Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 155.57 Billion |

| Market Size (2026) | USD 173.26 Billion |

| Market Size (2031) | USD 274.86 Billion |

| Growth Rate (2026 - 2031) | 9.67% CAGR |

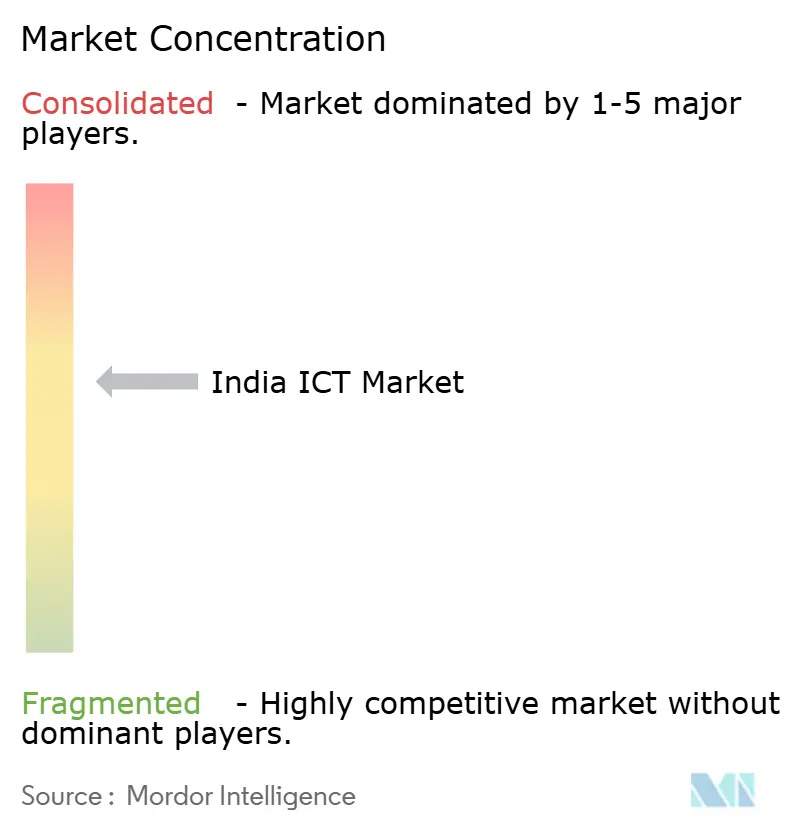

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India ICT Market Analysis by Mordor Intelligence

The India ICT Market size is expected to grow from USD 155.57 billion in 2025 to USD 173.26 billion in 2026 and is forecast to reach USD 274.86 billion by 2031 at 9.67% CAGR over 2026-2031. Continued sovereign-cloud mandates, surging on-device artificial-intelligence inference, and the maturing Production Linked Incentive program are accelerating the spending curve beyond the 2020-2025 trajectory. Enterprises are refactoring monolithic workloads into micro-services that run on certified sovereign clouds, a shift that is increasing demand for hybrid-cloud orchestration tools and DevSecOps talent. Simultaneously, mobile-first consumption has pushed monthly data traffic above 20 exabytes, prompting operators to densify 5G coverage and hyperscalers to add capacity in South and North India. The Production Linked Incentive scheme is steering laptop, tablet, and server assembly inland, trimming import dependence and shortening lead times for local buyers.

Key Report Takeaways

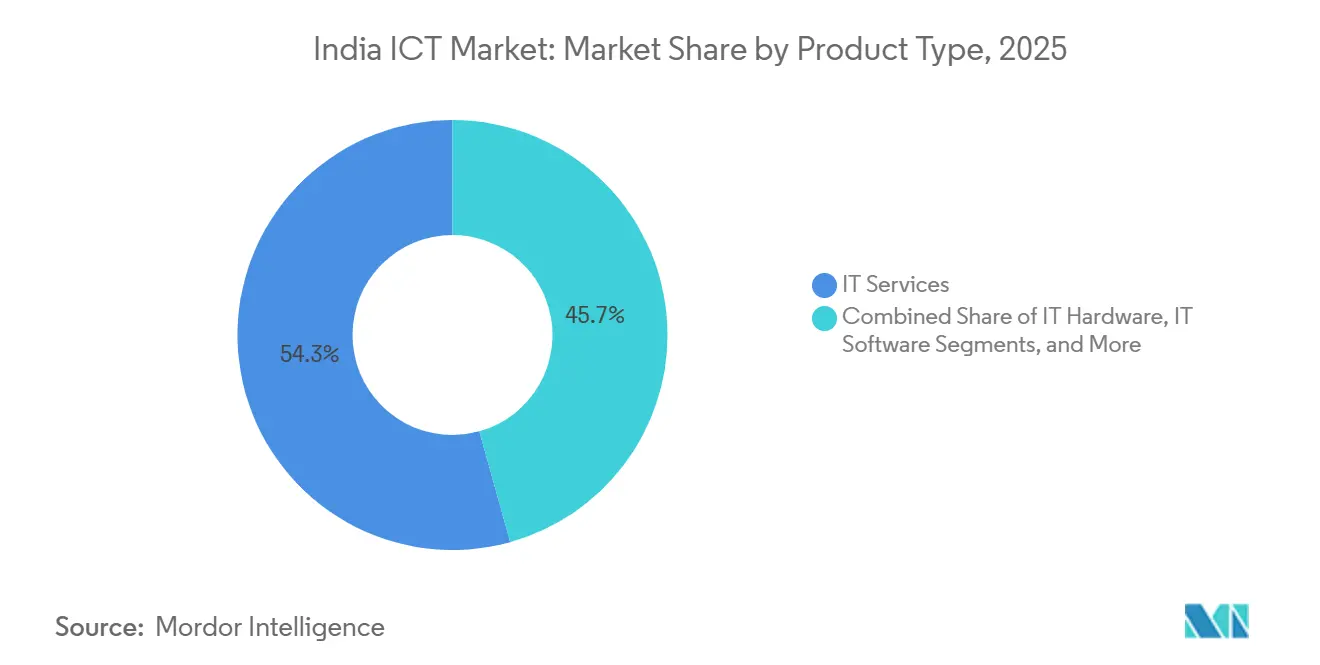

- By product type, IT Services led with 54.32% revenue share in 2025 and IT Security and Cybersecurity is projected to record a 10.08% CAGR through 2031.

- By enterprise size, large enterprises captured 63.14% spending in 2025 while small and medium-sized enterprises are set to expand at a 9.82% CAGR to 2031.

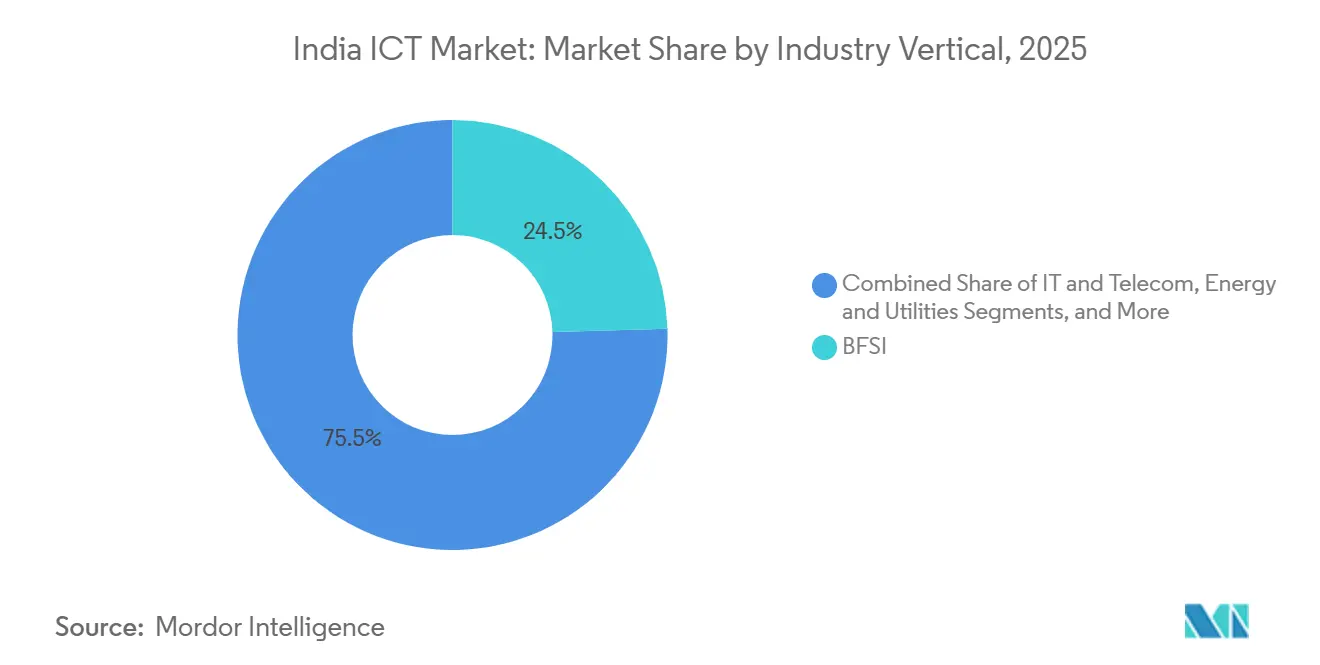

- By industry vertical, BFSI held 24.54% share of the India ICT market size in 2025 and Healthcare and Life Sciences is forecast to grow at an 11.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India ICT Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Cloud Services Among Indian SMEs | +1.5% | National, concentrated in West and South India | Short term (≤ 2 years) |

| Government-Led Digital India Programme and e-Governance Push | +1.8% | National, with early gains in Delhi, Mumbai, Bengaluru | Medium term (2–4 years) |

| Expansion of Domestic Electronics Manufacturing Schemes (PLI) | +1.2% | National, led by Tamil Nadu, Karnataka, Uttar Pradesh | Long term (≥ 4 years) |

| Surge in Mobile Data Consumption and 5G Rollout | +2.1% | National, urban clusters first, spill-over to tier-2 cities | Medium term (2–4 years) |

| Rising Venture Capital Investment in Indian SaaS Start-Ups | +1.0% | Global, with product development in Bengaluru, Chennai | Medium term (2–4 years) |

| Growing Demand for Cybersecurity Solutions Amid Stringent Data Protection Bill | +1.3% | National, critical infrastructure and BFSI focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-Led Digital India Programme and e-Governance Push

The Digital India initiative has progressed from connectivity roll-outs to service-layer innovation, illustrated by the India Stack clearing 12.5 billion Unified Payments Interface transactions in December 2025, a 28% year-on-year rise.[1]National Payments Corporation of India, “UPI Transaction Statistics,” npci.org.in State procurement agencies now require cloud-first architectures, forcing legacy software vendors to re-platform applications onto sovereign clouds approved by the Ministry of Electronics and IT. Artificial intelligence-enabled vendor-discovery tools within the Government e-Marketplace have compressed procurement cycle time by 35% and increased transaction transparency across 62,000 ICT suppliers. DevSecOps skills for cloud-native development are therefore in short supply, so domestic integrators have teamed with global hyperscalers to build localized capability centers. Healthcare reforms under Ayushman Bharat have generated 580 million health identifiers, catalyzing the adoption of Fast Healthcare Interoperability Resources across 45,000 public facilities. Tight residency rules on audit trails and encryption heighten entry barriers for non-compliant foreign vendors.

Surge in Mobile Data Consumption and 5G Rollout

India’s 5G subscriber base exceeded 120 million by end-2025, underpinned by 400,000 base stations across 200 cities from Reliance Jio and Bharti Airtel. Average monthly data use reached 22 gigabytes per user as high-definition video, cloud gaming, and hybrid-work video conferencing proliferated. Industrial pilots show network-slicing has cut end-to-end latency below 10 milliseconds in automotive and port-logistics settings. Millimeter-wave auctions in 2025 unlocked fixed-wireless access that challenges legacy fiber where penetration is under 15%. Edge data-center operators such as Yotta Infrastructure and CtrlS Datacenters have earmarked USD 1.2 billion for additional capacity to serve real-time analytics workloads. Compliance with the Telecommunications Act 2023 obliges operators to store call-detail records for 180 days, creating new managed-compliance service revenue pools.

Expansion of Domestic Electronics Manufacturing Schemes (PLI)

The Production Linked Incentive scheme has attracted INR 35,000 crore (USD 4.2 billion) in commitments from 42 applicants, among them Dell, HP, Acer, and domestic champions Dixon Technologies and Lava International. Domestic output of laptops and tablets jumped to 8.2 million units in fiscal 2025, narrowing import bills and curbing supply-chain hiccups for enterprise buyers. Component localization, particularly in printed-circuit-board assembly and display panels, remains concentrated overseas, limiting potential value-addition to below 50% by 2027. A phased manufacturing program for networking equipment launched in October 2025 has linked incentives to export commitments, positioning India as a regional hardware hub. State governments in Tamil Nadu and Karnataka supply single-window clearances and power subsidies, shaving the total cost of ownership by 12-15% versus coastal China. Mandatory quality-control orders across 15 ICT categories have improved device reliability, in turn reducing warranty claims for enterprise customers.

Growing Demand for Cybersecurity Solutions Amid Stringent Data Protection Bill

The Digital Personal Data Protection Act took effect in April 2025, threatening penalties up to INR 250 crore (USD 30 million) for breaches of sensitive personal data. Ransomware incidents climbed 42% year-on-year in 2025, with healthcare, logistics, and manufacturing sectors at heightened risk. Zero-trust network access rollouts are accelerating as hybrid work models proliferate and application programming interface attack surfaces expand. The Reserve Bank of India has mandated multifactor authentication and end-to-end encryption for all payment system operators, spurring the build-out of security operations centers and the outsourcing of managed detection and response. Domestic vendors such as Quick Heal Technologies leverage in-country data residency to gain share over global rivals in regulated verticals. Security certifications like ISO 27001 now appear in 72% of BFSI RFPs issued in 2025, making compliance a purchasing prerequisite.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Shortage of High-Skilled IT Talent in Tier 2 Cities | -0.9% | National, acute in Indore, Coimbatore, Jaipur | Medium term (2–4 years) |

| Volatility in Rupee Exchange Rates Impacting Imported Hardware Costs | -0.7% | National, affects hardware OEMs and systems integrators | Short term (≤ 2 years) |

| Fragmented Last-Mile Connectivity in Rural Areas | -0.5% | Rural India, concentrated in East and North-East regions | Long term (≥ 4 years) |

| Rising Geopolitical Scrutiny on Foreign Cloud Providers | -0.4% | National, affects multinational enterprises and government | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Persistent Shortage of High-Skilled IT Talent in Tier 2 Cities

India added 290,000 net IT employees in fiscal 2025, yet attrition in tier-2 hubs such as Coimbatore and Indore stayed above 22%, four percentage points higher than Bengaluru. The National Skill Development Corporation opened 150 Centers of Excellence for emerging technologies during 2025, but graduation numbers trail demand by roughly 35%.[2]National Skill Development Corporation, “Technology Skilling Initiatives,” nsdcindia.org Enterprises cite 40% longer recruitment cycles in tier-2 locations and higher training costs to close proficiency gaps in Kubernetes orchestration and secure software development life cycles. Global Capability Centers entering Ahmedabad and Visakhapatnam struggle to attract mid-career domain experts, limiting their shift from cost arbitrage to innovation hubs. The Ministry of Education introduced four-year artificial-intelligence degrees at National Institutes of Technology in 2024, but the first cohort will graduate in 2028. Uneven broadband quality further curbs Skill India Digital adoption, leaving many participants without hands-on lab access.

Volatility in Rupee Exchange Rates Impacting Imported Hardware Costs

The rupee depreciated 4.8% against the U.S. dollar in calendar 2025, lifting landed prices for servers, storage arrays, and network switches by roughly 6%. Original-equipment manufacturers with limited local assembly pass through up to 80% of currency swings to enterprise buyers within 90 days, compressing capital-expenditure plans. While the Production Linked Incentive scheme reduced dependence on laptop imports, processors, memory modules, and solid-state drives remain 90% import-reliant. Multi-year contracts that lock pricing via vendor-managed inventory shift working capital burdens to suppliers who then defer investments in local capacity. Forward-hedging costs rose to 3.2% for 12-month contracts in late 2025, eroding distributor margin buffers. Documentation under the Foreign Exchange Management Act adds roughly 15 extra procurement days for high-performance computing imports.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Anchor Revenue, Security Drives Growth

IT Services generated 54.32% of 2025 revenue, reaffirming India’s role as a global delivery hub for application development, infrastructure management, and business-process outsourcing. The India ICT market share of IT Security and Cybersecurity is projected to widen as that sub-segment expands at a 10.08% CAGR through 2031, driven by stringent data protection penalties and rising ransomware attacks. Comparing the historical 7.5% CAGR for IT Services during 2020-2025 with the forecast 9.2% run rate through 2031 highlights the pivot toward high-value consulting and cloud-migration mandates. Hardware assembly volumes rose to 8.2 million laptops and tablets in fiscal 2025 under the Production Linked Incentive scheme, yet supply chains still depend heavily on imported chipsets, which exposes costs to forex swings.[3]Ministry of Electronics and IT, “Digital India Programme,” meity.gov.in

Enterprises are diverting funds from perpetual software licenses to pay-as-you-go SaaS, a move that has expanded India ICT market size for cloud and platform services at mid-teen growth rates. Domestic SaaS vendors like Zoho and Freshworks capitalize on localized compliance and rupee-denominated pricing to win mid-market clients in manufacturing and retail. Managed security services, covering 24/7 security-operations-center monitoring and regulatory reporting, are gaining mindshare as organizations confront skill shortages in threat hunting. Hyperscalers are answering data-localization rules by committing USD 15 billion in cumulative capacity additions by 2027, sparking ancillary demand for colocation and disaster-recovery services. Business-process outsourcing, meanwhile, is shifting toward knowledge-process work in legal and clinical research, sustaining India’s 38% slice of global BPO revenue despite wage inflation.

By Enterprise Size: SMEs Accelerate, Large Enterprises Optimize

Large enterprises controlled 63.14% of 2025 spending, anchored by multi-year modernization in BFSI, manufacturing, and telecom. Yet their growth is moderating as core-system refreshes approach completion, prompting CIOs to reallocate budgets toward generative-AI pilots and data-analytics platforms. Small and medium-sized enterprises are projected to grow at a 9.82% CAGR to 2031, reflecting easier access to credit under the Emergency Credit Line Guarantee Scheme and falling upfront infrastructure costs through cloud adoption. The India ICT market size for SMEs benefits from pay-per-transaction SaaS, which has cut infrastructure spending by around 40% while accelerating time-to-digital for smaller retailers and logistics operators.

SMEs leverage unified communications, digital payments, and customer-relationship-management SaaS to close competitive gaps versus larger incumbents, with adoption rates exceeding 35% in retail and logistics by 2025. Large enterprises are embedding AI-driven automation into software-development life cycles, trimming billable headcount and improving release velocity. Tech spending is also shifting from capex to opex models via platform-as-a-service consumption inside the Government e-Marketplace, which processed ICT orders worth INR 2 trillion (USD 24 billion) during fiscal 2025. Mandatory electronic invoicing for businesses above INR 50 million (USD 0.54 million) turnover compels SMEs to deploy cloud-based enterprise-resource-planning and tax compliance suites, further deepening digital penetration.

By Industry Vertical: BFSI Leads, Healthcare Surges

BFSI accounted for 24.54% of 2025 spend as banks modernized core systems and met Reserve Bank cybersecurity directives. The India ICT market share of Healthcare and Life Sciences is smaller today, yet it is growing fastest, with that vertical expected to expand at a 11.19% CAGR to 2031 on the back of Ayushman Bharat electronic health record mandates and a telemedicine surge to 18 million consultations per month. Telecom operators, meanwhile, invested more than USD 12 billion in 2025 to virtualize network functions and deploy edge compute, underscoring the sector’s shift from voice services to low-latency platforms.

Government and public administration entities are embracing cloud-first procurement, as evidenced by the 12.5 billion transactions recorded in December 2025, showcasing the scalability of the India Stack. Retail, e-commerce, and logistics outfits deploy warehouse management algorithms and omnichannel customer engagement, driving ICT outlays up 14% year-on-year in 2025. Manufacturing plants integrate industrial IoT sensors and digital twins, reducing unplanned downtime by up to 22% and boosting investment in predictive-maintenance analytics platforms. Power utilities are installing smart-meter infrastructure in line with the Ministry of Power's mandate to deploy 250 million devices by 2027, creating sustained demand for edge analytics and cybersecurity. Sector-specific regulations in finance and capital markets continue to enforce data-localization and audit-trail requirements that uphold robust ICT spend levels.[4]Reserve Bank of India, “Credit Guarantee Schemes for SMEs,” rbi.org.in

Geography Analysis

South India captured the largest slice of 2025 revenue, anchored by Bengaluru’s 1,800 Global Capability Centers and Chennai’s electronics corridor that built 4.2 million laptops and tablets under the Production Linked Incentive scheme. The India ICT market in the south is expected to grow at a 9.4% CAGR through 2031, driven by hyperscale investments totaling USD 6 billion from Microsoft Azure, Amazon Web Services, and Google Cloud to meet data-residency mandates. Karnataka and Tamil Nadu offer single-window clearances and power subsidies that reduce the cost of ownership by up to 15% compared with coastal China, encouraging the formation of OEM clusters. Hyderabad and Bengaluru host AI research laboratories and start-up incubators such as T-Hub, which supported 450 SaaS ventures and produced 18 unicorns by 2025, reinforcing innovation-led growth.

West India, namely Maharashtra and Gujarat, holds the second-largest share, powered by Mumbai’s BFSI ecosystem and Pune’s auto-electronics base, where ICT spending climbed 9.1% in 2025. The fiber backbone of the Mumbai-Pune industrial corridor delivers sub-5-millisecond latency, underpinning real-time trading and algorithmic systems for capital markets. North India is closing the gap as Noida and Gurugram attract hyperscale data-centers to serve e-governance workloads, with the region projected to post the fastest 9.8% CAGR to 2031. National Informatics Centre cloud zones in Delhi further pull public-sector SaaS investments northward.

East India, including West Bengal and Odisha, remains the smallest contributor owing to fragmented last-mile connectivity, yet business-process outsourcing clusters in Kolkata are gaining momentum on state tax incentives. The BharatNet program aims to link 250,000 gram panchayats via fiber by 2027, a move that could expand telemedicine and e-commerce in under-served areas. Regional data-center policies in Maharashtra, Karnataka, and Telangana, which reimburse capital expenditure and waive electricity duty, shape investment flows toward southern and western hubs.

Competitive Landscape

The India ICT market is moderately concentrated; the top five IT services vendors, Tata Consultancy Services, Infosys, HCL Technologies, Wipro, and Tech Mahindra, control roughly major share of services revenue. Automation is compressing billable headcount by 8-10% each year, pushing incumbents toward outcome-based contracts that embed generative-AI copilots into software development workflows.

Reliance Jio and Bharti Airtel bundle enterprise connectivity with managed security, edge compute, and unified communications, positioning themselves as one-stop solution providers for SME clients. Demand for hybrid-cloud orchestration opens white space that domestic integrators fill through alliances with Red Hat and VMware, assuring workload portability across sovereign and global clouds.

Vertical-specific SaaS challengers are expanding rapidly; Zoho holds 15% of the Indian CRM segment by combining localized compliance with rupee pricing, while Freshworks is broadening into IT service management after its NASDAQ listing. Data-residency rules create barriers for foreign clouds lacking in-country zones, giving Tata Communications, CtrlS Datacenters, and Yotta Infrastructure first-mover edge in sovereign-cloud offerings certified by the Ministry of Electronics and IT. Strategic activity includes Infosys acquiring a European engineering-services firm for USD 1.5 billion to deepen Industry 4.0 skills and HCL Technologies partnering with Google Cloud on generative-AI solutions for BFSI clients. Patent filings, notably the 42 submitted by Persistent Systems in 2025, indicate a pivot from pure staff augmentation to IP-led differentiation. Security certifications such as ISO 27001 dominate tender prerequisites, underscoring cybersecurity’s role as a competitive moat.

India ICT Industry Leaders

Tata Consultancy Services Limited

Infosys Limited

HCL Technologies Limited

Wipro Limited

Tech Mahindra Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Tata Consultancy Services committed USD 500 million for an artificial-intelligence R and D center in Bengaluru, with plans to hire 2,000 specialists by December 2026.

- December 2025: Reliance Jio introduced managed security-as-a-service for SMEs, bundling endpoint protection, SOC monitoring, and compliance reporting under the Digital Personal Data Protection Act.

- November 2025: Infosys closed a USD 1.5 billion deal for a European engineering-services company, adding 8,000 engineers to its Industry 4.0 portfolio.

- October 2025: Microsoft India announced a USD 3 billion expansion of Azure capacity, adding three availability zones in Mumbai, Bengaluru, and Hyderabad.

India ICT Market Report Scope

The India ICT market is witnessing significant growth, driven by increasing digital transformation initiatives, advancements in IT infrastructure, and the rising adoption of emerging technologies such as cloud computing, artificial intelligence, and the Internet of Things (IoT). The market is also supported by government policies promoting digitalization and the expansion of IT services across various industry verticals.

The India ICT Market Report is Segmented by Product Type (IT Hardware, IT Software, IT Services, IT Infrastructure, IT Security/Cybersecurity, Communication Services), Enterprise Size (Small and Medium-sized Enterprises, Large Enterprises), Industry Vertical (Government and Public Administration, BFSI, IT and Telecom, Energy and Utilities, Retail E-commerce and Logistics, Manufacturing and Industry 4.0, Healthcare and Life Sciences, Oil and Gas, Other Industry Verticals). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By Industry Vertical

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-commerce, and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Other Industry Verticals |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-commerce, and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Other Industry Verticals | ||

Key Questions Answered in the Report

What is the projected value of the India ICT market in 2031?

The India ICT market is forecast to reach USD 274.86 billion by 2031.

How fast is the cybersecurity segment growing?

Cybersecurity spending is expected to register a 10.08% CAGR between 2026-2031.

Which region is growing fastest in India’s ICT landscape?

North India is projected to post the quickest 9.8% CAGR through 2031 as data-center investments accelerate.

Why are SMEs driving future ICT demand?

Government credit guarantees and affordable SaaS models allow SMEs to digitize operations while keeping upfront costs low.

How does the Digital Personal Data Protection Act influence ICT spending?

The Act imposes stiff breach penalties, compelling enterprises to invest heavily in zero-trust architectures and managed security services.

What is the market concentration level among IT services providers?

The top five vendors command about 42% of services revenue, translating to a moderate concentration score of 6.

Page last updated on: