United Kingdom Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

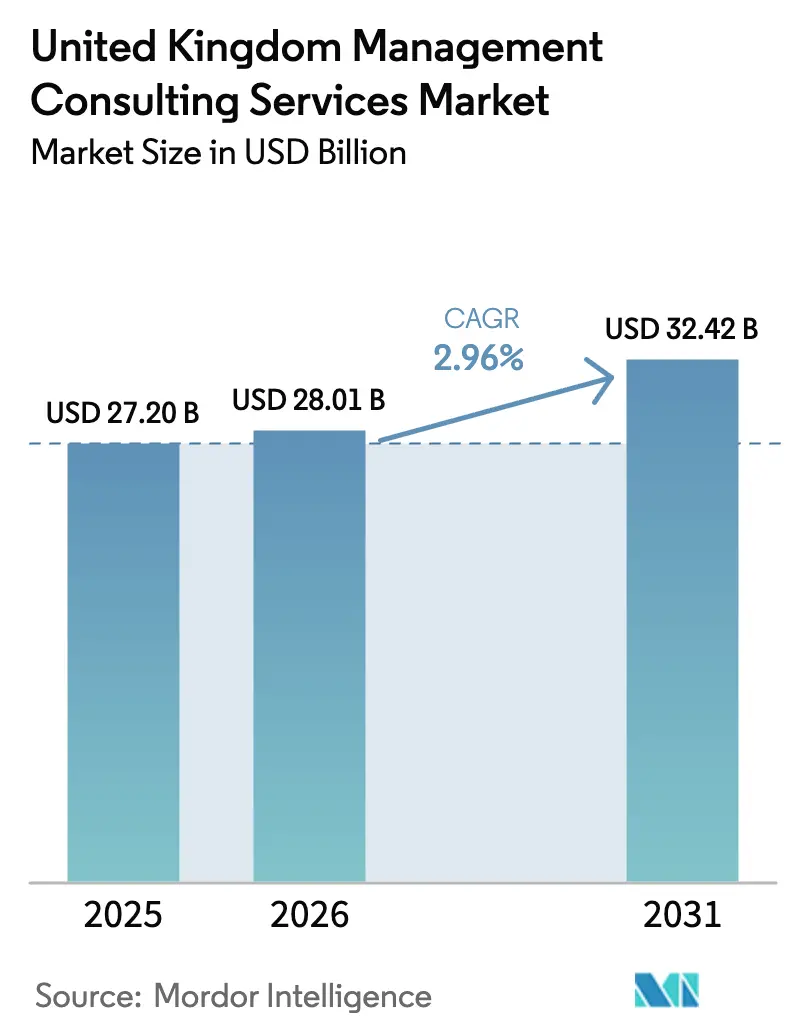

| Base Year Market Size (2025) | USD 27.20 Billion |

| Market Size (2026) | USD 28.01 Billion |

| Market Size (2031) | USD 32.42 Billion |

| Growth Rate (2026 - 2031) | 2.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Management Consulting Services Market Analysis by Mordor Intelligence

The United Kingdom management consulting services market size is expected to grow from USD 27.20 billion in 2025 to USD 28.01 billion in 2026 and is forecast to reach USD 32.42 billion by 2031 at 2.96% CAGR over 2026-2031. Slower headline growth reflects the maturity of the United Kingdom management consulting services market, yet steady demand persists as enterprises accelerate AI deployment, overhaul legacy IT estates, and respond to net-zero rules. Brexit-driven regulatory divergence keeps compliance engagements buoyant, while the public sector’s GBP 6.5 billion G-Cloud framework channels transformation spend toward cloud and cybersecurity mandates. Talent shortages and wage inflation add cost pressure, but they simultaneously boost advisory work on workforce strategy. Hybrid delivery models gain traction as 94% of businesses pursue carbon-cutting measures and 14% already use AI in production environments, signaling widening adoption curves that sustain project pipelines.

Key Report Takeaways

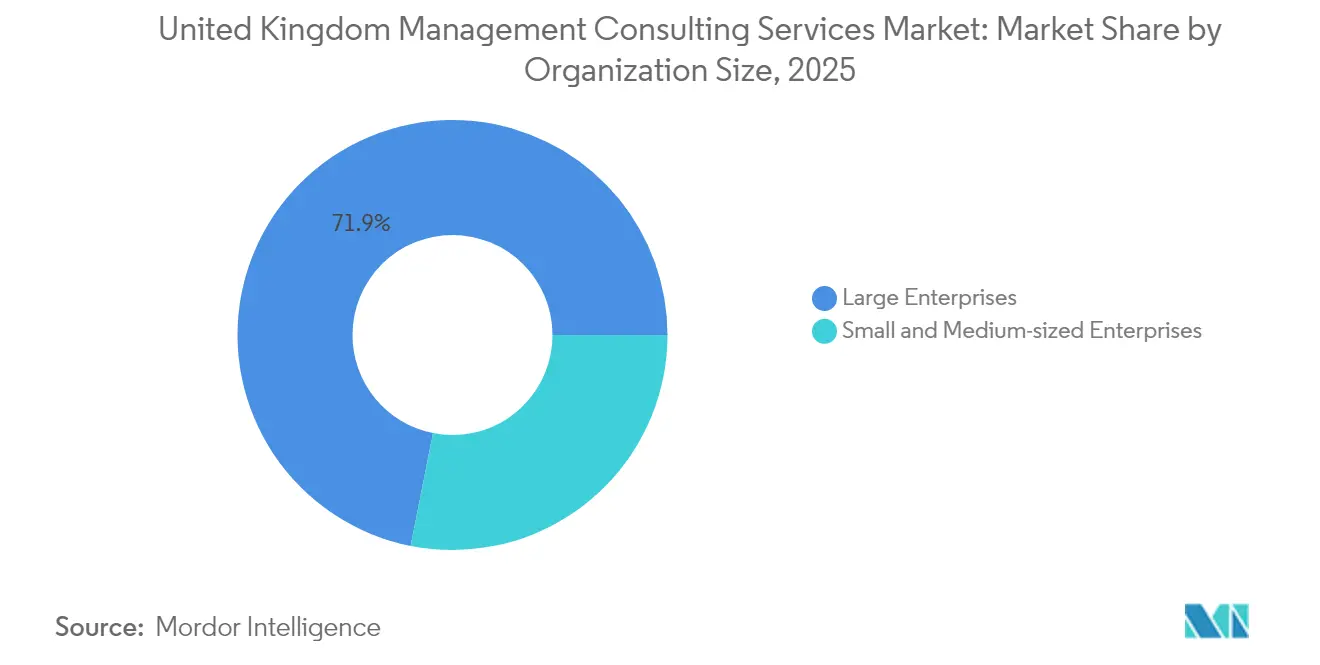

- By organization size, large enterprises controlled 71.88% of the United Kingdom management consulting services market share in 2025, while SMEs are expanding at a 4.24% CAGR through 2031.

- By service type, operations consulting led with 36.17% revenue share in 2025; technology consulting is projected to advance at a 6.23% CAGR to 2031.

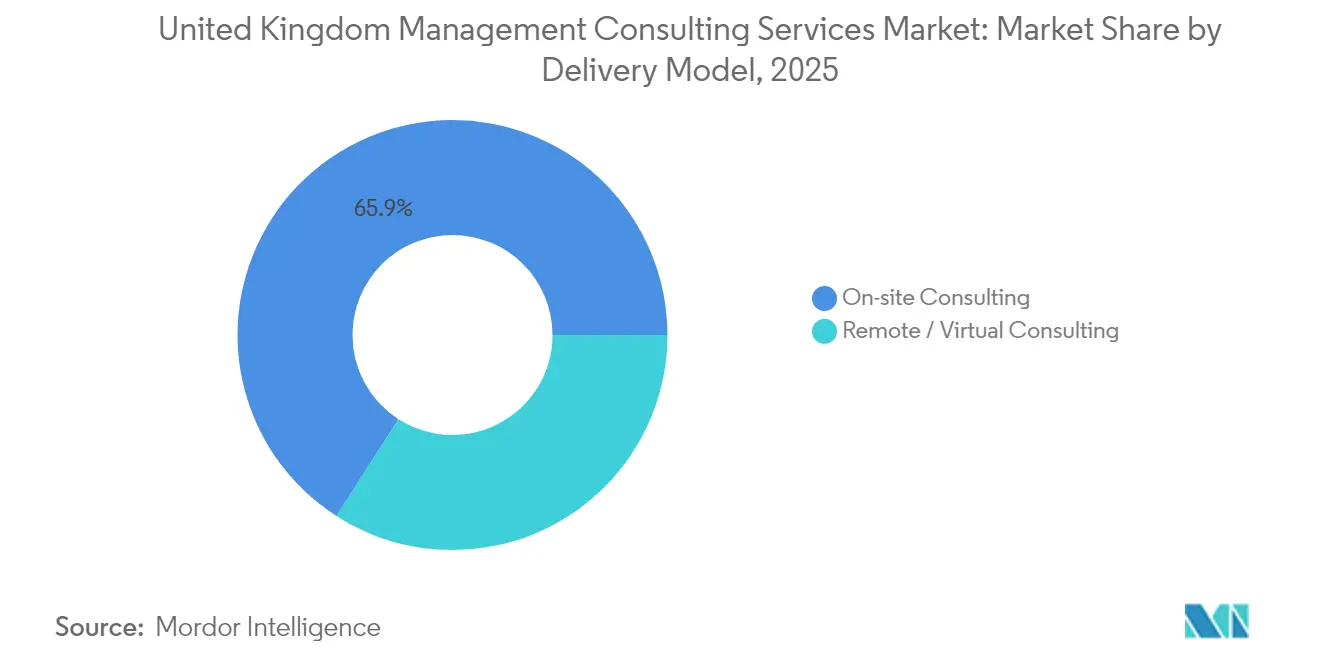

- By delivery model, on-site engagements held 65.92% of the United Kingdom management consulting services market size in 2025, while remote consulting is growing at a 4.49% CAGR through 2031.

- By end-user industry, financial services accounted for 24.63% share in 2025 and healthcare & life sciences is advancing at a 9.44% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating digital transformation initiatives | +0.8% | National, with concentration in London and Manchester | Medium term (2-4 years) |

| AI-led productivity and innovation mandates | +0.6% | Global, with early adoption in financial services | Short term (≤ 2 years) |

| Net-zero and ESG regulatory pressure | +0.4% | National, with spillover to international operations | Long term (≥ 4 years) |

| Post-Brexit regulatory complexity across industries | +0.3% | National, with cross-border implications | Medium term (2-4 years) |

| Regional consulting demand surge beyond London hubs | +0.2% | Northern England, Scotland, Wales | Medium term (2-4 years) |

| Export-oriented growth of UK consulting services | +0.2% | Global, leveraging UK regulatory expertise | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Digital Transformation Initiatives

Public-sector procurement demonstrates record technology spend: the Matrix Programme alone allocates GBP 144.3 million to ERP modernization across nine departments, and G-Cloud 14 reserves GBP 6.5 billion for cloud services through 2026 GOV.UK. The NHS earmarks GBP 3.4 billion for digital upgrades, including Ambient Voice Technologies that deliver 15-20% clinical productivity gains. Private enterprises follow suit as 98% of technology employees seek AI literacy, prompting advisory work in learning design and change management. Google’s partnership to upskill 100,000 civil servants underscores long-run demand for capability-building engagements.

AI-Led Productivity and Innovation Mandates

PwC finds that more than 95% of its clients now run generative-AI workstreams, racking up over 3,000 enterprise use cases. AI strategy projects, priced between GBP 335 and GBP 1,900 per consultant day, cover architecture blueprints, governance, and model-risk controls. Deloitte’s pact with Anthropic to train 15,000 professionals highlights the scale of reskilling underway. Financial institutions pilot real-time compliance bots, while hospitals test AI triage to optimize resource scheduling—each rollout requiring specialist advisory oversight.

Net-Zero and ESG Regulatory Pressure

Draft UK Sustainability Reporting Standards (UK SRS) will become mandatory from January 2026, pushing corporates to embed climate metrics into statutory statements. [1]Department for Science, Innovation & Technology, “Matrix Programme ERP Services,” gov.ukIFRS S1 and S2 endorsements elevate transparency obligations and usher in demand for assurance and target-setting roadmaps. With half of businesses already cutting emissions, consultancies design decarbonization pathways, procurement policies, and green-finance models. Homes England’s GBP 958.7 million advisory framework explicitly includes ESG, signaling entrenched public-sector commitments.

Post-Brexit Regulatory Complexity Across Industries

Automotive type-approval reform exemplifies the United Kingdom’s divergence from EU regimes while preserving export eligibility, creating multi-jurisdictional compliance tasks. Financial-services regulation evolves via crypto-asset oversight and payment-safeguarding updates that compel banks to refresh risk matrices. Customs amendments adjust duty-relief criteria, requiring manufacturing and retail exporters to redesign supply-chain documentation. Collectively, these shifts anchor a steady stream of regulatory-advisory engagements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macroeconomic volatility and public-sector budget tightening | -0.7% | National, with regional variations | Short term (≤ 2 years) |

| Acute talent shortages and wage inflation | -0.5% | National, concentrated in London and tech hubs | Medium term (2-4 years) |

| SME cash-flow strain from chronic late-payment culture | -0.4% | National, with higher impact in manufacturing and construction | Medium term (2-4 years) |

| Commoditisation risk from AI tools and gig-consultant platforms | -0.3% | Global, with early impact in standardized service areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Macroeconomic Volatility and Public-Sector Budget Tightening

The new government’s drive to curb external consulting spend coincides with a fragile growth outlook; Q1 2024 GDP expanded just 0.7%. [2]Office for National Statistics, “GDP quarterly national accounts,” ons.gov.uk NHS England’s planned consolidation aims to save GBP 500 million annually, trimming discretionary advisory budgets. Yet pharmaceuticals and regulated utilities continue to source external expertise, cushioning downside impacts.

Acute Talent Shortages and Wage Inflation

Eighty percent of employers report difficulty filling roles, and starting salaries have risen for 52 straight months. [3]Hudson RPO, “The 2024 United Kingdom talent market outlook,” hudsonrpo.com Visa-salary thresholds jumped to GBP 38,700 for technologists, escalating total compensation by 45%. Consultancies respond by automating delivery tasks with proprietary AI, but investment in training and retention compresses margins. Skills gaps threaten 380,000 jobs and GBP 27.6 billion of value by 2030, forcing firms to embed capability-building modules in client proposals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: SMEs Drive Consulting Democratization

The United Kingdom management consulting services market size remained dominated by large enterprises in 2024, but SMEs displayed faster volume growth. Cost-efficient digital platforms and outcome-based contracts help SMEs access expertise once reserved for multinationals. Approximately 55% of small businesses lack internal tech talent, prompting external-advisory uptake. Late-payment cultures saddle SMEs with GBP 25,000 average debt, constraining spend; Fair Payment Code reforms are expected to loosen cash flow and further enlarge the United Kingdom management consulting services market for smaller firms.

Large corporates continue to fuel high-value transformation deals: Phoenix Group’s GBP 500 million partnership with Wipro on digital re-platforming typifies multi-year engagements demanding cross-functional teams. The United Kingdom management consulting services market share held by enterprises therefore remains substantial, but consultant toolkits calibrated for SME budgets unlock incremental expansion.

By Service Type: Technology Consulting Drives Growth Amid Operations Leadership

Operations consulting retained 36.17% of 2025 revenue, underlining enduring demand to streamline supply chains and reduce cost in the aftermath of Brexit disruptions. Advisory teams focus on process mining, lean redesign, and resilience modeling. Meanwhile, technology consulting’s 6.23% CAGR reflects skyrocketing AI and cloud projects that elevate digital to board-level priority. The United Kingdom management consulting services market size captured by technology engagements will eclipse strategy work by decade-end as CIOs accelerate modernization roadmaps.

Hybrid offerings blend operations re-engineering with embedded AI, creating bundled value propositions. HR consulting expands steadily as firms battle talent scarcity, while strategy consulting navigates funding cycles affected by macro uncertainty. ESG mandates spur niche compliance boutiques; nevertheless, technology integration remains the catalytic force reshaping the United Kingdom management consulting services market.

By Delivery Model: Remote Consulting Gains Ground Despite On-Site Preference

Although face-to-face collaboration still accounts for 65.92% of spend, the pandemic-era shift toward digital collaboration tools persists. Clients now tolerate fully virtual diagnostics and training sprints, reserving on-site presence for kickoff and change-leadership workshops. Employment tribunal disputes around forced office returns illustrate cultural tensions but have not derailed remote-first projects.

Technology-heavy workstreams—cyber assessments, data-architecture builds, AI-model tuning—lend themselves to distributed teams. Consequently, the United Kingdom management consulting services market size attributable to virtual delivery is expanding at 4.49% CAGR. Firms differentiate through secure cloud environments that satisfy data-protection standards, enabling seamless cooperation across geographies.

By End-User Industry: Healthcare Surge Challenges Financial Services

Financial services kept the largest slice of 2025 revenue at 24.63%, driven by regulatory overhauls spanning crypto-asset compliance and conduct-risk remediation. However, NHS digital modernization accelerates healthcare’s 9.44% CAGR, as hospital trusts adopt cloud EMRs, AI triage, and cybersecurity defenses. The United Kingdom management consulting services market share for healthcare projects is poised to close the gap with banking by 2031.

Energy-transition consulting intensifies as utilities target net-zero and hydrogen portfolios, while retail seeks omnichannel operating models. Government departments, despite cost-cut drives, still commission outcome-based contracts for mission-critical systems—often under pay-by-results arrangements that mitigate budget caps.

Geography Analysis

The United Kingdom management consulting services market remains anchored in London, yet regional hubs from Manchester to Edinburgh post rapid percentage gains. London’s gravitational pull stems from its finance cluster and central government, ensuring a steady stream of regulatory and strategy mandates. Nonetheless, EY’s plan to raise Manchester headcount to 2,000 by 2026 underscores the North’s digital ascendancy. Manchester expects GBP 2 billion extra GVA by 2026, attracting consultancies keen on lower operating costs. Leeds forecasts 21% economic expansion within a decade, bolstered by fintech clusters.

Scotland leverages energy-transition projects in offshore wind and green hydrogen, drawing operations and sustainability advisors. Wales pursues advanced manufacturing and life sciences clusters that require process optimization services. The East of England matches London’s 1.7% projected growth, propelled by Cambridge-led biotech innovation. Digital connectivity fosters distributed delivery: London practices manage Northern clients remotely, while regional boutiques win national contracts via Crown Commercial Service frameworks. Internationally, British consultancies export Brexit-honed regulatory expertise to Commonwealth markets, extending the global footprint of the United Kingdom management consulting services market.

Competitive Landscape

Big Four incumbents dominate but face nimble challengers wielding AI-powered playbooks. Deloitte, PwC, EY, and KPMG jointly capture an estimated 55% of fee revenue. Yet acquisitions such as CGI’s takeover of BJSS, adding 2,400 cloud engineers, demonstrate how IT services players consolidate consulting muscle. Bridgepoint’s investment in Argon & Co signals private-equity appetite for operations specialists. Grant Thornton’s strategic funding from Cinven and the prospective RSM transatlantic merger illustrate mid-tier scale-up strategies.

Technology adoption shapes rivalry: PwC’s reseller agreement for ChatGPT Enterprise and Deloitte’s Anthropic partnership embed generative AI in delivery workflows, slashing turnaround times. Smaller boutiques differentiate through depth—Baringa in energy transition, PA in public-sector innovation—while platform-based gig-consultant models commoditize standardized tasks. Public-sector frameworks like Digital Outcomes 7 lower entry barriers, enabling micro-firms to win slices of the United Kingdom management consulting services market.

United Kingdom Management Consulting Services Industry Leaders

Accenture plc

Deloitte Touche Tohmatsu Limited (DTTL)

PricewaterhouseCoopers LLP

Ernst and Young Global Limited

KPMG International Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Google Cloud partnered with the United Kingdom Government to modernize public services and train 100,000 civil servants in AI by 2030.

- June 2025: KPMG launched KPMG Law US, extending technology-enabled legal services across 80 jurisdictions.

- April 2025: Bridgepoint announced a strategic investment in Argon & Co to accelerate global operations-transformation offerings.

- March 2025: Mercer completed its acquisition of SECOR Asset Management to bolster investment consulting capabilities.

United Kingdom Management Consulting Services Market Report Scope

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Technology Consulting |

| Other Service Types |

| On-site Consulting |

| Remote / Virtual Consulting |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Financial Services (BFSI) |

| Manufacturing and Industrial |

| Energy and Utilities |

| Government and Public Sector |

| Real Estate and Construction |

| Retail and Consumer Goods |

| Media, Entertainment and Sports |

| Hospitality and Travel |

| Other End-user Industries |

| By Organization Size | Large Enterprises |

| Small and Medium-sized Enterprises | |

| By Service Type | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Technology Consulting | |

| Other Service Types | |

| By Delivery Model | On-site Consulting |

| Remote / Virtual Consulting | |

| By End-user Industry | IT and Telecommunications |

| Healthcare and Life Sciences | |

| Financial Services (BFSI) | |

| Manufacturing and Industrial | |

| Energy and Utilities | |

| Government and Public Sector | |

| Real Estate and Construction | |

| Retail and Consumer Goods | |

| Media, Entertainment and Sports | |

| Hospitality and Travel | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current value of the United Kingdom management consulting services market?

The market generated USD 28.01 billion in 2026 and is forecast to reach USD 32.42 billion by 2031.

Which service line is expanding fastest?

Technology consulting is growing at 6.23% CAGR, outpacing all other segments.

How big is the opportunity in healthcare advisory?

Healthcare and life sciences projects are advancing at a 9.44% CAGR, the highest among end-user industries.

What share of spending comes from financial services clients?

Financial institutions accounted for 24.63% of 2025 revenue.

Are SMEs significant buyers of consulting services?

Yes; although large enterprises dominate, SME engagements are rising at 4.24% CAGR as modular, cost-effective offerings spread.

How are regional hubs influencing demand?

Cities such as Manchester, Leeds, and Edinburgh post faster growth than London as firms seek lower costs and tap local tech talent.

Page last updated on: