Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

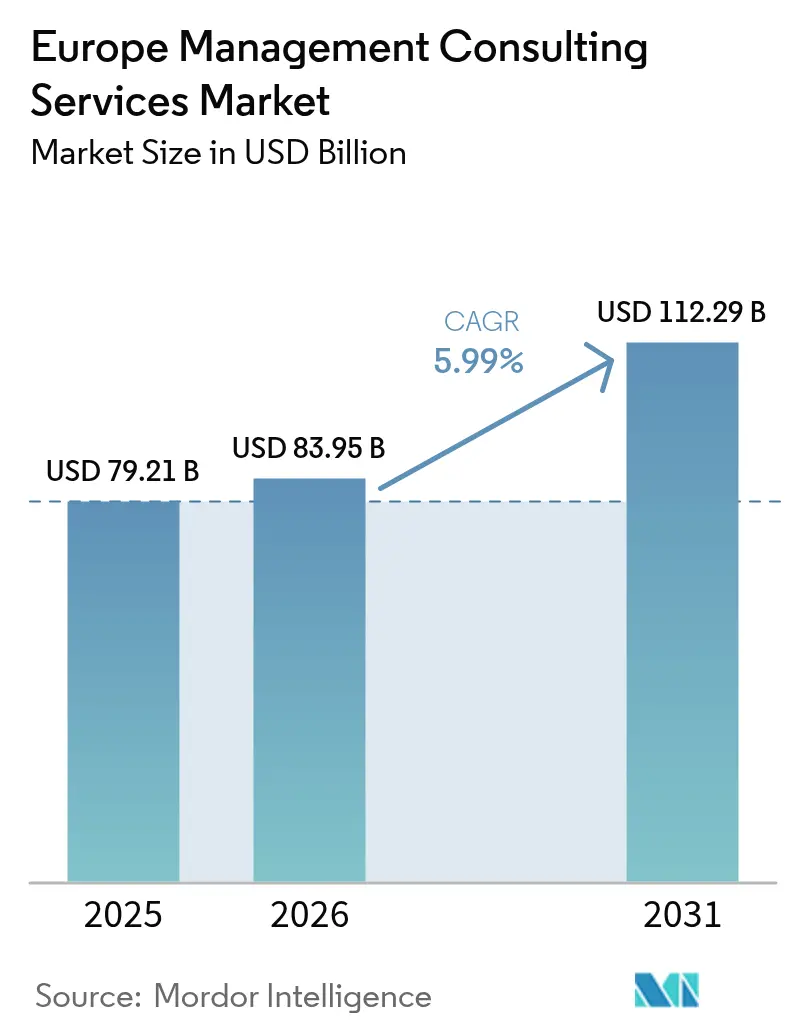

| Base Year Market Size (2025) | USD 79.21 Billion |

| Market Size (2026) | USD 83.95 Billion |

| Market Size (2031) | USD 112.29 Billion |

| Growth Rate (2026 - 2031) | 5.99% CAGR |

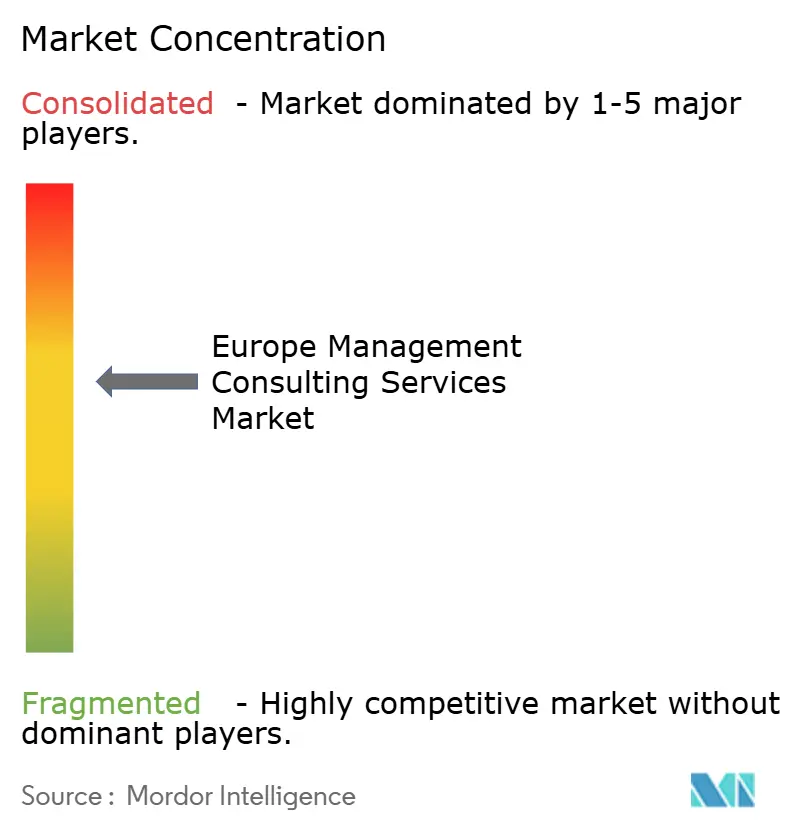

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Management Consulting Services Market Analysis by Mordor Intelligence

Europe management consulting market size in 2026 is estimated at USD 83.95 billion, growing from 2025 value of USD 79.21 billion with 2031 projections showing USD 112.29 billion, growing at 5.99% CAGR over 2026-2031. Surging digital-transformation investments, expanding ESG regulations, and accelerating AI adoption position consulting firms as indispensable partners for strategic realignment and operational efficiency. Operations excellence engagements dominate current spending, yet the rapid scale-up of generative-AI programs is shifting wallet share toward digital and analytics advisory. Regionally, DACH retains leadership on the back of Germany’s strong industrial base, while Central and Eastern Europe (CEE) posts the quickest gains as EU funds flow toward modernization. Competitive intensity is rising as boutique specialists and freelance platforms pressure traditional fee structures, prompting the Big Four to double down on technology ecosystems and outcome-based pricing.

Key Report Takeaways

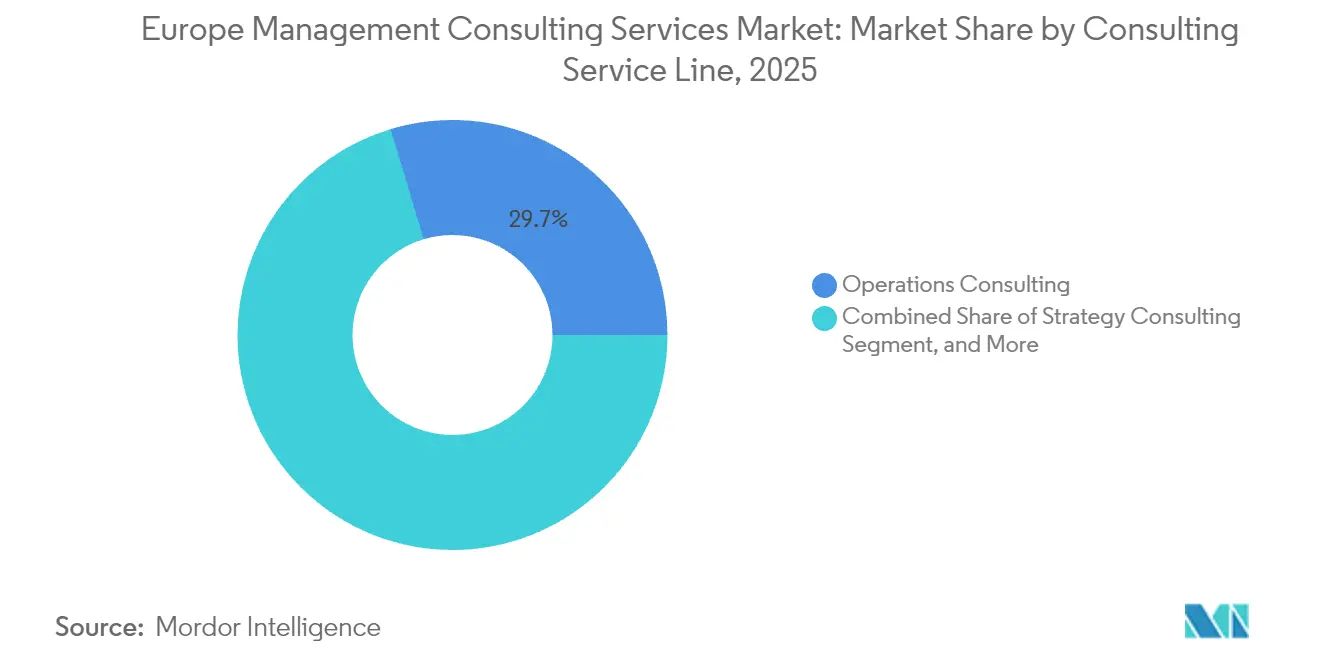

- By consulting service line, Operations Consulting held 29.65% of the Europe management consulting market share in 2025; Digital/AI Consulting is advancing at a 12.29% CAGR through 2031.

- By client industry, Financial Services led with 33.05% share of the Europe management consulting market size in 2025, while Healthcare and Life Sciences posts the fastest 9.92% CAGR to 2031.

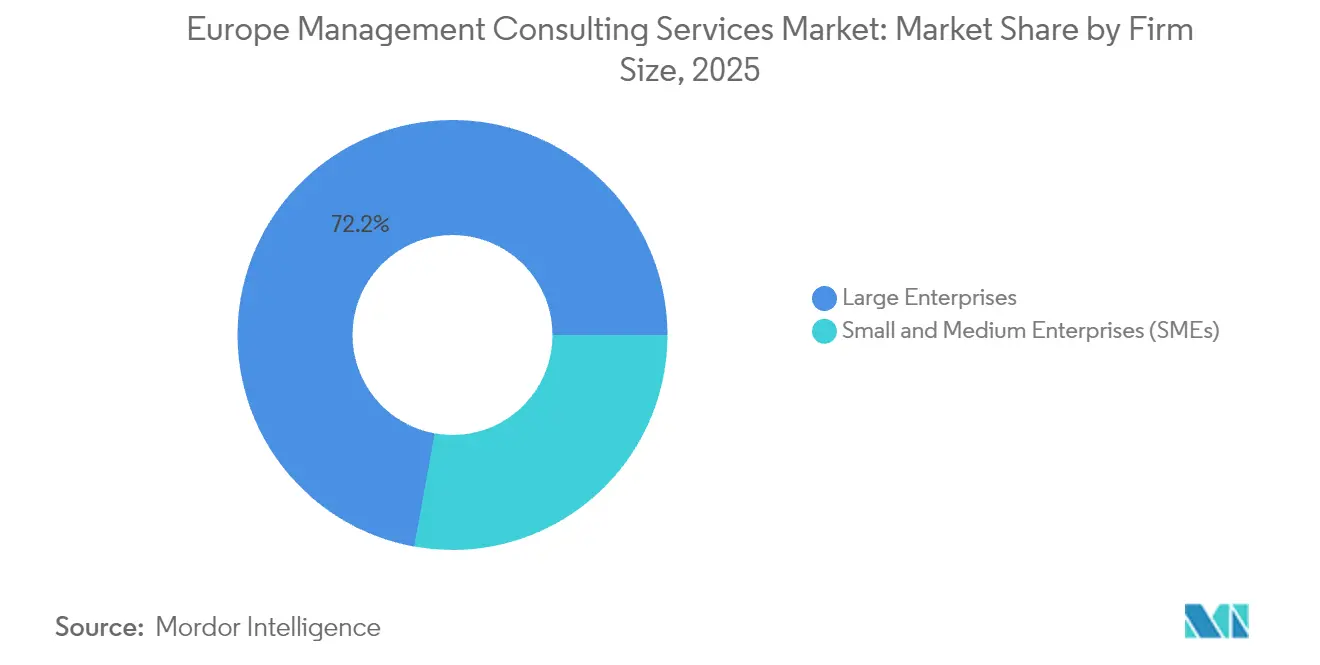

- By firm size, large enterprises accounted for 72.15% of the Europe management consulting market size in 2025, and SMEs are expanding at an 8.33% CAGR on the back of subscription-based models.

- By delivery model, on-site projects captured 57.62 of % Europe management consulting market share in 2025, whereas fully remote delivery recorded the highest 14.71% CAGR to 2031.

- By geography, DACH dominated with 26.28% European management consulting market share in 2025, and CEE is projected to grow at a 7.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in digital-transformation spending | +1.8% | Global; strongest in DACH and UK | Medium term (2-4 years) |

| Escalating demand for advanced analytics and AI | +1.5% | DACH; Nordics; spillover to Southern Europe | Long term (≥ 4 years) |

| ESG-linked regulatory complexity | +1.2% | EU-wide; notable in DACH and France | Medium term (2-4 years) |

| Cyber-security compliance mandates | +1.0% | EU-wide; focus on Financial Services | Short term (≤ 2 years) |

| Subscription-based consulting uptake | +0.8% | UK and DACH; expanding to Southern Europe | Long term (≥ 4 years) |

| SME decarbonization road-maps demand | +0.6% | EU-wide; Nordic leadership | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Digital-Transformation Spending

European companies lifted digital-transformation outlays to USD 1.1 trillion in 2024, up 9% year on year, with software and IT services absorbing most of the budget [1]Cognizant, “Gen AI is taking hold in DACH businesses,” cognizant.com. DACH businesses plan average generative-AI investments of USD 37 million during 2025, yet 71% concede progress is lagging due to talent gaps. Industrial icons such as Fresenius cut SAP administration time by 50% following cloud migration, proving hard ROI to boards. Nordic consultancies, now worth EUR 2.77 billion, attribute over one-third of revenue to digital projects. Manufacturing players like Evyap have shaved 23% scrap using IoT analytics, reinforcing demand for end-to-end technology advisory.

Escalating Demand for Advanced Analytics and AI Advisory

Generative-AI adoption moved from proof-of-concept to mission-critical, with 77% of European financial-services leaders expecting significant productivity lifts and 68% predicting job-role redesign within 12 months. Despite appetite, 35% lack concrete upskilling road-maps, opening advisory opportunities. UK consulting firms earmark GBP 1.9 million per firm for AI-capability build-outs through 2026. Partnership ecosystems are pivotal, illustrated by NTT Data’s tie-up with Mistral AI to deliver sovereign enterprise AI for regulated sectors. The Big Four collectively plan more than USD 5 billion in AI platform investments by 2030, signaling long-run advisory capacity expansion.

ESG-linked Regulatory Complexity

The EU’s Corporate Sustainability Reporting Directive (CSRD) introduces 80 disclosure requirements and 800 data points, expanding compliance to roughly 50,000 companies beginning 2024. Double-materiality assessments now inform capital-allocation strategies, embedding consulting support deep in finance and risk functions. BBVA’s ESG-infused digital banking overhaul, underpinned by advisors, produced EUR 8.02 billion profit while growing digital customer acquisition to 65%. SMEs struggle most; although 72% leverage data, specialized ESG expertise remains scarce, driving demand for modular advisory offerings. Consultancies now embed sustainability analytics into core transformation road-maps to secure license-to-operate credentials for clients.

Cyber-security Compliance Mandates

The Digital Operational Resilience Act (DORA) and the NIS2 directive impose binding cyber-security standards on financial entities and critical infrastructure, effective January 2025. European firms allocate 9% of IT budgets to information security, up 1.9 percentage points year on year, while 89% foresee additional hiring to meet NIS2 obligations. Average breach costs have hit EUR 4.4 million, with human error driving 68% of incidents, underlining the need for integrated technical and change-management consulting. Compliance-linked demand accelerates short-cycle assessments, SOC modernization projects, and multi-year cyber-risk governance programs for banks and insurers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe talent shortage and attrition | −1.2% | Global; acute in DACH and UK | Short term (≤ 2 years) |

| Fee-rate pressure from professional procurement | −0.8% | EU-wide; mature markets | Medium term (2-4 years) |

| AI-driven self-service strategy platforms | −0.6% | DACH, UK, Nordics | Long term (≥ 4 years) |

| Rise of freelance consulting marketplaces | −0.4% | UK, DACH; gradual EU expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Severe Talent Shortage and Attrition

Turnover in European consulting averages 13.25%, with junior attrition at the Big Four hitting 22%, fueled by long hours and burnout. The gap widens in cyber-security, where 76% of staff lack formal credentials, amplifying delivery risk. German firms are hiking salaries 2.5% on average for 2025 as part of retention pushes, with entry-level bumps of 3.5%. Persistent shortages limit project-ramp speed, compelling firms to prioritize margin-rich accounts and further squeeze growth in commoditized workstreams.

Fee-rate Pressure from Professional Procurement

Sophisticated procurement teams leverage macro uncertainty to negotiate down day rates and demand performance guarantees. Deloitte UK saw consulting revenue slip 1% in 2024 under pricing strain. German consultants expect 11.9% growth in 2025 versus 9.4% for international peers, pointing to local price competition and market maturation. Sustainability consulting illustrates the squeeze: basic assignments run GBP 300-400, but specialized ESG expertise climbs past GBP 1,000, forcing firms to prove differential value. Freelance marketplaces intensify the dynamic, creating transparent benchmarks and eroding legacy premium margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Operational Excellence Holds Leadership

Operations Consulting captured 29.65% of the European management consulting market size in 2025 as companies aimed to streamline costs and future-proof supply networks amid volatile demand. Strategy Consulting, while foundational, now ranks behind digital engagements as boardrooms seek tangible quick wins from productivity projects. Digital/AI Consulting is scaling fastest, advancing at a 12.29% CAGR into 2031, fueled by AI roadmap design, data-platform integration, and cloud-migration mandates.

The Europe management consulting market increasingly values specialized sub-services such as sustainability advisory and risk compliance, which spike alongside new EU directives. Technology-centric mandates dominate procurement pipelines; banks like Credit Europe reduced onboarding time from two weeks to 15 minutes after micro-services re-platforming, illustrating payback from tech-led operational redesign . Risk and compliance work accelerates due to DORA and NIS2, while ESG advisory gains momentum under CSRD rules. Firms building cross-domain squads that blend sector expertise with analytics talent are winning multiyear retainer deals.

By Client Industry: Financial Services Stays in Front

Financial Services commanded 33.05% of the Europe management consulting market share in 2025 on the back of regulatory complexity, fintech disruption, and multi-cloud modernization. Healthcare and Life Sciences posts the fastest 9.92% CAGR as providers digitize clinical pathways and pharma accelerates RandD analytics.

In banking, BBVA’s fully digital acquisition engine delivered 11.1 million new customers and EUR 8.02 billion profit, underscoring advisory ROI. Manufacturing workloads emphasize Industry 4.0 retrofits, whereas public-sector projects focus on citizen-experience redesign. Energy, retail, and logistics segments increasingly seek decarbonization blueprints, bundling strategy with execution support. Integration of AI across verticals is broadening addressable spend for consultancies equipped with sectorized IP.

By Firm Size: Enterprise Wallet Dominates, but SME Growth Surges

Large enterprises retained 72.15% of spend in 2025, reflecting their need for full-stack transformation partners across global footprints. Yet SMEs deliver the fastest 8.33% CAGR as modular, subscription-based consulting makes high-quality advice affordable.

Euroclear’s phased transformation showcases enterprise appetite for multi-year programs marrying business and IT alignment. On the SME side, the COSME guarantee facility unlocked EUR 54 billion in financing, spurring outsourced advisory uptake as firms pivot toward e-commerce and cross-border trade. Networked delivery models allow consultancies to blend local talent with remote centers of excellence, optimizing price-to-value ratios for smaller clients.

By Delivery Model: Hybrid Engagements Gain Ground

On-site projects still account for 57.62% Europe management consulting market share, particularly for complex change programs requiring executive alignment and workshop-intensive design. Yet fully remote engagements grow 14.71% CAGR as clients embrace virtual collaboration to cut travel costs and access niche skills.

The Central Denmark Region’s RPA initiative automated 80 processes via a largely remote consulting team, saving 50,000 hours within the first year. Hybrid models that blend short on-site sprints with continuous virtual delivery are emerging as the default for pan-European rollouts, enabling firms to manage carbon footprints and offer competitive pricing.

Geography Analysis

DACH remained the anchor of the Europe management consulting market in 2025, securing 26.28% market share and generating EUR 3.86 billion revenue in Germany alone with 11.9% growth . Strong industrial players and high RandD intensity sustain consulting demand, while Switzerland’s finance-centric economy and Austria’s gateway role to CEE add further momentum. Generative-AI investment plans averaging USD 37 million per firm highlight future advisory pipelines despite talent constraints. Regulatory complexities such as DORA across financial institutions layer in recurring compliance engagements.

The UK and Ireland form Europe’s second-largest consulting cluster, benefiting from London’s global finance hub and Dublin’s tech concentration. The UK market eyes 6.1% growth in 2026 as consultancies earmark GBP 1.9 million each for AI capability build-out. Post-Brexit, firms have opened over 312 regional offices to tap local talent pools and offset wage inflation. Energy-transition projects fuel double-digit growth in Scotland and Northern England, while financial-services compliance remains a London mainstay.

France and Benelux leverage large industrial and public-sector clients; France’s sovereign-cloud strategy accelerated after Carlyle’s EUR 525 million acquisition of Ciril Group. The Nordics, valued at EUR 2.83 billion, excel in digital government, with Sweden growing 6.7%. CEE posts the strongest 7.71% CAGR, propelled by EU structural funds and near-shoring of manufacturing. Poland and Czech Republic are scaling advisory contracts in supply-chain digitization, while Hungary benefits from automotive electrification projects.

Competitive Landscape

The Europe management consulting market reflects moderate concentration: the Big Four capture an estimated 55-60% of regional revenue, yet boutique specialists and digital-first challengers are rapidly eating share. Deloitte posted USD 67.2 billion global revenue in 2024, with EMEA leading at 8.5% growth. PwC, EY, and KPMG each surpassed USD 38 billion globally, but UK consulting revenues slipped as procurement scrutiny tightened and discretionary spend fell. To defend margins, incumbents are funneling USD 5 billion-plus into generative-AI studios, data-platform accelerators, and managed-services offerings.

Strategic alliances underpin differentiation: NTT Data’s pact with Mistral AI positions it as a sovereign-AI leader for regulated clients across finance and defense. Meanwhile, Carlyle’s buy-out of Ciril Group signals private-equity appetite for cloud and cybersecurity horizontal plays. The gig economy exerts price pressure; high-caliber independents now win complex sustainability work by leveraging platforms that match niche expertise to short-cycle mandates, pushing traditional firms toward outcome-based contracts and proprietary IP solutions.

Boutique strategy houses—Roland Berger, Oliver Wyman, PA Consulting—capitalize on sector depth and agile delivery to secure transformation road-maps in aerospace, healthcare, and energy. Technology giants such as Accenture and Capgemini blend consulting with system-integration scale, offering clients one-stop execution. The competitive chessboard thus oscillates between breadth of capability and depth of specialization, driving acquisitions, talent poaching, and co-innovation partnerships.

Europe Management Consulting Services Industry Leaders

Deloitte Touche Tohmatsu LLP

Ernst & Young Global Limited

Boston Consulting Group

PricewaterhouseCoopers LLP

KPMG International Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Carlyle acquired French sovereign-cloud provider Ciril Group for EUR 525 million (USD 570 million), reinforcing Europe’s push for digital autonomy.

- July 2025: NTT Data partnered with Mistral AI to launch managed sovereign enterprise-AI services for finance, defense, and public sectors.

- May 2025: EY released a 23-point manifesto to bolster EU competitiveness, citing a 4% fall in FDI and urging accelerated digital and sustainability alignment.

- January 2025: KPMG Germany reported EUR 2.61 billion revenue, up 9.6%, with Advisory reaching EUR 1.129 billion and 2,600 new hires.

Europe Management Consulting Services Market Report Scope

Management consulting firms assist organizations in increasing their efficiency. The firms examine operations and determine existing organizational inefficiencies, which include several factors, like high raw material costs and HR policies. The study tracks revenue generation through vendor offerings of various consulting services among users.

The European management consulting services market is segmented by type (HR consulting, strategy consulting, and operations consulting) and application (IT and telecommunication, manufacturing, energy, healthcare, public sector, retail, and healthcare). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Consulting Service Line

| Strategy Consulting |

| Operations Consulting |

| Technology / Digital Consulting |

| HR Consulting |

| Financial Advisory |

| Risk and Compliance Consulting |

| Sustainability and ESG Advisory |

By Client Industry

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Retail and Consumer Goods |

| Healthcare and Life Sciences |

| Financial Services |

| Transportation and Logistics |

By Firm Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

By Delivery Model

| On-site Consulting |

| Hybrid (On-site and Remote) |

| Fully Remote / Virtual Consulting |

By Country

| DACH (Germany, Austria, Switzerland) |

| UK and Ireland |

| France and Benelux (France, Belgium, Netherlands, Luxembourg) |

| Nordics (Sweden, Norway, Denmark, Finland) |

| Southern Europe (Spain, Italy, Portugal, Greece) |

| Central and Eastern Europe (Poland, Czech Republic, Hungary, etc.) |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| Technology / Digital Consulting | |

| HR Consulting | |

| Financial Advisory | |

| Risk and Compliance Consulting | |

| Sustainability and ESG Advisory | |

| By Client Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Retail and Consumer Goods | |

| Healthcare and Life Sciences | |

| Financial Services | |

| Transportation and Logistics | |

| By Firm Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Delivery Model | On-site Consulting |

| Hybrid (On-site and Remote) | |

| Fully Remote / Virtual Consulting | |

| By Country | DACH (Germany, Austria, Switzerland) |

| UK and Ireland | |

| France and Benelux (France, Belgium, Netherlands, Luxembourg) | |

| Nordics (Sweden, Norway, Denmark, Finland) | |

| Southern Europe (Spain, Italy, Portugal, Greece) | |

| Central and Eastern Europe (Poland, Czech Republic, Hungary, etc.) |

Key Questions Answered in the Report

What revenue does the Europe management consulting market generate in 2026?

The market generates USD 83.95 billion in 2026 and is on track to reach USD 112.29 billion by 2031.

Which service line is growing fastest across European consultancies?

Digital/AI Consulting is the fastest-growing, expanding at a 12.29% CAGR through 2031 as generative-AI adoption scales.

How large is consulting demand from financial-services clients?

Financial Services accounts for 33.05% of spending, the largest share among all client industries.

Which region leads European consulting activity?

The DACH region (Germany, Austria, Switzerland) holds 26.28% market share, the highest of any regional cluster.

Page last updated on: