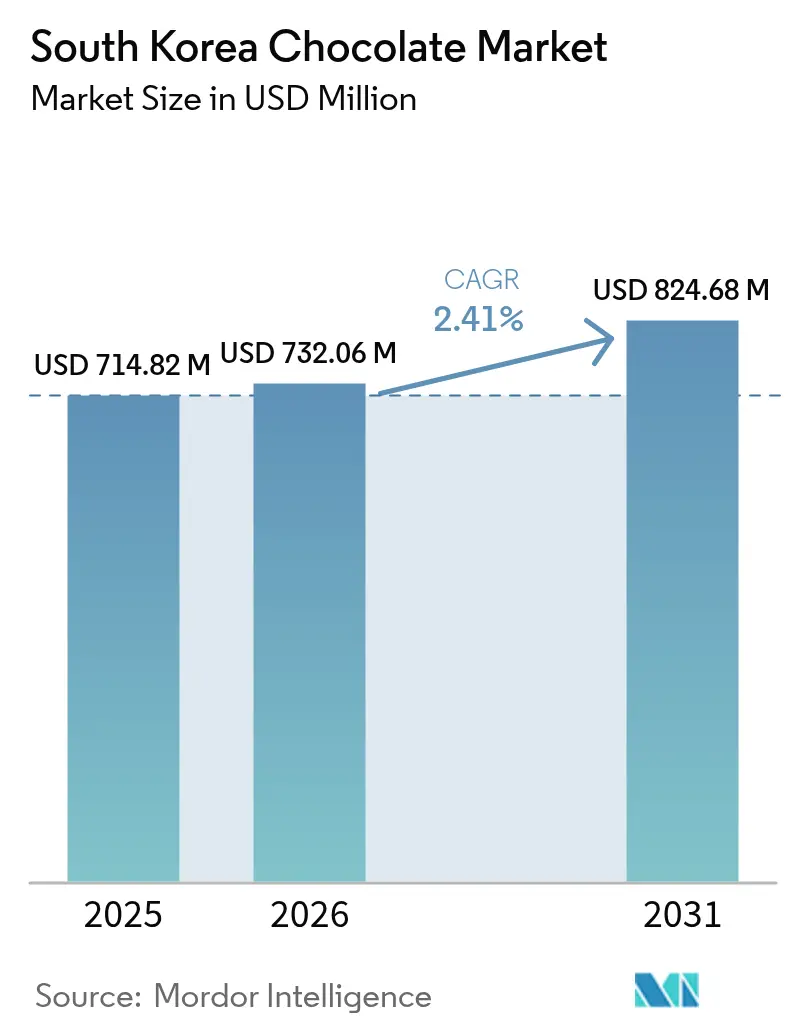

| Base Year Market Size (2025) | USD 714.82 Million |

| Market Size (2026) | USD 732.06 Million |

| Market Size (2031) | USD 824.68 Million |

| Growth Rate (2026 - 2031) | 2.41% CAGR |

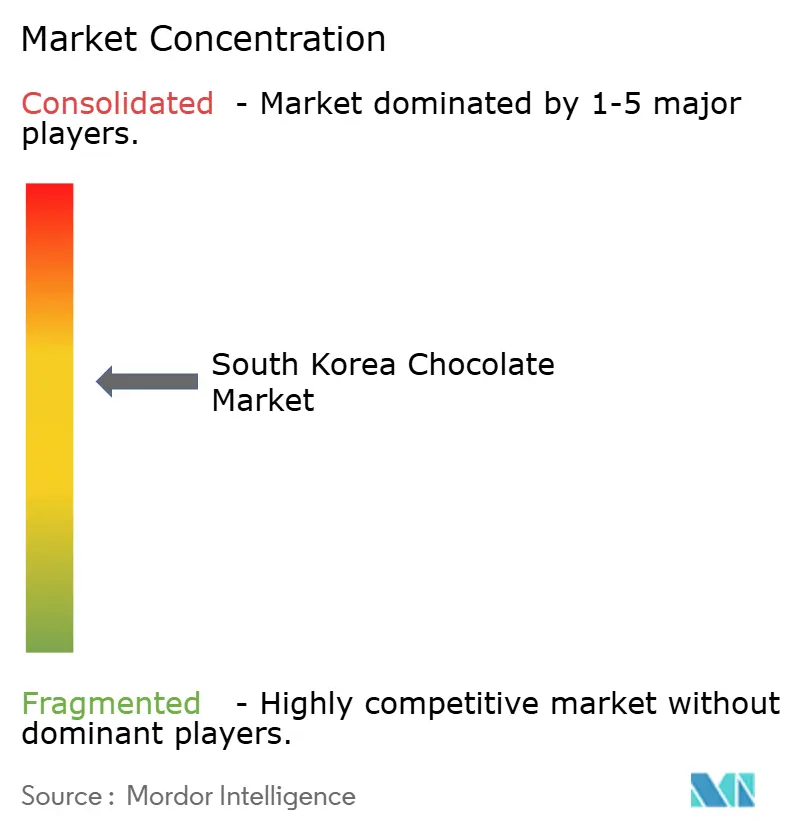

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Chocolate Market Analysis by Mordor Intelligence

The South Korean chocolate market size was valued at USD 714.82 million in 2025 and estimated to grow from USD 732.06 million in 2026 to reach USD 824.68 million by 2031, at a CAGR of 2.41% during the forecast period (2026-2031). This growth trajectory reflects the market's evolution, where consumers increasingly balance everyday chocolate consumption with a growing appetite for premium offerings. The market dynamics are shaped by social media's influence on consumer preferences, alongside a notable shift towards health-conscious chocolate options. South Korea's deeply embedded gift-giving traditions continue to drive substantial seasonal sales, particularly during cultural celebrations like Valentine's Day and White Day. The Ministry of Food and Drug Safety (MFDS) implements comprehensive quality control measures for domestic and imported chocolates, fostering consumer trust in the market. The industry's development is accelerated by the robust growth of e-commerce platforms, increased introduction of sugar-free alternatives responding to Korea's health-conscious consumer base, and calculated market entries by global chocolate manufacturers. This market environment maintains moderate competitive intensity while providing viable opportunities for specialized market participants.

Key Report Takeaways

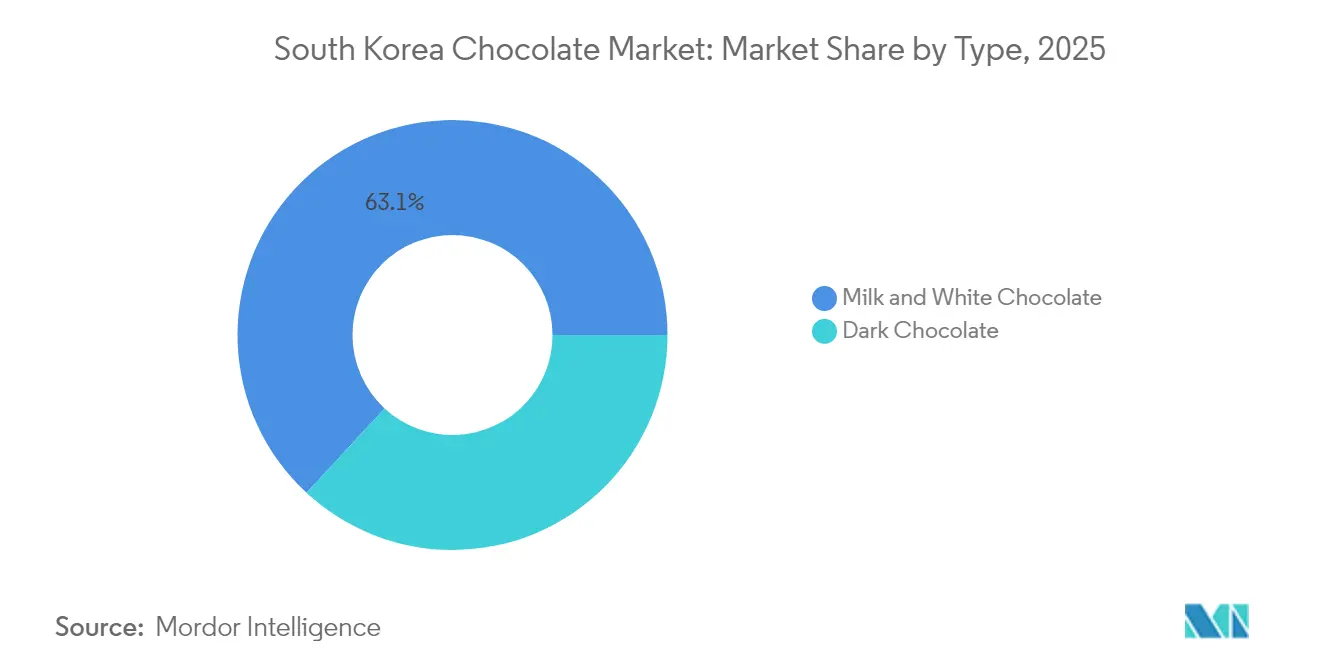

- By type, milk-and-white variants led with 63.12% of South Korea chocolate market share in 2025 while dark chocolate is projected to log the fastest 3.60% CAGR through 2031.

- By category, sugar-based products commanded 81.70% of the South Korea chocolate market size in 2025 and sugar-free lines are forecast to rise at 3.44% CAGR.

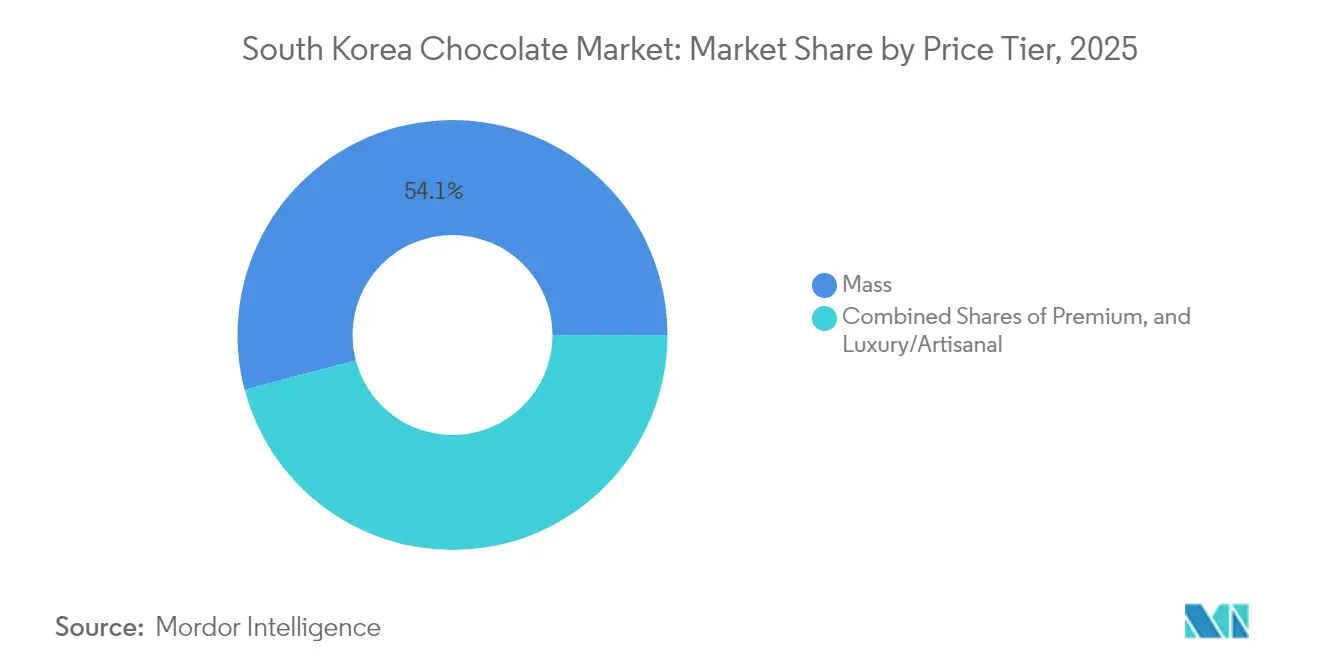

- By price tier, mass-market SKUs accounted for 54.10% revenue in 2025; the luxury/artisanal tier is poised for a 3.62% CAGR through 2031.

- By distribution, supermarkets and hypermarkets held 46.05% revenue share in 2025, whereas online retail is on track for a 3.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Evolving taste preferences toward international and fusion flavors | +0.8% | National, concentrated in Seoul and Busan metropolitan areas | Medium term (2-4 years) |

| Rising popularity of premium and artisanal chocolates | +0.6% | National, with early gains in affluent urban districts | Long term (≥ 4 years) |

| Growing demand for organic, vegan, and gluten-free chocolates | +0.4% | National, led by health-conscious millennials and Gen Z | Medium term (2-4 years) |

| Expansion of global brands and international offerings | +0.5% | National, particularly in major retail chains | Short term (≤ 2 years) |

| Strong tradition of chocolate gift-giving | +0.3% | National, culturally embedded across all regions | Long term (≥ 4 years) |

| Growing awareness of sustainable/ethical sourcing and packaging | +0.2% | National, driven by corporate ESG initiatives | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Evolving Taste Preferences Toward International and Fusion Flavors

Korean consumers show increasing preference for international chocolate varieties and fusion flavors, influenced by their exposure to global culture through K-pop, Korean dramas, and international travel. The Dubai chocolate trend in December 2023 illustrates this shift, as TikTok-driven demand for pistachio-filled chocolates significantly increased pistachio cream imports and pistachio-flavored ice cream imports in 2024. Social media accelerates the adoption of international flavors, prompting convenience stores to introduce localized versions of trending products. The market shows sustained demand for European dark chocolates, Japanese matcha combinations, and Southeast Asian fruit-infused varieties. Korean manufacturers have adapted by creating fusion products that combine traditional Korean ingredients, such as red bean paste and green tea, with international chocolate formats. This trend is particularly strong among young consumers, who view chocolate consumption as both a cultural expression and an opportunity for social media content.

Rising Popularity of Premium and Artisanal Chocolates

The luxury chocolate segment in South Korea demonstrates significant market expansion, surpassing the broader confectionery market's performance. This growth reflects a fundamental shift in consumer behavior, where Korean buyers increasingly prioritize premium quality over quantity in their chocolate purchases. The trend is particularly pronounced among urban professionals and dual-income households, whose rising disposable income enables exploration of premium confectionery options. International luxury brands, including Godiva, ROYCE', and Hotel Chocolat, have strategically established their presence through exclusive boutiques in premium shopping districts, while domestic manufacturers have invested substantially in developing artisanal production capabilities to compete in this profitable market segment. The premium chocolate category has evolved beyond product quality to encompass sophisticated packaging design, compelling brand narratives, and immersive retail experiences that justify premium price positioning. The market sees growing consumer interest in single-origin chocolates and bean-to-bar products, appealing to discerning customers who value craftsmanship and supply chain transparency. The strong corporate gifting culture in Korea further drives premium chocolate sales, with businesses selecting luxury chocolates for client relationship management and employee recognition during traditional gift-giving seasons.

Growing Demand for Organic, Vegan, and Gluten-Free Chocolates

Korean consumers demonstrate a strong inclination toward functional chocolate alternatives that harmonize with their health and wellness aspirations while fulfilling their desire for indulgence. The country's zero-sugar movement has transformed the carbonated beverage market, subsequently influencing the chocolate segment, where sugar-free variants exhibit robust market performance. Rising consumer consciousness regarding pesticide residues and environmental sustainability propels the demand for organic chocolate products, while vegan alternatives resonate with the younger demographic embracing plant-based lifestyle choices. Korean manufacturers establish strategic partnerships with health food companies to innovate products incorporating alternative sweeteners such as stevia and monk fruit. International brands have responded to the increasing awareness of celiac disease by introducing gluten-free certified offerings. This health-conscious evolution aligns seamlessly with Korea's deep-rooted emphasis on functional foods, fostering a dynamic market for enhanced chocolate products featuring probiotics, collagen, and traditional Korean ingredients like ginseng and red ginseng.

Expansion of Global Brands and International Offerings

International chocolate manufacturers are strategically expanding their footprint in South Korea by capitalizing on the strong consumer preference for foreign food brands and the advantageous trade conditions established under the Korea-US Free Trade Agreement. Mars, a significant player in the global confectionery market, has demonstrated substantial market penetration through carefully crafted localized products and strategic retail partnerships. International brands have successfully integrated into South Korea's deeply rooted gift-giving traditions by developing market-specific packaging solutions and seasonal product offerings tailored to local celebrations and customs. Following the established pattern of other multinational food companies, these manufacturers are investing in domestic production facilities across South Korea to optimize their supply chain operations and reduce import-related expenses, thereby strengthening their competitive position in the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter food labeling and regulatory requirements for ingredients | -0.3% | National, enforced by MFDS nationwide | Short term (≤ 2 years) |

| Complexity in logistics for cold-chain chocolate delivery | -0.2% | National, particularly affecting rural and remote areas | Medium term (2-4 years) |

| Volatility in foreign exchange affecting import costs/pricing | -0.4% | National, impacting all imported chocolate products | Short term (≤ 2 years) |

| Sustainability demands raising production and packaging costs | -0.2% | National, driven by corporate ESG compliance requirements | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Food Labeling and Regulatory Requirements for Ingredients

The Ministry of Food and Drug Safety (MFDS) maintains a comprehensive regulatory framework for chocolate products, which significantly impacts market dynamics, especially affecting small-scale importers and artisanal producers. The regulations encompass detailed Korean-language labeling requirements, including comprehensive ingredient declarations, nutritional content information, allergen notifications, and manufacturing facility documentation. The standards establish specific minimum cocoa content thresholds for different chocolate categories [1]Source: Ministry of Food and Drug Safety, “Labeling and Ingredient Rules,” mfds.go.kr. For international manufacturers, HACCP certification protocols add substantial complexity to the market entry process. The regulations also mandate strict lead content limitations for cocoa powder, necessitating thorough testing procedures. The MFDS food additive approval system restricts manufacturers to using only approved substances in their formulations, which constrains product innovation and the development of new ingredient combinations. While these regulatory measures ensure consumer protection and food safety, they create significant market entry challenges that favor established companies with robust compliance infrastructure over smaller specialty producers.

Complexity in Logistics for Cold-Chain Chocolate Delivery

The chocolate supply chain in Korea faces significant operational challenges and mounting cost pressures due to stringent temperature-controlled distribution requirements. This is particularly evident during the summer months when ambient temperatures substantially exceed the optimal storage conditions for chocolate products. Premium and artisanal chocolates demand even more rigorous temperature controls to preserve their quality characteristics and prevent bloom formation throughout the transportation and storage processes. The rapidly expanding e-commerce chocolate retail market has intensified the demand for sophisticated cold-chain solutions, as direct-to-consumer deliveries require specialized packaging and time-sensitive shipping protocols. The distribution challenges become more pronounced in rural and remote areas, where extended transportation distances and limited cold-storage infrastructure create substantial barriers to market expansion. Domestic manufacturers and importers must make substantial investments in comprehensive cold-chain infrastructure, including refrigerated warehousing facilities, temperature-controlled transportation vehicles, and specialized packaging materials, resulting in increased operational costs throughout the distribution network.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Dark Chocolate Gains Health-Conscious Momentum

Dark chocolate is experiencing significant momentum in the South Korean confectionery market, with projections indicating a CAGR of 3.60% through 2031. This growth trajectory is particularly noteworthy when compared to the established dominance of milk and white chocolate segments, which currently command a substantial 63.12% market share in 2025. The increasing consumer preference for dark chocolate aligns with broader health and wellness trends in Korea, where consumers actively seek products with higher cocoa content. The viral Dubai chocolate phenomenon has further amplified dark chocolate's appeal, as Korean consumers increasingly associate darker varieties with premium quality and sophisticated taste profiles.

The traditional milk and white chocolate segments continue to maintain their market leadership position through deeply entrenched consumer preferences and extensive retail distribution networks. These segments particularly excel during cultural gift-giving occasions such as Valentine's Day and White Day, where they remain the preferred choice for many consumers. The market demonstrates clear generational preferences, with younger consumers gravitating toward dark chocolate variants due to their perceived health benefits and lower sugar content. In contrast, older demographic groups maintain their loyalty to conventional milk chocolate formulations. White chocolate occupies a distinct market position, finding its primary applications in seasonal product launches and premium confectionery offerings, where it serves specific consumer preferences and usage occasions.

By Category: Sugar-Free Alternatives Accelerate Amid Wellness Trends

The South Korean chocolate market remains firmly anchored in traditional sugar-based products, which account for 81.70% of market share in 2025. This dominance reflects deeply ingrained consumer preferences and well-established manufacturing processes that have been refined over decades. However, the market is experiencing a notable shift as sugar-free alternatives emerge as a significant growth segment, advancing at a 3.44% CAGR through 2031.

South Korea's transformation in zero-sugar consumption patterns is reflected in the substantial expansion of the carbonated beverage alternatives market during the post-pandemic period. Companies like Lotte Chilsung are strategically diversifying their sugar-free product portfolios to address the evolving preferences of health-conscious consumers. This market adaptation specifically targets individuals managing diabetes, consumers focused on weight management, and parents seeking nutritionally balanced beverage options for their children.

By Price Tier: Luxury Segment Outpaces Mass Market

Mass-market chocolate dominates the South Korean confectionery landscape with a 54.10% market share in 2025. This significant market presence is attributed to established distribution networks spanning convenience stores, supermarkets, and online platforms, combined with competitive pricing strategies that ensure broad consumer accessibility. Meanwhile, the luxury and artisanal segments demonstrate robust growth potential, projected to expand at a 3.62% CAGR through 2031, indicating a notable shift in consumer preferences.

The market's evolution reflects the sophisticated purchasing behavior of Korean consumers who balance everyday chocolate consumption with premium indulgences. The premium segment's growth trajectory is strengthened by the strategic expansion of international luxury brands into the Korean market, alongside the emergence of local artisanal chocolatiers. This growth is further amplified by Korea's deeply rooted corporate gifting culture, where premium chocolate presentations serve as important business relationship tools. Luxury chocolate manufacturers have successfully positioned their products by emphasizing traditional craftsmanship, authenticating single-origin cocoa sourcing, and creating immersive retail environments that validate their premium pricing structure.

By Distribution Channel: Online Retail Transforms Shopping Patterns

The retail landscape for chocolate distribution in South Korea demonstrates a clear dominance of traditional brick-and-mortar establishments, with supermarkets and hypermarkets commanding a substantial 46.05% market share in 2025. This leadership position stems from their widespread physical presence across urban and suburban areas, combined with deeply ingrained consumer shopping patterns. In parallel, the online retail segment is experiencing significant momentum, projected to expand at a 3.81% CAGR through 2031, as consumers increasingly embrace digital shopping platforms. This shift reflects broader changes in South Korean retail dynamics, particularly evident in the surge of online food purchases among younger generations and time-constrained dual-income households. The convenience store channel maintains its robust performance through strategically positioned outlets, capitalizing on impulse purchases and implementing agile product rotation strategies to feature trending items like Dubai chocolate varieties. Specialty stores have carved out their niche by focusing on premium, organic, and imported chocolate selections, where product expertise and carefully curated assortments serve discerning consumers.

The digital transformation of retail channels has created new market opportunities, particularly for direct-to-consumer brands, subscription services, and businesses offering personalized chocolate products. This market evolution has simplified distribution, allowing artisanal chocolate producers to reach consumers nationwide without extensive physical retail networks. Established chocolate brands are using e-commerce platforms to launch new products and build customer relationships through digital engagement. The combination of traditional retail presence and digital channels demonstrates the transformation of chocolate retail in South Korea's consumer market. South Korea's e-commerce market continues to expand, with food and beverage leading at 30% of total online sales. The market is projected to grow at a CAGR of 7.8% through 2028, supported by robust digital infrastructure, secure payment systems, and high consumer confidence in online shopping .

Geography Analysis

The South Korean chocolate market functions within a unified national framework, with regional variations reflecting population density and urban-rural distribution patterns. The Seoul metropolitan area and major urban centers, including Busan, Daegu, and Incheon, remain instrumental in driving consumption patterns. These regions benefit from substantial consumer purchasing power, strong international brand presence, and advanced retail infrastructure that effectively supports premium product segments.According to International Monetary Fund South Korea's GDP per capita based on purchasing power parity (PPP) is projected to reach approximately USD 65,110 in 2025, reflecting strong consumer purchasing power well above the global average .

The geographic distribution mirrors South Korea's predominantly urban population structure, creating concentrated demand centers that enable streamlined distribution and marketing approaches. International chocolate manufacturers typically choose Seoul as their entry point before expanding their presence to other major cities. Meanwhile, domestic companies like Lotte and Orion have established comprehensive distribution networks that effectively serve consumers across both urban and rural markets.

Rural areas face distinct challenges in cold-chain logistics, where extended transportation routes and insufficient refrigerated infrastructure limit the availability of premium products and online shopping options. The Ministry of Food and Drug Safety implements comprehensive regulatory standards throughout the country, ensuring consistent product quality and safety requirements across regions. This regulatory uniformity creates favorable conditions for implementing national brand strategies and managing import procedures effectively.

Competitive Landscape

The South Korean chocolate market demonstrates a balanced competitive environment, where established Korean conglomerates operate alongside international brands. Each player employs distinct positioning strategies and leverages distribution networks to maintain market presence. Domestic industry leaders Lotte Wellfood and Orion have built their success on deep-rooted local market understanding, strong retail partnerships, and the ability to develop products that resonate with Korean cultural preferences. Meanwhile, international companies such as Mars, Ferrero, and Nestlé maintain their competitive edge through established global brand recognition and premium market positioning. This market structure has created viable opportunities for artisanal producers and specialty brands that focus on serving health-conscious consumers, premium gift markets, and specific flavor preferences that remain underserved by mass-market companies.

The adoption of advanced technology has emerged as a crucial differentiator in the competitive landscape, particularly in areas such as e-commerce capabilities, supply chain optimization, and consumer engagement platforms. These technological advancements enable companies to effectively capture and respond to emerging trends, such as the recent Dubai chocolate phenomenon. Market participants continue to enhance their operations through investments in cold-chain logistics infrastructure, digital marketing initiatives, and sophisticated data analytics systems, allowing them to better understand and respond to evolving consumer preferences with agile product development strategies.

The current market dynamics indicate significant potential for industry consolidation through various strategic initiatives. Companies are exploring opportunities for partnerships, acquisition activities, and joint ventures that effectively combine local market expertise with international brand portfolios. These strategic alignments allow organizations to leverage complementary strengths, particularly in technological capabilities and market access, creating more robust and competitive business entities in the South Korean chocolate market.

South Korea Chocolate Industry Leaders

Lotte Wellfood Co., Ltd.

Orion Confectionery Co., Ltd.

Crown Confectionery Co., Ltd.

Ferrero International S.A.

Mars, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Orion Corp. announced a $580 million investment over three years to expand its snack manufacturing capacity, bolstering its position in the South Korean chocolate and confectionery market.

- October 2024: Saudi Arabia’s Vlinder Chocolate entered South Korea capitalizing on the viral “Dubai chocolate” trend. The brand introduced six Middle Eastern-inspired chocolate flavors, gained approval through strict import requirements, and is now sold via major Korean e-commerce platforms.

- March 2023: South Korea Lotte Confectionery Co. announced its rebranding with the name of Lotte Wellfood as part of further global expansion. The company supplies sweets, chocolates, biscuits, and snacks and the market expansion will further help the company grow.

South Korea Chocolate Market Report Scope

Chocolate is a food product made from the fruit of a cacao tree (Theobroma cacao) and is available as solid, liquid, or paste. South Korea Chocolate Market is segmented by type, product, and distribution channel. By type, the market is further segmented into milk/white chocolate and dark chocolate. By product, the market is divided into soft lines/selflines, boxed assortments, countlines, seasonal chocolates, molded chocolates, and others. By distribution channel, the market is further segmented into supermarkets/ hypermarkets, specialist retailers, convenience/grocery stores, online retail stores, and other distribution channels. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Type

| Dark Chocolate |

| Milk and White Chocolate |

By Category

| Sugar |

| Sugar- free |

By Price Tier

| Mass |

| Premium |

| Luxury/Artisanal |

By Distribution Channel

| Supermarkets/ Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail |

| Others |

| By Type | Dark Chocolate |

| Milk and White Chocolate | |

| By Category | Sugar |

| Sugar- free | |

| By Price Tier | Mass |

| Premium | |

| Luxury/Artisanal | |

| By Distribution Channel | Supermarkets/ Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail | |

| Others |

Key Questions Answered in the Report

How fast is the South Korea chocolate market expected to grow to 2031?

The South Korea chocolate market value is projected to advance from USD 732.06 million in 2026 to USD 824.68 million by 2031, reflecting a 2.41% CAGR.

Which chocolate type is seeing the quickest uptake among Korean consumers?

Dark chocolate leads in growth with a 3.60% CAGR, propelled by wellness perceptions and social-media flavor trends.

Why are sugar-free chocolates gaining traction?

Rising health awareness and the broader national zero-sugar movement have lifted sugar-free chocolate sales at a 3.44% CAGR.

What role does e-commerce play in chocolate distribution?

Online retail is the fastest-growing channel, expanding at a 3.81% CAGR thanks to same-day delivery services and temperature-controlled packaging.

How does MFDS regulation shape the market?

Strict cocoa-content and labeling rules elevate compliance costs but also reinforce consumer confidence in product safety across all brands.

Page last updated on: