Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

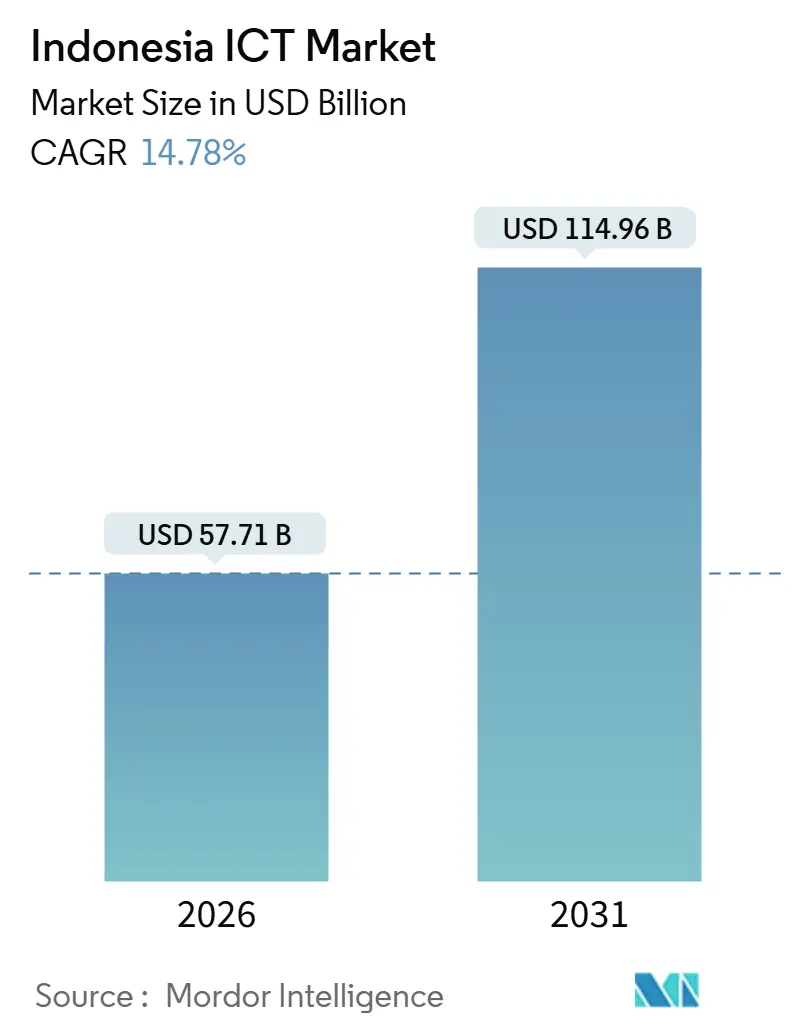

| Market Size (2026) | USD 57.71 Billion |

| Market Size (2031) | USD 114.96 Billion |

| Growth Rate (2026 - 2031) | 14.78% CAGR |

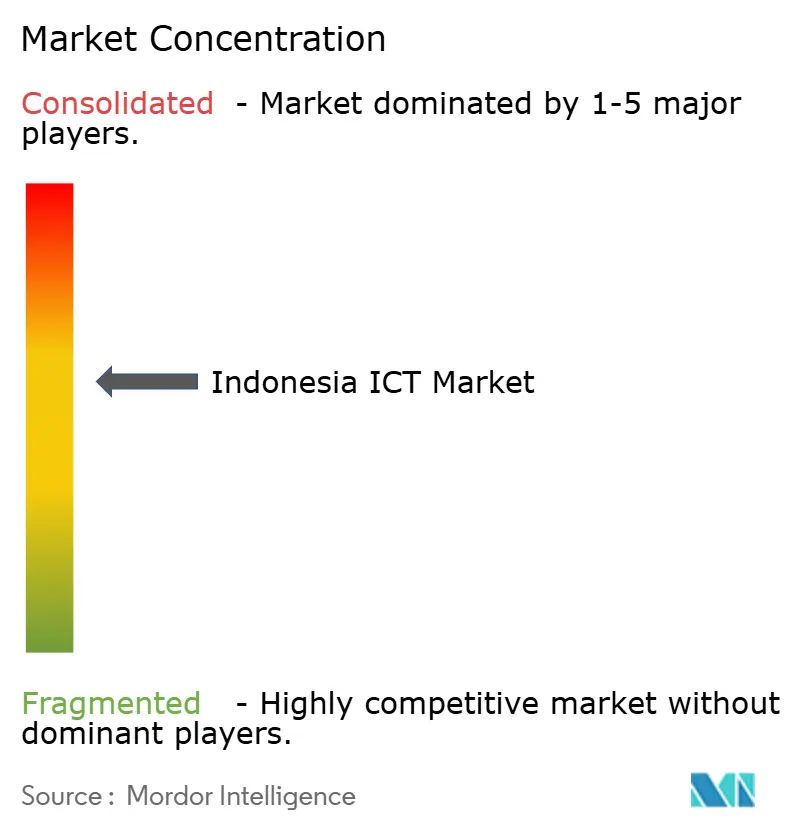

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Indonesia ICT Market Analysis by Mordor Intelligence

Indonesia ICT market size is USD 57.71 billion in 2026 and is projected to reach USD 114.96 billion by 2031, reflecting a 14.78% CAGR. Multiple demand vectors are converging, including the government’s data-localization mandates that compel hyperscalers to invest in local capacity, the deployment of SATRIA-1 that unlocks connectivity in the eastern archipelago, and the rapid shift from legacy infrastructure to hybrid cloud. Enterprises are outsourcing transformation to system integrators to mitigate execution risk, which keeps services spending ahead of hardware outlays. Competitive intensity is rising as domestic telcos bundle connectivity with managed services while global vendors navigate TKDN rules and elevated power tariffs. These dynamics collectively reinforce the Indonesia ICT market’s momentum, even as talent shortages and cybersecurity threats weigh on project execution.

Key Report Takeaways

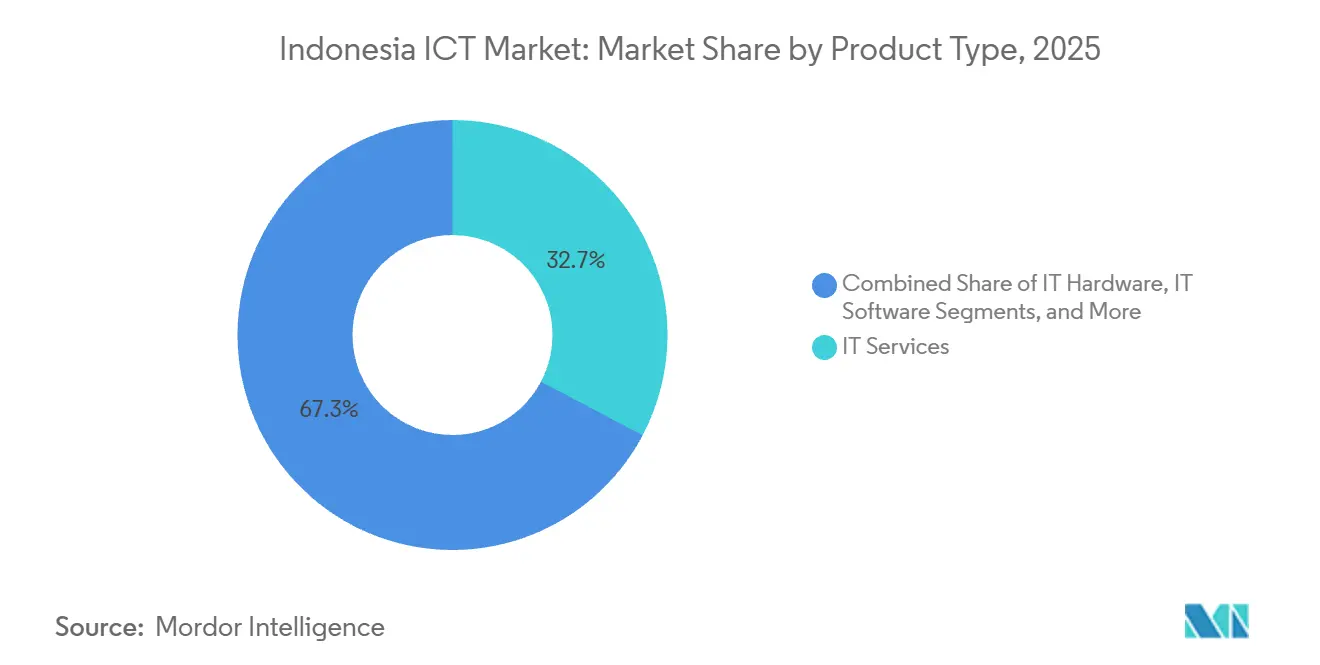

- By product type, IT services captured 32.73% of the Indonesia ICT market share in 2025 while expanding at a 15.22% CAGR through 2031.

- By enterprise size, small and medium-sized enterprises are advancing at a 15.67% CAGR in the Indonesia ICT market, outpacing large-enterprise growth despite holding only 37.16% of spending in 2025.

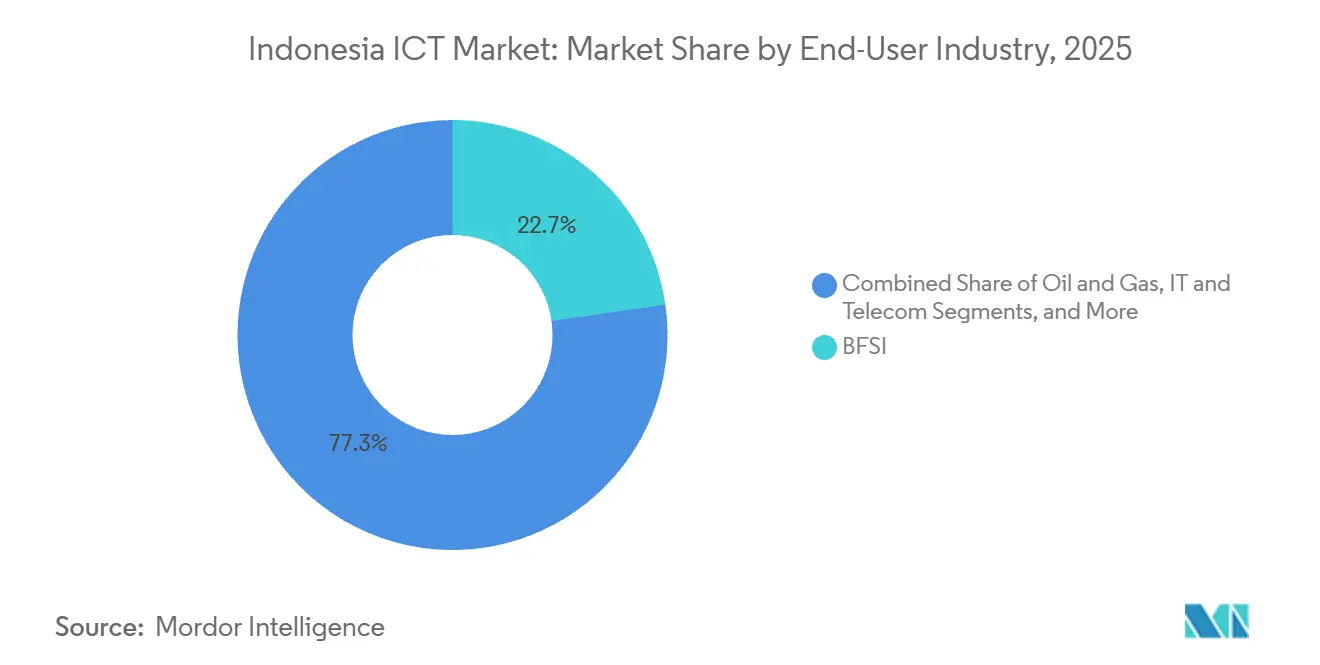

- By end-user industry, healthcare recorded the fastest growth at a 15.18% CAGR in the Indonesia ICT market, whereas BFSI maintained the largest 22.74% revenue share in 2025.

- By deployment model, hybrid architectures grew at 15.44% annually even as cloud commanded 46.83% of the Indonesia ICT market size in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital transformation of Indonesian enterprises | +3.2% | Jakarta, Surabaya, Bandung | Medium term (2-4 years) |

| Government digital-skills and infrastructure push | +2.8% | Eastern provinces | Long term (≥ 4 years) |

| E-commerce boom spurring online payments | +2.5% | Urban centers | Short term (≤ 2 years) |

| Palapa Ring and SATRIA-1 satellite roll-out | +2.1% | Kalimantan, Sulawesi, Papua | Medium term (2-4 years) |

| AI-driven localization of cloud services | +1.8% | National | Medium term (2-4 years) |

| Shift to green data centers amid high power tariffs | +1.4% | Java island | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation Of Indonesian Enterprises

Modernization initiatives dominate technology budgets as conglomerates migrate SAP and Oracle workloads to cloud-native stacks while deploying IoT sensors on factory floors. Accenture’s collaboration with Indosat to build a sovereign AI cloud shows how telcos are recasting themselves as transformation partners rather than pure connectivity utilities. Mandatory TKDN thresholds reward local software development, prompting regional integrators to package turnkey offerings that combine compliance and technical execution. Manufacturing receives explicit policy support through the Making Indonesia 4.0 roadmap. Yet uneven in-house skill levels make outsourcing attractive, which explains the sustained double-digit expansion of services revenue within the Indonesia ICT market.

Government Digital-Skills And Infrastructure Push

The Digital Talent Scholarship delivered 1 million graduates between 2018 and 2024 and targets 100,000 more in 2025. SATRIA-1’s 150 Gbps backbone now supports 30,000 public facilities, complementing the under-utilized 36,000-km Palapa Ring fiber. These initiatives extend basic connectivity to provinces that historically lacked reliable bandwidth and create new addressable demand for cloud, cybersecurity, and e-government platforms. However, employer surveys reveal that many graduates require six months of additional training before they can run production workloads, highlighting persistent capability gaps that temper the Indonesia ICT market’s near-term productivity gains.

E-Commerce Boom Spurring Online Payments

Indonesia’s e-commerce gross merchandise value is projected at USD 65 billion to USD 71 billion in 2025.[1]Google and Temasek, “e-Conomy SEA Report 2025,” blog.google Bank Indonesia’s QRIS standard unifies previously fragmented QR schemes, and by mid-2025 had enrolled 60 million users and more than 40 million merchants. Core banking platforms are under stress, triggering replacement cycles that favor cloud-native vendors. E-wallet providers now pivot toward merchant services such as working-capital financing, thereby expanding their IT budgets for fraud analytics and data-platform upgrades. Consolidation among fintech lenders, driven by stricter OJK rules, funnels capital toward fewer but better-capitalized players, which lifts spending on cybersecurity and compliance tools.

Palapa Ring And SATRIA-1 Satellite Roll-Out

While Palapa Ring operates at only 50-60% capacity, SATRIA-1’s immediate impact on health centers and schools demonstrates the latent demand once connectivity barriers fall. Provincial governments can now procure telemedicine and distance-learning solutions, catalyzing local system-integrator ecosystems. Plans to augment capacity with low-earth-orbit constellations could reduce bandwidth costs but may fragment interoperability if open standards lag. Vendors that bundle managed connectivity with edge applications stand to gain early mover advantage across eastern provinces, thereby broadening the geographic footprint of the Indonesia ICT market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of advanced ICT talent | -2.3% | National | Medium term (2-4 years) |

| Data-privacy and cyber-security concerns | -1.6% | BFSI and government | Short term (≤ 2 years) |

| Local-content rules inflate hardware costs | -1.1% | National | Long term (≥ 4 years) |

| Rising electricity tariffs threaten data-center OpEx | -0.9% | Java | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage Of Advanced ICT Talent

Indonesia needs 9 million ICT professionals by 2030, but current education pipelines will supply only 6 million.[2]World Bank, “Indonesia Digital Economy and ICT Talent Gap,” worldbank.org Salaries for senior cloud engineers in Jakarta climbed 25-30% each year since 2023, eroding cost advantages versus regional hubs. Global vendors launch in-house academies to assure certification-grade skills, yet enterprises still budget six to twelve months of shadowing before new hires achieve full productivity. Services firms now blend local juniors with seasoned offshore architects from India or the Philippines, which mitigates wage inflation but introduces coordination overhead and potential data-sovereignty friction.

Data-Privacy And Cyber-Security Concerns

Ransomware attacks surged in 2025, prompting 67.7% of executives to rank cyber defenses as a top investment priority. The Personal Data Protection Law imposes fines up to IDR 6 billion (USD 375,000) for non-compliance, yet inconsistent enforcement leaves enterprises uncertain about liability. Legal ambiguity slows cloud migrations as teams debate residency boundaries. Indonesia counts fewer than 10,000 CISSP-certified professionals, a ratio far below global norms, fueling demand for outsourced security operations. Concentration of monitoring data in a handful of MSSPs magnifies systemic risk if any provider is breached.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Outpace Hardware As Transformation Accelerates

IT services held 32.73% of the Indonesia ICT market share in 2025 and will grow at a 15.22% CAGR through 2031. Managed security and cloud platform services claim the lion’s share as enterprises outsource transformation complexity. Hardware refresh cycles lengthen while software budgets tilt toward SaaS subscriptions. Zero-trust architectures merge infrastructure and security domains, forcing vendors to deliver integrated stacks. The Indonesia ICT market size for services stands to double by 2031 as ransomware threats and compliance mandates intensify.

Demand for localized SaaS in Bahasa Indonesia encourages domestic software houses, which leverage TKDN incentives to compete with multinationals. Nevertheless, talent scarcity delays large-scale ERP migrations, requiring phased rollouts that extend project timelines. Communication services margins compress under 5G capital intensity, pushing telcos to concentrate on enterprise IoT and edge analytics as value-add layers.

By Enterprise Size: SMEs Digitalize Faster Than Large Incumbents

Large enterprises contributed 62.84% of 2025 spend, yet SMEs clock the fastest 15.67% CAGR, shrinking the gap. Government programs integrated 17 million micro-businesses into e-commerce and fintech ecosystems, lowering onboarding hurdles. QRIS ubiquity lets merchants accept cashless payments via smartphones, sparing them point-of-sale capex. Low-code platforms further democratize application creation, reducing dependence on scarce developers and propelling SME adoption inside the Indonesia ICT market.

Legacy modernization burdens large state-owned enterprises. Mainframe dependencies and complex compliance layers stretch migration roadmaps to multi-year horizons. Telkom Indonesia’s fiber spin-off reallocates capital toward cloud and security, yet reorganizations can delay internal IT upgrades. Vendors able to serve both high-velocity cloud-native SMEs and risk-averse incumbents position themselves for outsized wallet share.

By End-User Industry: Healthcare Surges As BFSI Matures

Healthcare posted the quickest 15.18% CAGR, catalyzed by SATUSEHAT’s integration of 10,000 facilities into a unified data exchange. Real-time electronic health records and telemedicine appointments underpin demand for cloud hosting, cybersecurity, and analytics. Interoperability gaps persist because older hospital systems use proprietary formats, necessitating middleware investments that service integrators eagerly supply within the Indonesia ICT market.

BFSI maintains the largest vertical slice at 22.74% but grows more modestly as open-banking APIs, digital rupiah pilots, and advanced fraud detection top upgrade agendas. Fintech consolidation narrows the competitive field to well-capitalized firms that spend heavily on secure infrastructure. Retail and e-commerce invest in omnichannel platforms, and manufacturing adopts IoT for predictive maintenance, all contributing to diversified vertical growth.

By Deployment Model: Hybrid Architectures Bridge Legacy And Cloud

Cloud deployments represented 46.83% of 2025 revenue, yet hybrid approaches led growth at 15.44% CAGR because data-localization rules demand in-country workloads. Microsoft’s Jakarta region and Oracle’s Batam site offer compliant cloud options. Hybrid lets banks keep core ledgers on-premise while running collaboration suites in the cloud, balancing compliance and cost. The Indonesia ICT market size allocated to hybrid is projected to overtake pure cloud by 2029 if TKDN thresholds tighten further.

Operational complexity rises as teams manage dual toolchains for on-premise and cloud assets. Skill shortages heighten this burden, spurring managed-service providers to bundle observability and security across environments. Indosat’s Sahabat-AI model, tuned for five local languages, shows how cloud platforms deliver differentiated AI at scale.

Geography Analysis

Jakarta, Surabaya, and Bandung collectively account for roughly two-thirds of Indonesia ICT market revenue. The SATRIA-1 satellite, however, extends broadband to Papua, Maluku, and Nusa Tenggara, catalyzing first-time demand for connectivity-enabled services. Provincial health clinics adopt telemedicine, and district schools deploy cloud-hosted learning systems. Sumatra and Kalimantan’s resource industries deploy IoT to monitor oil, gas, and plantation assets, diversifying regional uptake.

Telkom Indonesia’s nationwide GraPARI shops give it unrivaled last-mile reach, while foreign vendors rely on distributor partnerships. The XL Axiata-Smartfren merger combines 94.5 million subscribers, enabling the entity to cross-sell enterprise 5G and IoT across underserved provinces. Batam positions itself as a regional data-center node thanks to proximity to submarine cables and a tax-free regime that lures hyperscalers. Nonetheless, talent shortages and logistics hurdles outside Java temper adoption velocity.

Regional disparity remains stark. While Jakarta pilots AI copilots and advanced analytics, SMEs in eastern islands are only beginning to digitize invoicing. Vendors that tailor go-to-market models to local purchasing power and digital literacy will accelerate penetration and broaden the Indonesia ICT market.

Competitive Landscape

The top ten vendors control roughly 40-45% of total spend, indicating moderate fragmentation. Telkom Indonesia, Indosat Ooredoo Hutchison, and the XL Axiata-Smartfren entity bundle connectivity, cloud, and managed security, creating high switching costs. Hyperscalers such as Microsoft and Oracle build in-country regions to comply with data residency, bypassing telco infrastructure for direct enterprise engagements. TKDN rules steer foreign vendors toward joint ventures with domestic integrators, redistributing value creation locally.

Vertical specialization emerges as the key differentiator. Accenture’s sovereign AI cloud focuses on regulated workloads in BFSI and government, leveraging localized language models and in-country hosting.[3]Accenture. "Accenture and Indosat Partnership for Sovereign AI Cloud." September 2024. https://www.accenture.com Equinix’s USD 74 million JK1 data center targets multi-cloud interconnection for latency-sensitive edge applications. Startups offering low-code platforms undercut multinational license fees and win SMEs by shipping pre-built templates configured for Indonesian tax and payroll rules.

Edge computing presents a white-space opportunity, though commercial use cases remain nascent. Data-center operators invest in regional points-of-presence to capture future demand for autonomous vehicles and industry 4.0 workloads. Meanwhile, rising electricity tariffs compel operators to secure renewable power purchase agreements or risk margin erosion, which may eventually favor capital-intensive hyperscalers.

Indonesia ICT Industry Leaders

-

PT Telkom Indonesia (Persero) Tbk

-

Indosat Ooredoo Hutchison Tbk

-

XL Axiata Tbk

-

Huawei Technologies Co., Ltd.

-

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Bank Indonesia issued draft guidelines for real-time gross settlement integration with blockchain-based digital rupiah pilots, targeting sandbox completion by Q3 2026

- November 2025: Tata Consultancy Services committed USD 1 billion to its HyperVault platform for PDPL-compliant secure data management

- April 2025: Microsoft confirmed a USD 1.7 billion AI-cloud investment and pledged to train 840,000 Indonesians.

- October 2025: Telkom Indonesia finalized the spin-off of its 200,000-km fiber network into Infranexia to focus capital on cloud and cybersecurity services

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Indonesia's ICT market as the total yearly spending on hardware, packaged and custom software, service and support activities, telecommunication subscriptions, and emerging digital platforms that enable the creation, storage, transmission, and use of electronic information across enterprises and government. Spending linked purely to consumer-grade electronics (TVs, game consoles) or over-the-top media subscriptions is not included.

Scope Exclusion: Standalone consumer home-entertainment devices remain outside the boundary, ensuring we stay focused on business-centric ICT demand.

Segmentation Overview

-

By Product Type

-

IT Hardware

- Computer Hardware

- Networking Equipment

- Peripherals

- IT Software

-

IT Services

- IT Consulting and Implementation

- IT Outsourcing (ITO)

- Business Process Outsourcing (BPO)

- Managed Security Services

- Cloud and Platform Services

- IT Infrastructure

-

IT Security / Cybersecurity

- Application Security

- Cloud Security

- Data Security

- Network Security

- Endpoint Security

- Infrastructure Protection

- Integrated Risk Management

- Identity and Access Management (IAM)

- Communication Services

-

IT Hardware

-

By Enterprise Size

- Small and Medium-sized Enterprises

- Large Enterprises

-

By End-user Industry Vertical

- BFSI

- Government and Public Sector

- Oil and Gas

- IT and Telecom

- Retail, E-Commerce and Consumers

- Manufacturing and Industrial

- Energy and Utilities

- Healthcare

- Other End-user Industry Verticals (Transport, Logistics, Education, Hospitality)

-

By Deployment Model

- On-premise

- Cloud

- Hybrid

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured surveys with local CIOs, telecom planners, cloud architects, and channel distributors across Java, Sumatra, and Kalimantan helped us validate typical license stacks, margin structures, and expected 5G-driven traffic growth. Feedback from start-ups, large public agencies, and mid-size retailers closed data gaps on SaaS seat counts and cybersecurity adoption.

Desk Research

We began with Indonesia's Statistics Bureau tables on ICT value-added, Kominfo budget papers, and Bank Indonesia payment statistics, which locate spending flows inside the wider economy. Trade bodies such as Apjatel and the Indonesian Data Centre Provider Organization offered granular fiber-mile additions and installed megawatt capacity, while patent queries on Questel helped us track fast-moving security software innovations. Company 10-Ks, Telkom's investor decks, and regional press carried by Dow Jones Factiva rounded out pricing references for devices and cloud blocks. Acknowledging space limits, many further public and subscription sources were consulted for cross-checks and clarification.

A second sweep gathered customs shipment lines through Volza, IMTMA tooling reports for server imports, and Asia Metal figures for semiconductor input costs, giving us cost benchmarks that underpin hardware volumes. These datasets allowed us to anchor average selling prices and spot anomalies before modelling.

Market-Sizing & Forecasting

We built a top-down model beginning with national ICT spending reported in the public accounts, which is then split by fiber penetration rates, enterprise IT spend-to-GDP share, smartphone adoption, data-center megawatt build-out, average cloud price index, and Kominfo capital plans. Target segment totals are subsequently cross-checked with selective bottom-up supplier tallies (sampled device shipments × ASP and managed-service contract values) to fine-tune each pool. Multivariate regression on the six variables above drives our 2025-2030 forecast, while scenario bands adjust for currency swings and policy shifts. One mention only: top-down and bottom-up reconciliation ensures internal consistency without over-engineering.

Data Validation & Update Cycle

Model outputs pass through variance audits, peer review, and an analyst sign-off. We refresh every twelve months, re-opening the workbook sooner if large policy, pricing, or merger events occur. Clients therefore receive the latest vetted snapshot.

Why Mordor's Indonesia ICT Baseline Numbers Stand Up

Published estimates often differ; definition edges, input lists, and refresh timing rarely align.

Key gap drivers here include whether consumer gadgets are mixed with enterprise budgets, how foreign-currency spends are converted, and the pace at which cloud price deflation is embedded. Mordor Intelligence reports only business-direct ICT outlays, applies quarter-average rupiah rates, and revises the model annually, whereas other publishers may use headline retail electronics sales, single-day FX rates, or longer refresh cycles.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 46.57 B (2025) | Mordor Intelligence | - |

| USD 43.80 B (2024) | Global Consultancy A | includes consumer electronics and blends household broadband with enterprise circuits |

| USD 45.20 B (2024) | Trade Journal B | relies on survey-based spend intentions, limited validation against fiscal data |

| USD 50.00 B (2024) | Industry Service C | applies fixed USD-IDR rate and omits price-erosion adjustments for cloud workloads |

Taken together, the comparison shows that when scope, currency handling, and update cadence are normalized, Mordor's disciplined approach offers a balanced, transparent baseline that decision-makers can trace back to concrete variables and repeatable steps.

Key Questions Answered in the Report

What is the forecast CAGR for Indonesia ICT through 2031?

The Indonesia ICT market is projected to expand at a 14.78% CAGR from 2026 to 2031.

Which product category leads spending?

IT services accounted for 32.73% spending in 2025 and continues to outpace hardware and software growth.

Why are hybrid deployments growing faster than pure cloud?

Enterprises adopt hybrid architectures to satisfy data-localization mandates while leveraging cloud scalability, resulting in a 15.44% CAGR for this model.

How does the SATRIA-1 satellite influence regional demand?

By connecting 30,000 public facilities in remote provinces, SATRIA-1 unlocks new demand for telemedicine, e-government, and education services.

Which industry vertical is expanding most quickly?

Healthcare is advancing at a 15.18% CAGR due to the nationwide SATUSEHAT data-exchange platform.

What challenges threaten market growth?

Talent shortages, cybersecurity risks, and rising electricity tariffs increase project costs and execution complexity.

Page last updated on: