Senegal Distribution Boards Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

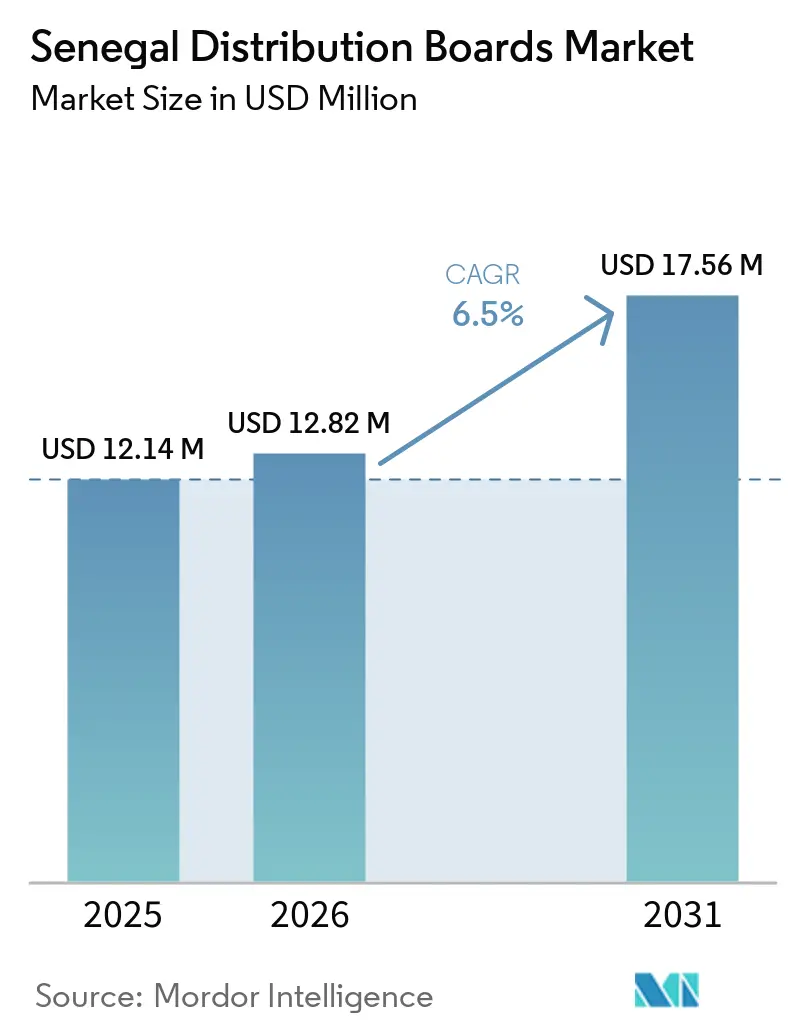

| Base Year Market Size (2025) | USD 12.14 Million |

| Market Size (2026) | USD 12.82 Million |

| Market Size (2031) | USD 17.56 Million |

| Growth Rate (2026 - 2031) | 6.50% CAGR |

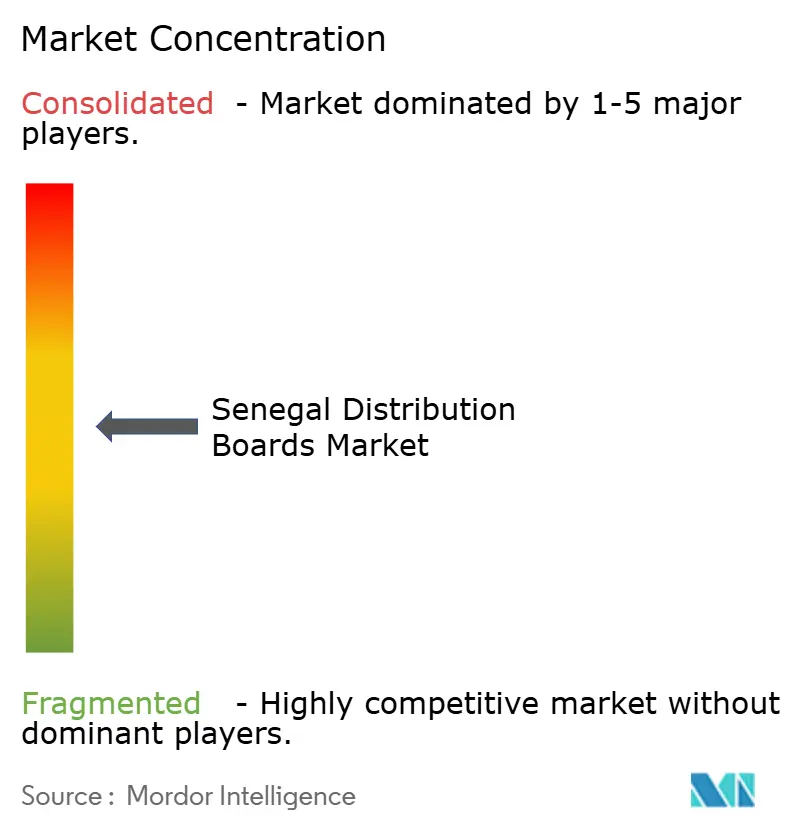

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Senegal Distribution Boards Market Analysis by Mordor Intelligence

The Senegal Distribution Boards Market size is projected to expand from USD 12.14 million in 2025 and USD 12.82 million in 2026 to USD 17.56 million by 2031, registering a CAGR of 6.5% between 2026 and 2031. The Senegal distribution boards market is supported by SENELEC's 46,713 km distribution network, which includes 21,505 km of medium-voltage lines, 25,208 km of low-voltage lines, and 12,401 HTA/BT substations in 2025, creating a broad installed base for recurring replacement and upgrade demand.[1]Source: SENELEC, “Distribution Network Statistics 2025,” SENELEC, senelec.sn The Senegal distribution boards market is also being lifted by the World Bank-backed PADAES program, which targets 4,000 km of new and rehabilitated power lines and 200,000 household connections, and by VINCI Energies' contract with SENELEC to install 1,350 km of high-voltage lines and 8 very-high-voltage substations.[2]Source: World Bank, “Senegal Closing on Universal Electricity Access,” World Bank, worldbank.org Commercial construction in Dakar and Diamniadio, industrial electrification in special economic zones, and new renewable and storage projects are widening the range of board specifications required across the country.[3]Source: Eiffage, “Production and Storage in Senegal,” Eiffage, app.eiffage.com The market is also shaped by import dependence, corrosion-related specification upgrades in coastal zones, and the growing need for monitoring-ready boards as utilities modernize grid management systems.[4]Source: CVCI, “Structurer et Déployer un Appareillage Électrique Courant Fort Conforme et Durable pour Projets Tertiaires et Industriels au Sénégal et en Afrique de l'Ouest,” CVCI, cvci.fr The Senegal distribution boards market remains moderately fragmented because global Original Equipment Manufacturers (OEMs) compete on specification and approvals, while local assemblers serve cost-sensitive orders and EPC-led packages.

Key Report Takeaways

- By type, final distribution boards held 46.8% of the Senegal distribution boards market share in 2025, while sub-main distribution boards are projected to grow at 7.9% CAGR through 2031.

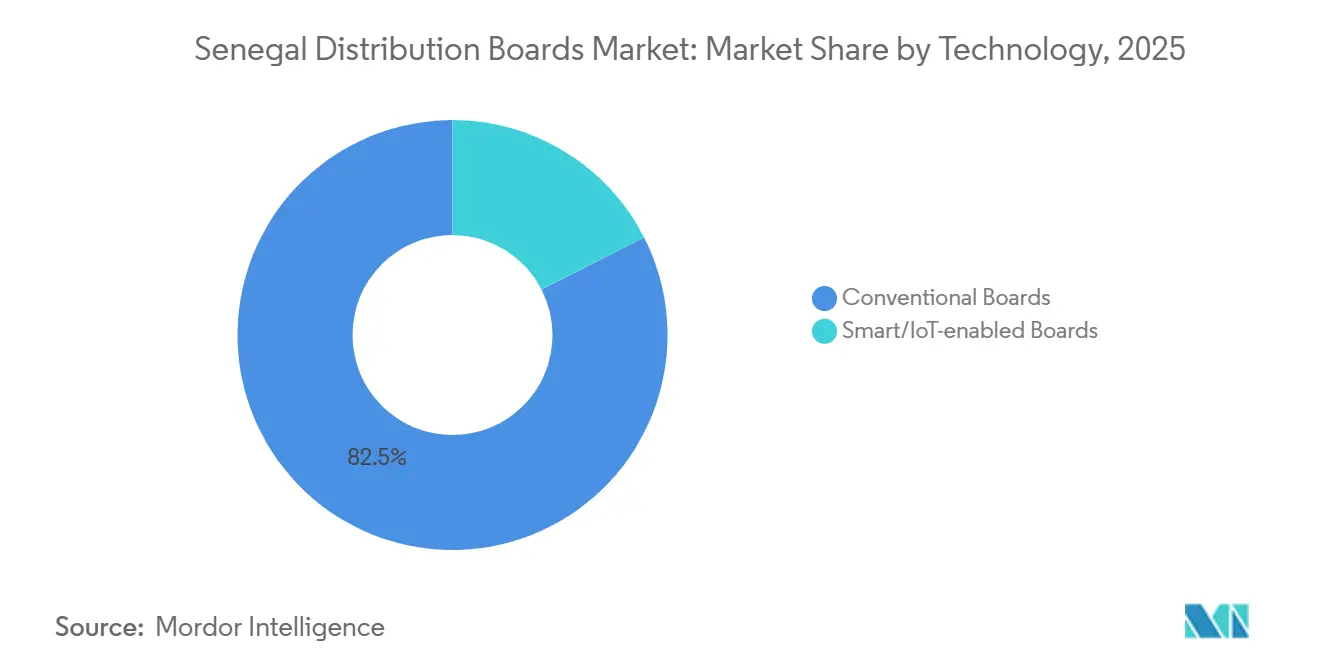

- By technology, conventional boards held 82.5% share in 2025, while smart and IoT-enabled boards are projected to expand at 11.4% CAGR through 2031.

- By mounting type, wall-mounted panels captured 71.2% share in 2025, while floor and free-standing boards are forecast to grow at 8.1% CAGR through 2031.

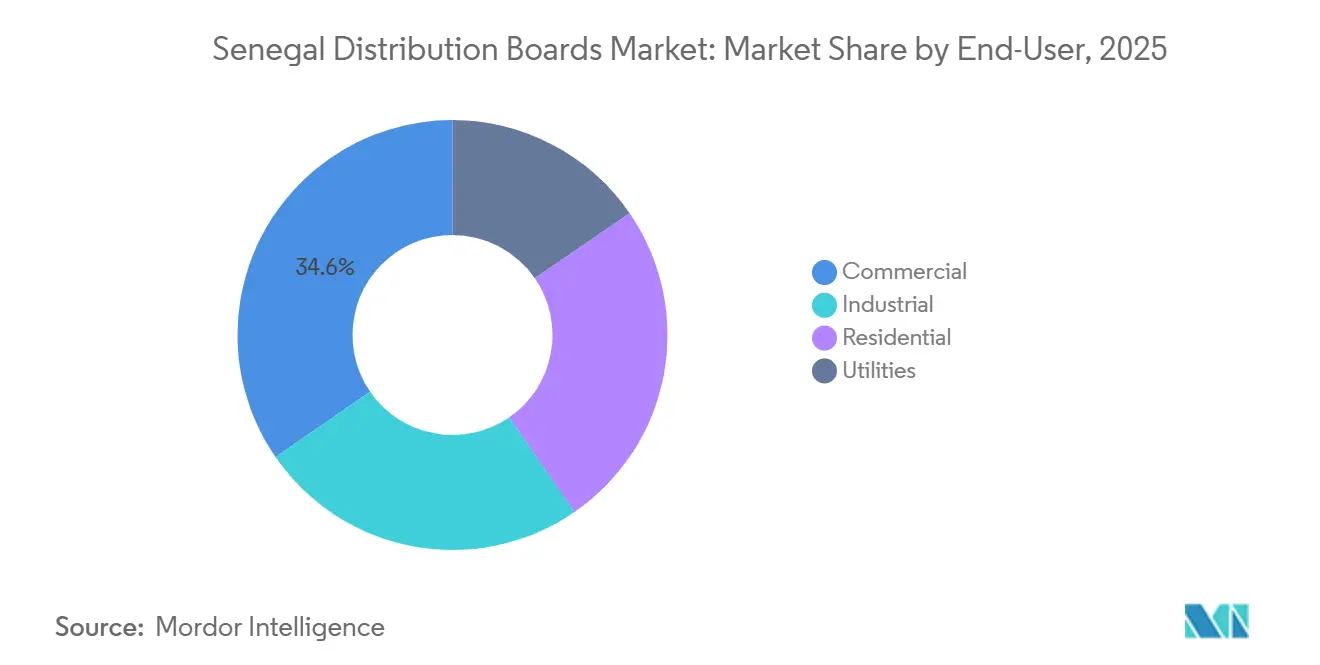

- By end-user, commercial accounted for 34.6% share of the Senegal distribution boards market size in 2025, while utilities are projected to grow at 8.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Senegal Distribution Boards Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Building and mixed-use project pipeline | +1.4% | Dakar, Diamniadio, Saint-Louis, Thiès | Medium term (2–4 years) |

| Commercial and industrial electrification growth | +1.2% | Diamniadio SEZ, Sandiara SEZ, Dakar industrial corridors | Medium term (2–4 years) |

| Grid densification and rural/peri-urban access expansion | +1.8% | National, with early gains in Kolda, Sédhiou, Kaolack, Tambacounda | Short term (≤ 2 years) |

| Renewable, storage, and gas-to-power integration | +1.0% | Saint-Louis (gas pipeline), Kolda (solar+BESS), national gas-to-power programme | Medium term (2–4 years) |

| Smart-meter-led feeder monitoring retrofits | +0.6% | Dakar initially, spill-over to national MV network | Long term (≥ 4 years) |

| Local tropicalized panel assembly partnerships | +0.5% | Dakar, Thiès, peri-urban industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Densification and Rural/Peri-Urban Access Expansion

Grid extension remains the strongest near-term demand driver in the Senegal distribution boards market because every new line and substation creates direct hardware positions. The World Bank's (Projet d'Appui au Développement de l'Accès à l'Électricité au Sénégal) project targets 4,000 km of new and rehabilitated power lines, 200,000 household connections, and the electrification of 600 health clinics. Additional Financing 3, approved in April 2026, added EUR 5.2 million, which is equivalent to USD 5.9 million, and this extends the active investment cycle for access works. Millennium Challenge Account (MCA) Senegal II also installed around 660 km of medium-voltage lines across southern and central regions, which broadens the installed base for downstream final and sub-main boards. The Senegal distribution boards market benefits because rural access projects favor durable, low-maintenance, dust- and humidity-resistant boards rather than standard urban configurations.

Building and Mixed-Use Project Pipeline

The Senegal distribution boards market is also supported by the widening construction pipeline in planned urban nodes and service-led districts. The Diamniadio International Industrial Platform was developed with a dedicated 30 kV electrical delivery station and progressive network capacity rising from 10 MW to 50 MW. That kind of site needs main, sub-main, and final boards across offices, utility rooms, tenant spaces, and support facilities. A mixed-use layout also improves revenue per project because one site can require several board categories under one coordinated installation. The Senegal distribution boards market, therefore, gains from projects that combine business, hospitality, logistics, and urban utility demand within one electrical footprint.

Renewable, Storage, and Gas-to-Power Integration

The Senegal distribution boards market is changing as new generation technologies demand different protection and enclosure standards. SENELEC started converting the 335 MW Bel Air thermal complex to natural gas in May 2025, which changes auxiliary power distribution needs at the plant. Eiffage completed a 16 MWp photovoltaic plant with 26 MWh of battery storage in northern Senegal in October 2025, adding a project type that needs dedicated inverters and battery management switchboards. These assets operate under thermal and protection conditions that differ from standard building installations, which raises demand for tropicalized, higher Ingress Protection (IP)-rated, and more engineered assemblies. The Senegal distribution boards market is therefore gaining more application-specific demand instead of relying only on basic connection growth.

Commercial and Industrial Electrification Growth

The Senegal distribution boards market is seeing stronger industrial demand in corridors where manufacturing capacity and power delivery are being built together. The Diamniadio platform already includes MV/LV TGBT (Tableau Général Basse Tension) infrastructure and expandable capacity for industrial tenants. Industrial users need high-amperage main boards, downstream sub-main boards, and repeat retrofit work as production loads change after occupancy. That creates a more stable procurement cycle than single-order utility projects alone. The Senegal distribution boards market also benefits because industrial customers tend to value reliability, service support, and board coordination more than low upfront cost alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import dependence for breakers, busbars, and enclosures | -1.5% | National, most acute in secondary cities outside Dakar | Medium term (2–4 years) |

| Certification and protection-coordination bottlenecks | -0.8% | National; SENELEC homologated list governs utility-facing products | Long term (≥ 4 years) |

| Coastal corrosion and heat-derating cost pressure | -0.5% | Dakar, Mbour, Saint-Louis, Ziguinchor coastal corridor | Medium term (2–4 years) |

| Thin digital-board service coverage outside Dakar | -0.4% | Peri-urban and rural zones; Dakar-exclusive SmartSen coverage | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Import Dependence for Breakers, Busbars, and Enclosures

Import dependence remains the most persistent brake on the Senegal distribution boards market. Most molded-case breakers, miniature breakers, busbars, and standard enclosures are imported before local workshops complete wiring, assembly, and labeling. This raises land cost and makes project delivery sensitive to overseas manufacturing schedules and port handling. CHINT's 2025 semi-annual report identified West Asia and Africa as a priority expansion corridor, which highlights why regional stocking and distribution capacity matter for smaller Senegalese builders. The Senegal distribution boards market remains exposed because local assembly has improved responsiveness, but not component self-sufficiency.

Coastal Corrosion and Heat-Derating Cost Pressure

The Senegal distribution boards market faces a clear cost challenge in coastal zones where corrosion resistance is not optional. CVCI documented that Dakar and adjacent coastal locations require stronger protection against saline exposure, often shifting specifications toward IP65-rated or stainless-steel enclosures. A project case in Senegal used American Iron and Steel Institute (AISI) 316 stainless-steel cabinets rated IP66 and IP67 for a coastal heat-recovery installation, showing how environmental exposure raises material cost and enclosure quality thresholds. High ambient temperatures also force engineers to derive breakers or oversize frames, which raises the cost per ampere in main and sub-main boards. The Senegal distribution boards market, therefore, sees stronger value concentration in coastal projects, but it also sees tighter margins where buyers resist those higher specifications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Final Distribution Boards Anchor Volume as Sub-Main Boards Drive Faster Growth

Final distribution boards held 46.8% of the Senegal distribution boards market share in 2025, which made them the largest type segment. This lead came from residential and peri-urban connection activity because each added household or small commercial unit requires a final board for basic protection and meter termination. The World Bank's PADAES program targets 200,000 new household connections, which keeps final board demand broad and repetitive. The installed scale of SENELEC's low-voltage network also supports replacement demand across a large base of existing nodes. In the Senegal distribution boards industry, this segment remains the clearest link between electrification policy and recurring hardware volume.

Main distribution boards remain important for larger commercial buildings, industrial sites, and utility installations where incoming loads need higher current handling and stronger coordination. The Diamniadio platform provides a reference case because it uses a structured MV/LV delivery architecture that can be repeated across expanding tenant bases. Sub-main distribution boards are projected to grow at 7.9% CAGR through 2031, which is the fastest pace within type segmentation. That growth reflects rising use of layered power distribution in hospitals, industrial parks, hotels, and multi-level commercial buildings. Schneider Electric's 2025 launch of MasterPacT MTZ Active in West Africa supports this retrofit opportunity because facilities can add digital monitoring without replacing the full switchboard.

By Technology: Conventional Boards Sustain Scale While Smart and IoT Boards Set the Growth Path

Conventional boards held 82.5% of the technology segment in 2025, which kept them dominant across the installed base. The Senegal distribution boards market still depends on conventional boards in rural electrification, standard housing, and light commercial applications because they are easier to procure and maintain under tight budget limits. SENELEC's network included 12,401 HTA/BT (medium-voltage/low-voltage) substations in 2025, and that large installed base supports a long replacement cycle for standard low-voltage assemblies. Price sensitivity also remains high in peri-urban and rural programs where digital features do not yet justify their added cost. For the Senegal distribution boards industry, conventional volume will remain important even as smart-board specifications broaden.

Smart and IoT-enabled boards are projected to grow at 11.4% CAGR through 2031, which is the fastest rate within technology. MCA Senegal II launched training in May 2025 for SENELEC agents on communicating protection and sectioning devices for the 30 kV network outside Dakar. Akilee's SmartSen platform already supervises Dakar's distribution network from source substations to HTA/BT nodes, which gives the market a clear operating model for monitoring infrastructure. Adoption should widen as feeder monitoring, metering integration, and remote control become more common outside the capital. The Senegal distribution boards market is therefore moving toward a split structure where conventional boards carry scale and smart boards capture the strongest growth rate.

By Mounting Type: Wall-Mounted Panels Serve the Mass Market While Floor-Standing Formats Gain Industrial Traction

Wall-mounted boards captured 71.2% of the Senegal distribution boards market size in 2025, which reflects the weight of residential and light commercial demand. This format is standard in apartments, clinics, banks, telecom offices, and smaller service buildings where space efficiency and ease of access matter. In Dakar and other coastal locations, these boards often shift from standard indoor protection levels to higher IP ratings where corrosion exposure is present. Hager Group's product range and West African distribution presence align closely with this segment of the market. Wall-mounted boards, therefore, retain a stable role in the broadest volume layer of demand.

Floor and free-standing boards are projected to grow at 8.1% CAGR through 2031, which places them above the wall-mounted segment in growth terms. These boards are used in utility rooms, industrial plants, large hotels, and energy sites where higher current levels and maintenance access are essential. The Senegal distribution boards market is seeing more of this demand as industrial parks, gas-linked assets, and storage systems come online. CHINT's participation in the Boucle de Ferlo project strengthens its visibility in larger engineered installations and supports its push into related low-voltage opportunities. Since most floor-standing systems are assembled to order, lead-time control remains a key factor in project awards.

By End-User: Commercial Segment Leads Current Demand While Utilities Accelerate

The commercial segment held 34.6% share of the Senegal distribution boards market size in 2025, making it the largest end-user category. Demand is concentrated around Dakar and Diamniadio, where hotels, offices, event facilities, and service buildings cluster around the country's strongest urban load centers. Commercial buyers also tend to require better enclosure quality, cleaner documentation, and stronger after-sales support than basic residential projects. That gives approved OEM-linked assemblers an advantage in specification-driven tenders. The Senegal distribution boards market continues to draw solid value from this segment even when unit counts are lower than in residential access programs.

Utilities are projected to grow at 8.8% CAGR through 2031, which is the fastest pace among end users. This growth reflects the fact that every new feeder extension, substation package, and grid reinforcement project creates dedicated positions for protection and control boards. The World Bank's access program, Millennium Challenge Account (MCA) Senegal II network works, and VINCI Energies' substation and line contract all expand the number of utility nodes that need board installation or later replacement. Residential demand still supports stable final-board volume, but utilities are expanding faster because infrastructure buildout adds entirely new equipment positions across the network. That keeps utility procurement central to the Senegal distribution boards market through the forecast period.

Geography Analysis

Dakar and the wider Grand Dakar area remain the main demand center for the Senegal distribution boards market in 2026. This zone combines the country's densest commercial construction activity, the largest concentration of private substations, and the most complex utility interfaces. SENELEC reported 8,958 public HTA/BT substations and 3,327 private substations nationally in 2025, and a large share of private-site demand sits in Dakar's tertiary and industrial districts. VINCI Energies' program with SENELEC is expanding the electrical backbone that supports new urban connections through major line and substation works. Coastal exposure in Dakar also pushes many projects toward IP65 or stainless-steel enclosures, which lifts value per unit and raises technical thresholds for suppliers.

Saint-Louis and the northern corridor are emerging as a secondary demand zone in the Senegal distribution boards market. The Boucle de Ferlo project added three 225 kV substations at Ndioum, Linguère, and Touba 2, strengthening upstream reliability across northern and interior regions. Northern solar and storage activity is also widening demand for engineered main and sub-main boards beyond the capital. As reliability improves, downstream low-voltage expansion should create more recurring demand in localities that previously had weaker grid access.

Southern and central Senegal form the growth frontier for the Senegal distribution boards market because access programs are moving into dispersed localities while regional grid integration raises the strategic value of domestic infrastructure. MCA Senegal II's Projet Accès includes around 660 km of medium-voltage distribution lines across Kolda, Tambacounda, Fatick, Kaolack, and Sédhiou, which broadens the installed base for final and sub-main boards. The World Bank's Organisation pour la Mise en Valeur du fleuve Gambie (OMVG) regional interconnection brief and the Regional Electricity Regulatory Association (ERERA)'s 2026 electricity market governance meeting both point to a more connected West African power system, which increases the relevance of standards, metering, and protection coordination in Senegal. Xinhua reported in February 2026 that Livoltek, affiliated with Hexing Group, established a joint venture with SENELEC at Diamniadio to co-produce equipment adapted to heat and saline conditions, showing that suppliers increasingly view Senegal as a local production and regional access point. Together, these shifts make regional-facing compliance and local adaptation more important to supplier strategy than they were in Senegal's earlier domestic-only growth phase.

Competitive Landscape

The Senegal distribution boards market is moderately fragmented at the OEM level and more concentrated at the project execution level. Schneider Electric, Legrand, ABB, Hager, and CHINT compete for specification with engineers, architects, and utility buyers, while local Senegalese assemblers supply boards using imported breakers, busbars, and enclosures. This structure allows premium projects to stay brand-led while cost-sensitive orders move through local assembly channels. The Senegal distribution boards market also gives EPC contractors a stronger role than in many small electrical markets because large utility and infrastructure packages are awarded as integrated contracts. That keeps procurement influence split between OEMs, assemblers, and turnkey project managers.

Strategic moves since 2025 show how companies are positioning for the next phase of the Senegal distribution boards market. Schneider Electric launched MasterPacT MTZ Active in West Africa in August 2025, and its retrofit-ready design suits aging low-voltage switchboards in commercial and industrial facilities. CHINT used its role in Senegal's Boucle de Ferlo transmission project to strengthen credibility with utility-linked customers and downstream specifiers. Hager Group's 2024 acquisition of Advizeo broadened its smart building and energy management capability, which supports monitored low-voltage applications in commercial settings. These moves show that board suppliers are competing on connected functionality, project references, and service reach, not only on equipment price.

The Senegal distribution boards market still has room in tropicalized IEC-compliant assembly and in smart boards that can work with utility monitoring architecture. Akilee's SmartSen model and Schneider's retrofit products show where board intelligence can add value, but deployment outside Dakar remains limited. VINCI Energies and Eiffage Énergie Systèmes remain important because they specify and procure boards within larger SENELEC infrastructure packages. Compliance with SENELEC approval requirements and IEC standards continues to favor suppliers with proven documentation and local execution support.

Senegal Distribution Boards Industry Leaders

Schneider Electric SE

Legrand SA

ABB Ltd.

SMART ENERGIES

Brilltech Engineers Pvt. Ltd

- *Disclaimer: Major Players sorted in no particular order

Geopolitical Scenarios and Their Impact on the Senegal Distribution Boards Market

Active conflicts and trade realignments continue to affect the Senegal distribution boards market through freight risk, input-cost pressure, sourcing shifts, and regional integration changes. The table below summarizes the directional effect of the main geopolitical factors retained after source screening.

Red Sea Crisis: Freight Cost Inflation and Extended Lead Times for Electrical Components

Red Sea shipping insecurity remains a real external risk for the Senegal distribution boards market because Senegal imports most breakers, busbars, and enclosures. Frontiers in Political Science documented that attacks on commercial shipping in the Red Sea disrupted maritime flows and forced rerouting that increased transit time and insurance pressure. Industry experts reported renewed focus on Red Sea transits in July 2025 after further Houthi attacks, which shows that this risk remained active rather than temporary. For Dakar-based assemblers, longer shipping cycles weaken schedule certainty and favor firms with stronger working capital or local stockholding. The Senegal distribution boards market, therefore, faces a freight-led cost premium even when domestic demand stays firm.

Russia-Ukraine War: Copper and Steel Costs Keep Pressure on Board Economics

The Senegal distribution boards market is also exposed to higher commodity costs because copper and steel remain core inputs for busbars, wiring, breaker contacts, and enclosures. Deutsche Bank's 2026 commodities outlook and World Bank-linked commodity commentary both pointed to continued firmness in copper prices during 2026 before later easing. These conditions matter in Senegal because local assemblers are price takers on imported components and cannot easily absorb raw-material inflation under fixed-price contracts. The effect is more visible in higher-amperage industrial and utility boards where copper content is larger. The Senegal distribution boards market, therefore, remains vulnerable to margin compression when tender prices move more slowly than material costs.

Geopolitical Scenarios Impact Analysis

| Geopolitical Factor | Impact Direction | Impact Magnitude on Market | Primary Channel | Timeline |

|---|---|---|---|---|

| Red Sea shipping disruptions | Negative | High | Supply chain and landed cost | Short term (≤ 2 years) |

| Russia-Ukraine war and commodity cost pressure | Negative | Moderate-High | Input cost inflation | Medium term (2-4 years) |

| US-China trade tensions and sourcing diversion | Mixed | Moderate | Competitive landscape and sourcing | Medium term (2-4 years) |

| China's zero-tariff policy toward Africa | Positive | Moderate | Procurement cost reduction | Short-medium term (≤ 3 years) |

| Sahel instability and regional corridor realignment | Negative | Low-Moderate | Logistics and project sentiment | Medium term (2-4 years) |

| Source: Mordor Intelligence | ||||

Recent Industry Developments

- March 2026: The World Bank approved a EUR 5.20 million additional credit for the Senegal Energy Access Scale-Up Project (PADAES, P176620), extending grid densification works and household connection targets. The additional financing sustains procurement of HTA/BT substation equipment and final distribution boards beyond the original project timeline.

- January 2026: CHINT delivered critical power equipment for three new 225 kV substations, Ndioum, Touba 2, and Linguère, commissioned by SENELEC as part of the Plan Sénégal Émergent transmission expansion. The project, completed in 2025 and publicly announced in January 2026, marks CHINT's first major utility-equipment reference in Senegal's HV transmission segment, establishing a credibility base for LV board specification wins.

Senegal Distribution Boards Market Report Scope

A distribution board, also known as a panelboard, breaker panel, or electric panel, is a component of an electricity supply system that distributes electrical power into subsidiary circuits while providing protective fuses or circuit breakers. The distribution board market involves the production, distribution, and sale of these panels, serving residential, commercial, industrial, and utility sectors, from small consumer units in homes to large switchboards in industrial facilities.

The Senegal Distribution Boards Market is segmented into type, technology, mounting type, and end-user. By type, the market is segmented into main distribution boards, sub-main distribution boards, and final distribution boards. By technology, the market is segmented into conventional boards and smart/IoT-enabled boards. By mounting type, the market is segmented into wall-mounted and floor/free-standing boards. By end-user, the market is segmented into utilities, industrial, commercial, and residential sectors. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Main Distribution Boards (MDB) |

| Sub-Main Distribution Boards (SMDB) |

| Final Distribution Boards (FDB) |

| Conventional Boards |

| Smart/IoT-enabled Boards |

| Wall-Mounted |

| Floor/Free-Standing |

| Utilities |

| Industrial |

| Commercial |

| Residential |

| By Type | Main Distribution Boards (MDB) |

| Sub-Main Distribution Boards (SMDB) | |

| Final Distribution Boards (FDB) | |

| By Technology | Conventional Boards |

| Smart/IoT-enabled Boards | |

| By Mounting Type | Wall-Mounted |

| Floor/Free-Standing | |

| By End-User | Utilities |

| Industrial | |

| Commercial | |

| Residential |

Key Questions Answered in the Report

What is the current market size of Senegal Distribution Boards Market?

The Senegal Distribution Boards Market size is projected to expand from USD 12.14 million in 2025 and USD 12.82 million in 2026 to USD 17.56 million by 2031, registering a CAGR of 6.5% between 2026 to 2031.

What is the forecast growth rate through 2031?

The market is expected to expand at a 6.5% CAGR between 2026 and 2031.

Which board type leads demand in Senegal?

Final distribution boards led the type mix in 2025 with a 46.8% share because electrification and last-mile connections require high-volume deployment.

Which technology is growing the fastest?

Smart and IoT-enabled boards are forecast to grow at 11.4% CAGR through 2031 as monitoring and communication needs increase.

Which end-user is expanding the fastest?

Utilities are projected to grow at 8.8% CAGR because new substations, feeder extensions, and grid upgrades add new protection and control positions.

Why does Dakar remain the key demand center?

Dakar combines the highest concentration of commercial projects, private substations, utility upgrades, and coastal-specification requirements, which keeps it ahead in both volume and value.

Page last updated on: