Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

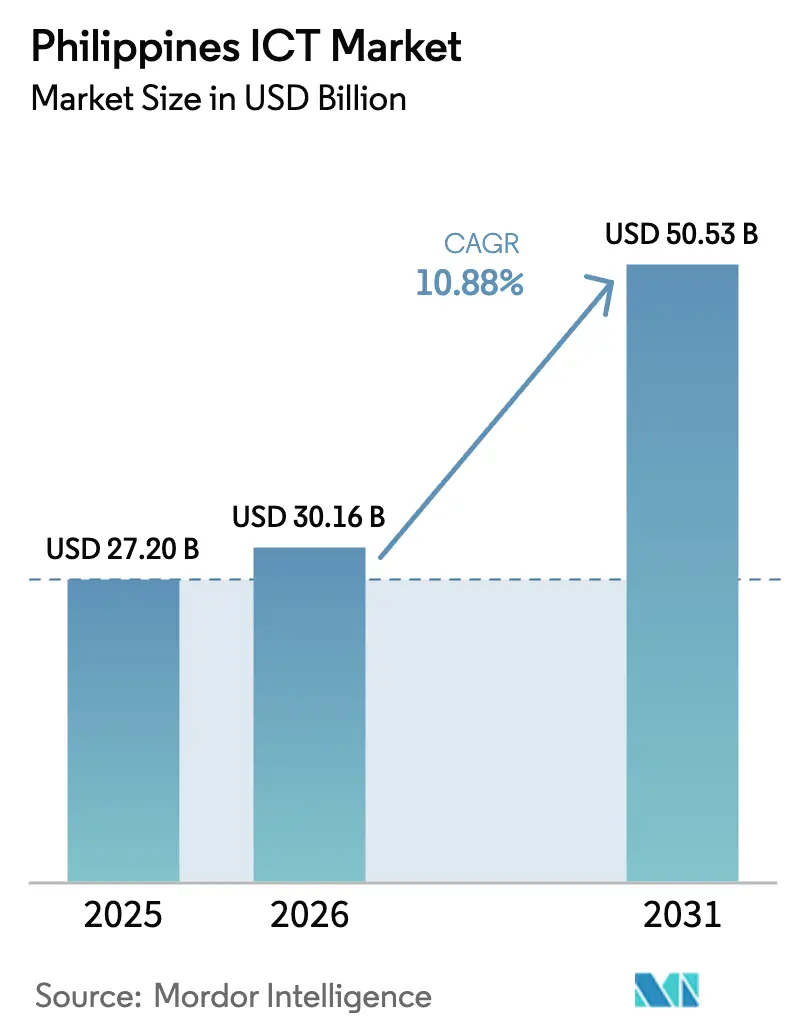

| Base Year Market Size (2025) | USD 27.2 Billion |

| Market Size (2026) | USD 30.16 Billion |

| Market Size (2031) | USD 50.53 Billion |

| Growth Rate (2026 - 2031) | 10.88% CAGR |

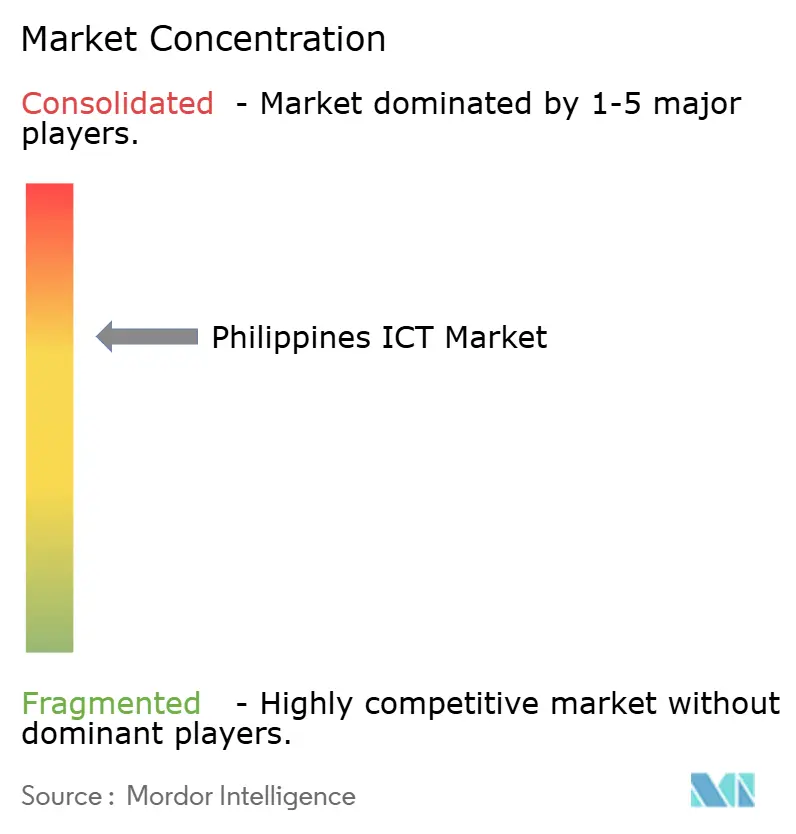

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines ICT Market Analysis by Mordor Intelligence

The Philippines ICT market size was valued at USD 27.2 billion in 2025 and estimated to grow from USD 30.16 billion in 2026 to reach USD 50.53 billion by 2031, at a CAGR of 10.88% during the forecast period (2026-2031). This strong trajectory reflects the archipelago’s liberalized foreign‐investment regime, large‐scale 5G roll-outs, more than USD 10 billion in hyperscale data-center commitments, and a government digitalization plan that is migrating over 70% of public services online.[1]Department of Information and Communications Technology, “e-Government Masterplan 2022-2028 Progress Dashboard,” dict.gov.ph Intensifying demand for cloud, edge, and cybersecurity solutions is reinforcing spending momentum, while tower-sharing policies and new common-tower companies are widening network reach to underserved provinces.[2]PLDT Inc., “Apricot Cable System Lands in the Philippines,” pldt.comSimultaneously, the Philippines ICT market is benefiting from ASEAN supply-chain diversification, which is drawing semiconductor assembly, data-analytics, and AI workloads toward the country’s growing pool of skilled talent.[3]Asian Development Bank, “Technical and Vocational Education and Training in the Philippines,” adb.org Heightened competition among fixed and mobile operators is compressing tariffs but stimulating investment in fiber backhaul, private 5G, and satellite links that collectively lift service quality and geographic coverage.

Key Report Takeaways

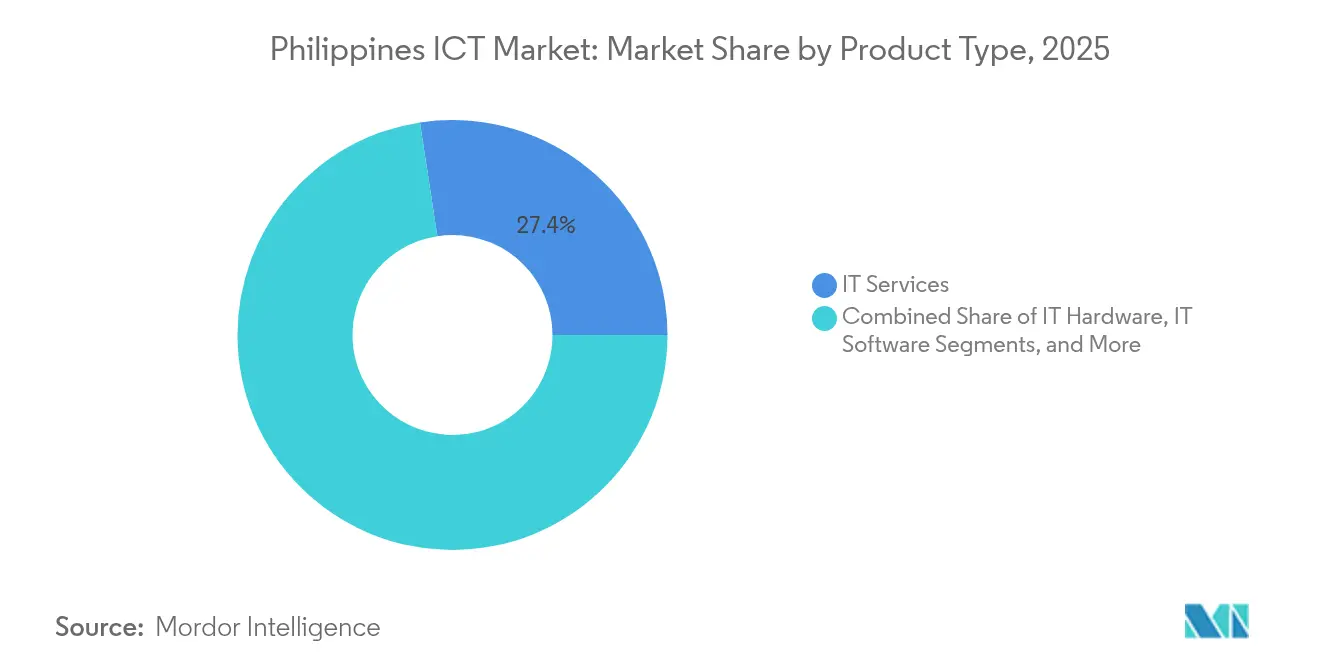

- By product type, IT services held 27.42% of Philippines ICT market share in 2025, security is advancing at an 11.65% CAGR through 2031.

- By enterprise size, large enterprises commanded 60.52% of Philippines ICT market share in 2025, SMEs are projected to grow at a 12.22% CAGR to 2031.

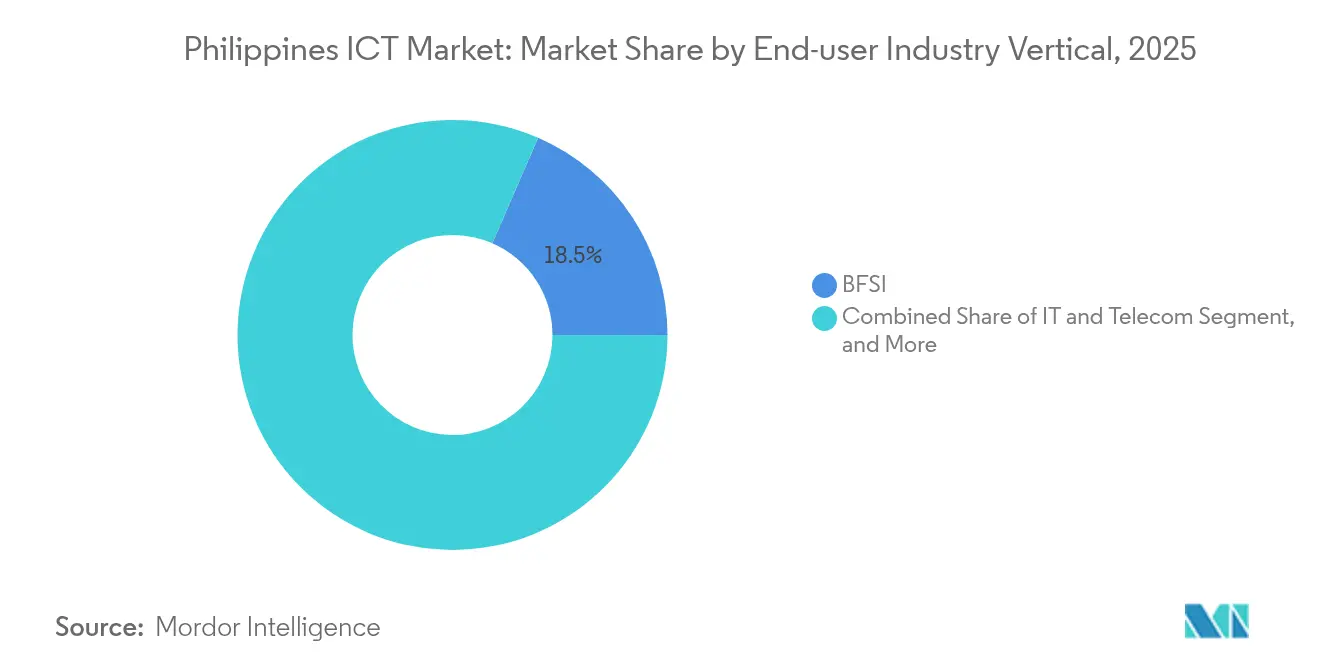

- By end-user industry vertical, BFSI captured 18.48% of Philippines ICT market size in 2025, gaming and esports are set to grow at a 12.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G rollout | +1.8% | Metro Manila, Cebu, Davao | Medium term (2-4 years) |

| Accelerated cloud adoption by SMEs | +1.5% | Urban centers nationwide | Short term (≤ 2 years) |

| Government e-Gov Masterplan 2022-2028 | +2.1% | National; priority in GIDA regions | Long term (≥ 4 years) |

| Surge in hyperscale data-center investment | +1.9% | Manila-Laguna-Cavite growth corridor | Medium term (2-4 years) |

| Digital-payments boom via e-wallets | +1.2% | Rural and urban markets | Short term (≤ 2 years) |

| Growing tech-startup ecosystem | +0.9% | Cebu, Davao, Iloilo | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G Rollout Drives Infrastructure Modernization

The commercial Philippines ICT market is accelerating network modernization as Globe and PLDT jointly surpassed 100 additional Geo-Isolated and Disadvantaged Area (GIDA) 5G sites in 2025. Expanded mid-band spectrum and the new Apricot subsea cable now lift international capacity 33%, positioning the country as a redundancy hub for hyperscale traffic. 5G private networks are extending to logistics, mining, and precision agriculture where fiber remains impractical, while edge nodes colocated within new data centers deliver sub-10 ms latency critical for smart-factory analytics. Carriers are also experimenting with open-RAN to drive down radio costs and diversify vendors, reinforcing long-run capital efficiency. Collectively, these activities are adding depth and resilience to national connectivity, enabling low-latency applications and boosting the Philippines ICT market’s attractiveness to global cloud providers.

Government e-Gov Masterplan Accelerates Public-Sector Digitalization

The Department of Information and Communications Technology has already taken 70% of public services online, issued more than 1 million digital signatures, and deployed 438 VSAT terminals in remote barangays to fulfill e-Gov targets. As ministries migrate databases into sovereign clouds, demand for secure IaaS, SaaS, and integration services grows steadily. Procurement platforms leveraging blockchain for land titling and grant disbursement are being piloted, signaling future opportunities for specialist system integrators. Meanwhile, the Digital Bayanihan program backed by France, Singapore, and multilateral partners supplies skills training for local officials, thus reinforcing long-term adoption. These initiatives deepen the Philippines ICT market penetration into rural regions and produce a reliable public-sector revenue stream for vendors.

Hyperscale Data-Center Investment Transforms Digital Infrastructure

Open-equity rules now allowing 100% foreign participation underpin over USD 10 billion in announced capacity additions from STT GDC, PLDT, and other operators between 2025-2028. Newly commissioned facilities in Sta. Rosa and planned mega-sites in Cavite collectively add more than 200 MW IT load, supporting emerging AI and high-frequency trading workloads with fault-tolerant design and multiple submarine-cable on-ramps. Investment momentum is spilling into secondary cities where edge modules handle latency-sensitive gaming and fintech services. Demand for liquid cooling, modular UPS, and green-energy PPAs is rapidly expanding the addressable Philippines ICT market for specialized infrastructure vendors

Digital-Payments Boom Reshapes Financial-Services ICT

Digital wallet penetration reached 52.8%, and flagship platform GCash grew to 86 million users by mid-2025, setting new transaction peaks across peer-to-peer, merchant, and government payments. Real-time rails are accelerating uptake of anti-fraud analytics, compliance automation, and AI-driven credit scoring, especially among unbanked consumers in rural Luzon and Mindanao. With the central bank targeting a 70% cash-less ratio by 2026, banks and wallet providers are scaling cloud-native cores, deploying biometric KYC, and exploring blockchain-based remittances for the USD 36 billion overseas-worker corridor. Each initiative enlarges the Philippines ICT market addressable by fintech, cybersecurity, and reg-tech suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Last-mile connectivity gaps | −1.4% | Eastern Visayas, ARMM, remote islands | Long term (≥ 4 years) |

| Persistent IT-talent shortage | −1.7% | Nationwide | Medium term (2-4 years) |

| Rising electricity costs | −1.1% | Manila-Laguna data-center corridor | Short term (≤ 2 years) |

| Cyber-extortion and ransomware | −0.8% | BFSI, healthcare clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent IT-Talent Shortage Constrains Market Growth

Only 1 in 10 technical applicants meets AI, data-analytics, or cybersecurity hiring thresholds, leaving an estimated 200,000 vacancies unfille. Although TESDA has tripled online enrollments since 2023, hands-on exposure to Industry 4.0 equipment remains scarce outside flagship universities. Enterprise-based apprenticeships account for less than 4% of total training, dampening the Philippines ICT market’s ability to absorb high-value projects. The Semiconductor and Electronics Industries in the Philippines Foundation is lobbying for incentive packages and a USD 500 million skills fund to stave off regional talent leakage, but any impact is unlikely before 2027.

Rising Electricity Costs Threaten Data-Center Economics

Wholesale power prices climbed more than 20% in the past 12 months and could triple again by 2029 under current generation-mix projections. Data-center operators consume up to 150 GWh annually per campus, exposing them to cost volatility and carbon-reduction scrutiny. Grid instability necessitates multi-feed redundancy and on-site diesel backup, elevating capex by roughly 15% per MW. Operators are responding with solar PPAs, waste-heat reuse, and immersion cooling, but unless renewable penetration climbs above 35% the Philippines ICT market will see margin pressure that could delay fresh hyperscale commitments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Lead Digital-Transformation Wave

IT services controlled 27.42% of Philippines ICT market share in 2025 as enterprises shifted capital budgets toward outcome-based managed solutions for cloud migration, AI pilots, and process automation. The segment is forecast to outpace hardware spending through 2031 as international hyperscalers deepen partnerships with local integrators and telcos bundle 5G-enabled edge solutions. At the same time, IT security contributes the fastest incremental revenue, rising at an 11.65% CAGR thanks to ransomware frequency and new data-privacy directives.

The hardware slice remains subdued because the semiconductor assembly base posted just 1-2% top-line growth in 2025 after back-to-back contractions in 2023–2024. Nonetheless, near-shoring from China and incentives for electric-vehicle components are renewing investment in printed-circuit and substrate facilities that could lift hardware contributions after 2027. Communication-services spend is resilient as fiber and satellite deployments race to meet bandwidth demand, strengthening the Philippines ICT market’s foundation for higher-layer software and platform revenues.

By Enterprise Size: SME Growth Outpaces Large-Enterprise Adoption

Large enterprises supplied 60.52% of Philippines ICT market size in 2025, channeling budgets into private 5G, sovereign cloud, and AI-enabled customer-experience platforms. Conglomerates are reinforcing disaster-recovery posture through dual-site data-center contracts and micro-segmented security architectures that favor vertically integrated service providers.

SMEs, however, are expanding spending at a 12.22% CAGR as cloud-first policies remove capital barriers. Low-code SaaS, subscription cybersecurity, and government innovation vouchers underpin adoption, especially in manufacturing and creative industries outside Metro Manila. Yet uneven rural broadband and limited venture funding still curb the Philippines ICT industry’s ability to unlock the full SME opportunity.

By End-User Industry Vertical: Gaming Leads Digital Innovation

BFSI retained the largest Philippines ICT market size share at 18.48% in 2025 on the strength of real-time payments and digital bank licenses. Investments in fraud analytics, open-banking APIs, and blockchain remittances are set to intensify through 2031.

Gaming and esports post the highest growth at 12.86% CAGR as rising disposable incomes, 5G latency improvements, and new tax incentives attract publishers and tournament organizers. Edge data centers in Cebu and Davao reduce ping times for multiplayer titles, while fintech integrations enable instant prize payouts. Early adoption of AR/VR and cloud gaming further enlarges the Philippines ICT market addressable by content-delivery, cybersecurity, and localized payment-gateway vendors.

Geography Analysis

Metro Manila controls more than half of current Philippines ICT market revenues, leveraging dense fiber rings, multiple submarine-cable landings, and a deep talent pool. The Apricot cable, operational since February 2025, raises Manila’s total international capacity above 140 Tbps and diversifies routes away from the South China Sea. This surge is drawing hyperscalers, fintechs, and AI startups to Quezon City and Bonifacio Global City, lifting data-center absorption and premium office rents.

Central business districts in Cebu, Davao, and Iloilo are forming secondary hubs, backed by DICT’s free-Wi-Fi, startup grants, and expanded VSAT connectivity. Eastern Communications extended 400 Gbps links into Mindanao, while tower-cos break ground on colocation sites that shorten deployment timelines. These advances raise the Philippines ICT market’s regional diversity and mitigate over-reliance on Luzon.

Despite progress, roughly 25 million citizens in 7,000-plus barangays remain underserved. Tower density of 0.15 per 1,000 population trails regional peers, and license-processing delays add 6-12 months to site energization. Ongoing common-tower buildouts, satellite resellers, and PPP funding proposals aim to narrow the divide, but last-mile economics continue to weigh on nationwide Philippines ICT market penetration.

Competitive Landscape

The market remains moderately concentrated: PLDT and Globe collectively exceed 80% share of national fixed-line and mobile infrastructure, leveraging capex scale to entrench network quality advantages. Both raised fresh funding PLDT secured PHP 4 billion in green loans, while Globe allotted PHP 1 billion to a Bataan fiber expansion underscoring the duopoly’s capital firepower. Regulatory pressure via the Konektadong Pinoy bill seeks to open dark-fiber leasing and cut broadband pricing, hinting at potential dilution of incumbent power.

Hyperscale newcomers shift bargaining power dynamics. ENDECGROUP’s 300 MW campus and STT GDC’s 124 MW build introduce alternative long-haul interconnection paths, giving enterprises optionality beyond telco colocation offers. Cybersecurity remains undersupplied relative to threat volumes, presenting white-space for niche vendors capable of bundling monitoring, incident response, and compliance tooling.

International entrants often partner rather than compete head-on: Revolut’s Manila tech hub illustrates the attraction of local talent and pro-digital policy frameworks. Microsoft’s pledge to train 100,000 Filipinos in AI complements the National AI Strategy’s workforce pillar, signaling collaborative skills development. Unified standards mandated for government ICT procurement could favor large integrators with certified processes, posing entry hurdles for smaller challengers.

Philippines ICT Industry Leaders

Accenture plc

Cisco Systems, Inc.

Oracle Corporation

Amazon.com Inc.

International Business Machines Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Huawei and Converge ICT deployed the DC OptiX 2.0 WDM platform, boosting inter-data-center bandwidth 20-fold and cutting rack space by 70%.

- April 2025: PLDT inaugurated its 11th data center in Sta. Rosa and announced a record-scale Cavite facility slated for 2026.

- April 2025: The Department of Trade and Industry partnered with INCIT to roll out the Smart Industry Readiness Index nationwide.

- March 2025: Converge ICT began reselling Starlink services to remote communities and automated backbone operations with Ribbon’s MUSE platform.

Philippines ICT Market Report Scope

The Philippines ICT market tracks revenue accrued through the sale of ICT offerings including IT hardware, IT software, IT services, IT infrastructure and communication services that are being used in various end-user industry across the Country.

The Philippine ICT market is segmented by type (IT hardware (computer hardware, networking equipment, peripherals), IT software, IT services (managed services, business process services, business consulting services, cloud services), IT infrastructure/data centers (colocation data centers, data center storage, data center servers, data center compute), IT security/ cybersecurity (application security, cloud security, data security, identity and access management, infrastructure protection, integrated risk management, network security equipment, endpoint security), communication services), enterprise size (small and medium enterprises, large enterprises), by industry vertical (BFSI, IT & Telecom, government, retail & e-commerce, manufacturing, energy & utilities, others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By End-user Industry Vertical

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-commerce, and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Gaming and Esports |

| Other Verticals |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-commerce, and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Gaming and Esports | ||

| Other Verticals | ||

Key Questions Answered in the Report

How big will the Philippines ICT market be by 2031?

Forecasts show the Philippines ICT market will reach USD 50.53 billion by 2031, growing at a 10.88% CAGR.

Which segment is growing the fastest?

IT security, driven by heightened ransomware risk, is projected to post an 11.65% CAGR through 2031.

Why are hybrid clouds gaining ground?

Enterprises combine on-premise control with public-cloud scalability to meet data-sovereignty rules and cost targets, pushing hybrid adoption at a 12.63% CAGR.

How will electricity prices affect data-center operators?

Rising power costs are compressing margins, making renewable PPAs and energy-efficient cooling essential for new builds over the next five years.

What drives ICT demand outside Metro Manila?

Government Wi-Fi programs, new tower-company investments, and startup incentives are spurring regional hubs in Cebu, Davao, and Iloilo.

Which new technologies will shape the market by 2031?

5G private networks, edge computing, AI-enabled analytics, and blockchain-based payment and land-registry systems will dominate enterprise roadmaps.

Page last updated on: