Kenya ICT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year Market Size (2025) | USD 11.19 Billion |

| Market Size (2026) | USD 11.81 Billion |

| Market Size (2031) | USD 15.48 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kenya ICT Market Analysis by Mordor Intelligence

Kenya ICT market size in 2026 is estimated at USD 11.81 billion, growing from 2025 value of USD 11.19 billion with 2031 projections showing USD 15.48 billion, growing at 5.55% CAGR over 2026-2031. The growth trajectory rests on four inter-locking forces: accelerated 5G coverage that lifts enterprise connectivity revenue, cloud-first government procurement that tilts spending toward infrastructure-as-a-service, a steep rise in cybersecurity investment that boosts managed service demand, and large-scale fiber build-outs that bring underserved counties online. Competitive dynamics continue shifting away from pure connectivity; operators, cloud hyperscalers, and specialist platforms now court public-sector and SME contracts with bundled connectivity, cloud, and security offerings. At the same time, sovereign-cloud requirements and data-protection rules favor providers willing to localize data centers and certify compliance controls, thereby injecting a regulatory dimension into market entry strategies. Finally, substantial fintech, gaming, and AI use-cases diversify revenue streams and position the Kenya ICT market as East Africa’s digital growth bellwether.

Key Report Takeaways

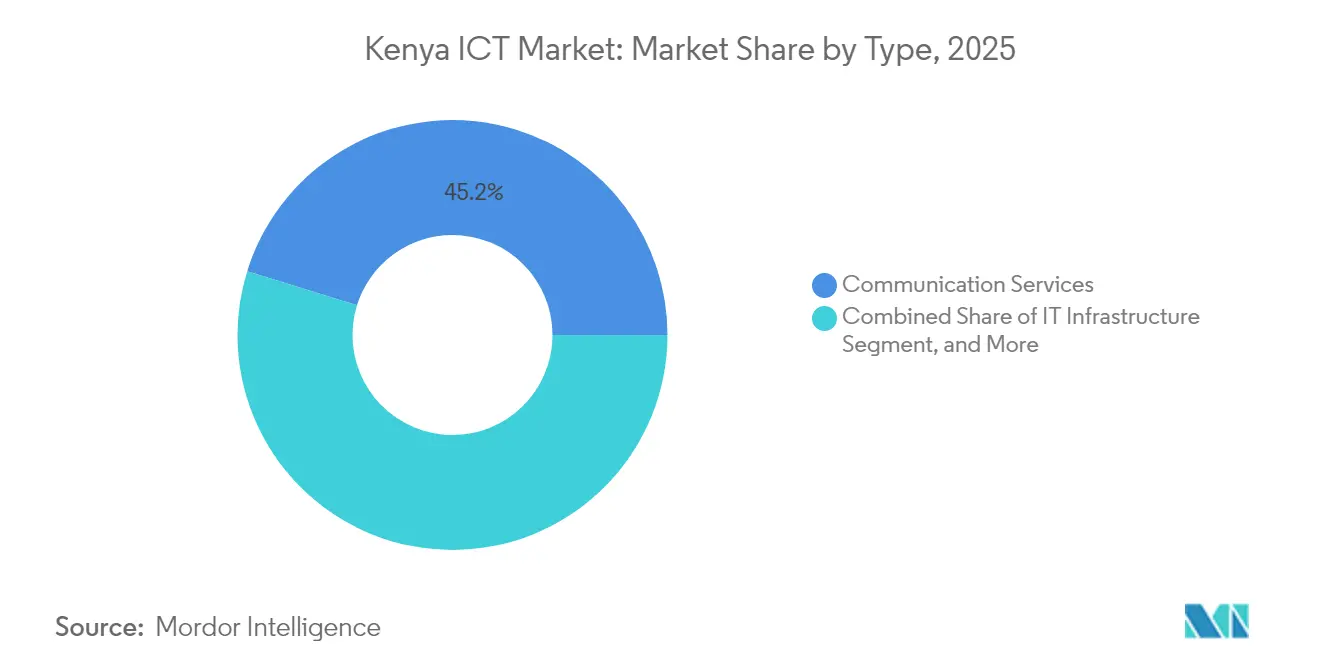

- By type, communication services led with 45.20% of Kenya ICT market share in 2025, while cloud services delivered the fastest 9.55% CAGR through 2031.

- By size of enterprise, large enterprises accounted for 57.05% of the Kenya ICT market size in 2025; SMEs posted a 7.20% CAGR over the same horizon.

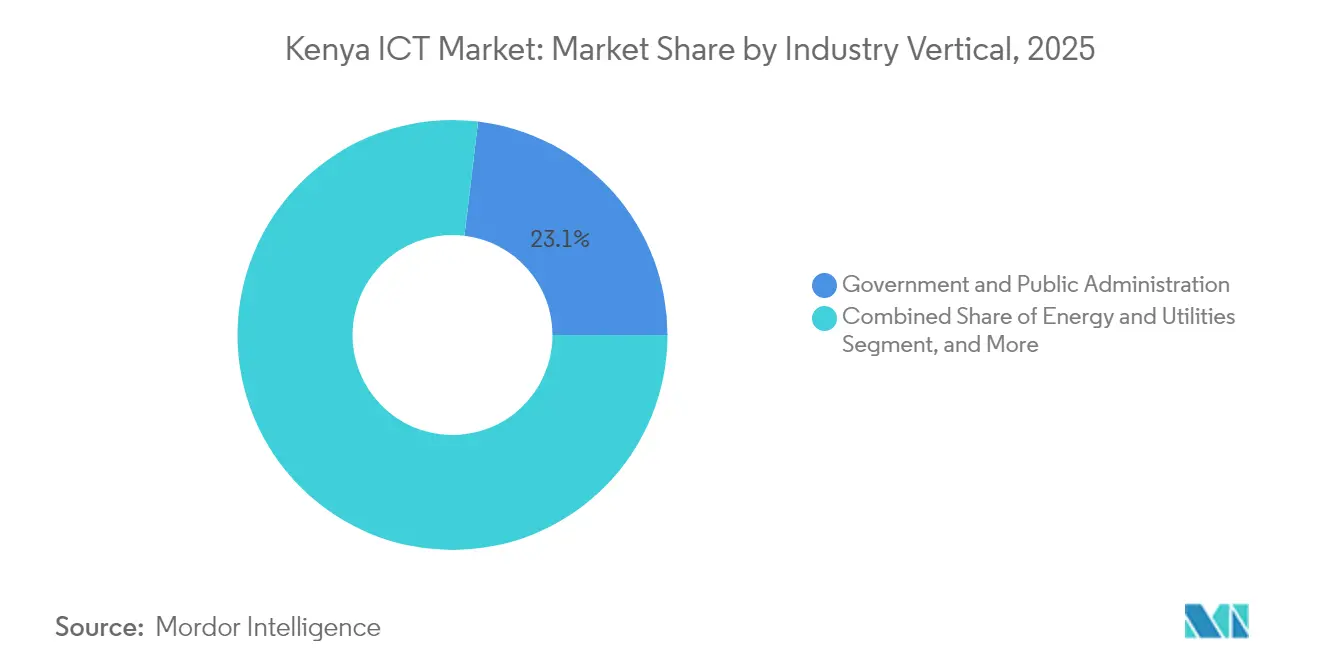

- By industry vertical, government and public administration captured 23.10% revenue share in 2025, whereas gaming and esports advanced at an 8.25% CAGR to 2031.

- By deployment model, on-premises solutions held 53.75% of Kenya ICT market share in 2025 and cloud-only models are projected to expand at a 9.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kenya ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G roll-out acceleration | +1.2% | National (Nairobi, Mombasa, Kisumu) | Medium term (2-4 years) |

| Cloud-first public-sector procurement | +1.0% | National government hubs | Short term (≤ 2 years) |

| Surge in cybersecurity spend | +0.8% | Financial and government sectors | Short term (≤ 2 years) |

| Digital Superhighway fiber build-out | +0.7% | Underserved counties | Long term (≥ 4 years) |

| Locally owned GPU clusters for AI | +0.5% | Nairobi, Konza City | Long term (≥ 4 years) |

| Scrapping of 30% local-equity rule | +0.4% | Major urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G Roll-out Acceleration

Safaricom activated 5G in strategic urban corridors and priced unlimited tiers from KES 2,999 for 10 Mbps to KES 10,000 for 250 Mbps, positioning the protocol as a premium enterprise enabler [1]Safaricom PLC, “Five-G FAQs,” safaricom.co.ke. Airtel’s 50% speed upgrade on existing bands ignited a technology arms race that spurs densification spending across Tier 1 cities. Early use-cases center on low-latency industrial IoT for manufacturing plants, hospitals, and financial-trading floors. Higher average revenue per user offsets spectrum fees and infrastructure capex, sustaining operator margins. Over the medium term 5G’s network-slicing capabilities are expected to unlock consumption-based SLAs that further widen enterprise adoption.

Cloud-first Public-sector Procurement

The State Department for ICT and Digital Economy budgeted KES 22.5 billion (USD 174 million) for cloud-native platforms in 2024, replacing capex-heavy legacy refreshes with OPEX-driven contracts [2]Open Budget Kenya, “State Departments Budget Data,” openbudget.or.ke. Parallel fiber investments under the Digital Superhighway plan guarantee 100,000 km of backbone capacity and 25,000 Wi-Fi hotspots, laying physical foundations for workload migration. Microsoft’s USD 1 billion geothermal-powered data-center in Naivasha delivers sovereign-cloud options addressing residency mandates. Procurement scorecards now weight sustainability credentials and local-partner participation, pushing hyperscalers to form consortia with domestic integrators. The near-term effect is a steeper switch from perpetual-license software to subscription-based infrastructure-as-a-service across ministries and county agencies.

Surge in Cybersecurity Spend

Kenya logged 2.5 billion cyber events in Q1 2025, a 201.7% rise year-on-year that reframed security as a board-level differentiator. The regulator issued 13.2 million advisories, citing a 228.3% jump in vulnerabilities and an 11.8% hike in web-application attacks [3]Communications Authority of Kenya, “Cyber Security Report Q1 2024-25,” ca.go.ke. Financial institutions and government agencies now procure managed detection and response platforms bundled with threat-intelligence feeds. AI-generated malware accelerates attack velocity, prompting enterprises to adopt zero-trust frameworks and multi-factor authentication. As a result, managed security services are forecast to outpace general IT services through 2027, anchoring bundled cloud-connectivity-security offerings.

Digital Superhighway Fiber Build-out

The 100,000-km Digital Superhighway extends Kigali-Mombasa undersea capacity across inland counties, facilitated by the Eastern Africa Regional Transport, Trade and Development Facilitation Project’s 730-km spur in the northwest. Fiber penetration lifts cloud uptake in agriculture, education, and health sectors, historically hampered by poor backhaul. The Horn of Africa Gateway Development Project links Kenyan routes to Ethiopia and Somalia, realizing a cross-border data corridor that positions Nairobi as a carrier-neutral traffic exchange. Long-term, pervasive fiber underpins edge-compute nodes that shave latency for IoT and streaming workloads, sustaining demand for hybrid deployment models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of digitalization for SMEs | –0.8% | Rural and peri-urban areas | Medium term (2-4 years) |

| Acute digital-skills shortage | –0.6% | Technical roles nationwide | Long term (≥ 4 years) |

| Data-center power-supply bottlenecks | –0.4% | Nairobi and major cities | Short term (≤ 2 years) |

| Fiscal austerity delaying IT projects | –0.3% | All government tiers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Digitalization for SMEs

Kenyan SMEs confront a KES 2.3 trillion (USD 17.8 billion) financing gap that constrains ICT upgrades. Cloud adoption among this segment remains 15%, deterred by subscription fees, integration complexity, and data-privacy fears [4]Alliance of Digital Finance and Fintech Associations, “Cloud Computing Report 2024,” alliancedfa.org. Traditional banks demand collateral ill-suited to intangible software assets, slowing loan approvals. Equipment leasing and revenue-share models are emerging but lack a supporting regulatory sandbox to scale nationally. Consequently, many micro-retailers rely on basic mobile payment apps, postponing inventory management or e-commerce platform investments until costs fall.

Acute Digital-skills Shortage

The sector employs 300,000 workers, yet vacancies in cybersecurity, DevOps, and data science remain unfilled for months, pushing salaries for senior security analysts to KES 400,000 per month. Government programs such as the Citizens Digital Skills initiative boost foundational literacy but do not immediately close high-end skill gaps. Enterprises import expertise from South Africa or India, extending project timelines and raising delivery costs. Private bootcamps are scaling, yet certification standards remain fragmented. Over the long term, co-location of academic research at Konza City aims to improve talent pipelines, but the shortage will weigh on project velocity through 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Communication Services Anchor Market Foundation

Communication services commanded 45.20% of Kenya's ICT market share in 2025, proving the sector’s historic role as the connectivity backbone. Meanwhile, cloud services are projected at a 9.55% CAGR, underpinning the transition to platform-based revenue. Communication-service ARPU benefits from integrated mobile money; M-PESA alone generated KES 161.1 billion (USD 1.2 billion) in service income, spotlighting fintech-telecom convergence. Hardware vendors face thin margins due to import duties and currency volatility, moving their focus toward installation and maintenance contracts. Infrastructure players, buoyed by submarine-cable landings, channel investments into Tier 3 data centers that host sovereign clouds.

Cloud momentum reflects enterprise flight from capex-heavy servers to pay-as-you-go compute. Software-as-a-service simplifies deployment for HR, accounting, and CRM functions among resource-constrained firms. Major telcos now spin up platform divisions combining 5G, edge compute, and managed Kubernetes, aiming to capture cloud adjacency revenue. The Kenya ICT market continues shifting value from pipes to platforms, challenging legacy operators to monetize dormant network APIs through open banking and IoT use-cases. Specialized software integrators that certify data-residency compliance gain ground, raising the bar for international entrants.

By Size of Enterprise: SME Growth Drives Market Expansion

Large enterprises held 57.05% of the Kenya ICT market size in 2025 because they budget for multilayer security, ERP, and private cloud stacks. Conversely, SMEs will expand at a 7.20% CAGR through 2031 as mobile-first apps and subscription pricing lower entry barriers. County Aggregation and Industrial Parks, backed by KES 1.13 billion in state funding, supply shared power and connectivity that foster cluster adoption. Digital-lending apps integrate credit scoring into e-commerce workflows, allowing SMEs to finance inventory and point-of-sale terminals via micro-loans.

SMEs prioritize cost-predictable solutions: bundled 4G/5G broadband, cloud POS, and WhatsApp-based order management. Vendors offering turnkey subscription kits gain traction, whereas bespoke ERP remains unaffordable for micro-retailers. Security features often lag, raising exposure to phishing attacks and prompting insurers to demand compliance audits for cyber-cover. In response, managed-service providers package endpoint protection with connectivity bundles, smoothing SME entry into formal digital commerce. Over the forecast window, SME uptake stands to reshape revenue structures toward a broader customer base, diluting dependence on a few large accounts.

By Industry Vertical: Government Leadership Enables Private Sector Adoption

Government and public administration commanded 23.10% revenue share in 2025, using policy leverage to drive electronic procurement, tax collection, and citizen-service portals. Cloud-based ID systems and digital-signature platforms push ministries to modernize, creating anchor tenants for new data centers. Banking, financial services, and insurance exploit regulatory sandboxes to launch mobile-micro-credit and insure-tech services. Healthcare digitalization gains momentum through platforms like M-TIBA that manage patient wallets and claims.

Gaming and esports, although nascent, register the fastest 8.25% CAGR as smartphone penetration surpasses 85% and youth demographics skew demand toward mobile titles. Venture capital targets local studios producing Afrofuturist content, while telcos bundle low-latency data plans for gamers. Manufacturing pilots IoT sensors that feed cloud analytics for predictive maintenance. Energy utilities deploy smart meters and data-layer APIs that enable pay-as-you-go solar. Across verticals, data-protection compliance dictates vendor selection, advantaging providers with a Kenyan data-center presence.

By Deployment Model: Hybrid Strategies Balance Security and Flexibility

On-premises deployments retained 53.75% market share in 2025 largely due to data-sovereignty clauses in financial-services and public-sector regulations. Cloud-only systems, however, rise at a 9.45% CAGR because they minimize upfront hardware outlays and shorten implementation cycles. Enterprises gravitate toward hybrid setups that keep sensitive workloads in local racks while bursting compute-intensive tasks to public clouds.

The Data Protection Act 2019 obliges controllers to document cross-border transfers, nudging CIOs toward multi-cloud architectures that localize customer PII while sending anonymized analytics to global regions. Edge computing gains favor in agriculture and mining, where connectivity can be intermittent; rugged edge gateways sync periodically with central clouds. Vendors responding with unified management consoles and consumption-based pricing secure longer contracts. Over time, maturing cloud-security certifications mitigate earlier reservations, accelerating the shift of test/dev and disaster-recovery workloads to the cloud.

Geography Analysis

Kenya leads East Africa’s digital scene by virtue of six undersea cable landings, political stability, and a liberalized telecom policy that abolished the 30% local-equity rule for foreign tech firms in 2024. Nairobi concentrates hyperscaler regions, fintech headquarters, and venture funds, forming the nucleus of the “Silicon Savannah.” Data-center capacity clusters along the Mombasa-Nairobi fiber spine, enabling low-latency replication across facilities and catalyzing hybrid-cloud adoption among banks.

Regional connectivity projects extend the Kenya ICT market footprint into Uganda, Tanzania, and Ethiopia through cross-border fiber and wholesale IP transit. The Digital Superhighway’s 100,000-km backbone pushes last-mile rollouts into pastoral counties, narrowing the digital divide. Internet penetration rose to 85.2% in 2025, while mobile subscriptions climbed past the population size, providing fertile ground for OTT video, e-learning, and telehealth.

Future growth pivots on Konza Technology City, a planned smart-city 60 km south of Nairobi offering tax incentives, reliable power, and dedicated research zones. The government earmarks plots for semiconductor assembly, AI labs, and BPO campuses. Secondary cities like Kisumu and Eldoret gain data-center satellites to support regional demand. A stable macro-framework and English-language capability position Kenya as a service hub for Francophone neighbors seeking Anglophone outsourcing talent.

Competitive Landscape

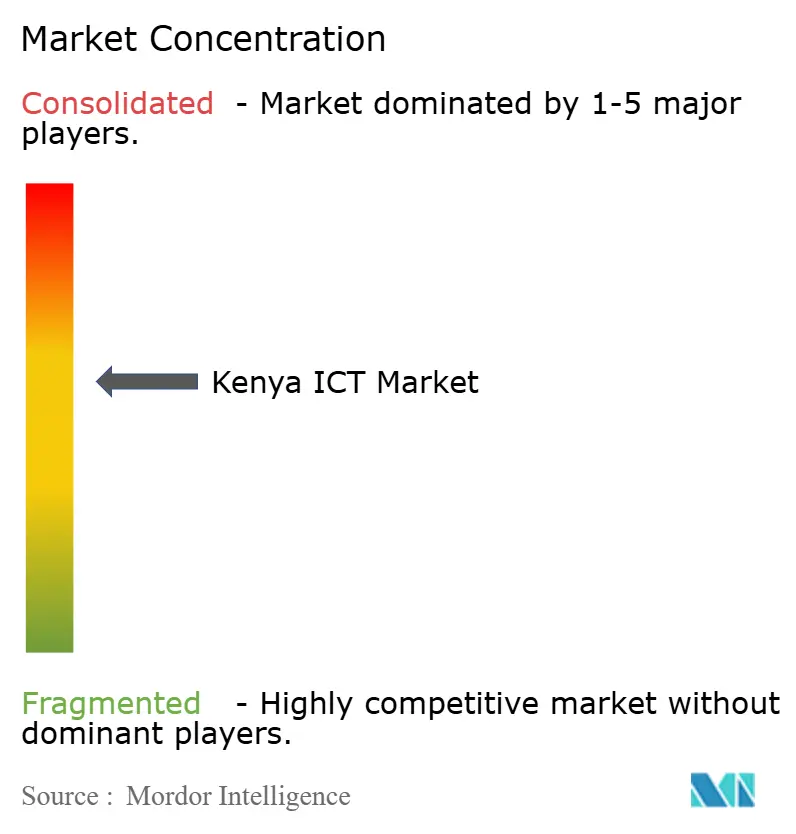

Kenya’s ICT arena remains moderately concentrated: the top five operators share roughly 55% of sector revenue, leaving room for niche specialists. Safaricom’s USD 3 billion revenue milestone illustrates the scale achievable through vertical integration of mobile money and connectivity. Airtel and Telkom compete on price and network modernization, including Open-RAN trials that lower vendor lock-in. International giants Microsoft, Oracle, and Google localize cloud regions to satisfy residency rules and tap public-sector workloads.

Strategic moves emphasize platform ecosystems. Safaricom adopted Red Hat OpenShift to harden its payments stack and expose APIs to fintech developers. Microsoft partners with G42 for a 1 GW geothermal data center, enabling carbon-neutral compute and drawing sustainability-minded clients. Oracle’s impending cloud region targets regulated industries seeking alternative architectures. Competition increasingly revolves around meeting compliance audits, uptime SLAs, and green-energy metrics rather than sheer bandwidth.

White-space opportunities appear in health-tech, agri-tech, and AI model localization. Domestic startups leverage mobile payments to bundle agronomic advice, while global hyperscalers court them with credits and incubators. Managed-service providers differentiate via certified security operations centers, vital in a threat landscape recording double-digit attack growth. M&A chatter surrounds mid-tier ISPs and SaaS firms seeking capital for nationwide rollouts; their acquisition could consolidate fragmented share and lift operator economies of scale.

Kenya ICT Industry Leaders

Honeywell International Inc

The International Business Machines Corporation (IBM)

Oracle Corporation

Microsoft Corporation

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Safaricom committed USD 500 million to build AI-ready GPU clusters across East Africa.

- May 2025: Microsoft and G42 broke ground on a USD 1 billion geothermal-powered data center in Naivasha.

- March 2025: Safaricom migrated M-PESA to Red Hat OpenShift for improved availability.

- July 2025: Siscom unveiled a crowd-invested server program addressing local infrastructure funding gaps.

Kenya ICT Market Report Scope

Information and communication technology (ICT) is an extensive term that includes a range of communication technologies. These encompass wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and diverse media applications. Together, these technologies enable users to store, access, transmit, retrieve, and manipulate information in digital formats.

Kenya’s ICT market is segmented by type (hardware, software, services, and telecommunication services), size of enterprise (small and medium enterprises and large enterprises), and industry vertical (BFSI, IT and telecom, government, retail and e-commerce, manufacturing, energy and utilities, and other industry verticals). The market sizes and forecasts are provided in value (USD) for all the above segments.

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| Government and Public Administration |

| Banking, Financial Services and Insurance (BFSI) |

| Energy and Utilities |

| Retail, E-Commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas (Up-, Mid-, Down-stream) |

| Gaming and Esports |

| Education |

| On-Premises |

| Cloud-Only |

| Hybrid |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| Communication Services | ||

| By Size of Enterprise | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | Government and Public Administration | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Energy and Utilities | ||

| Retail, E-Commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas (Up-, Mid-, Down-stream) | ||

| Gaming and Esports | ||

| Education | ||

| By Deployment Model | On-Premises | |

| Cloud-Only | ||

| Hybrid | ||

Key Questions Answered in the Report

What is the current value of the Kenya ICT market?

The market stands at USD 11.81 billion in 2026.

How fast is the sector expected to grow?

It is projected to post a 5.55% CAGR between 2026 and 2031.

Which segment is growing the quickest?

Cloud services are advancing at a 9.55% CAGR through 2031.

Why are SMEs important to future expansion?

SMEs will expand spending at 7.20% CAGR as mobile-first and subscription models lower adoption costs.

Page last updated on: