Jordan ICT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

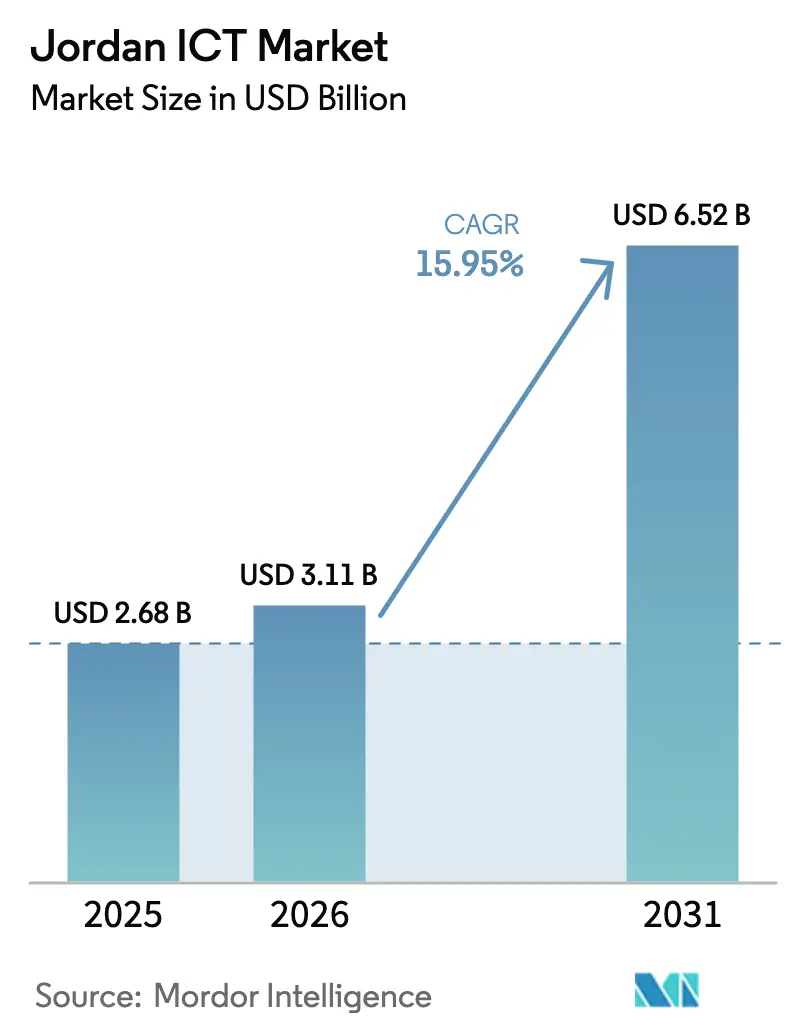

| Base Year Market Size (2025) | USD 2.68 Billion |

| Market Size (2026) | USD 3.11 Billion |

| Market Size (2031) | USD 6.52 Billion |

| Growth Rate (2026 - 2031) | 15.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Jordan ICT Market Analysis by Mordor Intelligence

Jordan ICT market size in 2026 is estimated at USD 3.11 billion, growing from 2025 value of USD 2.68 billion with 2031 projections showing USD 6.52 billion, growing at 15.95% CAGR over 2026-2031.[1]World Bank, “World Bank Approves $200 Million to Support Youth Technology and Jobs Project in Jordan,” worldbank.org Continued government digitization, sizable international funding, and regional demand for cloud and data-center capacity position the kingdom as a Levant technology hub. Public-sector digital programs anchor domestic spending, while 5G rollouts, Arabic AI applications, and startup activity in the Aqaba Special Economic Zone expand addressable opportunities. Enterprise preferences are shifting toward managed and cloud-based models, and hybrid deployments are gaining ground as organizations balance security and flexibility. Moderate market fragmentation allows local specialists to coexist with global vendors, yet the battle for specialized talent and power-grid reliability outside Amman remains a brake on long-term growth.

Key Report Takeaways

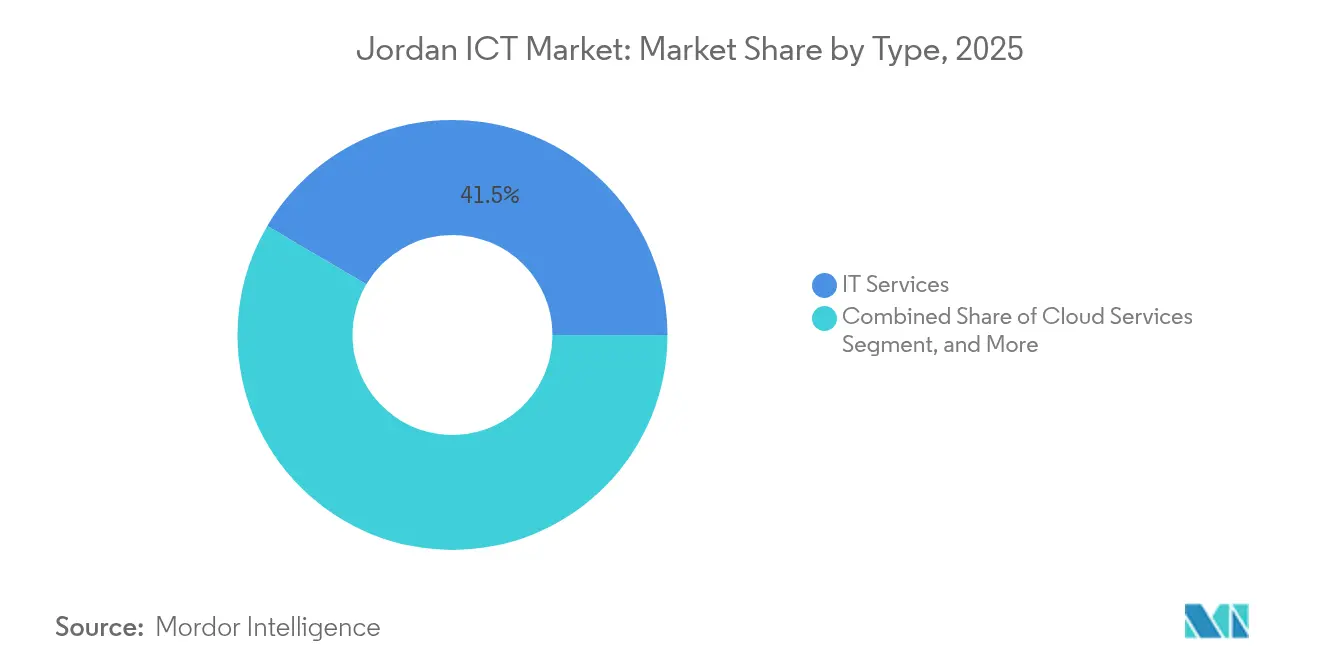

- By type, IT Services held 41.53% of Jordan ICT market share in 2025; Cloud Services are advancing at a 16.08% CAGR to 2031.

- By enterprise size, large organizations commanded 61.17% share of Jordan ICT market size in 2025, while SMEs post the fastest 16.12% CAGR through 2031.

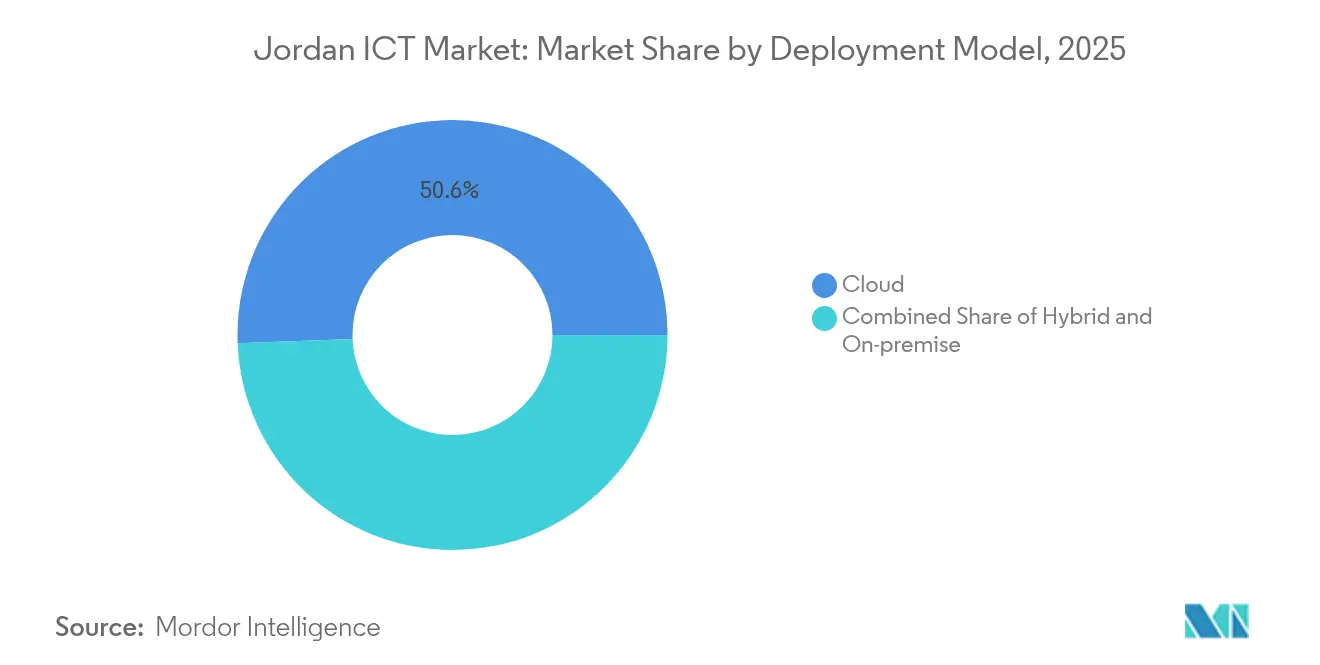

- By deployment model, cloud captured 50.62% share in 2025; hybrid solutions are forecast to expand at 16.20% CAGR between 2026-2031.

- By end-user vertical, government and public administration led with an 18.05% revenue share in 2025, whereas gaming and esports record the highest 16.58% CAGR to 2031.

- Zain Jordan, Orange Jordan, and Umniah together contributed just under one-half of overall telecommunications revenue in 2024, indicating moderate concentration across core network services

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Jordan ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital transformation across industries | +2.8% | National, strongest in Amman and Aqaba | Medium term (2-4 years) |

| 5G network deployment | +2.1% | Nationwide, urban priority | Short term (≤ 2 years) |

| Digital Jordan 2025 and e-government spending | +3.2% | National, public-sector focus | Long term (≥ 4 years) |

| Tech-startup boom in Aqaba SEZ | +1.4% | Aqaba Special Economic Zone | Medium term (2-4 years) |

| Adoption of Arabic AI and NLP | +1.8% | Government and banking sectors | Long term (≥ 4 years) |

| Regional data-center investments | +2.3% | Jordan-centered with wider MENA reach | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Digital Transformation in Industries

Enterprises integrate AI, blockchain, and cloud to streamline production and services, with empirical studies placing digital transformation’s path coefficient at 0.764 for accounting efficiency. Manufacturing firms perform Industry 4.0 readiness checks, and micro-enterprises that adopted resource-efficient production saved JOD 125,190 (USD 176,000) and cut energy use by 28% in first-year rollouts. SMEs link sustainability with digital tools to win regional contracts, while service providers invest in automation to raise customer satisfaction. The outcome elevates local competitiveness and draws regional clients who look for cost-effective yet innovative partners in the Jordan ICT market. Transformation momentum directly widens the addressable base for software, services, and connectivity solutions.

Rapid 5G Network Development Across the Nation

Umniah, Orange Jordan, and Zain Jordan backed by Ericsson introduce nationwide 5G, upgrading radio networks and core infrastructure. Enhanced bandwidth supports autonomous logistics, industrial IoT, and telemedicine, spurring fresh demand for edge computing and cybersecurity. Regulatory provisions for spectrum sharing accelerate rural coverage, narrowing the digital divide and creating fertile ground for cloud adoption among small towns. As 5G subscribers grow, operators bundle enterprise solutions, unlocking new revenue streams inside the Jordan ICT market. Early returns validate continued capital spending, signaling a stronger medium-term outlook for network equipment vendors.

Government-led Digital Jordan 2025 Program and e-Gov Spending

Digital Jordan 2025 covers 68 AI projects and mandates e-invoicing through JoFotara, compelling every VAT-registered firm to deploy XML/JSON invoices with QR authentication. The National Electronic Portal for SMEs centralizes public services, while the Digital Inclusion Policy creates Universal Service Fund mechanisms. These measures push ministries and regulated industries toward cloud infrastructure, identity management, and cybersecurity upgrades. Stable funding and clear milestones give suppliers visibility, enticing multinationals to form joint ventures with local integrators. The public sector’s purchasing power sets technical standards that ripple through banking, healthcare, and utilities, enlarging Jordan ICT market demand.

Regional Data-Center Investments Positioning Jordan as Levant Cloud Hub

Aqaba Digital Hub expands submarine connectivity by linking Egypt and Jordan through the Coral Bridge cable, improving bandwidth economics for the Levant. Facilities such as Zain’s “The Bunker” offer Tier III colocation to regional clients seeking political stability and flexible data-sovereignty rules. Energy pricing and skilled labor give Jordan a cost edge over peers, while relaxed data-localization in the Aqaba SEZ helps multinationals meet cross-border compliance. With Middle East capacity set to double by 2030, investors channel capital toward redundant power, cooling, and security in Amman and Aqaba. These projects cement Jordan ICT market standing as a preferred disaster-recovery and latency-optimized node.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-workforce shortage | -1.9% | National, sharpest in advanced domains | Long term (≥ 4 years) |

| Data-theft risk | -0.8% | Enterprise and government workloads | Medium term (2-4 years) |

| Power-grid instability outside Amman | -1.2% | Secondary cities and rural districts | Short term (≤ 2 years) |

| Geopolitical risk premium on venture capital | -1.6% | Startup and growth-stage funding | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Skilled Workforce

Roughly 7,000 tech graduates enter the market yearly, yet many exit for higher pay abroad, deepening domestic shortages in AI, cybersecurity, and cloud engineering. SMEs lack bench depth for large projects, and inconsistent English proficiency limits international contracting potential. Public-private initiatives like One Million Jordanian Coders increase baseline digital literacy, but advanced specialization supply remains thin. The talent gap inflates wage costs and delays project delivery, prompting some firms to outsource complex workloads. Over time, shortages hamper Jordan ICT market scale-up and deter foreign direct investment in high-skill operations.

Intermittent Power-Grid Instability Outside Amman

Recurring outages in secondary regions disrupt telecom links and data-center uptime, discouraging distributed infrastructure deployment. Rural cloud nodes face high backup-power costs, and international operators cluster in Amman to mitigate risk. Grid unreliability restricts digital inclusion targets and slows the extension of e-services to peripheral districts. Local firms must invest in UPS and diesel generation, squeezing margins and elongating payback periods. Until reliability measures mature, the constraint caps broader geographic spread for Jordan ICT market services.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Leadership Drives Market Evolution

Jordan ICT market size for IT Services stood at a commanding 41.53% share in 2025, propelled by consulting, integration, and managed offerings that underpin enterprise modernization agendas. Cloud Services, though smaller, register a rapid 16.08% CAGR as companies migrate workloads seeking elasticity and cost control. Demand for IT Hardware persists through network upgrades and device refresh cycles, while software spending concentrates on ERP and CRM suites to institutionalize best practices. Service-oriented consumption accelerates as customers favor outcome-based contracts over capital procurement. ZainTECH’s acquisition of Specialized Technical Services, which employs over 350 professionals, illustrates consolidation that bundles connectivity with transformation expertise.

Digital-first roadmaps convert project-based engagements into annuity managed-service deals, improving vendor revenue visibility. Cybersecurity consulting gains importance in light of e-invoicing mandates, and communication services enjoy uplift from 5G-enabled unified collaboration. The shift from hardware ownership to service consumption redefines partner ecosystems and reinforces Jordan ICT market positioning as a regional solution provider.

By Enterprise Size: SME Digitization Accelerates Growth

Large organizations captured 61.17% of Jordan ICT market share in 2025, thanks to sizable IT budgets in banking, telecom, and public administration. SMEs, however, are expanding at a 16.12% CAGR, buoyed by cloud adoption, digital payments, and government support programs. Among 167,519 registered enterprises, 99.5% are classified as SMEs, representing untapped digital potential. Portal initiatives and fintech innovations lower entry barriers, enabling micro-firms to leapfrog to online sales and accounting.

Usage studies show social-media tools score above 3.4 in perceived usefulness, ease, and cost efficiency for business continuity among SMEs. Cloud subscriptions replace upfront server purchases, and pay-as-you-go models spread costs across operating budgets. As more small firms formalize processes, demand grows for cybersecurity, data analytics, and AI chatbots, widening Jordan ICT market exposure to entrepreneurial segments.

By Deployment Model: Hybrid Solutions Gain Momentum

Cloud captured 50.62% Jordan ICT market share in 2025, underscoring widespread acceptance of virtualized resources. Hybrid configurations post the fastest 16.20% CAGR, allowing enterprises to keep sensitive workloads on-premise while tapping public-cloud agility for standard functions. Banks and ministries maintain data sovereignty through private clouds, yet pair them with Azure or AWS for analytics sandboxes. On-premise environments persist where latency, control, or regulation demand local hosting.

Capital Bank Jordan’s phased migration highlights cost and performance gains that influence peers. Vendors reply with multicloud management suites, and telecom players bundle off-premise infrastructure with local hosting to capture hybrid demand. The pattern stabilizes OPEX profiles and diversifies vendor ecosystems inside the Jordan ICT market.

By End-user Industry Vertical: Government Leadership Enables Broader Adoption

Government and public administration owned an 18.05% slice of Jordan ICT market size in 2025 due to e-government portals, AI pilots, and mandatory e-invoicing. Gaming and esports clock a 16.58% CAGR to 2031, benefiting from tournament venues and Arabic content studios such as Tamatem Games. BFSI accelerates digital banking, while energy utilities pilot smart-grid telemetry.

Retail logistics deploy omnichannel platforms, and manufacturing embraces Industry 4.0 for export competitiveness. Healthcare advances telemedicine and electronic records, improving rural access. Cross-industry uptake confirms technology’s central role in national competitiveness, anchoring the multiyear expansion of Jordan ICT market revenues.

Geography Analysis

Amman accounts for most Jordan ICT market activity, hosting headquarters, data centers, and innovation labs. Reliable power, dense fiber backbones, and skilled labor pools encourage multinationals to base regional operations in the capital. Government agencies test AI services that later cascade into private-sector adoption, adding to metropolitan demand.

Aqaba Special Economic Zone emerges as a secondary hub by leveraging relaxed data-localization, tax incentives, and the new Coral Bridge subsea cable that boosts international bandwidth. Startups cluster around fintech and logistics, and data-center investors exploit lower land costs and seaport proximity. Hybrid deployments route disaster-recovery workloads to Aqaba facilities, reinforcing national resilience.

Secondary cities such as Irbid and Zarqa trail due to intermittent grid power and smaller talent pools. Nevertheless, telcos extend 5G coverage, and Universal Service Fund initiatives promise fiber links to schools and clinics. Over the forecast horizon, balanced regional development remains contingent on infrastructure upgrades that broaden participation in Jordan ICT market growth.

Competitive Landscape

Competition is moderate, with the top three operators Zain Jordan, Orange Jordan, and Umniah commanding the bulk of telecom infrastructure, while software and services remain fragmented among global and local providers. Operators enter cloud and cybersecurity arenas to protect revenue as voice services plateau. ZainTECH’s acquisition of Specialized Technical Services fuses network reach with digital consulting, showing a convergence trend.

Local innovators focus on Arabic AI, fintech, and gaming. Mawdoo3 expanded its crowdsourced encyclopedia after a strategic investment from Naif Al Rajhi Investment, sharpening its NLP edge for Arabic content.[2]Tracxn, “Mawdoo3 – Company Profile,” tracxn.com Algebra Intelligence raised USD 310,000 to commercialize energy-monitoring AI, highlighting niche analytics opportunities.[3]The Startup Scene, “Jordan’s Algebra Intelligence to Launch App with Pre-Seed Funding,” thestartupscene.me Compliance expertise around JoFotara e-invoicing adds competitive moats for system integrators able to bundle tax, security, and cloud capabilities.

Partnerships between hyperscalers and telcos shape hybrid-cloud supply chains, while venture funds like ADQ’s USD 100 million technology vehicle signal institutional appetite despite geopolitical premiums. Market power diffuses beyond core networks, giving room for SMEs with vertical depth to capture value inside the Jordan ICT market.

Jordan ICT Industry Leaders

Microsoft Corporation

Google, LLC

Wipro Limited

Cisco Systems Inc.

Telefonaktiebolaget LM Ericsson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Algebra Intelligence raised USD 310,000 in pre-seed funding led by Oasis500 to build the TaQTak AI energy-monitoring platform targeting real-time plant analytics.

- January 2025: INTRACOM Jordan signed a USD 1.8 million SAN consolidation contract with Paltel Group covering EMC supply, installation, and configuration.

- December 2024: Inspire for Solutions Development sponsored the 4th Digital Transformation Jordan conference showcasing IBM automation and Atlassian ITSM.

- November 2024: Mawdoo3 secured strategic funding from Naif Al Rajhi Investment to expand Arabic AI content services.

Jordan ICT Market Report Scope

ICT encompasses a spectrum of technological tools that facilitate the transmission and processing of information. The term itself is an amalgamation of information, communication, and technology. The study tracks key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study also tracks the revenue accrued from various ICT types that are used in various industry verticals across Jordan.

The Jordanian ICT market is segmented by type (hardware, software, IT services, and telecommunication services), size of enterprises (small and medium enterprises and large enterprises), and industry vertical (BFSI, IT and telecom, government, retail and e-commerce, manufacturing, energy and utilities, and other industry verticals). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| On-premise |

| Cloud |

| Hybrid |

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| (Up/Mid/Down-stream) |

| Gaming and Esports |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Deployment Model | On-premise | |

| Cloud | ||

| Hybrid | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| Energy and Utilities | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| (Up/Mid/Down-stream) | ||

| Gaming and Esports | ||

Key Questions Answered in the Report

What is the current value of the Jordan ICT market in 2026?

Jordan ICT market size stands at USD 3.11 billion in 2026.

How fast is the market expected to grow by 2031?

The market is projected to expand to USD 6.52 billion by 2031, delivering a 15.95% CAGR.

Which segment leads spending by type?

IT Services hold the largest 41.53% share driven by digital-transformation consulting and managed services.

Which deployment model is growing the quickest?

Hybrid cloud solutions exhibit the fastest 16.20% CAGR as firms balance flexibility with data control.

Why is gaming and esports important for future growth?

Gaming and esports register a 16.58% CAGR, supported by regional tournaments and Arabic content studios such as Tamatem Games.

What key challenge could slow market expansion?

A sustained shortage of specialized tech talent, with brain drain to higher-paying markets, threatens growth potential and adds wage pressure.

Page last updated on: