Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

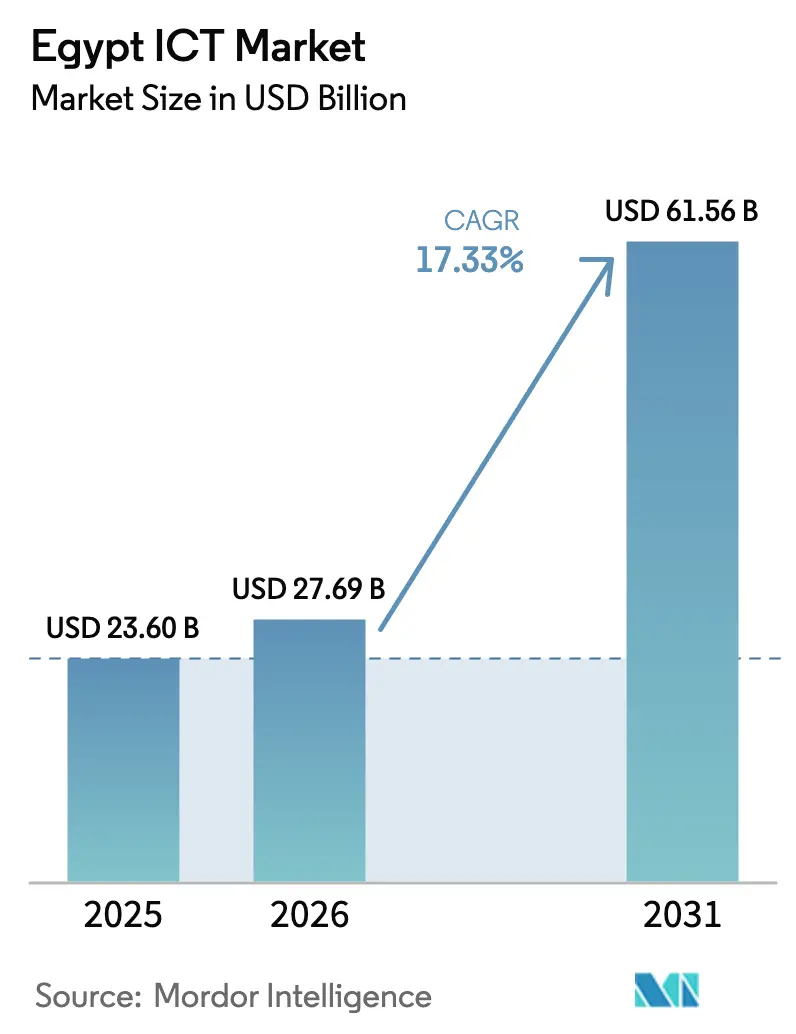

| Base Year Market Size (2025) | USD 23.60 Billion |

| Market Size (2026) | USD 27.69 Billion |

| Market Size (2031) | USD 61.56 Billion |

| Growth Rate (2026 - 2031) | 17.33% CAGR |

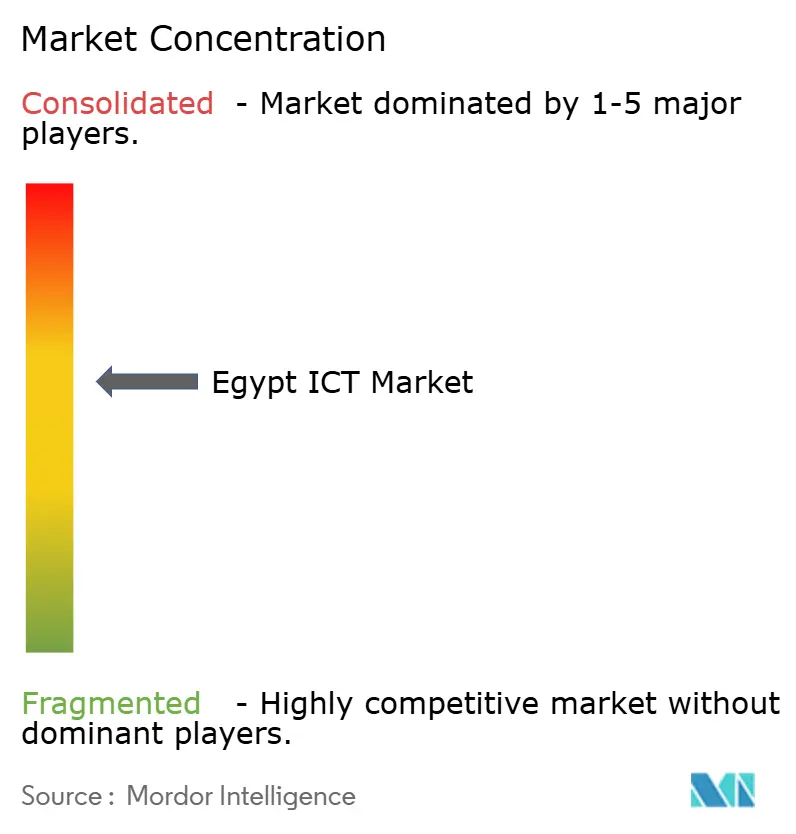

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt ICT Market Analysis by Mordor Intelligence

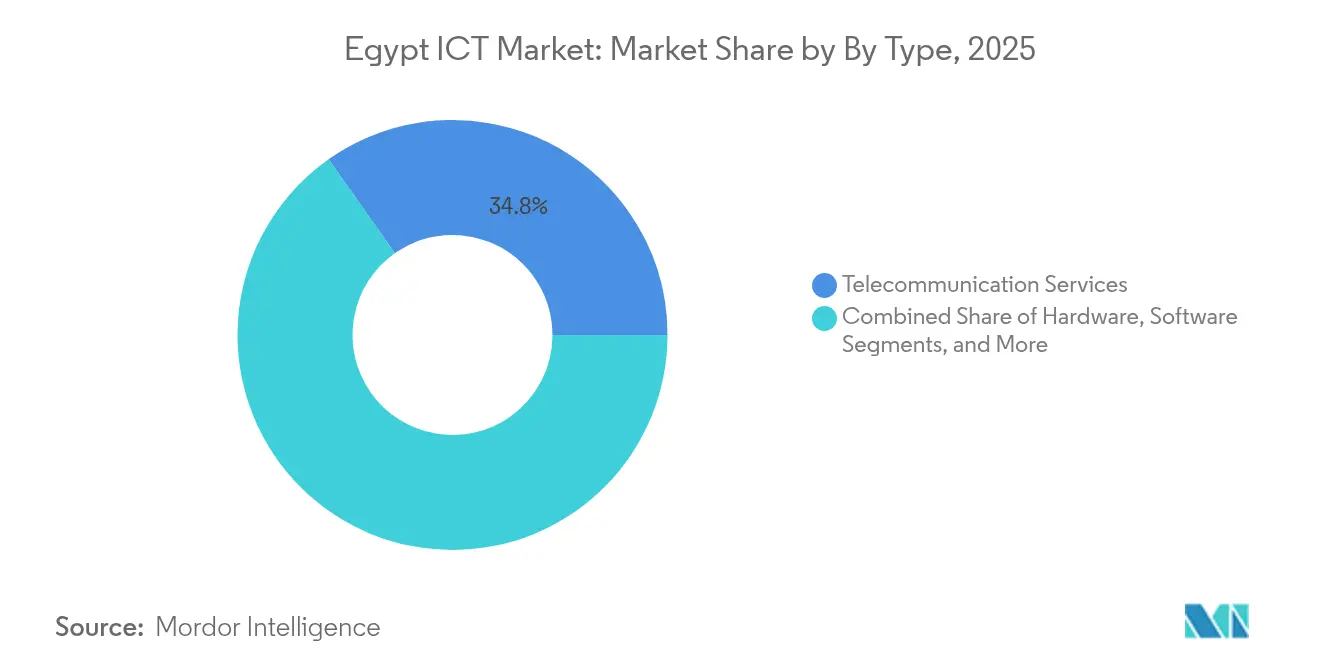

The Egypt ICT market size was valued at USD 23.60 billion in 2025 and estimated to grow from USD 27.69 billion in 2026 to reach USD 61.56 billion by 2031, at a CAGR of 17.33% during the forecast period (2026-2031). The rapid expansion stems from the government’s Digital Egypt program, large-scale data-center commitments from Gulf sovereign funds, and Egypt’s status as the primary landing point for 15 active undersea cables[1]Submarine Networks Team, “Egypt,” Submarine Networks, submarinenetworks.com . Telecommunications services currently hold 35.24% revenue share, while IT services lead growth at a 17.15% CAGR as enterprises accelerate cloud and AI adoption. Large enterprises account for 61.15% of spending, but SME demand is catching up thanks to subsidized financing and advisory schemes from the European Bank for Reconstruction and Development. Public-sector digitalization keeps government and public administration the top vertical at 24.81% share, yet BFSI is the fastest-growing vertical at 22.19% CAGR as fintech volumes scale.

Key Report Takeaways

- By type, telecommunications services led with 34.78% of Egypt's ICT market share in 2025, while IT services are advancing at a 17.47% CAGR through 2031.

- By enterprise size, large enterprises held 60.62% of the Egypt ICT market in 2025; SMEs record the highest projected CAGR at 15.78% to 2031.

- By industry vertical, the government and public sector captured 24.55% share of the Egyptian ICT market size in 2025; BFSI is projected to expand at a 21.84% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-wide cloud migration | +3.2% | Greater Cairo, New Administrative Capital | Medium term (2-4 years) |

| “Digital Egypt” citizen-service platform | +4.1% | Nationwide, rural expansion | Long term (≥4 years) |

| Gulf-funded hyperscale data-center build-out | +2.8% | Cairo, Suez Canal Economic Zone | Short term (≤2 years) |

| Undersea-cable landing ecosystem | +2.3% | Mediterranean and Red Sea coasts | Long term (≥4 years) |

| Egypt Post rural fintech roll-out | +1.9% | Remote governorates | Medium term (2-4 years) |

| Arabic generative-AI localization | +1.7% | Nationwide, regional export potential | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Government-wide Cloud Migration

A mandatory “cloud-first” decree requires every ministry to place new workloads on EG-CLOUD by 2026. Forty percent of core applications already run on the government platform, lowering agency IT operating costs by 35% and cutting service delivery times from hours to minutes[2]Ruba Obied, “The Egypt Government Cloud Strategy,” United Nations ESCWA, unescwa.org. Ministries report 60% faster release cycles, and the Ministry of Finance completed end-to-end budget automation on Oracle Hyperion, releasing real-time dashboards for parliamentary oversight. The policy spurs complementary investments in network security, identity management, and sovereign data zones, giving domestic service providers a stable pipeline through 2030.

“Digital Egypt” Citizen-Service Platform

The Digital Egypt super-app delivers 182 online public services to more than 9 million users and processed 750 million transactions in 2024, up 280% year on year. Its API-driven architecture links payment rails, telcos, and utilities, allowing citizens to settle taxes, traffic fines, and utility bills in minutes. Transaction success rates exceed 99.8%, while rural uptake has doubled since Egypt Post converted 200 branch offices into digital hubs. The platform’s data lake also underpins predictive analytics for subsidy targeting and pandemic response, reinforcing long-term adoption.

Gulf-Funded Hyperscale Data-Center Build-out

Abu Dhabi’s Khazna broke ground on a USD 250 million, 50 MW campus slated for 2026 full capacity, while Elsewedy Electric and Gulf Data Hub committed USD 2.1 billion to a 192 MW complex inside the Suez Canal Economic Zone. These projects exploit abundant renewable energy and proximity to cable landings, delivering a total cost of ownership up to 40% below comparable European sites. The resulting capacity attracts hyperscale cloud providers and AI workloads, anchoring Egypt ICT market growth.

Undersea-Cable Landing Ecosystem

Egypt hosts 15 active systems and five more under construction, including 2Africa and Medusa, giving operators redundant Mediterranean–Red Sea routes that cut round-trip latency by 25% relative to Gibraltar paths. Telecom Egypt’s WeConnect platform bundles 14 cables into a single commercial offer, enabling OTTs to buy capacity on demand. Cable density also encourages manufacturers to localize fiber-optic production, highlighted by Elsewedy’s USD 500 million plant west of Damietta.

Restraints Impact Analysis*

| Restraint | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Senior cyber-talent shortfall | -2.1% | Cairo, Alexandria | Medium term (2-4 years) |

| Foreign-exchange scarcity for hardware | -1.8% | Nationwide | Short term (≤2 years) |

| Fragmented SME tech demand beyond Cairo | -1.3% | Upper Egypt, remote governorates | Long term (≥4 years) |

| Legacy IT lock-in at state-owned companies | -0.9% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Senior Cyber-Talent Shortfall

Egypt’s cybersecurity workforce deficit stands at roughly 3,000 professionals, triple the available supply for senior roles, pushing vacancy periods to 8-12 months and inflating salaries by 30% annually. The National Cybersecurity Strategy aims to certify 1,000 specialists per year through the Cyber Talents program, yet demand outpaces output. Prolonged gaps expose enterprises to phishing incidents, which rose 49% in Cairo during 2024, prompting banks and telcos to outsource SOC operations to international vendors.

Foreign-Exchange Scarcity for Hardware

Three sequential devaluations since 2022 raised import prices 40-60%, delaying refresh cycles for PCs, servers, and network gear[3]Stasha Igrutinovic, “Digitalising SMEs on a Shoestring,” European Bank for Reconstruction and Development, ebrd.com . Seventy-eight percent of SMEs report postponing upgrades because banks cannot supply hard currency, forcing many to run unsupported operating systems. The electronics localization initiative, including Hisense’s USD 38 million appliance plant in the Suez Canal Economic Zone, covers only 15% of domestic demand, leaving the Egypt ICT market exposed to volatile FX conditions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Telecommunications Backbone Underpins Digital Expansion

Telecommunications services captured 34.78% of Egypt's ICT market share in 2025, reflecting continued capital expenditure on 5G licenses worth USD 675 million and fiber backhaul stretching to 40,000 towers. IT services are projected to grow the fastest at 17.47% CAGR, powered by public-sector outsourcing deals totaling USD 1.575 billion in FY 2022/23. Hardware demand cooled because of FX tightness, yet data-center server purchases surged as hyperscale builds progress. Software investment shifts toward SaaS and AI platforms aligned with the National AI Strategy 2025–2030, which targets 250 AI companies and 30,000 specialists.

In the forecast window, fixed-wireless access and private 5G slices will enable Industry 4.0 in the New Administrative Capital and Suez Canal Economic Zone, while local ISVs bundle Arabic NLP engines into e-commerce, edtech, and health-tech solutions. Regulatory frameworks such as the Personal Data Protection Law spur security spending, benefiting system integrators and MSSPs.

By Enterprise Size: Large Budgets Dominate but SME Upside Accelerates

Large enterprises commanded 60.62% of Egypt's ICT market in 2025, thanks to multi-year capex programs at telcos, banks, and energy majors. Vodafone and Orange alone earmarked more than USD 609 million and USD 284 million, respectively, for fiber-to-site projects through 2031. These organizations adopt zero-trust architectures, robotic process automation, and hybrid cloud, bolstering their resilience.

SMEs post a 15.78% CAGR outlook. The EBRD’s Shoestring pilots show 30% efficiency gains from barcode tracking and low-cost IoT sensors among furniture exporters. Government-sponsored “Digital Egypt Builders” offers EGP 2 million soft loans and tech bootcamps, aiming to cover 100,000 SMEs by 2026. Fintech operators such as Fawry Business provide cloud bookkeeping and e-invoice APIs that lower adoption barriers.

By Industry Vertical: Public Sector Leads While Banks Sprint Ahead

Government and public administration accounted for 24.55% of spending in 2025 as 63 state-owned companies pursued process automation and e-procurement frameworks, processing EGP 2.5 trillion in electronic payments over eleven months. BFSI, though smaller, registers a 21.84% CAGR. Real-time payment rails, Egypt’s first digital bank, and AI-powered call-center agents elevate digital wallet penetration beyond 48 million active accounts.

Healthcare is next in line, with Vodafone Business supporting 314 connected hospitals and 6 million patients through telehealth dashboards. Manufacturing leverages subsidized automation audits under the Smart Industry Readiness Index, encouraging MES deployments among cement and textiles firms.

Geography Analysis

Cairo and the emerging New Administrative Capital concentrate roughly 64.30% of Egypt ICT market revenues, housing head offices, hyperscale data centers, and 5G densification projects. The Smart Capital initiative embeds IoT sensors in traffic, lighting, and utility grids, fostering data-driven municipal services.

The Suez Canal Economic Zone is fast becoming a secondary hub as land prices and renewable-energy availability attract Gulf-backed data centers, electronics OEMs such as Hisense, and submarine cable factories, cementing Egypt’s east-west connectivity role.

Upper Egypt and the Delta witness accelerated rural digitization under the “Decent Life” fiber program, plus outsourcing delivery centers in Assiut, where wages are 40% below Cairo levels, yet talent retention is high.

Competitive Landscape

Telecom Egypt monopolizes fixed infrastructure and owns WeConnect, granting it strategic control over cable landings. Mobile market shares are fragmented with Vodafone at 44%, Orange at 33%, and e& Egypt at 22%, fostering competitive pricing and aggressive 5G rollouts.

Hyperscale data centers bring new entrants: Khazna, Gulf Data Hub, and Raya compete for cloud tenants while partnering with local utilities for sustainable power. Their combined pipeline exceeds 1 GW, signaling a structural shift toward hosted services.

Enterprise IT is dominated by global vendors—IBM, Microsoft, Cisco—leveraging seventy-year local footprints and joint innovation centers. Domestic champions like Fawry and e-Finance capitalize on regulatory know-how and nationwide agent networks, enabling fintech services to 50 million users.

Egypt ICT Industry Leaders

Accenture Plc

SAP SE

Dell Technologies, Inc.

Telecom Egypt S.A.E.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: President El-Sisi unveiled the “Digilians” skills initiative to train 5,000 learners yearly in AI, coding, and cybersecurity.

- undefinedFeb 2025: Telecom Egypt and Orange Egypt signed EGP 15 billion connectivity deals covering nationwide fiber-to-site for 5G.

- February 2025: Egypt Post partnered with Visa to widen rural digital payment acceptance.

- January 2025: Fawry introduced “Fawry Business,” expanding from consumer payments into enterprise SaaS.

- January 2025: ITIDA and Konecta agreed to a USD 100 million Gen-AI center in New Cairo.

Egypt ICT Market Report Scope

Information and communication technologies (ICT) encompass a wide array of communication technologies, including the internet, computers, wireless networks, software, cell phones, videoconferencing, middleware, social networking, and various media applications. These technologies empower users to store, access, transmit, retrieve, and manipulate information digitally.

The Egyptian ICT market is segmented by type (hardware, software, IT services, and telecommunication services), size of enterprise (small and medium enterprises and large enterprises), and industry vertical (BFSI, IT and telecom, government, retail and e-commerce, manufacturing, energy and utilities, and other industry verticals). The market sizes and forecasts are provided in value terms (USD) for all the above segments.

By Type

| Hardware | Computer Hardwar |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

By End-user Enterprise Size

| Large Enterprises |

| SMEs |

By End-user Industry Vertical

| BFSI |

| Government and Public Administration |

| Retail, E-commerce and Logisitcs |

| Manufacturing and Industry 4.0 |

| Halthcare and Life Sciences |

| Gaming and Esports |

| Oil and Gas (Up-, Mid-, Down-stream) |

| Energy and Utilities |

| Other Verticals |

| By Type | Hardware | Computer Hardwar |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By End-user Enterprise Size | Large Enterprises | |

| SMEs | ||

| By End-user Industry Vertical | BFSI | |

| Government and Public Administration | ||

| Retail, E-commerce and Logisitcs | ||

| Manufacturing and Industry 4.0 | ||

| Halthcare and Life Sciences | ||

| Gaming and Esports | ||

| Oil and Gas (Up-, Mid-, Down-stream) | ||

| Energy and Utilities | ||

| Other Verticals | ||

Key Questions Answered in the Report

How large will Egypt’s ICT spending be by 2031?

The Egypt ICT market size is projected to reach USD 61.56 billion by 2031, up from USD 27.69 billion in 2026.

Which segment is expanding the quickest?

IT services is forecast to grow at a 17.47% CAGR, the highest among all type segments.

Why is cloud deployment gaining most traction?

A mandatory government cloud-first policy and hyperscale data-center investments give cloud models a cost and agility advantage, driving an 18.19% CAGR.

What is fueling BFSI technology demand?

Real-time payment networks, Egypt’s first digital bank, and AI-driven customer service tools are boosting BFSI ICT outlays, resulting in a 21.84% CAGR.

Which geographic clusters attract the bulk of data-center investment?

Greater Cairo and the Suez Canal Economic Zone host most hyperscale projects due to fiber proximity and renewable power availability.

Page last updated on: