Ivory Coast Distribution Boards Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

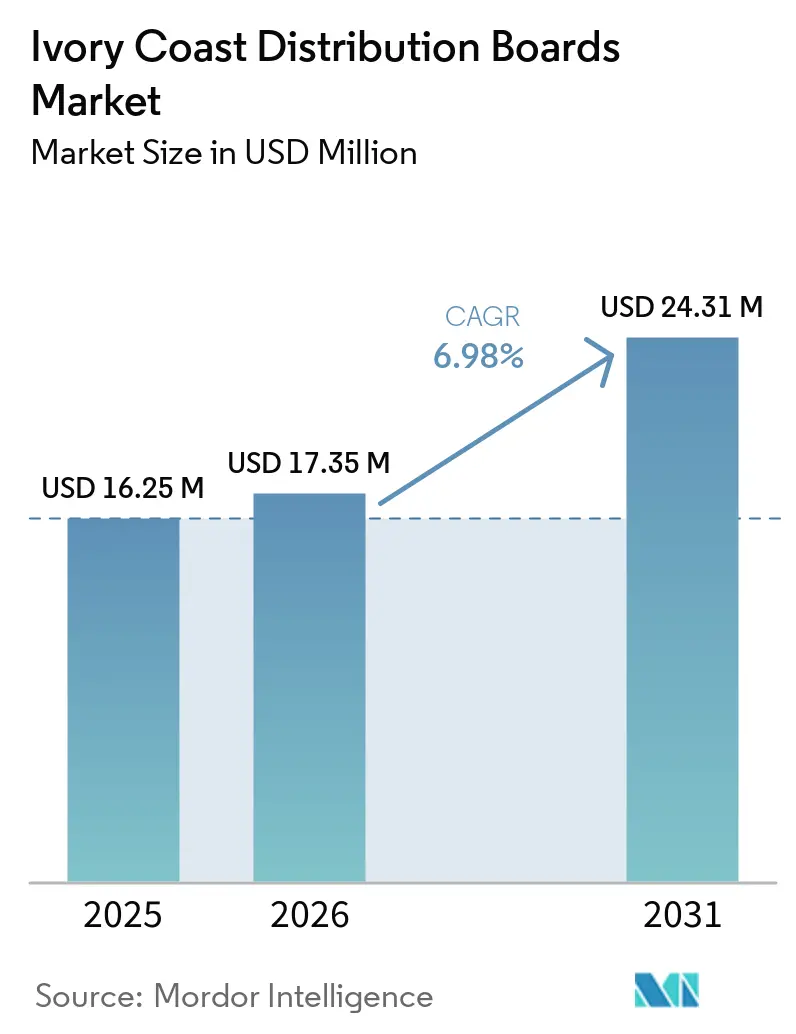

| Base Year Market Size (2025) | USD 16.25 Million |

| Market Size (2026) | USD 17.35 Million |

| Market Size (2031) | USD 24.31 Million |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ivory Coast Distribution Boards Market Analysis by Mordor Intelligence

The Ivory Coast Distribution Boards Market size is projected to be USD 16.25 million in 2025, USD 17.35 million in 2026, and reach USD 24.31 million by 2031, growing at a CAGR of 6.98% from 2026 to 2031. The Ivory Coast distribution boards (DB) market is being supported by a clear shift from first-time electrification toward network reinforcement, reliability improvement, and replacement demand as the national power system moves closer to full coverage. Electricity demand in Côte d'Ivoire grows at an average of 8% each year, which keeps pressure on feeders, substations, and end-use distribution equipment even after connection growth begins to mature.[1]République de Côte d’Ivoire, “Electricity Demand Growth,” Portail de l’Économie Ivoirienne, economie-ivoirienne.ci Large public power plans, industrial buildouts, and new solar-linked grid interfaces are widening the number of installation points that require distribution boards, from factory entry points to local distribution nodes. The Ivory Coast distribution boards (DB) market also benefits from tighter technical compliance in regulated channels, which supports certified suppliers and limits the room for uncertified low-cost products in formal procurement. At the same time, import dependence, cost pressure on smart products, and grid-connection approval complexity continue to slow some purchase decisions and push part of the upgrade cycle into later years.

Key Report Takeaways

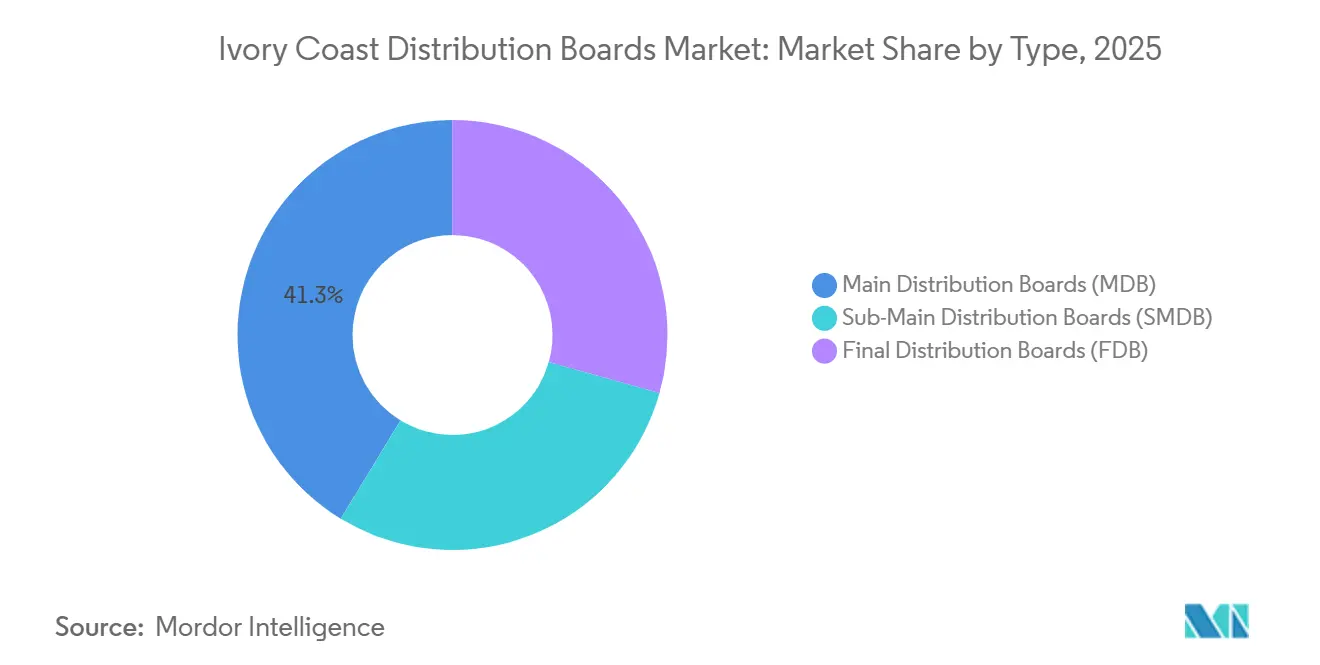

- By type, Main Distribution Boards held 41.3% of revenue in 2025, while Final Distribution Boards are projected to grow at an 8.8% CAGR through 2031.

- By technology, Conventional Boards accounted for 74.2% share of the Ivory Coast distribution boards (DB) market size in 2025, while Smart or Internet of Things (IoT)-enabled Boards are forecast to expand at an 11.2% CAGR through 2031.

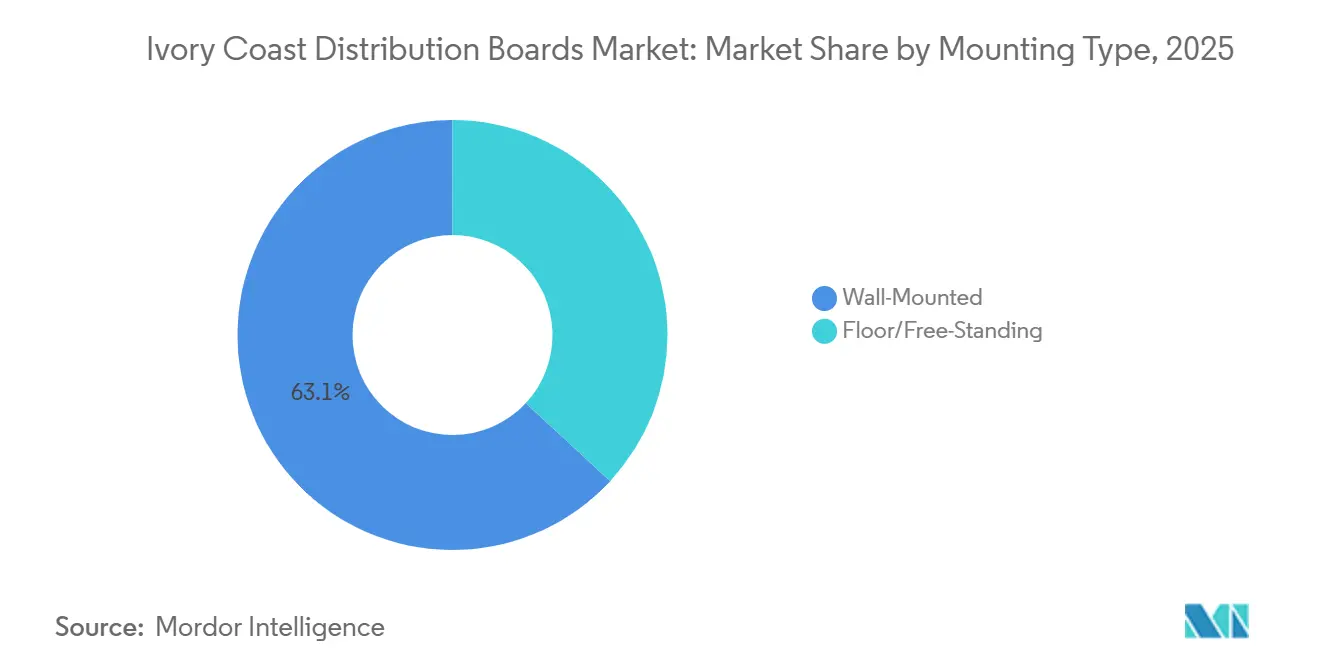

- By mounting type, Wall-Mounted Boards held 63.1% in 2025, while Floor or Free-Standing boards are expected to grow at an 8.1% CAGR through 2031.

- By end-user, Commercial held 36.3% in 2025, while Residential is projected to advance at a 9.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Ivory Coast Distribution Boards Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction-Led Commercial And Residential Buildout | +1.8% | National, with early gains in Abidjan, Bouaké, Yamoussoukro | Short term (≤ 2 years) |

| Industrial And Commercial Electrification Growth | +1.4% | National, concentrated in PEIA Abidjan, Ferkessédougou, San Pedro | Medium term (2-4 years) |

| Grid Strengthening And Rural And Urban Network Expansion | +1.2% | National, rural catchment zones and secondary cities | Medium term (2-4 years) |

| Smart Metering And Digital Power Monitoring | +0.7% | Concentrated in Abidjan urban core, spill-over to Commercial and Industrial (C&I) hubs | Long term (≥ 4 years) |

| Eligible-Customer Open Access For >10 GWh Users | +0.4% | National, early gains for high-consumption industrial users | Long term (≥ 4 years) |

| C&I Solar Retrofits And Self-Generation Integration | +0.6% | National, C&I hubs in Abidjan and agro-industrial northern regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Construction-Led Commercial and Residential Buildout

Construction activity is creating layered panel demand because the same project often requires final boards, sub-main boards, and main boards at different electrical points. In the Ivory Coast distribution boards (DB) market, that pattern shortens the distance between civil progress and electrical procurement because developers increasingly specify complete board packages early in the build cycle. Affordable housing, peri-urban densification, and mixed-use development are also favoring standard layouts that can be repeated with limited redesign from one site to the next. This supports faster ordering for wall-mounted and pre-assembled products, especially in residential blocks and smaller commercial buildings. It also improves the position of suppliers that can deliver ready-configured systems rather than only loose components. The result is a market in which installation volume is rising not only with new floor space, but also with the number of connected units and feeder points inside each development.

Industrial and Commercial Electrification Growth

Industrial electrification is adding higher-value demand because factories, logistics platforms, and process facilities require larger ratings and more complex distribution architectures. The Ivory Coast distribution boards (DB) market is seeing this effect most clearly around structured industrial platforms, where each tenant needs a dedicated intake and internal distribution structure. The PEIA industrial park, which began operations in January 2024 with a total investment of USD 316 million, brings together agro-processing, construction materials, pharmaceuticals, and logistics in one operating cluster. That raises demand for main distribution board (MDB) and sub-main distribution board (SMDB) systems at factory entrances, internal process zones, and service buildings. Electricity demand growth of 8% a year also points to sustained power intensity from productive users, which keeps the case strong for added distribution capacity and recurring replacements. Industrial and commercial users, therefore, remain important for average selling value even when residential units account for more physical board counts.

Grid Strengthening and Rural and Urban Network Expansion

Grid reinforcement is widening the number of network points that need new or upgraded distribution boards, especially where urban load growth has moved faster than earlier design assumptions. The Ivory Coast distribution boards (DB) market benefits from this because each reinforcement step, from secondary distribution nodes to public service connections, creates a separate installation event rather than a single system purchase. The Millennium Challenge Corporation (MCC) compact supports automation, smart grid, rural extension, and off-grid electrification planning, which will shape procurement requirements for future network nodes and local service points.[2]Millennium Challenge Corporation, “Côte d’Ivoire Regional Energy Compact,” MCC, mcc.gov Rural extension also changes the demand mix because community transformer points and simplified local networks typically require lower-rated but more numerous board installations. In cities, reinforcement work tends to favor higher-rated assemblies and more structured protection schemes due to denser commercial load. This dual pattern allows the market to grow in both unit volume and technical depth at the same time.

Smart Metering and Digital Power Monitoring

Digital metering is making board intelligence more relevant because the value of feeder-level visibility rises once endpoints are already digitized. The Ivory Coast distribution boards (DB) market is now seeing a stronger case for smart-capable boards in utility, industrial, and premium commercial settings where load data can improve maintenance and uptime. Compagnie Ivoirienne d'Électricité (CIE) stated at SIREXE 2024 that 75% of its clients already use smart meters, with another 10% on distance metering and the remainder moving through active migration. That installed base gives smart boards a more practical role because they can connect distribution nodes to an already digitized metering environment. The International Finance Corporation (IFC)-backed Scaling Solar award for 80 MW of capacity in August 2025, with construction beginning by March 2026, also supports the need for smarter grid-interface equipment at intermittent generation points. Smart products will still remain concentrated in regulated and higher-value projects because the upfront cost premium is material in price-sensitive segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import Dependence For Critical Electrical Inputs | -1.1% | National, highest exposure in large public-sector infrastructure procurements | Short term (≤ 2 years) |

| High Lifecycle And Maintenance Costs | -0.8% | National, most acute in rural and secondary urban installations | Medium term (2-4 years) |

| Grid-Connection Code And Certification Burden | -0.5% | National, concentrated in HV and smart-board installations | Medium term (2-4 years) |

| Limited Local Smart-Board Integration Depth | -0.4% | National, concentrated in Abidjan and secondary urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Import Dependence For Critical Electrical Inputs

Import reliance remains a direct constraint because most advanced board components still come from outside the country. In the Ivory Coast distribution boards (DB) market, this creates exposure to shipping delays, supplier lead times, and exchange-rate pressure on items sourced in USD-heavy trade channels. The problem is more visible in formal infrastructure projects because procurement windows are fixed, while delivery schedules for key electrical components can move. Trade policy may reduce some cost pressure over time, but specialized assemblies and certified switchgear are less likely to see near-term relief than simpler tariff lines. Local activity is still concentrated in enclosure customization and basic value addition rather than deeper engineering or testing capability. This leaves public and industrial buyers vulnerable to repeat procurement bottlenecks whenever demand spikes or project timelines tighten.

High Lifecycle And Maintenance Costs

Operating conditions also hold back upgrades because lifecycle cost matters as much as purchase cost for many buyers. The Ivory Coast distribution boards (DB) market faces this issue in coastal humidity zones, dusty inland areas, and overloaded networks where component wear can rise faster than planned maintenance cycles. Smaller buyers often respond by choosing simpler conventional boards that are cheaper to replace even if they offer fewer monitoring benefits. That cost logic slows the move toward premium smart products outside top-tier commercial and utility installations. Service coverage and spare-part access remain uneven beyond Abidjan, which reduces confidence in higher-specification systems that depend on stronger after-sales support. The result is a market where buyers may recognize the technical value of smart monitoring, yet still delay upgrades because the full ownership burden remains difficult to absorb.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: MDB Anchors Revenue As Final Boards Drive Volume

Main Distribution Boards held 41.3% of the Ivory Coast distribution boards (DB) market share in 2025, which reflected their role as the first organized intake point in commercial buildings, industrial sites, and utility-linked installations. That share is tied more to system importance and rating intensity than to unit count, because one MDB often anchors a much larger electrical architecture beneath it. In practice, this keeps MDB demand closely linked to projects that require clear load segregation, protection coordination, and structured downstream routing. Formal procurement also tends to favor established specifications in this category, which supports the position of larger global brands in higher-value projects. As a result, MDBs remain the value anchor of the portfolio even when other board types sell in larger physical numbers.

Sub-Main Distribution Boards continue to gain relevance as projects become more layered and more vertically organized inside the same site. Multi-tenant commercial buildings, mixed-use blocks, and industrial plots need this intermediate layer to separate loads by floor, function, or process line. That makes SMDBs important in growing urban clusters where the electrical design is more segmented than in detached or low-rise assets. Final Distribution Boards, however, are forecast to grow at an 8.8% CAGR through 2031, which shows how much the expansion story is now being shaped by connection count rather than only by large-capacity projects. Affordable housing and small-business buildouts support that pattern because each new unit usually requires its own final board, even when its load remains modest. The fastest growth, therefore, sits at the lower end of the system hierarchy, while the highest single-project value still sits at the top.

Main boards also benefit from the way utilities and industrial operators handle compliance and reliability. Where uptime risk is high, buyers are less willing to compromise on protection quality, enclosure strength, and certification. That purchasing behavior keeps the type segment more resilient than commodity categories during periods of pricing pressure. It also helps explain why value growth does not always track volume growth one for one. In the Ivory Coast distribution boards (DB) market, the type mix therefore shows a clear split between revenue concentration in upstream boards and installation momentum in downstream boards.

By Technology: Conventional Boards Hold Share While Smart Boards Gain Ground In Regulated Use Cases

Conventional Boards accounted for 74.2% of the Ivory Coast distribution boards (DB) market size in 2025, which confirms that price, contractor familiarity, and straightforward installation still shape most purchasing decisions. This remains the default choice for residential projects, smaller commercial sites, and many routine replacement jobs where advanced monitoring is not essential. Conventional products also fit the country’s current service environment better because they require less specialized commissioning and less digital support after installation. That advantage is especially relevant outside major urban centers where maintenance networks are thinner. For these reasons, conventional boards will continue to hold the larger share through the forecast period.

Smart or IoT-enabled Boards are still the faster-moving technology layer and are projected to grow at 11.2% CAGR through 2031. Their adoption is strongest where users can measure the return from better visibility, remote alerts, and better load management. Utility-grade projects, industrial parks, premium offices, and renewable energy interfaces are the main early-use cases because downtime and power quality matter more in those settings. The growth path is also supported by the country’s strong smart meter base, which makes digital integration at the distribution level more practical than it would be in a fully analog environment. That does not remove the cost barrier, but it does make the functionality easier to justify in regulated and high-load applications.

The technology split also carries an important pricing consequence. Conventional boards will drive a large share of incremental units, yet smart boards will influence product specification, supplier positioning, and margin structure in the more formal end of the market. This means the technology transition will not be uniform across customer groups or geographies. In the Ivory Coast distribution boards (DB) market, technology adoption is therefore less about a full shift away from conventional products and more about selective digital layering where the operational case is already visible. That pattern will keep the technology mix uneven through 2031, even as digital features become more available.

By Mounting Type: Wall-Mounted Boards Set The Baseline While Floor-Standing Units Rise With Industrial Load

Wall-Mounted boards represented 63.1% of the market in 2025, reflecting their fit with the most common installation profiles in homes, small commercial units, and light industrial settings. Their share is supported by ease of placement, lower space requirements, and simpler installation in standard building layouts. This makes them the practical default in high-volume categories where project speed matters more than complex internal arrangement. The segment also benefits from the large number of smaller connections being added or upgraded in residential and peri-urban settings. That broad compatibility keeps wall-mounted units central to the market baseline.

Floor or Free-Standing boards are projected to grow at 8.1% CAGR through 2031 because industrial and utility installations require larger ratings, more circuit density, and greater room for modular configuration. These products are better suited to facilities that need higher ampacity, more advanced segregation, and a more elaborate internal topology. Industrial parks and process industries are the clearest demand drivers because they need boards that can handle multiple feeders and future load expansion. This is one of the few areas where local value addition could deepen if domestic operators invest in fabrication, busbar work, and functional testing capability. For now, that gap still favors imported or internationally specified systems in more complex projects.

The mounting split also shows how end-user mix shapes product design choices. Wall-mounted units align with standardized, repeatable projects, while floor-standing systems align with bespoke engineering and heavier-duty applications. That difference affects not only the selling price, but also leads times, service requirements, and the channel through which products are sold. In the Ivory Coast distribution boards (DB) market, mounting type therefore acts as a useful proxy for the divide between mass installation demand and specification-driven procurement. It also shows where domestic assembly could expand if the capability improves over time.

By End-User: Commercial Leads Current Value While Residential Drives The Fastest Expansion

Commercial held 36.3% of revenue in 2025, which reflected the concentration of offices, retail facilities, hospitality assets, and public buildings in the formal construction pipeline. These sites typically require an organized hierarchy of MDB and SMDB installations, which raises average project value relative to smaller residential jobs. Commercial demand also tends to move through clearer specifications and formal contractor channels, which supports branded products and more structured procurement. That makes the segment important for both revenue quality and supplier visibility in the country. It remains the strongest current value pool even as the broader installed base continues to widen.

Residential is projected to grow at 9.0% CAGR through 2031, making it the fastest-growing end-user category in the Ivory Coast distribution boards (DB) market. The main driver is the rising number of connections and dwelling units rather than the high unit value per installation. Affordable housing, peri-urban densification, and the continuing push to improve access and supply quality all support final board demand in this segment. That creates a market where volume expansion can remain strong even when individual system specifications stay relatively simple. Residential growth is therefore central to unit demand, installer activity, and repeat replacement needs.

Industrial users remain highly important because they purchase larger and more complex board systems, even if they do not match residential unit counts. Utilities also matter because digital network management and metering compliance make them likely early adopters of smart-enabled boards in formal projects. This means no single end-user group defines the whole opportunity. Instead, value leadership and volume leadership sit in different parts of the market. The Ivory Coast distribution boards (DB) market will therefore continue to rely on commercial and industrial projects for value while residential demand provides the strongest growth momentum.

Geography Analysis

Greater Abidjan remains the core demand center because it combines the country’s main port, its largest concentration of office space, its densest industrial base, and a major share of new formal construction. The Ivory Coast distribution boards (DB) market is most concentrated in this urban zone because higher building density and larger connected loads create more frequent demand for MDB and SMDB systems. Abidjan also carries a high share of replacement and reinforcement demand, not only new installation demand, because mature urban networks require upgrades as loads rise. This keeps the city important for both premium project supply and routine panel renewal. The urban mix also favors suppliers that can serve contractors quickly with both standardized products and customized assemblies.

Commercial corridors and industrial districts inside Abidjan shape the technical mix of orders. Office, hospitality, retail, and public administration sites usually need more layered distribution structures than smaller secondary-city assets. Industrial clusters add further demand for larger enclosures, higher ratings, and more detailed internal separation. The city also remains the main entry point for imported electrical products, which strengthens its role in distribution, stocking, and after-sales support. That channel advantage matters because faster delivery can influence specification choice when project timelines are tight.

Secondary cities are gaining weight as new power and industrial investments spread beyond the capital. Bouaké, San Pedro, Yamoussoukro, Ferkessédougou, and other emerging nodes are drawing attention because industrial parks, logistics assets, and public infrastructure are broadening the geography of formal electrical procurement. The PEIA development model supports this shift by creating structured industrial locations outside a single urban core. These locations are important because they require upstream distribution architecture as well as internal panelization for tenant operations. As this network of secondary demand centers expands, the country’s procurement map becomes less dependent on a single metropolitan area.

Rural and peri-urban zones form a different demand profile. Here, board requirements are more likely to involve lower ampacity, simpler single-phase layouts, and outdoor-rated enclosures suited to local service conditions. The MCC compact is important in this context because it supports the preparation of master plans for automation, smart grids, rural extension, and off-grid electrification, all of which will influence future procurement patterns outside the largest cities. The Ivory Coast distribution boards (DB) market, therefore, has a clear geographic split between high-value urban demand and broader but simpler rural and peri-urban installations.

Competitive Landscape

The Ivory Coast distribution boards (DB) market has a dual structure in which global brands serve the more formal and higher-specification end of demand, while a wider local tier competes on responsiveness, customization, and price. Schneider Electric, Legrand, ABB, Siemens, and Hager remain visible in premium projects and in supply relationships linked to established electrical distributors. Domestic names such as SOCOMELEC IVOIRE, SERELEC, SOGELEC, PIGELEC, and SIMELEC add competitive pressure by working closer to customers and by adapting enclosure formats to local needs. This creates a market that is neither tightly consolidated nor entirely commoditized. Premium specification, channel reach, and certification matter, but so do service speed and on-the-ground assembly support.

Compliance remains one of the clearest advantages for larger international suppliers. Grid-connected procurement works under a regulatory structure that places weight on approved technical standards and metering compatibility, which naturally favors suppliers with stronger certification depth. That makes it harder for uncertified imports to compete in regulated projects even when their upfront pricing is lower. It also helps explain why large brands remain strongest in utilities, industrial projects, and other high-specification applications. In the Ivory Coast distribution boards (DB) market, compliance does not remove competition, but it does shape where that competition becomes most intense.

Strategic moves by leading companies show a clear effort to defend share across multiple price bands. Schneider Electric introduced the GoPact range in West Africa to address mid-market demand and counter low-cost imports more directly. The company also launched the MasterPacT MTZ Active circuit breaker in August 2025 for higher-end industrial and utility use cases where safety, digitization, and connectivity matter more. In August 2025, it also introduced the DBSeT all-in-one digital panel board, which signaled growing interest in smarter downstream board formats rather than only upstream switchgear. These moves suggest that leading suppliers are no longer relying only on premium positioning, and are instead building a fuller ladder from cost-conscious buyers to digitally advanced users.

White-space opportunities still exist for domestic operators that can move beyond basic enclosure work. One opening sits in locally assembled smart boards for industrial tenants that need mid-range current ratings with stronger monitoring capability. Another sits in pre-wired final board sub-assemblies for housing developers that want faster electrical completion without deep in-house engineering. The Ivory Coast distribution boards (DB) market is therefore likely to keep a mixed competitive profile, with global brands retaining strength in certified systems while local firms expand around customization, assembly, and project responsiveness.

Ivory Coast Distribution Boards Industry Leaders

Schneider Electric SE

Legrand SA

ABB Ltd.

Hager Group

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SUCAF-CI expanded its on-site solar capacity toward 8 MWp at its Niakara facility, targeting more than 25% solar contribution to its energy mix, reducing grid draw and implying reconfiguration of the facility's existing distribution board architecture for hybrid grid-solar supply.

- August 2025: IFC and the Government of Côte d'Ivoire announced Infinity Power Holding as the winning bidder for 2 grid-connected solar PV plants totalling 80 MW at record-low tariffs of EUR 0.032-0.033 per kWh under the World Bank Scaling Solar programme, construction began by March 2026 with completion targeted by end-2026.

Ivory Coast Distribution Boards Market Report Scope

A distribution board (DB), also referred to as an electrical panel, breaker box, or fuse box, serves as the central component of an electrical system. It receives the main power supply from the grid and distributes it into smaller subsidiary circuits, ensuring safe and efficient power delivery to lights, outlets, and appliances within a building.

The Ivory Coast Distribution Boards Market is segmented into type, technology, mounting type, and end-user. By type, the market is segmented into main distribution boards (MDB), sub-main distribution boards (SMDB), and final distribution boards (FDB). By technology, the market is segmented into conventional boards and smart/IoT-enabled boards. By mounting type, the market is segmented into wall-mounted and floor/free-standing systems. By end-user, the market is segmented into utilities, industrial, commercial, and residential sectors. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Main Distribution Boards (MDB) |

| Sub-Main Distribution Boards (SMDB) |

| Final Distribution Boards (FDB) |

| Conventional Boards |

| Smart/IoT-enabled Boards |

| Wall-Mounted |

| Floor/Free-Standing |

| Utilities |

| Industrial |

| Commercial |

| Residential |

| By Type | Main Distribution Boards (MDB) |

| Sub-Main Distribution Boards (SMDB) | |

| Final Distribution Boards (FDB) | |

| By Technology | Conventional Boards |

| Smart/IoT-enabled Boards | |

| By Mounting Type | Wall-Mounted |

| Floor/Free-Standing | |

| By End-User | Utilities |

| Industrial | |

| Commercial | |

| Residential |

Key Questions Answered in the Report

What is the current size of the Ivory Coast distribution boards (DB) market?

The Ivory Coast distribution boards (DB) market stands at USD 17.35 million in 2026 and is projected to reach USD 24.31 million by 2031 at a 6.98% CAGR.

Which product type leads demand in Côte d'Ivoire?

Main Distribution Boards led revenue with 41.3% share in 2025 because they remain the main intake point for commercial, industrial, and utility-linked electrical systems.

Which technology segment is growing the fastest?

Smart or IoT-enabled Boards are projected to grow at 11.2% CAGR through 2031, supported by rising smart meter use and greater digital monitoring needs.

Why is residential demand rising so quickly?

Residential is expected to grow at 9.0% CAGR through 2031 because affordable housing delivery, peri-urban expansion, and continuing connection growth are increasing unit-level installations.

Why does Abidjan matter so much for suppliers?

Greater Abidjan remains the largest demand center because it combines port access, office development, industrial density, and a large share of replacement and reinforcement work.

What is the main risk for manufacturers and distributors?

Import dependence remains the clearest near-term risk because advanced components still rely heavily on overseas supply, which affects cost, lead time, and project scheduling.

Page last updated on: