Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.04 Billion |

| Market Size (2026) | USD 8.38 Billion |

| Market Size (2031) | USD 11.44 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Oilfield Services Market Analysis by Mordor Intelligence

The Africa Oilfield Services Market size is projected to expand from USD 8.04 billion in 2025 and USD 8.38 billion in 2026 to USD 11.44 billion by 2031, registering a CAGR of 6.42% between 2026 to 2031.

Shifting capital toward deep-water prospects in West Africa and gas monetization schemes in East Africa is sustaining double-digit growth in offshore spending, while mature onshore producers lean on enhanced oil recovery programs to stem decline. Indigenous contractors are expanding rapidly under stricter local-content mandates, yet multinationals still dominate high-complexity services such as directional drilling and subsea installation. Digital-twin platforms and remote-operations centers are trimming non-productive time, improving rig utilization, and narrowing the cost spread between conventional and unconventional wells. Security risks in the Niger Delta and Cabo Delgado continue to raise lifting costs, but improved oil prices above USD 80 per barrel are unlocking long-deferred drilling budgets, supporting an upcycle for the Africa oilfield services market through at least 2028.

Key Report Takeaways

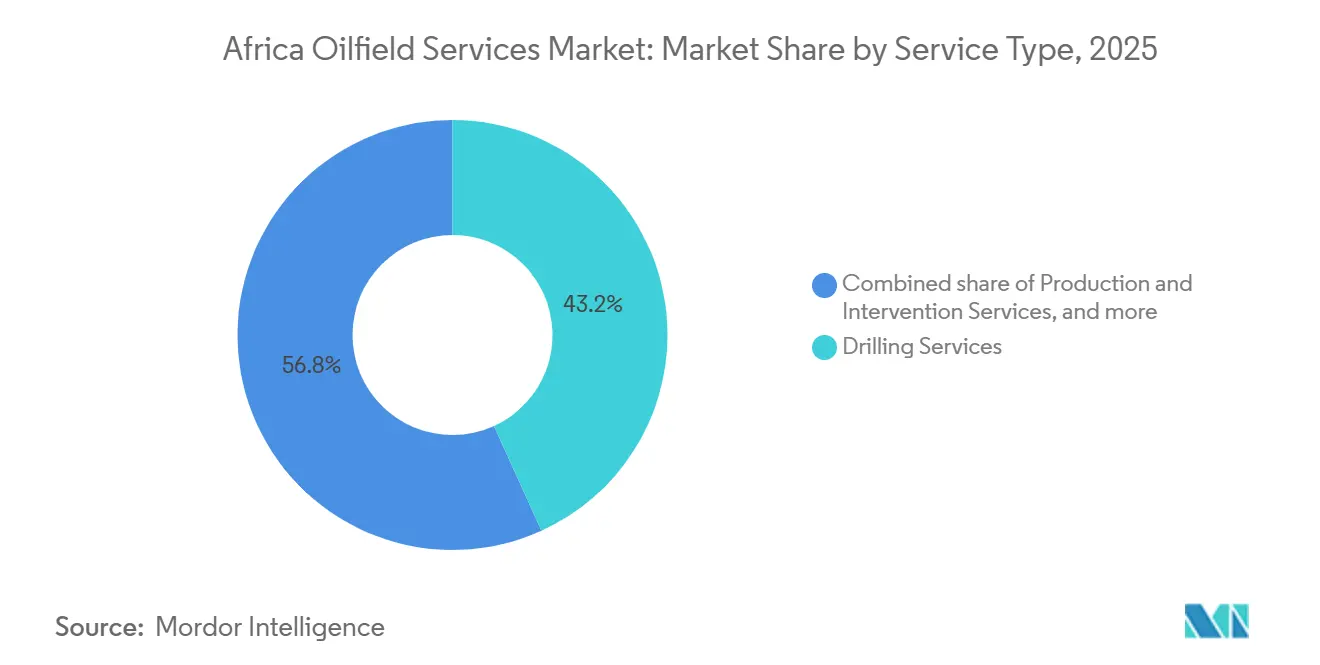

- By service type, drilling captured 43.2% of the Africa oilfield services market share in 2025, and is forecast to expand at a 6.8% CAGR through 2031.

- By location, onshore operations held 76.9% of the Africa oilfield services market size in 2025, whereas offshore work is projected to grow at an 8.4% CAGR to 2031.

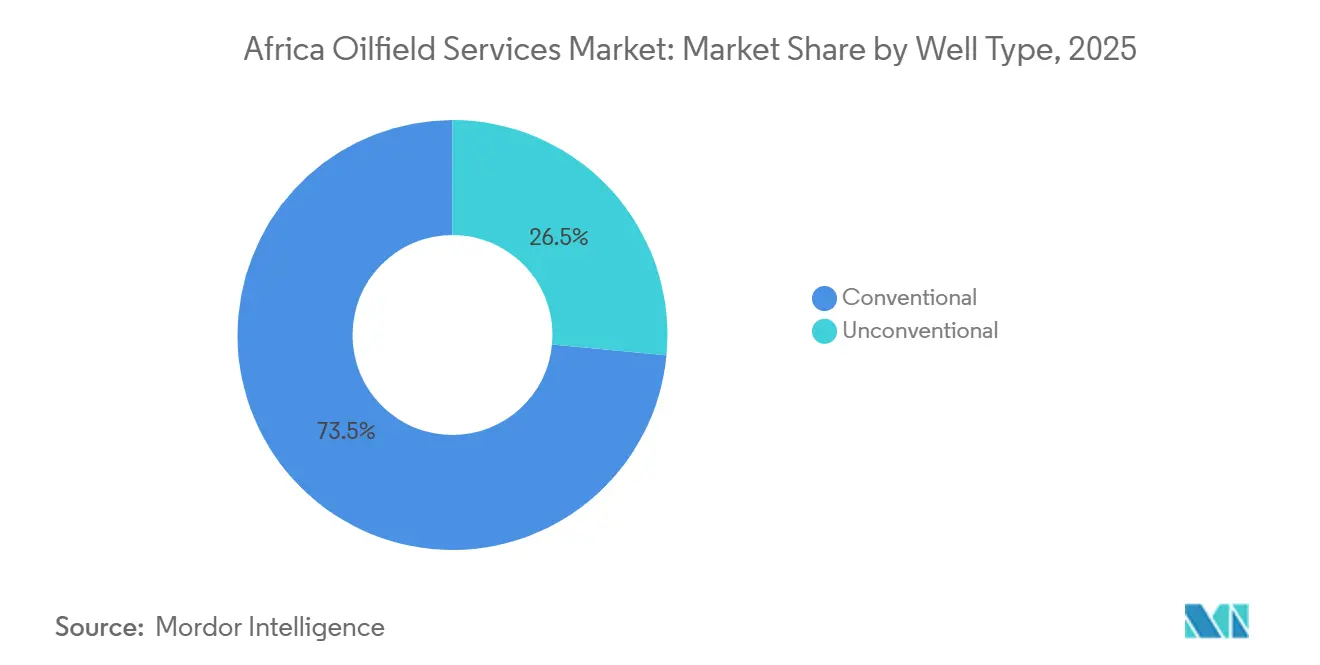

- By well type, conventional wells accounted for 73.5% of the Africa oilfield services market share in 2025; unconventional activity is rising at a 7.9% CAGR through 2031.

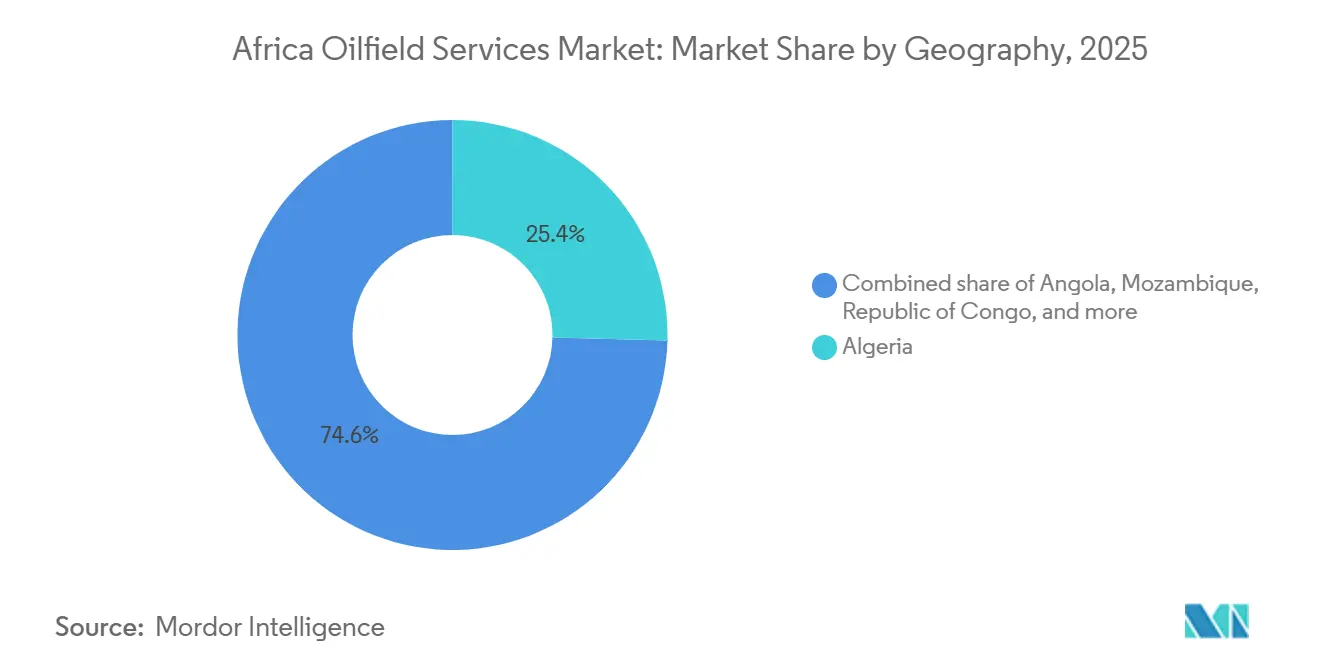

- By geography, Algeria led with 25.4% revenue share in 2025, while Mozambique is advancing at the highest 9.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Oilfield Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising deep-water exploration campaigns | +1.2% | Nigeria, Angola, Ghana, Equatorial Guinea | Medium term (2-4 years) |

| Recovery in oil prices boosting CAPEX | +1.5% | Algeria, Nigeria, Angola | Short term (≤ 2 years) |

| Demand for enhanced-oil-recovery | +0.8% | Algeria, Nigeria, Angola | Long term (≥ 4 years) |

| Local-content mandates | +0.9% | Nigeria, Angola, Ghana, Mozambique | Medium term (2-4 years) |

| Adoption of remote ops & digital twins | +0.6% | Nigeria, Angola, Egypt, Algeria | Medium term (2-4 years) |

| Surge in FLNG infrastructure | +1.1% | Mozambique, Nigeria, Senegal, Mauritania | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Deep-Water Exploration Campaigns in West Africa

Operators are steering a larger slice of exploration budgets toward pre-salt and ultra-deep-water acreage that offers multi-billion-barrel potential, underpinning premium day rates for seventh-generation drillships. Shell’s USD 5 billion sanction of Bonga North in late 2024 mobilized subsea tree, riser, and dynamic-positioning packages that will keep contractors busy through 2028.[1]Reuters Staff, “Shell Gives Final Green Light to Nigeria’s Bonga North Project,” Reuters, reuters.com Angola’s Azule Energy followed with a USD 1.2 billion award to TechnipFMC for Block 15/06 in early 2025, validating integrated EPC models that bundle drilling, completion, and installation.[2]TechnipFMC Investor Relations, “Azule Energy Awards TechnipFMC Integrated Subsea Contract,” technipfmc.com Ghana’s Pecan field, already producing 40,000 bpd, is tendering a fourth development well, sustaining demand for jack-ups and cementing services. Concentrated activity gives specialized contractors like Transocean and Valaris pricing power, with day rates topping USD 400,000, while land-focused firms endure margin compression. The deep-water pivot is therefore a primary growth vector for the Africa oilfield services market over the medium term.

Recovery in Oil Prices Boosting CAPEX by NOCs & IOCs

Brent prices above USD 80 in 2025 restored economic viability for projects shelved during the 2020 downturn. Sonatrach earmarked USD 50 billion for upstream work through 2028, granting Schlumberger a five-year integrated-services contract covering 12 concessions.[3]Schlumberger, “2025 Annual Report,” slb.com Nigeria’s NNPC secured USD 3 billion in financing to rehabilitate 21 marginal fields, an initiative expected to lift production by 200,000 bpd by 2027, thereby expanding opportunities for workover rigs and coiled-tubing units. Angola reopened licensing for eight offshore blocks in 2024; bids from TotalEnergies, Equinor, and Chevron depend on prices staying above USD 75 to justify high front-end costs. Although price volatility remains a risk, multiyear service contracts locked in during the current upcycle give the Africa oilfield services market a revenue floor through the short term.

Demand for Enhanced-Oil-Recovery in Mature Onshore Fields

Half-century-old Saharan and Niger Delta fields are entering tertiary phases, necessitating polymer flooding, carbon dioxide injection, and thermal stimulation. Sonatrach’s pilot CO₂-EOR in Hassi Messaoud injects 500,000 tons annually to raise recovery from 30% to 42%, potentially unlocking USD 2 billion in future injection equipment orders. Nigeria’s joint-venture operators are evaluating water-alternating-gas schemes but remain hampered by community disputes that keep EOR penetration below 15% of feasible reserves. Baker Hughes captured a USD 180 million artificial-lift package in Angola aimed at extending nine concessions by a decade. Sustained crude prices and ready access to low-cost CO₂ dictate project economics, positioning Algeria and Angola at the forefront of EOR adoption across the Africa oilfield services market.

Local-Content Mandates Spurring Indigenous Service Firms

Revised regulations now require up to 50% domestic participation for onshore drilling in Nigeria and 40% subcontracting for subsea work in Angola. Oando Energy Services won a USD 450 million, three-year contract in 2025 to supply drilling fluids and wellhead equipment for 40 wells, a record award for a Nigerian contractor. Saipem formed a joint venture with Sonasurf to fabricate flexible pipeline spools in Luanda, meeting Angola’s Presidential Directive 4/2024 while retaining engineering control. Ghana’s local-content matrix pushed Tullow’s Jubilee expenditure to 62% domestic in 2024, up from 48% in 2020. These rules fragment the value chain, lowering blended margins for global integrators but enlarging the addressable market for indigenous entrants, a dynamic that will keep the Africa oilfield services market competitive.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Political instability & security risks | -1.3% | Nigeria, Libya, Mozambique | Short term (≤ 2 years) |

| Regulatory uncertainty & slow licensing | -0.7% | Angola, Nigeria, Libya | Medium term (2-4 years) |

| Investor decarbonization pressure | -1.1% | Nigeria, Angola | Long term (≥ 4 years) |

| Skilled-labor shortage | -0.5% | Nigeria, Angola, Ghana | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Political Instability & Security Risks in Key Basins

Pipeline sabotage in Nigeria’s Niger Delta adds USD 8 to USD 12 per barrel to lifting costs, and Shell divested its onshore stake for USD 2.4 billion in early 2025 to avoid community disputes and flaring penalties.[4]Financial Times Reporters, “Shell Sells Nigeria Onshore JV to Local Consortium,” ft.com Cabo Delgado insurgent attacks totaled 47 in 2024, and TotalEnergies’ onshore LNG rebuild depends on a still-fragile security cordon. Libya’s rival factions forced three production shutdowns in 2024, driving drillers to demand advance payments or sovereign guarantees. These security premiums erode margins and nudge capital toward stable jurisdictions, moderating the near-term revenue trajectory of the Africa oilfield services market.

Investor Decarbonization Pressure Curbing Financing

Fourteen of the twenty largest project-finance banks now restrict funding for high-flaring exploration projects. TotalEnergies’ East African Crude Oil Pipeline faced a nine-month financing delay in 2024 after shareholder backlash, raising the project’s weighted-average cost of capital by 120 basis points. Shell’s Nigerian divestments were also driven by activist scrutiny over annual spill costs exceeding USD 400 million. In contrast, Eni raised USD 4.7 billion for Coral Sul’s second train in 2025, signaling investor appetite for gas-aligned, lower-carbon assets. This bifurcation creates a two-speed Africa oilfield services market, where oil-prone exploration faces capital rationing while gas infrastructure secures funding.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Drilling Anchors Revenue, Completion Lags

Drilling held 43.2% of the Africa oilfield services market share in 2025, propelled by multi-well deep-water programs in Angola and Nigeria. The segment is expected to advance at 6.8% through 2031, with Sonatrach slated to drill 120 exploration and appraisal wells and Azule Energy restarting Block 15/06 campaigns. Completion services captured about 28% of revenue but lag in growth because multi-stage hydraulic fracturing remains limited to Algeria’s tight-gas plays. Production-optimization services such as artificial lift are gaining traction: Baker Hughes installed 34% more units in Angola during 2025, illustrating rising demand for life-extension tools. Decommissioning, though still niche, is emerging as a high-margin play after Subsea 7’s USD 320 million Escravos contract, emphasizing widening opportunities beyond drilling.

While drilling retains volume leadership, automation, remote steering, and dual-activity rigs are narrowing the cost gap with ancillary services. As contractors upgrade fleets and integrate digital workflows, EBITDA margins for drilling could converge with completion by decade-end, preserving the segment’s centrality to the Africa oilfield services market.

By Location: Onshore Scale Meets Offshore Momentum

Onshore operations generated 76.9% of the Africa oilfield services market size in 2025, anchored by Algeria’s Saharan giants and Nigeria’s Niger Delta. Offshore revenue, though just 23.1%, is expanding at an 8.4% CAGR, outstripping onshore’s 5.7%. Ultra-deep campaigns below 2,000 m water depth require high-spec drillships like Transocean’s Deepwater Asgard, delivered to Angola under a USD 540 million contract. Onshore faces structural headwinds, security, aging rigs, and lower contractor returns, yet remains indispensable for NOC output targets. Offshore’s share is set to reach 28% by 2031, fueled by pre-salt discoveries and FLNG tie-backs, but absolute onshore spend will still rise in line with Algeria’s gas push and Nigeria’s marginal-field revival.

The diverging growth paths mean service providers must balance land-rig fleets for volume with deepwater assets for margin. Firms that straddle both arenas will be best positioned to capture the Africa oilfield services market’s blended growth.

By Well Type: Conventional Dominance, Unconventional Upside

Conventional wells accounted for 73.5% of the Africa oilfield services market size in 2025, reflecting superior reservoir quality in the Niger Delta and Saharan basins. Unconventional activity - tight gas, shale, and coal-bed methane - is rising at a 7.9% CAGR through 2031 and is poised for further upside as Algeria commercializes Timimoun and Ahnet. Halliburton’s USD 680 million fracturing award for 42 horizontals in Timimoun exemplifies the emerging demand profile. Cost parity is improving; pad drilling and zipper fracs cut per-well expenses by 23% between 2023 and 2025. Still, conventional wells remain cheaper and less technically demanding, ensuring their numerical dominance through 2031. The well-type mix could shift to 68% conventional and 32% unconventional by 2031, supplying a broader technology runway for pressure-pumping fleets within the Africa oilfield services market.

Geography Analysis

Algeria secured 25.4% of Africa's oilfield services market revenue in 2025, driven by Sonatrach's USD 12 billion upstream budget and integrated project awards to Schlumberger and Weatherford. Mozambique, the fastest-growing geography at 9.5% CAGR, benefits from Coral Sul's expansion and Mozambique LNG's restart, which together require 14 subsea wells, 180 km of flowlines, and two FPSO units. Nigeria, contributing 22%, lags continental growth due to Niger Delta unrest and Shell's asset divestments, though NNPC's marginal-field program offers upside.

Angola's 18% share rests on Azule Energy's Block-15/06 spending and renewed licensing. Egypt accounts for 12%, sustained by Eni's Zohr and BP's West Nile Delta programs that keep 32 land rigs and six jack-ups active. Ghana's Jubilee and TEN complexes supply 5% of revenue but face plateauing output absent discoveries. Libya fluctuates between 4% and 6%, contingent on cease-fire durability, while Senegal, Gabon, Equatorial Guinea, and Congo form an 8% "Rest of Africa" cluster highlighted by Woodside's Sangomar first oil in mid-2024.

North Africa offers scale but runs regulatory inertia; West Africa promises high-margin deep-water work tempered by security risk; East Africa blends frontier gas potential with insurgent threats. Portfolio diversification across these blocs helps operators hedge geopolitical volatility, yet the center of gravity is tilting toward Algeria and Mozambique as gas monetization and transition alignment reshape capital flows in the Africa oilfield services market.

Competitive Landscape

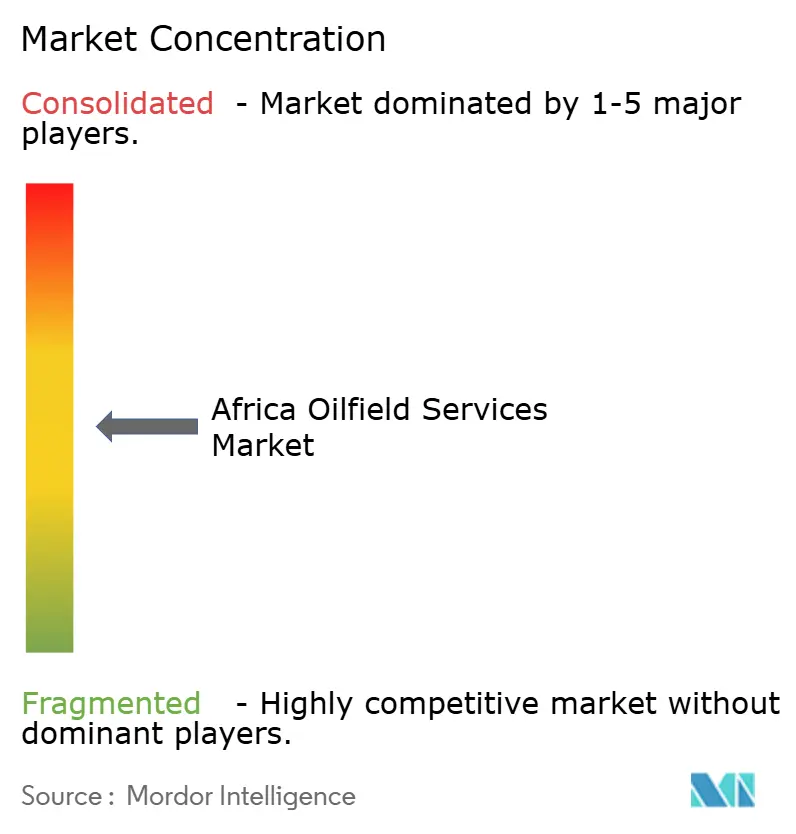

The Africa oilfield services market shows moderate concentration: the top five players commanded roughly 48% of 2025 revenue, led by Schlumberger, Halliburton, and Baker Hughes. Schlumberger’s USD 2.1 billion, five-year Sonatrach deal underscores an integrated-project-management strategy that bundles drilling, wireline, and stimulation under performance incentives. Halliburton and Baker Hughes are vying for a technological edge; Halliburton’s iCruise rotary-steerable and Baker Hughes’ Leucipa automation each slash non-productive time by up to 20%. Weatherford, TechnipFMC, and Subsea 7 round out the top tier, excelling in wireline, subsea, and decommissioning niches.

Local-content rules are allowing indigenous entrants like Seplat Energy and Oando Energy Services to vertically integrate and undercut multinationals by up to 18% in onshore work. Saipem’s flexible-pipe JV with Sonasurf and TechnipFMC’s fabrication plans in Nigeria illustrate hybrid models that satisfy compliance without surrendering engineering control. White-space opportunities in carbon-capture wells, geothermal drilling, and decommissioning widen the competitive canvas, promising new revenue pools even as traditional margins compress.

Going forward, multinational integrators will dominate deep-water and high-tech segments, while domestic firms take larger slices of land-rig, logistics, and low-complexity services. The result is a two-tier Africa oilfield services market that stays contestable, innovative, and regionally diverse.

Africa Oilfield Services Industry Leaders

Schlumberger Limited

Weatherford International Plc

Baker Hughes Company

Halliburton Company

TechnipFMC plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Shell Nigeria Exploration and Production Company (SNEPCo) and Sunlink Energies have entrusted Halliburton with an Integrated Drilling Services contract. This contract, situated in OML 144 offshore Nigeria, sees Halliburton playing a pivotal role in the HI gas field's development, ensuring a steady feed gas supply to Nigeria LNG's Train 7 facility.

- November 2025: Agiba Petroleum Company, under Egypt’s Ministry of Petroleum and Mineral Resources, drilled two new oil and gas production wells in the Western Desert. Efforts are currently focused on integrating these wells into the existing production facilities. The newly named wells, Dorra-36 and West Yasmine-3, have yielded encouraging early results. Initial flow tests reveal a combined output of approximately 1,650 barrels of crude oil and about 19 million cubic feet of natural gas daily.

- August 2025: National Energy Services Reunited Corp. secured multiple Production Services contracts in Algeria and Libya, with a total estimated value exceeding USD 100 million. Spanning durations of three to five years, these contracts cover essential Production Services segments, including Coiled Tubing, Nitrogen & Pumping Services, Cementing, and Hydraulic Fracturing.

Africa Oilfield Services Market Report Scope

Oilfield services (OFS) refer to all the services that support onshore and offshore oil and gas extraction and production processes. These services include drilling and formation evaluation, well construction, and completion services.

The Africa oilfield services market is segmented by service type, location, well type, and geography. By service type, the market is segmented into drilling services, completion services, production and intervention services, and other services. By location, the market is segmented into onshore and offshore. By well type, the market is segmented into conventional and unconventional. The report also covers market size and forecasts for the African oilfield services market across major countries. For each segment, the market size and forecasts have been done based on revenue (USD).

By Service Type

| Drilling Services |

| Completion Services (Cementing, Hydraulic Fracturing) |

| Production and Intervention Services |

| Other Services (OSV, seismic, decomm., aviation) |

By Location

| Onshore |

| Offshore |

By Well Type

| Conventional |

| Unconventional |

By Geography

| Nigeria |

| Angola |

| Algeria |

| Egypt |

| Libya |

| Republic of Congo |

| Ghana |

| Mozambique |

| Rest of Africa |

| By Service Type | Drilling Services |

| Completion Services (Cementing, Hydraulic Fracturing) | |

| Production and Intervention Services | |

| Other Services (OSV, seismic, decomm., aviation) | |

| By Location | Onshore |

| Offshore | |

| By Well Type | Conventional |

| Unconventional | |

| By Geography | Nigeria |

| Angola | |

| Algeria | |

| Egypt | |

| Libya | |

| Republic of Congo | |

| Ghana | |

| Mozambique | |

| Rest of Africa |

Key Questions Answered in the Report

What is the current value of the Africa oilfield services market?

The Africa oilfield services market size stood at USD 8.38 billion in 2026 and is set to reach USD 11.44 billion by 2031.

Which segment generates the largest revenue?

Drilling services lead the revenue table with 43.2% market share in 2025, driven by deep-water campaigns in Nigeria and Angola.

Which country is growing fastest for service demand?

Mozambique shows the highest growth, expanding at a 9.5% CAGR thanks to Coral Sul and Mozambique LNG developments.

How are local-content rules affecting competition?

Stricter rules in Nigeria and Angola are channeling low-complexity services to indigenous contractors, lowering entry barriers while pushing multinationals toward high-tech offshore work.

What technology trends are cutting drilling costs?

Remote-operations centers, digital-twin platforms, and automated steering systems are reducing non-productive time by up to 20% and improving rig efficiency.

How does political risk influence investment decisions?

Security issues in the Niger Delta, Cabo Delgado, and Libya add costs and uncertainty, steering capital toward more stable basins such as Algeria and Egypt.

Page last updated on: