Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

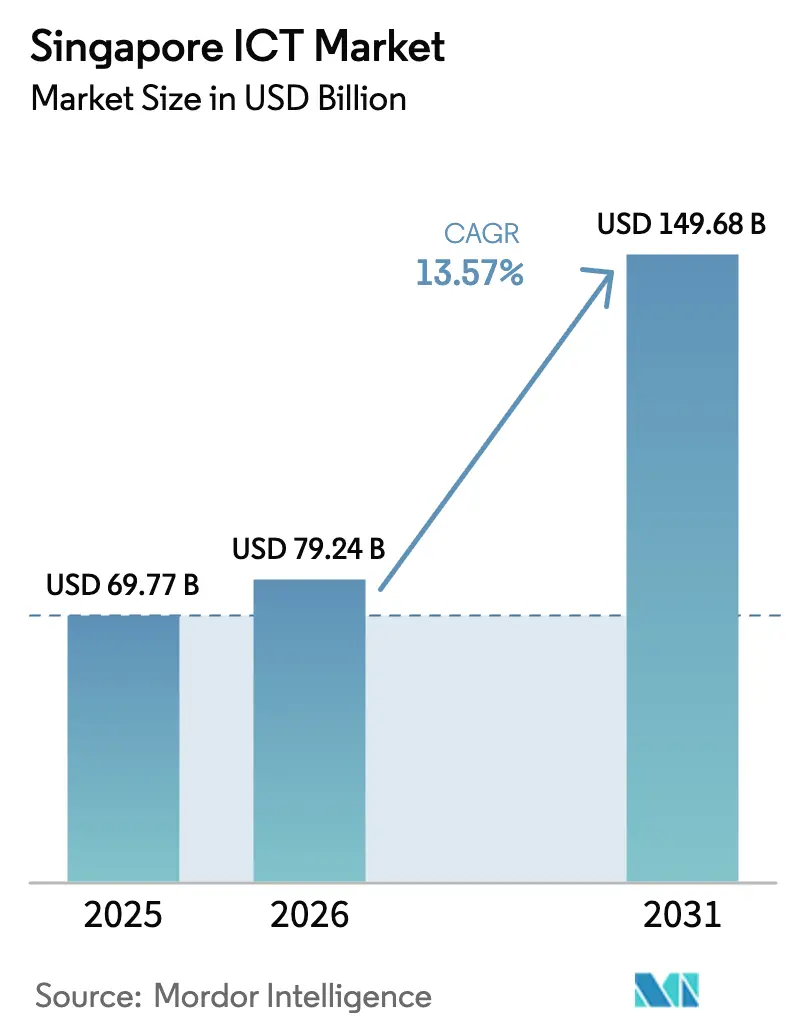

| Base Year Market Size (2025) | USD 69.77 Billion |

| Market Size (2026) | USD 79.24 Billion |

| Market Size (2031) | USD 149.68 Billion |

| Growth Rate (2026 - 2031) | 13.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore ICT Market Analysis by Mordor Intelligence

The Singapore ICT market size is expected to grow from USD 69.77 billion in 2025 to USD 79.24 billion in 2026 and is forecast to reach USD 149.68 billion by 2031 at 13.57% CAGR over 2026-2031. Singapore’s surge pivots on Smart Nation 2.0 funding, hyperscale data-center investments, and accelerated enterprise migration to cloud and AI platforms. Multinational cloud providers are racing to expand local capacity, while small and medium enterprises (SMEs) leverage software-as-a-service to close capability gaps with larger rivals. Sector momentum is also reinforced by healthcare digitalization, digital-only banking licenses, and the National AI Compute Resource (NACR) that lowers barriers to advanced analytics. Heightened spending, however, collides with power-grid limits and a widening cybersecurity talent gap that lifts operating costs and elongate project lead times.

Key Report Takeaways

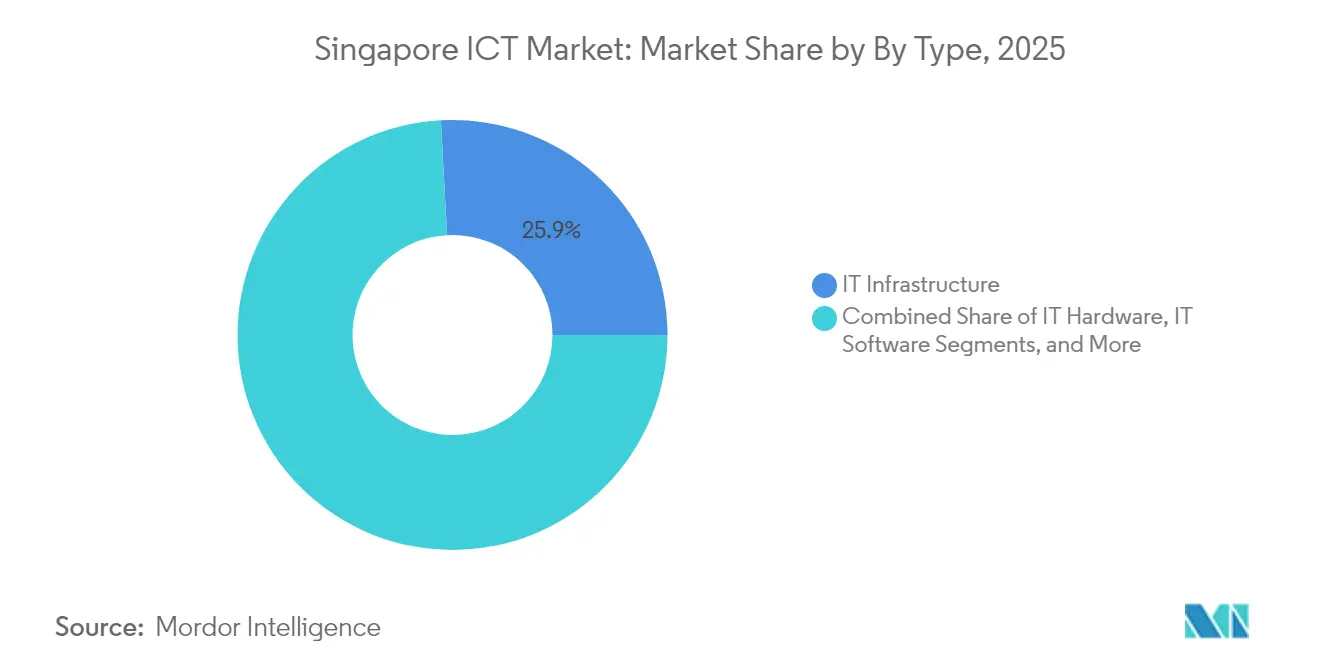

- By type, IT infrastructure captured 25.86% of Singapore ICT market share in 2025, while IT software is forecast to grow at a 16.35% CAGR through 2031.

- By enterprise size, large enterprises held 66.78% of the Singapore ICT market size in 2025; SMEs are advancing at a 14.88% CAGR to 2031.

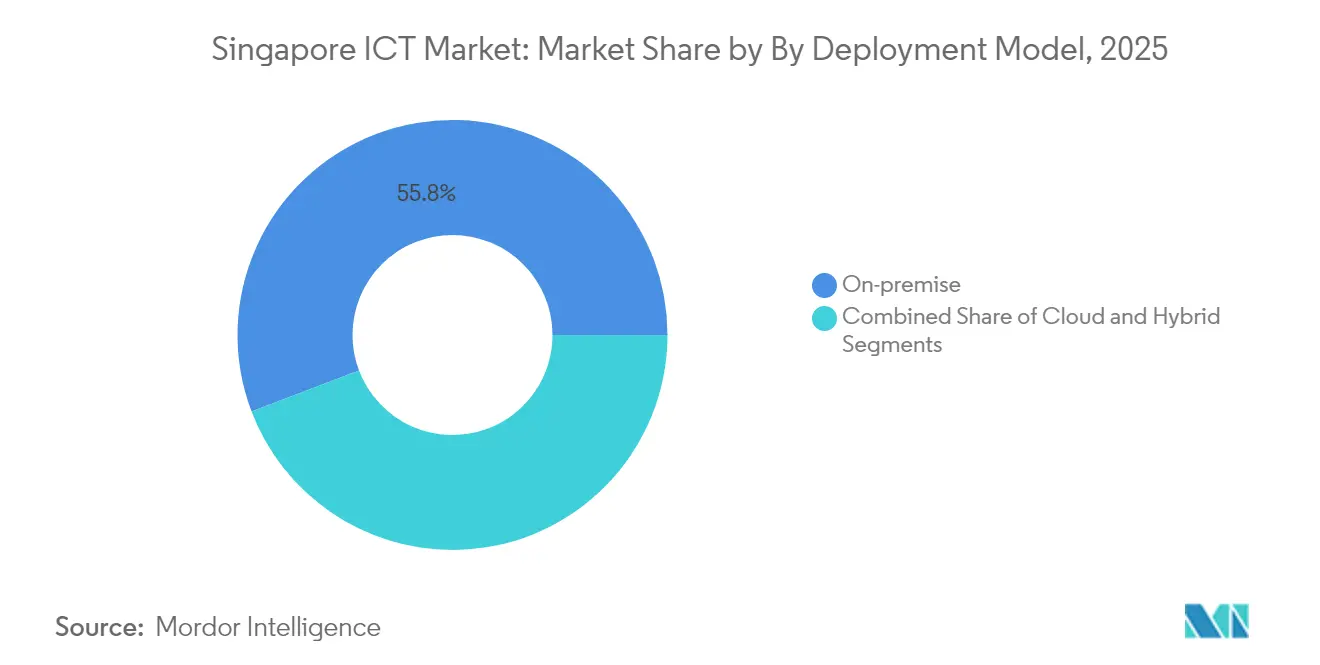

- By deployment model, on-premise solutions led with 55.78% of the Singapore ICT market size in 2025, yet cloud deployments are expanding at a 17.15% CAGR.

- By vertical, BFSI accounted for 21.78% of the Singapore ICT market share in 2025, whereas healthcare and life sciences are poised for an 17.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Smart-Nation Expenditure Surge | +2.1% | National, urban hubs | Medium term (2–4 years) |

| Rapid 5G Roll-out and Adoption | +1.8% | National, enterprise focus | Short term (≤ 2 years) |

| Enterprise Cloud-first Mandates | +2.3% | National, SME-driven growth | Medium term (2–4 years) |

| Digital Bank Licenses Boost BFSI Tech Spend | +1.4% | National, financial district | Short term (≤ 2 years) |

| National AI Compute Resource Roll-out | +1.9% | National, research nodes | Long term (≥ 4 years) |

| Green-Powered Hyperscale Data-center Incentives | +1.6% | National, industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Smart-Nation Expenditure Surge

Smart Nation 2.0 moves Singapore from digital adoption toward digital-first governance, channeling USD 3.3 billion in fiscal 2024 into cybersecurity, data platforms, and modernized infrastructure. The outlay accelerates procurement of analytics engines, edge devices, and real-time processing tools, catalyzing demand far beyond the public sector. Regulatory requirements that mirror these standards push private organizations, especially in finance and healthcare, to upgrade legacy systems. Vendors specializing in API orchestration and cross-platform security gain direct access to large multi-year contracts, while interoperable frameworks reduce integration friction across verticals.

Enterprise Cloud-first Mandates

Cloud-first policies have flipped infrastructure planning, with cloud workloads growing 17.7% against 11.2% for on-premise deployments. Multi-cloud strategies lessen vendor lock-in and satisfy data-sovereignty rules, prompting a USD 3.5 billion domestic cloud market. SMEs drive the fastest uptake, using subscription-based AI, analytics, and automation to match big-company capabilities. Secondary demand is emerging for unified observability dashboards, hybrid connectivity fabrics, and automated policy governance that keep distributed environments in regulatory compliance.

Digital Bank Licenses Boost BFSI Tech Spend

New digital banking licenses have carved out cloud-native players that skip expensive core conversions, channeling fresh spending into API-first architectures, real-time fraud analytics, and conversational interfaces [1]Economic Development Board, “SAP invests S$12 million in its Digital Innovation Accelerator to boost adoption of Business AI in Singapore,” edb.gov.sg. Incumbents respond with accelerated modernization budgets, raising total BFSI technology outlays even as overall vertical growth slows. Compliance automation, blockchain integration, and zero-trust security become must-have modules, opening niches for SaaS vendors with proven fintech credentials.

National AI Compute Resource Roll-out

The NACR allocates USD 270 million to local supercomputing clusters, positioning Singapore as Southeast Asia’s AI proving ground. Accessible capacity lowers experimentation barriers for startups and researchers, while joint programs with universities expand the skilled-talent pipeline. Corporate adopters benefit from proximity to high-density compute, trimming latency for inference workloads in healthcare diagnostics and industrial simulation. Complementary investments, such as SAP’s USD 8.9 million Digital Innovation Accelerator, signal a multiplier effect across the software stack.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Skilled Digital Talent | -1.7% | Nationwide, AI/ML roles | Long term (≥ 4 years) |

| Escalating Cyber-attack Surface | -1.2% | Enterprise networks | Short term (≤ 2 years) |

| Power-grid Capacity Caps on New DC Builds | -0.9% | Industrial zones | Medium term (2–4 years) |

| Wage Inflation from Foreign-Labor Curbs | -1.1% | Technology clusters | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Skilled Digital Talent

A shortage of 2,800 to 4,400 cybersecurity professionals shackles rollout schedules and elevates salary costs, even as security demand is set to hit USD 4.82 billion by 2029. The gap extends to AI engineers and cloud architects, forcing SMEs to compete with multinationals on compensation. Government-backed upskilling programs, including IBM’s SkillsBuild, which targets 4,500 learners, will narrow deficits only gradually. Firms therefore pivot to low-code platforms, AI-assisted development, and managed services that reduce reliance on scarce specialists.

Escalating Cyber-attack Surface

Rapid digitalization widens exposure, with 5G, IoT, and cloud APIs multiplying entry points for threat actors. The attack surface expansion drives near-term adoption of zero-trust architectures, secure access service edge (SASE) frameworks, and AI-enabled anomaly detection. Yet implementation is slowed by fragmented legacy systems and overlapping regulatory mandates. Insurers are also tightening underwriting criteria, raising premiums on firms lacking mature cybersecurity postures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Software Innovation Drives Infrastructure Modernization

IT infrastructure owned 25.86% of Singapore ICT market size in 2025, underlining continued investment in data centers, networking gear, and server capacity . The segment benefits from hyperscale expansion commitments such as AWS’s USD 12 billion plan, but year-on-year growth is moderating as virtualization densifies server racks. IT software outpaces all other categories with a 16.35% CAGR, propelled by cloud-native platforms, AI toolchains, and workflow automation suites. This software pivot lifts demand for container orchestration, micro-services security, and agile integration services. Parallel expansion of infrastructure and applications underpins a balanced growth profile. Companies increasingly adopt subscription pricing for enterprise software, flattening capex spikes and smoothing cash flows. Hardware margins tighten amid commoditization, though specialized AI accelerators and edge devices command premiums. Major vendors such as SAP anchor R&D in Singapore, exemplified by its Digital Innovation Accelerator that aligns industry-specific AI models with local use cases . The interplay of high-capacity infrastructure with advanced software creates a virtuous cycle that keeps the Singapore ICT market on its upward trajectory.

By End-User Enterprise Size: SME Digital Democratization Accelerates

Large enterprises held 66.78% of Singapore ICT market share in 2025, leveraging budgets and in-house talent to execute complex, multi-domain digitization. Growth, however, is slowing to 12.84% as many have already completed first-wave transformations. SMEs, in contrast, are posting a 14.88% CAGR, driven by government grants and cloud subscriptions that compress deployment cycles. The widening availability of turnkey AI services empowers small firms to integrate chatbots, analytics, and robotic process automation without owning expensive hardware. Training initiatives keep the pipeline of digital talent flowing to smaller companies. IBM’s SkillsBuild is one example that provides free certification tracks for data analytics and cybersecurity . Financial incentives such as the Productivity Solutions Grant reimburse up to 70% of qualifying tech investments, further equalizing adoption conditions. As SMEs scale, they form a sizeable customer base for managed-service providers and value-added resellers, reinforcing a diversified vendor ecosystem that underpins the Singapore ICT market.

By Deployment Model: Hybrid Architectures Bridge Legacy and Cloud

On-premise systems still command 55.78% of Singapore ICT market size in 2025, reflecting strict data-sovereignty rules and sunk investment in proprietary hardware . Yet cloud deployments are advancing at a 17.15% CAGR, supported by local availability zones from AWS, Google, and Microsoft. Hybrid patterns are fast becoming standard operating models, allowing enterprises to address latency-sensitive workloads on-premise while exploiting elastic compute for peak demand. Enterprise maturity in cloud governance is improving. Organizations are building centralized FinOps teams and deploying automated policy engines to optimize resource usage across multi-cloud estates. Compliance frameworks issued by the Infocomm Media Development Authority (IMDA) now certify sovereign cloud configurations, lowering risk perceptions. Edge computing is gaining traction as a complement to hyperscale, balancing workloads across micro-data centers that relieve pressure on the national power grid.

By End-User Industry Vertical: Healthcare Digitalization Outpaces Financial Services

BFSI retained the largest slice of Singapore ICT market size at 21.78% in 2025, buoyed by digital banking, reg-tech, and cybersecurity programs . Spending intensity remains high as incumbent banks fortify core systems against new digital upstarts. Still, healthcare and life sciences post the fastest 17.93% CAGR through 2031. Precision medicine, AI-driven diagnostics, and tele-consult platforms are scaling rapidly within public and private hospitals, supported by NACR resources and strict data-privacy enforcement. Manufacturing is also lifting ICT demand via Industry 4.0 retrofits, including IoT sensors and predictive maintenance. Government and public services prioritize citizen-centric portals and backend modernization that aligns with Smart Nation KPIs. Meanwhile, retail and logistics firms revise omnichannel roadmaps to account for same-day delivery expectations. Although gaming and esports attract attention, the vertical remains nascent relative to high-value enterprise segments and therefore contributes a smaller revenue share.

Geography Analysis

Singapore’s single-city geography concentrates ICT investment within a compact yet high-density market. Smart Nation 2.0 earmarked USD 3.3 billion for nationwide cybersecurity, data analytics, and digital infrastructure, stimulating first-tier demand across public and private sectors. Pairing this with a USD 760 million slate of new subsea cables reinforces the city-state’s status as a Southeast Asian data gateway. Domestic broadband upgrades to 10 Gbps and extensive 5G coverage raise the baseline for digital service quality.

The regulatory environment remains one of the most transparent in Asia. IMDA mandates clear data-protection requirements and issues licenses that foster competition without compromising security. Local talent initiatives, backed by public–private partnerships, aim to produce job-ready graduates in AI and cloud technologies to sustain expansion. Such predictability has drawn multi-billion-dollar data-center pledges from AWS, Google, and Equinix, anchoring the Singapore ICT market.

Regional connectivity plans extend influence beyond national borders. The Bifrost and upcoming Vietnam-Singapore cables will enlarge subsea capacity and shorten latency to North America and neighboring economies. This makes Singapore the preferred hosting location for regional SaaS vendors and fintech platforms. High-capacity links also encourage edge deployments in nearby markets, with Singapore acting as the command center for multi-country digital operations.

Competitive Landscape

The Singapore ICT market displays moderate fragmentation with pockets of high concentration. Hyperscale cloud infrastructure is dominated by AWS, Microsoft Azure, and Google Cloud, whose combined footprints exceed 70% of available hyperscale capacity. In contrast, software and managed-services segments are populated by regional specialists, system integrators, and startups that address niche requirements such as reg-tech, automation, and vertical AI applications.

Strategic partnerships are the preferred path to scale. IBM and the National University of Singapore launched an AI research center focused on green computing and safety, aligning public research with enterprise demand. SAP tripled its local R&D headcount to accelerate business-AI projects tailored for Southeast Asian clients. These moves reflect an ecosystem anchored on co-innovation rather than pure vendor lock-in, giving enterprises a broad menu of interoperable solutions.

Barriers to entry are rising. Power-grid caps limit new data-center licenses, favoring incumbents that hold existing allocations. Talent shortages inflate wages and push vendors to adopt automation, raising the capital intensity of service-delivery models. Regulatory compliance remains stringent but predictable, rewarding providers that can certify sovereign-cloud architectures and zero-trust postures. Overall, supplier rivalry is shaped by differentiation in domain expertise and the ability to deliver quantifiable ROI to discerning enterprise buyers.

Singapore ICT Industry Leaders

Singapore Telecommunications Ltd. (Singtel)

StarHub Ltd.

M1 Ltd.

Amazon Web Services (AWS) Singapore

Google Asia Pacific Pte. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: GIC and Silver Lake completed a USD 1.7 billion acquisition of Zuora, enlarging Singapore’s footprint in global SaaS billing.

- January 2025: SAP Labs Singapore announced the expansion of local R&D operations, tripling headcount to 420 and adding nine AI researchers by 2030 through the NUS Industrial Postgraduate Programme.

- December 2024: Keppel and Sovico began talks on a USD 150 million Vietnam–Singapore subsea cable to boost regional data-center interconnection.

- August 2024: IBM and the National University of Singapore unveiled plans for an AI research and innovation center focused on green compute.

Singapore ICT Market Report Scope

Information and Communication Technologies or ICT is a broader term for Information Technology (IT). It refers to all communication technologies, such as wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and other media applications and services enabling users to store, access, transmit, retrieve, and manipulate information in a digital form.

Singaporean ICT market tracks revenue accrued through the sale of ICT offerings including IT hardware, IT software, IT services, IT infrastructure and communication services that are being used in various end-user industry across the Country.

The Singaporean ICT market is segmented by type (IT hardware (computer hardware, networking equipment, peripherals), IT software, IT services (managed services, business process services, business consulting services, cloud services), IT infrastructure/data centers (colocation data centers, data center storage, data center servers, data center compute), IT security/ cybersecurity (application security, cloud security, data security, identity and access management, infrastructure protection, integrated risk management, network security equipment, endpoint security), communication services), enterprise size (small and medium enterprises, large enterprises), by industry vertical (BFSI, IT & Telecom, government, retail & e-commerce, manufacturing, energy & utilities, others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| Communication Services |

By End-User Enterprise Size

| Small and Medium Enterprises |

| Large Enterprises |

By Deployment Model

| On-premise |

| Cloud |

| Hybrid |

By End-user Industry Vertical

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas (Up-, Mid-, Down-stream) |

| Gaming and Esports |

| Other Verticals |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| Communication Services | ||

| By End-User Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Deployment Model | On-premise | |

| Cloud | ||

| Hybrid | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| Energy and Utilities | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas (Up-, Mid-, Down-stream) | ||

| Gaming and Esports | ||

| Other Verticals | ||

Key Questions Answered in the Report

How large is the Singapore ICT market in 2026?

The Singapore ICT market size reached USD 79.24 billion in 2026.

What is the predicted growth rate for Singapore’s ICT sector through 2031?

The market is forecast to expand at a 13.57% CAGR to USD 149.68 billion by 2031.

Which enterprise segment is growing faster, SMEs or large corporations?

SMEs are expanding at a 14.88% CAGR, outpacing large enterprises’ 12.84% growth.

Which deployment model is advancing the quickest?

Cloud deployments are rising at a 17.15% CAGR, driven by multi-cloud and hybrid strategies.

Page last updated on: