New Zealand Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

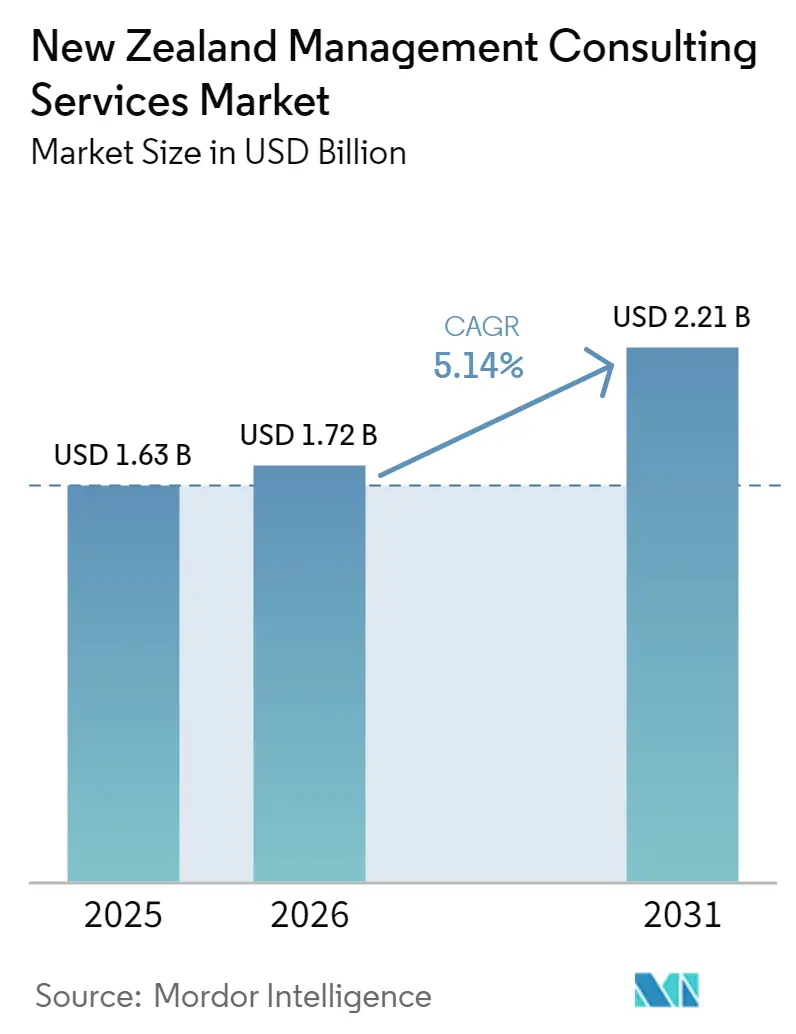

| Base Year Market Size (2025) | USD 1.63 Billion |

| Market Size (2026) | USD 1.72 Billion |

| Market Size (2031) | USD 2.21 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

New Zealand Management Consulting Services Market Analysis by Mordor Intelligence

The New Zealand management consulting services market size was valued at USD 1.3 billion in 2025 and estimated to grow from USD 1.38 billion in 2026 to reach USD 1.82 billion by 2031, at a CAGR of 5.69% during the forecast period (2026-2031). Corporate and government buyers are turning to external advisors as sweeping public sector restructuring, digital-first strategies, and tight labor pools strain internal capabilities. Mandatory climate disclosure rules and the government’s estimate of a NZD 76 billion (USD 46.36 billion) artificial intelligence opportunity are accelerating demand for ESG, data, and technology consulting. Large transformation programs in water infrastructure, health, and education are creating multi-year consulting pipelines while SMEs adopt fractional, remote, and productized advisory models. Competition is intensifying as Big Four firms defend share against global strategy houses, technology integrators, indigenous boutiques, and gig-based specialists.

Key Report Takeaways

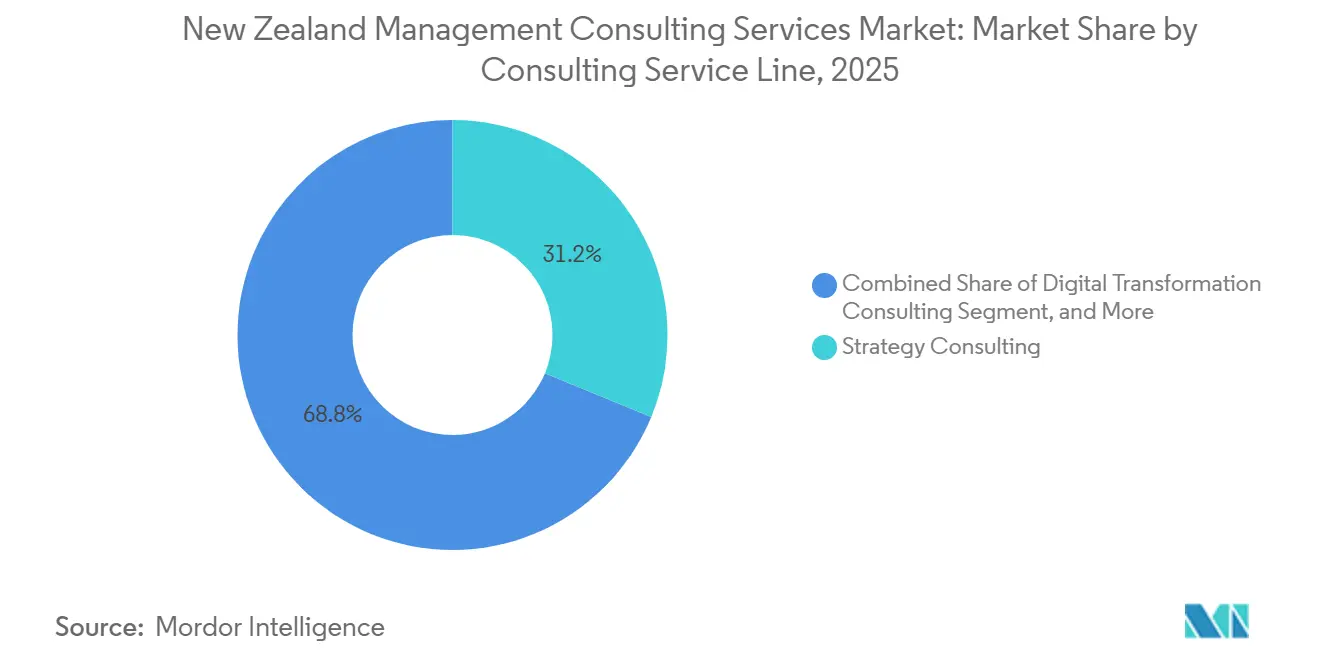

- By consulting service line, Strategy Consulting led with 31.23% revenue share in 2025 while Digital Transformation Consulting is projected to expand at a 6.24% CAGR through 2031.

- By organization size, Large Enterprises held 64.48% of the New Zealand management consulting services market share in 2025, whereas Small and Medium-Sized Enterprises are tracking a 5.88% CAGR to 2031.

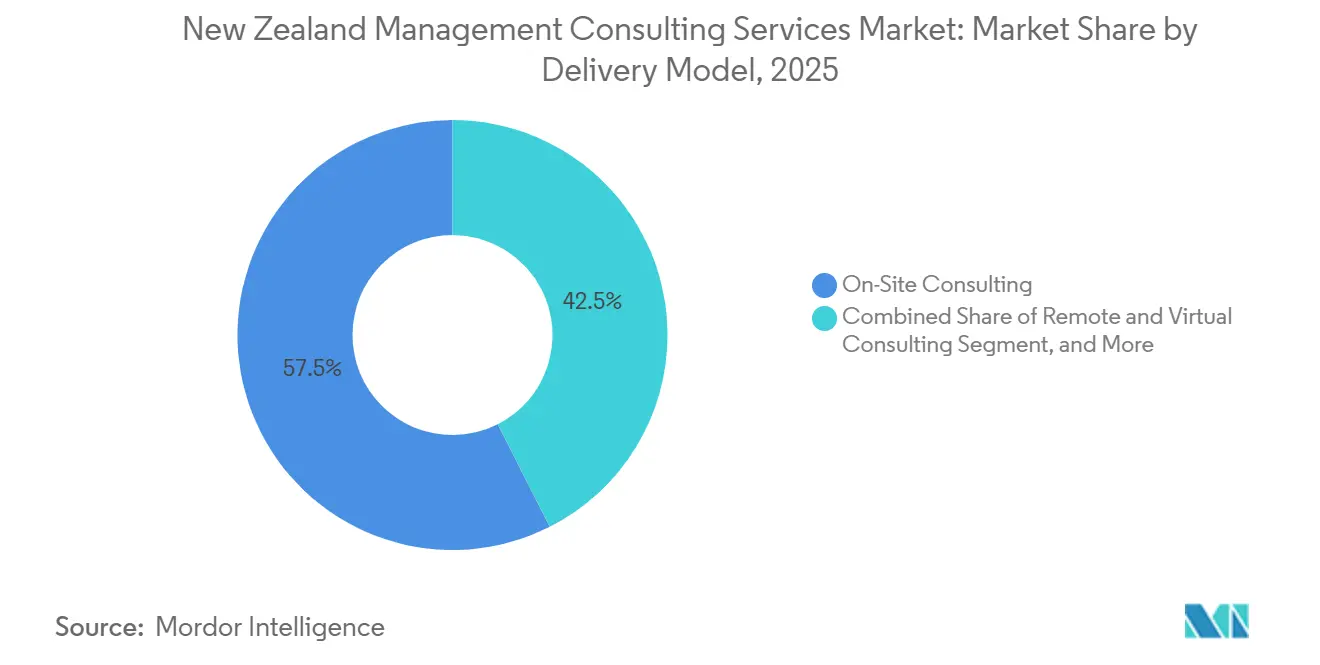

- By delivery model, On-Site Consulting accounted for 57.46% of the New Zealand management consulting services market size in 2025 and Remote and Virtual Consulting is advancing at a 6.43% CAGR through 2031.

- By end-user industry, the Public Sector captured 29.78% share of the New Zealand management consulting services market in 2025 and Energy and Resources is forecast to grow fastest at a 5.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

New Zealand Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-First Transformation Programs Across Corporates | +1.2% | National, early concentration in Auckland and Wellington | Medium term (2-4 years) |

| Public Sector Mega-Reforms (Three Waters, Health, Education) | +1.5% | National, infrastructure focus in regional councils | Long term (≥ 4 years) |

| Accelerating ESG and Climate-Transition Advisory Demand | +0.9% | National, regulatory pressure on listed entities and large emitters | Short term (≤ 2 years) |

| Persistent Domestic Skills Shortages Elevating Outsourcing | +1.0% | National, acute in technology and specialized advisory roles | Medium term (2-4 years) |

| Māori Economic Renaissance Spurring Culturally Anchored Advisory | +0.4% | National, early gains in Northland, Bay of Plenty, East Coast | Long term (≥ 4 years) |

| Uptake of Generative-AI-Enabled Remote Consulting for SMEs | +0.7% | National, faster adoption in urban SME clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital-First Transformation Programs Across Corporates

Enterprises are embedding cloud, data, and AI capabilities across operations, finance, and customer touchpoints in line with the government’s Digital Strategy for Aotearoa that targets a digitally inclusive economy by 2030. Banks, telcos, and retailers are migrating core systems to hyperscaler platforms, automating middle-office workflows, and piloting generative AI chatbots. The NZD 70 million (USD 42.7 million) New Zealand Institute for Artificial Intelligence and Technology, announced in 2025, is fostering public-private pilot projects that require advisory around AI ethics, governance, and change management.[1]Ministry of Business, Innovation and Employment, “New Zealand Institute for Artificial Intelligence and Technology Funding Announcement,” mbie.govt.nz Consulting firms are building dedicated AI practices, partnering with AWS, Microsoft Azure, and Google Cloud, and productizing diagnostic tools to shorten sales cycles. These moves cement digital transformation as the fastest-growing revenue stream in the New Zealand management consulting services market.

Public Sector Mega-Reforms (Three Waters, Health, Education)

The shift from the scrapped Three Waters model to the Local Water Done Well framework obliges councils to present credible financial and service plans for infrastructure programs estimated between NZD 120 billion and NZD 185 billion (USD 73.2-112.85 billion) over 30 years.[2]Department of Internal Affairs, “Local Water Done Well: Reform Framework,” dia.govt.nz Health New Zealand, stewarding a USD 18.4 billion 2025-26 budget, is rolling out digital health records, workforce planning, and clinical redesigns that exceed internal capacity.[3]Health New Zealand, “Statement of Performance Expectations 2025/26,” health.govt.nz Education authorities are modernizing school property and digital learning strategies that require procurement, risk, and stakeholder management expertise. These reforms are generating sustained demand for strategy, program management, and financial advisory, bolstering the New Zealand management consulting services market through 2031.

Accelerating ESG and Climate-Transition Advisory Demand

Mandatory climate-related financial disclosures introduced in 2023 and an emissions reduction target of 50% below 2005 levels by 2030 are forcing around 170 large entities to quantify climate risks and plan decarbonization pathways.[4]Financial Markets Authority, “Climate-Related Financial Disclosures Guidance,” fma.govt.nz Energy, agriculture, and transport clients are commissioning consultants for Scope 3 measurement, green finance structuring, and transition scenario modeling. Financial institutions are embedding climate metrics into lending, pushing corporate borrowers toward credible roadmaps. Consulting firms have responded by merging sustainability teams, hiring carbon accountants, and integrating assurance with strategy work, elevating ESG to a core growth pillar within the New Zealand management consulting services industry.

Persistent Domestic Skills Shortages Elevating Outsourcing

Statistics New Zealand’s 2024 Human Capital Analysis underscores persistent mismatches in digital and analytical roles, aggravated by tighter skilled-migrant settings.[5]Statistics New Zealand, “Human Capital Analysis 2024,” stats.govt.nz Organizations unable to fill vacancies are outsourcing project leadership, data analytics, and even interim C-suite roles. Public agencies, constrained by pay caps and lengthy hiring cycles, increasingly default to consulting panels for time-sensitive mandates. Firms leverage flexible resourcing and offshore centers to marshal scarce talent rapidly, reinforcing a structural reliance that supports the New Zealand management consulting services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying War-for-Talent Inflating Consultant Salaries | -0.8% | National, highest pressure in Auckland and Wellington | Short term (≤ 2 years) |

| Government Fee Pressure Under New Procurement Rules | -0.6% | National, affecting central and local government bids | Short term (≤ 2 years) |

| Heightened Conflict-of-Interest Scrutiny on Big Four Split | -0.5% | National, focus on audit-consulting separation | Medium term (2-4 years) |

| Gig-Platform Consultants Eroding Traditional Fee Structures | -0.4% | National, faster penetration in SME segment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying War-for-Talent Inflating Consultant Salaries

Scarce digital, data, and ESG specialists are commanding premium pay, prompting firms to offer retention bonuses and accelerated promotions that lift cost bases. Public sector buyers, bound by value-for-money rules, resist higher day rates, creating a profitability squeeze for vendors. Some consultancies are offshoring analytics or automating research with generative AI to contain costs, yet these moves risk quality lapses and client pushback. The salary spiral therefore dampens margins and slows deal closure, constraining the New Zealand management consulting services market in the near term.

Government Fee Pressure Under New Procurement Rules

Revised government procurement guidance emphasizes fixed-price contracts, transparent margin disclosure, and competitive rebidding on multiyear panels, trimming fee headroom for large programs. Agencies have capped single-supplier engagement values, fragmenting scopes across multiple vendors and diluting scale efficiencies. Firms must invest in bid compliance and post-award reporting, adding overhead that smaller boutiques struggle to absorb. While the policy raises accountability, it tempers growth prospects for providers heavily exposed to the public sector share of the New Zealand management consulting services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Strategy Maintains the Lead While Digital Rises

Strategy Consulting held a 31.23% share of the New Zealand management consulting services market in 2025, underscoring the public sector’s reliance on road-mapping and multiyear implementation support. Demand for restructuring playbooks, stakeholder engagement blueprints, and market-entry guidance from foreign investors sustains a double-digit contribution to the New Zealand management consulting services market size at the front end of major government reforms.

Digital Transformation Consulting is set to expand at a 6.24% CAGR through 2031, outpacing every other service line as cloud migrations, AI pilots, and data modernization programs mature. Operations, HR, and Risk Consulting provide counter-cyclical revenue that smooths the overall New Zealand management consulting services market growth curve, while niche offerings, legal support, indigenous advisory, and sector-specific analytics, offer boutiques room to differentiate. The steady broadening of service menus reinforces the versatility of the New Zealand management consulting services industry.

By Organization Size: Large Enterprises Still Dominate but SMEs Accelerate

Large Enterprises accounted for 64.48% of the New Zealand management consulting services market share in 2025 because complex regulatory obligations and multibillion-dollar transformation agendas require tier-one advisors and global delivery capacity. Ongoing ESG compliance, enterprise resource planning upgrades, and health-system integrations keep consulting spend high among banks, telcos, and government agencies.

Small and Medium-Sized Enterprises, however, are projected to grow at a 5.88% CAGR, capturing incremental slices of the New Zealand management consulting services market size as remote collaboration, fixed-price modules, and gig-based specialists reduce engagement thresholds. Subsidized advisory grants and the rise of fractional CFO and CIO models broaden access, expanding the client base of the New Zealand management consulting services market. This shift diversifies revenue streams for firms willing to tailor scope, cadence, and pricing to resource-constrained operators within the broader New Zealand management consulting services industry.

By Delivery Model: Remote Gains Ground, Hybrid Becomes the Norm

On-Site engagements captured 57.46% of the New Zealand management consulting services market in 2025, largely because sensitive policy design and high-stakes stakeholder workshops still favor face-to-face collaboration. Security protocols at banks and ministries continue to require consultants on client premises for key milestones, anchoring a sizable portion of the current New Zealand management consulting services market size.

Remote and Virtual Consulting is forecast to grow at 6.43% CAGR through 2031 as video platforms, digital whiteboards, and AI-assisted facilitation prove effective for data analysis and strategy sessions. A hybrid approach, on-site at kickoff and governance checkpoints, remote for analytics and drafting, is emerging as standard operating practice, driving efficiency without sacrificing intimacy. This blended model strengthens margins and expands geographic reach across the New Zealand management consulting services market while aligning with client cost-containment goals.

By End-User Industry: Public Sector Anchors Demand, Energy Transitions Fuel Growth

The Public Sector held 29.78% of the New Zealand management consulting services market size in 2025, reflecting unprecedented mega-reforms in water, health, and education. Ministries prize firms with deep policy credentials and ability to mobilize multidisciplinary teams quickly, locking in retainer-style arrangements that stabilize the New Zealand management consulting services market.

Energy and Resources is projected to grow fastest at 5.96% CAGR as utilities navigate emissions caps and renewable portfolio mandates. Consultants are mapping hydrogen pilots, decommissioning timelines, and green-finance structures that unlock investment, ensuring the segment’s rising contribution to the overall New Zealand management consulting services market. Banking, ICT, and manufacturing round out demand with cybersecurity, customer-experience redesign, and supply-chain resiliency mandates that keep the New Zealand management consulting services industry diversified.

Geography Analysis

Auckland and Wellington together represent the lion’s share of the New Zealand management consulting services market, anchored by corporate headquarters, capital-city ministries, and investor relations hubs. Auckland’s concentration of banks, telcos, and retail giants fuels digital-transformation and M&A advisory pipelines, sustaining a robust slice of the New Zealand management consulting services market size. Wellington’s public-sector dominance guarantees steady demand for policy design, governance frameworks, and program-management services that stabilize billings for firms heavily exposed to the New Zealand management consulting services market.

Secondary urban centers such as Hamilton, Tauranga, and Palmerston North add growth pockets as agri-tech ventures, logistics parks, and tertiary institutions seek scale-up strategies and operations tuning. Māori economic development projects in Northland, Bay of Plenty, and the East Coast further diversify regional consulting needs through culturally anchored business-planning assignments that mainstream firms are now beginning to chase. These trends spread the footprint of the New Zealand management consulting services market beyond the traditional Golden Triangle.

On the South Island, Christchurch serves as the engineering and rebuild nucleus, commissioning supply-chain redesign, construction program controls, and digital-twin modeling. Agriculture and tourism corridors from Canterbury to Otago require sustainability audits, precision-farming roadmaps, and workforce-planning playbooks. Queenstown’s tourism rebound is reviving destination-management and infrastructure-financing mandates. Collectively, these initiatives add incremental layers of demand that reinforce the national breadth of the New Zealand management consulting services market.

Competitive Landscape

Big Four firms, Deloitte, PwC, EY, and KPMG, retain the largest combined share of the New Zealand management consulting services market by leveraging multidisciplinary breadth, brand assurance, and government panel positions. They continue to acquire digital agencies, embed data scientists, and invest in proprietary AI accelerators to safeguard margin and relevance. Global strategy houses McKinsey, Boston Consulting Group, and Bain capture C-suite transformation mandates, using thought-leadership content and senior-partner access to secure premium engagements within the New Zealand management consulting services market.

Technology-led players such as Accenture, IBM, and Capgemini fuse advisory with implementation and managed-service contracts, positioning themselves as end-to-end partners for cloud migrations and platform integrations. Indigenous and public-policy boutiques such as MartinJenkins and Nous Group win mission-critical assignments where contextual insight and community trust outweigh scale, underscoring fragmentation in the New Zealand management consulting services market. Gig platforms and freelance networks like Talmix and Catalant are gaining traction among SMEs, unbundling traditional services into modular offerings that compress fee structures and nudge incumbents to explore asset-based consulting in the evolving New Zealand management consulting services industry.

Firms experimenting with generative-AI copilots for research, synthesis, and slide drafting report productivity lifts of 20-30%, but must address data-privacy, model-hallucination, and skills-retraining challenges. Price pressure from government procurement reforms and rising consultant salaries incentivize near-shore delivery from Australia and the Philippines. Meanwhile, heightened conflict-of-interest monitoring could force structural separation between audit and advisory arms at the Big Four, potentially redistributing contracts across the broader New Zealand management consulting services market.

New Zealand Management Consulting Services Industry Leaders

Deloitte New Zealand Limited

Ernst and Young Business Solutions New Zealand Ltd,

KPMG Services Limited New Zealand

Accenture New Zealand Limited

PricewaterhouseCoopers Consulting (New Zealand) GP Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Government shortlisted three consortia for the Warkworth-Te Hana motorway, preferred bidder in 2026.

- May 2025: Deloitte New Zealand expanded its AI and data analytics practice by hiring 15 senior specialists to help corporates adopt generative-AI customer-service tools.

- February 2025: PwC New Zealand consolidated ESG, carbon accounting, and transition services under a dedicated sustainability practice in response to mandatory climate-disclosure rules.

- January 2025: Accenture New Zealand formed a strategic partnership with Microsoft to deliver integrated Azure-based cloud and AI advisory for banks and telcos.

New Zealand Management Consulting Services Market Report Scope

The New Zealand Management Consulting Services Market Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current size of the New Zealand management consulting services market?

The market stood at USD 1.38 billion in 2026 and is projected to reach USD 1.82 billion by 2031 at a 5.69% CAGR.

Which consulting service line is growing the fastest in New Zealand?

Digital Transformation Consulting is forecast to grow at 6.24% CAGR through 2031 as firms invest in cloud, AI, and data-modernization programs.

Why are SMEs increasing their use of consulting services?

Remote delivery, productized fixed-price modules, and government-subsidized advisory grants lower cost barriers, enabling SMEs to access fractional expertise.

How are government procurement reforms affecting consulting contracts?

New rules cap single-supplier values, emphasize fixed-price bids, and require greater transparency, putting downward pressure on fees and rewarding agile multi-vendor teams.

Which end-user industry is expected to see the fastest consulting spend growth?

Energy and Resources is projected to expand at 5.96% CAGR as companies develop decarbonization roadmaps and invest in renewable projects.

What competitive advantages are firms pursuing in the New Zealand market?

Leading firms are integrating generative-AI tools, acquiring digital agencies, and forming cloud-platform alliances to improve productivity and capture technology-led mandates.

Page last updated on: