India Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

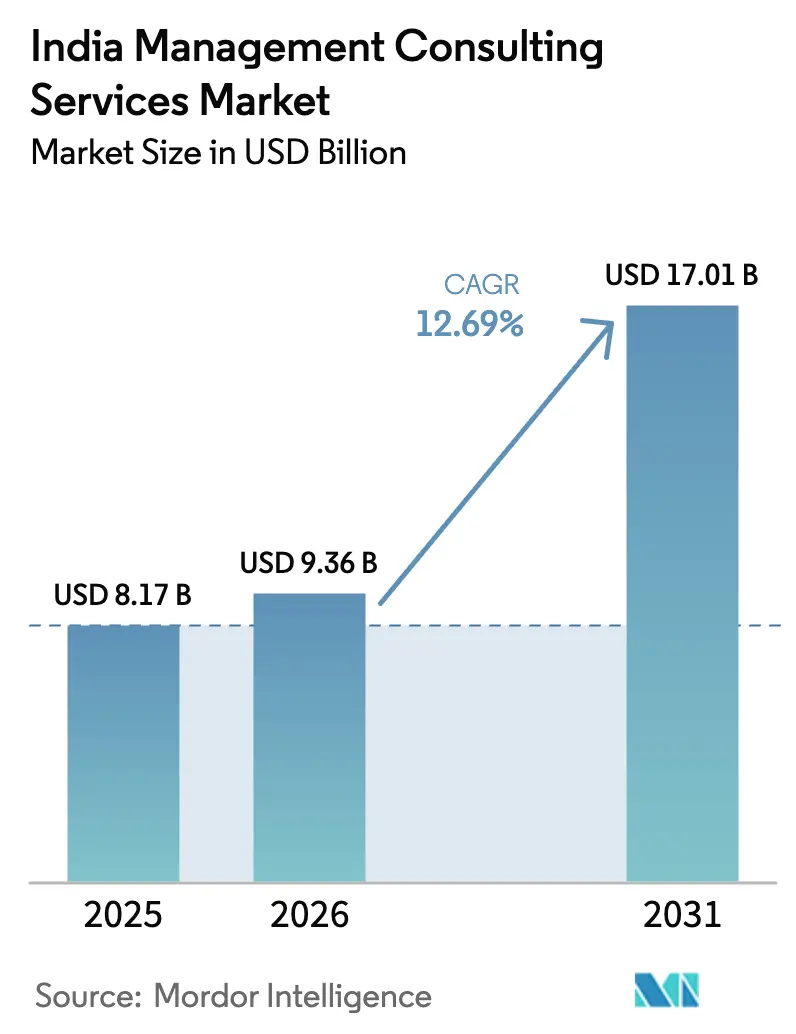

| Base Year Market Size (2025) | USD 8.17 Billion |

| Market Size (2026) | USD 9.36 Billion |

| Market Size (2031) | USD 17.01 Billion |

| Growth Rate (2026 - 2031) | 12.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Management Consulting Services Market Analysis by Mordor Intelligence

The India management consulting services market size is projected to expand from USD 8.17 billion in 2025 and USD 9.36 billion in 2026 to USD 17.01 billion by 2031, registering a CAGR of 12.69% between 2026 and 2031. A decisive budget shift away from legacy information-technology upkeep toward transformation programs, coupled with mandatory sustainability disclosures, is accelerating demand for advisory support. Corporations are directing capital into cloud-native operating models, generative-AI pilots, and enterprise-wide ESG frameworks, while venture-backed small and medium-sized enterprises (SMEs) seek growth-strategy roadmaps that protect runway and unlock later-stage capital. Simultaneously, more than 1,580 global capability centers (GCCs) already operate in India, prompting multinationals to pursue hybrid advisory engagements that combine headquarters workshops with remote analytics delivery. Competitive intensity remains high as global strategy houses, Big Four advisory arms, and Indian IT majors converge on the same digital-transformation budgets, compressing fees and normalizing outcome-based pricing. Talent attrition to product-management roles and venture-capital funds, together with the rise of AI-driven self-service diagnostic platforms, present structural headwinds.

Key Report Takeaways

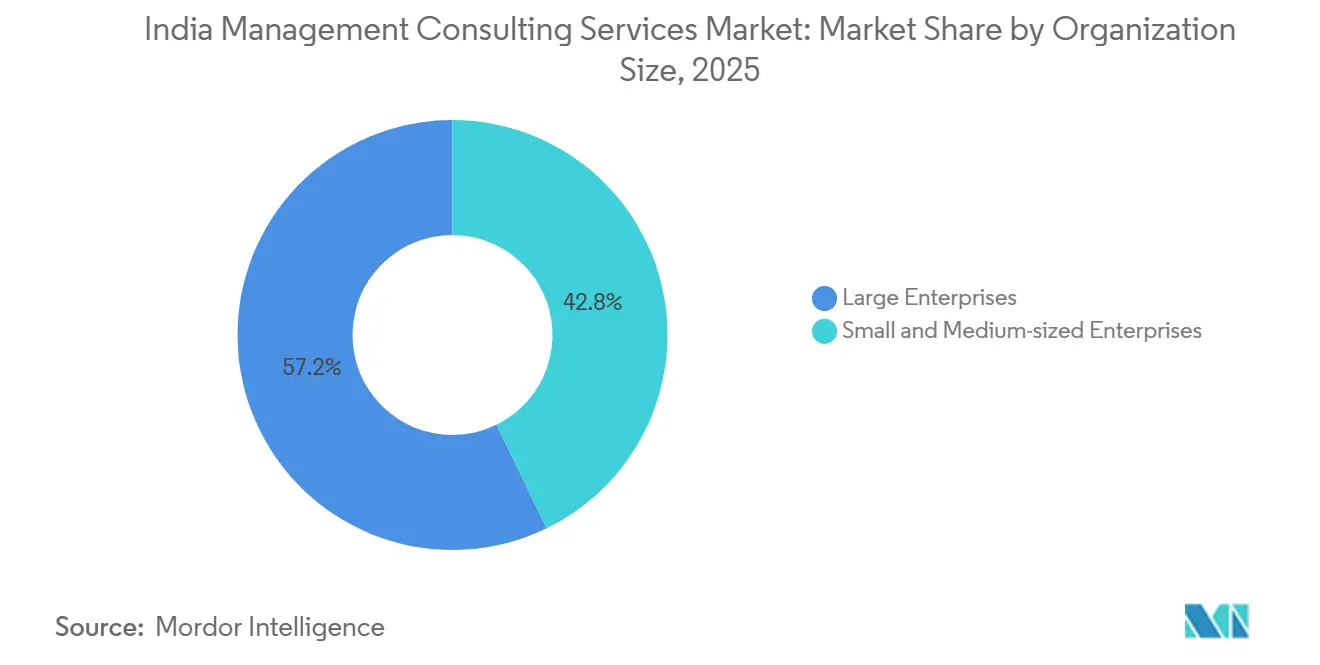

- By organization size, large enterprises led with 57% revenue share in 2025, while SMEs are forecast to advance at a 13.30% CAGR through 2031.

- By service type, strategy consulting commanded 31.50% of the India management consulting services market share in 2025, whereas technology consulting is projected to grow at a 12.96% CAGR to 2031.

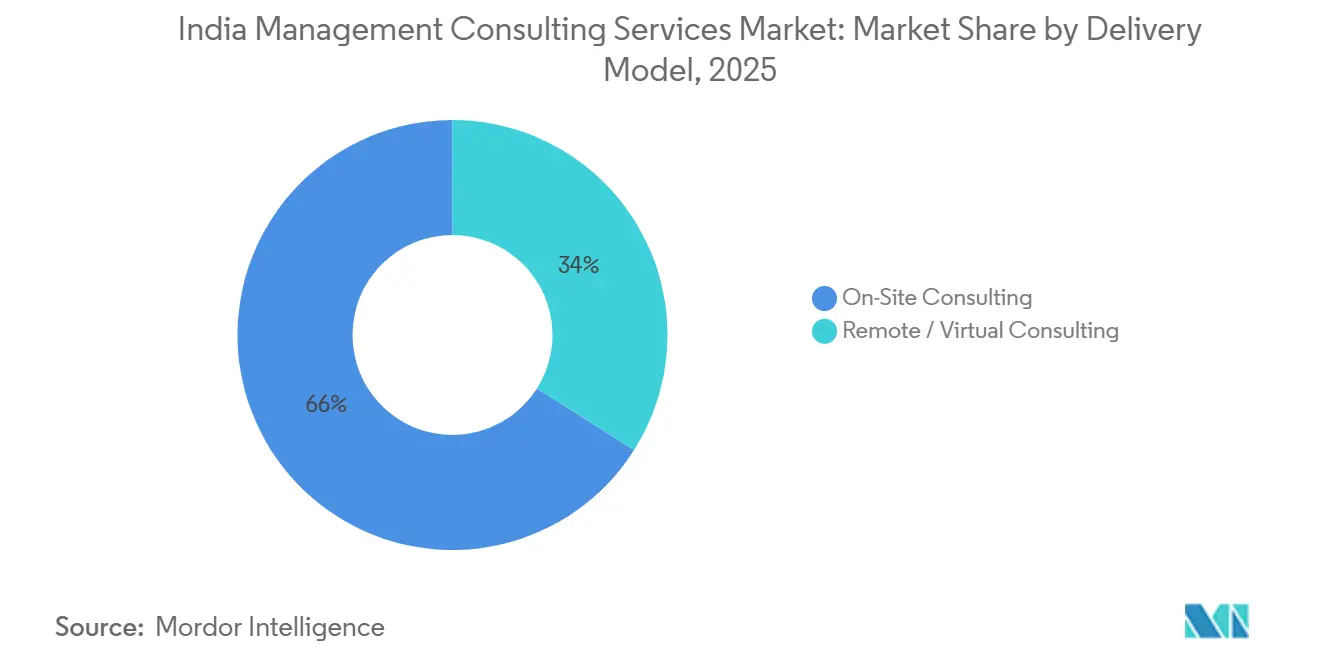

- By delivery model, on-site consulting accounted for 62% of the India management consulting services market size in 2025, but remote or virtual consulting is projected to expand at a 13.42% CAGR between 2026 and 2031.

- By end-user industry, IT and telecommunications controlled 18.20% share in 2025, yet healthcare and life sciences are advancing at a 13.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Digital-Transformation Spend by Large Indian Corporates | +2.80% | National, concentrated in Mumbai, Bengaluru, Delhi NCR, Hyderabad | Medium term (2-4 years) |

| Mandatory ESG-Reporting Advisory Needs Post-SEBI BRSR Rollout | +1.90% | National, with early compliance in top 1,000 listed entities | Short term (≤ 2 years) |

| Rise of GCCs Demanding Hybrid Consulting Engagements | +2.30% | Bengaluru, Hyderabad, Pune, Chennai, Gurugram | Medium term (2-4 years) |

| Rapid VC-Backed SME Scaling Requiring Growth-Strategy Consulting | +1.60% | Tier-1 and Tier-2 cities with startup ecosystems | Short term (≤ 2 years) |

| Corporate Succession Planning Amidst Generational Transitions | +1.20% | National, with concentration in family-owned conglomerates | Long term (≥ 4 years) |

| Demand for Deal-Ready Operational Turnaround Playbooks | +1.40% | National, aligned with IBC case admissions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Digital-Transformation Spend by Large Indian Corporates

Boards approved USD 110 billion of digital-initiative budgets in fiscal 2025, 15% higher than the prior year, prioritizing cloud migration, data-platform consolidation, and omnichannel customer journeys. Finance leaders embedded predictive analytics into forecasting cycles, supply-chain chiefs deployed real-time visibility tools, and human-resources functions automated hiring workflows to support growth at scale. KPMG’s 2025 CEO Outlook found 72% of Indian chief executives planning double-digit annual technology budget increases through 2027, keeping consultants on retainer for change-management and process-reengineering mandates. Continuous-transformation programs are replacing one-off IT implementations, lengthening engagement tenures and deepening consultant integration inside client operations. Generative-AI pilots compound complexity, as only 18% of projects reached production scale in 2025, underscoring the need for advisory guidance on governance, talent reskilling, and data readiness.

Mandatory ESG-Reporting Advisory Needs Post-SEBI BRSR Rollout

The Securities and Exchange Board of India imposed Business Responsibility and Sustainability Reporting on the top 1,000 listed companies starting fiscal 2023, adding quantitative disclosure obligations across nine principles and 46 indicators. By fiscal 2025, more than 1,200 entities were subject to BRSR Core assurance, creating immediate demand for materiality assessments, Scope 3 emissions modeling, and supply-chain human-rights due diligence. Penalties for non-compliance and mandatory third-party assurance pushed companies to hire consultants with carbon-accounting and water-footprint expertise. EY recorded a 40% year-on-year rise in BRSR engagements during 2025, with average contract values between USD 150,000 and USD 500,000. Banks and investors added ESG clauses to lending covenants, pressuring mid-market borrowers to secure advisory support to maintain credit access.

Rise of GCCs Demanding Hybrid Consulting Engagements

India hosted 1,580 GCCs employing 1.66 million professionals in 2024, and 40% of recent mandates cover advanced engineering and analytics. Multinationals establishing GCCs commission market-entry studies, talent-acquisition blueprints, and operating-model designs that link onshore governance to offshore execution. Deloitte reported 65% of surveyed GCCs planning to expand Indian headcount by more than 20% within three years, with consultant spend focused on capability-maturity mapping and stack rationalization. Hybrid engagement structures, where strategy workshops occur at headquarters and remote teams deliver analytics from Indian delivery centers, reduce client cost yet broaden engagement lifecycles.

Rapid VC-Backed SME Scaling Requiring Growth-Strategy Consulting

Startups secured USD 11.3 billion across 1,217 deals in 2024, with 68% flowing into Series A and later rounds where governance and go-to-market precision outweigh growth-at-any-cost. Venture investors mandate external advisors for market-sizing, unit-economics validation, and pre-IPO readiness. Founders typically commission eight-to-twelve-week projects priced at USD 50,000-200,000, sometimes swapping equity kickers for fees. As the funding winter pivoted focus toward profitability, demand for operational-turnaround playbooks and cash-burn control accelerated, presenting opportunities for boutique consultancies fluent in startup culture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Pricing Pressure from IT Services Majors | -1.80% | National, most acute in mid-market segments | Short term (≤ 2 years) |

| Talent Attrition to Product-Management and VC Ecosystem | -1.30% | Bengaluru, Mumbai, Delhi NCR | Medium term (2-4 years) |

| Growing Client Preference for Outcome-Based Fee Structures | -0.90% | National, concentrated in venture-backed firms | Medium term (2-4 years) |

| AI-Led Self-Service Diagnostics Reducing Basic Consulting Demand | -1.10% | National, affecting entry-level engagements | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Pricing Pressure from IT Services Majors

Tata Consultancy Services, Infosys, and Wipro embed consulting in multi-year transformation deals, leveraging delivery-center scale to undercut pure-play firms by 20-30%. TCS Interactive, Infosys Consulting, and Wipro Consulting each posted double-digit 2025 revenue growth, with typical contracts ranging between USD 2 million and USD 10 million. Bundled offerings spanning strategy, implementation, and managed services appeal to chief information officers seeking single-vendor accountability, forcing independent consultancies to migrate either up-stream into board-level advisory or down-stream into execution, both of which compress margins.

Talent Attrition to Product-Management and VC Ecosystem

Mid-career consultants capture 30-40% pay premiums by moving into product management positions or venture capital associate roles that offer equity upside. Attrition climbed to 22-25% in 2025, particularly among high-performers. The exodus shrinks bench depth, inflates recruitment cost, and accelerates junior staff promotion, which can dilute client-delivery quality. Firms respond with deferred compensation, secondments, and profit-sharing, adding 8-12% to overheads in an already price-sensitive market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: SMEs Move From Fringe to Growth Engine

The India management consulting services market size for SMEs is projected to accelerate at 13.30% CAGR during 2026-2031, outpacing the overall industry. Venture capitalists insist on robust governance and unit economics clarity before releasing funds, while digital-native founders often lack process expertise. Engagements typically concentrate on commercial-excellence playbooks, pricing architecture, and capital-efficiency dashboards, with consultants accepting milestone-linked equity for fees, aligning incentives across parties. Government schemes such as Startup India reimburse part of advisory spend, further lowering entry barriers.

Large enterprises maintained 57% revenue in 2025 by funding multi-million-dollar transformation roadmaps covering cloud strategy, ESG reporting, and post-merger integration. However, their growth moderates as internal strategy units absorb routine work and captive centers manage operational rollouts. Clients still rely on external advisers for board-level decisions, but consultants must articulate proprietary frameworks and change-management credentials to protect fee premium. Over the forecast horizon, SMEs provide the faster-growing book, but large corporations remain essential for scale and marquee references.

By Service Type: Technology Consulting Becomes Strategy in Action

Strategy consulting controlled 31.50% of the India management consulting services market share in 2025, yet technology consulting is forecast at 12.96% CAGR, reflecting that architectural choices now determine competitive advantage. Generative-AI pilots, cloud-native stacks, and zero-trust security frameworks demand cross-disciplinary teams that fuse industry insight with engineering fluency. Advisory firms consequently bundle market-entry analyses with data-governance roadmaps and workforce-reskilling plans, illustrating the dissolution of neat service silos.

Operations consulting stays resilient as manufacturers incorporate lean programs and supply-chain risk mapping. HR consulting gains traction from succession planning and GCC talent-war challenges. Other service types, risk, compliance, and sustainability, ride the BRSR mandate, with PwC and EY reporting 40% year-on-year ESG-related revenue growth in 2025. Overall, clients increasingly judge proposals on integrated capabilities rather than legacy service labels, forcing consultancies to orchestrate multidisciplinary delivery squads.

By Delivery Model: Remote Finds Its Equilibrium with Hybrid

On-site engagements preserved 62% revenue in 2025 because discovery workshops and politically sensitive decisions favor in-person interaction. Yet remote consulting is set for a 13.42% CAGR as clients accept distributed teams to trim travel expenditure and compress timelines. Consultants leverage virtual whiteboards, code-sharing platforms, and always-on communication channels to run parallel workstreams that would previously require sequential on-site sprints. The hybrid norm is stabilizing at two to three in-person visits per month, supplemented by daily virtual stand-ups.

Remote delivery also opens the national talent pool, allowing firms to deploy subject-matter experts from lower-cost cities without relocation. Consultants can carry simultaneous projects, boosting utilization but demanding stringent engagement-management discipline to protect quality. Clients remain cautious of remote-only setups for culture-change programs and executive coaching, signaling that physical presence still signals commitment where emotions and power dynamics run high.

By End-User Industry: Healthcare and Life Sciences Ascend the Growth Ladder

Healthcare and life sciences lead the growth league at 13.88% CAGR through 2031, powered by localized clinical trials, biosimilar regulatory tracks, and hospital-chain consolidation. Consultants orchestrate site-selection analytics, Central Drugs Standard Control Organisation dossier preparation, and digital patient-recruitment strategies. Multinationals redirecting trials from China leverage India’s cost and genetic diversity advantages, putting pressure on advisory teams to compress study timelines without compromising compliance.

IT and telecommunications commanded 18.20% revenue in 2025, reflecting relentless digital-transformation cycles. Growth moderates as technology players mature and insource some capability, yet GCC expansion keeps advisory pipelines healthy. BFSI clients seek guidance on open-API frameworks, neo-bank launches, and Reserve Bank cloud-security guidelines, ensuring a steady stream of regulatory-driven projects. Manufacturing, energy, government, real estate, retail, media, and hospitality segments each present cyclical opportunities aligned with policy incentives, capital markets, and consumer sentiment swings.

Geography Analysis

Demand maps closely to Tier-1 metros Mumbai, Bengaluru, Delhi NCR, Hyderabad, Pune, and Chennai contributing roughly 75% of 2025 revenue. Mumbai’s dominance in financial-services advisory rests on its concentration of banks, insurers, and capital-markets firms. Bengaluru remains the technology-consulting epicenter, hosting over 450 GCCs and serving as the innovation lab for global software majors. Delhi NCR channels government and public-sector engagements because of proximity to federal ministries, while Hyderabad and Pune cater to pharmaceutical and automotive clusters requiring supply-chain optimization.

Tier-2 cities such as Ahmedabad, Jaipur, Kochi, Coimbatore, and Visakhapatnam are forecast to grow two to three points faster than the national average as state governments champion smart-city initiatives and regional conglomerates professionalize. Infrastructure improvements, dedicated freight corridors, and upgraded airports reduce logistical friction, yet limited consultant talent supply keeps fee benchmarks marginally below metro rates. Advisory firms often rotate staff on short stints or offer location premiums to seed local practices.

Cross-border mandates remain nascent less than 5% of 2025 billings but are rising as Indian consultancies open Southeast Asian and Middle Eastern offices to export India-centric expertise. Zinnov’s Dubai hub and RedSeer’s Southeast Asia expansion illustrate the ambition to reposition India as a knowledge-export node rather than solely a cost-arbitrage site.

Competitive Landscape

The India management consulting services market features moderate fragmentation. The top ten firms McKinsey, Boston Consulting Group, Bain, Deloitte, PwC, EY, KPMG, Tata Consultancy Services, Infosys, and Wipro held an estimated 45-50% revenue in 2025, leaving room for sector-focused boutiques. Pricing pressure is fiercest in the USD 100 million-1 billion revenue band where clients trade brand pedigree for cost certainty, accepting outcome-based fee clauses that tie remuneration to realized value.

Global strategy houses protect premium positioning by maintaining low partner leverage and deploying proprietary diagnostic assets. Their challenge is retaining mid-level talent drawn to product-management opportunities promising equity and decision autonomy. Big Four advisory arms cross-sell from audit relationships and invest in sector-specific centers of excellence, while IT majors bundle consulting into digital-transformation programs, using delivery-center scale to offer integrated roadmaps from strategy through managed services.

White-space opportunities cluster around BRSR compliance, operational-turnaround playbooks for Insolvency and Bankruptcy Code cases, and succession planning for family-owned conglomerates. Boutiques such as Zinnov (engineering R and D), RedSeer (consumer analytics), and Technopak (retail supply-chain) win projects by offering founder-led engagements and deep domain knowledge. Technology investment is redefining cost curves: Accenture alone invested more than USD 1 billion in AI and cloud tools in fiscal 2025, and early adopters report 10-15% project-delivery cost reduction from generative-AI knowledge-management systems.

India Management Consulting Services Industry Leaders

McKinsey & Company Inc.

Boston Consulting Group Inc.

Deloitte Touche Tohmatsu India LLP

PricewaterhouseCoopers Services LLP

Accenture Solutions Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Deloitte India launched a Generative-AI Center of Excellence in Bengaluru, pledging USD 50 million across three years and hiring 500 specialists.

- December 2025: PwC India acquired a minority stake in Praxis Global Alliance to strengthen growth-strategy and digital-transformation offerings for mid-market clients.

- November 2025: Infosys Consulting partnered with the Confederation of Indian Industry to release a subsidized BRSR compliance toolkit for small-cap listed companies.

- October 2025: McKinsey opened its seventh Indian office in Pune, focusing on automotive and industrial manufacturing clients with plans to hire 200 consultants.

India Management Consulting Services Market Report Scope

The India Management Consulting Services Market Report is Segmented by Organization Size (Large Enterprises, Small and Medium-Sized Enterprises), Service Type (Strategy Consulting, Operations Consulting, HR Consulting, Technology Consulting, Other Service Types), Delivery Model (On-Site Consulting, Remote/Virtual Consulting), End-User Industry (IT and Telecommunications, Healthcare and Life Sciences, Financial Services, Manufacturing and Industrial, Energy and Utilities, Government and Public Sector, Real Estate and Construction, Retail and Consumer Goods, Media Entertainment and Sports, Hospitality and Travel, Other End-User Industries), and Geography (India). The Market Forecasts are Provided in Terms of Value (USD).

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Technology Consulting |

| Other Service Types |

| On-Site Consulting |

| Remote / Virtual Consulting |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Financial Services (BFSI) |

| Manufacturing and Industrial |

| Energy and Utilities |

| Government and Public Sector |

| Real Estate and Construction |

| Retail and Consumer Goods |

| Media, Entertainment and Sports |

| Hospitality and Travel |

| Other End-User Industries |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Service Type | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Technology Consulting | |

| Other Service Types | |

| By Delivery Model | On-Site Consulting |

| Remote / Virtual Consulting | |

| By End-User Industry | IT and Telecommunications |

| Healthcare and Life Sciences | |

| Financial Services (BFSI) | |

| Manufacturing and Industrial | |

| Energy and Utilities | |

| Government and Public Sector | |

| Real Estate and Construction | |

| Retail and Consumer Goods | |

| Media, Entertainment and Sports | |

| Hospitality and Travel | |

| Other End-User Industries |

Key Questions Answered in the Report

What revenue trajectory is forecast for the India management consulting services market between 2026 and 2031?

The market is projected to rise from USD 9.36 billion in 2026 to USD 17.01 billion by 2031, reflecting a 12.69% CAGR.

Which client segment shows the fastest consulting-spend growth in India?

SMEs are expected to grow consulting spend at 13.30% CAGR through 2031, outpacing large enterprises.

Which service line is expanding quickest within consulting engagements?

Technology consulting is projected to grow at 12.96% CAGR as companies integrate cloud and generative-AI architectures.

Why is healthcare a high-growth end-user vertical for consultants?

Clinical-trial localization, biosimilar pathways, and hospital-chain consolidation are driving a 13.88% CAGR in healthcare-related consulting demand.

How are delivery models shifting post-pandemic?

Hybrid structures combining limited on-site visits with virtual delivery are becoming standard, enabling remote consulting to grow at 13.42% CAGR.

What is the main pricing pressure on traditional consultancies?

Integrated IT services majors bundle strategy with implementation, undercutting standalone firms by up to 30% on comparable engagements.

Page last updated on: