Norway Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

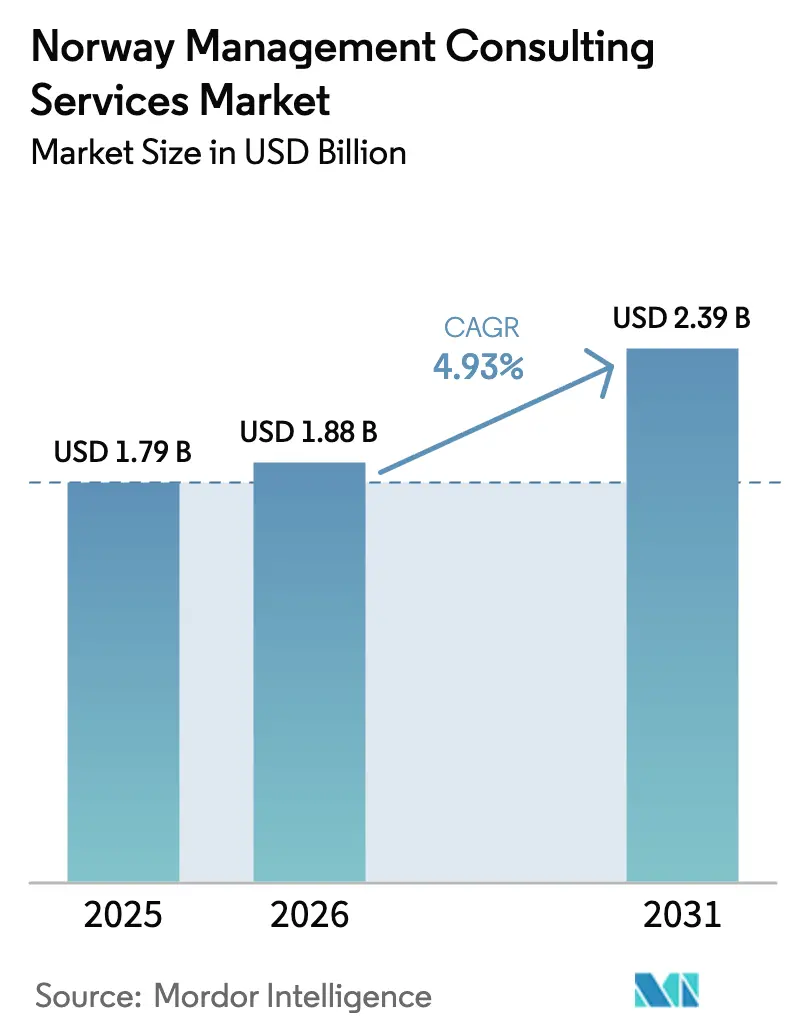

| Base Year Market Size (2025) | USD 1.79 Billion |

| Market Size (2026) | USD 1.88 Billion |

| Market Size (2031) | USD 2.39 Billion |

| Growth Rate (2026 - 2031) | 4.93% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Norway Management Consulting Services Market Analysis by Mordor Intelligence

The Norway management consulting services market size was valued at USD 1.79 billion in 2025 and estimated to grow from USD 1.88 billion in 2026 to reach USD 2.39 billion by 2031, at a CAGR of 4.93% during the forecast period (2026-2031). Norway’s push to become a digital-first economy, mandatory sustainability disclosures under EU rules, and heightened private-equity deal flow are the primary growth engines. Large enterprises continue to invest heavily in enterprise-wide transformation, yet small and medium-sized firms are accelerating spending as public funding programs lower the entry barrier to expert advice. Technology consulting is expanding faster than traditional operations work because public bodies plan for 80% AI adoption by 2025, creating multi-year implementation projects. Simultaneously, ESG mandates trigger sustained demand for strategy and reporting guidance, while outsourced expertise remains critical because domestic talent gaps persist across data, AI, and cybersecurity roles.

Key Report Takeaways

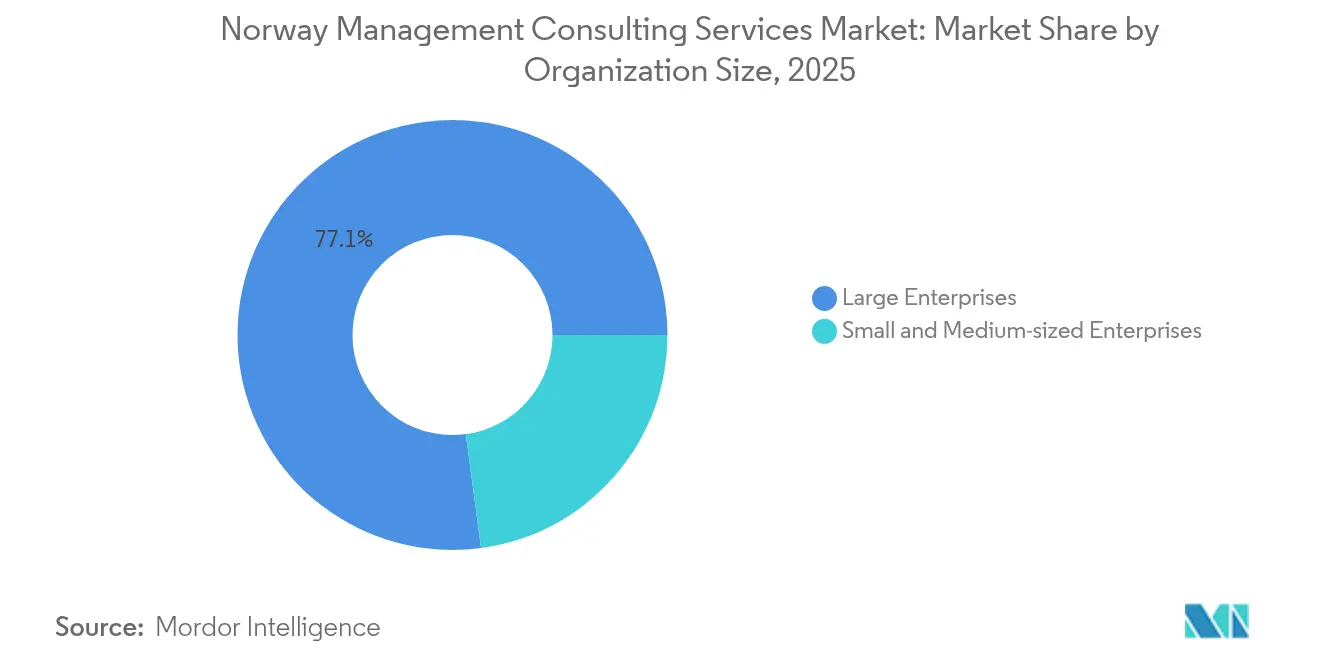

- By organization size, large enterprises held 77.12% of Norway management consulting services market share in 2025; small and medium-sized enterprises are advancing at a 5.41% CAGR to 2031.

- By service type, operations consulting led with 32.85% revenue share in 2025, while technology consulting is projected to expand at a 5.63% CAGR through 2031.

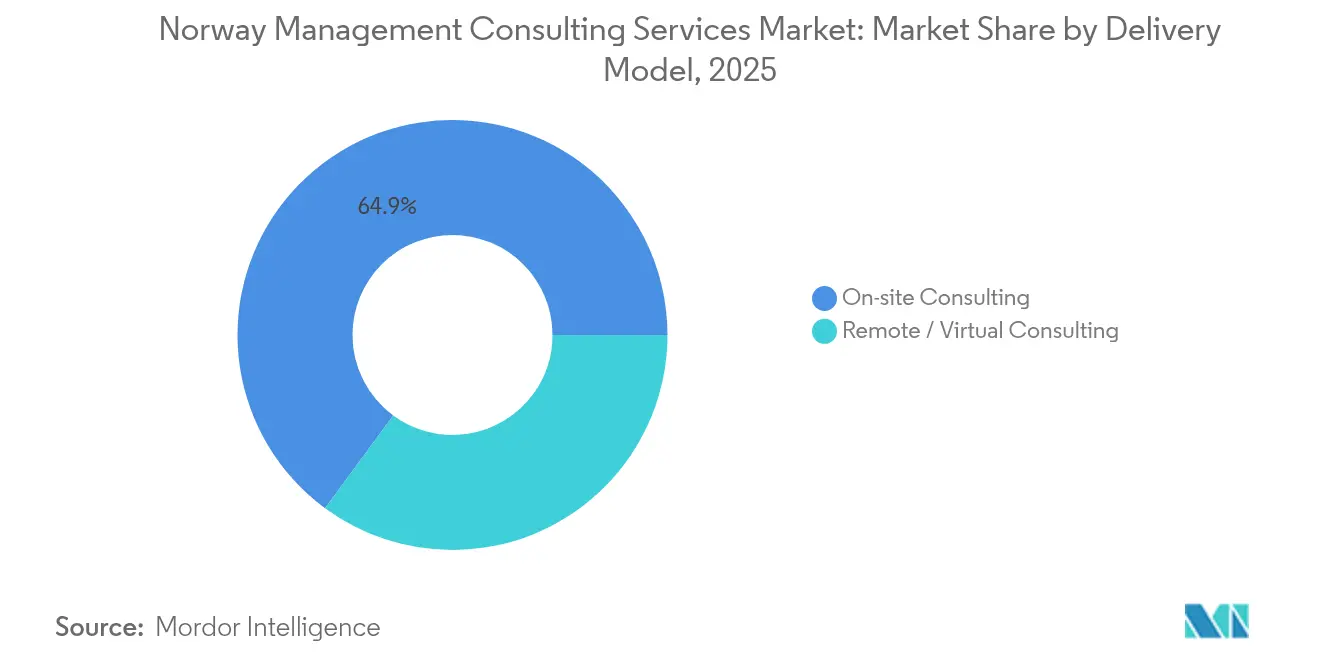

- By delivery model, on-site engagements commanded 64.90% of the Norway management consulting services market size in 2025; remote and virtual delivery is growing at a 5.45% CAGR between 2026-2031.

- By end-user industry, financial services accounted for 26.21% share of the Norway management consulting services market size in 2025; healthcare and life sciences is the fastest-growing vertical at a 5.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Norway Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-first transformation programmes | +1.2% | Oslo, Bergen and national roll-outs | Medium term (2-4 years) |

| Mandatory ESG and EU-taxonomy reporting | +0.9% | Nationwide | Short term (≤ 2 years) |

| Outsourced expertise to close talent gaps | +0.8% | Nationwide, tech and engineering clusters | Long term (≥ 4 years) |

| M&A and private-equity deal flow | +0.7% | Oslo financial district | Medium term (2-4 years) |

| Public-sector “Digital Norway” megaprojects | +0.6% | National with regional pilots | Long term (≥ 4 years) |

| NBIM stewardship push for sustainability | +0.5% | Global portfolio, Norway-based coordination | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital-first transformation programmes across Norwegian industry

Government strategy targets the world’s most digital public sector by 2030, underpinning NOK 1.1 billion of funding for entrepreneurship and advanced technologies. Enterprises mirror that ambition: Telenor’s AI factory signals private-sector acceleration and spurs advisory demand for architecture design, change-management and data governance. The Directorate of Health’s revamp of citizen-facing platforms generated 2.25 million monthly visits and demonstrated the complexity of large-scale system integration. Consulting firms gain because many organisations lack in-house capabilities to orchestrate cloud, AI and cybersecurity roadmaps at the required pace. As additional ministries adopt similar digitisation blueprints, sustained fee pools emerge across infrastructure, process re-engineering and vendor selection.

Mandatory ESG and EU-taxonomy reporting deadlines

The Corporate Sustainability Reporting Directive (CSRD) obliges thousands of Norwegian companies to publish granular climate and social metrics from 2024 filings. [1]European Commission, “Corporate Sustainability Reporting Directive,” europa.euSeventy-nine percent of large corporations already referenced climate issues in 2023 reports, up from 50% two years earlier, highlighting the steep learning curve. NBIM reinforces the momentum by insisting its NOK 19.7 trillion portfolio achieve net-zero emissions by 2050. Firms now turn to consultants for double-materiality analyses, taxonomy alignment and audit-ready data processes. The Norwegian Transparency Act adds parallel human-rights due-diligence duties, widening the compliance perimeter. Continuous revisions to EU guidance mean ESG advisory remains a recurring, not one-off, revenue stream.

Outsourced expertise to close domestic talent gaps

Norway registers Europe’s widest mismatch between job vacancies and available skills, especially for software, AI and engineering roles. [2]Norges Bank Investment Management, “Climate Action Plan 2024,” nbim.no More than 16,000 developer positions were open at the start of 2025, while offshore energy expects 3,000 retirements by 2028. Average salary jumps of 5.6% and specialist pay scales exceeding NOK 1.4 million for AI architects inflate delivery costs. Corporates therefore prefer project-based consultants who carry ready-made teams and can exit once targets are hit. For advisory firms, the chronic gap translates into resilient utilisation rates and pricing opportunities in high-skill niches such as data science, zero-trust cyber and industrial automation.

M&A and private-equity deal flow requiring advisory

Transaction volume climbed 20% year-on-year to 862 deals in 2024, supported by lower interest rates and cash-rich funds. Private equity accounted for almost one-third of activity, concentrating on software and construction roll-ups that demand commercial, IT and operational due-diligence. Cross-border complexity escalated as Norwegian buyers pursued regional expansion, illustrated by a leading bank’s SEK 12 billion purchase of a Swedish asset manager. Integration planning, synergy verification and post-merger cultural alignment form an expanding pipeline for consultants specialised in finance, HR and digital integration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising fee pressure and service commoditisation | −0.8% | Nationwide, standardised offerings | Short term (≤ 2 years) |

| Wage inflation and talent retention challenges | −0.6% | Oslo and Bergen tech hubs | Medium term (2-4 years) |

| Oil-and-gas cyclicality dampening spend | −0.4% | Stavanger and Bergen | Medium term (2-4 years) |

| Stricter conflict-of-interest regulations | −0.3% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising fee pressure and service commoditisation

Clients have become price-sensitive as routine deliverables—process mapping, PMO support, basic ERP configuration—are perceived as interchangeable. Public agencies launched panels that award work primarily on lowest-cost criteria, pushing average day-rates down by 8% between 2023 and 2025. [3]Statistics Norway, “Salary Growth 2024–2025,” ssb.no Private corporates likewise insource standard IT support once internal capabilities mature. To protect margins, consulting firms bundle proprietary analytics tools and outcome-based pricing, yet continuous rate erosion in commoditised segments remains a headwind.

Wage inflation and talent retention challenges

Average personnel costs rose 5.6% in 2024 and specialist technology salaries climbed even faster, eroding operating margins in people-intensive business models. The scarcity of senior cloud engineers and data scientists fuels bidding wars among employers. Voluntary turnover at tier-one consultancies exceeded 19% in 2024 as staff pursued equity-linked packages in scale-ups. Firms are forced to invest in automation of low-value tasks, near-shore delivery centres and revamped career paths to offset escalating payroll and retention bonuses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: Enterprise Dominance Drives Market Scale

Large enterprises generated 77.12% of the Norway management consulting services market in 2025, reflecting multi-year transformation budgets spanning digital banking, procurement overhauls and global ESG compliance. Equinor alone channelled NOK 142.6 billion of procurement through Norwegian suppliers, creating system-integration and supplier-development assignments. DNB’s branch-light operating model triggered data-management and omnichannel consulting programmes that reduced over-the-counter transactions by 82%.

Small and medium-sized companies are expanding engagement volumes at a 5.41% CAGR as simplified grant schemes and cloud solutions cut adoption barriers. The government’s NOK 1.1 billion entrepreneurship package funds advisory vouchers, while digital accounting and e-invoicing mandates encourage SMEs to seek process-optimisation guidance. As a result, consultants increasingly design fixed-price, modular offerings to match SME budget cycles, driving incremental revenue yet adding scale complexity for service providers.

By Service Type: Operations Leadership Meets Technology Acceleration

Operations consulting retained a 32.85% revenue share in 2025 due to Norway’s high-cost environment, which motivates efficiency projects across energy, consumer goods and public services. However, technology consulting is the fastest mover with a 5.63% CAGR to 2031 because ministries aim for 80% public-sector AI uptake, and private boards prioritise data-driven decision-making. Specialist AI and cloud advisory frequently pairs with cyber-resilience mandates as organisations adopt zero-trust architectures.

Strategy and HR consulting maintain mid-single-digit growth rates. Sustainability road-mapping dominates board agendas after the CSRD, pushing demand for decarbonisation playbooks and taxonomy alignment. On the people side, integrated talent-analytics and workforce-planning engagements gain traction as companies search for ways to narrow chronic skills gaps and manage wage inflation.

By Delivery Model: Remote Consulting Gains Strategic Momentum

On-site delivery still covers 64.90% of 2025 spend because complex stakeholder workshops, regulatory inspections and sensitive data sets require physical presence. Yet remote engagements are growing at a 5.45% CAGR on the back of ubiquitous fibre coverage and client familiarity with collaborative platforms. Firms leverage virtual toolkits—digital whiteboards, AI-driven transcription and secure sandbox environments—to reduce travel costs and accelerate sprint cycles.

Hybrid models now dominate technology sprints: core architects operate remotely, while local teams handle change-management and stakeholder alignment. This dual approach helps consultancies tap scarce global expertise without breaching data-residency rules. As Norway upgrades national cloud infrastructure, the addressable pool for remote experts will rise further, especially for niche domains such as quantum security and advanced predictive maintenance.

By End-user Industry: Financial Services Leadership Amid Healthcare Emergence

Financial institutions contributed 26.21% of the Norway management consulting services market size in 2025, driven by open-banking roll-outs, Treasury platform modernisation and stringent anti-money-laundering frameworks. Meanwhile, the healthcare and life-sciences vertical is projected to expand at 5.18% CAGR because Norway leads Europe in tele-consultation penetration and is piloting AI-supported radiology at national scale.

Energy and utilities engagements focus on green-transition road-maps as operators target net-zero commitments. Manufacturing clients demand automation and circular-economy redesigns to satisfy export-market buyers. Retailers upgrade supply-chain visibility and in-store payment systems to lift resilience and reduce carbon footprints. Cross-sector ESG, cyber and data-analytics themes underpin consulting revenue diversity.

Geography Analysis

Consulting revenue is concentrated in Oslo, which hosts the bulk of corporate headquarters, financial regulators and technology start-ups. Bergen follows, buoyed by energy majors and a thriving aquaculture cluster. Stavanger remains a core market despite oil price swings because operators are retrofitting assets for carbon capture and offshore wind.

Northern counties are emerging hotspots due to critical-minerals exploration and defence-industry expansion supported by government incentives. The Norwegian coastline presents growing opportunities tied to maritime digitalisation and green shipping corridors. Remote municipalities tap national grants to implement cloud-based citizen services, broadening regional demand for project-management and cyber-security expertise.

Overall, urban hubs will continue to dominate value, yet regional infrastructure spending ensures consulting penetration spreads, supporting inclusive growth for the Norway management consulting services market.

Competitive Landscape

The field is moderately fragmented. Global “Big Four” and strategy specialists capture high-value mandates in finance, energy transition and national digitalisation. Nordic-anchored firms leverage cultural proximity and language fluency to secure public-sector frameworks. Niche boutiques specialising in AI, cyber or ESG advisory exhibit double-digit growth, although scaling beyond 200 consultants remains challenging.

Consolidation is visible in technology consulting. Recent mergers create entities exceeding USD 1 billion in sales, enabling end-to-end cloud and licensing propositions. Price competition intensifies in commoditised segments; firms defend yields through proprietary accelerators and managed-service wraps. Talent scarcity forces heavy investment in internal academies and near-shore centres.

Opportunities arise in cross-border M&A integration, data-governance outsourcing and green industrial-strategy formulation. Firms able to combine sector depth with digital accelerators are best placed to win multi-year transformation frameworks across Norway management consulting services market clients.

Norway Management Consulting Services Industry Leaders

Accenture AS

PricewaterhouseCoopers AS

Ernst & Young AS

Deloitte AS

KPMG AS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Japan’s Mitsubishi acquired salmon assets in Norway and Canada, signalling consulting needs in cross-border integration and aquaculture growth.

- May 2025: Naval Group and Akkodis signed a letter of intent tied to Norway’s future frigate program, opening defence-sector advisory work.

- April 2025: Equinor confirmed NOK 142.6 billion of Norwegian procurement, underpinning supplier-development consulting pipelines.

- October 2024: Norway’s largest bank agreed to purchase a Swedish peer for USD 1.14 billion, adding post-merger integration mandates.

Norway Management Consulting Services Market Report Scope

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Technology Consulting |

| Other Service Types |

| On-site Consulting |

| Remote / Virtual Consulting |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Financial Services (BFSI) |

| Manufacturing and Industrial |

| Energy and Utilities |

| Government and Public Sector |

| Real Estate and Construction |

| Retail and Consumer Goods |

| Media, Entertainment and Sports |

| Hospitality and Travel |

| Other End-User Industries |

| By Organization Size | Large Enterprises |

| Small and Medium-sized Enterprises | |

| By Service Type | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Technology Consulting | |

| Other Service Types | |

| By Delivery Model | On-site Consulting |

| Remote / Virtual Consulting | |

| By End-user Industry | IT and Telecommunications |

| Healthcare and Life Sciences | |

| Financial Services (BFSI) | |

| Manufacturing and Industrial | |

| Energy and Utilities | |

| Government and Public Sector | |

| Real Estate and Construction | |

| Retail and Consumer Goods | |

| Media, Entertainment and Sports | |

| Hospitality and Travel | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current value of the Norway management consulting services market?

The market is valued at USD 1.88 billion in 2026.

Which segment of the Norway management consulting services market is growing the fastest?

Technology consulting is expanding at a 5.63% CAGR due to nationwide AI adoption targets.

How significant are ESG regulations for consulting demand in Norway?

Mandatory CSRD and the national Transparency Act are adding 0.9 percentage points to forecast CAGR, making ESG advisory a recurring revenue stream.

Why are small and medium-sized enterprises increasing consulting spend?

Simplified grant schemes and digital-first policies help SMEs access expertise once reserved for large corporations, driving a 5.41% CAGR for the segment.

Which geography within Norway shows the highest consulting demand?

Oslo remains the largest hub because it hosts most corporate headquarters and financial institutions.

What challenges threaten profitability for consulting firms operating in Norway?

Rising fee pressure on commoditised services and wage inflation that lifts salary costs by 5.6% annually are the primary headwinds.

Page last updated on: