South Africa Molded Case Circuit Breaker (MCCB) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

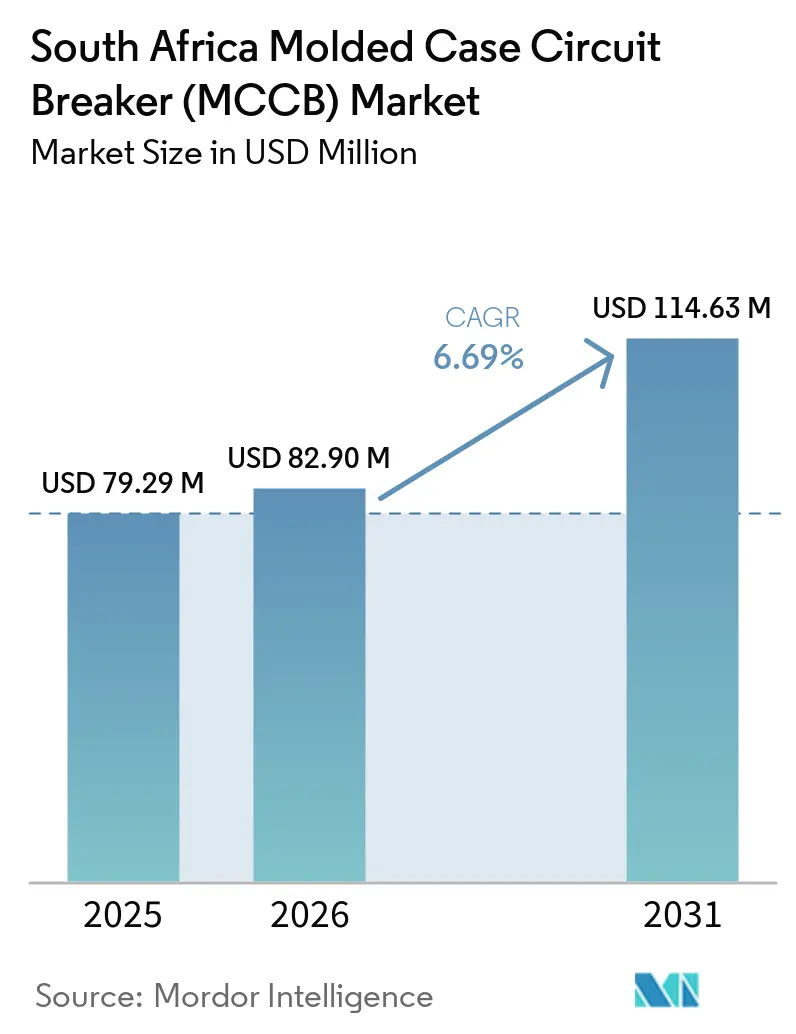

| Base Year Market Size (2025) | USD 79.29 Million |

| Market Size (2026) | USD 82.90 Million |

| Market Size (2031) | USD 114.63 Million |

| Growth Rate (2026 - 2031) | 6.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Molded Case Circuit Breaker (MCCB) Market Analysis by Mordor Intelligence

The South Africa Molded Case Circuit Breaker Market size was valued at USD 79.29 million in 2025 and is estimated to grow from USD 82.90 million in 2026 to reach USD 114.63 million by 2031, at a CAGR of 6.69% during the forecast period (2026-2031). The South Africa molded case circuit breaker (MCCB) market is benefiting from a rare overlap of transmission expansion, commercial and industrial solar with storage adoption, and large data center construction, which is lifting demand across both standard and high-specification protection applications.[1]Equinix, “Equinix Expands In South Africa,” Equinix, Eskom’s transmission and distribution expansion plan is creating a direct equipment pipeline because every new substation, feeder upgrade, and renewable connection point needs low-voltage protection at auxiliary and interface levels. The South Africa molded case circuit breaker (MCCB) market is also being shaped by a dual-speed buying pattern, with price-led decisions in mainstream building and light industrial projects and performance-led decisions in utility, storage, and data center installations. Competitive conditions remain firm in the premium tier because Schneider Electric, ABB, Eaton, and Siemens influence specifications early in the project cycle, while CBI-electric and ACTOM defend local positions through certification depth, local compliance support, and rand-based pricing. Upside remains constrained by exchange-rate swings and grey-market inflows, but certified products continue to gain traction where procurement teams cannot absorb compliance or liability risk under formal project conditions.

Key Report Takeaways

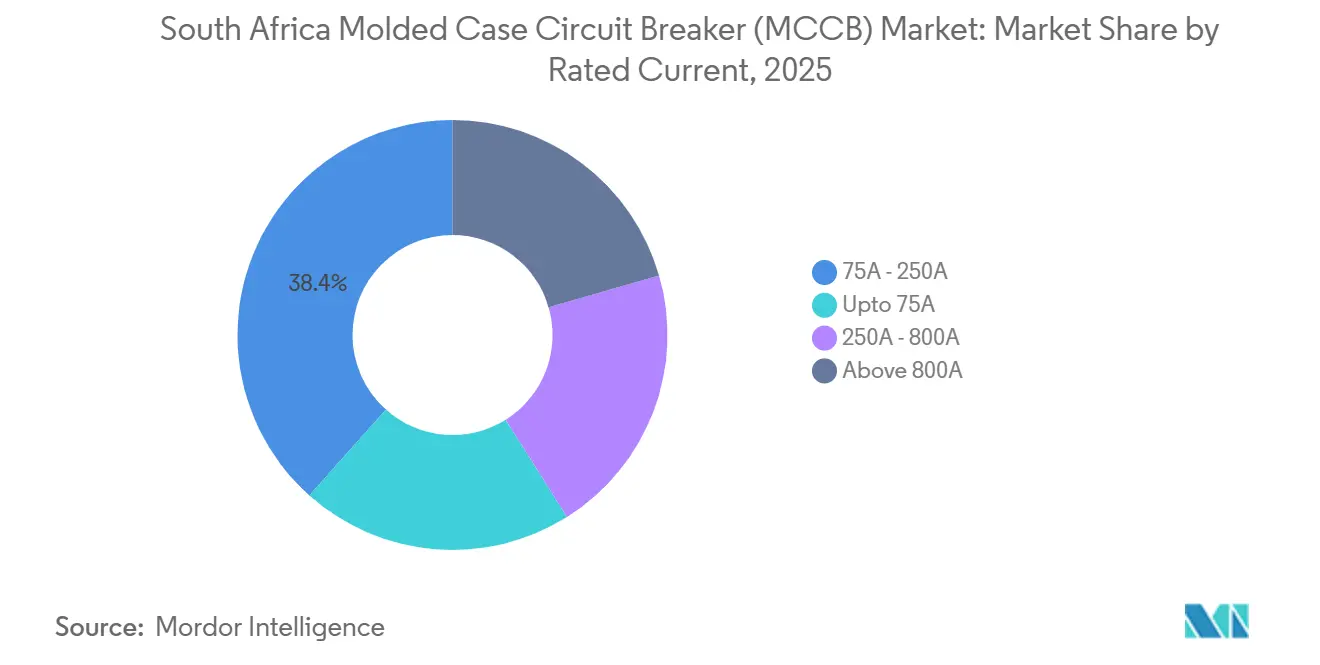

- By rated current, 75A to 250A held 38.4% of the South Africa molded case circuit breaker (MCCB) market size in 2025, while 250A to 800A is projected to expand at a 7.1% CAGR through 2031.

- By trip-unit technology, thermal-magnetic units held 52.6% of South Africa molded case circuit breaker (MCCB) market share in 2025, while microprocessor-based units recorded the highest projected CAGR at 8.4% through 2031.

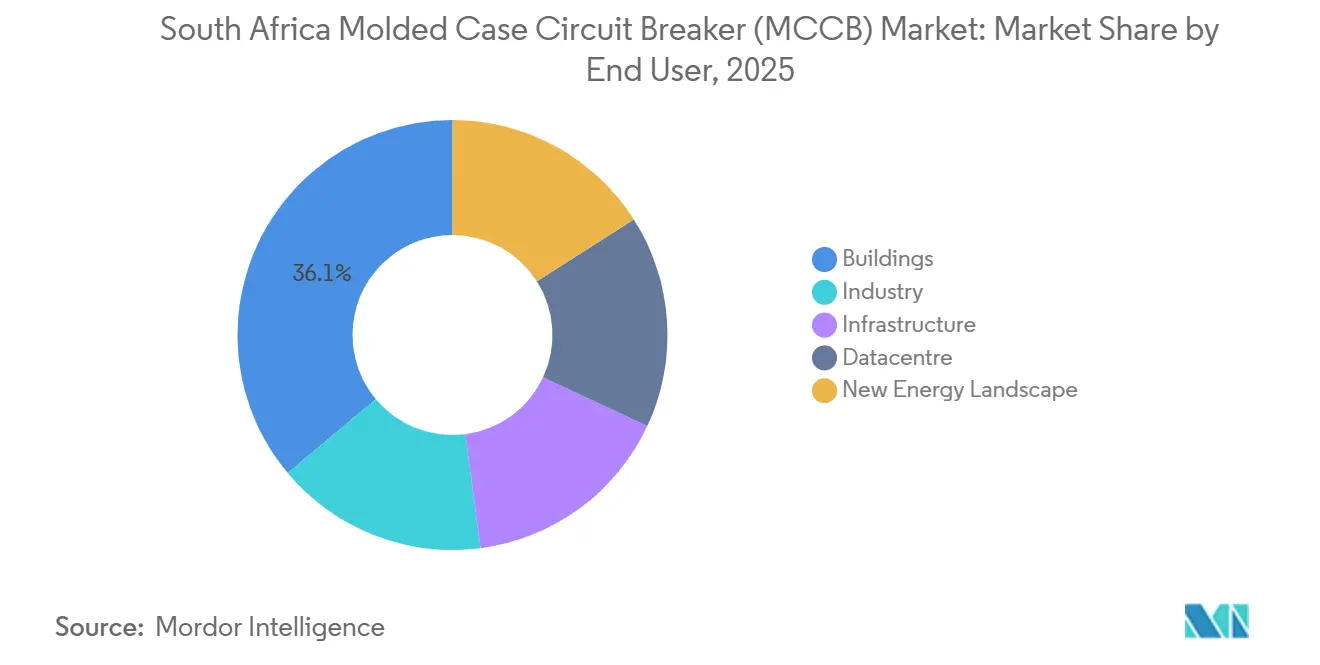

- By end user, buildings accounted for 36.1% of the South Africa molded case circuit breaker (MCCB) market size in 2025, while the data center segment is advancing at a 12.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Molded Case Circuit Breaker (MCCB) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Eskom grid build-out and substation expansion | +2.0% | National, concentrated in Gauteng, Mpumalanga, Northern Cape, and Limpopo transmission corridors | Medium term (2-4 years) |

| C&I solar plus storage protection demand | +1.4% | National, strongest in Gauteng, Western Cape, and KwaZulu-Natal | Short term (≤ 2 years) |

| Industrial retrofit and backup-power hardening | +1.1% | National, concentrated in Limpopo, North West, and Eastern Cape industrial clusters | Medium term (2-4 years) |

| Compliance-led shift toward certified premium breakers | +0.7% | National, with early gains in data center and infrastructure-grade project channels | Medium term (2-4 years) |

| Expansion of locally stocked project channels | +0.5% | Urban centers and tier-2 distribution hubs nationally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Eskom Grid Build-Out and Substation Expansion

South Africa’s grid expansion cycle is creating a measurable demand floor for MCCBs across transmission and distribution interfaces.[2]Eskom, “Transmission Development Plan 2025-2034,” Eskom, Eskom’s 5-year capital program targets 8,362 km of new transmission lines, 82,415 MVA of transformer capacity, 1,714 km of distribution lines, and 1,110 MVA of distribution transformer capacity by 2031, which directly raises procurement needs for low-voltage auxiliary protection, motor starter protection, and ancillary supply circuits. Each main transmission station typically needs several hundred MCCB units across low-voltage boards, so volume growth is tied to the number and scale of new stations rather than only to headline grid spending. The Independent Transmission Projects Procurement Programme adds another layer because private line developers tend to favor certified and digitally compatible protection equipment, which supports higher average selling prices in the South Africa molded case circuit breaker (MCCB) market. Policy support also remains clear, with the Ministry confirming in May 2026 that transmission expansion is central to the country’s energy transition path, which lowers pipeline uncertainty for switchgear suppliers.

C&I Solar Plus Storage Protection Demand

Commercial and industrial embedded generation is now a major demand engine for breaker selection in rooftop, ground-mount, and hybrid energy systems. South Africa’s C&I embedded generation base passed 5.6 GW by January 2026, after 1.6 GW of new solar capacity was added in 2025, and this installed base is increasingly being paired with battery storage as tariff pressure and storage economics improve. Each solar plus storage project requires MCCBs for inverter protection, bus sectioning, AC sub-distribution, and disconnect duties, which places most of the demand in the 75A to 800A range. JUWI Renewable Energies committed ZAR 6 billion, which was USD 320 million, to build 340 MW of private solar projects in 2025 for customers including Teraco, Glencore, Sasol, and Air Liquide, showing the project scale now feeding the South Africa molded case circuit breaker (MCCB) market. The move from solar-only systems to hybrid battery-backed systems is also shortening replacement cycles because legacy breakers often do not meet the fault withstand and selective coordination needs that newer storage architectures demand.

Industrial Retrofit and Backup-Power Hardening

Manufacturing, mining, and agribusiness sites are increasing electrical upgrades after years of deferred maintenance during the load-shedding period. Backup generators, UPS installations, and battery energy storage systems create secondary MCCB demand at incoming feeders, bus ties, and generator paralleling points, which supports above-average value growth in higher current frames. ACTOM’s acquisition of JUEL Batteries for storage expansion shows how local electrical equipment firms are repositioning around integrated power hardening, and those broader system scopes usually bundle breaker specification into the overall project package. WEG Africa reinforced its South African manufacturing presence in May 2026, and that improves lead times for industrial retrofit work while supporting locally available IEC 60947-2 certified products across demanding current ranges. This broadens the serviceable opportunity for the South Africa molded case circuit breaker (MCCB) market because retrofit projects increasingly need certified protection that aligns with legal duties under occupational safety and electrical installation rules.

Compliance-Led Shift Toward Certified Premium Breakers

The shift from uncertified devices toward SABS and NRCS-compliant products is becoming one of the most durable quality changes in the South Africa molded case circuit breaker (MCCB) market. Joint 2025 enforcement actions by the SAPS Anti-Counterfeit Unit and the NRCS increased scrutiny on non-compliant circuit breakers sold through informal channels and online platforms, which pushed specifiers and contractors to tighten document checks before project award. This shift is strongest in data center, utility, and REIPPPP-linked procurement because those buyers routinely require valid LOA certification and SANS 60947-2 type-test documentation before products are approved. The same compliance cycle is helping locally stocked certified channels expand because contractors prefer product availability that does not depend on lengthy new import approvals, and that supports faster project conversion for approved suppliers. NRCS compulsory specification VC 8036 and SANS 60947-2 remain the baseline rules behind this shift, and those standards favor suppliers that can combine certification depth with responsive local support.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FX-linked import cost volatility | -1.0% | National, most acute for importers without local production or natural ZAR-denominated hedging | Short term (≤ 2 years) |

| LOA interpretation and approval delays | -0.6% | National, with greater impact on smaller importers and new product entrants | Medium term (2-4 years) |

| Grey-market uncertified breaker inflows | -0.8% | National, concentrated in price-sensitive commercial and residential distribution channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

FX-Linked Import Cost Volatility

Exchange-rate volatility remains a direct cost pressure because most MCCBs sold in South Africa are imported from Europe, Asia, or Brazil. The USD to ZAR rate touched ZAR 17.25 on March 23, 2026, before recovering to ZAR 16.40 by mid-May 2026, and that swing quickly changes landed cost assumptions for distributors and import-led brands. For suppliers without local production or effective hedging, a weaker rand can erase operating margin gains that higher shipment volumes would otherwise deliver. The South Africa molded case circuit breaker (MCCB) market, therefore, sees periodic inventory caution because distributors cut safety stock when replacement cost visibility becomes weak. That behavior creates short-term availability gaps and gives locally priced suppliers such as CBI-electric and ACTOM a structural advantage during volatile periods.

Grey-Market Uncertified Breaker Inflows

Grey-market inflows continue to distort pricing in the lower end of the South Africa molded case circuit breaker (MCCB) market, especially in price-sensitive commercial and residential channels. Safehouse stated in April 2026 that 65% of South African consumers prioritize price above all else, which helps low-cost non-compliant products find buyers despite the safety risk. NRCS capacity constraints add to the problem because limited post-market surveillance and lengthy approval handling make it harder to keep pace with the scale of imported low-voltage products entering the country. This creates a two-tier structure where compliant suppliers carry the full cost of certification, while unregistered imports undercut them on shelf price without matching documentation or proven trip performance. The issue is most damaging where purchasers focus on upfront cost, but it is less effective in formal projects because responsible-person liability under South African installation and safety rules keeps certified products preferred in high-value applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rated Current: Mid-Range Volume Leads While Higher Frames Grow Faster

The 75A to 250A band held 38.4% of the South Africa molded case circuit breaker (MCCB) market size in 2025, making it the value leader across the country’s active building, sub-main, and light industrial panel applications. This range benefits from the broadest installer familiarity, the deepest local stocking, and the strongest price competition, so it remains the default choice for many building services projects in Gauteng, Cape Town, and other urban centers. It also faces the heaviest grey-market pressure because buyers in lower-risk commercial circuits are more likely to trade down when the performance gap is not immediately visible. VC 8036 applies across current ranges and sets the same formal entry barrier for all suppliers, but enforcement gaps still matter most in this mid-volume band.

The 250A to 800A segment is projected to expand at a 7.1% CAGR through 2031, which makes it the fastest-growing rated-current range in the South Africa molded case circuit breaker (MCCB) market. Demand is being lifted by inverter-side AC protection, storage bus sectioning, and transformer secondary protection in industrial, solar, and data center projects. Commercial rooftop and ground-mount solar systems in the 100 kW to 1 MW range usually require breaker frames between 250A and 630A, so the rise of solar plus battery systems maps closely to this band’s growth path. At the low end, up-to-75A products face gradual substitution from DIN-rail miniature circuit breakers, while above-800A frames remain a narrower specification-led niche for large facilities where OEMs such as WEG, ABB, and Schneider Electric compete directly through engineering channels.

By Trip-Unit Technology: Thermal-Magnetic Breadth Meets Digital Upgrade Demand

Thermal-magnetic trip units accounted for 52.6% of South Africa molded case circuit breaker (MCCB) market share in 2025, supported by lower acquisition cost and broad suitability for standard industrial and commercial duty. In many building distribution boards, agricultural sites, and conventional motor starter applications, the fixed overload profile of thermal-magnetic units remains adequate for the operating requirement. Their position is also protected by installer familiarity, spare-part availability, and lower sensitivity to harsh electrical environments in some industrial locations. For those reasons, thermal-magnetic units continue to anchor the installed base across much of the South Africa molded case circuit breaker (MCCB) industry.

Electronic trip units occupy the middle layer of the technology mix because they add programmable protection curves that help designers isolate faults without tripping entire feeders. Microprocessor-based MCCBs are projected to grow at an 8.4% CAGR through 2031, reflecting stronger demand from data centers and advanced infrastructure projects where communications, fault logging, and selective coordination are no longer optional. These features are increasingly important in Tier III and Tier IV data center designs, where protection coordination is part of uptime strategy rather than only a compliance exercise. ABB’s September 2025 expansion of its manufacturing footprint for Emax 3 and related protection products also points to stronger global capacity support for high-specification breaker families that South African buyers will increasingly require.

By End User: Buildings Provide Scale While Data Centers Set the Growth Pace

Buildings held a 36.1% share in 2025, which made them the largest end-user base for the South Africa molded case circuit breaker (MCCB) market. Commercial construction, mixed-use development, retail rollouts, and formal electrification projects continue to create steady replacement and new-installation demand for standard breaker ranges. This segment supports the scale economics of the 75A to 250A band because those frames match common distribution duties in building services. SANS 10142-1 also gives the formal contractor channel a compliance floor that favors documented products over low-cost, uncertified alternatives.

Industry, infrastructure, and the new energy landscape are all growing at mid-range rates, but data centers stand out with a 12.3% CAGR through 2031. South Africa’s live critical IT capacity stood at 300 MW to 350 MW in 2025, with another 120 MW to 200 MW announced or under construction, which shows why the South Africa molded case circuit breaker (MCCB) market is moving toward higher-specification selections in this segment. Equinix announced plans in March 2026 to add 160 MW across Johannesburg and Cape Town as part of a ZAR 7.5 billion (~USD 0.45 billion) investment program, and Microsoft also committed an additional USD 329 million to South African data center investment, reinforcing a multi-year project flow for advanced protection equipment. Because these projects are designed through engineering consultancies and carry strict documentation requirements, certified electronic and microprocessor-based breakers hold a structural advantage over grey-market options.

Geography Analysis

Gauteng represented the dominant regional demand center in 2026, supported by its concentration of commercial construction, industrial activity, and large data center campuses. Johannesburg and Pretoria host the deepest hyperscale project pipeline, including Teraco’s JB7 phase and Vantage’s 80 MW campus, both of which create breaker demand from incoming protection to generator bus tie and low-voltage sub-distribution. Eskom’s distribution business has committed ZAR 38 billion (~USD 2.30 billion) over 5 years to network upgrades nationwide, and Gauteng’s urban density makes it the most project-intensive location within that program. JUWI’s 2025 solar portfolio, which included projects serving Teraco in Johannesburg, shows how self-generation and core facility electrical protection are now being specified together at the same site.

The Western Cape is now a co-primary demand zone for the South Africa molded case circuit breaker (MCCB) market because it combines a stronger compliance culture, renewable energy density, and expanding data center activity. Teraco’s CT2 Cape Town expansion, completed in November 2025, added 32 MW across 8 halls with on-site solar and battery storage, which increased project demand at every power conversion interface. Schneider Electric’s March 2026 deployment of RM AirSeT at Western Cape Fruit Processors in Grabouw highlights the broader industrial upgrade trend in the province, where medium-voltage renewal often triggers accompanying low-voltage protection replacement SE.COM. The City of Cape Town and the Western Cape’s agricultural base are also pushing resilience planning, which keeps backup power and distributed energy projects active outside the traditional construction cycle. South Africa added between 2.5 GW and 3 GW of solar capacity across 2024 and 2025, and a meaningful share of that activity was tied to Western Cape commercial and agricultural demand.

KwaZulu-Natal, the Northern Cape, and Limpopo remain smaller in value, but they are structurally important growth regions for the South Africa molded case circuit breaker (MCCB) market. KwaZulu-Natal’s port, logistics, and cold-chain upgrades are supporting demand in the 250A to 800A range because automation and refrigerated handling systems require more robust distribution protection. The Northern Cape and Limpopo sit closer to the country’s renewable build-out, and each new solar or wind facility needs MCCBs for auxiliary power and related low-voltage distribution. NTCSA’s 75 active transmission projects targeting 37 GW of new generation connection capacity by 2030 give these provinces a clear infrastructure pipeline, especially for suppliers that can support field service outside the main metros.

Competitive Landscape

The South Africa molded case circuit breaker (MCCB) market is moderately consolidated in the premium tier, where Schneider Electric, ABB, Eaton, and Siemens shape specifications through engineering relationships, technical sales depth, and established local distribution. Their position is reinforced by strong SANS 60947-2 documentation and LOA compliance records, which remain critical in data center, utility, and infrastructure-grade procurement. Schneider Electric’s Africa Innovation Hub in Midrand and its March 2026 NExT program show how premium players are shifting from simple product sales toward bundled electrification and automation solution models SE.COM. That strategy matters because the South Africa molded case circuit breaker (MCCB) market increasingly rewards vendors that can influence the full switchgear and energy-management stack at the specification stage.

Local manufacturers keep meaningful positions because they can combine rand-based pricing, faster delivery, and South African certification support in ways many imported brands must reproduce through local partners. CBI-electric and ACTOM are strongest where buyers value auditable compliance records and localized service response, especially in formal utility, industrial, and contractor channels. ACTOM’s July 2025 Customer Experience Centre in Johannesburg strengthened its engagement with specifiers and end users at a time when local-content preference is becoming more visible in project procurement. Siemens South Africa’s May 2026 localization of 8DA medium-voltage switchgear manufacturing with Private National Grid also fits this pattern because localized production improves local-content credentials and reduces import exposure. These moves support a competitive environment where the South Africa molded case circuit breaker (MCCB) market remains open, but scale advantages are strongest for suppliers with local technical depth.

The mid-market tier is more fragmented, with WEG, Legrand, Hager, LOVATO, CHINT, and other brands competing across distributor-led channels. WEG’s May 2026 financing partnership with Energy Venture Capital is strategically important because it embeds WEG equipment into funded hybrid energy projects and creates a more captive route to specification. Chinese suppliers remain active in the 75A to 250A band because price competition is sharp there, but their position is weaker in higher-specification projects where documentation depth and certification responsiveness matter more. The clearest white-space opportunity in the South Africa molded case circuit breaker (MCCB) market remains the new energy landscape, where locally stocked, NRCS-compliant products tailored for battery storage and renewable auxiliary power could secure early reference wins.

South Africa Molded Case Circuit Breaker (MCCB) Industry Leaders

Schneider Electric SE

ABB Ltd

Eaton Corp plc

Siemens AG

Legrand SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: WEG Africa and Energy Venture Capital formed a funding partnership to co-finance hybrid energy projects in South Africa, with facility amounts ranging from R5 million to R500 million (approximately USD 30.5 million) per project. The partnership integrates WEG's low- and medium-voltage switchgear, BESS, solar, and EV charging infrastructure as specified system components within financed deployments, creating a captive MCCB specification channel in the C&I energy transition segment.

- May 2026: Siemens South Africa announced the localisation of its 8DA gas-insulated medium-voltage switchgear manufacturing in partnership with Private National Grid. The move reduces import dependency for grid infrastructure, deepens local content credentials, and positions Siemens for expanded participation in NTCSA's R157 billion (approximately USD 9.6 billion) five-year transmission capital programme.

South Africa Molded Case Circuit Breaker (MCCB) Market Report Scope

The Molded Case Circuit Breaker (MCCB) is engineered to shield circuits from overcurrents, overloads, and short circuits. Encased in robust molded plastic for enhanced durability, the MCCB is adept at managing higher current capacities compared to its standard circuit breaker counterparts.

The South Africa Molded Case Circuit Breaker (MCCB) Market is segmented into rated current, trip-unit technology, and end-user. By rated current, the market is segmented into up to 75A, 75A–250A, 250A–800A, and above 800A. By trip-unit technology, the market is segmented into thermal-magnetic, electronic, and microprocessor-based systems. By end-user, the market is segmented into buildings, industry, infrastructure, datacentre, and new energy landscape applications. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Upto 75A |

| 75A - 250A |

| 250A - 800A |

| Above 800A |

| Thermal-Magnetic |

| Electronic |

| Microprocessor-Based |

| Buildings |

| Industry |

| Infrastructure |

| Datacentre |

| New Energy Landscape |

| By Rated Current | Upto 75A |

| 75A - 250A | |

| 250A - 800A | |

| Above 800A | |

| By Trip-Unit Technology | Thermal-Magnetic |

| Electronic | |

| Microprocessor-Based | |

| By End User | Buildings |

| Industry | |

| Infrastructure | |

| Datacentre | |

| New Energy Landscape |

Key Questions Answered in the Report

What is current market size of South Africa molded case circuit breaker market?

The South Africa Molded Case Circuit Breaker Market size was valued at USD 79.29 million in 2025 and is estimated to grow from USD 82.90 million in 2026 to reach USD 114.63 million by 2031, at a CAGR of 6.69% during the forecast period (2026-2031).

Which rated current range is leading demand in South Africa?

The 75A to 250A range led with 38.4% of value in 2025 because it matches mainstream commercial building and light industrial distribution needs.

Which current band is growing the fastest?

The 250A to 800A range is projected to grow at 7.1% CAGR through 2031, supported by solar inverter protection, battery storage, and transformer secondary applications.

Why are data centers important for breaker suppliers in South Africa?

Data centers are the fastest-growing end-user segment, with a 12.3% CAGR through 2031, and they require advanced breaker coordination, communications capability, and strict certification support.

What is limiting sales in lower-priced channels?

Exchange-rate volatility raises import costs, while uncertified grey-market products continue to pressure compliant suppliers in price-sensitive channels.

Which trip-unit technology is growing fastest?

Microprocessor-based breakers are projected to grow at 8.4% CAGR through 2031 because advanced facilities need selective coordination, fault logging, and digital communications.

Page last updated on: