Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 17.74 Billion |

| Market Size (2026) | USD 19.68 Billion |

| Market Size (2031) | USD 33.08 Billion |

| Growth Rate (2026 - 2031) | 10.95% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand ICT Market Analysis by Mordor Intelligence

The Thailand ICT market size is expected to grow from USD 17.74 billion in 2025 to USD 19.68 billion in 2026 and is forecast to reach USD 33.08 billion by 2031 at 10.95% CAGR over 2026-2031. This expansion reflects the country’s push to become a regional digital hub, propelled by nationwide 5G coverage, hyperscale data-center investment, and a government cloud-first mandate. Telecommunications service providers monetize 5G network slicing for industrial IoT, while foreign direct investment exceeding USD 1 billion in AI-ready, liquid-cooled facilities anchors the data-center ecosystem. The Thailand ICT market is also buoyed by Industry 4.0 modernization across the Eastern Economic Corridor, rising demand for cybersecurity services, and virtual-bank licensing that expands fintech infrastructure. At the same time, the market confronts talent shortages and stricter data-localization rules that heighten compliance costs.

Key Report Takeaways

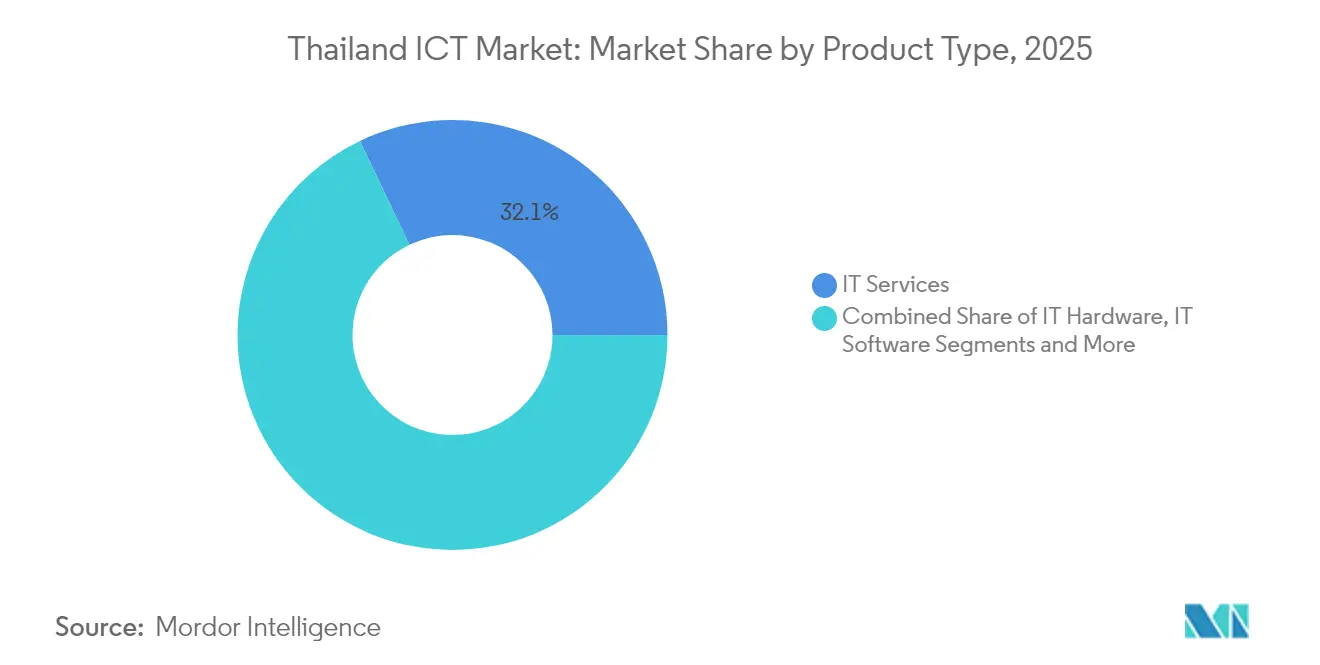

- By product type, IT Services held 32.08% of the Thailand ICT market share in 2025; Cloud Services within this category is projected to grow at an 11.45% CAGR through 2031.

- By enterprise size, Large Enterprises commanded 59.25% of the Thailand ICT market size in 2025, whereas Small and Medium Enterprises are expected to expand at a 12.05% CAGR through 2031.

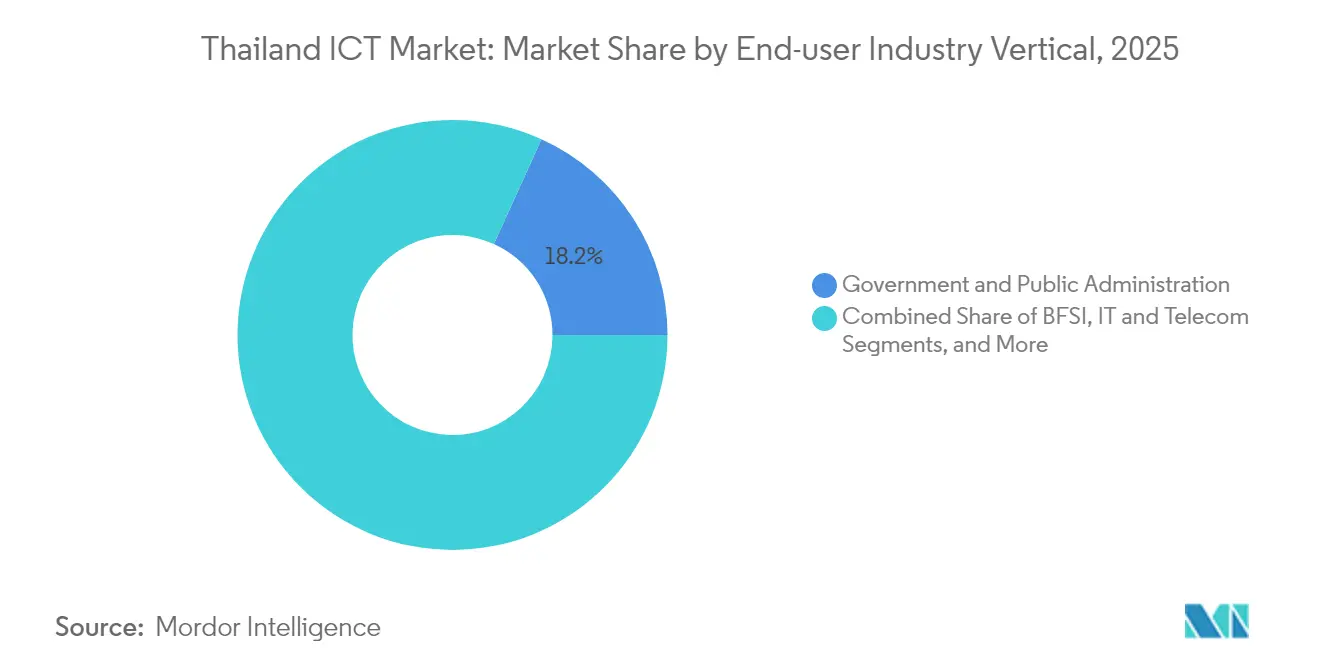

- By end-user vertical, Government and Public Administration captured 18.21% of the Thailand ICT market share in 2025, yet Gaming and Esports is on track for a 12.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G network deployment and subscriber uptake | +2.8% | National, with early gains in Bangkok, Chonburi, Chiang Mai | Short term (≤ 2 years) |

| Government "Cloud-First" policy accelerating adoption | +2.1% | National, concentrated in government agencies and SOEs | Medium term (2-4 years) |

| Enterprise Industry 4.0 digital-transformation surge | +1.9% | Eastern Economic Corridor, Bangkok Metropolitan Region | Medium term (2-4 years) |

| Hyperscale data-center FDI inflows | +1.7% | Bangkok Metropolitan Region, Eastern Economic Corridor | Long term (≥ 4 years) |

| Virtual-bank licensing fuelling fintech infrastructure | +1.4% | National, with concentration in urban centers | Medium term (2-4 years) |

| AI-ready, liquid-cooling data-center hub ambitions | +1.2% | Bangkok Metropolitan Region, Chonburi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G Network Deployment and Subscriber Uptake

Nationwide 5G roll-out reached 95% population coverage by 2024, enabling edge-computing use cases for predictive maintenance in manufacturing and real-time logistics tracking. Operators deploy network-slicing to offer dedicated throughput for mission-critical applications, unlocking enterprise revenue streams that move beyond consumer voice and data. The National Broadcasting and Telecommunications Commission’s spectrum allocations and infrastructure-sharing rules lower deployment costs for rural areas, accelerating adoption outside Bangkok. Manufacturers in the Eastern Economic Corridor integrate 5G sensors with AI analytics to cut unplanned downtime and boost throughput. Rising 5G handset penetration fuels subscriber migration, pushing average data consumption to double-digit gigabyte levels per user each month.[1] Advanced Info Service, “AIS 5G Coverage Reaches 95% Population,” ais.co.th

Government “Cloud-First” Policy Accelerating Adoption

Since 2024, every public-sector agency must justify on-premises procurements as exceptions, prompting ministries to migrate legacy systems onto domestic cloud regions certified under ISO 27001 and the Personal Data Protection Act. The THB 15 billion (USD 0.47 billion) Smart Nation Smart Life program funds shared API gateways and a sovereign large-language-model platform dubbed ThaiLLM hosted in government-approved clouds. State-owned enterprises now publish service catalogs through a single procurement portal, giving private vendors a clear roadmap for integration. The policy has catalyzed similar behavior in regulated industries, with financial institutions benchmarking cloud-security baselines against the government framework. As a result, the Thailand ICT market enjoys a multiplier effect as cloud skills, reference architectures, and procurement templates trickle into the private sector.[2]Digital Government Development Agency, “Cloud-First Policy Implementation,” dga.or.th

Enterprise Industry 4.0 Digital-Transformation Surge

Manufacturers adopt IoT sensors, digital twins, and AI vision systems to raise productivity by up to 30%, aligning with Asia-Pacific Economic Cooperation’s Smart Monodzukuri objectives. Automotive suppliers deploy predictive maintenance to cut unscheduled downtime by 40%, while food processors integrate farm-to-fork traceability dashboards that meet export compliance standards. Government subsidies ease initial setup costs for SMEs, although implementation complexity remains a hurdle. Analytics-driven quality assurance shortens inspection times and reduces scrap rates, directly improving gross margins. The surge in demand for integration services underpins steady growth in the Thailand ICT market, stimulating partner ecosystems of system integrators and device makers.[3]Asia-Pacific Economic Cooperation, “Smart Monodzukuri Initiative,” apec.org

Hyperscale Data-Center FDI Inflows

Foreign investors commit capital to Bangkok and Chonburi facilities that feature liquid-cooling racks optimized for GPU clusters running AI workloads. STT GDC’s USD 240 million campus and similar deployments by global cloud providers drive a cluster effect in fiber backhaul, renewable-energy supply contracts, and specialized construction services. The Board of Investment grants eight-year tax holidays and permits majority foreign ownership in the Eastern Economic Corridor, narrowing the incentive gap with Singapore and Malaysia. New entrants increase inter-connection density, lowering latency for users and enabling local hosting that meets data-sovereignty rules. These inflows reinforce Thailand’s ambition to position itself as the preferred secondary data-center node for ASEAN enterprises.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented SME digital-skills and cyber-readiness gap | -1.8% | National, with acute impact in rural and secondary cities | Long term (≥ 4 years) |

| Shortage of advanced ICT talent and rising labor cost | -1.5% | Bangkok Metropolitan Region, Eastern Economic Corridor | Medium term (2-4 years) |

| Stricter data-localization mandates increasing TCO | -1.1% | National, affecting multinational enterprises | Short term (≤ 2 years) |

| Soaring cyber-fraud liability dampening ICT budgets | -0.9% | National, concentrated in financial services and e-commerce | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented SME Digital-Skills and Cyber-Readiness Gap

Nine in ten Thai SMEs lack formal digital investment plans, and many who do migrate to cloud overlook basic security configurations such as multi-factor authentication or role-based access. Limited awareness of zero-trust frameworks leaves smaller firms exposed to phishing and ransomware that can cripple operations for weeks. Government vouchers under the SME 4.0 program subsidize training and consulting, yet usage remains below 30% because owners prioritize immediate cash-flow concerns. Cyber-insurance premiums climb as underwriters factor in elevated breach frequency among small businesses. Without continuous skills development, the Thailand ICT market risks slower cloud uptake outside the urban core.

Shortage of Advanced ICT Talent and Rising Labor Cost

Demand for AI engineers, cloud architects, and cybersecurity analysts far exceeds domestic supply. Senior professionals command 40-50% salary premiums compared with 2022, eroding cost advantages that once attracted off-shoring contracts to Thailand. Enterprises resort to accelerated reskilling boot camps, while universities expand STEM enrollment but face a multi-year lead time before graduates enter the workforce. The talent crunch hits SMEs hardest, limiting their ability to execute complex digital projects and forcing greater reliance on managed-service providers. Over time, wage inflation could redirect foreign investment to neighboring markets unless talent pipelines scale rapidly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Integration Drives Market Evolution

IT Services contributed the largest 32.08% slice of the Thailand ICT market share in 2025, led by managed services contracts and multi-cloud migration projects. Telecom operators outsource network operations centers, and manufacturers engage system integrators for predictive-maintenance deployments. Within this umbrella, Cloud Services is forecast to grow at an 11.45% CAGR as enterprises refactor monolithic applications into API-driven microservices. Hardware demand holds steady on the back of 5G radio upgrades and data-center capital expenditure, while cybersecurity outlays accelerate due to persistent threat vectors.

The migration from capex to opex spending reshapes vendor revenue models. PTT Exploration and Production’s move to a cloud-native development platform reduced application release cycles by 480%, illustrating payoffs realized when legacy systems are modernized. Edge-computing appliances proliferate in manufacturing plants to meet low-latency requirements, creating fresh revenue for hardware vendors certified under National Broadcasting and Telecommunications Commission standards. The Thailand ICT market incorporates low-code development tools that empower business analysts to prototype applications, easing pressure on scarce developer talent.

By End-User Enterprise Size: SME Acceleration Reshapes Demand

Large Enterprises represented 59.25% of the Thailand ICT market size in 2025 thanks to established IT budgets and transformation roadmaps. Yet SMEs are expected to register the fastest 12.05% CAGR through 2031, aided by SaaS platforms that eliminate upfront infrastructure expenses. Subsidized cloud-migration vouchers and turnkey e-commerce packages lower technology adoption barriers for smaller firms.

The democratization of advanced analytics widens the customer base for AI-powered bookkeeping, customer-relationship-management, and inventory control solutions. Digital payment ubiquity further nudges micro-businesses online, enhancing addressable demand for cybersecurity and data-protection services. To serve cost-sensitive SMEs, vendors bundle managed security with productivity suites, striking a balance between functionality and affordability. Consequently, the Thailand ICT market diversifies beyond metropolitan conglomerates into provincial secondary cities.

By End-User Industry Vertical: Gaming Leads Digital Entertainment Surge

Government and Public Administration consumed 18.21% of Thailand ICT market size in 2025, reflecting cloud-first procurement and nationwide e-service rollouts. Yet Gaming and Esports is projected to grow at 12.98% CAGR aided by mobile-first game development, official recognition of esports as a sport, and expanding tournament infrastructure. Cloud gaming reduces hardware barriers, while 5G low-latency connectivity elevates the player experience.

BFSI spends aggressively on core-system modernization and fraud-analytics ahead of virtual-bank launches. Manufacturing digitization anchors Industry 4.0 investments, with electronics exports topping USD 46.2 billion in 2023. Healthcare’s telemedicine uptake persists beyond the pandemic, driving electronic health-record modernization in provincial hospitals. Each vertical stages technology roadmaps suited to sector-specific regulation and competitive dynamics, broadening revenue streams across the Thailand ICT market.

Geography Analysis

The Bangkok Metropolitan Region and the Eastern Economic Corridor jointly generated roughly 69.40% of Thailand ICT market value in 2025, owing to dense fiber infrastructure, proximity to submarine cables, and the presence of multinational headquarters. Bangkok’s colocation campuses achieve sub-5 millisecond intra-city latency, catering to latency-sensitive fintech and gaming workloads. Chonburi’s industrial estates host data-center megaprojects that supply adjacent smart-factory zones with edge-compute capacity.

Government smart-city pilots extend to provincial hubs such as Chiang Mai, where digital-nomad ecosystems stimulate demand for cloud-based collaboration suites. Southern tourist provinces deploy contactless payment and smart-transport systems to elevate visitor experience, yet overall ICT penetration remains below urban centers due to bandwidth constraints. The THB 15 billion (USD 0.47 billion) nationwide infrastructure program aims to close the digital divide through fiber backbone expansion and satellite connectivity for islands and mountainous areas, presenting upside for rural ISP partnerships.

Competitive positioning within ASEAN hinges on maintaining political stability and neutral trade relations. Thailand trails Singapore and Malaysia in submarine-cable density but narrows the gap with projects such as the Asia Direct Cable landing in Rayong. Board of Investment incentives that include eight-year tax holidays and relaxed foreign-ownership caps in special economic zones continue to attract hyperscale commitments. Collectively, these geographic dynamics reinforce sustained expansion of the Thailand ICT market across diverse provinces.

Competitive Landscape

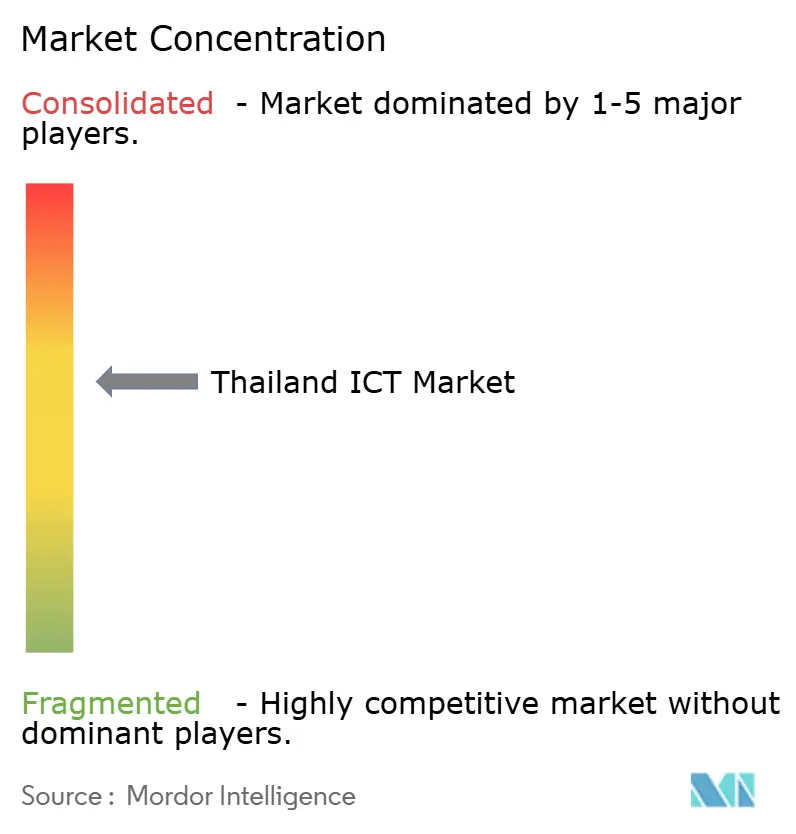

The Thailand ICT market exhibits moderate concentration: top telecom operators Advanced Info Service and True Corporation dominate 5G infrastructure, yet cloud services, cybersecurity, and system integration remain fragmented among global and domestic players. Cloud hyperscalers AWS, Google, and Microsoft anchor local regions to capture growth in regulated workloads, while Chinese providers court cost-sensitive SMEs with aggressive pricing.

Telecom carriers differentiate through AI-enabled network optimization and bundled content to bolster average revenue per user. The True-dtac amalgamation achieved spectrum efficiency and scale advantages without breaching antitrust thresholds, illustrating consolidation trends inside telecom. In IT Services, domestic integrators partner with global software vendors to deliver verticalized solutions for manufacturing, banking, and healthcare.

Competition now centers on platform ecosystems rather than single products. Vendors integrate 5G private networks, edge-computing, and managed security into holistic offerings. The emergence of sovereign AI models sparks alliances between data-center operators and research institutes to secure compute resources. Over the forecast period, white-space opportunities lie in SME-focused SaaS suites, managed detection and response services, and cloud-finops tooling, ensuring vibrant rivalry across the Thailand ICT market.

Thailand ICT Industry Leaders

Cisco Systems Inc.

IBM Corporation

Dell Technologies Inc.

Amazon Web Services, Inc.

Huawei Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Intouch Holdings and Gulf Energy Development received shareholder approvals to merge telecom, digital, and energy assets, streamlining ownership of strategic ICT holdings ahead of regional expansion plans.

- February 2025: Bangkok-based Tellink signed a definitive business-combination agreement with U.S. SPAC Arogo Capital Acquisition Corp., valuing the eSIM specialist at USD 350 million with an intent to list on the Nasdaq Global Market, signaling foreign investor confidence in the Thailand ICT market.

- February 2025: Deloitte Digital released a press note announcing the integration of Appsynth’s 70-person product-innovation team, enhancing its ability to deliver mobile-first solutions for Thai enterprises.

- January 2025: Cal-Comp Electronics (Thailand) outlined its AI automation roadmap for 2025, targeting production optimization for regional SMEs shifting manufacturing to Southeast Asia.

Thailand ICT Market Report Scope

The Thailand ICT market is defined based on the revenues generated from the type such as hardware, software, IT infrastructure, public cloud services, IT services and telecom services that are being used in various end-user industry across the country.

The Thailand ICT market is segmented by type (hardware (storage devices, networking equipment (switches, routers, access points, network security appliances, etc.),computing devices (PCs, tablets, smartphones, etc.),others (peripherals including printers, copiers, etc.)), software (enterprise software (ERP, CRM, SCM, HCM, BI etc.), IT Management (ITSM, Storage & Archiving, Network software, etc.) , BPM and other software (collaboration tools, business process management, etc.), IT infrastructure (data centers,high-performance computing, including processors and servers), public cloud service (infrastructure as a service (IaaS), platform as a service (PaaS) software as a service (SaaS)), IT services (application (or software) services, professional technology services (IT consulting & implementation services, deployment and support, training and education services) outsourcing and managed service (BPO services, application management, IT outsourcing, network and endpoint outsourcing services)), telecommunication services (voice services, data services)), size of enterprise (small and medium enterprise and large enterprise), and industry vertical (BFSI, IT & telecom, government, retail, and e-commerce, manufacturing, energy and utilities and other industry verticals). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By End-user Industry Vertical

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-commerce, and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Gaming and Esports |

| Other Verticals |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-commerce, and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Gaming and Esports | ||

| Other Verticals | ||

Key Questions Answered in the Report

What is the projected value of the Thailand ICT market in 2031?

It is expected to reach USD 33.08 billion, expanding at an 10.95% CAGR.

Which segment holds the largest share of technology spending in Thailand?

IT Services leads with 32.08% of Thailand ICT market share in 2025.

Why are hybrid deployments gaining traction among Thai enterprises?

Hybrid models balance data-sovereignty compliance with access to cloud innovation and are forecast to grow at a 12.3% CAGR.

How does 5G influence industrial digitalization in Thailand?

Nationwide 5G enables IoT-driven predictive maintenance and edge analytics, accelerating Industry 4.0 adoption.

Which vertical is the fastest-growing user of ICT solutions?

Gaming and Esports is set for a 12.98% CAGR through 2031 as mobile gaming and cloud gaming expand.

Page last updated on: